In-Vitro Diagnostics Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.66 Billion |

| Market Size (2031) | USD 12.36 Billion |

| Growth Rate (2026 - 2031) | 5.04% CAGR |

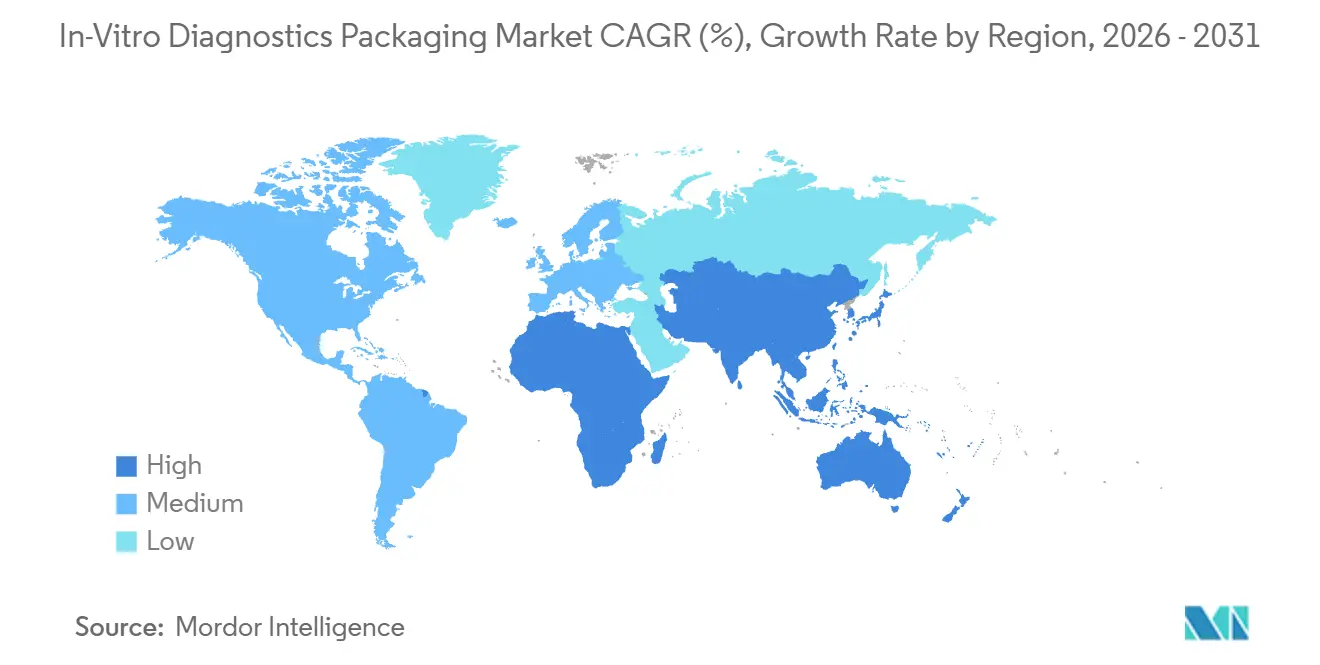

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

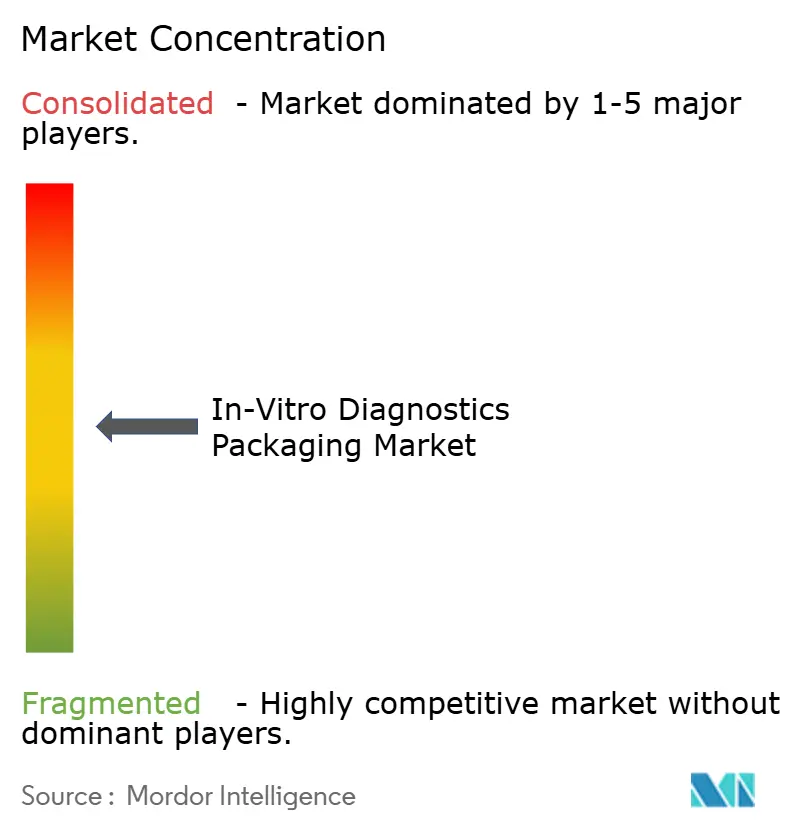

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

In-Vitro Diagnostics Packaging Market Analysis by Mordor Intelligence

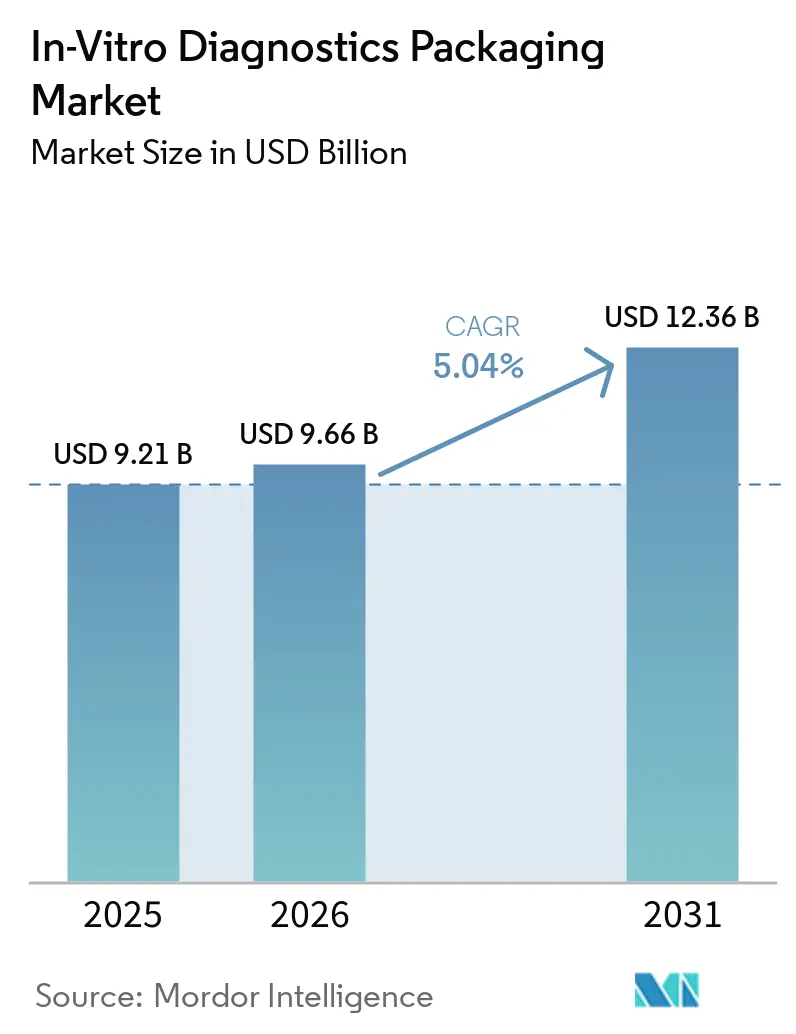

The in-vitro diagnostics packaging market size is projected to be USD 9.21 billion in 2025, USD 9.66 billion in 2026, and reach USD 12.36 billion by 2031, growing at a CAGR of 5.04% from 2026 to 2031. Strong laboratory automation adoption, rapid expansion of at-home test formats, and stricter container-closure integrity rules are reinforcing demand across materials from polypropylene to cyclic olefin copolymer. Polymer suppliers are moving away from legacy glass and commodity resins toward specialized grades that survive gamma sterilization and deep-freeze biobanking, aligning with newly enforced EU MDR and IVDR requirements. Regional dynamics continue to favor North America’s high-throughput reference labs, while Asia-Pacific’s new clinic build-outs and government screening programs accelerate volume growth. At the same time, sustainability targets under Europe’s Packaging and Packaging Waste Regulation amplify interest in recycled and bio-based inputs, even though medical-grade recycling infrastructure is still emerging.

Key Report Takeaways

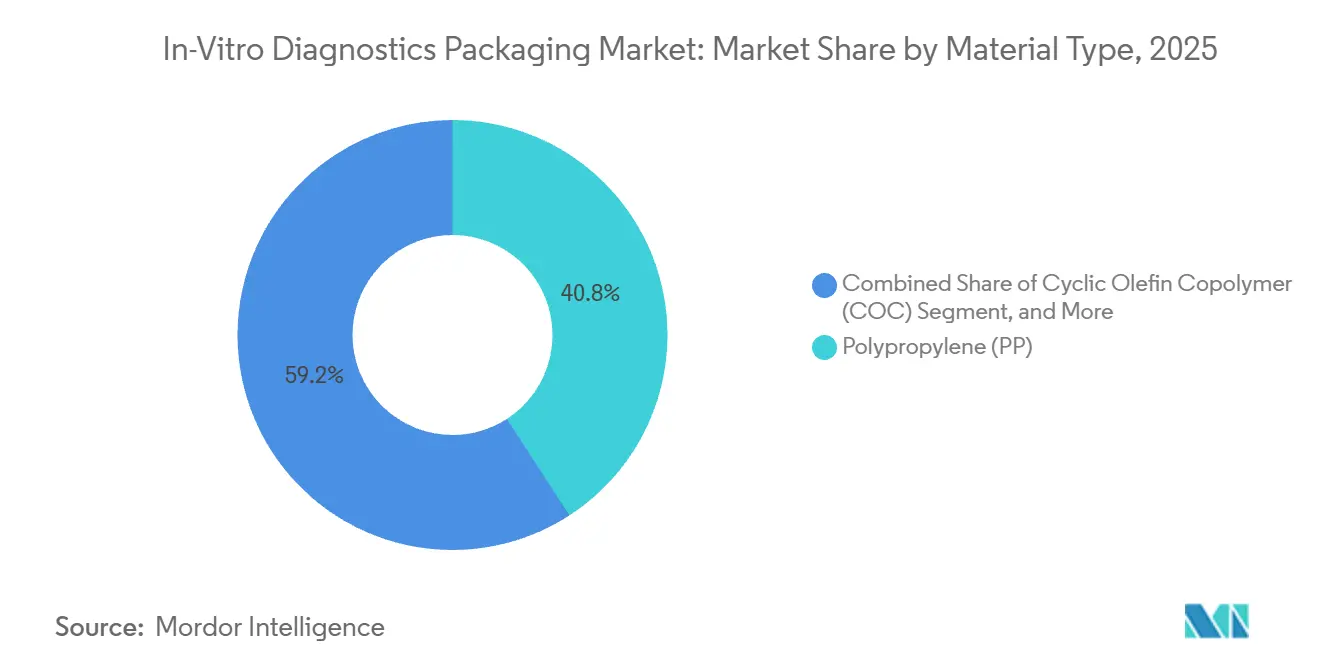

- By material type, polypropylene led with 40.84% of the in-vitro diagnostics packaging market share in 2025, while cyclic olefin copolymer is set to expand at a 6.43% CAGR through 2031.

- By product type, tubes accounted for 38.27% of the in-vitro diagnostics packaging market size in 2025, and closures are advancing at a 6.83% CAGR to 2031.

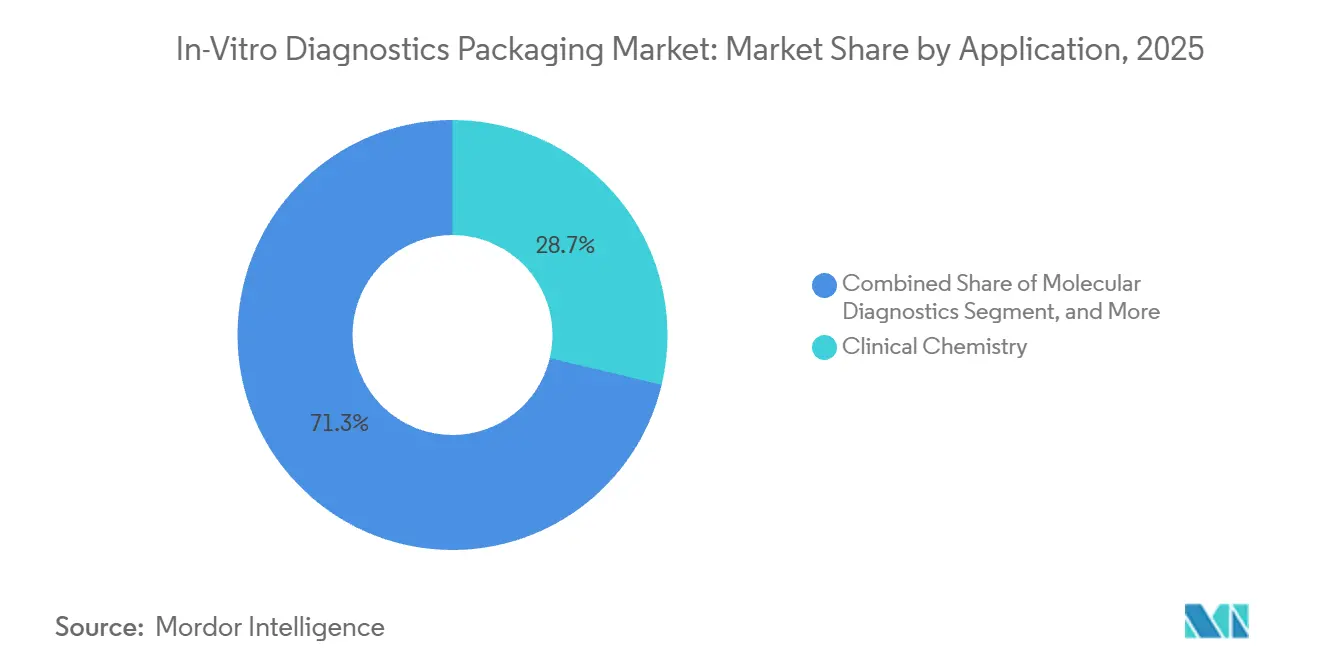

- By application, clinical chemistry accounted for 28.72% in 2025, whereas molecular diagnostics is projected to post a 6.52% CAGR through 2031.

- By end user, diagnostic laboratories accounted for 45.82% of market share in 2025, yet home healthcare providers are on track for a 6.76% CAGR over the forecast period.

- By geography, North America dominated with 39.87% in 2025, while Asia-Pacific recorded the fastest regional CAGR of 7.12% from 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global In-Vitro Diagnostics Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Tubes | +1.2% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Proliferation of At-Home Point-of-Care Tests | +1.0% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Automation Surge in High-Throughput Molecular Labs | +0.9% | North America, Europe, and urban Asia-Pacific hubs | Medium term (2-4 years) |

| Shift Toward Pre-Bar-Coded Primary Containers | +0.7% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Increasing Adoption of Vacuum Blood Collection Systems | +0.6% | Global, with rapid uptake in Asia-Pacific and South America | Medium term (2-4 years) |

| Biobank Expansion Fueling Cryogenic Vial Demand | +0.5% | North America, Europe, and China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Tubes

Vacuum and specialty specimen tubes keep the in-vitro diagnostics packaging market on a steady growth path. Blood collection centers have replaced manual syringes with evacuated tubes that cut hemolysis by double-digit margins, reducing repeat draws and labor costs.[1]Wiley Online Library, “Journal of Clinical Laboratory Analysis,” onlinelibrary.wiley.com Safety-engineered variants such as shielded needle systems obtained EU MDR certification in 2024 and now feature in hospital tenders across Europe.[2]BD, “Vacutainer Eclipse Blood Collection System,” bd.com Parallel progress in liquid-biopsy oncology is driving the uptake of cell-free DNA tubes that stabilize nucleic acids for 2 weeks without refrigeration, a necessity in logistics-challenged regions.[3]Greiner Bio-One, “VACUETTE Blood Collection Tubes,” gbo.com Robotic sample handlers add yet another design filter, as consistent sidewall thickness and barcode alignment within half-millimeter tolerances are essential for gripper accuracy. Collectively, these shifts confirm tubes as the volume anchor of the in-vitro diagnostics packaging market.

Proliferation of At-Home Point-of-Care Tests

Reimbursement reforms and patient convenience continue to pull testing from lab benches to living rooms, fueling the in-vitro diagnostics packaging market. United States guidance released in 2024 clarified labeling and child-resistance rules for over-the-counter kits, accelerating product approvals. A top-selling antigen test shipped more than 200 million clamshell packs in 2024, underscoring how durable primary packaging boosts consumer trust. Standards bodies now recommend that home-use formats mirror pharmaceutical moisture-barrier performance, effectively merging two supply chains. Digital integration raises the bar further, as regulators in the United Kingdom now require QR codes that route users to electronic instructions, increasing serialization complexity but improving traceability.[4]MHRA, “Guidance on Point-of-Care Tests,” gov.uk The result is a design environment where usability, security, and connectivity converge, lifting volumes for cap-and-carton suppliers that can meet the new checklist.

Automation Surge in High-Throughput Molecular Labs

Next-generation sequencers and fully automated extraction robots reshape material choices inside the in-vitro diagnostics packaging industry. A flagship sequencing platform now processes 20 000 genomes a year, demanding ultra-low DNA-binding plates fabricated from cyclic olefin copolymer, which retains clarity and integrity under 50 kGy gamma sterilization. Extraction instruments insist on conical tube bottoms to avoid reagent retention, pushing converters to retool older flat-bottom molds. Collaborative development is rising; one leading IVD company co-created RFID-capped tubes with a packaging partner to curb mislabeling by 95%. Such co-engineering not only secures dedicated demand streams but also embeds added-value electronics into primary containers, enlarging the revenue pool of the in-vitro diagnostics packaging market.

Shift Toward Pre-Bar-Coded Primary Containers

Hospitals seek zero-defect specimen identification, and pre-printed tubes are the favored remedy, adding sustained lift to the in-vitro diagnostics packaging market. Accreditation bodies highlight that labeling mishaps dominate pre-analytical errors, prompting investment in ready-coded consumables. A United States teaching hospital documented 22-minute reductions in patient turnaround after installing a bar-code-enabled draw system, translating to seven-figure annual savings. Uptake is still uneven because pre-coded tubes carry premiums near 20%, although new accreditation scoring in India rewards their use and may close the gap. Durability challenges linger, as sterilization cycles can bleach conventional inks, pushing suppliers toward laser etching that marginally increases per-unit costs but guarantees legibility across multiple autoclave passes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental Concerns Around Single-Use Plastics | -0.8% | Europe and North America, with emerging pressure in Asia-Pacific | Medium term (2-4 years) |

| Supply Chain Volatility for Medical-Grade Polymers | -0.6% | Global, with acute impact in Europe and Asia-Pacific | Short term (≤ 2 years) |

| Stringent EU MDR and IVDR Labeling Mandates | -0.5% | Europe, with spillover to export-oriented manufacturers globally | Long term (≥ 4 years) |

| Cost Pressures from Centralized Procurement in Public Health Systems | -0.4% | South America, Africa, and South Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Environmental Concerns Around Single-Use Plastics

Europe’s Packaging and Packaging Waste Regulation fixes a 65% recycled-content target by 2030, placing immediate pressure on single-use medical consumables. Because used diagnostic tubes are bio-hazardous, normal curbside systems reject them, so hospitals must invest in dedicated autoclaves and grinding hubs, each costing up to USD 5 million. Pilot programs prove technical feasibility but remain small, covering 42% diversion at best. Bio-based polypropylene has emerged as an alternative with a meaningful carbon delta, yet its 25% price premium keeps market share below 2%. New carbon-border tariffs effective in 2026 will narrow that cost delta, but until then, sustainability rules temper the overall growth of the in-vitro diagnostics packaging market.

Supply Chain Volatility for Medical-Grade Polymers

Polypropylene prices spiked 18% in early 2024 after a Middle East plant outage sidelined more than a million metric tons of annual propylene feedstock capacity. Smaller converters without long-term contracts absorbed the full hit, forcing pass-through surcharges and straining tender commitments. Parallel disruptions in PET supply, tied to delayed shipments of purified terephthalic acid, increased air-freight moves that quadrupled logistics spend for some European buyers. Regulatory shifts add another shock: pending United States PFAS bans will outlaw many legacy moisture-barrier coatings by 2027, shortening shelf life for certain molecular tubes by six months unless alternative coatings improve. Emerging markets add their own hurdles; India’s revised polypropylene standard now mandates batch-level certificates that extend import clearance by several weeks. The cumulative uncertainty erodes margins and complicates production planning across the in-vitro diagnostics packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: COC Gains Ground on Sterilization Compatibility

Polypropylene dominated the in-vitro diagnostics packaging market with 40.84% share in 2025, reflecting its low cost and proven sterilization tolerance. The segment benefited from high-volume injection molding lines, which kept conversion costs below USD 0.05 per tube. Cyclic olefin copolymer is now the fastest riser set to expand at a 6.43% CAGR through 2031, because its clarity and chemical inertness meet stringent next-generation sequencing cartridge specs. COC also shows tenfold break resistance compared with borosilicate glass, slashing transit damage claims and lowering insurance premiums for reference labs. Regulators have tightened integrity test protocols under updated Annex 1, favoring materials with predictable seal performance. Hybrid co-injection, which layers COC within a polypropylene shell, reduces raw-material spend by nearly one-fifth without compromising USP Class VI compliance. Glass still holds niche appeal in cryogenic and solvent-heavy reagent kits, but rising liability for microcracks signals a gradual erosion.

Material innovation mirrors regional compliance nuances. Japan’s extractables-and-leachables rule now adds up to four extra months to approvals for unfamiliar polymers. In the European Union, helium leak tests mandated for sterile uses favor stiffer polymers, giving COC an incremental boost. Suppliers pursuing sustainable differentiation are trialing bio-based polypropylene, yet uptake remains modest because end users in the in-vitro diagnostics packaging market still prioritize sterility and regulatory familiarity over carbon metrics. Expect multiple polymer chemistries to coexist, with share shifts governed by sterilization dose tolerance, transparency, and recycling compatibility.

By Product Type: Closures Lead on Safety Innovation

Tubes retained 38.27% of share in 2025, but closures outpaced all product classes, charting a 6.83% forecast CAGR as regulations elevate tamper-evidence and child-resistance requirements. ISO 8317 updates, mirrored in United States Poison Prevention Packaging enforcement, compel diagnostic brands to retrofit caps with visual or tactile breach indicators. One recent launch uses a color-changing liner that flips hue when opened, trimming counterfeit incidents by two-fifths in pilot markets. Induction-sealed foils likewise gain ground, since they remove torque variability during robot handling and boost container-closure integrity scores. Vials, although lower in unit volume, capture premium value because cyclic olefin formats avoid delamination and cut adsorption of fragile enzymes. Metal ROPP caps, a pharmaceutical staple, are reappearing on high-value molecular kits due to their long vacuum retention, satisfying recent accreditation guidance that calls for laser-based headspace leak tests.

Petri dishes and multi-well plates fill specialized microbiology or cell-culture needs, but their share remains single digits. Secondary packaging, specimen bags, and desiccant inserts round out the category, each shaped by moisture-barrier and biohazard containment standards. As direct-to-patient shipments climb, outer cartons must now survive small-parcel drop tests and carry QR codes that link to interactive instructions, pushing converters to multipass digital print systems. Product-level diversification therefore hinges on safety functionality, automation fit, and e-commerce resilience, elements that jointly steer revenue distribution across the in-vitro diagnostics packaging market.

By Application: Molecular Diagnostics Reshape Packaging Specs

Clinical chemistry currently anchors demand with 28.72% of market share in 2025, but molecular diagnostics is scaling faster on a 6.52% CAGR, rewriting specification playbooks. Cell-free DNA tubes featuring proprietary stabilizers hold plasma integrity for two weeks, enabling global shipment without dry ice, a benefit valued at USD 50 per specimen in remote collection routes. Sequencing workflows rely on ultra-clear COC plates to prevent fluorescence scatter, while PCR tests favor conical microtubes that accommodate magnetic-bead extraction. Routine panels remain cost-sensitive, so serum-separator tubes with gel barriers dominate in-hospital chemistries, reducing centrifuge load and cutting error rates. Hematology's relevance hinges on precise EDTA dosages, which now require gravimetric fills accurate to ±2%, driving automation upgrades among regional converters.

Assay miniaturization transforms volume economics; microfluidic chips absorb microliter samples, shifting unit demand from 5 mL tubes toward 1.5 mL formats that still demand robust bar-coding and sensor compatibility. Regulatory categories are splintering, with the United States CLIA waiver encouraging simplified home-use molecular kits that marry pharmaceutical packaging rigor with consumer ergonomics. The confluence of oncology, infectious disease, and genetic screening will therefore keep molecular subsegments as the innovation frontier, progressively enlarging their place in the in-vitro diagnostics packaging market.

By End User: Home Healthcare Redefines Usability Standards

Diagnostic laboratories commanded 45.82% share in 2025, leveraging bulk contracts that pare tube prices to pennies and supporting full robotic lines that grip containers at 50 newtons without slippage. Yet home healthcare providers post the speediest climb, rising at a 6.76% CAGR as value-based insurance favors decentralized sampling. Tubes bound for consumers need textured grip zones, color-coded caps, and leak-proof seals that tolerate over-tightening. Kit makers are also adding desiccant pouches and pictorial instructions adhering to ISO 15223-1 icons, bridging literacy gaps.

Academic and research institutes pursue specialty cryogenic vials fit for -196 °C storage, a niche fueled by large-scale biobank expansions that will need tens of millions of new containers. Hospitals gravitate toward integrated cartridges compatible with handheld analyzers, demanding prolonged sensor calibration stability and refrigerated supply chains. Cybersecurity guidance now applies whenever QR or NFC codes appear on packs, extending validation timelines for digital elements. These multilayer compliance tracks heighten the design gap between professional lab consumables and patient-centric kits, prompting converters to develop dual road maps inside the in-vitro diagnostics packaging market.

Geography Analysis

North America keeps its leadership with 39.87% of market share in 2025, underpinned by large reference laboratories, national biobank programs, and widespread ISO 15189 accreditation that mandate pre-bar-coded tubes and advanced closure integrity. Federal funding for laboratory automation, pegged at USD 4.5 billion in 2026, maintains present-day capex cycles while private insurers reimburse advanced molecular tests, preserving premium material usage. Canada’s universal model adds stable baseline volumes, though tends to favor cost-efficient polypropylene over high-end COC.

Asia-Pacific is the growth engine of the in-vitro diagnostics packaging market, on track for a 7.12% CAGR through 2031. China’s Healthy China 2030 blueprint continues to add thousands of primary clinics, each equipped with basic hematology and chemistry analyzers that run high-volume vacuum tubes. India’s Ayushman Bharat scheme covers 500 million citizens, expanding test access but enforcing pricing that pressures converters to drive down unit costs. South Korea and Australia advance top-tier molecular diagnostics, driving demand for COC- and RFID-capable tubes, while language-specific labeling rules in remote Australian communities require dual-language cartons.

Europe remains sizable, although post-Brexit divergence and EU MDR transition expenses add budget strain. France and Germany prefer premium glass or hybrid vials, sustaining volume for borosilicate specialists. South America’s largest buyer is Brazil’s public system that awards multi-year tenders to lowest bidders, compressing margins yet guaranteeing throughput. The Middle East, led by Saudi Arabia and the United Arab Emirates, channels sovereign investment into state-of-the-art reference labs linked to economic diversification initiatives. Africa remains two-track, with private South African groups matching European quality while donor-funded programs in Nigeria and Kenya source low-cost, ambient-stable specimen carriers.

Competitive Landscape

The in-vitro diagnostics packaging market remains moderately fragmented, with players such as Becton, Dickinson and Company, Greiner AG, Terumo, Thermo Fisher Scientific, and others competing on vertical integration, proprietary geometries, and regulatory head starts. Recent megadeals, including a USD 17.3 billion proteomics acquisition that bundled low-binding plates, reflect the push to secure captive demand pipelines. Focused expansion plays also surface, as a USD 100 million COC vial plant in North Macedonia aims directly at European and Middle Eastern cartridge programs.

Technology capability is a new moat. European accreditation bodies now recommend laser-based headspace analysis for container-closure checks, a method requiring in-house metrology systems costing USD 2 million each. Suppliers that invested early secured first-mover advantage, because smaller converters must outsource tests at USD 5,000-10,000 per SKU, elongating commercialization. Patent filings reinforce lead positions; one glass leader submitted a dozen surface-coating patents over 2024-2025 aimed at reducing protein adsorption in liquid-biopsy tubes.

Sustainability creates whitespace. Fewer than 15% of participants currently offer verifiable recycled-content products despite looming 2030 mandates, leaving room for entrants able to qualify post-consumer medical-grade resin streams. Hybrid glass-plastic vials that balance break resistance with low extractables also widen differentiation. Overall, supplier strategies oscillate between capacity scale-ups in core polymers and high-margin niches such as RFID caps, all under the shadow of evolving sterility, integrity, and environmental rules that reshuffle competitive ranking inside the in-vitro diagnostics packaging market.

In-Vitro Diagnostics Packaging Industry Leaders

Thermo Fisher Scientific Incorporated

Corning Incorporated

DWK Life Sciences

Amcor plc

AptarGroup Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: SCHOTT Pharma initiated a joint trial with a leading oncology laboratory network to validate gamma-sterilized COC vials for automated liquid-biopsy lines.

- November 2025: The European Cooperation for Accreditation released a position paper endorsing laser-based headspace analysis for all primary containers, expected to influence ISO 15189 audits.

- August 2025: Corning reached mechanical completion of its USD 500 million North Carolina glass tubing expansion, adding 150 million vial capacity for molecular diagnostics.

- May 2025: Greiner Bio-One doubled production of VACUETTE CAT tubes at its Kremsmuenster plant to meet Southeast Asian demand for gel-barrier formats.

Global In-Vitro Diagnostics Packaging Market Report Scope

The in-vitro diagnostics packaging market involves tests performed on samples, such as blood or tissue, taken from the human body. In vitro diagnostics can detect diseases or other conditions, and can also be used to monitor a person’s overall health to help cure, treat, or prevent diseases.

The In-Vitro Diagnostics Packaging Market Report is Segmented by Material Type (Polypropylene, Polyethylene Terephthalate, Borosilicate Glass, Cyclic Olefin Copolymer, and Other Material Types), Product Type (Bottles, Vials, Tubes, Petri Dishes, Closures, and Other Product Types), Application (Clinical Chemistry, Molecular Diagnostics, Hematology, and Other Applications), End User (Hospitals, Diagnostic Laboratories, Academic and Research Institutes, and Home Healthcare Providers), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Polypropylene (PP) |

| Polyethylene Terephthalate (PET) |

| Borosilicate Glass |

| Cyclic Olefin Copolymer (COC) |

| Other Material Types |

| Bottles |

| Vials |

| Tubes |

| Petri dishes |

| Closures |

| Other Product Types |

| Clinical Chemistry |

| Molecular Diagnostics |

| Hematology |

| Other Applications |

| Hospitals |

| Diagnostic Laboratories |

| Academic and Research Institutes |

| Home Healthcare Providers |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Nigeria | |

| Rest of Africa |

| By Material Type | Polypropylene (PP) | |

| Polyethylene Terephthalate (PET) | ||

| Borosilicate Glass | ||

| Cyclic Olefin Copolymer (COC) | ||

| Other Material Types | ||

| By Product Type | Bottles | |

| Vials | ||

| Tubes | ||

| Petri dishes | ||

| Closures | ||

| Other Product Types | ||

| By Application | Clinical Chemistry | |

| Molecular Diagnostics | ||

| Hematology | ||

| Other Applications | ||

| By End User | Hospitals | |

| Diagnostic Laboratories | ||

| Academic and Research Institutes | ||

| Home Healthcare Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the in-vitro diagnostics packaging market today?

It stands at USD 9.66 billion in 2026, with a forecast value of USD 12.36 billion by 2031.

Which material is growing fastest in diagnostics packaging?

Cyclic olefin copolymer leads on a projected 6.43% CAGR because it tolerates high gamma doses and offers glass-like clarity.

What region shows the strongest growth momentum?

Asia-Pacific is projected to rise at 7.12% per year through 2031 thanks to new clinic construction and public screening programs.

Why are closures drawing investor interest?

Updated ISO 8317 and tamper-evidence mandates push closures ahead of other products with a 6.83% CAGR forecast.

How does sustainability affect procurement decisions?

European 65% recycled-content rules and global PFAS restrictions force buyers to favor recyclable resins and fluorine-free coatings despite higher costs.

Page last updated on: