Saudi Arabia Data Center Construction Market Size and Share

Market Overview

| Study Period | 2025 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

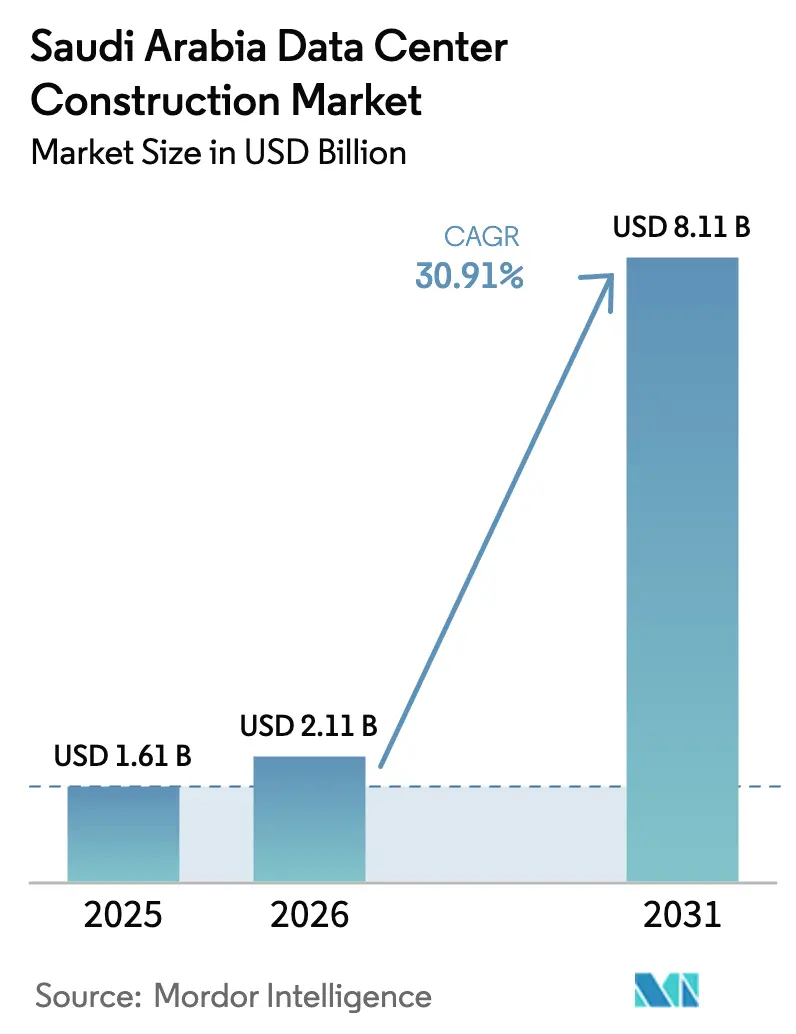

| Base Year Market Size (2025) | USD 1.61 Billion |

| Market Size (2026) | USD 2.11 Billion |

| Market Size (2031) | USD 8.11 Billion |

| Growth Rate (2026 - 2031) | 30.91% CAGR |

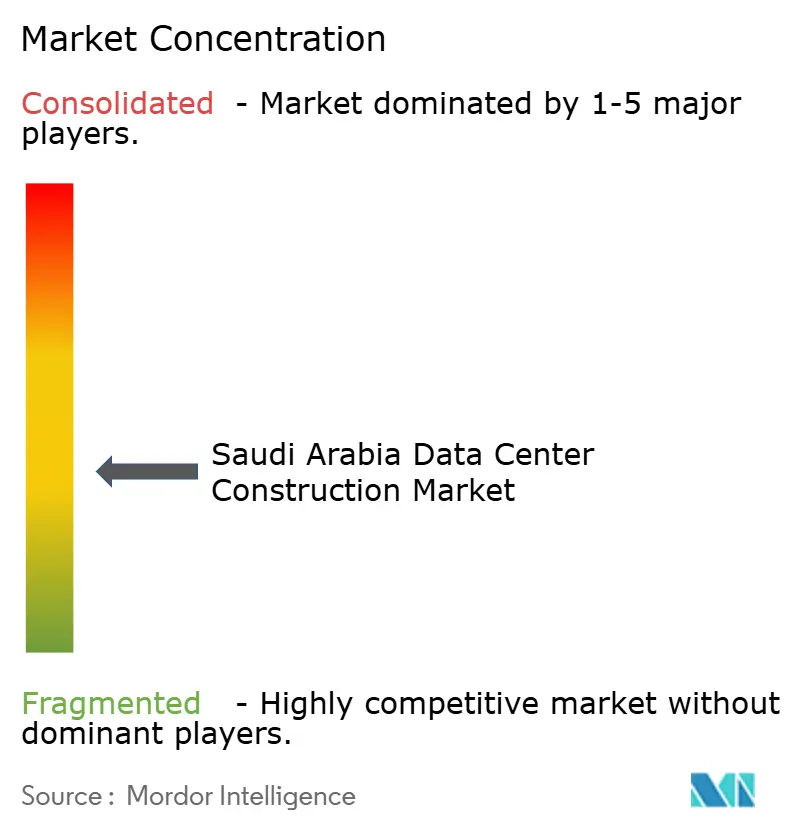

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Data Center Construction Market Analysis by Mordor Intelligence

The saudi arabia data center construction market size was valued at USD 1.61 billion in 2025 and estimated to grow from USD 2.11 billion in 2026 to reach USD 8.11 billion by 2031, at a CAGR of 30.91% during the forecast period (2026-2031). A combination of Vision 2030 incentives, mandatory data-sovereignty rules, and rapid submarine-cable additions has made the Kingdom the fastest-growing regional hub for artificial-intelligence infrastructure. Hyperscale cloud providers have committed multi-billion-dollar capital programs, while domestic conglomerates channel large sums into power-dense facilities designed for graphics-processing-unit clusters. Demand is also propelled by 5G edge roll-outs, the proliferation of generative-AI workloads in energy and finance, and significant public-sector digitalization projects. Grid modernization and renewable-energy integration shape electrical designs, and liquid-cooling adoption accelerates as operators address desert-climate constraints.

Key Report Takeaways

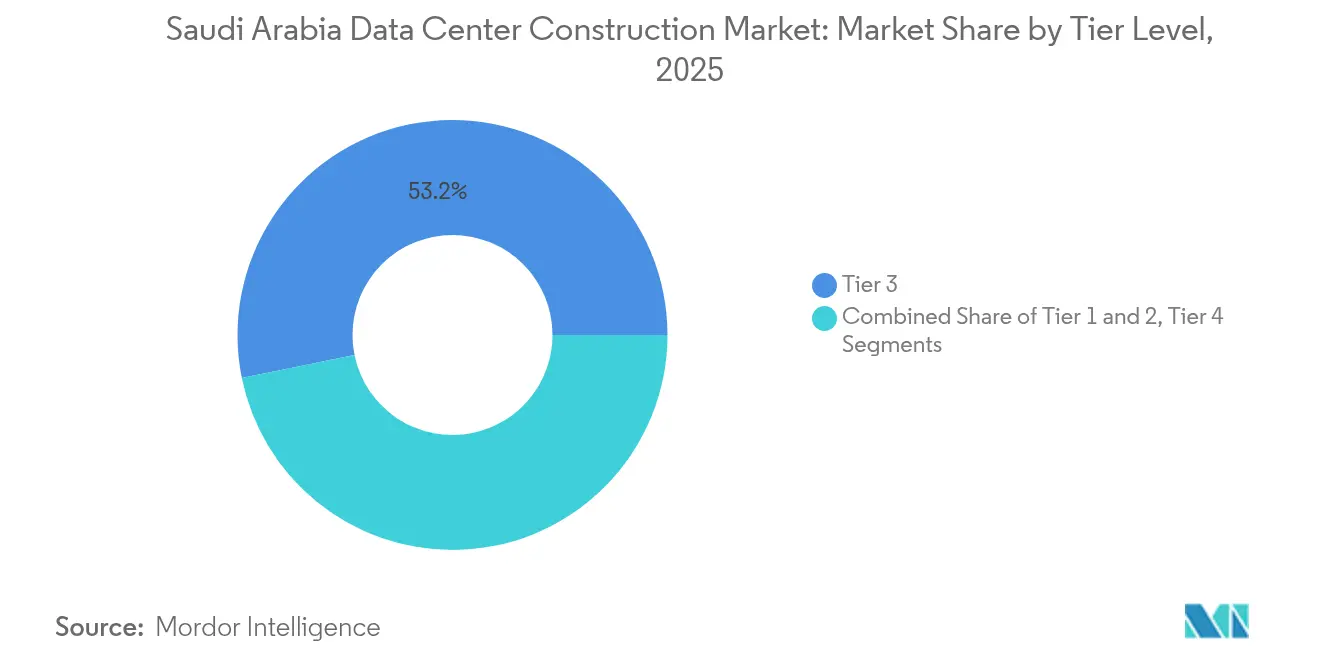

- By tier type, Tier 3 commanded 53.20% of the saudi arabia data center construction market share in 2025, yet Tier 4 is projected to expand at a 31.34% CAGR through 2031.

- By data-center type, colocation retained 56.40% revenue share in 2025, while self-build hyperscalers show the highest growth at a 31.75% CAGR.

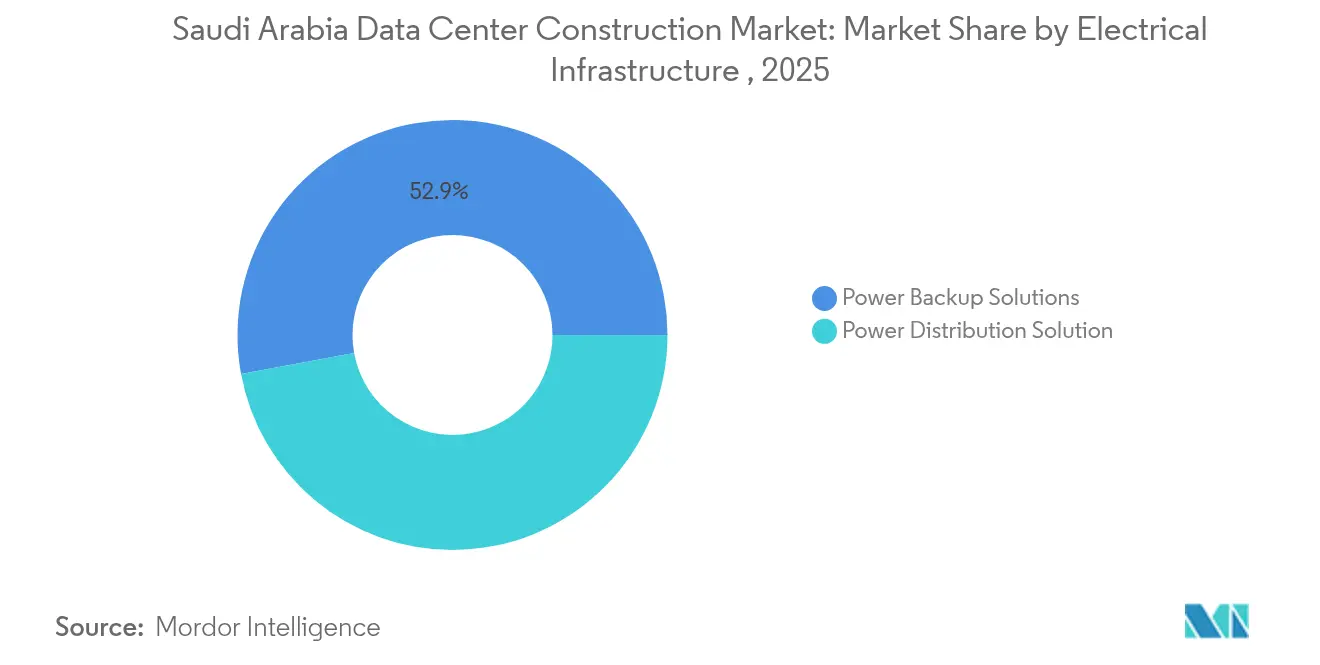

- By electrical infrastructure, power-backup systems held 52.90% share of the saudi arabia data center construction market size in 2025; power-distribution solutions are forecast to advance at 31.12% CAGR between 2026-2031.

- By mechanical infrastructure, cooling systems accounted for 41.30% spending in 2025, whereas servers and storage lead growth at a 31.96% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Data Center Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government incentives for hyperscale investments (Vision 2030 and PIF accelerators) | +8.2% | National, concentrated in Riyadh, Jeddah, NEOM | Long term (≥ 4 years) |

| Mandatory data-sovereignty rules pushing in-country build-outs | +6.8% | National, with spillover to regional operators | Medium term (2-4 years) |

| 5G roll-out driving edge and micro-modular facilities | +4.3% | Urban centers: Riyadh, Jeddah, Dammam | Short term (≤ 2 years) |

| AI / Gen-AI workload localisation by Saudi corporates | +7.1% | National, early adoption in energy and finance sectors | Medium term (2-4 years) |

| Royal Commission "NEOM" zero-carbon DC blueprint attracting global operators | +3.8% | NEOM region, demonstration effect nationally | Long term (≥ 4 years) |

| Surge in submarine cable landings (2Africa, Blue-Raman) lifting coastal DC demand | +2.4% | Coastal cities: Jeddah, Yanbu, Dammam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government incentives for hyperscale investments

Vision 2030 allocates USD 100 billion to technology, including accelerated permit pathways that cut data-center approvals to six months.[1]Communications, Space & Technology Commission, “Data Center Licensing Framework,” cst.gov.sa Public Investment Fund equity participation and subsidized electricity tariffs have already attracted commitments exceeding USD 15 billion from AWS and Microsoft. Direct fiscal support alters project economics and secures long-term sovereign control of critical compute capacity.

Mandatory data-sovereignty rules pushing in-country build-outs

The Personal Data Protection Law, effective September 2024, makes local hosting compulsory for entities processing resident data, forcing multinationals to shift away from Bahrain and Dubai. Cross-border transfers now need case-by-case clearance, turning national capacity into a legal requirement rather than a cost choice. Cloud providers therefore prioritise sovereign regions to avoid regulatory penalties.

5G roll-out driving edge and micro-modular facilities

Population coverage of 78% in 2024 and median download speeds beyond 300 Mbps create latency thresholds impossible for remote hubs. Telecom operators, therefore, invest in prefabricated micro-modules that can be installed near radio-access nodes in weeks. These sites allow new revenue streams such as real-time analytics and autonomous-vehicle telemetry.

AI / Gen-AI workload localization by Saudi corporates

Aramco doubled data-center power capacity to accommodate 1,500 PB, running industrial large-language models that need continuous uptime.[2] Aramco, “Aramco Expands Digital Infrastructure,” aramco.com Similar GPU-driven expansions at STC and IBM’s Riyadh lab demonstrate how domestic enterprises internalise AI compute, limiting exposure to cross-border latency and security risks.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic shortage of Tier 3+ certified specialists | -4.1% | National, acute in emerging tech hubs outside Riyadh | Medium term (2-4 years) |

| Water-scarcity restrictions on traditional chilled-water cooling | -2.8% | Desert regions, less impact on coastal areas | Long term (≥ 4 years) |

| Long lead-times for 132 kV grid connections outside Riyadh cluster | -3.2% | Secondary cities and industrial zones outside Riyadh | Medium term (2-4 years) |

| Stringent Saudization quotas raising project labour costs | -2.1% | National, particularly affecting international contractors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic shortage of Tier 3+ certified specialists

The local talent pool lags behind facility roll-outs, compelling operators to import expertise and driving wage inflation of 40-60% above Gulf averages. Delayed staffing pushes commissioning schedules and reduces availability for concurrent builds.

Water-scarcity restrictions on traditional chilled-water cooling

With 70% of freshwater derived from desalination, regulators increasingly favour liquid-immersion and rear-door heat-exchanger systems. Microsoft has pledged “zero-water” Saudi facilities by 2026, [3]Microsoft, “Microsoft Cloud Region Progress Update,” microsoft.com setting a precedent that may render legacy chilled-water plants obsolete in arid interiors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tier Type: Momentum Shifts Toward Tier 4 Reliability

Tier 3 facilities held 53.20% revenue in 2025, but Tier 4 is on track to grow 31.34% annually as AI workloads demand concurrent maintainability. Groq’s USD 1.5 billion language-processing-unit campus in Dammam exemplifies enterprises opting for fault-tolerant architectures that prevent any single point of failure.

Higher capital intensity is offset by premium pricing; clients in energy and finance accept 40-60% cost uplifts to safeguard autonomous drilling or algorithmic-trading platforms. Over the forecast, the saudi arabia data center construction market expects Tier 4 footprints to extend beyond hyperscalers into regulated industries, raising the overall resiliency baseline.

By Data Center Type: Hyperscalers Redefine Sovereign Ownership

Colocation remains sizable with 56.40% of 2025 spend, yet self-build projects are rising 31.75% per year as cloud majors demand direct oversight of security, power and network architecture. The saudi arabia data center construction market size for self-build campuses is projected to exceed USD 3.35 billion by 2031. Providers counterbalance by offering hybrid suites: center3 pairs dedicated halls with shared meet-me rooms linked to the 2Africa cable. This blend enables enterprise migration paths while preserving hyperscale economics.

By Electrical Infrastructure: High-Voltage Distribution Leads Expansion

Power-backup equipment captured 52.90% of the Saudi Arabia data center construction market size in 2025, reflecting the need for uninterruptible operations. Looking ahead, power-distribution gear registers the highest 31.12% CAGR as operators move from 480 V to 13.8-132 kV designs that lower line losses and match renewable-energy inputs.

Large campuses such as DataVolt’s 1.5 GW NEOM complex necessitate purpose-built substations and dynamic load-balancing systems that integrate solar arrays. Investment risers include bus-duct lines, static-switch boards and advanced energy-storage modules.

By Mechanical Infrastructure: Compute Density Drives Server and Storage Spend

Cooling systems still command 41.30% share, but servers and storage post a 31.96% CAGR through 2031, supported by escalating GPU counts per rack. Immersion cooling has moved from pilot to mainstream, yielding 70% energy savings and 20% floor-space reduction.

The Saudi Arabia data center construction market benefits from localised manufacturing: HPE’s ProLiant Gen11 production line in the Kingdom cuts lead times and fulfils Saudization objectives. Rack vendors now ship 60 kW-rated cabinets as standard, compared with 10 kW designs only two years earlier.

Geography Analysis

Riyadh concentrates roughly 273 MW of installed IT load, leveraging governmental demand, financial services customers, and proximity to national grid upgrades. The capital, therefore, remains the anchor of the Saudi Arabia data center construction market. Coastal hubs Jeddah and Dammam each host more than 120 MW, supported by 2Africa and Africa-1 cable landings that enable sub-25 ms round-trip latency to three continents.

NEOM introduces a third development pole. Its regulatory autonomy, full renewable-energy supply, and zero-liquid-discharge mandate attract operators targeting ESG-driven clients. DataVolt’s USD 5 billion Oxagon campus will deploy 1.5 GW, profoundly shifting the Saudi Arabia data center construction market share toward the northwest corridor once operational.

Secondary cities such as Yanbu, Medina, and Abha emerge as edge sites aligned with 5G clusters. However, extended lead-times for 132 kV grid access and limited specialist labour slow hyperscale ambitions in these zones. Incentives tied to industrial diversification programmes may gradually bridge the gap as power-transmission projects complete after 2027.

Competitive Landscape

The landscape sits at a moderate concentration level. Incumbent telecom operator STC leverages 25 data centers and submarine-cable assets, while neutral-host firms like center3 and Gulf Data Hub add regional interconnection depth. Hyperscalers, including AWS and Microsoft, commit to directly owned campuses, altering procurement standards and accelerating the adoption of liquid cooling and on-site solar arrays.

Domestic groups such as Alfanar and Mobily diversify into digital infrastructure, using existing electrical-engineering and fibre portfolios to win EPC contracts. Equipment partnerships, illustrated by DataVolt’s USD 20 billion Supermicro framework, underpin multi-gigawatt roll-outs and create bargaining power in server and rack pricing.

Strategy differentiation focuses on renewable-energy sourcing, heat-reuse schemes, and compliance with Saudization targets. Operators building workforce academies achieve faster commissioning and lower turnover costs than rivals dependent on expatriate talent.

Saudi Arabia Data Center Construction Industry Leaders

Alfanar Group

Linesight

ICS Arabia

SALFO SA

ALEC Engineering & Contracting

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: DataVolt signed a USD 20 billion memorandum with Supermicro to build hyperscale AI campuses powered by renewables.

- March 2025: Alfanar Group committed USD 1.4 billion for four Saudi facilities focused on high-density rack.

- February 2025: Groq opened a USD 1.5 billion AI compute centre in Dammam with 19,000 LPUs

- February 2025: LEAP 2025 conference generated USD 20 billion of AI and data-center pledges, including Equinix’s USD 1 billion cloud facility.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the Saudi Arabia data center construction market as all capital spending devoted to new-build or major expansion projects that integrate civil works, electrical distribution, mechanical cooling, fire-safety systems, and fit-out of white-space for IT racks. Values, therefore, capture engineering, procurement, and construction (EPC) outlays tied to Tier I-IV facilities regardless of ownership model (enterprise, colocation, or hyperscale).

Scope Exclusion: ongoing facility operations and routine maintenance services are outside our sizing universe.

Segmentation Overview

- By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

- By Data Center Type

- Colocation

- Self-build Hyperscalers (CSPs)

- Enterprise and Edge

- By Infrastructure

- By Electrical Infrastructure

- Power Distribution Solution

- Power Backup Solutions

- By Mechanical Infrastructure

- Cooling Systems

- Racks and Cabinets

- Servers and Storage

- Other Mechanical Infrastructure

- General Construction

- Service - Design and Consulting, Integration, Support and Maintenance

- By Electrical Infrastructure

- Tier 1 and 2

Detailed Research Methodology and Data Validation

Primary Research

We spoke with EPC project directors, colocation strategy heads, hyperscaler procurement leads, and local code consultants across Riyadh, Jeddah, and Dammam. Interviews clarified average build-time slippage, liquid-cooling uptake, and real-world cost per megawatt, helping us reconcile secondary clues and refine escalation assumptions.

Desk Research

Our analysts began with statutory data, Saudi Ministry of Municipal, Rural Affairs and Housing permits, CST capacity filings, GASTAT construction price indices, and ZATCA import tariffs for switchgear and CRAC units. To benchmark regional power costs and diesel trends, we reviewed Saudi Energy Efficiency Center and IEA series, while white papers from Uptime Institute and the Saudi Green Building Forum provided design and tier adoption signals. Paid feeds such as D&B Hoovers and Dow Jones Factiva supplied contractor revenue splits and project announcements. This list is indicative; many additional public and proprietary sources informed the study.

Market-Sizing & Forecasting

A top-down model starts with historical building permits and announced IT-load pipelines; these are priced using region-specific $/MW benchmarks adjusted for steel and copper indices. Results are cross-checked bottom-up with sampled contractor invoices and channel checks on generator, UPS, and chiller shipments. Key drivers, Vision 2030 hyperscale commitments, grid connection lead times, local steel inflation, preferred tier mix, and average rack density, feed a multivariate regression that projects spend through 2030. Where supplier roll-ups lack full visibility, we impute gaps using average project size by tier and apply conservative occupancy ramps.

Data Validation & Update Cycle

Outputs undergo variance testing against independent capacity trackers and listed contractor backlogs. Senior analysts review anomalies before release. The dataset is refreshed each year, with interim mid-cycle updates triggered by material investment announcements.

Why Mordor's Saudi Arabia Data Center Construction Baseline Is Dependable

Published estimates often diverge because firms choose different cost scopes, tier definitions, and currency bases.

Key gap drivers include whether fit-out labor is capitalized, the treatment of self-built hyperscale shells, escalation factors for steel, and refresh cadence. Our study reports 2025 spend in constant-2024 dollars, applies verified Vision 2030 project lists, and is updated annually; practices some providers skip.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.61 B (2025) | Mordor Intelligence | - |

| USD 0.23 B (2024) | Regional Consultancy A | excludes hyperscale shell works, uses headline contract value only |

| USD 2.31 B (2024) | Global Consultancy B | counts facility operations spend and applies global $/MW without Saudi cost deflators |

These comparisons show that Mordor's disciplined scope selection, Saudi-specific cost curves, and yearly refresh cycle provide a balanced, transparent baseline planners can trust.

Key Questions Answered in the Report

What is the projected value of the Saudi Arabia data center construction market in 2031?

The market is expected to reach USD 8.11 billion by 2031, reflecting a 30.91% CAGR from 2026.

Which tier classification is growing fastest?

Tier 4 infrastructure shows the highest growth, expanding at 31.34% annually as AI workloads require concurrent maintainability.

Why are hyperscalers choosing self-build projects in Saudi Arabia?

Mandatory data-sovereignty rules and the need for custom high-density designs encourage cloud majors to own and operate facilities directly.

How does water scarcity influence cooling technology choices?

Operators shift toward liquid-immersion and rear-door heat-exchanger systems that reduce freshwater consumption by up to 70%.

Page last updated on: