Hardware Loop Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

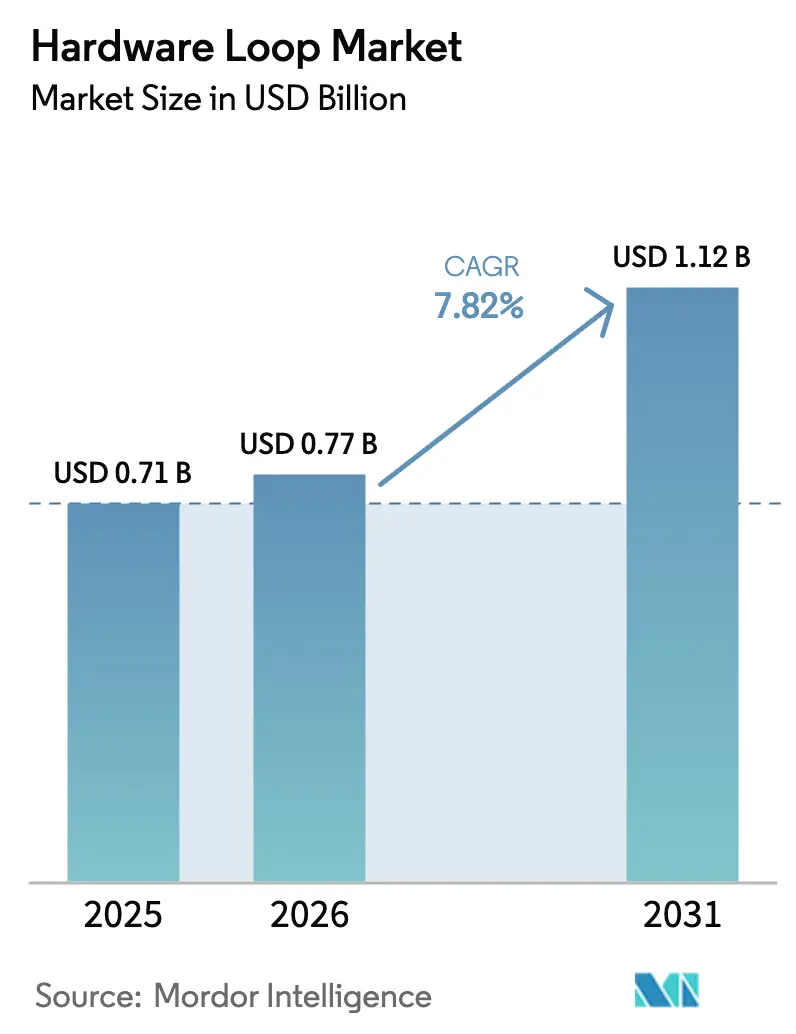

| Market Size (2026) | USD 0.77 Billion |

| Market Size (2031) | USD 1.12 Billion |

| Growth Rate (2026 - 2031) | 7.82% CAGR |

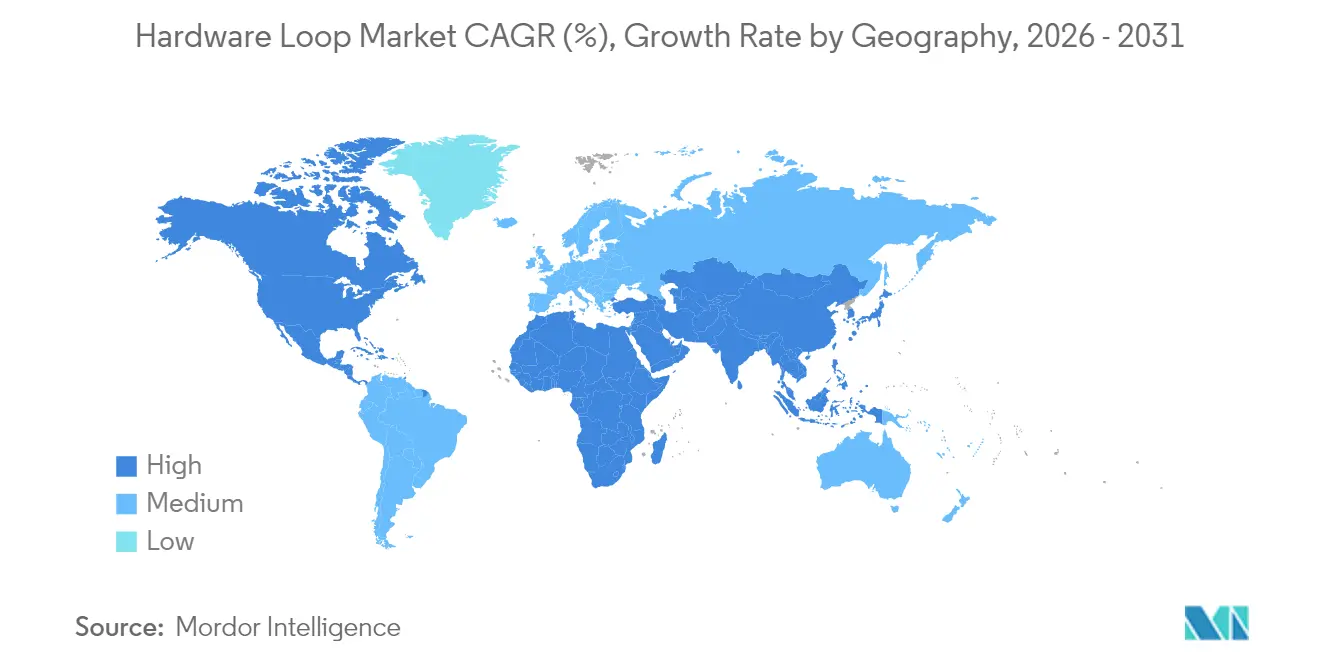

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

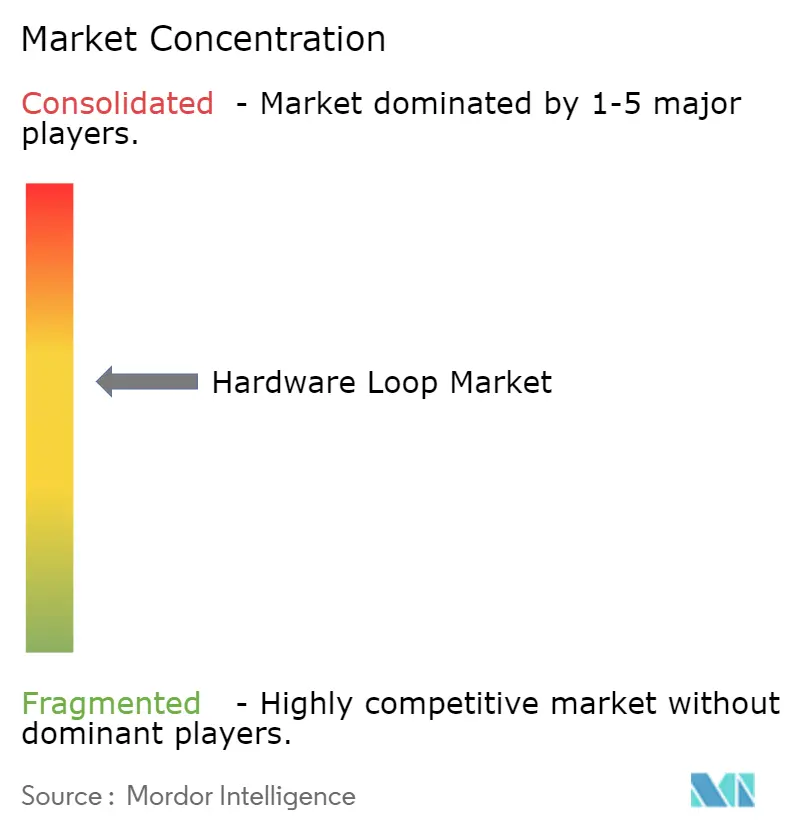

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hardware Loop Market Analysis by Mordor Intelligence

hardware loop market size in 2026 is estimated at USD 0.77 billion, growing from 2025 value of USD 0.71 billion with 2031 projections showing USD 1.12 billion, growing at 7.82% CAGR over 2026-2031. Growth stems from tightening functional-safety demands in automotive electronics, the shift to wide-bandgap power devices and the need for real-time embedded-system validation before physical rollout.[1]National Instruments, “Automotive Hardware-in-the-Loop (HIL) Test,” ni.com Europe’s vehicle OEM and tier-1 ecosystem, Asia’s manufacturing scale-up and North America’s OTA compliance push are converging to widen adoption. Suppliers are differentiating through high-fidelity solvers, cloud-delivered HIL-as-a-Service and middleware that knits together previously siloed tool chains. Service revenue outpaces hardware as integrators, trainers and managed-test providers plug the engineering-talent gap. Capital intensity for MHz-range FPGA rigs and the scarcity of real-time processor specialists temper momentum but have catalysed pay-per-use models and low-entry-cost starter kits.

Key Report Takeaways

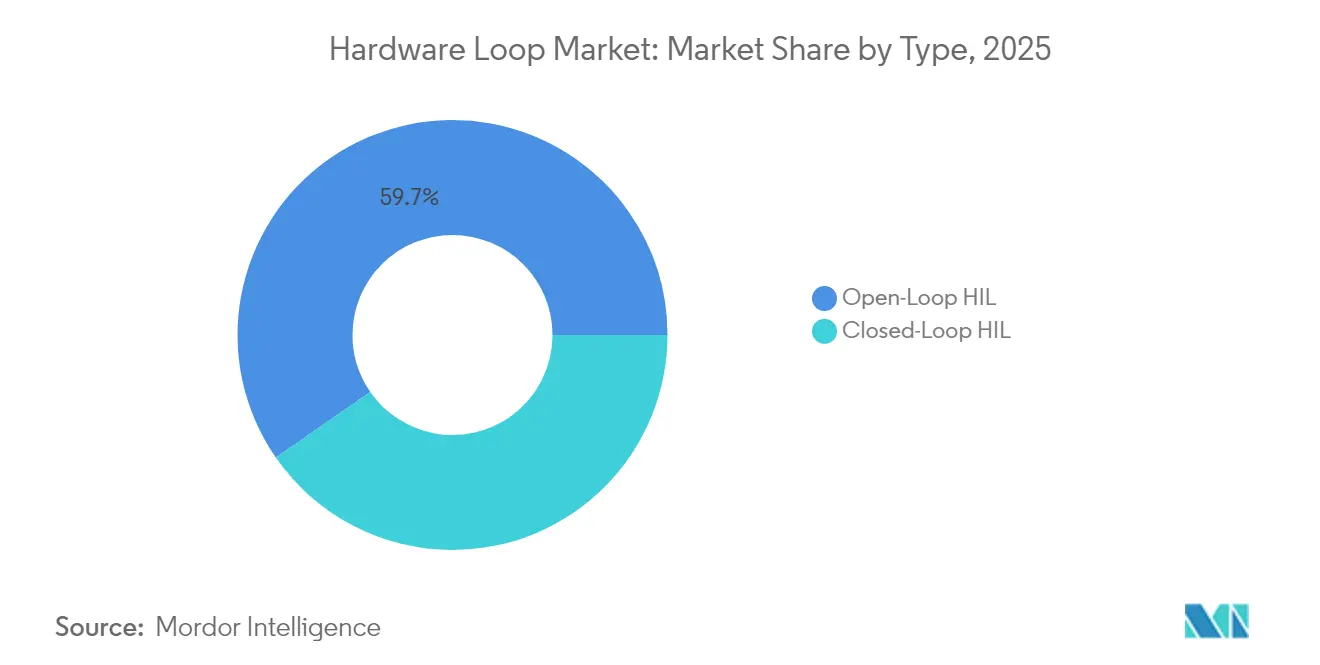

- By type, Open-Loop systems held 59.65% of the hardware loop market share in 2025; Closed-Loop solutions are projected to expand at an 8.04% CAGR to 2031.

- By component, hardware commanded 54.35% of the hardware loop market size in 2025, while services post the fastest 9.73% CAGR through 2031.

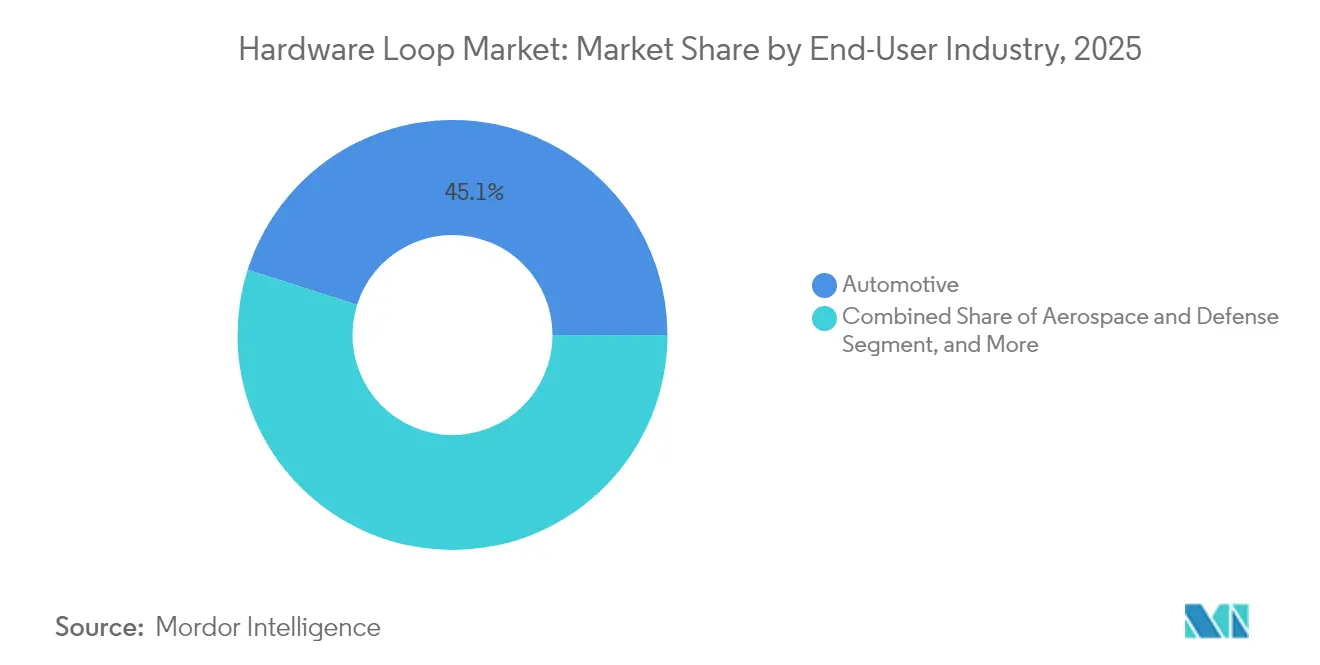

- By end-user, automotive led with 45.10% revenue share in 2025; energy & power is forecast to grow 9.28% annually to 2031.

- By model complexity, mid-fidelity rigs captured 48.25% in 2025; high-fidelity platforms are the fastest riser at 9.44% CAGR to 2031.

- By geography, Europe dominated with 31.95% revenue share in 2025 on the back of stringent safety mandates and dense OEM clusters.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hardware Loop Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV high-voltage e-powertrain validation needs | +2.1% | Europe, spillover to North America & Asia-Pacific | Medium term (2-4 years) |

| OTA software-update compliance testing surge | +1.8% | North America, growing in Europe | Short term (≤2 years) |

| Safety-critical ADAS/AD regulatory mandates | +1.6% | Asia & Europe | Medium term (2-4 years) |

| Rapid adoption of power-electronics SiC/GaN modules | +1.4% | Global, initial Asia-Pacific | Medium term (2-4 years) |

| Rise of digital twins in industrial equipment | +1.2% | Nordics & DACH, global spread | Long term (≥4 years) |

| Renewable-microgrid controller optimisation | +0.9% | Middle East, rising Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

EV High-Voltage e-Powertrain Validation Needs

Premium EV platforms increasingly operate at 800 V, exposing legacy test benches to arc-flash and thermal-runaway risks. European OEMs therefore deploy multi-channel HIL rigs that blend battery, inverter and motor models to stress controllers in real-time with fault injection. Nanosecond-level switching and electro-thermal coupling require FPGA-accelerated solvers, a capability smaller suppliers now commercialise to gain share. As e-axle, on-board charger and bidirectional-V2G features proliferate, the hardware loop market will secure long-tail volume from tier-1 propulsion specialists

OTA Software-Update Compliance Testing Surge

North American rule-making obliges manufacturers to prove that remote patches neither degrade safety nor expose cybersecurity gaps. Valeo’s cloud-native HILaaS lets software teams replay thousands of update permutations across virtualised ECUs with deterministic latency.[2]Valeo, “Valeo Partners with AWS to Transform Software-Defined Vehicle Development,” stocktitan.net This hosted approach trims capex and helps offset the shortage of FPGA programmers. Europe is building similar schemes as UNECE type-approval evolves, elevating test-case breadth and driving recurring-revenue streams for platform vendors.

Safety-Critical ADAS/AD Regulatory Mandates

UNECE’s Global Technical Regulation on ADS weaves simulation, test-track and public-road results into a multi-pillar validation stack.[3]United Nations Economic Commission for Europe, “Global Technical Regulation on Automated Driving System,” unece.org HIL anchors the stack by letting engineers inject synthetic sensor feeds, spoof GNSS data and model edge-case physics that would be unsafe in traffic. Implementation costs have pushed OEMs to partner with domain-specific test houses, enlarging the services slice of the hardware loop market.

Rapid Adoption of Power-Electronics SiC/GaN Modules

SiC traction inverters and GaN chargers switch in the MHz domain, overwhelming legacy CPU-based benches. Suppliers such as Plexim launched 5 ns-resolution solvers that allow converter startups to debug control loops without burning devices. Demand originates in Asia-Pacific where consumer-electronics fast chargers and solar inverters crest first, before scaling worldwide.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of Real-Time Processor Talent for HIL Integration | -1.2% | Global, with acute impact in North America and Europe | Medium term (2-4 years) |

| Capital-Intensive FPGA-Based Systems for MHz-Range Switching | -0.9% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Reliability Concerns in Ultra-High-Voltage (>1 kV) Emulation | -0.7% | Global, with particular focus on automotive and energy sectors | Medium term (2-4 years) |

| Fragmented Vendor Tool-Chain Interoperability | -0.5% | Global, with higher impact in multi-vendor environments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Scarcity of Real-Time Processor Talent for HIL Integration

Vacancies demanding FPGA design, deterministic-OS tuning and multi-domain modelling outstrip the talent pipeline. Vendors embed drag-and-drop GUIs and AI-assisted auto-coding to flatten learning curves, but complex-physics cases still need deep expertise. Universities are partnering with suppliers to seed competence yet the gap will persist mid-term, delaying project start-ups and elongating sales cycles within the hardware loop market

Capital-Intensive FPGA-Based Systems for MHz-Range Switching

High-end benches exceed USD 0.5 million once amplifiers, racks and licences compile, deterring SMEs in emerging economies. Pay-as-you-go cloud benches ease entry but security and latency questions limit their use for power-stage hardware couplings. Cost-down road-maps around off-the-shelf SoC FPGAs and modular amplifiers could neutralise the restraint in the next two years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Closed-Loop HIL Gaining Momentum

Open-loop benches controlled 59.65% of the hardware loop market in 2025 thanks to simplicity and lower entry cost. They suit early software sanity checks where feedback is unnecessary. Closed-loop platforms, while smaller, are expanding at an 8.04% CAGR as autonomous-driving, aerospace flight-control and high-frequency power-electronics projects demand bidirectional dynamics. The hardware loop market size allocated to closed-loop rigs is projected to climb steadily because digital-twin co-simulation now feeds plant-level states back into the ECU, heightening realism.

Wider adoption flows from tool-chain maturity and declining FPGA card prices. Case studies in hybrid-vehicle energy-flow validation proved ≤2% deviation from track data, convincing OEM quality boards to migrate from pure simulation to closed-loop benches. As vehicle zonal architectures converge diverse sensors and actuators onto consolidated controllers, closed-loop rigs allow entire subnetworks to be validated in unison, strengthening functional-safety dossiers.

By Component: Services Sector Experiencing Rapid Growth

Hardware-encompassing I/O, signal conditioning and compute engines-retained 54.35% of 2025 revenue. Heavy capex for multi-MHz amplifiers cements its lead. Yet services are compounding at 9.73% as integrators weave benches into DevOps pipelines, cloud orchestration and cybersecurity workflows. Scarcity of domain engineers pulls enterprises toward turnkey HIL-as-a-Service, typified by Valeo’s AWS-hosted lab that outsources regression runs overnigh.

Training demand spikes when new solvers arrive; supplier academies now bundle certification paths to shorten onboarding. Managed maintenance contracts guarantee deterministic latency across software upgrades, converting one-off licence sales into recurring revenue. Consequently, the hardware loop market size tied to services will likely outstrip physical-box growth beyond 2027.

By End-User Industry: Energy and Power Sector Surging

Automotive owned 45.10% of hardware loop market share in 2025 due to ADAS and electrification complexity. Aerospace & defense follow with fly-by-wire and radar validation workloads. Energy & power, although smaller, is accelerating at 9.28% CAGR as utilities digitalise substations and roll out microgrids. Renewable intermittency forces EMS algorithms to coordinate PV, wind and storage in real time; HIL benches stress-test these controllers against grid-code contingencies, trimming commissioning risk.

A study posting 58% summer and 50% winter OPEX savings by optimising microgrid control after HIL validation unlocked budget to scale projects. Coupled with policy incentives, this result swings procurement towards high-fidelity rigs that ingest electromagnetic transient models. The hardware loop industry thus finds a fresh addressable pool outside automotive.

By Model Complexity: High-Fidelity Systems Show Strong Growth

Mid-fidelity benches, balancing detail and cost, managed 48.25% of 2025 revenue. They decode system-level interactions adequately for many embedded targets. Low-fidelity rigs persist for early code bring-up. High-fidelity platforms, however, register the steepest 9.44% CAGR as SiC/GaN converters, megawatt-class drives and grid-forming inverters need nanosecond-accurate transient capture. The hardware loop market size tied to plant-level benches will therefore widen, though CAPEX hurdles remain.

Vendors leverage SoC FPGAs and real-time Linux patches to compress bill-of-material while lifting solver cell counts. Academic-industry consortia prototype MW-scale motor-generator interfaces that maintain phase lock within 0.1° under load steps, meeting grid-code thresholds and validating high-fidelity’s value proposition.

Geography Analysis

Europe retained 31.95% of global revenue in 2025, underpinned by Euro NCAP-driven safety upgrades, strong tier-1 clusters and EU CCAM road-maps that mandate robust validation. National grants bankroll pilot lines integrating HIL with over-the-air testflows, benefitting suppliers headquartered in Germany and France. High-voltage EV adoption ensures steady demand for battery-thermal and inverter benches, while aerospace primes lift orders for flight-control simulators.

North America ranks second. Federal funding into connected-vehicle simulation and stringent OTA cybersecurity rules propel bench utilisation. Cloud hyperscalers, already dominant in enterprise IT, now co-develop low-latency streaming protocols for HIL, reinforcing the region’s tilt toward service-led consumption. Defense primes broaden use cases to hypersonic system validation, securing multi-year framework contracts that stabilise supplier revenue.

Asia-Pacific posts the fastest 8.12% CAGR. China’s EV export surge, Japan’s robotics leadership and South Korea’s semiconductor depth energise demand. Policymakers back cross-border AV pilot zones, obliging common safety-validation toolchains. Indigenous vendors grow rapidly on price-optimised FPGA cards, yet global brands maintain lead in ultra-high-fidelity niches. Emerging South-East Asian plants, eager for Industry 4.0 maturity, adopt starter HIL kits bundled with cloud dashboards, widening the customer base across SME tiers.

Competitive Landscape

The segment is moderately concentrated; dSPACE, National Instruments and MathWorks occupy strong positions across Europe and North America, while OPAL-RT and RTDS excel in power-system niches. Strategic alliances shape differentiation: Rohde & Schwarz paired with IPG Automotive to overlay radar-HIL into scenario simulators, raising entry barriers. Suppliers introduce orchestration middleware that glues SIL, HIL and PHIL stages into a single CI/CD pipeline, a critical feature for software-defined vehicle programmes.

Cloud-delivery disrupts traditional box sales. Valeo’s AWS offering and OPAL-RT’s PHIL Prime service showcase subscription economics that lower adoption thresholds yet lock customers into vendor ecosystems. Talent shortages spur integrators to wrap turnkey delivery, moving competition from hardware spec sheets to service quality.

New entrants counterpose niche excellence: FPGA-solver houses commercialise 5 ns time-steps, GNSS-specialist aiMotive fuses sat-nav spoofing with drive-train HIL, and Plexim’s Nanostep widens designer reach. Consolidation remains plausible as larger players acquire solver IP or service firms to fill portfolio gaps and secure share in the growing hardware loop market.

Hardware Loop Industry Leaders

The MathWorks, Inc.

dSPACE GmbH

ETAS

Vector Informatik GmbH

Qualcomm Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: OPAL-RT Technologies unveiled the PHIL Prime Test Bench for renewable-energy applications.

- April 2025: Rohde & Schwarz and IPG Automotive launched an integrated radar HIL solution.

- March 2025: Advantech debuted an NVIDIA-powered HIL server for precision-navigation systems.

- January 2025: Valeo and AWS introduced HILaaS for software-defined vehicles

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the hardware-in-the-loop market as all commercial platforms that couple real-time simulation computers with physical input-output interfaces to validate embedded control software across automotive, aerospace, power, and industrial systems. The model includes open-loop and closed-loop rigs, associated real-time processors, signal conditioning cards, and system-level integration services that ship as a bundled solution.

Scope exclusion: pure software-only model-in-the-loop tools and generic test benches that lack real-time co-simulation capability were set outside this assessment.

Segmentation Overview

- By Type

- Open-Loop HIL

- Closed-Loop HIL

- By Component

- Hardware (Signal Conditioning, Power Stage, FPGA/CPU, I/O)

- Software (Real-Time OS, Modeling Tools, Visualization)

- Services (Integration, Training, Maintenance)

- By End-User Industry

- Automotive

- Aerospace and Defense

- Electronics and Semiconductor

- Industrial Equipment and Robotics

- Energy and Power (Renewables, Micro-grids)

- Research and Education

- By Model Complexity

- Low-Fidelity (Controller-Level)

- Mid-Fidelity (System-Level)

- High-Fidelity (Plant-Level with Power Stage)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- South East Asia

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- GCC

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with HIL bench engineers at OEMs, test-system architects at Tier-1 suppliers, and regional instrumentation distributors provided insight on average channel margins, capacity utilization, and procurement cycles across North America, Europe, and Asia-Pacific. Follow-up surveys with certification consultants and academic labs helped us stress-test assumption ranges for model complexity migration from mid- to high-fidelity rigs.

Desk Research

Mordor analysts started with public domain building blocks such as United Nations Comtrade shipment codes for real-time simulation chassis, SAE and ISO standards on functional-safety testing, and Eurostat data on electric-vehicle production. Industry guidance from bodies such as the International Council on Systems Engineering, national aviation authorities, and the U.S. Energy Information Administration helped us map end-use intensity trends. Company 10-Ks and investor decks supplied hardware revenue splits, while news archives within Dow Jones Factiva and component bills from D&B Hoovers clarified competitive footprints.

Trade association white papers on autonomous mobility, patent families queried through Questel, and customs import manifests from Volza sharpened volume estimates and ASP corridors. The sources named above are illustrative; many additional references informed data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down reconstruction drew on production counts of electric vehicles, flight-control computers, and megawatt power converters, which are then tempered by HIL penetration rates derived from interviews. Select bottom-up roll-ups of chassis shipments from leading vendors acted as reasonableness checks before totals were locked. Key variables like average selling price per rack, annual test-rig refresh interval, regulatory homologation volumes, digital-twin adoption rate, and capital-expenditure share of R&D budgets drive our multivariate regression forecast. Where supplier data were partial, interpolation against three-year moving averages filled gaps and was flagged for additional verification.

Data Validation & Update Cycle

Outputs pass a two-level analyst peer review, followed by variance screening against independent indicators such as semiconductor real-time-clock sales and ISO 26262 homologation filings. The model is refreshed yearly, and an interim update is triggered if material events, major emission mandates or breakthrough processor launches, shift demand fundamentals. A final pre-publication sweep ensures clients receive the current validated view.

Why Mordor's Hardware Loop Baseline Commands Confidence

Estimates published across research houses rarely align because each author chooses unique scope lines, currency bases, and refresh cadences. Understanding these levers is essential before relying on any number for investment planning.

Key gap drivers stem from how some studies bundle generic automation benches, apply uniform ASP inflation, or project growth off historical CAGR trendlines without checking real-time adoption signals. Our disciplined inclusion logic, annual refresh, and dual-path validation make Mordor's 2025 value of USD 0.71 billion the dependable midpoint.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.71 bn (2025) | Mordor Intelligence | |

| USD 1.00 bn (2024) | Global Consultancy A | Bundles generic test benches and software-only tools |

| USD 0.95 bn (2024) | Industry Data Firm B | Uses static 15% ASP uplift across forecast, limited primary validation |

| USD 0.74 bn (2024) | Regional Consultancy C | Excludes power-electronics rigs, extrapolates from North America sample only |

In summary, while figures differ, our balanced mix of public statistics, expert insight, and iterative cross-checks gives decision-makers a transparent, reproducible grounding that stands up to scrutiny and remains responsive to market shifts.

Key Questions Answered in the Report

What is driving demand in the hardware loop market?

Rising functional-safety mandates, high-voltage EV systems, OTA-update compliance and the use of SiC/GaN power devices are elevating real-time validation needs, pushing enterprises toward sophisticated HIL benches.

Which region currently leads hardware loop adoption?

Europe holds 31.95% of 2025 revenue, buoyed by stringent vehicle-safety rules and a dense network of automotive OEMs and tier-1 suppliers.

Why are services growing faster than hardware sales?

Integration complexity and the shortage of real-time-processor experts lift demand for training, managed testing and cloud HIL-as-a-Service, resulting in a 9.73% CAGR for the services component segment.

How are wide-bandgap semiconductors affecting HIL requirements?

SiC and GaN devices switch at MHz frequencies, necessitating FPGA-based benches with nanosecond-resolution solvers to model high-speed power-electronics behaviour accurately.

What limits wider hardware loop adoption?

Capital-intensive FPGA rigs and a global talent shortage in deterministic real-time system design are primary restraints, especially for SMEs and emerging-market users.

Which end-user segment offers the fastest growth?

The energy and power sector is expanding at 9.28% annually as microgrid and renewable-integration projects rely on HIL to validate complex controller interactions before field deployment.

What is the forecast value for the hardware loop market in 2031?

The hardware loop market is forecast to reach USD 1.12 billion by 2031, translating into a 7.82% CAGR

Page last updated on: