China Pharmaceutical Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

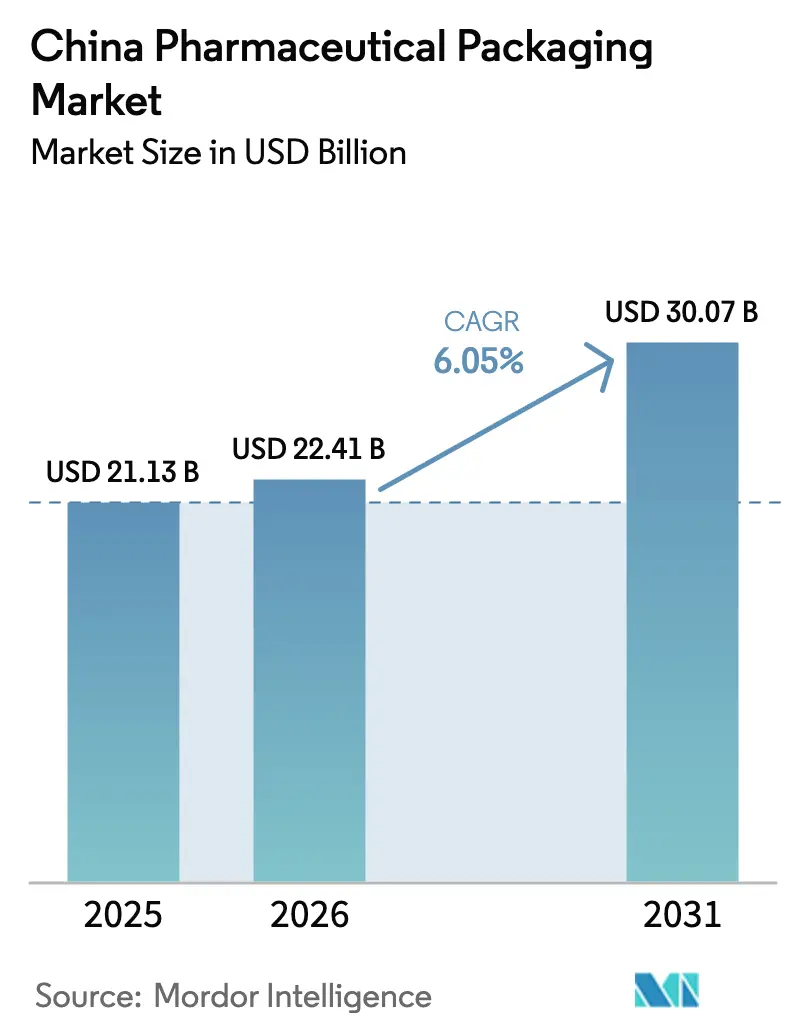

| Base Year Market Size (2025) | USD 21.13 Billion |

| Market Size (2026) | USD 22.41 Billion |

| Market Size (2031) | USD 30.07 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

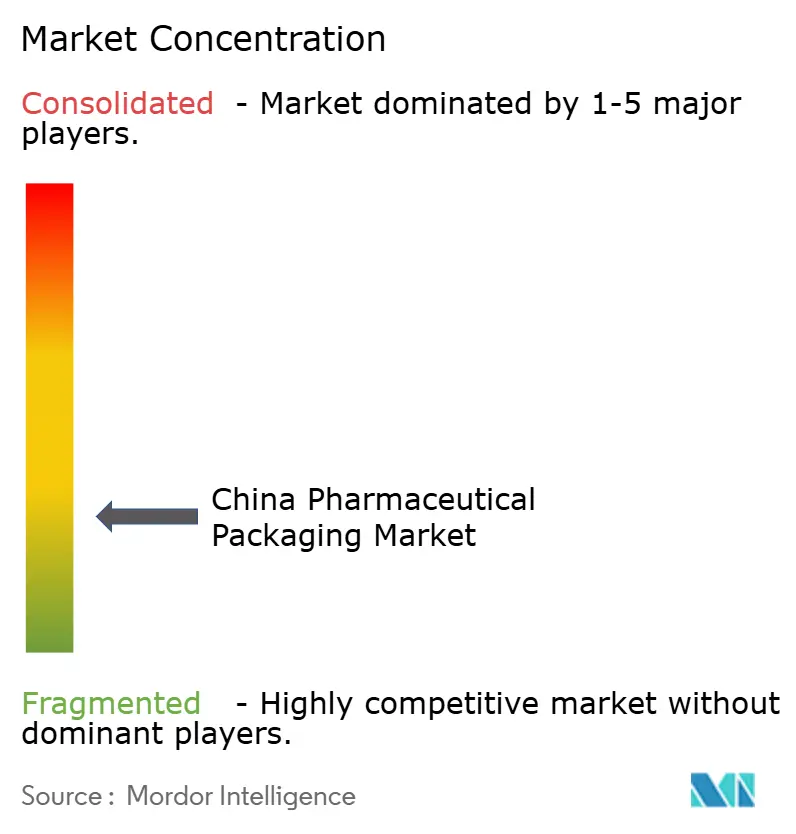

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Pharmaceutical Packaging Market Analysis by Mordor Intelligence

The China pharmaceutical packaging market size is expected to grow from USD 21.13 billion in 2025 to USD 22.41 billion in 2026 and is forecast to reach USD 30.07 billion by 2031 at 6.05% CAGR over 2026-2031. Supply-side investments in biologics capacity, carbon-neutrality pledges that push recyclable formats, and tightening anti-counterfeit rules combine to accelerate premium packaging adoption across the China pharmaceutical packaging market. Regulatory alignment with International Council for Harmonisation guidelines now requires unit-level serialization, driving capital spending on smart lines even as raw-material cost swings curb profit margins. Intensifying biomanufacturing programs—from the Ministry of Industry and Information Technology’s USD 4.17 billion outlay for 2025—to multinational R&D hubs in Beijing raise demand for sterile vials, prefillable syringes, and composite barrier materials. Meanwhile, cross-border e-pharmacy expansion to RMB 21.4 trillion (USD 3.3 trillion) lifts parcel-ready secondary and tertiary packs that withstand longer supply chains.

Key Report Takeaways

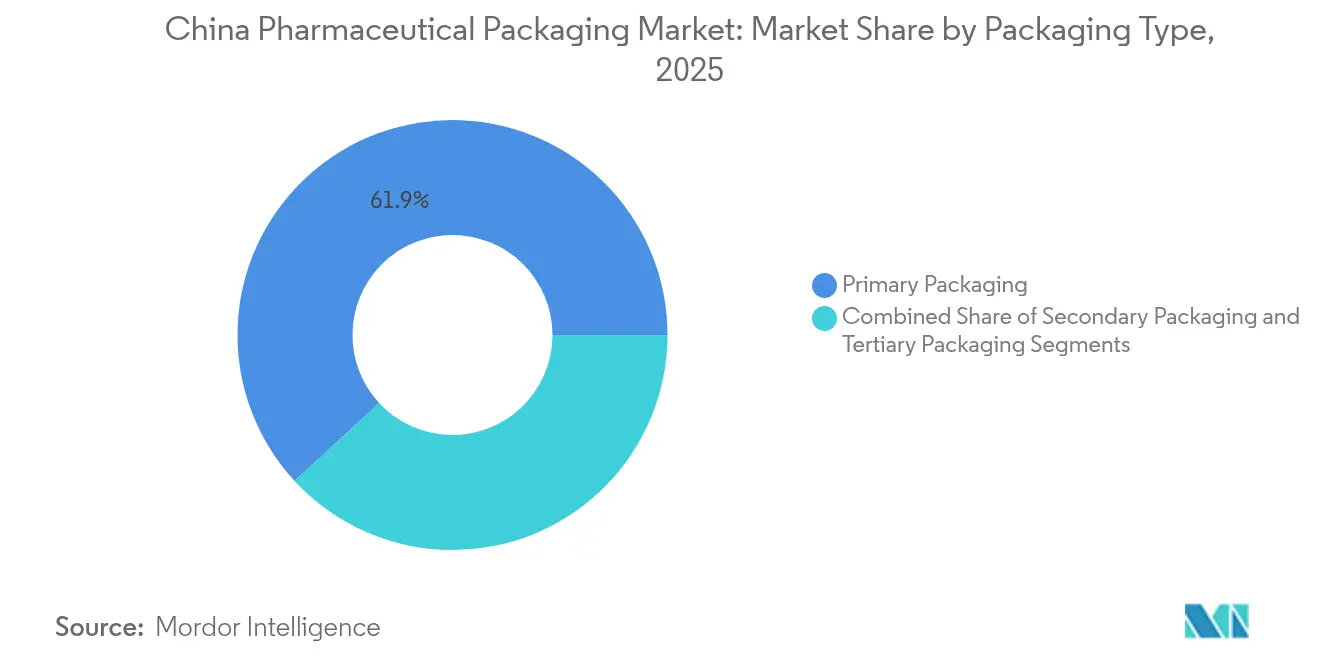

- By packaging type, primary packaging held 61.88% of China pharmaceutical packaging market share in 2025; parenteral formats are poised to expand at a 9.12% CAGR through 2031.

- By material, plastics captured 50.05% revenue in 2025, while paper & paperboard are projected to grow at an 8.35% CAGR to 2031.

- By drug form, solid orals controlled 42.12% share of the China pharmaceutical packaging market size in 2025, yet parenteral formulations lead growth at 9.12% CAGR.

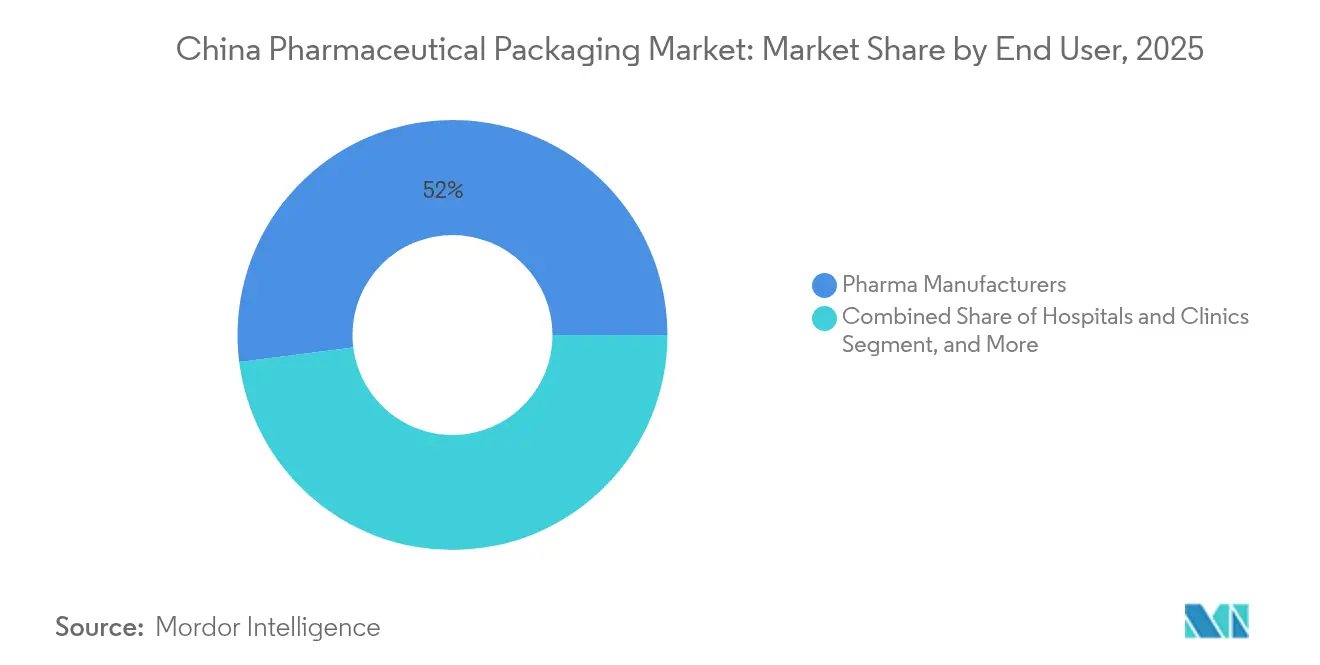

- By end user, pharmaceutical manufacturers accounted for 52.01% share in 2025, whereas hospitals and clinics are expected to register the fastest 9.12% CAGR during 2026-2031.

- By technology, conventional formats kept 59.85% share in 2025, while smart packaging solutions integrating NFC or RFID are forecast to advance at 8.47% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Pharmaceutical Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory clamp-down on counterfeit medicines | +1.2% | National, early gains in Tier 1 cities | Medium term (2-4 years) |

| Expansion of domestic generics and biologics manufacturing base | +1.8% | National, concentrated in Jiangsu, Shandong, Guangdong | Long term (≥ 4 years) |

| Ageing population driving chronic-care drug volumes | +1.5% | National, accelerated in northeastern provinces | Long term (≥ 4 years) |

| Provincial reimbursement tilt toward patient-friendly formats | +0.9% | Provincial variations, strongest in developed regions | Medium term (2-4 years) |

| Cross-border e-pharmacy boom needing parcel-ready packs | +0.7% | National, concentrated in coastal trading hubs | Short term (≤ 2 years) |

| Carbon-neutrality targets boosting recyclable/biopolymer packs | +0.6% | National, led by Beijing, Shanghai, Shenzhen | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Clamp-Down on Counterfeit Medicines

Enhanced oversight now extends from active ingredients to every packaging layer, underpinned by the National Medical Products Administration’s YY 1001-2024 standards for all-glass syringes. Mandatory serialization at each saleable unit has curtailed supply-chain opacity, prompting larger converters to install interoperable track-and-trace systems that harmonize with EU FMD and U.S. DSCSA rules. Provincial authorities in Shanghai and Shenzhen deploy blockchain-enabled customs channels that shorten clearance times while authenticating serialized codes. Early adopters of open architecture solutions record fewer product-recall incidents and negotiate premium pricing with multinational clients, whereas SMEs grapple with upfront investment and maintenance fees. Market exit of non-compliant lines removes low-price capacity, slowly lifting average selling prices for serialized packs in the China pharmaceutical packaging market.

Expansion of Domestic Generics and Biologics Manufacturing Base

China’s biopharma value exceeded CNY 650.6 billion (USD 91.5 billion) in 2024 and is projected to double by 2029, fueling a pivot from commodity bottles toward sterile barrier systems.[1]Sina Finance, “2024 China Biopharmaceutical Industry Panorama,” finance.sina.com.cn Provincial clusters in Jiangsu, Shandong, and Guangdong anchor integrated supply networks where bulk resin suppliers, container converters, and fill-finish plants co-locate to pare logistics cost. Luye Pharma’s U.S. FDA clearance for ERZOFRI®, a long-acting injectable, underscores domestic innovators’ rising demand for cyclic olefin polymer syringes that resist low-temperature storage. Multinationals deepen local footprints through R&D incubators and joint ventures, intensifying competition for packaging partners certified to U.S. and EU pharmacopeia standards. The resulting capacity race spurs capex in ISO 5 cleanrooms and nested vial trays, fortifying growth prospects for the China pharmaceutical packaging market.

Ageing Population Driving Chronic-Care Drug Volumes

Residents aged 65 and above surpassed 15% of the population in 2024, widening the chronic-disease burden and demanding packs that support daily adherence. The 2024 National Medical Insurance Drug List now reimburses roughly 3,900 products, compelling uniform labeling that simplifies regimen comprehension for elderly users. Northeastern provinces pilot color-coded blister sleeves with enlarged fonts to improve visibility, while tier-one hospitals in Beijing deploy NFC-enabled pill bottles that transmit dosage reminders to caregiver apps. Injectable therapies gain popularity, shifting volume toward sterile syringes and IV bags that demand high-clarity polypropylene or Type I borosilicate glass. This demographic wave secures a steady uptick in unit demand across the China pharmaceutical packaging market.

Provincial Reimbursement Tilt Toward Patient-Friendly Formats

Integration of Urban Employee and Urban-Rural insurance pools streamlines funding but preserves latitude for regional tender criteria. Wealthier municipalities reimburse single-dose, compliance-aid packs even at premium prices, prompting manufacturers to offer dual-SKU strategies: high-convenience formats for affluent cities and bulk bottles for price-sensitive counties. Carton converters adapt by adding braille and peel-off labels requested by provincial formularies. Diverse provincial policies thus create micro-markets inside the broader China pharmaceutical packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile petro-feedstock prices inflating plastic pack costs | -1.4% | National, concentrated in manufacturing hubs | Short term (≤ 2 years) |

| Capex burden of serialisation/anti-counterfeit lines for SMEs | -0.8% | National, most severe in Tier 2/3 cities | Medium term (2-4 years) |

| Impending PFAS restrictions threatening blister film obsolescence | -0.6% | National, early impact in export-oriented facilities | Medium term (2-4 years) |

| GMP packaging-design talent shortage slows innovation | -0.5% | National, acute in emerging biotech clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Petro-Feedstock Prices Inflating Plastic Pack Costs

High-density polyethylene averaged USD 910 per ton in 2024, but a 5 million-ton capacity influx in 2025 skews pricing unpredictably. Simultaneously, PVC import duties rose from 1% to 5.5%, adding USD 23 per ton and squeezing converters reliant on specialized film grades. Currency volatility and crude-oil price swings complicate long-term resin contracts, forcing packaging makers to diversify into glass or fiber substrates when feasible. Manufacturers unable to hedge resin exposure face shrinking margins within the China pharmaceutical packaging market.

Capex Burden of Serialisation/Anti-Counterfeit Lines for SMEs

Turn-key serialization suites that integrate vision inspection, cloud databases, and blockchain ledgers often exceed USD 2 million per line, a cost eclipsing annual revenue for many Tier-3 converters. Following the U.S. DSCSA deadline in 2024, several under-capitalized firms exited export channels, surrendering volume to larger peers. Domestic financing constraints spur consolidation waves as bigger groups absorb SME assets, incrementally raising the market concentration of the China pharmaceutical packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Primary Packaging Dominates Innovation

Primary containers captured 61.88% share in 2025 and are projected to grow at 8.96% CAGR through 2031 as drug-delivery functionality merges with containment. SCHOTT Pharma’s TOPPAC polymer syringe range posted 54% sales growth in 2024, signaling appetite for cyclic olefin solutions suitable for mRNA vaccines.Within the China pharmaceutical packaging market size for parenteral packs, nested ready-to-use configurations lower aseptic setup time in fill-finish plants. Secondary and tertiary packs evolve alongside booming e-commerce; corrugated shippers integrate shock sensors, enabling parcel-ready compliance for global export hubs in Shanghai free-trade zones.

Secondary packs advance at mid-single-digit growth, propelled by folding-carton demand that accompanies serialized QR codes and color-coded logistics labels. Tertiary formats integrate with AI-enabled Smart Customs scanners that clear pallets faster, reducing in-bond detention fees. Collectively, these shifts entrench primary-pack-centric innovation as the engine of the China pharmaceutical packaging market.

By Material: Sustainability Reshapes Material Selection

Plastics retained 50.05% share in 2025, buttressed by cost-effective HDPE bottles and polypropylene blisters. Yet fiber substrates clock an 8.35% CAGR as carbon-pricing schemes and hospital green-procurement policies gain traction. DS Smith’s TailorTemp shipper shows that molded-fiber can match thermal performance while trimming CO₂ by 40%. The China pharmaceutical packaging market size for glass vials and cartridges expands steadily amid biologics growth and premium positioning.

Aluminum remains critical for cold-form blisters when barrier integrity outweighs cost. SMEs explore poly(propylene carbonate) blends to meet impending PFAS prohibitions without sacrificing moisture resistance. Material substitution decisions thus balance regulatory headwinds, carbon accounting, and drug-stability imperatives across the China pharmaceutical packaging market.

By Drug Form: Parenteral Growth Accelerates

Solid orals formed 42.12% of 2025 revenue, yet parenteral units grow at a 9.12% CAGR on the back of oncology infusions and long-acting injectables. Hospitals favor ready-to-use prefilled syringes that reduce compounding risk and labour time, increasing cyclic olefin and borosilicate consumption within the China pharmaceutical packaging market. Topical patches gain share among urban asthma and COPD patients, spurring inhaler canister and foil pouch demand.

Ophthalmic solutions employ multi-dose preservative-free bottles enabled by blow-fill-seal technology, an area where TekniPlex expanded Italian capacity in 2024. Such diversification underscores the rising complexity of dosage-form-specific packaging in the China pharmaceutical packaging market.

By End User: Hospital Segment Drives Growth

Manufacturers still purchased 52.01% of packs in 2025, but hospital procurement is climbing at 9.12% CAGR as volume-based tendering channels packaging spend through provincial groups. Centralized orders favour bulk IV bags and nested syringe kits that streamline ward workflows, nudging converters to scale ISO 7 cleanrooms. Haleon’s USD 615 million investment to raise its Tianjin stake secures local supply for institution-channel products. Contract manufacturing organizations adapt by offering late-stage customization to align with diverse provincial barcoding rules, sustaining specialized niches inside the broader China pharmaceutical packaging industry.

By Technology: Smart Packaging Integration Accelerates

Conventional formats still comprised 59.85% revenue in 2025, but connected packs climb at 8.47% CAGR as adherence monitoring and cold-chain visibility become standard. Gerresheimer’s Gx Cap, piloted in local oncology trials, embeds an NFC tag that records each opening event, boosting dose-time accuracy. Anti-counterfeit layers—UV inks, tamper sleeves, and dynamic holograms—expand to comply with nationwide rollout of serialization. Sustainability overlaps with technology: Amcor’s recycled-aluminum Stelvin capsule blends carbon cuts with scannable authenticity markers. These converging trends accelerate digital adoption rates across the China pharmaceutical packaging market.

Geography Analysis

East-coast provinces spearhead output, with Jiangsu, Shandong, and Guangdong anchoring export-oriented drug and packaging plants connected to seaports and bonded zones. The China pharmaceutical packaging market size for these regions benefits from established resin supply chains, cleanroom clusters, and local tax incentives. The Yangtze River Delta’s life-sciences corridor hosts SCHOTT, Gerresheimer, and domestic glass majors, facilitating rapid deployment of ready-to-fill vial capacity that meets EU GMP.

Inland, Sichuan and Hubei leverage government grants to lure fill-finish projects, yet lag in GMP-trained packaging engineers, slowing material localization. Western provinces tap central funds for hospital expansion, raising demand for low-cost bulk bottles that suit centralized procurement budgets. At the same time, Smart Customs systems in 71 cities reduce inspection time for serialized export shipments, enabling faster turnaround for e-pharmacy parcels leaving Shenzhen or Shanghai airports.

Beijing and Shanghai cluster R&D investments—AstraZeneca’s USD 2.5 billion centre and Eli Lilly’s incubator—creating pilot grounds for high-end sustainable and smart packs aimed at early-phase clinical trials. Cross-border e-commerce sellers leverage these hubs for drop-shipping high-value biologics, demanding ultra-insulated cartons and data-logger integration. The geographic mosaic of policy, talent, and infrastructure thus shapes growth trajectories inside the China pharmaceutical packaging market.

Competitive Landscape

The China pharmaceutical packaging market is fragmented, yet rising compliance costs spur consolidation. International players—Amcor, SCHOTT Pharma, Gerresheimer—command premium biologics segments thanks to proprietary polymers, molded-glass know-how, and global validation. Domestic firms counter with cost competitiveness and familiarity with shifting provincial tenders.

Strategic moves illustrate this divergence. Gerresheimer recorded 9.2% organic growth in drug-delivery systems by expanding cyclic olefin syringe lines in Changzhou.[3]Gerresheimer, “Preliminary Figures FY 2024,” gerresheimer.comTekniPlex boosted European blister-film capacity, then routed Asia-bound volumes via free-trade zones to serve China biotech exports. DS Smith introduced fiber-based chill boxes targeting specialty pharmacy couriers, muscling into segments once dominated by expanded polystyrene.

Meanwhile, Chinese converters pursue mergers: Lakeside Holding’s acquisition of Hupan Pharmaceutical widens contract packing capabilities across oral solids and liquids. As serialization deadlines thin SME ranks, top-tier firms accumulate share, steadily lifting bargaining power upstream and downstream. This evolution reshapes competitive intensity in the China pharmaceutical packaging industry.

China Pharmaceutical Packaging Industry Leaders

Gerresheimer Shuangfeng Pharmaceutical Glass (Danyang) Co. Ltd (Gerresheimer AG)

West Pharmaceutical Services Inc.

Taishan Xinhua Pharmaceutical Packaging Co. Ltd

Ningbo Zhengli Pharmaceutical Packaging

Amcor Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: AstraZeneca committed USD 2.5 billion for a Beijing global R&D centre.

- March 2023: Eli Lilly opened its first non-U.S. innovation incubator in Beijing.

- January 2025: DS Smith launched TailorTemp, a fiber-based temperature-controlled pack achieving 40% CO₂ reduction.

- January 2025: PCI Pharma Services invested more than USD 365 million to enlarge EU and U.S. advanced drug-delivery facilities.

China Pharmaceutical Packaging Market Report Scope

The study considers revenues accrued from the sales of different pharmaceutical packaging products offered by various vendors operating in the market. The market is tracked in terms of revenue in USD. This report analyzes the factors that impact geopolitical developments in the studied market based on the prevalent base scenarios, key themes, and application of vertical-related demand cycles. The estimates for the Chinese pharmaceutical packaging market include all the costs associated with pharmaceutical packaging solution manufacturing, from raw material procurement to the end-user industry. It includes the cost of material used, the cost of other associated products such as inks and adhesives, closures, and the cost of related services like finishing, printing, labeling and marking, packing, and transporting. The estimates exclude the cost of the content that is or is to be packed inside the pharmaceutical packaging solution.

The Chinese pharmaceutical packaging market is segmented by packaging type (primary packaging (pharmaceutical plastic bottles, bottles and jars, blister packaging, pre-fillable syringes, vials and ampoules, IV containers, prefillable inhalers, and other primary packaging products) and secondary packaging (folding boxes and cartons (paper-based), corrugated shipping containers (paper-based), bags and pouches (flexible), clamshells (paper and plastic), and other secondary packaging products)). The report offers market forecasts and size in value (USD) for all the above segments.

| Primary Packaging | Plastic Bottles (HDPE, PET) |

| Blister Packs (PVC, Cold-form Alu) | |

| Pre-fillable Syringes | |

| Vials and Ampoules | |

| IV Containers | |

| Inhalers | |

| Others Primary Packaging | |

| Secondary Packaging | Folding Cartons |

| Corrugated Shippers | |

| Bags and Pouches | |

| Clamshells and Trays | |

| Tertiary Packaging |

| Plastics |

| Glass |

| Aluminium Foil / Laminate |

| Paper and Paperboard |

| Solid Oral |

| Parenteral |

| Topical / Transdermal |

| Inhalation |

| Ophthalmic |

| Other Drug Form |

| Pharma Manufacturers |

| Contract Manufacturing Organisations (CMOs) |

| Hospitals and Clinics |

| Conventional |

| Aseptic and Sterile |

| Smart and Connected (NFC/RFID) |

| Anti-counterfeit / Serialisation |

| Sustainable / Recyclable Solutions |

| By Packaging Type | Primary Packaging | Plastic Bottles (HDPE, PET) |

| Blister Packs (PVC, Cold-form Alu) | ||

| Pre-fillable Syringes | ||

| Vials and Ampoules | ||

| IV Containers | ||

| Inhalers | ||

| Others Primary Packaging | ||

| Secondary Packaging | Folding Cartons | |

| Corrugated Shippers | ||

| Bags and Pouches | ||

| Clamshells and Trays | ||

| Tertiary Packaging | ||

| By Material | Plastics | |

| Glass | ||

| Aluminium Foil / Laminate | ||

| Paper and Paperboard | ||

| By Drug Form | Solid Oral | |

| Parenteral | ||

| Topical / Transdermal | ||

| Inhalation | ||

| Ophthalmic | ||

| Other Drug Form | ||

| By End-User | Pharma Manufacturers | |

| Contract Manufacturing Organisations (CMOs) | ||

| Hospitals and Clinics | ||

| By Technology | Conventional | |

| Aseptic and Sterile | ||

| Smart and Connected (NFC/RFID) | ||

| Anti-counterfeit / Serialisation | ||

| Sustainable / Recyclable Solutions | ||

Key Questions Answered in the Report

What is the current size of the China pharmaceutical packaging market?

The market stands at USD 22.41 billion in 2026 and is forecast to rise to USD 30.07 billion by 2031 at a 6.05% CAGR.

Which packaging type leads revenue in China?

Primary packaging dominates with 61.88% share in 2025 as demand for sterile vials, syringes, and high-barrier blisters accelerates.

How fast is smart packaging growing in China?

Smart and connected formats using NFC or RFID are expected to post an 8.47% CAGR between 2026 and 2031.

What raw-material risks affect Chinese converters?

Volatile polyethylene and PVC prices, coupled with higher import tariffs, compress margins and compel diversification into glass and fiber substrates.

Why are parenteral packs the fastest-growing drug-form segment?

Biologics expansion and hospital preference for ready-to-use injectables push parenteral packaging volume at a 9.12% CAGR through 2031.

How do carbon-neutrality goals influence material choices?

Provincial green-procurement policies reward recyclable or fiber-based packs, prompting an 8.35% CAGR for paper & paperboard solutions.

Page last updated on: