Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

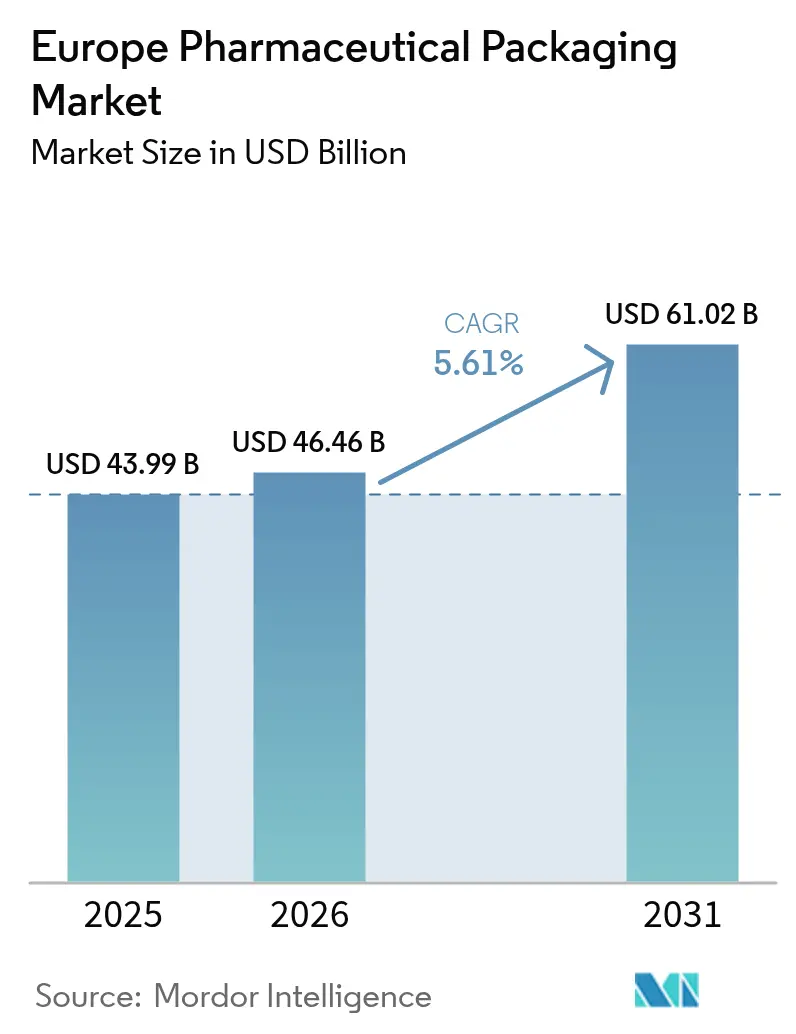

| Base Year Market Size (2025) | USD 43.99 Billion |

| Market Size (2026) | USD 46.46 Billion |

| Market Size (2031) | USD 61.02 Billion |

| Growth Rate (2026 - 2031) | 5.61% CAGR |

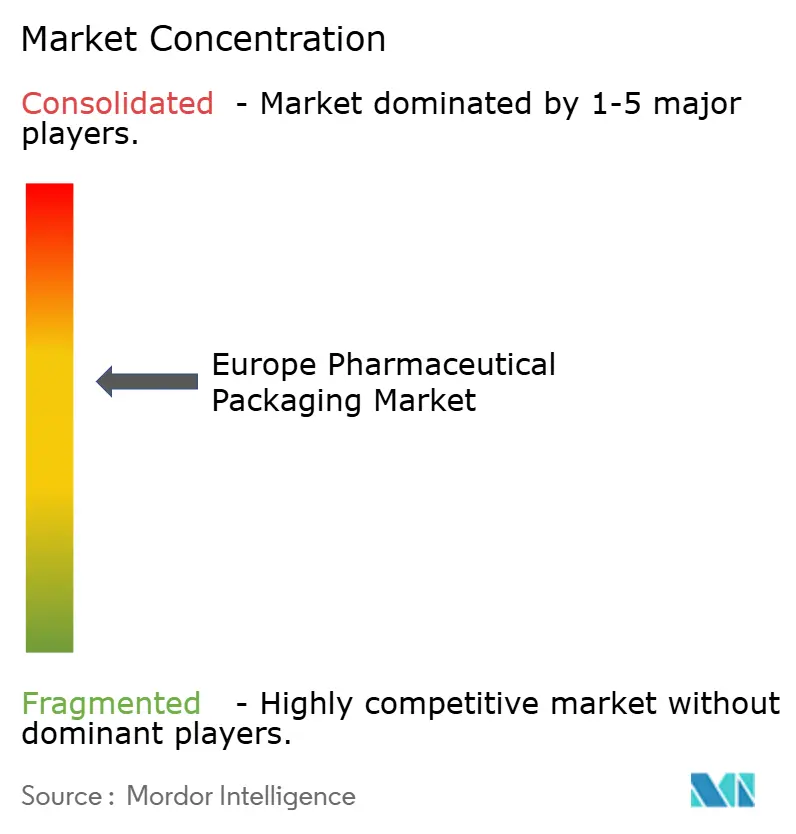

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Pharmaceutical Packaging Market Analysis by Mordor Intelligence

The Europe pharmaceutical packaging market size was valued at USD 43.99 billion in 2025 and estimated to grow from USD 46.46 billion in 2026 to reach USD 61.02 billion by 2031, at a CAGR of 5.61% during the forecast period (2026-2031). Demand is expanding as biologics and injectable therapies move to the commercial forefront, forcing drugmakers to favor pre-fillable syringes, ready-to-fill vials, and temperature-controlled distribution formats. Parallel to this shift, the European Commission’s Packaging and Packaging Waste Regulation (PPWR) is setting recycled-content thresholds that encourage converters to qualify medical-grade recycled polyethylene terephthalate and high-density polyethylene at scale. Logistics providers are adding GDP-compliant cold-chain hubs, while label specialists are equipping secondary packs with NFC chips to meet the requirements of the Falsified Medicines Directive. Capital intensity is high, with glass and plastics suppliers investing more than EUR 2 billion (USD 2.2 billion) in aseptic fill-finish and recycled-content extrusion lines from 2023 to 2027.

Key Report Takeaways

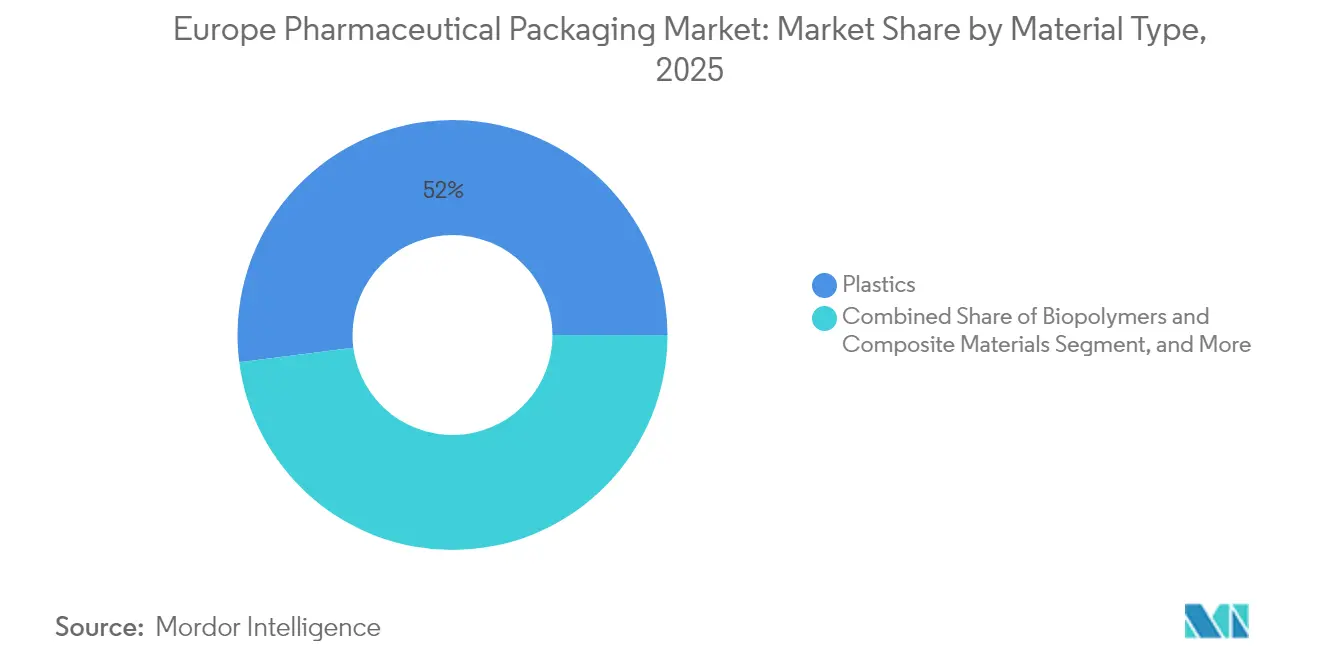

- By material type, plastics led with a 52.03% share of the Europe pharmaceutical packaging market in 2025, while biopolymers and composite materials are projected to expand at a 6.86% CAGR through 2031.

- By packaging type, primary formats captured 62.10% of the Europe pharmaceutical packaging market share in 2025 and are anticipated to grow at the highest CAGR of 6.58% from 2026 to 2031.

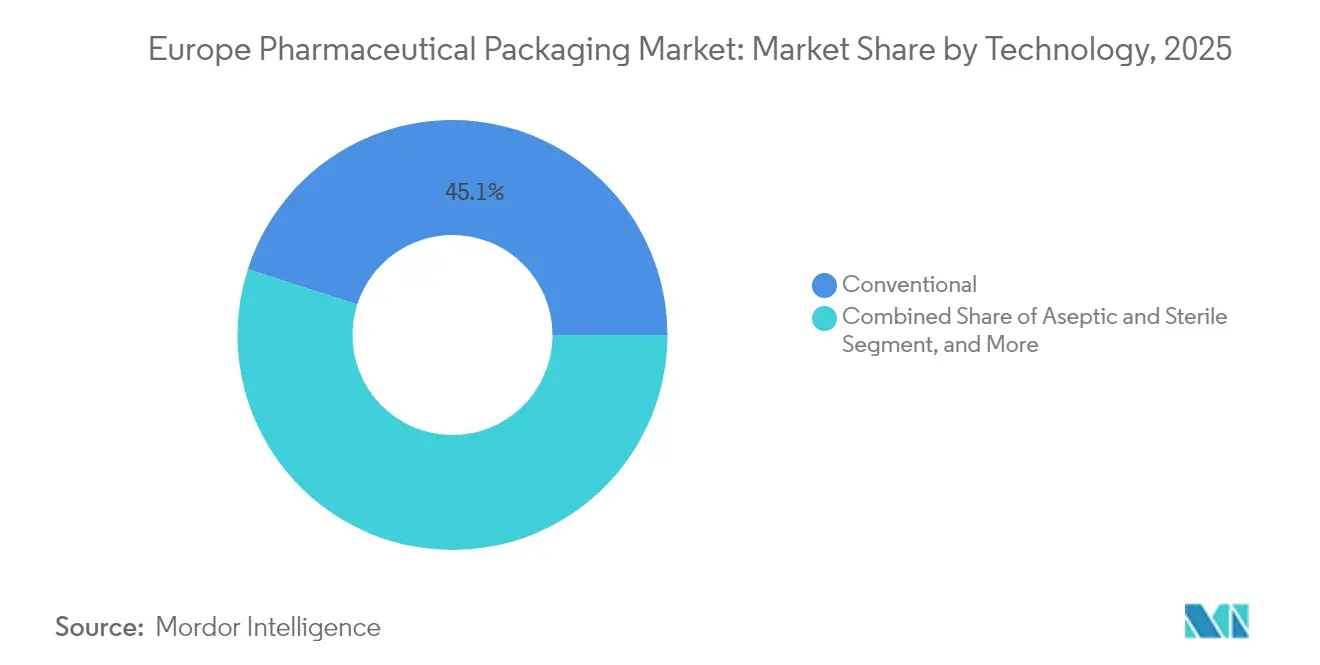

- By technology, conventional designs held 45.05% of the Europe pharmaceutical packaging market share in 2025, whereas smart and connected solutions are forecast to register the quickest 7.55% CAGR over the same horizon.

- By end user, pharmaceutical manufacturers accounted for 54.40% of the Europe pharmaceutical packaging market share in 2025, while contract manufacturing and packaging organizations are poised for a 6.36% CAGR through 2031.

- By country, Germany dominated the Europe pharmaceutical packaging market with a 22.30% share in 2025, and Poland is expected to post the fastest growth rate of 7.72% during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Pharmaceutical Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of Biologics and Injectable Therapies | +1.2% | Germany, France, Switzerland, with spillover to Poland and Italy | Medium term (2-4 years) |

| Stringent EU Serialization Mandates | +0.9% | EU-27, UK, Switzerland | Short term (≤ 2 years) |

| Rising Demand for Patient-Friendly Drug Delivery Formats | +0.8% | Germany, France, UK, Nordics | Medium term (2-4 years) |

| Adoption of NFC-Enabled Smart Labels for Anti-Counterfeiting | +0.7% | EU-27, with early adoption in Germany, France, Italy | Short term (≤ 2 years) |

| Expansion of Temperature-Controlled Mail-Order Pharmacies | +0.6% | Germany, Netherlands, Poland, UK | Medium term (2-4 years) |

| Recycled Medical-Grade Plastics Mandate Under EU PPWR | +0.5% | EU-27 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth of Biologics and Injectable Therapies

Biologics accounted for more than 30% of new molecular entities approved by the European Medicines Agency in 2024, elevating demand for parenteral containers with low extractables and tight dimensional tolerances. SCHOTT Pharma reported EUR 2.095 billion (USD 2.30 billion) in fiscal 2024 revenue, 78% of which came from drug containment solutions, including Type I borosilicate vials and cyclic olefin polymer cartridges.[1]SCHOTT Pharma, “Annual Report 2024,” schott.com West Pharmaceutical Services derived USD 1.98 billion from proprietary components, including NovaPure stoppers and Daikyo Crystal Zenith syringes in the nine months to September 2024. Stevanato Group grew its first-half 2024 revenue 11.6% year over year, driven by EZ-fill vials and the Nexa autoinjector platform. A September 2024 alliance among Gerresheimer, Stevanato, and SCHOTT Pharma is expected to harmonize ready-to-fill specifications, potentially reducing qualification timelines for biosimilars, particularly in Poland and Italy, where contract manufacturing growth is strongest.

Stringent EU Serialization Mandates

The Falsified Medicines Directive requires every prescription pack distributed in the European Union to carry a unique identifier and a tamper-evident device, generating a EUR 1.2 billion aftermarket for serialized labels, 2D barcodes, and NFC-equipped cartons through 2026.[2]European Medicines Agency, “Falsified Medicines Directive,” ema.europa.eu Schreiner MediPharm has expanded its NFC label portfolio to support authentication and patient engagement use cases. CCL Industries reported CAD 5.1 billion (USD 3.75 billion) revenue for the first nine months of 2024, with healthcare and specialty labels benefiting from aggregation upgrades. The United Kingdom has mirrored EU serialization rules post-Brexit, compelling label converters to deliver interoperable solutions for pan-European supply chains.

Adoption of NFC-Enabled Smart Labels for Anti-Counterfeiting

Near-field communication labels embed encrypted chips that confirm product provenance, register custody transfers, and deliver patient-facing content. AptarGroup’s Pharma segment earned USD 445 million in Q3 2024, supported by connected inhalers and autoinjectors linked to cloud-based medication-adherence dashboards. German and French payers, who are piloting outcomes-based reimbursement, now request adherence data harvested via smart packs for biologics priced above EUR 500 per dose. As a result, pharmaceutical brands are integrating IoT-ready NFC tags during secondary-pack design stages rather than retrofitting late in the cycle.

Expansion of Temperature-Controlled Mail-Order Pharmacies

Direct-to-patient distribution is scaling as advanced therapy medicinal products receive EMA guidance for home administration. UPS Healthcare invested USD 500 million in GDP-certified hubs across Poland and the Netherlands during 2024, raising European cold-chain capacity by 30%. DHL Supply Chain inaugurated automated cold stores in Germany and Spain that monitor real-time temperature excursions via IoT-enabled shippers.[3]UPS Healthcare, “European Cold-Chain Expansion,” ups.com Redcare Pharmacy commissioned a 25,000-square-meter fulfillment center in Germany, capable of handling biologics and over-the-counter items at multiple temperatures. Visibility into last-mile integrity is reducing reimbursement cycles as payers track therapy outcomes in real-time.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Pharmaceutical-Grade Raw Material Prices | -0.8% | EU-27, UK, with acute impact in Germany, France, Italy | Short term (≤ 2 years) |

| Increasing Sustainability Compliance Costs | -0.5% | EU-27 | Medium term (2-4 years) |

| Capacity Bottlenecks for Pharma-Grade Molded Glass Vials | -0.6% | Germany, France, Italy, with spillover to Poland | Short term (≤ 2 years) |

| Extended CE-Mark Review Timelines for Combination Products | -0.4% | EU-27, UK, Switzerland | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Pharmaceutical-Grade Raw Material Prices

Borosilicate glass tubing and cyclic olefin copolymer resins climbed 18-22% in 2024 as European energy costs surged. Continuous glass furnaces require an operating temperature of 1,500 °C, anchoring producers to natural-gas inputs that remain vulnerable to geopolitical shocks. West Pharmaceutical Services now secures its supply with multi-year resin contracts to protect Daikyo Crystal Zenith components from spot-price fluctuations. Elevated input costs have accelerated material-substitution studies involving cyclic olefin polymer and polyethylene terephthalate glycol; however, these alternatives require extensive stability data before EMA approval.

Capacity Bottlenecks for Pharma-Grade Molded Glass Vials

COVID-19 vaccination campaigns and biosimilar launches are expected to stress European molded-glass capacity through mid-2024, with lead times peaking at 28 weeks before easing to 16-20 weeks in Q4 2024. SCHOTT Pharma is installing new furnaces in Hungary and Serbia, which will enable the production of 1 billion vials per year by 2026. Nonetheless, the 18-to 24-month commissioning window for ISO 15378-certified lines keeps supply tight, sustaining pricing power for incumbents. Pharmaceutical firms, therefore, prioritize ready-to-fill platforms that shorten fill-finish cycles and lower particulate risks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Biopolymers Gain Momentum as PPWR Deadlines Near

Plastics dominated the Europe pharmaceutical packaging market with a 52.03% share in 2025, led by polyethylene terephthalate bottles and polypropylene blister films. Glass remained second in value, owing to Type I borosilicate vials and cartridges, a segment fortified by EUR 1.5 billion (USD 1.65 billion) in furnace investments from Gerresheimer, Schott Pharma, and SGD Pharma between 2023 and 2027. Biopolymers and composite materials are projected to grow at a 6.86% CAGR, driven by brand owners seeking to meet PPWR recycled-content requirements without compromising barrier properties. Amcor and Nolato are qualifying polylactic and polyhydroxyalkanoate resins for non-contact layers that still meet the ISO 15378 process validation thresholds.

Regulatory hurdles slow the uptake of biopolymers in primary containers, yet converters with scale can amortize validation costs, creating a two-tier supplier landscape. As PPWR enforcement tightens after 2028, growth in plastics for oral-solid dosage formats will moderate, while Glass and cyclic olefin polymers will retain their premium status in high-value biologics.

By Packaging Type: Primary Containers Capture Biologics Premium

Primary formats are expected to account for 62.10% of the Europe pharmaceutical packaging market size in 2025 and are projected to rise at a 6.58% CAGR through 2031. Bottles for tablets remain the largest sub-segment, but their growth lags as injectables and inhalables gain share. Pre-fillable syringes and cartridges underpin West Pharmaceutical Services’ USD 1.98 billion proprietary-components revenue, highlighting the margin leverage embedded in drug-delivery systems. Vials and ampules face intermittent supply constraints despite the introduction of new capacity in Hungary and Serbia.

Secondary packaging, which accounts for 30-35% of spending, grows in tandem with serialization and NFC adoption, as evidenced by CCL Industries’ healthcare-label revenue uptick. Tertiary corrugated packs hold the balance, aided by e-commerce distribution for chronic-disease therapies. The underlying shift concentrates value creation in primary packs where regulatory moats and technical complexity remain highest.

By Technology: Smart Solutions Outpace Conventional Formats

Conventional designs still accounted for 45.05% of 2025 revenue, but smart and connected formats are expected to compound at 7.55% through 2031 as serialization, anti-counterfeiting, and adherence monitoring converge. Schreiner MediPharm’s NFC labels, already embedded in oncology cartons, authenticate origin and push dosing reminders to smartphones.

AptarGroup’s connected inhalers stream sensor data to cloud dashboards, underpinning its USD 445 million Q3 2024 Pharma turnover. Aseptic-sterile technologies expand in lockstep with the growth of biologics, while recyclable-ready designs accelerate as PPWR milestones near.

By End User: Outsourced Capacity Accelerates Among Mid-Tier Biotechs

In-house pharmaceutical plants accounted for 54.40% of demand in 2025. Yet, contract manufacturing organizations are attracting investment, growing at a 6.36% CAGR, as mid-sized biotechs race to market without building costly fill-finish lines. Almac Group’s GBP 65 million (USD 81.9 million) packaging hub in the United Kingdom offers serialization and cold-chain services for late-phase trials.

Sandoz’s PLN 171 million (USD 43 million) center in Poland produces 4 billion serialized blister packs annually. Hospitals and clinics, the smallest segment, increasingly order unit-dose packs to curb medication error risks. The Europe pharmaceutical packaging market, therefore, splits between vertically integrated big pharma and outsourcing-oriented biotech innovators.

Geography Analysis

Germany generated 22.30% of the European pharmaceutical packaging market revenue in 2025, anchored by clustered glass-vial makers such as Gerresheimer and Schott Pharma, whose combined 2024 sales surpassed USD 4 billion. Energy-price volatility elevated input costs, leading converters to favor ready-to-fill formats that reduce furnace runtime and speed customer validation.

Poland is poised for the fastest 7.72% CAGR through 2031, as pharmaceutical companies establish greenfield aseptic and serialization-ready facilities, supported by government R&D incentives. Sandoz, Polpharma, and GSK collectively expanded packaging or API capacity during 2024, positioning the country as Central Europe’s logistics gateway.

The United Kingdom, France, Spain, and Italy jointly contribute 35-40% of the Europe pharmaceutical packaging market. The United Kingdom will maintain EU-equivalent serialization codes post-Brexit, ensuring cross-border packaging compatibility. France tightens biologic-stability testing, which drives Type I borosilicate demand, while Italy pilots outcomes-linked payment contracts that rely on NFC-enabled adherence data to facilitate reimbursement releases. Remaining Northern and Eastern European markets grow at roughly the regional average, with generic-dominant portfolios favoring cost-effective plastic blisters.

Competitive Landscape

Five leading suppliers account for around 35% of the primary-pack segment, while secondary and tertiary tiers remain fragmented. GERRESHEIMER, SCHOTT Pharma, and Stevanato agreed in September 2024 to standardize ready-to-fill vials and cartridges, allowing customers to dual-source without requiring repeated validation.

West Pharmaceutical Services builds IoT sensors into NovaPure stoppers to create closed-loop adherence feedback, differentiating its offer when payers demand outcome tracking. Amcor leverages its global scale to qualify recycled PET and HDPE that meet PPWR's recycled-content levels, thereby defending its share ahead of the 2030 deadline.

White-space opportunities favor connected packaging, biopolymer secondary packs, and modular fill-finish lines. Schreiner MediPharm and CCL Industries attack incumbents by embedding NFC chips into cartons at cost points mainstream brands can afford. ISO 15378 and EU-GMP Annex 1 validation cycles remain formidable entry barriers; however, niche digital-health expertise and recycled-material know-how can carve out profitable niches.

Europe Pharmaceutical Packaging Industry Leaders

Amcor Plc

Gerresheimer AG

Schott AG

AptarGroup Inc.

CCL Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Amcor began commercial production of a medical-grade blister film containing 30% recycled PET, certified to meet PPWR non-contact-layer requirements for prescription medicines sold across the EU.

- May 2025: SCHOTT Pharma’s new borosilicate glass furnace in Lukácsháza, Hungary, entered operation, supplying an additional 500 million moulded vials and syringes per year to European biologics producers.

- February 2025: Gerresheimer, SCHOTT Pharma and Stevanato Group released the first harmonized specification for Type I ready-to-fill cartridges, enabling biosimilar manufacturers to dual-source components without revalidation.

- January 2025: BSP Pharmaceuticals commenced commercial output at its ISO 13408-certified aseptic fill-finish plant in Latina, Italy, adding 400 million ready-to-fill vials to the region’s annual capacity.

Europe Pharmaceutical Packaging Market Report Scope

The Europe Pharmaceutical Packaging Market Report is Segmented by Material Type (Plastic, Glass, Paper and Paperboard, Metal/Foil, Biopolymers and Composite Materials), Packaging Type (Primary Packaging, Secondary Packaging, Tertiary Packaging), Technology (Conventional, Aseptic and Sterile, Smart and Connected (NFC/RFID), Anti-counterfeit / Serialisation, Sustainable / Recyclable Solutions, Child-Resistant and Tamper-Evident Solutions), End User (Pharmaceutical Manufacturers, Specialty/Biotech Firms, Contract Manufacturing and Packaging Organizations, Hospitals and Clinics), and Country (United Kingdom, Germany, France, Spain, Italy, Poland, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Plastic |

| Glass |

| Paper and Paperboard |

| Metal/Foil |

| Biopolymers and Composite Materials |

By Packaging Type

| Primary Packaging | Bottles |

| Blister Packs | |

| Pre-fillable Syringes | |

| Vials and Ampoules | |

| IV Containers | |

| Inhalers | |

| Other Primary Packagings | |

| Secondary Packaging | Folding Cartons |

| Labels and Inserts | |

| Bags and Pouches | |

| Trays | |

| Other Secondary Packagings | |

| Tertiary Packaging | Corrugated Shippers |

| Pallets | |

| Other Tertiary Packagings |

By Technology

| Conventional |

| Aseptic and Sterile |

| Smart and Connected (NFC/RFID) |

| Anti-counterfeit / Serialisation |

| Sustainable / Recyclable Solutions |

| Child-Resistant and Tamper-Evident Solutions |

By End User

| Pharmaceutical Manufacturers |

| Specialty/Biotech Firms |

| Contract Manufacturing and Packaging Organizations |

| Hospitals and Clinics |

By Country

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| Poland |

| Rest of Europe |

| By Material Type | Plastic | |

| Glass | ||

| Paper and Paperboard | ||

| Metal/Foil | ||

| Biopolymers and Composite Materials | ||

| By Packaging Type | Primary Packaging | Bottles |

| Blister Packs | ||

| Pre-fillable Syringes | ||

| Vials and Ampoules | ||

| IV Containers | ||

| Inhalers | ||

| Other Primary Packagings | ||

| Secondary Packaging | Folding Cartons | |

| Labels and Inserts | ||

| Bags and Pouches | ||

| Trays | ||

| Other Secondary Packagings | ||

| Tertiary Packaging | Corrugated Shippers | |

| Pallets | ||

| Other Tertiary Packagings | ||

| By Technology | Conventional | |

| Aseptic and Sterile | ||

| Smart and Connected (NFC/RFID) | ||

| Anti-counterfeit / Serialisation | ||

| Sustainable / Recyclable Solutions | ||

| Child-Resistant and Tamper-Evident Solutions | ||

| By End User | Pharmaceutical Manufacturers | |

| Specialty/Biotech Firms | ||

| Contract Manufacturing and Packaging Organizations | ||

| Hospitals and Clinics | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Poland | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the 2026 revenue base for pharmaceutical packaging in Europe?

Spending stands at USD 46.46 billion in 2026.

How quickly is European pharmaceutical packaging spending projected to expand?

Expenditure is forecast to grow at a 5.61% CAGR through 2031.

Which technology area shows the fastest expansion pace?

Smart and connected formats are advancing at a 7.55% CAGR.

Which European country exhibits the strongest growth outlook?

Poland is projected to achieve an 7.72% CAGR between 2026 and 2031.

Which material currently captures the largest share of packaging spend?

Plastics command 52.03% of 2025 revenue, leading all materials.

What regulation is most influencing material selection decisions?

The EU Packaging and Packaging Waste Regulation drives adoption of recycled-content plastics and biopolymers.

Page last updated on: