Smart Rings Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

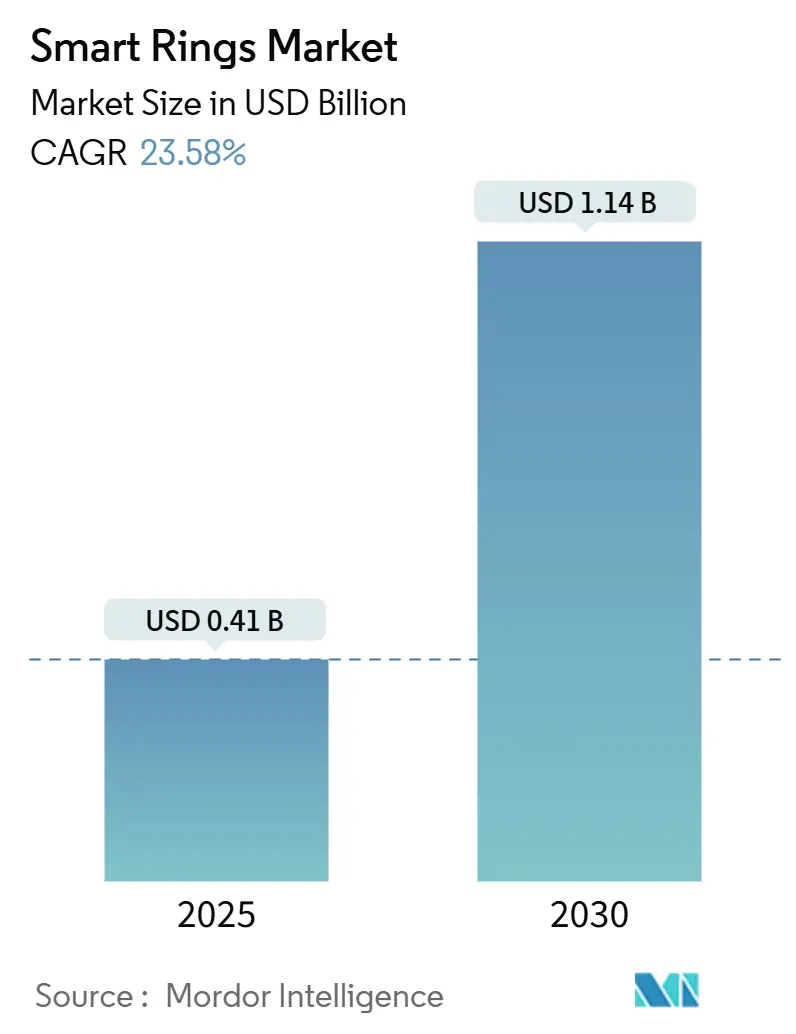

| Market Size (2025) | USD 0.41 Billion |

| Market Size (2030) | USD 1.14 Billion |

| Growth Rate (2025 - 2030) | 23.58% CAGR |

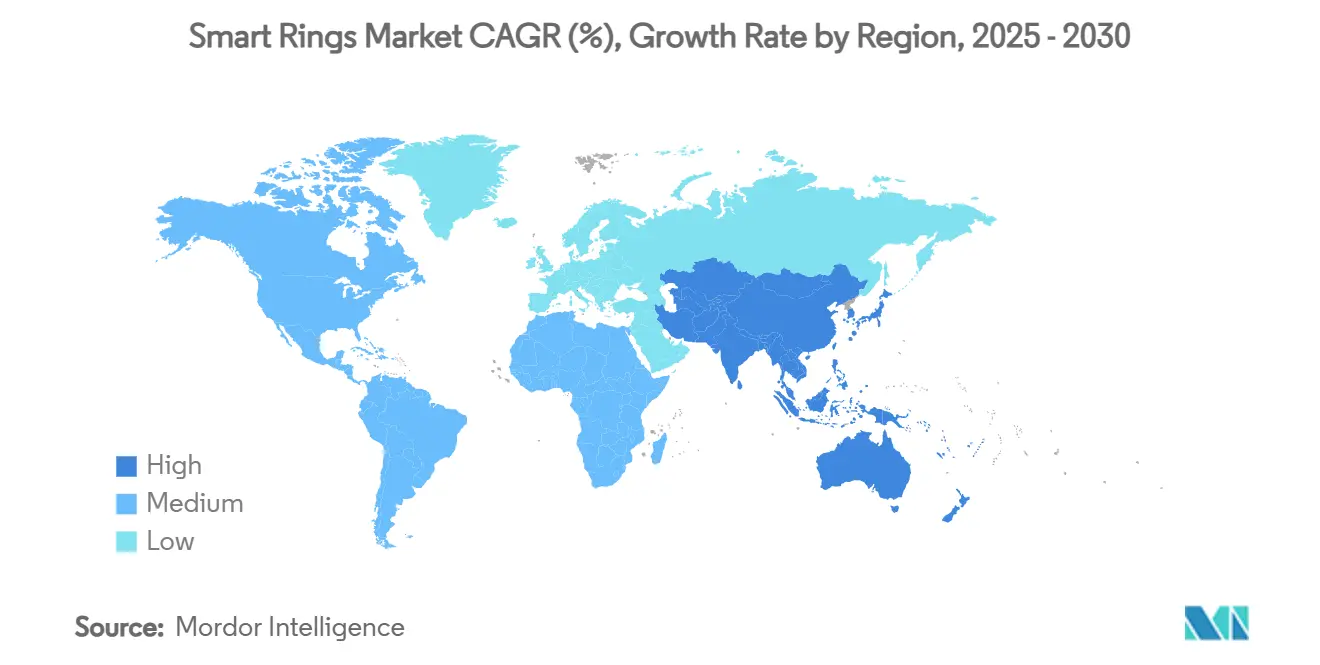

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Rings Market Analysis by Mordor Intelligence

The Smart Rings Market size is estimated at USD 0.41 billion in 2025, and is expected to reach USD 1.14 billion by 2030, at a CAGR of 23.58% during the forecast period (2025-2030).

Demand is fueled by the convergence of miniaturized sensors, rising consumer interest in continuous wellness tracking, and the preference for jewelry-like wearables that do not call attention in social or professional settings. Linked ring architectures currently dominate because they off-load computation to smartphones, unlocking richer analytics without compromising battery life. Institutional healthcare programs that distribute devices at no cost to patients are widening the addressable base, while premium launches such as 18-karat gold variants demonstrate an expanding value ladder. Competitive intensity will remain high as technology conglomerates blend proprietary ecosystems with aggressive intellectual-property defenses, forcing smaller firms to differentiate on specialized applications or pricing.

Key Report Takeaways

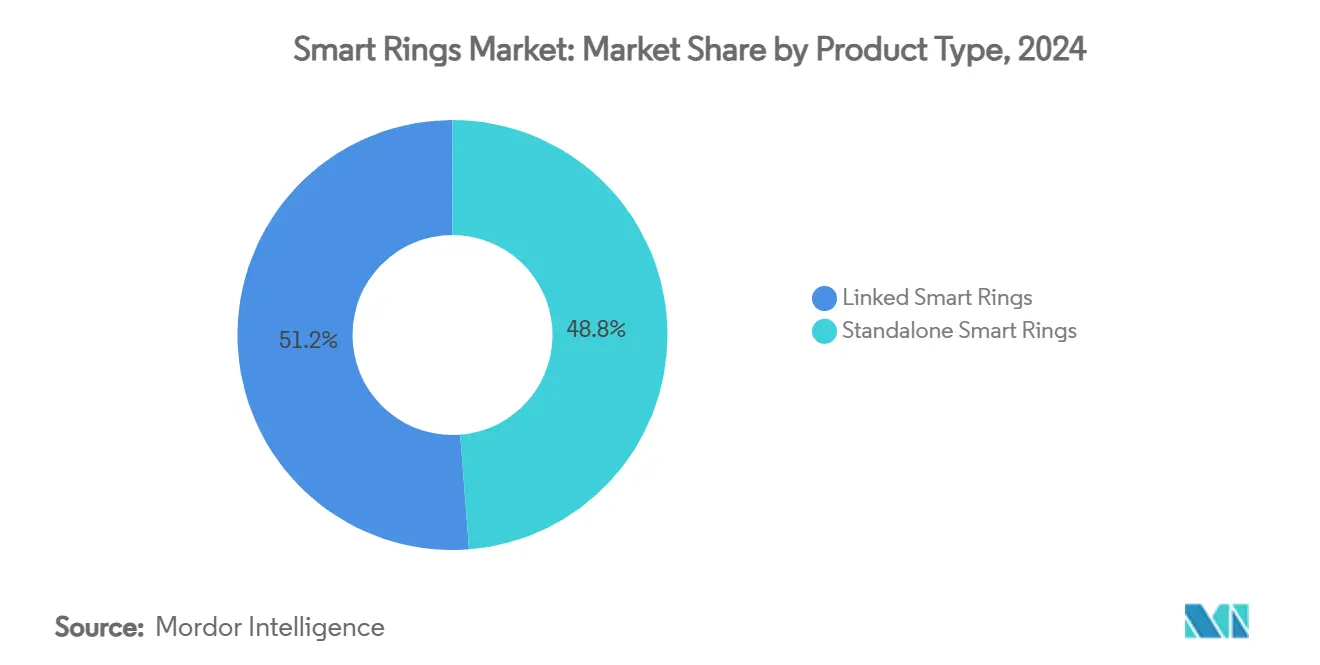

- By product type, Linked Smart Rings held 51.23% of the smart rings market share in 2024; Standalone Smart Rings are projected to expand at a 25.36% CAGR through 2030.

- By application, Sleep Monitoring captured 35.07% revenue share of the smart ring market in 2024; Female Health Tracking is forecast to accelerate at a 28.51% CAGR to 2030.

- By connectivity, Bluetooth Low Energy maintained 58.46% share of the smart ring market in 2024; Ultra-Wideband is advancing at a 30.06% CAGR as precision-tracking use cases mature.

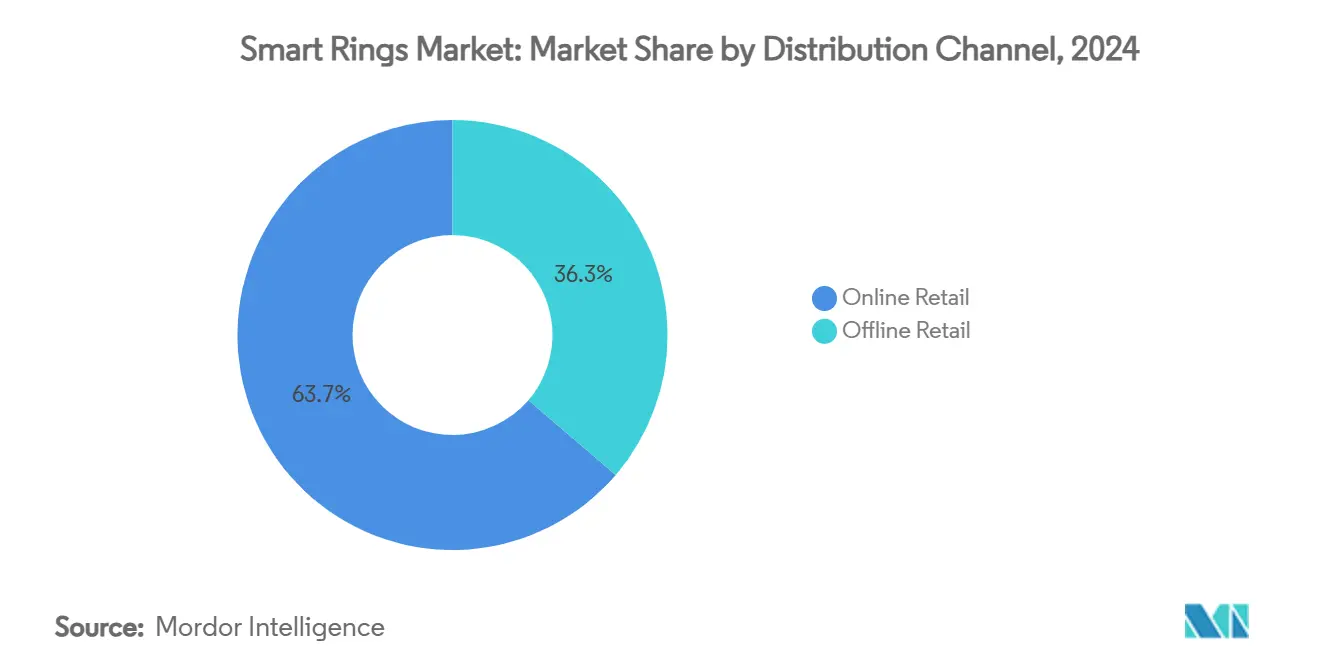

- By distribution channel, Online Retail accounted for 63.71% of the smart rings market size in 2024 and will continue growing at a 26.29% CAGR to 2030.

- By end user, Individual Consumers generated 65.06% of value in 2024; Healthcare Providers and Clinics represent the fastest-growing segment at a 25.84% CAGR.

- By geography, North America led with 38.67% revenue share in 2024; Asia-Pacific is poised for a 25.21% CAGR expansion to 2030.

Global Smart Rings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid miniaturisation of low-power sensors | +4.2% | Global, with concentration in Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Expanding health-insurance wellness programmes | +3.8% | North America & Europe, emerging in APAC | Short term (≤ 2 years) |

| Integration with digital IDs and contactless payments | +3.1% | Europe & Asia-Pacific leading, North America following | Medium term (2-4 years) |

| Surge in female-centric health tracking needs (fertility, menopause) | +2.9% | Global, with highest adoption in developed markets | Short term (≤ 2 years) |

| Growing preference for unobtrusive form factors over wrist wearables | +2.6% | Global, particularly in fashion-conscious demographics | Short term (≤ 2 years) |

| Adoption in professional sports for real-time biometrics | +1.8% | North America & Europe, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid miniaturization of low-power sensors

Research prototypes from the University of Waterloo demonstrate three-gram ring platforms combining photoplethysmography, accelerometry, and skin-temperature sensing—60% smaller than 2022 equivalents—without sacrificing 10-day battery autonomy.[1]Brandon B. et al., “Want a Noninvasive Health Monitor? Put a Ring on It,” TechXplore, techxplore.com These advances slash bill-of-materials costs and favor firms with deep semiconductor partnerships, exemplified by Samsung’s circuit-board collaboration with Meiko that tightens vertical integration. As the component count contracts, unit economics support mid-tier price points, broadening access beyond early adopters and lifting the smart rings market toward mainstream acceptance.

Expanding health-insurance wellness programs

Essence Healthcare distributes Oura Rings to Medicare Advantage members, signaling that insurers now view continuously collected behavioral data as actuarially accretive. Subsidized deployments remove upfront cost barriers, embed devices in care pathways, and create sticky data-analytics revenue streams for vendors. Government bodies follow suit; the U.S. Air Force adopted rings for aircrew performance monitoring, validating military-grade reliability requirements.

Integration with digital IDs and contactless payments

Infineon’s passive NFC chipsets power payment-enabled rings that need no battery, positioning the form factor as a successor to cards and phones in markets where contactless infrastructure is ubiquitous.[2]Infineon Technologies, “NFC Payment Ring,” infineon.com Mastercard-certified ring inlays from Digiseq shorten launch cycles for consumer brands, spawning lifestyle-driven adoption. As tokenization standards align across issuers, network effects will drive compounded uptake, especially in transit systems and event venues that prize frictionless access.

Surge in female-centric health tracking needs

Continuous core-temperature capture enables highly granular cycle prediction, an unmet clinical gap for the 1.9 billion women of reproductive age. Oura’s algorithm publishes period-start predictions with 95% accuracy, while academic prototypes now assay estradiol levels through sweat, edging toward medical-grade hormone analytics. Vendors that localize content and privacy controls for diverse cultural contexts will gain early-mover loyalty and premium pricing power.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short battery life and power-management limits | -2.8% | Global, particularly affecting standalone ring adoption | Short term (≤ 2 years) |

| Limited clinical validation hindering medical claims | -2.1% | North America & Europe with strict regulatory frameworks | Medium term (2-4 years) |

| Data-privacy and cybersecurity concerns | -1.9% | Europe & North America leading regulatory scrutiny | Medium term (2-4 years) |

| High ASP compared with smart-bands | -1.7% | Price-sensitive markets in APAC and emerging economies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Short battery life and power-management limits

Mainstream lithium-ion chemistries cap operating windows at under a week, interrupting longitudinal datasets and frustrating users who expect jewelry-like permanence. Every additional radio or sensor taxes the energy budget, forcing OEMs into feature-versus-endurance trade-offs.[3]Saft, “Providing Reliable Power along the IoT Value Chain,” saftbatteries.com Until solid-state batteries or RF energy-harvesting mature, marketing roadmaps must temper standalone ambitions.

Limited clinical validation hindering medical claims

In the smart ring market, Regulators require prospective trials for disease-management indications, yet many start-ups rely on retrospective datasets or consumer-grade accuracy. FDA clearances for pulse-oximetry and AFib in 2024 moved the bar, but full diagnostic labeling remains scarce, slowing payor reimbursement.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Linked Dominance Faces Standalone Challenge

Linked rings captured 51.23% of the smart rings market share in 2024, leveraging smartphone compute and cloud analytics for feature depth. This architecture minimizes on-board processing, stretches battery life, and fits within mid-tier pricing. The smart rings market size for linked solutions is forecast to increase at 21.4% CAGR as handset ecosystems in developing economies reach 90% penetration. Standalone models, however, register the highest 25.36% CAGR by removing phone dependence, a decisive benefit for athletes, field workers, and seniors. As ultra-low-power chipsets hit volume production, component overhead will shrink, narrowing the price delta and redistributing market power.

Linked devices also offer cross-selling synergies; Samsung preloads its Galaxy Health suite to lock users into its smartwatch-smartphone-earbuds stack, reinforcing platform stickiness. Standalone challengers counter with subscription-free propositions and niche health features such as ovulation tracking or on-finger ECG. Should battery density climb to 350 Wh/L, analysts expect standalone shipments to overtake linked units in Asia-Pacific by 2029, magnifying opportunities for brands unencumbered by smartphone compatibility constraints.

By Application: Sleep Monitoring Leads, Female Health Surges

Sleep Monitoring produced 35.07% of 2024 revenue, underpinned by the finger’s superior perfusion that yields cleaner nocturnal pulse signals than the wrist. The smart rings market size allocated to sleep analytics is projected to reach USD 0.40 billion by 2030, driven by employers that subsidize fatigue-reduction programs for shift workers. Conversely, Female Health Tracking posts a 28.51% CAGR, underlining its transformation from a “nice-to-have” feature to a standalone purchase driver. Fertility-focused millennials and perimenopausal cohorts alike view continuous temperature capture as a non-invasive alternative to lab work, encouraging pay-per-insight business models.

Vendors increasingly bundle incremental services-nutrition logging, glucose estimation, stress coaching-around the core sleep and female-health pillars to diversify revenue. Early adopters of tailored dashboards for obstetricians and endocrinologists may secure enterprise contracts that yield repeat-purchase lock-in, elevating lifetime value above direct-to-consumer churn rates.

By Connectivity Technology: BLE Dominance Challenged by UWB Innovation

Bluetooth Low Energy contributed 58.46% of 2024 shipments thanks to universal handset support, OTA firmware ease, and sub-1 mW idle draw. Yet Ultra-Wideband’s 30.06% CAGR illustrates a pivot toward spatial-computing interfaces. UWB-enabled rings control smart-home appliances through intuitive finger gestures with centimeter precision, a use case BLE cannot replicate. Once chipset prices fall below USD 3, analysts project UWB to eclipse NFC even for payments, as merchants value multi-purpose hardware that supports both transacting and presence-based personalization.

BLE remains indispensable for battery-sensitive health metrics; therefore, hybrid radios will become table stakes by 2027. Firmware orchestration that toggles radios intelligently will differentiate suppliers on endurance and latency, particularly in clinical telemetry.

By Distribution Channel: Online Retail Maintains Dominance

Two-thirds of 2024 revenue in the smart rings market flowed through direct websites and marketplaces, reflecting consumers’ need for sizing guides and rich content before purchase. The channel also affords OEMs higher gross margins and real-time demand analytics. Omnichannel leaders, however, are using pop-ups and electronics chains to capture impulse buyers; Best Buy launched end-cap displays with live biometrics demos to convert skeptical shoppers. By 2030, analysts expect a 60/40 split between online and offline as retail staff training matures and ring fitment kiosks reduce return rates. Overall online channel has maximum share with 63.71% along with highest growth rate of 26.29%.

By End User: Individual Consumers Drive Current Demand

Individual Consumers delivered 65.06% of 2024 sales, seeking wellness visibility and performance insights. Healthcare Providers and Clinics, though smaller today, chart the fastest 25.84% CAGR trajectory as telehealth reimbursement codes for continuous vitals expand in the United States and Europe. Device fleets provisioned to cardiac-rehab patients or metabolic-syndrome cohorts highlight an emerging B2B2C funnel that smooths cash-flow volatility and raises barriers to entry.

Corporate wellness programs procure rings in bulk to lower sick days, while defense and elite-sports clients validate robustness under extreme conditions. These institutional segments often mandate ISO-27001 data controls, raising switching costs once integration is complete.

Geography Analysis

North America anchored 38.67% of 2024 revenue in the smart rings market on the back of high average selling prices, mature digital-health reimbursement, and marquee sports sponsorships that amplify brand visibility. Device makers cultivate insurer alliances-Essence Healthcare offers rings to Medicare Advantage enrollees-to embed hardware within chronic-disease pathways, increasing replacement-cycle predictability. Legislative clarity around FDA device-software functions enhances investor confidence, drawing venture inflows that fund rapid firmware iteration.

Asia-Pacific logs the highest 25.21% CAGR in the smart rings market, with manufacturing scale in China and South Korea compressing BOMs and democratizing price points. Retail momentum in Japan, where Bic Camera expanded SOXAI Ring placement nationwide, confirms rising mainstream awareness. Concurrently, Chinese OEMs have released sub-USD 100 SKUs, forcing incumbents to delineate premium value or risk price erosion. The regional outlook brightens further as Samsung and Apple ready ecosystem-integrated offerings predicted to grow the addressable pool ten-fold.

Europe maintains steady double-digit growth underpinned by stringent GDPR safeguards that increase consumer trust in sharing intimate biometrics. Oura’s exclusive debut at John Lewis signaled a strategic push toward lifestyle positioning aligned with European fashion sensibilities. Widespread contactless payment infrastructure unlocks NFC ring use cases, while public-health authorities explore subsidized distribution to manage aging-population burdens.

Competitive Landscape

Oura Health retains brand leadership yet faces converging threats from conglomerates and agile start-ups. Its 100 granted and 270 pending patents undergird a defensive moat, evidenced by ongoing ITC litigation that seeks import bans on infringing products. Samsung’s preemptive lawsuit signals the scale of forthcoming legal jousts as tech titans assert cross-licensing leverage.

Strategic themes shaping the competitive field in the smart rings market include:

Ecosystem integration—Samsung bundles Smart-Things automations; Apple is rumored to link rings to Vision Pro gesture control.

Subscription economics—Oura’s USD 5.99 monthly tier competes with Ultrahuman’s no-fee model, prompting experimentation with tiered analytics.

Clinical validation—Movano and Happy Health secured FDA clearances for pulse-ox and AFib detection, positioning themselves for reimbursable pathways.

Premiumization—Ultrahuman’s 18-karat “Rare” line targets affluent niches at USD 1,830–2,196, signaling jewelry-category convergence.

Overall, top-five vendors account for roughly 55% of global revenue, suggesting a moderately concentrated landscape that still allows nimble entrants to find whitespace.

Smart Rings Industry Leaders

Oura Health Oy

Movano Inc.

Ultrahuman Healthcare Pvt. Ltd.

Circular SAS

McLear Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Ultrahuman introduced its 18-karat ‘Rare’ smart-ring series, aiming to capture luxury discretionary spending and diversify margins beyond subscription analytics.

- May 2025: Oura added AI-driven ‘Meals’ and ‘Glucose’ tracking, pushing into holistic metabolic management that raises customer stickiness across health domains.

- May 2025: Tangem secured a U.S. patent for a blockchain-enabled ring, signaling diversification of the smart rings market toward digital-asset custody and new revenue verticals.

- April 2025: Oura rolled out an AI assistant that contextualizes user metrics, a move to defend ARPU as hardware commoditizes.

Global Smart Rings Market Report Scope

| Standalone Smart Rings |

| Linked Smart Rings |

| Sleep Monitoring |

| Fitness and Wellness Tracking |

| Contactless Payments |

| Access Control and Security |

| Notification and Communication |

| Bluetooth Low Energy (BLE) |

| Near-Field Communication (NFC) |

| Ultra-Wideband (UWB) |

| Wi-Fi |

| Online Retail |

| Offline Retail (Consumer Electronics Stores) |

| Individual Consumers |

| Corporate and Enterprise Wellness Programs |

| Healthcare Providers and Clinics |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Product Type | Standalone Smart Rings | ||

| Linked Smart Rings | |||

| By Application | Sleep Monitoring | ||

| Fitness and Wellness Tracking | |||

| Contactless Payments | |||

| Access Control and Security | |||

| Notification and Communication | |||

| By Connectivity Technology | Bluetooth Low Energy (BLE) | ||

| Near-Field Communication (NFC) | |||

| Ultra-Wideband (UWB) | |||

| Wi-Fi | |||

| By Distribution Channel | Online Retail | ||

| Offline Retail (Consumer Electronics Stores) | |||

| By End User | Individual Consumers | ||

| Corporate and Enterprise Wellness Programs | |||

| Healthcare Providers and Clinics | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Colombia | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2025 valuation of the smart rings market?

The smart rings market size stands at USD 0.41 billion in 2025.

Which segment is expanding the fastest?

Standalone Smart Rings exhibit the highest growth at a 25.36% CAGR through 2030.

Why are insurers distributing smart rings?

Payers see continuous biometric data as a cost-effective tool for preventive care, reducing hospitalization expenses.

How long do current smart rings last on a single charge?

Lithium-ion models run 3–7 days, with R&D focused on solid-state or energy-harvesting alternatives.

Which region shows the strongest growth outlook?

Asia-Pacific leads with a projected 25.21% CAGR, buoyed by manufacturing scale and rising health awareness.

Are smart rings medically approved?

Several models have received FDA clearances for pulse-oximetry or AFib detection, though full diagnostic claims remain limited.

Page last updated on: