Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

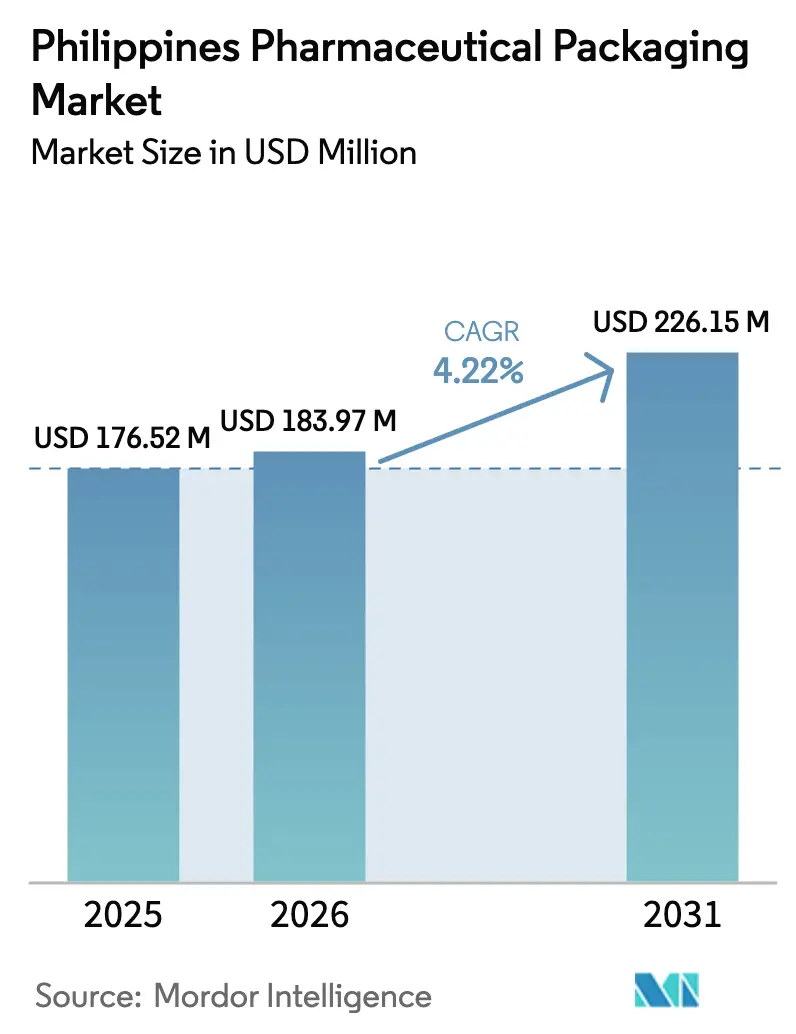

| Base Year Market Size (2025) | USD 176.52 Million |

| Market Size (2026) | USD 183.97 Million |

| Market Size (2031) | USD 226.15 Million |

| Growth Rate (2026 - 2031) | 4.22% CAGR |

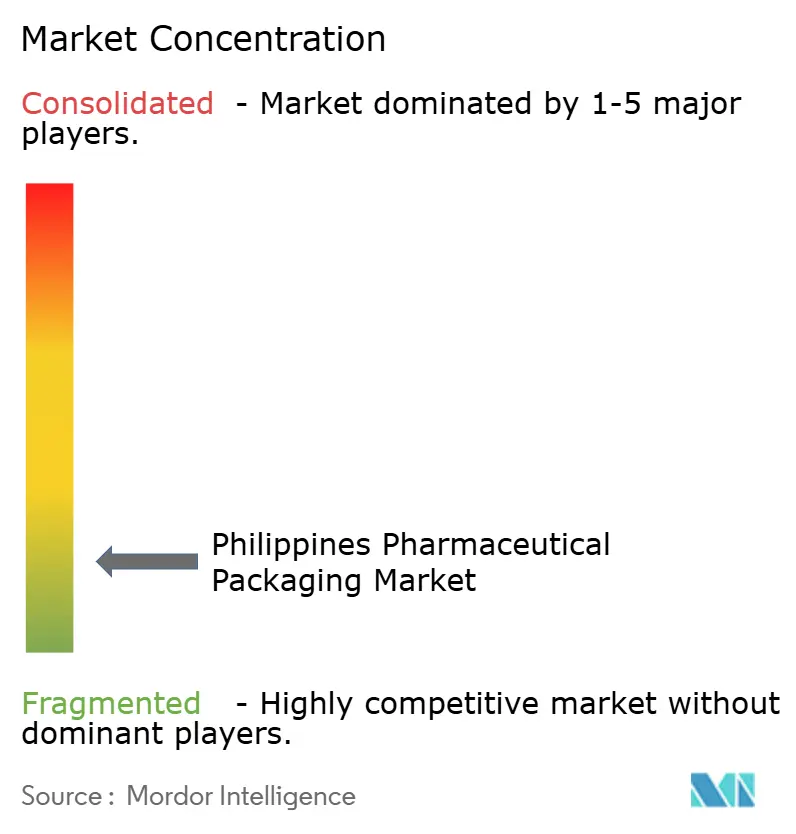

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Pharmaceutical Packaging Market Analysis by Mordor Intelligence

The Philippines pharmaceutical packaging market size in 2026 is estimated at USD 183.97 million, growing from 2025 value of USD 176.52 million with 2031 projections showing USD 226.15 million, growing at 4.22% CAGR over 2026-2031. A growing preference for patient-friendly formats, rapid expansion of contract manufacturing organizations (CMOs), and government procurement reforms further propel the Philippines pharmaceutical packaging market, while supply-chain vulnerabilities and cold-chain gaps temper its long-term growth trajectory.

Key Report Takeaways

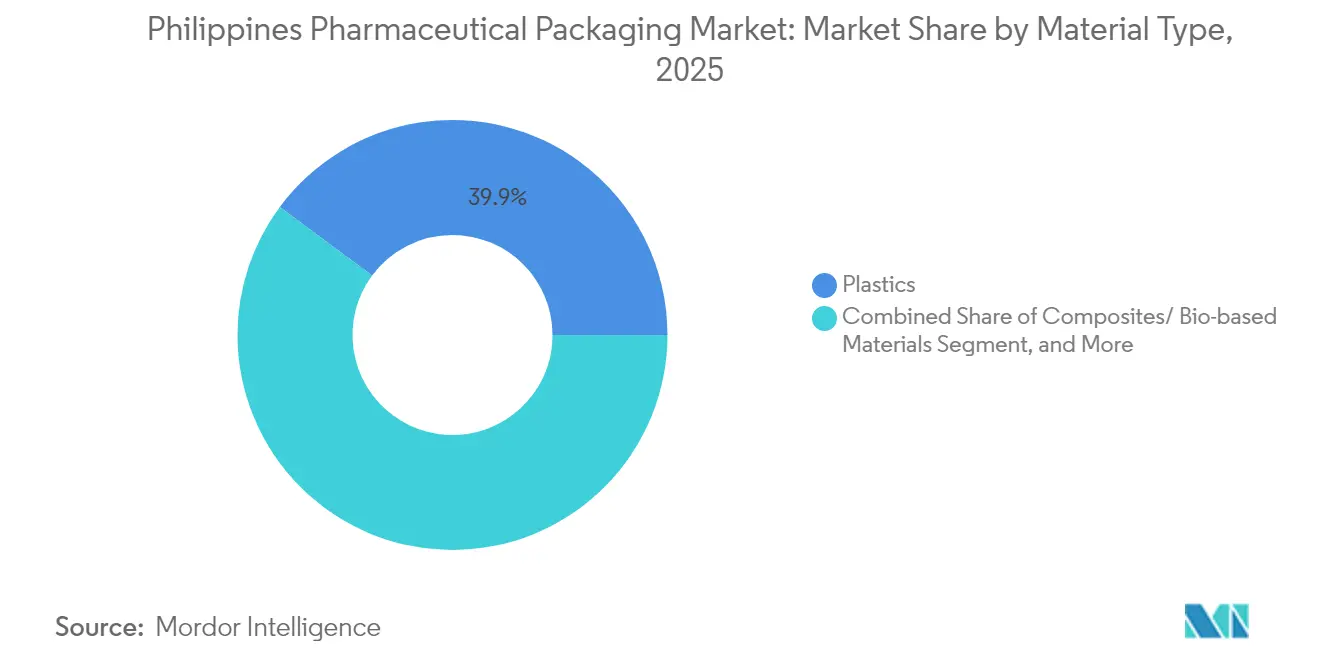

- By material type, plastics led with 39.85% revenue share in 2025, whereas composites and bio-based alternatives are forecast to expand at a 5.96% CAGR through 2031.

- By product type, bottles accounted for a 21.09% slice of the Philippines pharmaceutical packaging market share in 2025, while pouches and bags are poised to grow at a 5.34% CAGR to 2031.

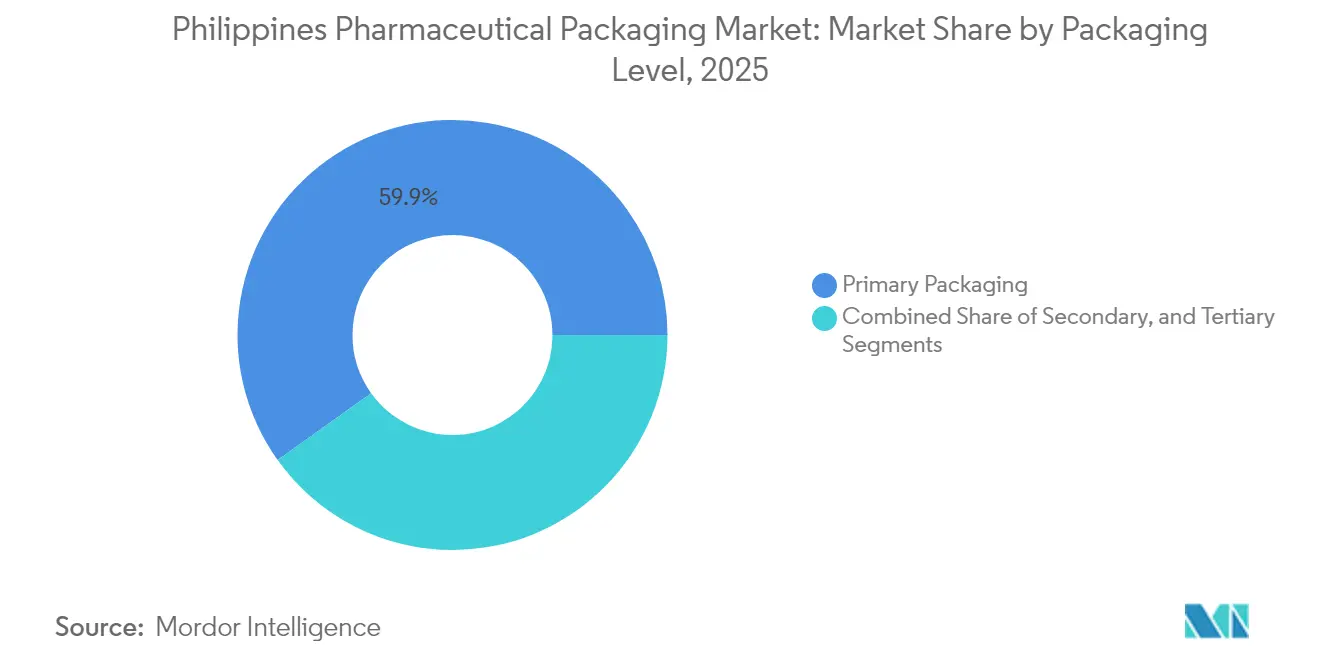

- By packaging level, primary formats commanded 59.88% of the Philippines pharmaceutical packaging market size in 2025 and are projected to grow at a 5.03% CAGR during the outlook period.

- By end-user, pharmaceutical manufacturing companies held 49.25% share in 2025, whereas contract packaging organizations are expected to post the fastest 5.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Philippines Pharmaceutical Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Generic Drug Production | +1.5% | National, PEZA ecozones | Medium term (2-4 years) |

| Increasing Government Procurement of Essential Medicines | +0.8% | National, public hospitals | Short term (≤ 2 years) |

| Expansion of Local Contract Manufacturing Organizations | +0.6% | Metro Manila, Laguna, Tarlac | Medium term (2-4 years) |

| Stringent Anti-Counterfeiting Regulations | +0.5% | Urban centers nationwide | Long term (≥ 4 years) |

| Rising Demand for Patient-Friendly Packaging | +0.4% | Urban aging clusters | Medium term (2-4 years) |

| Growth of E-Pharmacy Distribution Channels | +0.3% | Metro Manila, Cebu, Davao | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Generic Drug Production

Fast-tracked approvals, now limited to 45 days, have cut market-entry timelines, prompting local firms to reformulate labels and invest in compliant blister, bottle, and pouch solutions. The generic-drug spending pool is projected to reach USD 3.8 billion by 2028, and every new molecule requires serialization-ready packaging that meets the Department of Health’s generic-label mandate. Fiscal perks inside PEZA parks amplify volumes, while five India-based firms that scouted Philippine sites in August 2024 signal future demand for high-barrier bottles and tamper-evident seals. Packaging converters that pre-qualify materials under Good Manufacturing Practice guidelines are winning early supplier status with these green-field entrants, cementing volume commitments across 2025-2028 contract cycles. [1]Philippine News Agency, “BOI Invites Japanese Pharma Firms to Invest in PH,” pna.gov.ph

Increasing Government Procurement of Essential Medicines

The Philippine Pharma Procurement Inc. roadmap aims to increase the local-producer share of tenders to 50% by 2030, securing routine orders for suppliers already accredited under the Green Lane licensing system. The Clark pharmaceutical logistics hub, a USD 35.25 million investment, features GDP-certified warehousing that caters to suppliers of serialized cartons and pre-printed labels. Essential-medicine packs, diabetes strips, anti-hypertensive blister sleeves, and oncology vals must now carry traceability QR codes that sync with the Department of Health inventory platform. Converters offering end-to-end coding services and data-integrity audits command price premiums yet secure multiyear contracts, accelerating revenue diversification within the Philippines pharmaceutical packaging market.

Expansion of Local Contract Manufacturing Organizations

CMOs scale rapidly as multinationals outsource to lower-cost structures. PEZA’s Victoria Industrial Park houses 27 life-science tenants with export projections of USD 299.93 million, which in turn drive pull-through orders for high-speed filling, capping, and shrink-sleeve services. Lloyd Laboratories’ 1 million-capsule expansion highlights demand for HDPE bottles with child-resistant closures, while HSBC-facilitated dialogues bring AstraZeneca and GSK to evaluate joint-venture sterile-fill capability. These deals rely on domestically sourced cartons, leaflets, and serialized labels, creating a ripple effect across ink suppliers and RFID tag vendors already active in the Calabarzon industrial belts.

Stringent Anti-Counterfeiting Regulations

FDA Advisory 2025-0674 on counterfeit Bioflu tablets highlights the need for enhanced market surveillance.[2]Food and Drug Administration, “FDA Advisory 2025-0674,” fda.gov.phAdministrative Order 2024-0015 mandates the use of tamper-evident seals, covert inks, and serialized barcodes at the primary-pack level, encouraging suppliers to adopt integrated technology platforms. Vendors that bundle holographic lacquers with cloud-based verification portals differentiate in government tenders covering 1,800 public hospitals. Medium-sized local converters partner with European security label specialists, transferring knowledge on UV-traced adhesives and micro-text. Over the long term, anti-counterfeiting compliance raises capital barriers and nudges the Philippines pharmaceutical packaging market toward a quality-driven consolidation phase.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heavy Reliance on Imported Raw Materials | -0.7% | All manufacturing regions | Long term (≥ 4 years) |

| Limited Cold Chain Infrastructure | -0.5% | Rural and secondary cities | Medium term (2-4 years) |

| Price Sensitivity among Local Manufacturers | -0.4% | Regional SMEs | Short term (≤ 2 years) |

| Environmental Compliance Costs | -0.3% | Urban regulatory hotspots | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heavy Reliance on Imported Raw Materials

With 98% of active ingredients and most plastic resins imported, converters face currency swings and freight disruptions that compress margins. The Philippine Pharmaceutical Industry Association notes raw-material imports grew 15% between 2015-2019; the pandemic exposed lead-time spikes beyond 120 days, forcing converters to double buffer stocks. The lack of a domestic petrochemical base keeps resin prices 8-12% higher than those of regional peers, prompting some fillers to source preforms from Thailand and Malaysia. Although the Department of Trade and Industry considers tariff relief for pellet imports, short-term volatility persists, making cost-plus contracts difficult to secure for more than one bid cycle.

Limited Cold Chain Infrastructure

Berben Logistics increased its capacity to 10,000 pallets in 2024; however, the Cold Chain Association estimates national demand growth at 8-10% annually, leaving a persistent gap in provincial corridors. [3]DHL Group, “DHL Group to Invest EUR 500 Million in Asia Pacific,” dhl.com Rural vaccine campaigns rely on insulated shippers that must maintain temperatures between 2-8 °C for 72 hours, but fragmented island routes stretch delivery windows beyond the design specifications, risking spoilage. Packaging suppliers must develop higher-grade EPS liners, phase-change packs, and real-time IoT sensors, which will result in a 15-20% increase in unit costs. Smaller regional firms often balk at these premiums, slowing adoption despite FDA guidance on biologic stability requirements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Plastics Hold Scale While Sustainable Alternatives Accelerate

Plastics deliver the core volume advantage, capturing 39.85% of the Philippines pharmaceutical packaging market in 2025. HDPE bottles, PET jars, and polypropylene closures are the most commonly used materials because regulatory dossiers already reference their migration data, thereby reducing approval lead times. The Philippines pharmaceutical packaging market size for plastics is set to grow steadily, even as new Extended Producer Responsibility (EPR) rules raise recovery targets to 80% by 2028. EPR costs prompt brand owners to trial bio-based liners and recycled-content PET, which command price increases while unlocking tax credits.

Sustainable composites, although niche today, are projected to chart the fastest 5.96% CAGR as global clients incorporate life-cycle metrics into supplier scorecards. The Department of Science and Technology’s Green Packaging Laboratory pilots chitosan and pectin films, and early adopters among multinationals co-fund scale-up trials. Glass retains a loyal base in injectables that require Type I borosilicate integrity, while aluminum tubes fill steroid creams that require oxygen barriers. Collectively, these material pivots re-align supply chains, inviting joint ventures that embed resin recycling lines within ecozones, moves that sustain the Philippines pharmaceutical packaging market over the medium term.

By Product Type: Bottles Retain Share, Pouches Drive Convenience

Bottles owned 21.09% of the Philippines pharmaceutical packaging market share in 2025, thanks to their compatibility with high-speed lines serving OTC cough-cold syrups and vitamin liquids. Automated vision systems and induction-seal liners reduce contamination risk, solidifying their use in public hospital tenders. Meanwhile, the Philippines pharmaceutical packaging market size for pouches and bags grows fastest at 5.34% CAGR as e-pharmacies prefer lightweight laminate sachets that slash freight costs by 30%.

Blister packs remain central to solid-dose compliance, especially after the FDA endorsed wallet blister formats that support QR-linked adherence apps for patients with chronic diseases. Prefilled syringes and cartridges gain popularity in vaccination drives; vials and ampules maintain the security of specialty injectables. Cartons receive functional upgrades, including RFID inlays and braille embossing, while pallet corner boards transition to recycled paper to meet EPR audits. This product-mix evolution rewards converters who are agile enough to switch between short-run, personalized kits and high-volume, commodity batches without incurring downtime penalties.

By Packaging Level: Primary Dominance Highlights Regulatory Gravity

Primary formats, bottles, blisters, and vials captured 59.88% share in 2025 and are set for a 5.03% CAGR, underscoring their centrality to sterility and barrier integrity. Serialization laws now cascade directly onto primary packs, propelling the Philippines pharmaceutical packaging market toward integrated code-verification systems embedded at the filler head. High-capex cleanroom investments lock out opportunistic entrants yet widen moat advantages for incumbents certified under ISO 15378.

Secondary packs shoulder label-compliance duties and withstand distribution knocks; converters add tear-tapes and brand-protection inks that harmonize with logistic-level aggregation codes. Tertiary pallet stretch hoods migrate to thinner gauges yet retain puncture performance through metallocene blends. In aggregate, regulatory gravity and risk of cross-contamination keep primary formats in the strategic spotlight despite sustainability-driven shifts elsewhere in the value chain.

By End-User Industry: CMOs Outpace In-House Fillers

Pharmaceutical manufacturers contributed 49.25% of 2025 volumes, leveraging entrenched sites in Metro Manila and Laguna. Nonetheless, CMOs register the sharpest 5.88% CAGR because global sponsors now bundle packaging services within broader tech-transfer deals. Inside PEZA’s Victoria Park, CMOs co-locate blister thermoformers, bottle unscramblers, and ROC-enabled inspection lines to court small-molecule clients eyeing ASEAN export certificates.

Retail pharmacies and clinic chains order shelf-ready packs that optimize SKU density, while hospitals require unit-dose barcoding integrated with electronic medical records. The government’s 'Botika at Bakuna Para Sa Mamamayan' campaign adds rural health units that purchase standardized vaccine vial cartons, further stretching CMO order books. Together, these dynamics reinforce outsourcing momentum, deepening competitive intensity across the Philippines pharmaceutical packaging market.

Geography Analysis

Metro Manila remains the operational nucleus thanks to proximity to FDA headquarters, seaport access, and a skilled labor pool that houses over half of the active packaging plants. This corridor anchors fresh foreign direct investments, as CMOs plug into existing utility grids that assure class 100,000 cleanroom compliance. The surrounding Calabarzon belt benefits from land-lease economics and clusters of carton, ink, and resin suppliers that cut inbound trucking times to one day.

Strategic diversification gains traction northward. PEZA’s Victoria Industrial Park in Tarlac opened in July 2024, furnishing 34 hectares of tax-incentivized lots fitted with pharma-grade effluent lines and solar rooftops. Adjacent to Clark Freeport, the area evolves as a transport hub, linking an FDA-approved logistics center to Clark International Airport’s 24-hour cargo slot, which enables cold-chain lanes that shave last-mile lead times for Central Luzon hospitals.

Secondary metros, such as Cebu and Davao, capture incremental distribution volumes yet struggle with intermittent refrigerated storage, which curbs biologic penetration outside the central islands. Archipelagic logistics force packaging designs that endure multiple break-bulks, humidity swings, and inter-island vessel delays. Government infrastructure programmes, including roll-on roll-off port upgrades, aim to ease these friction points, promising broader regional uplift for the Philippines pharmaceutical packaging market over the forecast horizon.

Competitive Landscape

The field exhibits moderate fragmentation: global majors dominate high-barrier laminates and sterile packs, while mid-sized local companies thrive in secondary cartons and leaflets. Amcor’s Malaysia coating plant, completed in April 2025, supplies medical-grade roll stock to Philippine converters, reinforcing supply security for regional customers. Meanwhile, ALPLA Philippines’ Calamba site expands recycled-content HDPE capacity, tapping EPR-induced demand from vitamin bottlers.

Joint ventures emerge as a convenient route to regulatory familiarity: European security-label specialists embed micro-tagging lines within Manila facilities operated by local groups holding FDA site licenses. CMOs negotiate material rebates tied to volume thresholds, leveraging scale to undercut smaller packers confined to older lines. Sustainability emerges as the next battleground, and companies that can validate their cradle-to-gate carbon footprints increasingly edge out their peers in multinational audits.

Barriers remain high: ISO 15378 certification, serialization hardware, and cold-chain validation collectively increase capital intensity to over USD 4 million for a competitive primary-pack line. Consequently, merger talks among domestic converters pick up pace as they seek to reach volume efficiencies and bargaining heft in resin procurement. These moves are likely to inch the Philippines pharmaceutical packaging market toward greater concentration over the next five years.

Philippines Pharmaceutical Packaging Industry Leaders

Robicel Trading

Euro-med Laboratories Phil., Inc

Bestpak Packaging Solutions, Inc.

Netpak Phils., Inc.

Gl Otometz Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: De La Salle Medical and Health Sciences Institute inaugurated the Dr. Mariano Que College of Pharmacy, bolstering local R and D talent pools.

- September 2025: FDA Advisory 2025-0674 warned against counterfeit Bioflu tablets, spotlighting serialization urgency.

- April 2025: Clark International Airport Corporation and Philippine Pharma Procurement Inc. signed a PHP 2 billion pact to build a pharmaceutical logistics hub at Clark Freeport.

- April 2025: DHL Group earmarked EUR 500 million (USD 530 million) for Asia-Pacific healthcare-logistics upgrades, including GDP-certified hubs serving the Philippines.

Philippines Pharmaceutical Packaging Market Report Scope

The scope of the study provides an overall understanding of the pharmaceutical and pharmaceutical packaging sector in the Philippines. Further, a broad breakdown will be provided for the bottles and containers, syringes and cartridges, vials and ampoules, and lastly, pouches and packs. The other product types are not a part of the current scope of work. The report comprises a market overview and key trends, along with the details of the performance of the pharmaceutical vendors and pharma packaging sector in the country, recent developments, and the impact of COVID-19 on the market.

By Material Type

| Plastic | High-Density Polyethylene (HDPE) |

| Low-Density Polyethylene (LDPE) | |

| Polyethylene Terephthalate (PET) | |

| Other Plastics | |

| Glass | |

| Metal | |

| Paper and Paperboard | |

| Composites/ Bio-based Materials |

By Product Type

| Bottles |

| Vials and Ampoules |

| Blister Packs |

| Prefilled Syringes and Cartridges |

| Tubes |

| Pallets |

| Pouches and Bags |

| Carton Boxes |

| Other Product Types |

By Packaging Level

| Primary |

| Secondary |

| Tertiary |

By End-user Industry

| Pharmaceutical Manufacturing Companies |

| Contract Packaging Organizations |

| Retail and Institutional Pharmacies |

| Hospitals and Clinics |

| Other End-user Industries |

| By Material Type | Plastic | High-Density Polyethylene (HDPE) |

| Low-Density Polyethylene (LDPE) | ||

| Polyethylene Terephthalate (PET) | ||

| Other Plastics | ||

| Glass | ||

| Metal | ||

| Paper and Paperboard | ||

| Composites/ Bio-based Materials | ||

| By Product Type | Bottles | |

| Vials and Ampoules | ||

| Blister Packs | ||

| Prefilled Syringes and Cartridges | ||

| Tubes | ||

| Pallets | ||

| Pouches and Bags | ||

| Carton Boxes | ||

| Other Product Types | ||

| By Packaging Level | Primary | |

| Secondary | ||

| Tertiary | ||

| By End-user Industry | Pharmaceutical Manufacturing Companies | |

| Contract Packaging Organizations | ||

| Retail and Institutional Pharmacies | ||

| Hospitals and Clinics | ||

| Other End-user Industries |

Key Questions Answered in the Report

What is the current value of the Philippines pharmaceutical packaging market?

The market is valued at USD 183.97 million in 2026 and is forecast to climb to USD 226.15 million by 2031.

Which segment holds the largest share in Philippine drug packaging?

Primary formats such as bottles, blisters, and vials command 59.88% of 2025 revenue.

Why are CMOs growing faster than in-house packaging units?

Multinationals outsource to CMOs for cost efficiency, regulatory expertise, and ecozone-based tax incentives, driving a 5.88% CAGR for the segment.

How does the EPR law affect packaging materials?

It compels companies to recover 80% of plastic output by 2028, accelerating investment in bio-based and recycled materials.

What is the main supply-chain challenge for Philippine converters?

Heavy reliance on imported resins and APIs exposes converters to currency volatility and logistics delays, curbing margin stability.

Are anti-counterfeiting requirements mandatory for all medicine packs?

Yes, Administrative Order 2024-0015 enforces serialization and tamper-evident features on primary packaging across all prescription and OTC drugs.

Page last updated on: