Unit Dose Pharmaceutical Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

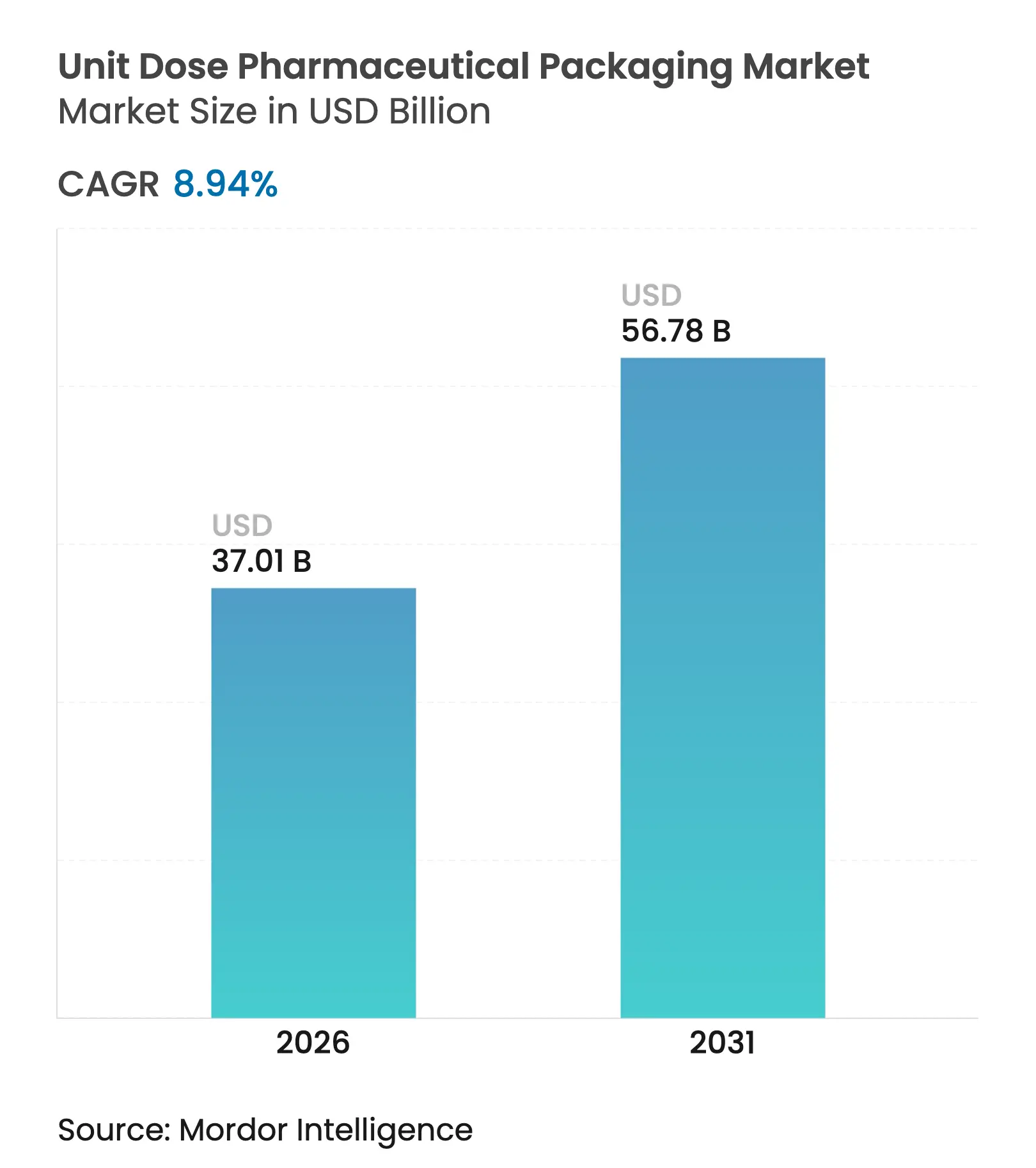

| Market Size (2026) | USD 37.01 Billion |

| Market Size (2031) | USD 56.78 Billion |

| Growth Rate (2026 - 2031) | 8.94 % CAGR |

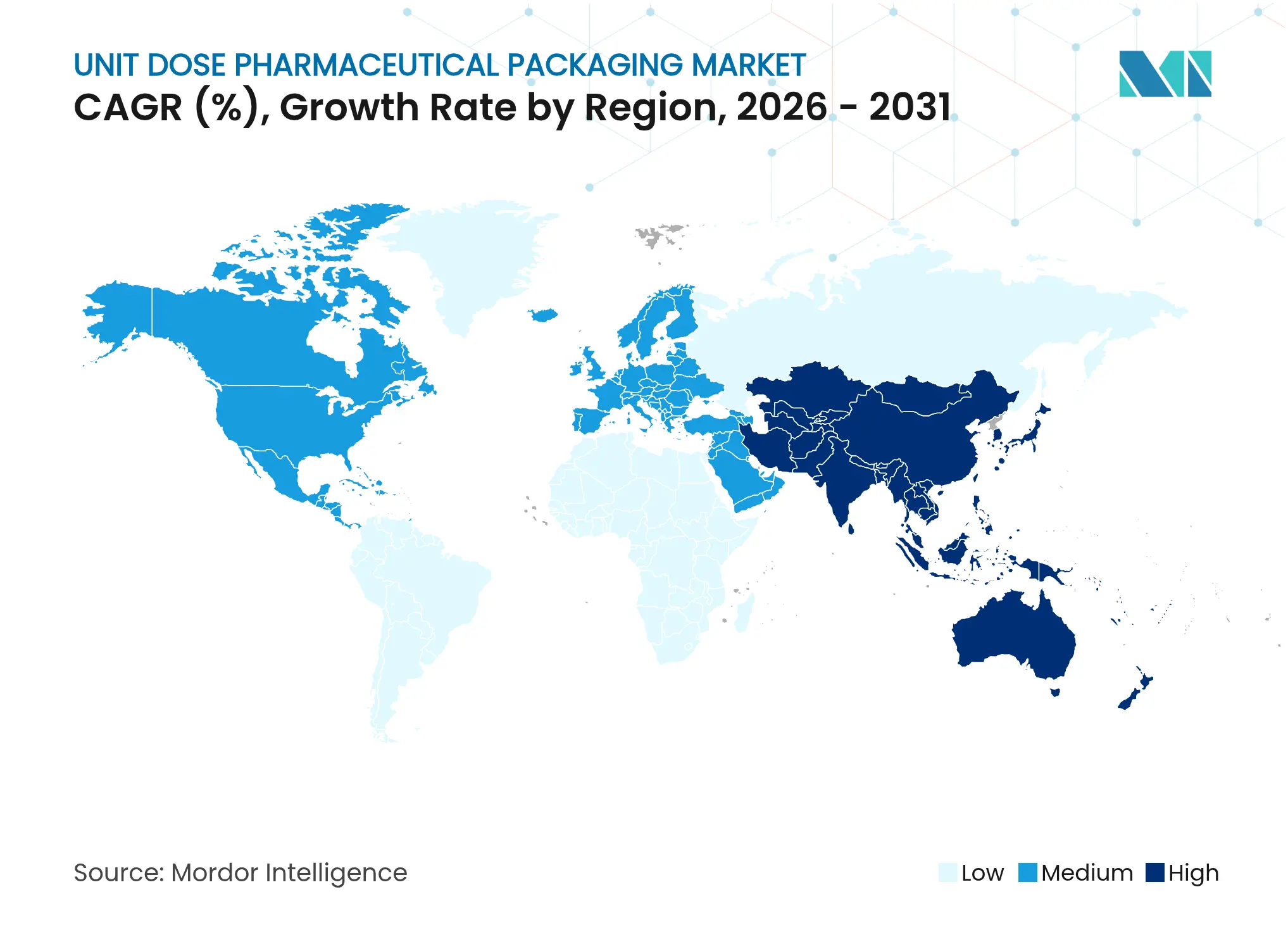

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Unit Dose Pharmaceutical Packaging Market Analysis by Mordor Intelligence

The unit dose pharmaceutical packaging market size is expected to grow from USD 33.97 billion in 2025 to USD 37.01 billion in 2026 and is forecast to reach USD 56.78 billion by 2031 at 8.94% CAGR over 2026-2031. Sustained growth arises from the confluence of chronic disease prevalence, stricter serialization mandates, and the rapid shift toward biologics that require sterile single-dose containment. Hospitals intensifying bar-coding adoption, retail pharmacies automating fulfillment, and governments demanding supply-chain transparency collectively reinforce demand for highly specialized unit presentations. At the same time, innovations such as AI-enabled micro-batch blister lines and wood-based plastic containers allow producers to respond to both personalization and sustainability pressures, thereby widening the addressable customer base. Competitive dynamics favor vertically integrated suppliers that pair primary containers with device platforms, yet regional contract packagers are scaling quickly to meet outsourcing volumes from mid-sized drug developers.

Key Report Takeaways

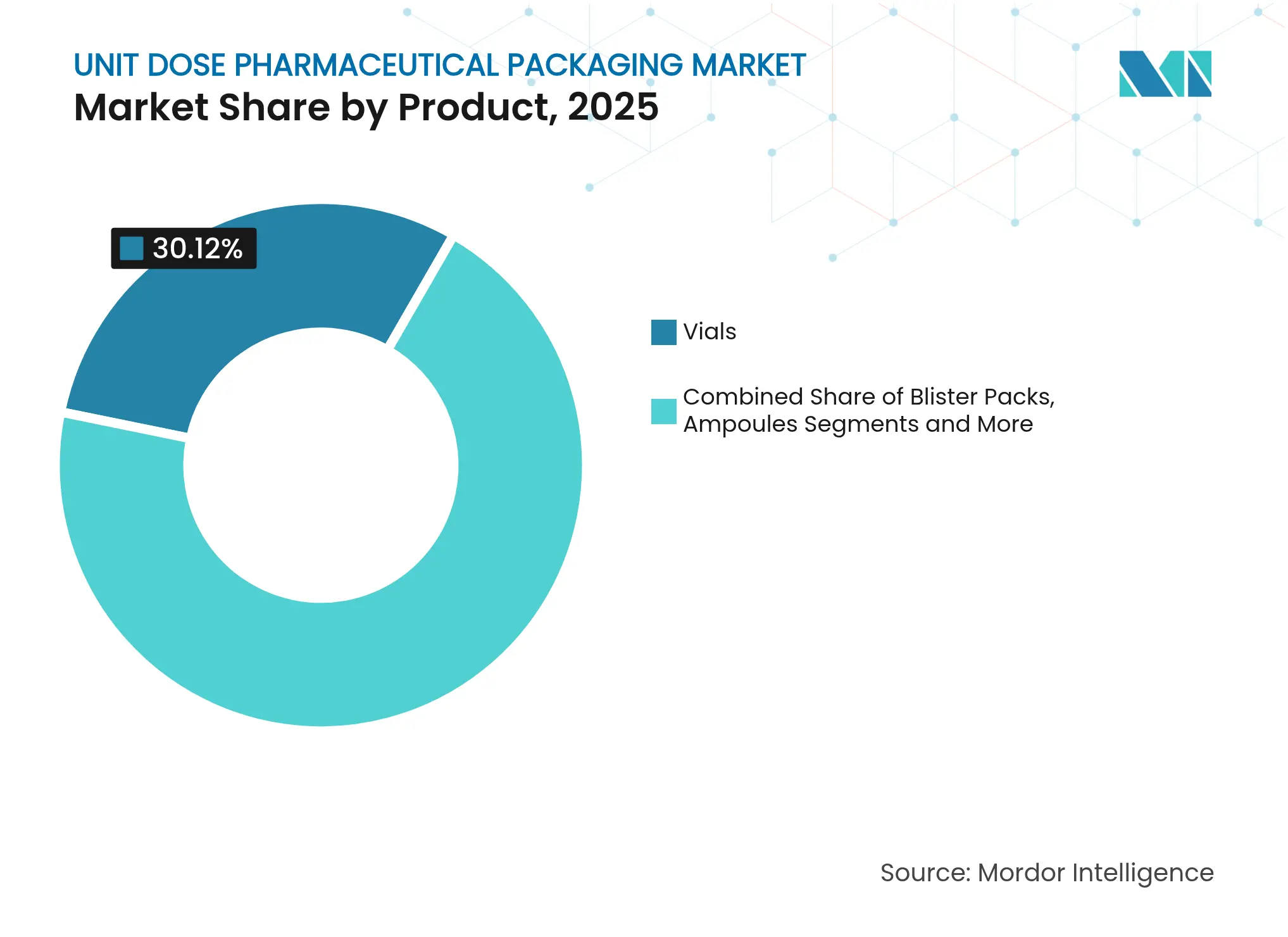

- By product category, vials held 30.12% of unit dose pharmaceutical packaging market share in 2025, while blister packs are projected to expand at a 12.31% CAGR to 2031.

- By material, plastics led with 47.95% revenue share in 2025; paper and paperboard are forecast to advance at an 11.09% CAGR through 2031.

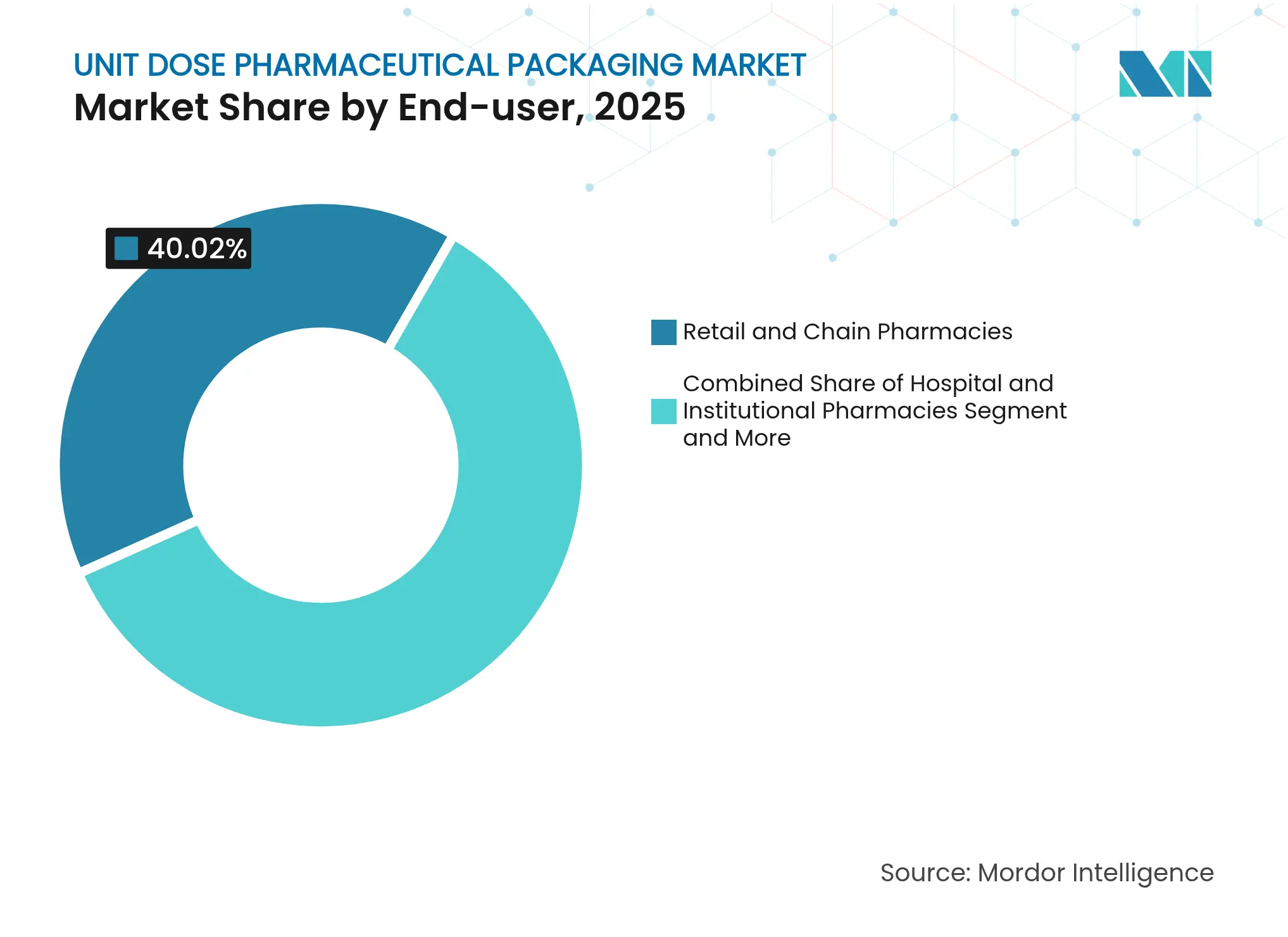

- By end-user, retail and chain pharmacies controlled 40.02% of the unit dose pharmaceutical packaging market size in 2025; contract drug manufacturers and re-packagers record the highest projected CAGR at 10.55% until 2031.

- By packaging technology, thermoforming accounted for 38.21% share of the unit dose pharmaceutical packaging market size in 2025, whereas smart and serialized formats are set to grow at a 12.6% CAGR to 2031.

- By geography, North America dominated with a 35.29% unit dose pharmaceutical packaging market share in 2025, while Asia-Pacific is poised to expand at a 13.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Unit Dose Pharmaceutical Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Escalating

prevalence of chronic diseases boosting demand for precise dosing

Escalating

prevalence of chronic diseases boosting demand for precise dosing

| +2.1% | Global, with concentration in North America and Europe | Long term (≥ 4 years) |

(~) %

Impact on CAGR Forecast

:

+2.1%

|

Geographic Relevance

:

Global,

with concentration in North America and Europe

|

Impact Timeline

:

Long

term (≥ 4 years)

|

Tighter

hospital bar-coding regulations for medication administration

Tighter

hospital bar-coding regulations for medication administration

| +1.8% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) | |||

Shift

toward biologics and injectables requiring sterile single-dose packs

Shift

toward biologics and injectables requiring sterile single-dose packs

| +2.3% | Global, led by North America and EU | Long term (≥ 4 years) | |||

Expansion

of outpatient and home-care drug delivery channels

Expansion

of outpatient and home-care drug delivery channels

| +1.6% | Global, with early adoption in North America | Medium term (2-4 years) | |||

AI-enabled

micro-batch blister line retrofits for personalized therapies

AI-enabled

micro-batch blister line retrofits for personalized therapies

| +0.9% | North America and EU, pilot programs in Asia-Pacific | Long term (≥ 4 years) | |||

Growth

in US 503B outsourcing facilities driving repackaging volumes

Growth

in US 503B outsourcing facilities driving repackaging volumes

| +1.2% | United States, with spillover to Canada | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Escalating Prevalence of Chronic Diseases Boosting Demand for Precise Dosing

Chronic diseases now account for 71% of global mortality, a burden that directly elevates the need for accurate dosing systems such as pre-measured vials, blisters, and pre-filled syringes. Hospital audits show medication errors fall by up to 85% when institutions convert from bulk to unit dose dispensing, strengthening the economic justification for premium packaging. Diabetes, oncology, and cardiovascular care dominate consumption as therapies require strict adherence and contamination-free handling. Manufacturers are scaling glass vial output and integrating RFID seals to support clinical traceability, while smart blister platforms feed dose-taking data back to physicians. This self-reinforcing loop of better outcomes and value-based procurement underpins long-term upside for the unit dose pharmaceutical packaging market.

Tighter Hospital Bar-Coding Regulations for Medication Administration

The bar-code rule under 21 CFR 201.25 obligates machine-readable identifiers on every prescription package sold in the United States.[1]U.S. Food and Drug Administration, “Guidance for Industry: Bar Code Label Requirements,” fda.gov Similar provisions within the EU Falsified Medicines Directive push serialization across 27 member states, making single-unit formats indispensable for bedside scanning. When bar-code medication administration (BCMA) is paired with unit dose packs, hospitals cut wrong-drug or wrong-dose events by 58%. Beyond safety, hospital risk managers link BCMA to lower malpractice exposure, encouraging senior leadership to budget for automated packaging feeds. As barcode compliance deadlines tighten, the unit dose pharmaceutical packaging market benefits from steady replacement of bulk bottles with serialized blister wallets and ready-to-inject cartridges.

Shift Toward Biologics and Injectables Requiring Sterile Single-Dose Packs

Biologics make up more than 80% of drugs in late-stage pipelines, and their inherent instability accelerates adoption of glass vials, pre-filled syringes, and cartridge systems that ensure container-closure integrity. [2]SCHOTT Pharma, “Solutions for Large-Volume Biologics,” schott-pharma.com Single-dose delivery eliminates preservative exposure, curbs microbial ingress, and prevents waste associated with multi-use vials discarded before exhaustion. The trend also fuels demand for cleanroom blow-fill-seal lines and nested RTU (ready-to-use) components that slash setup time for contract manufacturers. Weight-based dosing oncology regimens depend on milliliter-level accuracy, amplifying the market pull for camera-guided fill-finish modules. As self-administration of biologics rises, autoinjectors and wearable injectors packaged in sterilized nests stimulate a fresh wave of device-plus-package integration across the unit dose pharmaceutical packaging market.

Expansion of Outpatient and Home-Care Drug Delivery Channels

Home health visits in the United States increased 23% during 2024 as payers pivot to value-based models that favor in-home treatment. Patients outside clinical settings rely on unit dose pouches, color-coded blister cards, and tamper-evident vials that simplify self-medication. Easy-open lids, pictogram labeling, and audible clicks that confirm closure improve adherence for elderly consumers. Pharmacies integrate robotic micro-fulfillment centers that pre-sort and bag unit doses, freeing pharmacists for counseling and vaccinations. Lower readmission rates and shorter emergency visits give payers a financial incentive to reimburse premium packs, further broadening the unit dose pharmaceutical packaging market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High

capital and material costs of unit-dose formats

High

capital and material costs of unit-dose formats

| -1.4% | Global, particularly impacting emerging markets | Medium term (2-4 years) |

(~) %

Impact on CAGR Forecast

:

-1.4%

|

Geographic Relevance

:

Global,

particularly impacting emerging markets

|

Impact Timeline

:

Medium

term (2-4 years)

|

Sustainability

pressures on multilayer blister waste streams

Sustainability

pressures on multilayer blister waste streams

| -0.8% | EU and North America, expanding globally | Long term (≥ 4 years) | |||

Glass

vial shortages creating pack supply volatility

Glass

vial shortages creating pack supply volatility

| -1.1% | Global, with acute impact in North America and EU | Short term (≤ 2 years) | |||

Serialization-data

compliance burden on small repackagers

Serialization-data

compliance burden on small repackagers

| -0.6% | North America and EU, with spillover to Asia-Pacific | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Capital and Material Costs of Unit-Dose Formats

Dedicated blister and vial lines demand USD 5–15 million in investment versus USD 1–3 million for bulk bottle fillers.[3]AmerisourceBergen, “AmBer Unit Dose eBook,” amerisourcebergen.comValidation, cleanroom retrofits, and serialization modules can extend timelines by up to a year and inflate budgets by another 20–30%. Raw material usage per dose rises three-fold relative to bulk packs, and glass borosilicate vial pricing remains exposed to energy-cost swings. The economics squeeze small generic firms in price-controlled markets, slowing equipment upgrades and temporarily moderating expansion for the unit dose pharmaceutical packaging market.

Sustainability Pressures on Multilayer Blister Waste Streams

The EU Packaging and Packaging Waste Directive sets a 65% recycling requirement by 2025, yet aluminum–PVC blisters typically achieve below 15% recovery. Procurement policies inside European hospital groups already favor recyclable or mono-material packs, prompting brands to experiment with paper-based or bio-sourced substrates. While prototype solutions deliver a 40% CO₂ reduction, they add up to 25% in material cost and can compromise moisture-barrier performance. Until recycling infrastructure matures, these environmental headwinds will temper the otherwise robust trajectory of the unit dose pharmaceutical packaging market.

Segment Analysis

By Product: Vials Lead Market Share Despite Blister Pack Innovation

Vials captured USD 10.23 billion in 2025, translating to 30.12% of unit dose pharmaceutical packaging market share. Their pre-eminence stems from compatibility with biologics that demand high chemical resistance and low extractables. The growth of GLP-1 injectables and mRNA vaccines keeps capacity utilization high across leading borosilicate producers. Blister packs, by contrast, generated USD 8.59 billion but are forecast to post a 12.31% CAGR, propelled by AI-driven micro-batch lines that create personalized regimens and by GSM-enabled sensors tracking adherence. Ampoules, bottles, jars, and stick packs maintain niche appeal in emergency medicine and pediatric dosing where quick administration or taste masking is critical.

Blister design now integrates QR codes that relay expiry dates and dosing reminders, aligning with pharmacy automation software. Vial innovation centers on polymer-coated inner surfaces to mitigate delamination and siliconization defects. Dual-chamber cartridges enabling point-of-care reconstitution enter commercial scale, serving lyophilized biotech drugs with short shelf lives. These design evolutions, paired with stringent sterile manufacturing, anchor the product hierarchy that shapes value creation inside the unit dose pharmaceutical packaging market.

Note: Segment shares of all individual segments available upon report purchase

By Material: Plastics Dominate While Paper Gains Sustainability Momentum

Plastics represented USD 16.29 billion or 47.95% of 2025 sales, with polypropylene and cyclic olefin polymers leading due to their thermal stability and clarity. TekniPlex Healthcare’s 2024 expansion added multi-cavity injection blow molding cells that lift annual output capacity by 20%. Glass accounted for USD 9.42 billion and remains unrivaled for biologic stability, yet energy-intensive furnaces and supply volatility keep costs elevated. Paper and paperboard recorded only USD 2.8 billion in 2025, but its 11.09% CAGR outruns all other substrates as regulators elevate recycling targets. The joint UPM-Bormioli Pharma pilot bottle incorporates 50% wood-based resin, demonstrating early commercialization of bio-sourced feedstock.

Material choices increasingly flow from lifecycle-assessment dashboards used by procurement teams to balance barrier performance against waste-treatment cost. Mono-material high-barrier coatings on PET enable heat-seal blister webs that pass stability testing while remaining recyclable. Aluminum lidding remains vital for moisture-sensitive drugs, but converters experiment with thinner gauges and post-consumer recycled content. These shifts reinforce the strategic calculus that governs supplier R&D budgets across the unit dose pharmaceutical packaging market.

By End-user: Retail Pharmacies Lead While Contract Manufacturers Accelerate

Retail and chain pharmacies dispensed 40.02% of global unit doses in 2025, equivalent to USD 13.59 billion, supported by e-prescribing growth and store-level robotics that prep thousands of packs daily. Hospital pharmacies follow, relying on automated dispensing cabinets that recognize serialized blister cavities to curb diversion. Contract manufacturers and re-packagers generated USD 5.33 billion but are forecast to rise at a 10.55% CAGR as branded drug owners outsource surge volumes tied to specialty launches.

The unit dose pharmaceutical packaging market size for contract packers is projected to exceed USD 9.7 billion by 2031 as PCI Pharma Services, Stevanato Group, and Catalent commit more than USD 1 billion to sterile fill-finish suites. Home-health providers, though nascent, unlock new SKU combinations optimized for chronic therapies delivered via visiting nurses. As outsourcing deepens and care decentralizes, supplier segmentation will further refine service models from high-volume generics to ultra-small personalized runs.

Note: Segment shares of all individual segments available upon report purchase

By Packaging Technology: Thermoforming Leads While Smart Solutions Surge

Thermoforming brought in USD 12.98 billion during 2025, claiming 38.21% of market revenue thanks to its flexibility across tablets, capsules, and transdermal patches. The technology consumes PVC, PETG, COC, and novel fiber-based webs that pass child-resistance testing without metal foils. Cold-form foil blistering services high-barrier molecules but sacrifices line speed, holding a steady 15% share. Smart and serialized packaging, however, is slated to grow 12.6% annually through 2031, moving the unit dose pharmaceutical packaging market size for that niche from USD 4.39 billion to USD 8.95 billion. Integrations range from NFC chips embedded in lidding foils to blockchain receivers logging geolocation data.

Blow-fill-seal and nested RTU offerings support parenteral launches by minimizing manual aseptic handling. High-barrier spray coatings and plasma treatments lengthen shelf life for oxygen-sensitive biologics while enabling thinner walls—an approach that offsets rising raw material cost. Technology upgrades, once solely regulatory, now function as market-access enablers; payers in Germany reimburse adherence-verified packs at premiums of 4–6%. These converging forces reiterate the pivotal role of innovation inside the unit dose pharmaceutical packaging market.

Geography Analysis

North America generated USD 11.99 billion in 2025, representing 35.29% of global value, driven by FDA serialization enforcement and extensive biologic fill-finish capacity. Investments exceeding USD 6 billion across North Carolina alone, from Novo Nordisk and Eli Lilly, extend output of GLP-1 and mRNA vials, locking in regional leadership. Canada’s biologics corridor around Ontario amplifies sterile cartridge demand, while Mexico leverages maquiladora incentives to supply oral solid dose blisters to the United States.

Europe contributed USD 9.24 billion in 2025, buoyed by Germany, France, and Italy, where local device makers such as Gerresheimer and Stevanato scale vial, syringe, and cartridge production. The EU Falsified Medicines Directive underpins consistent ordering of serialized packs, and sustainability directives catalyze the shift toward fiber-based blisters with 40% lower CO₂ emissions. Eastern member states attract greenfield investments, narrowing supply chain lead times for pan-EU launches.

Asia-Pacific delivered USD 8.06 billion but will outpace all other regions at a 13.74% CAGR, lifting regional sales to USD 17.43 billion by 2031. China warms to PIC/S-aligned GMP, sparking demand for serialized blisters and bar-coded ampoules. India’s contract manufacturing surge, driven by generics exports, accelerates procurement of high-speed PVC-Alu blister lines. South Korea’s government-backed mRNA alliance channels funding into isolator-based vial filling, while Japan’s aging population sustains steady uptake of patient-friendly stick packs. Australia and Southeast Asian nations pilot home-infusion programs, broadening acceptance of pre-filled syringes.

South America and the Middle East and Africa jointly accounted for less than 10% of 2025 turnover but post compound growth above 11% as localization programs reduce reliance on imports. Brazil’s tax incentives in Goiás foster sterile vial clusters, and Saudi Arabia’s Vision 2030 investments pull in cartridge lines for insulin analogs. Although absolute volumes remain small, these frontier regions provide fresh runway for the unit dose pharmaceutical packaging market.

Competitive Landscape

Market Concentration

The unit dose pharmaceutical packaging market is moderately fragmented but tilts toward consolidation. The top five suppliers—West Pharmaceutical Services, Gerresheimer, SCHOTT Pharma, Stevanato Group, and Stevanato-owned Ompi—amass roughly 45% of global revenue. West’s proprietary devices arm recorded USD 2.89 billion in 2024, lifted by elastomer-coated plungers used in self-injection pens. Gerresheimer’s USD 180 million expansion in Georgia widens its U.S. foothold across inhalation cartridges and custom glass syringes.

Strategic investments remain skewed toward biologic fill-finish nodes and smart packaging. Stevanato opened a pre-sterilized EZ-fill hub in Cisterna di Latina to double syringe output for high-viscosity biologics. PCI Pharma Services added 545,000 ft² of injectable suites in Illinois, signalling accelerating outsourcing of complex secondary packaging. Suppliers differentiate via tech stacks that marry cloud-based serialization, RFID seals, and sustainability scorecards, positioning themselves as compliance partners rather than commodity converters.

M&A activity intensifies as scale becomes prerequisite for global brand support. Novo Holdings’ USD 16.5 billion acquisition of Catalent underscores the strategic value of integrated sterile manufacturing to secure obesity-drug supply. On the mid-tier, regional converters pool capital to afford DSCSA-grade track-and-trace lines. Price competition is muted in high-barrier niches but sharper in generics; nonetheless, vertical integration and IP around barrier coatings sustain margins above 20% EBITDA for the leaders. Over the forecast horizon, capacity expansions in Asia and automation upgrades worldwide will further define positioning inside the unit dose pharmaceutical packaging market.

Unit Dose Pharmaceutical Packaging Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Stevanato Group unveiled a new plant in Cisterna di Latina, Italy, dedicated to pre-sterilized EZ-fill syringes and cartridges, expanding capacity for biologic packaging solutions.

- May 2025: Stevanato Group reported record revenue of EUR 1,104 million for FY 2024, with high-performance syringes contributing 40% of total sales

- February 2025: Novo Holdings completed the USD 16.5 billion acquisition of Catalent, alongside Novo Nordisk’s USD 11 billion purchase of three fill-finish sites to bolster GLP-1 capacity.

- January 2025: Gerresheimer announced a USD 180 million expansion of its medical systems plant in Peachtree City, Georgia, adding 18,000 m² of space and 400 jobs.

- December 2025: SCHOTT Pharma posted EUR 957 million in revenue for FY 2024, a 12% rise year-on-year, with high-value vials representing 55% of turnover.

Table of Contents for Unit Dose Pharmaceutical Packaging Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Escalating prevalence of chronic diseases boosting demand for precise dosing

- 4.2.2Tighter hospital bar-coding regulations for medication administration

- 4.2.3Shift toward biologics and injectables requiring sterile single-dose packs

- 4.2.4Expansion of outpatient and home-care drug delivery channels

- 4.2.5AI-enabled micro-batch blister line retrofits for personalized therapies

- 4.2.6Growth in US 503B outsourcing facilities driving repackaging volumes

- 4.3Market Restraints

- 4.3.1High capital and material costs of unit-dose formats

- 4.3.2Sustainability pressures on multilayer blister waste streams

- 4.3.3Glass vial shortages creating pack supply volatility

- 4.3.4Serialization-data compliance burden on small repackagers

- 4.4Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

- 4.8Investment Analysis

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Product

- 5.1.1Blister Packs (Thermoform, Cold-form)

- 5.1.2Ampoules (Glass, Plastic)

- 5.1.3Vials (Glass, Polymer)

- 5.1.4Bottles and Jars (HDPE, PET)

- 5.1.5Pouches, Stick Packs and Sachets

- 5.1.6Other Product

- 5.2By Material

- 5.2.1Plastics (PP, PE, PVC, COC/COP)

- 5.2.2Glass (Borosilicate, Aluminosilicate)

- 5.2.3Metals (Aluminum Foil, Steel)

- 5.2.4Paper and Paperboard

- 5.3By End-user

- 5.3.1Hospital and Institutional Pharmacies

- 5.3.2Retail and Chain Pharmacies

- 5.3.3Home-Healthcare Providers

- 5.3.4Contract Drug Manufacturers and Re-packagers

- 5.4By Packaging Technology / Process

- 5.4.1Thermoforming

- 5.4.2Cold-Form Foil (Alu-Alu)

- 5.4.3Blow-Fill-Seal (BFS)

- 5.4.4Fill-Finish for Ready-to-Use Vials/Syringes

- 5.4.5High-Barrier Coating and Lamination

- 5.4.6Smart / Serialized Packaging Solutions

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Russia

- 5.5.2.7Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2India

- 5.5.3.3Japan

- 5.5.3.4South Korea

- 5.5.3.5Australia and New Zealand

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1Middle East

- 5.5.4.1.1United Arab Emirates

- 5.5.4.1.2Saudi Arabia

- 5.5.4.1.3Turkey

- 5.5.4.1.4Rest of Middle East

- 5.5.4.2Africa

- 5.5.4.2.1South Africa

- 5.5.4.2.2Nigeria

- 5.5.4.2.3Egypt

- 5.5.4.2.4Rest of Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1West Pharmaceutical Services Inc.

- 6.4.2Amcor plc

- 6.4.3Schott AG

- 6.4.4Gerresheimer AG

- 6.4.5AptarGroup Inc.

- 6.4.6SGD Pharma

- 6.4.7Stevanato Group

- 6.4.8Nipro PharmaPackaging

- 6.4.9Catalent Inc.

- 6.4.10Sharp Packaging Services

- 6.4.11Recipharm AB

- 6.4.12Ompi (Stevanato)

- 6.4.13Pacira BioSciences (DoseID solutions)

- 6.4.14UDG Healthcare plc

- 6.4.15Pacific Vial Manufacturing

- 6.4.16Pfizer CentreOne (Contract Packaging)

- 6.4.17Johnson & Johnson (Janssen Contract Services)

- 6.4.18Merck Contract Packaging

- 6.4.19TekniPlex Inc.

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1White-space and Unmet-Need Assessment

Global Unit Dose Pharmaceutical Packaging Market Report Scope

The market studies the demand for major Unit Dose Pharmaceutical Packaging for the major packaging products, including blister, ampoules, vials, prefilled syringe cartridges, bottles and jars, medication tubes, pouches, and other products, along with corresponding revenue accrued from the sales of these unit dose packaging products.

The unit dose packaging market is segmented by product (blister, ampoules, vials, prefilled syringe cartridges, bottles and jars, medication tubes, pouches, and other products), by material (paper & paperboard, metals, glass, and plastic), and by Geography (North America [United States and Canada], Europe [United Kingdom, Germany, France, and Rest of Europe], Asia Pacific [China, Japan, India, Australia and New Zealand, and Rest of Asia Pacific], Latin America [Brazil, Mexico, and Rest of Latin America], and Middle East and Africa [United Arab Emirates, Saudi Arabia, South Africa, and Rest of Middle East and Africa]. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.