Micro Switch Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

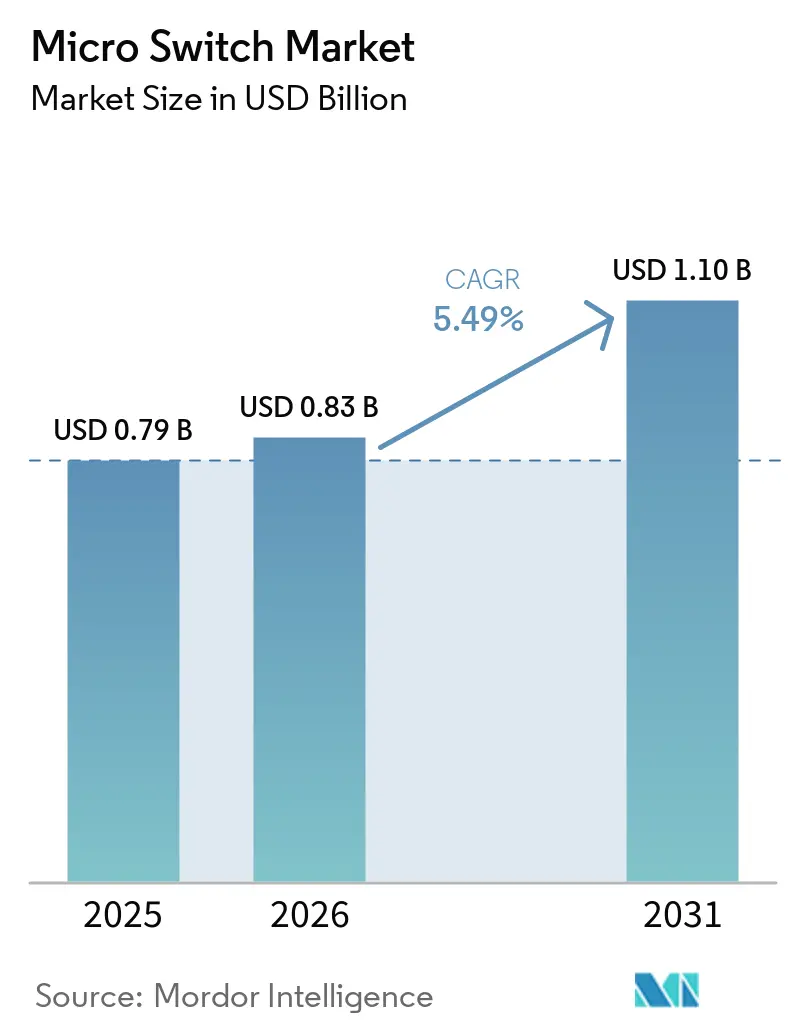

| Market Size (2026) | USD 0.83 Billion |

| Market Size (2031) | USD 1.10 Billion |

| Growth Rate (2026 - 2031) | 5.49% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Micro Switch Market Analysis by Mordor Intelligence

The Micro Switch Market size is projected to expand from USD 0.79 billion in 2025 and USD 0.83 billion in 2026 to USD 1.10 billion by 2031, registering a CAGR of 5.49% between 2026 to 2031. Momentum rests on the installed-base loyalty earned by electromechanical designs, even as solid-state Hall-effect and tunneling-magnetoresistance sensors court battery-powered devices. Demand for IP67-sealed limit switches in wind-turbine yaw systems, solar-tracker actuators, and food-service ovens is encouraging suppliers to raise contact-rating ceilings and improve enclosure integrity. Asia-Pacific appliance OEMs now fabricate switches in-house, compressing the cost curve for commoditized 5-ampere parts, while North American and European buyers prioritize IEC 61058 and UL 60335 compliance to guarantee traceable quality. The interplay between miniaturization, safety-code adherence, and input-cost volatility will determine whether the micro switch market sustains mid-single-digit expansion or yields volume to contactless alternatives.

Key Report Takeaways

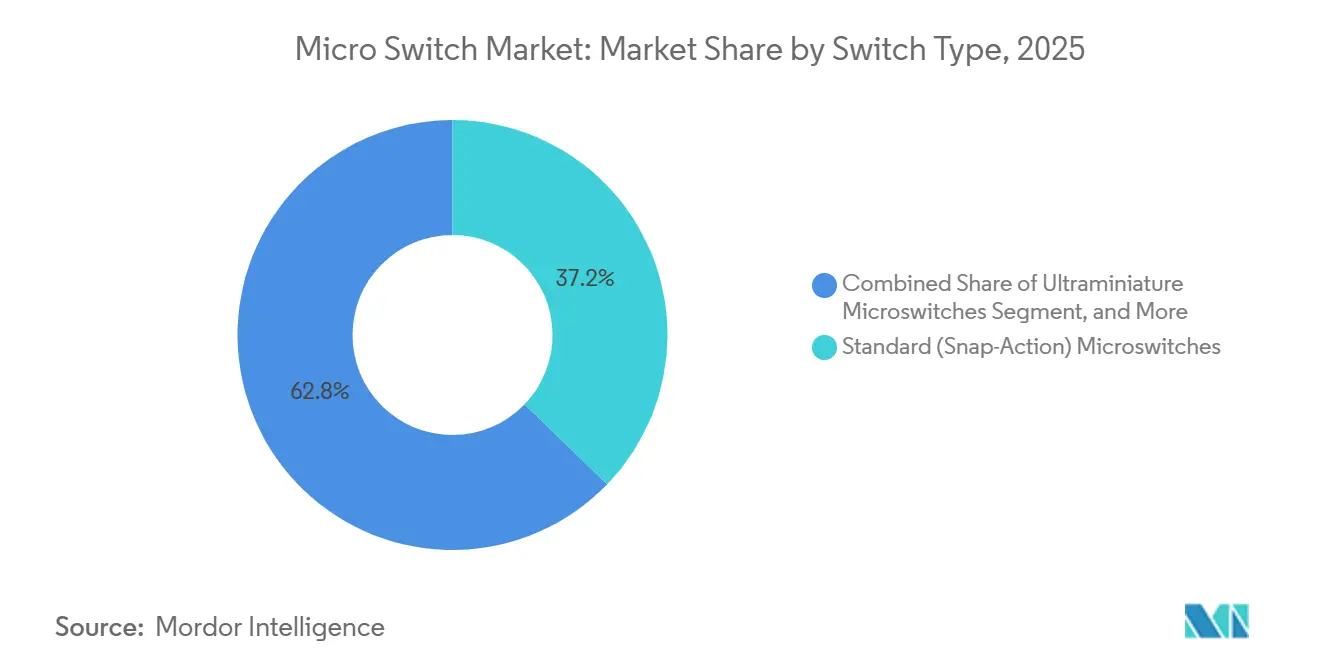

- By switch type, standard snap-action variants led with 37.2% of the micro switch market in 2025, while sealed and waterproof designs are forecast to expand at a 6.9% CAGR through 2031.

- By actuator type, lever-actuated designs accounted for 41.5% of the micro switch market in 2025, whereas roller-lever configurations are projected to grow at a 6.7% CAGR over the forecast period.

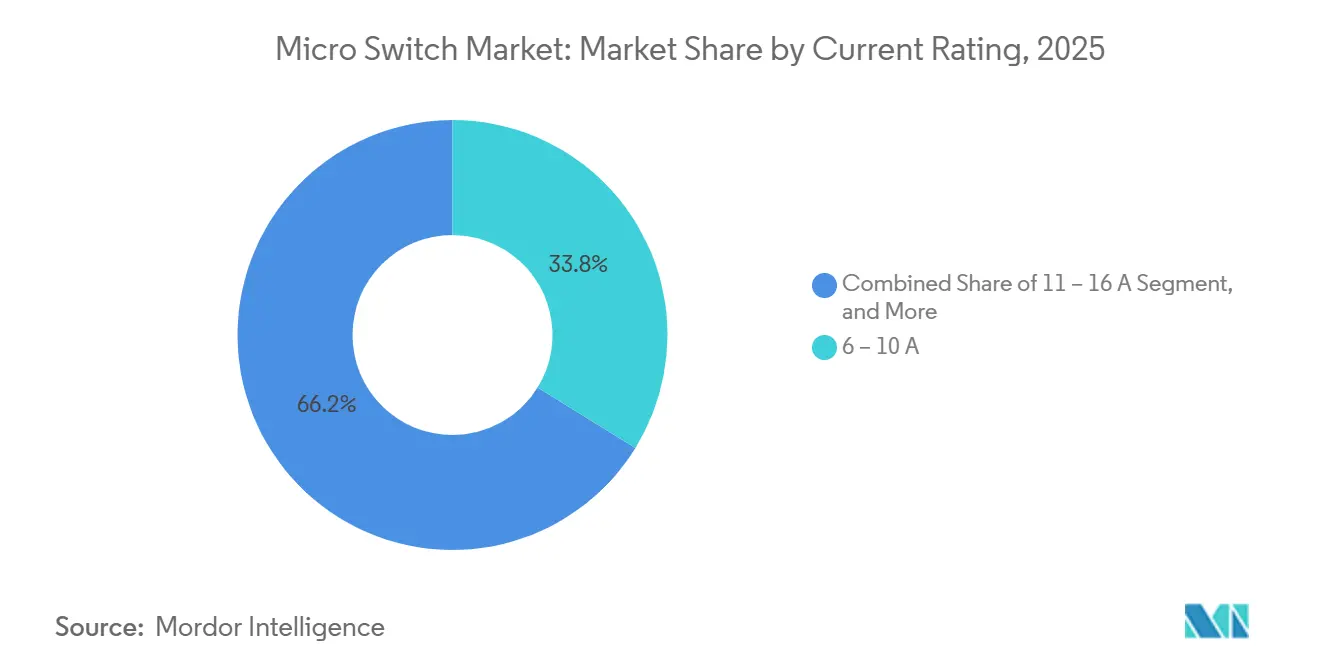

- By current rating, the 6-10 ampere bracket captured 33.8% of the micro switch market share in 2025, but above 16 ampere devices are advancing at a 6.5% CAGR to 2031.

- By end-user industry, home appliances held 26.9% of the micro switch market in 2025, and medical devices and instrumentation is expected to grow at a 6.4% CAGR during 2026-2031.

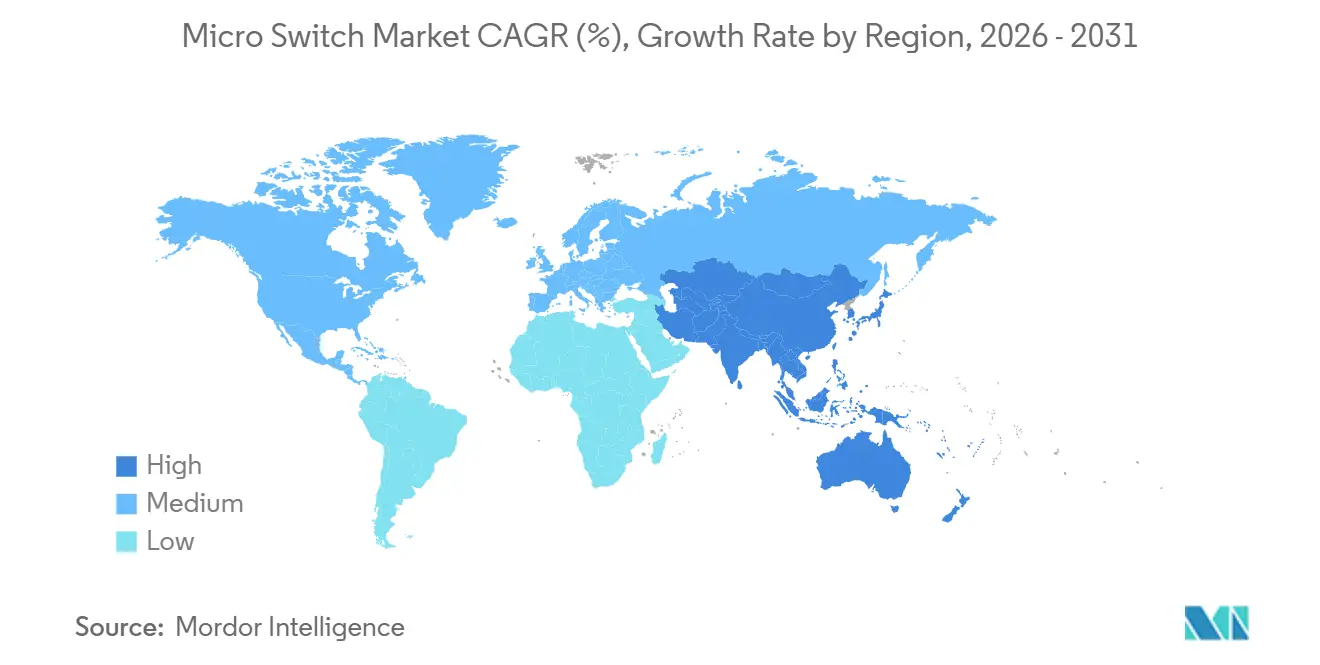

- By geography, Asia-Pacific commanded 42.7% of the micro switch market in 2025 and is estimated to post a 6.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Micro Switch Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing integration of microswitches in IoT-enabled smart-home appliances | +1.20% | North America and Asia-Pacific | Medium term (2–4 years) |

| Surge in automotive safety and ADAS sensor-redundancy requirements | +1.40% | North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Industrial automation retrofits demanding compact limit-switch alternatives | +1.10% | Europe, China, India | Medium term (2–4 years) |

| Rising adoption of sealed IP67 microswitches in outdoor renewable installations | +1.00% | Europe and China wind corridors, global spillover | Long term (≥ 4 years) |

| Rapid expansion of Chinese appliance OEMs with in-house switch sourcing | +0.90% | Asia-Pacific core | Short term (≤ 2 years) |

| Commercial food-service equipment compliance with stricter hygiene-switch standards | +0.60% | North America, Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Surge in Automotive Safety and ADAS Sensor-Redundancy Requirements

Global automakers' engineering Level-3 automation and above must meet ISO 26262 ASIL-D diagnostic coverage, which pushes tier-one suppliers to pair Hall sensors with snap-action microswitches as independent redundancy layers. Mechanical contacts introduce failure modes, such as weld or oxidation, that are statistically uncorrelated with magnetic-sensor drift, allowing safety architects to satisfy decomposition rules without up-specifying every component. Roller-lever actuators are favored because their positive-opening geometry guarantees contact separation at defined force thresholds, easing certification under IEC 61058-1.[1]SAE International, “Sensor Redundancy for Automated Driving Systems,” sae.org Demand for subminiature-footprint devices rated to −40 to 125 °C is therefore rising alongside electric-vehicle production. Suppliers that certify to IATF 16949 and document 1-million-cycle endurance gain a defensible edge in long-platform automotive programs.

Increasing Integration of Microswitches in IoT-Enabled Smart-Home Appliances

Matter-certified refrigerators, ovens, and washers embed microswitch interlocks to maintain hardware-level safety when wireless links fail. Appliance designers combine a USD 0.15 switch with a USD 2.50 system-on-chip, achieving dual-mode operation that meets UL 60335 without redesigning sheet-metal enclosures.[2]Homewell Technology, “Matter-Certified Smart Home Switches,” homewelltechnology.com As smart-home penetration in North America exceeds 40%, OEMs lock-in multiyear switch contracts to secure traceable quality and hedge against supply disruptions. Suppliers with ISO 9001 plants and local field-application engineers win preference over spot-market entrants. The result is stable, volume-driven demand that cushions margins even as commoditized current-rating segments face price pressure.

Industrial Automation Retrofits Demanding Compact Limit-Switch Alternatives

Factory owners updating conveyor lines and robot cells need to reclaim cabinet space for Ethernet switches and safety relays. Ultraminiature microswitches, often under 15 millimeters, replace bulky cam-operated limit switches without altering existing DIN-rail layouts. IP67 housings and 20-million-cycle mechanical ratings satisfy chemical-washdown and vibration requirements common in food, beverage, and automotive plants.[3]Azbil Corporation, “Compact Limit Switches with IP67 Protection,” azbil.com Despite the arrival of inductive and magnetic proximity sensors, mechanical devices keep share because their unit cost is one-third and they avoid electromagnetic-interference concerns inside variable-frequency-drive enclosures. Retrofit budgets, therefore, gravitate toward subminiature variants that blend reliability with plug-and-play interchangeability.

Rising Adoption of Sealed IP67 Microswitches in Outdoor Renewable Installations

Wind-turbine nacelles and solar-tracker gearboxes endure temperature swings up to 80 °C and high-humidity salt fog, which overwhelm unsealed switches in months.[4]Crouzet, “V4S-8318 and V5S-8320 Limit Switches for Wind Turbines,” crouzet.com Hermetically sealed devices rated for 10-million cycles protect revenue by preventing unplanned turbine shutdowns. Retrofit programs in Europe and China are replacing earlier open-frame switches to extend asset life by 5–7 years, a payback attractive under feed-in tariff schemes. Price premiums of 20–30% over standard variants are offset by avoided maintenance truck rolls. Vendors with proven sealing compounds and accelerated life-test data occupy a moat that low-cost entrants struggle to cross.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price pressure from commoditization and Chinese low-cost producers | -1.30% | Asia-Pacific and Middle East, global spillover | Short term (≤ 2 years) |

| Substitution risk from solid-state Hall-effect sensors in compact devices | -1.10% | North America, Europe, Japan | Medium term (2-4 years) |

| Supply-chain volatility of Ag-alloy contacts driving cost swings | -0.80% | Global | Short term (≤ 2 years) |

| Compliance burden with evolving RoHS and REACH halogen-free mandates | -0.50% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Pressure from Commoditization and Chinese Low-Cost Producers

Shenzhen contractors now quote 5-ampere snap-action switches at USD 0.08 in 10,000-piece lots, undercutting Japanese and European brands by up to 50%. Western incumbents watching margin erosion are exiting commodity categories and reallocating R&D toward aerospace and medical niches, but the retreat cedes appliance and low-current market share to Asia-based producers. High-volume Chinese facilities leverage IATF 16949 certification and automated inspection to court automotive tier-twos, accelerating the race to the bottom on price. As cost leadership reshapes the demand curve, only suppliers with automation, in-house plating, and hedged silver contracts can defend profitability. Short-run regional manufacturers face consolidation or exit.

Substitution Risk from Solid-State Hall-Effect Sensors in Compact Devices

Ultra-low-power Hall-effect and tunneling-magnetoresistance switches consume under 1 µA at standby and occupy 1.6-mm footprints, giving designers of wearables, IoT nodes, and hearing aids a battery-life advantage that mechanical parts cannot match. Magnetic sensors avoid contact bounce, enabling higher polling rates and simpler debounce firmware. Their off-state leakage and inability to provide visible contact separation, however, hinder penetration of safety-critical horizons such as industrial emergency stops. The most acute impact appears in consumer electronics, where mechanical buttons are disappearing from smartphones and tablets. As volumes migrate, electromechanical suppliers lose scale economies, leading to higher tool amortization costs that inflate unit pricing in the remaining segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Switch Type: Sealed Variants Gain Traction in Harsh Environments

The micro switch market size attributed to sealed and waterproof devices is growing faster than their standard counterparts, as renewable-energy and outdoor-equipment buyers specify IP67 ratings for long-life field service. Standard snap-action models retained 37.2% share in 2025 owing to entrenched use in appliances and light machinery, yet their outlook is tempered by Hall-sensor adoption in portable electronics and by Asia-Pacific OEM vertical integration.

Sealed switches command a 20-30% price premium but cut truck-roll maintenance costs across remote wind farms and solar arrays. Subminiature sealed formats, in particular, address medical pumps and handheld diagnostics where environmental sealing and miniature size intersect. Limit-switch form factors see steady uptake in industrial automation panels migrating to distributed I/O structures. Vendors combining hermetic sealing, self-cleaning contacts, and accelerated life-test results are well-positioned to leverage the 6.9% growth runway through 2031.

By Actuator Type: Roller-Lever Designs Serve Industrial Retrofits

Lever-actuated devices held 41.5% of 2025 demand, providing the versatility needed for appliance lids, safety gates, and hood-latch sensors. Roller-lever products, enjoying a 6.7% CAGR, replace bulky cam-operated limit switches during factory modernization, thanks to positive-opening mechanics that simplify IEC 61058-1 compliance.

Plunger styles remain staples in elevator call stations and push-button panels where linear travel dominates. Toggle and custom actuators thrive in aircraft cockpits and surgical instruments that mandate tactile confirmation. As collaborative robots proliferate, designers prefer roller levers offering up to 40% lower actuation force, preserving battery life in autonomous carts and handheld controllers. This retooling momentum sustains roller-lever growth well above the micro switch market average.

By Current Rating: High-Amperage Switches Address Food-Service Demands

The micro switch market size for the 6–10 ampere class reached the largest revenue share in 2025 at 33.8%, covering most household and light-industrial loads. Above-16-ampere grades, though smaller, are on a 6.5% CAGR trajectory as commercial ovens and high-temperature dishwashers upgrade to faster heating elements that draw more than 3,500 watts.

Up-to-5-ampere parts face fierce price competition, with bids below USD 0.10 driving margin compression and pushing Western vendors toward premium offerings. Between 11 and 16 amperes, silver-cadmium-oxide contacts remain the standard to cope with inductive motor loads. Solid-state relays nibble at some high-current niches, yet heat-sink requirements and leakage currents curb displacement in tight food-service enclosures, keeping mechanical designs relevant for splash-proof and hygiene-code compliance.

By End-User Industry: Renewable Energy Outpaces Legacy Appliances

Home appliances supplied 26.9% of shipments in 2025, but growth is flattening now that appliance OEMs fashion switches in-house and adopt Hall sensors for door-interlocks. Medical devices and instrumentation, in contrast, is set to expand at a 6.4% CAGR as wind-turbine retrofits and solar-tracker installations demand sealed limit switches rated for millions of cycles under vibration and salt-spray exposure.

Automotive platforms sustain volume by specifying mechanical redundancy for ASIL-D compliance in brake pedals and seat-belt buckles. Industrial automation remains steady, helped by IO-Link-enabled designs that stream actuation counts for predictive maintenance. Medical devices, while low in unit numbers, deliver outsized margins because UL 60601-1 and ISO 13485 qualification create entry barriers. Niche consumer electronics, such as gaming peripherals, sustain tactile-switch demand despite broader smartphone design shifts toward haptic displays.

Geography Analysis

Asia-Pacific, with 42.7% of 2025 revenue, is projected to post a 6.1% CAGR through 2031, powered by Chinese appliance production and expanding regional auto-electronics lines. Dongnan Electronics’ 300-million-unit annual capacity exemplifies scale economics that blunt import feasibility for lower-current models. Vietnam and India showcase emerging assembly hubs seeking local switch supply to secure tariff advantages and meet production-linked incentives, though inconsistent quality enforcement remains a hurdle. Japan and South Korea focus on high-reliability aerospace and automotive niches while gradually offshoring consumer volume to Southeast Asia.

Europe stabilizes as wind-farm retrofits and Industry 4.0 investments counterbalance declines in domestic appliance output. German and Swiss specialists cater to SIL-3 safety applications and renewable installations, leveraging local engineering support and short lead times. The United Kingdom’s post-Brexit customs friction adds a slight tailwind for regional distributors able to deliver just-in-time to auto plants in Germany, France, and the Czech Republic. Middle Eastern construction booms lift HVAC switch demand, but the region still imports the majority of components. Africa’s nascent appliance clusters in South Africa, Egypt, and Morocco open green-field opportunities for suppliers ready to establish distribution and technical training.

North America maintains share through automotive ADAS rollouts, FDA-regulated medical devices, and food-service hygiene upgrades that prefer UL-recognized parts. U.S. factories demand IP67 sealed switches for electric-vehicle battery packs and restaurant conveyor ovens, supporting premium pricing. Canadian auto parts plants integrate high-cycle subminiature devices into battery disconnects, while Mexican appliance lines rely on vendor-managed inventory programs to streamline logistics. South America stays replacement-driven due to macroeconomic headwinds, limiting new-build volumes. Collectively, these dynamics reveal a bifurcated landscape: Asia-Pacific drives volume, whereas North America and Europe underpin margins via regulatory and quality complexity.

Competitive Landscape

The top five suppliers, Omron, Honeywell, Alps Alpine, TE Connectivity, and Panasonic, command roughly 50% combined revenue, indicating moderate concentration. Their strategy centers on miniaturization, hermetic sealing, and IEC 61058 compliance to hold safety-critical ground.

High-volume Chinese contenders such as Defond, Salecom, and Zing Ear leverage 300-million-unit capacity and IATF 16949 pedigrees to win appliance and automotive tier-two contracts on cost leadership. Solid-state challengers, including Texas Instruments, Allegro MicroSystems, and Littelfuse, push contactless Hall and tunneling-magnetoresistance switches into battery-powered IoT devices, yet lack positive-opening action essential for industrial safety circuits.

M&A remains active: Lagercrantz’s April 2026 acquisition of Michael Smith Switchgear strengthens UK distribution, while Nidec Copal’s earlier roll-ups add bespoke actuator know-how for aerospace and medical customers. Forward differentiation may hinge on embedding IO-Link, RFID tagging, or diagnostic self-test features that elevate what has been a passive interlock into an active sensor node.

Micro Switch Industry Leaders

Omron Corporation

Honeywell International Inc.

Alps Alpine Co., Ltd.

TE Connectivity Ltd.

Panasonic Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Lagercrantz Group acquired Michael Smith Switchgear for USD 10.1 million, enhancing its UK industrial-automation footprint.

- April 2026: Renesas Electronics introduced the TP65B110HRU 650-V GaN switch for solar microinverters, achieving 98% efficiency at 200 kHz.

- March 2026: Electro Switch purchased E-MAX Instruments to add utility-sector monitoring and high-voltage disconnect expertise.

- February 2026: ZF’s Cherry division won the Plus X Award for its 6.5-mm WG sub-subminiature roller-lever switch, aimed at robotic grippers and medical interfaces.

Global Micro Switch Market Report Scope

The Micro Switch Market Report is Segmented by Switch Type (Standard Snap-Action, Subminiature, Ultraminiature, Limit-Switch Form-Factor, Sealed and Waterproof), Actuator Type (Plunger, Lever, Roller-Lever, Push-Button, Toggle and Custom), Current Rating (Up to 5 A, 6-10 A, 11-16 A, Above 16 A), End-User Industry (Home Appliances, Automotive, Industrial Automation, Medical Devices, Consumer Electronics, Other), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

| Standard (Snap-Action) Microswitches |

| Subminiature Microswitches |

| Ultraminiature Microswitches |

| Limit-Switch Form-Factor Microswitches |

| Sealed / Water-proof Microswitches |

| Plunger-Actuated |

| Lever-Actuated (Hinge, Simulated Roller) |

| Roller-Lever |

| Push-Button |

| Toggle and Custom Actuators |

| Up to 5 A |

| 6 - 10 A |

| 11 - 16 A |

| Above 16 A |

| Home Appliances |

| Automotive and Transportation |

| Industrial Automation and Machinery |

| Medical Devices and Instrumentation |

| Consumer Electronics |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Switch Type | Standard (Snap-Action) Microswitches | ||

| Subminiature Microswitches | |||

| Ultraminiature Microswitches | |||

| Limit-Switch Form-Factor Microswitches | |||

| Sealed / Water-proof Microswitches | |||

| By Actuator Type | Plunger-Actuated | ||

| Lever-Actuated (Hinge, Simulated Roller) | |||

| Roller-Lever | |||

| Push-Button | |||

| Toggle and Custom Actuators | |||

| By Current Rating | Up to 5 A | ||

| 6 - 10 A | |||

| 11 - 16 A | |||

| Above 16 A | |||

| By End-User Industry | Home Appliances | ||

| Automotive and Transportation | |||

| Industrial Automation and Machinery | |||

| Medical Devices and Instrumentation | |||

| Consumer Electronics | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current micro switch market size and where is it heading by 2031?

The micro switch market size stands at USD 0.83 billion in 2026 and is projected to reach USD 1.10 billion by 2031 at a 5.49% CAGR, according to figures compiled by Mordor Intelligence.

Which switch type is growing the fastest through 2031?

Sealed and waterproof variants are advancing at a 6.9% CAGR as renewable-energy and outdoor-equipment buyers seek IP67 durability, reports Mordor Intelligence.

Why are roller-lever actuators gaining popularity in factories?

Industrial retrofits favor roller-lever microswitches because their positive-opening action replaces bulky cam limit switches while simplifying IEC 61058 certification and saving panel space.

How is silver price volatility affecting microswitch producers?

Silver contacts make up more than 70% of material cost, and the 120% price spike in 2025 squeezed margins, prompting smaller manufacturers to consider lower-silver alloys that may shorten switch life.

What role do microswitches play in automotive safety architectures?

ISO 26262 ASIL-D systems pair mechanical microswitches with Hall sensors to achieve fault-diagnosis coverage above 90%, ensuring redundancy in brake pedals, steering columns, and seat-belt buckles.

Which regions offer the highest growth prospects for suppliers?

Asia-Pacific leads volume with a projected 6.1% CAGR through 2031, while North America and Europe deliver higher margins owing to stringent UL and IEC safety standards.

Page last updated on: