Market Overview

| Study Period | 2020 - 2031 |

|---|---|

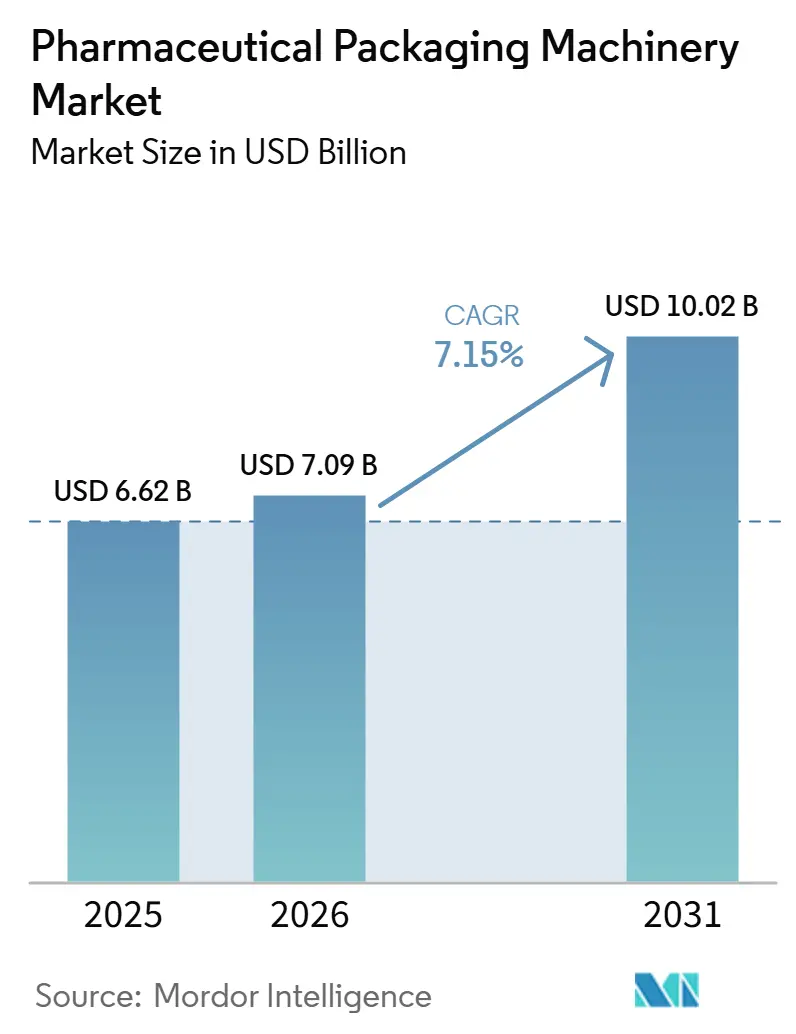

| Market Size (2026) | USD 7.09 Billion |

| Market Size (2031) | USD 10.02 Billion |

| Growth Rate (2026 - 2031) | 7.15% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical Packaging Machinery Market Analysis by Mordor Intelligence

The pharmaceutical packaging machinery market size was valued at USD 6.62 billion in 2025 and estimated to grow from USD 7.09 billion in 2026 to reach USD 10.02 billion by 2031, at a CAGR of 7.15% during the forecast period (2026-2031). Biologics and injectable therapies dominate late-stage pipelines, and their aseptic-fill needs have accelerated capital spending on precision equipment that manual or semi-automatic systems cannot match. Regulatory deadlines set by the U.S. Drug Supply Chain Security Act and the European Union Falsified Medicines Directive have moved packaging equipment from discretionary upgrades to non-negotiable compliance assets, intensifying demand for integrated filling, sealing, and aggregation capabilities. The cost of energy in Europe has doubled since 2021, prompting purchasing decisions to shift toward machines that reduce electricity consumption as part of overall equipment effectiveness strategies. Incumbent suppliers with modular, digitally connected platforms are leveraging service contracts and predictive-maintenance analytics to deepen customer stickiness and raise switching costs.

Key Report Takeaways

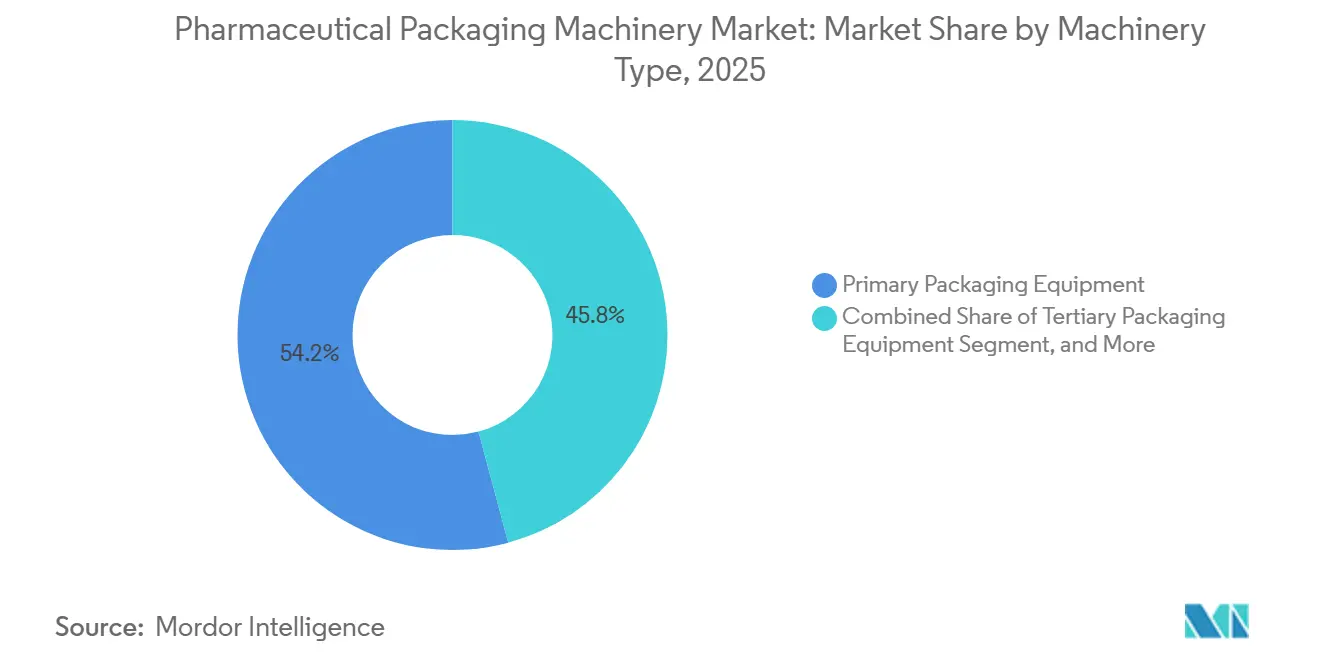

- By machinery type, primary packaging equipment led the pharmaceutical packaging machinery market, accounting for 54.18% of the market share in 2025. Meanwhile, secondary packaging equipment is forecast to expand at an 8.05% CAGR through 2031.

- By automation level, automatic systems captured 64.12% of the pharmaceutical packaging machinery market share in 2025 and are projected to advance at an 8.55% CAGR through 2031.

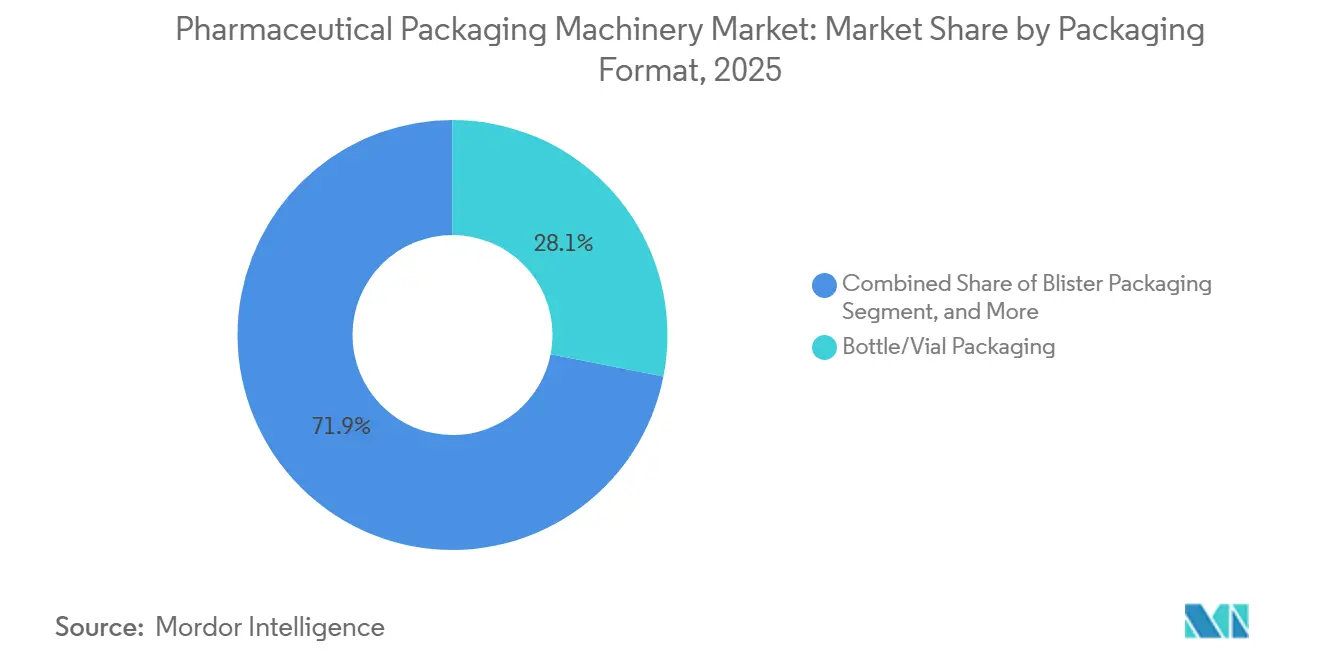

- By packaging format, bottle/vial packaging captured 28.10% of the pharmaceutical packaging machinery market share in 2025; cartoning and case packing is forecast to expand at an 8.90% CAGR through 2031.

- By application, parenterals held 29.30% of the pharmaceutical packaging machinery market size in 2025, whereas liquids are poised for the fastest expansion at a 9.05% CAGR.

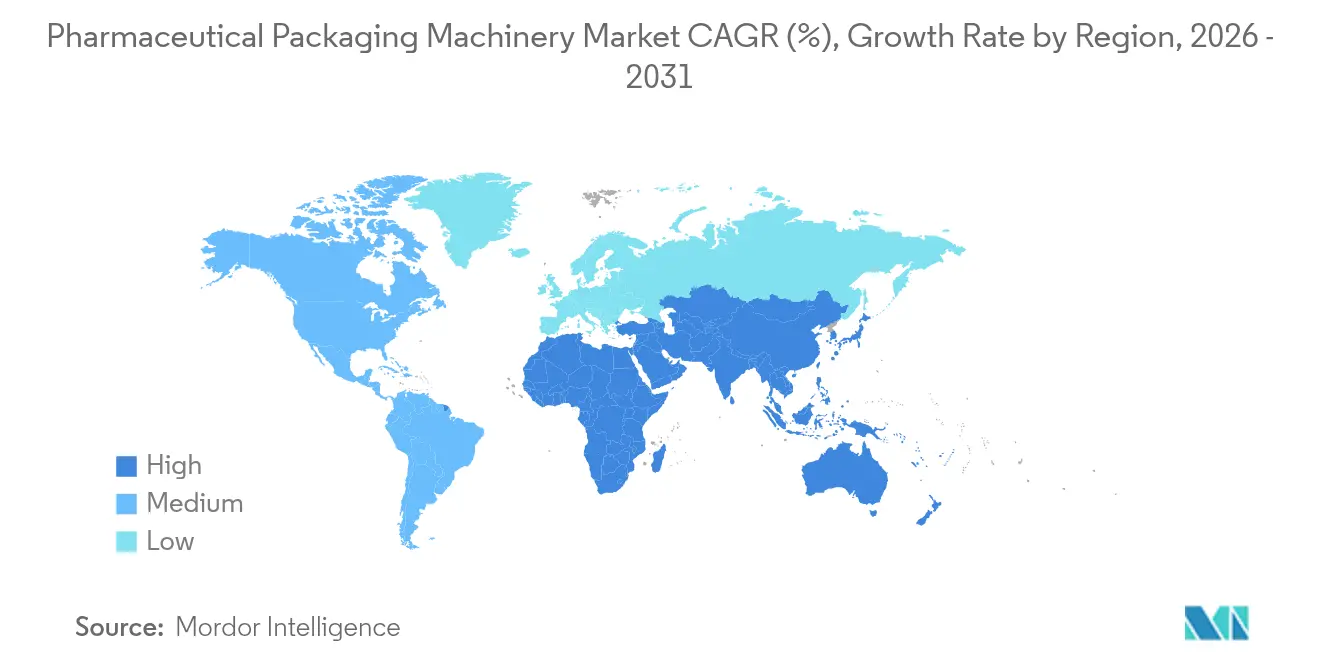

- By geography, North America retained 39.10% of the pharmaceutical packaging machinery market share in 2025; however, the Asia-Pacific region is expected to register a 9.30% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Pharmaceutical Packaging Machinery Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Serialization and Track and Trace Regulations | +1.8% | North America and Europe lead, global spill-over | Medium term (2-4 years) |

| Rapid Growth of Biologics and Injectable Drugs | +1.5% | North America and Europe core, Asia-Pacific manufacturing spill-over | Long term (≥4 years) |

| Increasing Demand for Automation and Industry 4.0 Integration | +1.3% | Global, highest adoption in North America and Western Europe | Medium term (2-4 years) |

| Rise of Personalized Small-Batch Manufacturing Workflows | +0.9% | North America and Europe, early Asia-Pacific uptake | Long term (≥4 years) |

| Reshoring and Nearshoring of Pharma Supply Chains | +0.7% | North America and Europe primary | Short term (≤2 years) |

| Energy-Efficient Machinery as a Procurement Criterion | +0.6% | Europe primary, global emergence | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Serialization and Track and Trace Regulations

Drug traceability laws require unit-level identifiers and aggregation from blister cavity to pallet, converting packaging machinery into essential compliance infrastructure. The U.S. DSCSA mandated fully interoperable traceability by November 2023, and by late 2024, more than 70% of domestic sites had installed serialization modules; however, case-level aggregation gaps persist.[1]European Medicines Agency, “Falsified Medicines Directive,” ema.europa.eu Europe’s directive enforces unique identifiers and tamper-evident closures, prompting retrofit cycles across legacy blister and bottle lines. China extended its deadline to 2025 for import drugs, spurring contract manufacturers that serve Western markets to fast-track equipment purchases. Supplier software now ships with region-specific compliance templates; however, this localization increases the total cost of ownership and validation timelines in the pharmaceutical packaging machinery market. ISO 15378 has become a de facto tender prerequisite, narrowing vendor pools to firms that can align equipment files with Good Manufacturing Practice records.

Rapid Growth of Biologics and Injectable Drugs

Eight of the top 10 therapies sold in 2024 were biologics packaged in vials, syringes, or autoinjectors that require ISO Class 5 environments and precise glass handling. The FDA issued 47 warning letters in 2024 for particulate contamination, reinforcing the zero-defect mandate and driving the installation of automated visual inspection cameras.[2]U.S. Food and Drug Administration, “Drug Supply Chain Security Act,” fda.gov Small batch sizes of gene and cell therapies make high-speed legacy fillers uneconomic, so modular machines capable of 30-minute format changes are preferred. The European Medicines Agency cleared 92 biologics in 2024, each requiring dedicated packaging validation runs that many firms outsource to flexible contract development and manufacturing partners. Suppliers respond with servo-driven dosing pumps and single-use flow paths that maintain sterility and shorten cleaning cycles.

Increasing Demand for Automation and Industry 4.0 Integration

Predictive analytics and electronic batch records are transitioning from pilot projects to purchasing criteria. Connected blister machines analyze sealing-plate temperature, foil tension, and feeder vibration to flag deviations before rejects occur, cutting waste by up to 30% in early adopters.[3]Syntegon Technology, “Connected Packaging,” syntegon.com FDA guidance published in 2024 explicitly favors electronic data integrity, accelerating moves away from paper lot travelers. Cloud-based genealogy modules store every container’s lineage, supporting remote audits but also creating cybersecurity attack surfaces; CISA advisories highlight default passwords and unpatched firmware as common vulnerabilities. Suppliers now bundle penetration testing and firmware patching into service contracts to mitigate risks of breaches in the pharmaceutical packaging machinery market.

Rise of Personalized Small-Batch Manufacturing Workflows

CAR-T and autologous therapies need “batch-of-one” equipment that fills, labels, and serializes a single patient’s dose, sometimes in hospital cleanrooms. The FDA cleared 16 cell and gene products in 2024, each shipped in cryogenic vials that require tamper-evident secondary packaging with temperature sensors. Suppliers have launched compact fillers that integrate robotics and barcode readers within two-square-meter footprints, enabling decentralized production near treatment centers. Becton Dickinson debuted a modular platform in 2024 specifically for point-of-care suites, reducing logistics costs associated with cold-chain transport. Platform economics shift from high volume to high mix, prompting suppliers to recoup R&D through software licenses and service bundles rather than physical unit sales.

Restraints Impact Analysis of Pharmaceutical Packaging Machinery Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Expenditure for Advanced Machinery | -1.2% | Global, acute in emerging markets | Medium term (2-4 years) |

| Stringent Validation and Compliance Complexity | -0.9% | Global, heaviest in North America and Europe | Long term (≥4 years) |

| Semiconductor and Servo Drive Shortages | -0.5% | Global residual effects | Short term (≤2 years) |

| Limited Skilled Mechatronics Talent | -0.7% | Asia-Pacific and South America primary | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for Advanced Machinery

Aseptic lines incorporating isolators, serialization modules, and in-line particle inspection can top USD 8 million, locking many generic manufacturers into aging assets. Forty percent of plants in emerging regions operate equipment that is more than 15 years old, compared with 12% in North America, widening a compliance gap that hinders export approvals. Leasing models have emerged, yet data-sharing clauses raise concerns about intellectual property. Public lenders, such as the European Investment Bank, offered EUR 500 million (USD 565 million) in loans in 2024 to support Eastern European upgrades, signaling that external financing is essential where private credit costs remain elevated.

Stringent Validation and Compliance Complexity

Installation, operational, and performance qualification can span 12 months and cost USD 1.5 million per line, tying up cash and delaying the commercial launch. FDA 2024 guidance emphasizes continuous process verification, so manufacturers must store years of statistical control data rather than completing three-batch studies. In 2024, EMA inspectors rejected 18% of protocols due to risk-assessment gaps, necessitating costly retesting. Suppliers counter by shipping pre-validated test scripts, but regulators still demand jurisdiction-specific evidence, prolonging approval cycles for multi-market launches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Pharmaceutical Packaging Machinery Market Segment Analysis

By Machinery Type:

Rising Traction for Downstream IntegrationPrimary equipment accounted for 54.18% of the pharmaceutical packaging machinery market in 2025, underscoring its mission-critical role in ensuring container integrity and sterility. However, secondary lines will expand at a faster rate of 8.05% CAGR because case- and pallet-level aggregation has become mandatory for global shipments. The pharmaceutical packaging machinery market size for secondary equipment is forecast to reach USD 3.44 billion by 2031, driven by retrofits that incorporate vision-inspection cameras and two-dimensional code printers. Antares Vision logged a 22% order spike for serialization modules in the Asia-Pacific region, revealing how export-oriented generic manufacturers prioritize downstream upgrades over full-line replacements.

Labeling and serialization machines form the fastest-moving niche, aided by the pharmaceutical packaging machinery market share gains of high-speed inkjet and laser coders operating at more than 400 packs per minute. Blister platforms are experiencing renewed investment as companies shift from bottles to unit-dose packs to enhance adherence, while cartoners are moving up the value chain by integrating variable data printing and tamper-evident sealing. Uhlmann’s 2024 modular cartoner allows for seamless switching between tuck-end and glue-seal formats without the need for tools, aligning with the high SKU proliferation of specialty drugs.

By Automation Level:

Automatic Lines Command a PremiumAutomatic systems accounted for 64.12% of installations in 2025, reflecting wage inflation and the precision needed for zero-defect packaging. The pharmaceutical packaging machinery market growth for automatic equipment is driven by collaborative robots that enable rapid changeovers without interrupting production lines. In India and China, manufacturing wages increased by 8% annually from 2019 to 2024, narrowing the labor arbitrage that once justified manual operations.

Semi-automatic machines still appeal to clinical-trial sites and emerging-market factories where product diversity outweighs throughput. Romaco reports that 35% of its emerging-market sales are semi-automatic units, serving as stepping-stones toward full automation. Marchesini’s collaborative cartoning cells, deployed in 2024, slash changeover times from 45 to 12 minutes, demonstrating how hybrid human-robot cells bridge capability gaps until skilled mechatronics labor pools mature.

By Packaging Format:

Cartoning and Aggregation Lead GrowthBottle and vial platforms held 28.10% market share in 2025, as oral solids and injectables still account for the bulk of unit volume. Cartoning and case-packing modules, however, are expected to post a 8.90% CAGR to 2031, as e-commerce channels and cold-chain shipments require tamper-evident cartons and machine-readable codes. The pharmaceutical packaging machinery market share for cartoning systems is expanding the fastest in the Asia-Pacific region, where contract manufacturers scaling biologics production require flexible carton dimensions for combination kits.

Blister machinery incorporates leak detection and 100% vision checks, raising capital costs by 25% yet reducing costly recalls. MULTIVAC’s 2024 adjustable cartoner automatically adapts to barcode-scanned dimensions, a feature designed for personalized therapies with variable dosing. Prefilled syringes and autoinjectors are driving a secondary investment wave in vial handling lines that are capable of gentle glass manipulation, while stick-pack lines are entering growth mode for pediatric nutrients and geriatric supplements that benefit from dose customization.

By Application:

Parenterals Drive Precision, Liquids Lead GrowthParenterals accounted for 29.30% of the pharmaceutical packaging machinery market size in 2025, reflecting high-margin biologics that demand isolators and barrier systems. Liquids are expected to expand at a 9.05% CAGR due to pediatric and geriatric preferences for easy-to-swallow formats. Oral liquid lines are migrating from glass to lightweight plastic bottles with child-resistant caps, pushing suppliers to engineer dual-material filling valves that prevent extractables.

Injectable approvals increased 12% year-over-year to 55 in 2024, requiring ISO Class 5 filling lines with a cost of USD 4 million or more. ACG’s 2024 viscous-liquid filler targets suspensions that challenge traditional pumps. Solid-dose blister machines add cavity-level serialization to deter opioid diversion, a capability regulators in Europe are evaluating for controlled substances.

Geography Analysis

North America Pharmaceutical Packaging Machinery Market

North America represents the largest regional base, accounting for 39.10% of 2025 revenue, thanks to DSCSA enforcement, reshoring incentives, and tax credits that subsidize capital outlays for sterile-fill projects in states such as North Carolina and Massachusetts. Investments in digital twins and energy monitoring aim to reduce commissioning time and operating expenses. Contract manufacturers in the United States are increasingly requiring turnkey solutions with validation documentation pre-aligned to FDA electronic record standards, thereby shortening the time to market.

APAC Pharmaceutical Packaging Machinery Market

The Asia-Pacific region exhibits the fastest trajectory, forecast at a 9.30% CAGR, driven by Indian and Chinese factories that seek to meet export specifications for the United States and the European Union. India shipped USD 27.9 billion in finished drugs in fiscal 2024, and this export dependency motivates firms to install European-grade serialization and vision systems. Chinese authorities have extended the serialization compliance deadline for imports to 2025, creating a short-term equipment procurement boom among export-oriented contract manufacturers.

Germany, Italy and Switzerland Pharmaceutical Packaging Machinery Market

Europe maintains a steady demand tied to replacement cycles rather than plant expansions. Manufacturers retrofit bottle, blister, and vial lines with aggregation cameras to comply with the EU directive’s full enforcement, which is expected to be reached in 2024, while energy-efficiency upgrades mitigate regionally high electricity costs. Germany, Italy, and Switzerland remain global engineering hubs, home to Syntegon, IMA, and Marchesini, which creates a dense service network that multinational drugmakers favor when sourcing equipment partners.

South America and MEA Pharmaceutical Packaging Machinery Market

South America and the Middle East, and Africa contribute smaller shares but offer targeted opportunities tied to domestic production policies. Brazil and Argentina introduced serialization regulations modeled after the DSCSA, stimulating the purchase of inkjet coders and case aggregators. Gulf Cooperation Council states are promoting local vaccine fill-finish plants under economic diversification frameworks, and suppliers who bundle training and validation support gain an early-mover advantage in these nascent markets.

Competitive Landscape

The top 10 suppliers controlled roughly 55% of 2024 revenue, yielding a moderately concentrated arena marked by specialization rather than pricing battles. No vendor exceeded a 12% share, so differentiation stems from technical service, modular platforms, and digital value-add. Syntegon, IMA, and Marchesini emphasize total cost of ownership through predictive-maintenance subscriptions that minimize downtime and extend warranty coverage. Coesia’s 2024 consolidation of niche brands into a single platform caters to pharmaceutical buyers seeking a one-stop source for primary, secondary, and serialization modules.

Software capabilities are emerging as competitive moats. Antares Vision filed a 2024 patent for blockchain-based serialization that integrates with SAP ERP, positioning the firm as a data-integrity partner rather than solely a hardware vendor. Smaller challengers, such as MG2 and Bausch + Ströbel, target flexible batch sizes with modular fillers that can expand from pilot to commercial scale without requiring infrastructure replacement, appealing to biologics startups and personalized medicine producers.

Raw material shortages that lengthened lead times in 2023 have abated; however, the scarcity of mechatronics engineers persists, especially in the Asia-Pacific region. Suppliers mitigate labor gaps by embedding augmented-reality service tools that guide local technicians through maintenance, reducing reliance on expatriate specialists. Energy-efficiency metrics add a new layer of competition as European clients weigh kilowatt-hour savings over list price.

Pharmaceutical Packaging Machinery Industry Leaders

Syntegon Technology GmbH

IMA S.p.A.

Marchesini Group S.p.A.

Uhlmann Group

Romaco Holding GmbH

- *Disclaimer: Major Players sorted in no particular order

Pharmaceutical Packaging Machinery Market Companies Covered in this Report

- Syntegon Technology GmbH

- IMA S.p.A.

- Marchesini Group S.p.A.

- Uhlmann Group

- Romaco Holding GmbH

- Optima Packaging Group GmbH

- MULTIVAC Group

- Körber AG (Medipak Systems)

- Antares Vision Group S.p.A.

- Coesia S.p.A.

- Bausch + Ströbel Maschinenfabrik Ilshofen GmbH + Co. KG

- ACG Packaging Private Limited

- Ishida Co. Ltd.

- PAC Machinery Group Inc.

- Accutek Packaging Equipment Companies Inc.

- Vanguard Pharmaceutical Machinery Inc.

- MG2 s.r.l.

- Becton Dickinson and Company

- SSI SCHÄFER Group

- Herma GmbH

- Videojet Technologies Inc.

Read Analysis of Pharmaceutical Packaging Machinery Companies

Recent Industry Developments in Pharmaceutical Packaging Machinery Market

- November 2025: Antares Vision Group acquired a California-based AI software startup specializing in edge analytics for vision systems, immediately integrating the technology into its flagship inspection cameras to boost sub-micron defect detection accuracy by 15%.

- July 2025: Marchesini Group debuted a collaborative-robot case-packer that executes up to 60 format changeovers per shift without stopping production, targeting personalized medicine facilities with high SKU turnover.

- May 2025: IMA Group inaugurated a digital-twin innovation center in Florence, Italy, where pharmaceutical clients can run full virtual factory acceptance tests before equipment ships, trimming on-site validation time by an estimated four weeks.

- February 2025: Syntegon Technology launched a cloud-based condition-monitoring service that streams real-time vibration, temperature, and vacuum data from installed fillers and cappers to a secure analytics portal, allowing customers to predict failures up to 10 days in advance and cut unplanned downtime by 25%.

Global Pharmaceutical Packaging Machinery Market Report Scope

Pharmaceutical packaging machinery refers to equipment designed to package pharmaceutical products, ensuring their safety, integrity, and compliance with regulatory standards. These machines handle various packaging processes, including primary, secondary, and tertiary packaging, as well as labeling and serialization.

The Pharmaceutical packaging machinery market report is segmented by Machinery Type (Primary, Secondary, Labelling and Serialization, Tertiary), Automation Level (Manual, Semi-Automatic, Automatic), Packaging Format (Blister, Bottle/Vial, Sachet and Stick Pack, Cartoning and Case Packing), Application (Solids, Liquids, Semi-Solids, Parenterals), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Segmentation Overview

By Machinery Type

| Primary Packaging Equipment |

| Secondary Packaging Equipment |

| Labelling and Serialization Equipment |

| Tertiary Packaging Equipment |

By Automation Level

| Manual |

| Semi-Automatic |

| Automatic |

By Packaging Format

| Blister Packaging |

| Bottle/Vial Packaging |

| Sachet and Stick Pack |

| Cartoning and Case Packing |

By Application

| Solids (Tablets/Capsules) |

| Liquids |

| Semi-Solids |

| Parenterals (Injectables) |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Nigeria | ||

| Rest of Africa | ||

| By Machinery Type | Primary Packaging Equipment | ||

| Secondary Packaging Equipment | |||

| Labelling and Serialization Equipment | |||

| Tertiary Packaging Equipment | |||

| By Automation Level | Manual | ||

| Semi-Automatic | |||

| Automatic | |||

| By Packaging Format | Blister Packaging | ||

| Bottle/Vial Packaging | |||

| Sachet and Stick Pack | |||

| Cartoning and Case Packing | |||

| By Application | Solids (Tablets/Capsules) | ||

| Liquids | |||

| Semi-Solids | |||

| Parenterals (Injectables) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of pharmaceutical packaging machinery in 2031?

The market is expected to reach USD 10.02 billion by 2031.

Which region will grow fastest through 2031?

Asia-Pacific, driven by contract manufacturing upgrades, is forecast to post a 9.30% CAGR.

Which machinery type leads current revenue?

Primary packaging equipment holds 54.18% of 2025 revenue because it safeguards product sterility.

How fast will automatic systems expand?

Automatic lines are projected to grow at an 8.55% CAGR as firms offset rising labor costs with robotics.

Why is serialization driving equipment retrofits?

Global laws require unit-level traceability, compelling manufacturers to add coding and aggregation modules or risk non-compliance.

What restrains mid-tier firms from adopting advanced lines?

Upfront costs can exceed USD 8 million, and validation can last up to 12 months, stretching capital budgets and launch timelines.

Page last updated on: