Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

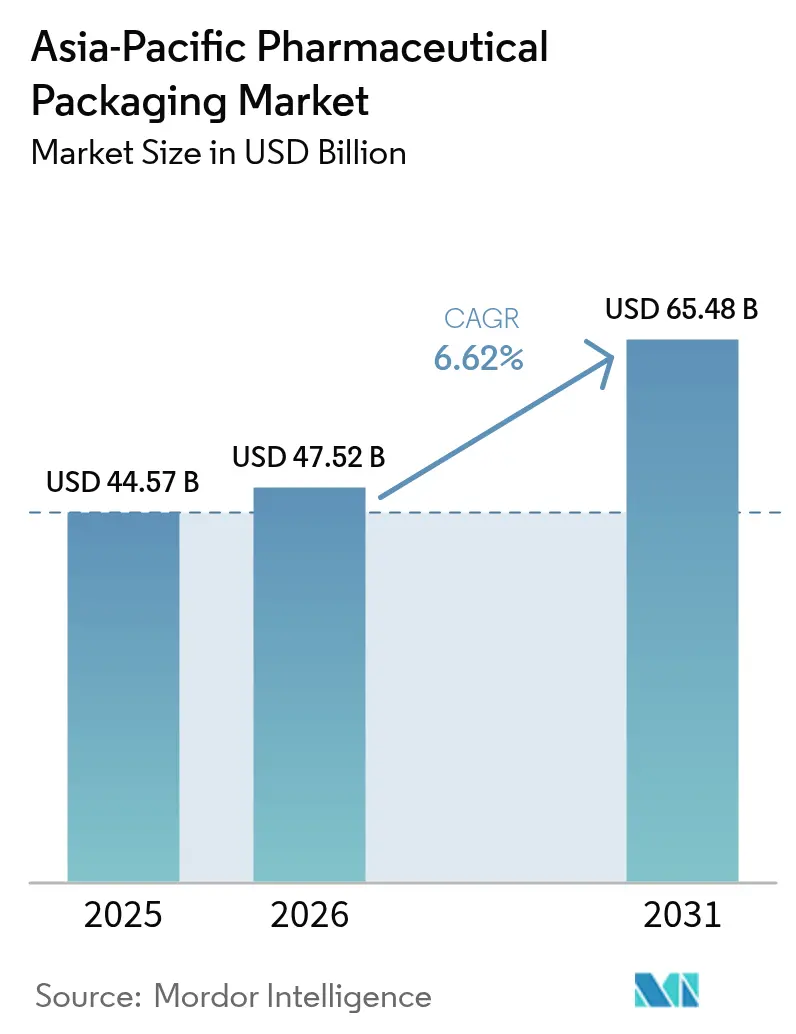

| Base Year Market Size (2025) | USD 44.57 Billion |

| Market Size (2026) | USD 47.52 Billion |

| Market Size (2031) | USD 65.48 Billion |

| Growth Rate (2026 - 2031) | 6.62% CAGR |

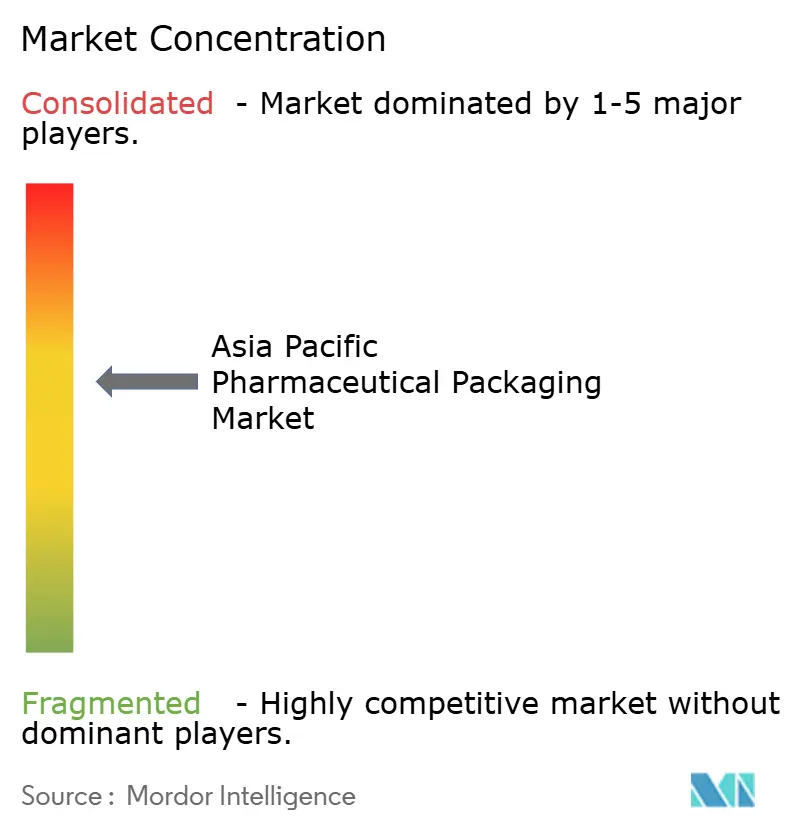

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Pharmaceutical Packaging Market Analysis by Mordor Intelligence

The Asia-Pacific pharmaceutical packaging market size is expected to grow from USD 44.57 billion in 2025 to USD 47.52 billion in 2026 and is forecast to reach USD 65.48 billion by 2031 at 6.62% CAGR over 2026-2031. The region’s scale as a contract-manufacturing hub, the rapid expansion of biologics, and tighter alignment with ICH Q3D and serialization mandates together underpin resilient demand for compliant, high-integrity packaging. Converter profitability is being tested by resin and alumina cost swings, yet the pivot toward value-added vials, pre-filled syringes, and ultra-barrier blisters is supporting margin recovery. National procurement programs that favor unit-dose packs, along with expanding health-coverage schemes, keep volumes high in cost-sensitive markets while premium formats for cell and gene therapies propel revenue growth in advanced economies. Intensifying regulatory scrutiny is shortening supplier lists, channeling orders to converters that can certify ISO 15378 lines and prove real-time environmental monitoring. Across every material and format, sustainability criteria are tightening, prompting shifts to cyclic olefins, thinner-gauge aluminum, and recycled PET, trends that will keep the Asia-Pacific pharmaceutical packaging market in a phase of ongoing capital reinvestment and technology upgrades.

Key Report Takeaways

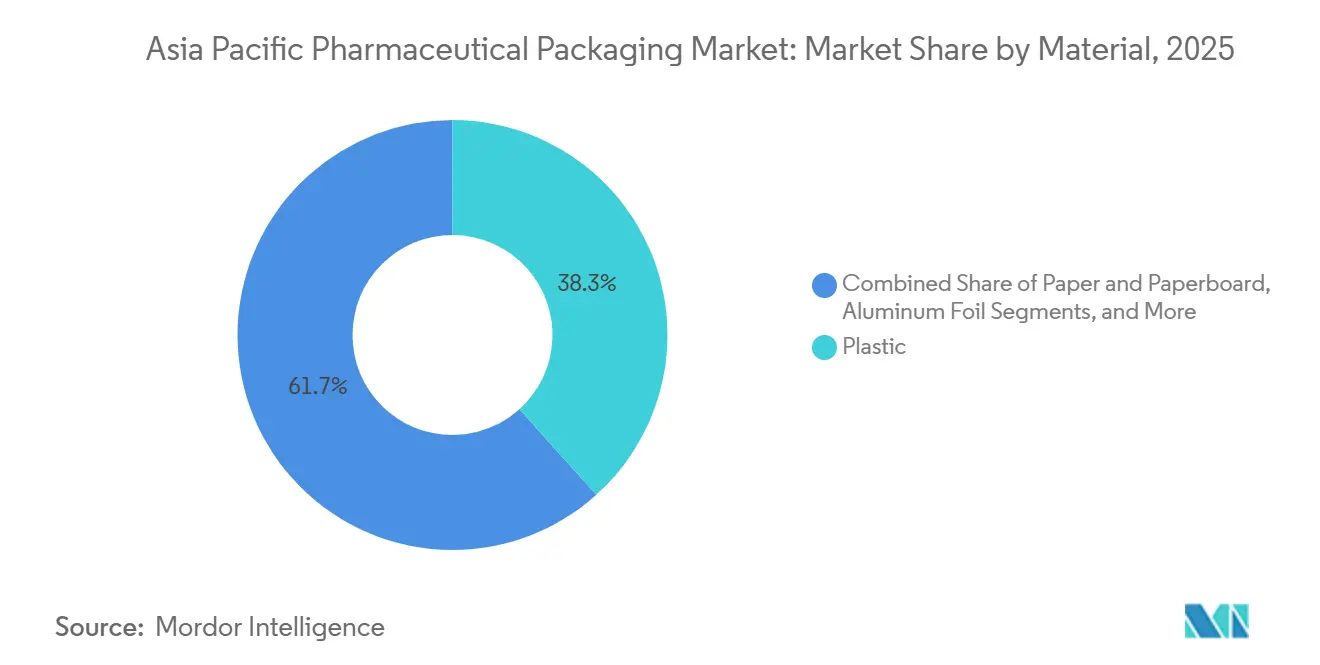

- By material, plastic led with 38.34% of the Asia-Pacific pharmaceutical packaging market share in 2025, while bioplastics and cyclic olefin copolymers are projected to expand at a 7.59% CAGR through 2031.

- By type, blister packs accounted for 32.57% of revenue in 2025, whereas vials are forecast to grow at an 8.32% CAGR from 2026-2031.

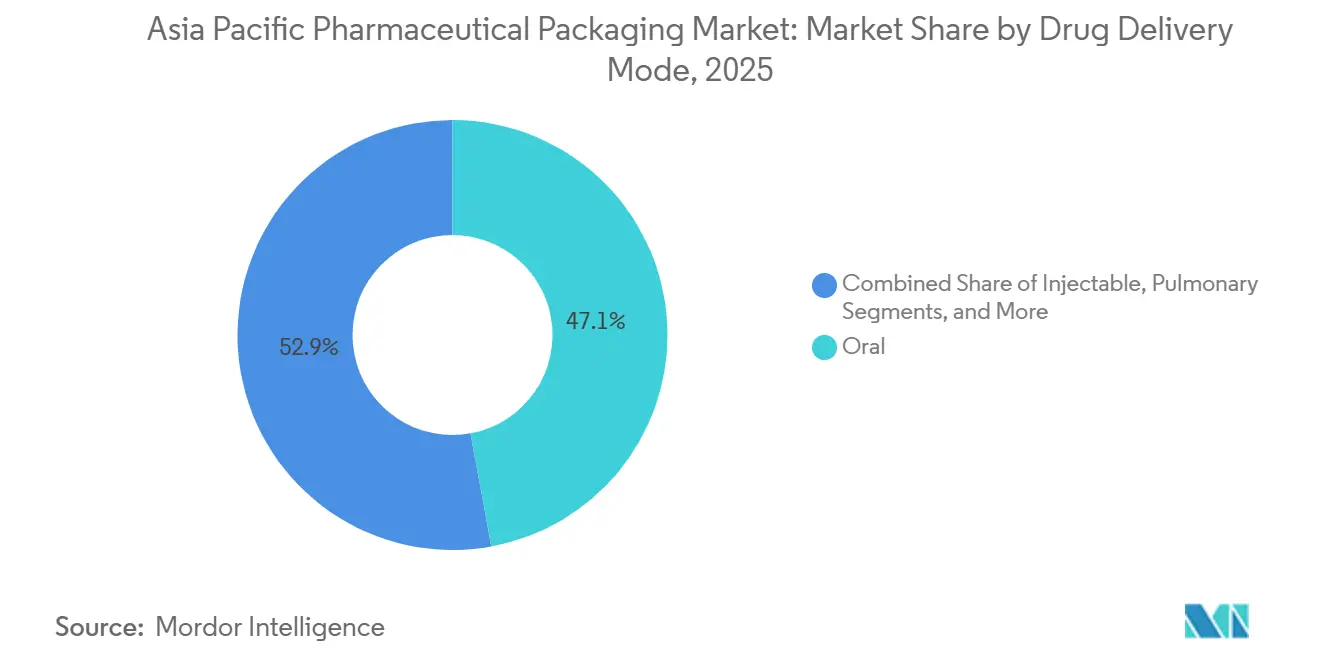

- By drug-delivery mode, oral delivery modes accounted for 47.12% revenue in 2025, and injectable formats are poised to grow at a 7.54% CAGR during the forecast period.

- By country, China accounted for 36.83% of regional revenue in 2025, yet India is expected to post the fastest growth at a 7.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Pharmaceutical Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Biologics Pipeline Demanding High-Integrity Primary Packaging | +1.8% | China, India, South Korea, Singapore | Medium Term (2–4 Years) |

| Accelerated Fill-Finish Outsourcing to Asia Driving Contract Packaging Volumes | +1.5% | India, China, South Korea | Short Term (≤ 2 Years) |

| Government Bulk-Procurement Schemes Favoring Cost-Efficient Blister Formats | +1.2% | India, Indonesia, Philippines, Vietnam | Short Term (≤ 2 Years) |

| Serialization Regulations Boosting Track-and-Trace Packaging | +1.0% | China, India, Japan, South Korea, Thailand, Malaysia | Medium Term (2–4 Years) |

| Surge in Low-Dose High-Potency OSD Drugs Spurring Adoption of High-Barrier PTP Foils | +0.7% | Japan, South Korea, Australia, Singapore | Medium Term (2–4 Years) |

| Growth of Temperature-Sensitive Cell-and-Gene Therapies Creating Demand for Cryo-Compatible Vials | +0.5% | Japan, South Korea, Australia, Singapore | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Rising Biologics Pipeline Demanding High-Integrity Primary Packaging

Biologics capacity additions across Asia-Pacific have triggered unprecedented demand for vials and pre-filled syringes that combine low extractables, dimensional consistency, and compatibility with lyophilization cycles. Contract manufacturers align with originator expectations by insisting on ISO 15378-certified lines and validated ICH Q3D dossiers, tilting procurement toward incumbents able to produce data packs within 18-24 months. Polymer vials, such as cyclic olefin formats, are gaining share where protein adsorption or delamination risk is unacceptable, reshaping the materials mix of the Asia-Pacific pharmaceutical packaging market.[1]Daikyo Seiko, “Crystal Zenith Cyclic Olefin Polymer Vials Receive Regulatory Approvals,” daikyo-seiko.com The result is a virtuous cycle in which converters that invest early in polymer capacity secure multi-year supply agreements, locking in volumes before furnace-based glass capacity can catch up. As pipeline molecules move from clinical to commercial scale, regional demand for high-integrity containers is set to rise steadily through the decade.

Accelerated Fill-Finish Outsourcing to Asia Driving Contract Packaging Volumes

Multinational drug makers have stepped up fill-finish transfers to India, China, and South Korea, attracted by cost savings and local market-access incentives. Each new suite energizes upstream demand for primary and secondary packs, typically bundling vials, stoppers, cartons, and serialization labels under a single master agreement. This dynamic reinforces consolidation, because contract manufacturers favor suppliers that can guarantee component compatibility and single-lot deliveries at cycle-time levels consistent with biologics turnarounds. In the Asia-Pacific pharmaceutical packaging market, the outsourcing wave translates into higher unit throughput and stricter service-level requirements, accelerating automation and the deployment of vision inspection across converter footprints. Suppliers unable to finance these upgrades risk displacement as large CDMOs streamline vendor bases to two or three qualified partners.

Government Bulk-Procurement Schemes Favoring Cost-Efficient Blister Formats

National health programs have made cost-efficient blisters indispensable in several populous economies. In India, mandatory unit-dose packaging for generics channeled billions of tablets through aluminum-based formats that help curb counterfeiting and dosage errors. Indonesia and Vietnam mirror this policy trajectory, cementing a baseline of blister demand even as higher-value parenterals grow. Converters competing in tenders must deliver landed cavity costs below pre-set thresholds, forcing relentless optimization of gauge thickness, forming pressure, and supply-chain localization. Although the per-unit margin is thin, scale volumes generate stable cash flows to fund the capital upgrades required for premium injectable formats, thereby knitting together the low- and high-end tiers of the Asia-Pacific pharmaceutical packaging market.

Serialization Regulations Boosting Track-And-Trace Packaging

China, India, and Japan are phasing in unit-level serialization, which is driving upgrades in printing, vision, and aggregation capabilities.[2]China Daily, “China Drug Administration Law Serialization Requirements,” chinadaily.com.cn Pharmaceutical firms are retrofitting more than 1,000 packaging lines, and each retrofit, in turn, drives demand for smart labels, tamper-evident closures, and data-integrated cartons. Mid-sized converters face capital hurdles in adopting compliant systems, prompting an uptick in mergers and facility divestitures. For well-capitalized suppliers, serialization legislation opens a recurring revenue stream in software service and maintenance, reinforcing their competitive moat inside the Asia-Pacific pharmaceutical packaging market. As deadlines near, serialized volume will surge, locking in technology standards that favor converters with global EPCIS connectivity and on-site validation expertise.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile resin and alumina prices squeezing converter margins | -0.9% | China, India, Southeast Asia | Short term (≤ 2 years) |

| Stringent PVC phase-out policies in Japan and South Korea | -0.6% | Japan, South Korea | Medium term (2–4 years) |

| Port congestion and cold-chain bottlenecks slowing export shipments | -0.4% | China, Singapore, South Korea | Short term (≤ 2 years) |

| Limited regional supply of pharma-grade borosilicate tubing | -0.3% | Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Stringent PVC Phase-Out Policies in Japan and South Korea

Environmental regulations in Japan and South Korea require the elimination of PVC in blisters by 2027-2028.[3]Ministry of Economy, Trade and Industry Japan, “PVC Phase-Out Regulations for Pharmaceutical Packaging,” meti.go.jp Converters must re-engineer tooling because polypropylene and polyester films require new sealing windows and cavity geometries, leading to validation expenses that can reach half a million U.S. dollars per SKU. Drug formulators may need moisture scavengers, which can delay launches and complicate stability programs. Collectively, tool-change expenses, validation timelines, and material cost premiums weigh on growth potential in two high-value markets, restraining the regional CAGR of the Asia-Pacific pharmaceutical packaging market until compliant capacities settle.

Volatile Resin and Alumina Prices Squeezing Converter Margins

Feedstock volatility remains the most immediate profitability risk.[4]ICIS Chemical Business, “PET Resin Prices in Asia Pacific Show Volatility in 2025,” icis.com Polyethylene terephthalate and alumina both posted double-digit price spikes during early 2025, eroding the thin 12-16% gross margins typical among small converters. Pharmaceutical customers rarely allow mid-contract pass-throughs, so exposure shifts upstream where hedging capacity is limited. A string of insolvencies among Indian and Chinese suppliers illustrates how quickly cost shocks can reshape the Asia-Pacific pharmaceutical packaging market. Larger players weather volatility by leveraging forward contracts and multisource strategies, whereas sub-scale operators increasingly exit or are acquired, accelerating consolidation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Polymer Migration Reshapes High-Value Applications

Bioplastics and cyclic olefin copolymers, while small today, are the fastest-growing slice of the Asia-Pacific pharmaceutical packaging market size and are forecast to climb at 7.59% CAGR as biologics sponsors pivot to low-extractable containers. Glass remains dominant for long-shelf-life injectables, with two suppliers jointly holding a majority of Asia-Pacific pharmaceutical packaging market share in Type I borosilicate. Aluminum foil, pressured by input cost volatility, is simultaneously moving to 20 micron gauges and tighter pinhole specifications, raising the qualification bar.

Converters see a dual-track future. Premium resin-based vials and cyclic olefin syringes capture value where biologic stability demands trump cost. Standard PET bottles and HDPE closures still anchor oral formulations but face extended producer-responsibility levies in Japan and South Korea. Paperboard cartons, commoditized yet essential, are streamlining dimensions for line-speed efficiency. The outcome is a material landscape where technical barriers, not volume alone, decide profitability.

By Type: Injectable Containers Lead Growth Trajectory

Vials headline the growth story, advancing at an 8.32% CAGR as GLP-1s, mRNA vaccines, and monoclonal antibodies scale. Blister packs held a 32.57% share in 2025, the largest among all formats, supported by unit-dose mandates in public procurement programs.

Plastic bottles and conventional syringes face incremental erosion as healthcare systems tighten adherence tracking and shift to unit-dose or ready-to-inject therapies. Ampoules retreat further into specialty emergency settings, while IV bags and stick packs post steady low-single-digit growth tied to hospital infrastructure spending. Caps and closures evolve fastest, adding child-resistance, senior-friendliness, and smart-label interfaces without compromising torque or seal integrity.

By Drug Delivery Mode: Injectable and Specialty Routes Accelerate

Injectables are set to be the high-velocity engine, growing 7.54% annually, powered by biosimilar launches and cell-therapy pipelines. Oral formats still outweigh all others in absolute terms, yet their share of Asia-Pacific pharmaceutical packaging market revenue is flattening as R&D budgets migrate toward biologics.

Pulmonary devices return to the spotlight following the approval of inhaled insulin, creating fresh demand for metered-dose inhaler valves and aluminum canisters. Topical and transdermal systems ride demographic aging trends, while ophthalmic products push packaging innovation with preservative-free multi-dose bottles that integrate membrane filters. All niche modes demand precise dimensional tolerances and contamination-control capabilities beyond what is common in mass-market OSD production.

Geography Analysis

China dominates with 36.83% of regional value, supported by the world’s largest API base and a growing biologics sector that keeps domestic demand robust. Continuous alignment with NMPA and ICH protocols tightens quality expectations, nudging smaller converters toward partnerships or exits. Furnace additions in Shandong are expanding glass supply, yet capacity still lags near-term biologics needs.

India is on a 7.71% CAGR trajectory through 2031 as its contract manufacturing and bulk procurement drivers converge. State tenders lock in volumes for local blister converters, while international CDMOs fuel high-spec vial demand. Regulatory rollouts, such as Track and Trace, create an ecosystem in which packaging, serialization, and data management converge, reinforcing the centrality of the Asia-Pacific pharmaceutical packaging market to global supply resiliency.

Japan and South Korea, which together account for about one-sixth of regional turnover, emphasize premium features and environmental compliance, creating disproportionate demand for cyclic olefins, polypropylene blister packs, and child-resistant closures. Australia and emerging ASEAN economies round out the map, with universal health coverage expansions and inward foreign direct investment shaping steady mid-single-digit advances in secondary and tertiary packaging demand.

Competitive Landscape

The Asia-Pacific pharmaceutical packaging market is moderately fragmented: the five largest suppliers account for roughly 42% of combined revenue. Scale players pursue vertical integration, acquiring fill-finish or label assets to deliver turnkey offerings. Recent moves include capacity expansions for vials in India and glass tubing furnaces in China, underscoring capital intensity as a competitive differentiator.

Technology adoption now defines market leadership. Firms introducing AI-assisted vision inspection report defect rates under 10 ppm, winning multiyear contracts from biologics makers that equate defect detection with patient safety and brand equity. Smaller converters counter by specializing in sustainability, recycled PET, or fiber-based blisters, carving out niches where larger rivals hesitate.

Mergers and private-equity rollups accelerate as serialization deadlines, PVC bans, and feedstock volatility raise the bar for compliance investment. Converters that cannot fund upgrades become acquisition targets, hastening consolidation and nudging the Asia-Pacific pharmaceutical packaging market toward higher concentration over the forecast window.

Asia-Pacific Pharmaceutical Packaging Industry Leaders

Amcor plc

Gerresheimer AG

Schott AG

West Pharmaceutical Services Inc

CCL Industries Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Gerresheimer announced a EUR 180 million (USD 195 million) expansion at Trivandrum, India, adding 1.2 billion vials of annual capacity with serialization-ready lines.

- January 2026: Schott commissioned a 3,500-metric-ton Type I borosilicate furnace in Jinyun, China, easing regional tubing constraints.

- December 2025: West Pharmaceutical Services sealed a USD 120 million, five-year supply pact with Samsung Biologics for cyclic olefin vials and FluroTec closures.

- November 2025: Amcor acquired a Rayong, Thailand, blister facility, boosting capacity by 2.4 billion cavities to serve Southeast Asian generics.

- October 2025: Nipro committed JPY 12 billion (USD 80 million) to expand pre-filled syringe output in Odate, Japan, targeting GLP-1 injectables.

Asia-Pacific Pharmaceutical Packaging Market Report Scope

The Asia-Pacific Pharmaceutical Packaging Market Report is Segmented by Material (Plastic, Paper and Paperboard, Glass, Aluminum Foil, Other Materials), Type (Ampoules, Blister Packs, Plastic Bottles, Syringes, Vials, IV Fluids, Stick Packs, Pouches and Sachets, Caps and Closures), Drug Delivery Mode (Oral, Injectable, Pulmonary, Topical and Transdermal, Other Modes), and Geography (China, India, Japan, South Korea, Australia, Rest of Asia-Pacific). Market Forecasts are Provided in Terms of Value (USD).

By Material

| Plastic |

| Paper and Paperboard |

| Glass |

| Aluminum Foil |

| Other Materials (Bioplastics, Cyclic Olefins) |

By Type

| Ampoules |

| Blister Packs |

| Plastic Bottles |

| Syringes |

| Vials |

| IV Fluids |

| Stick Packs |

| Pouches and Sachets |

| Caps and Closures |

By Drug Delivery Mode

| Oral |

| Injectable |

| Pulmonary |

| Topical and Transdermal |

| Other Modes |

By Country

| China |

| India |

| Japan |

| South Korea |

| Australia |

| Rest of Asia-Pacific |

| By Material | Plastic |

| Paper and Paperboard | |

| Glass | |

| Aluminum Foil | |

| Other Materials (Bioplastics, Cyclic Olefins) | |

| By Type | Ampoules |

| Blister Packs | |

| Plastic Bottles | |

| Syringes | |

| Vials | |

| IV Fluids | |

| Stick Packs | |

| Pouches and Sachets | |

| Caps and Closures | |

| By Drug Delivery Mode | Oral |

| Injectable | |

| Pulmonary | |

| Topical and Transdermal | |

| Other Modes | |

| By Country | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How fast is injectable packaging demand growing in Asia-Pacific?

Injectable formats are projected to expand at a 6.62% CAGR between 2026-2031, the quickest among all delivery routes.

Which country will post the highest growth in regional pharmaceutical packaging?

India is forecast to rise at a 7.71% CAGR through 2031 on the back of contract manufacturing and bulk-procurement momentum.

What share did blister packs hold in 2025?

Blister packs captured 32.57% of Asia Pacific pharmaceutical packaging market revenue in 2025.

Why are cyclic olefin vials gaining popularity?

They offer low extractables, reduced protein adsorption, and compatibility with sensitive biologics, supporting a 7.59% CAGR in bioplastics and cyclic olefins.

How concentrated is supplier power in the region?

The top five converters controlled about 42% of revenue in 2025, indicating moderate concentration with ongoing consolidation.

Page last updated on: