Micro And Nano PLC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

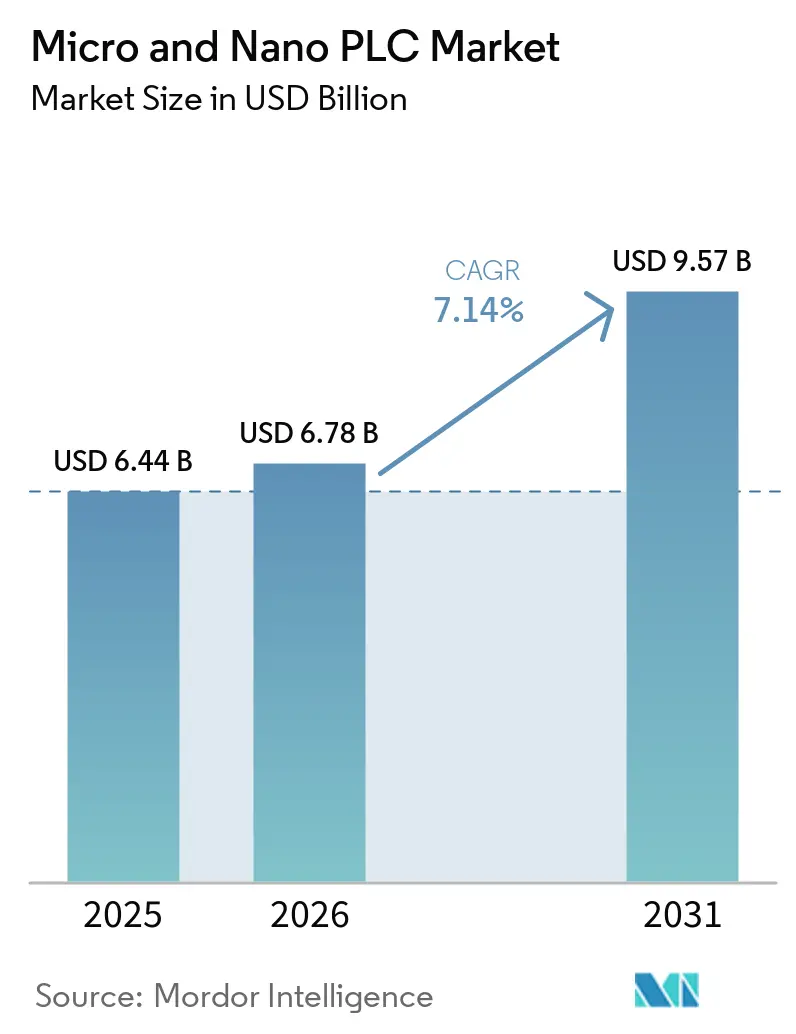

| Market Size (2026) | USD 6.78 Billion |

| Market Size (2031) | USD 9.57 Billion |

| Growth Rate (2026 - 2031) | 7.14% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Micro And Nano PLC Market Analysis by Mordor Intelligence

The micro and nano PLC market size is expected to grow from USD 6.44 billion in 2025 to USD 6.78 billion in 2026 and is forecast to reach USD 9.57 billion by 2031 at 7.14% CAGR over 2026-2031. The micro and nano PLC market is benefiting from a steady shift away from relay-based control in small standalone machines, where compact programmable control improves flexibility without adding major panel complexity. The same hardware is also being used as an entry point for plant connectivity, which gives the micro and nano PLC market a broader role in automation projects than simple machine logic alone. Demand remains strongest where machine footprints are tight, engineering teams are lean, and users want practical upgrades rather than full control system replacement. Competitive pressure is rising because premium global brands are expanding software and cybersecurity features while lower-cost suppliers are tightening pricing in entry-level configurations. Vendors that combine secure architectures, open programming environments, and easier brownfield integration are positioned to win more of the micro and nano PLC market through 2031.

Key Report Takeaways

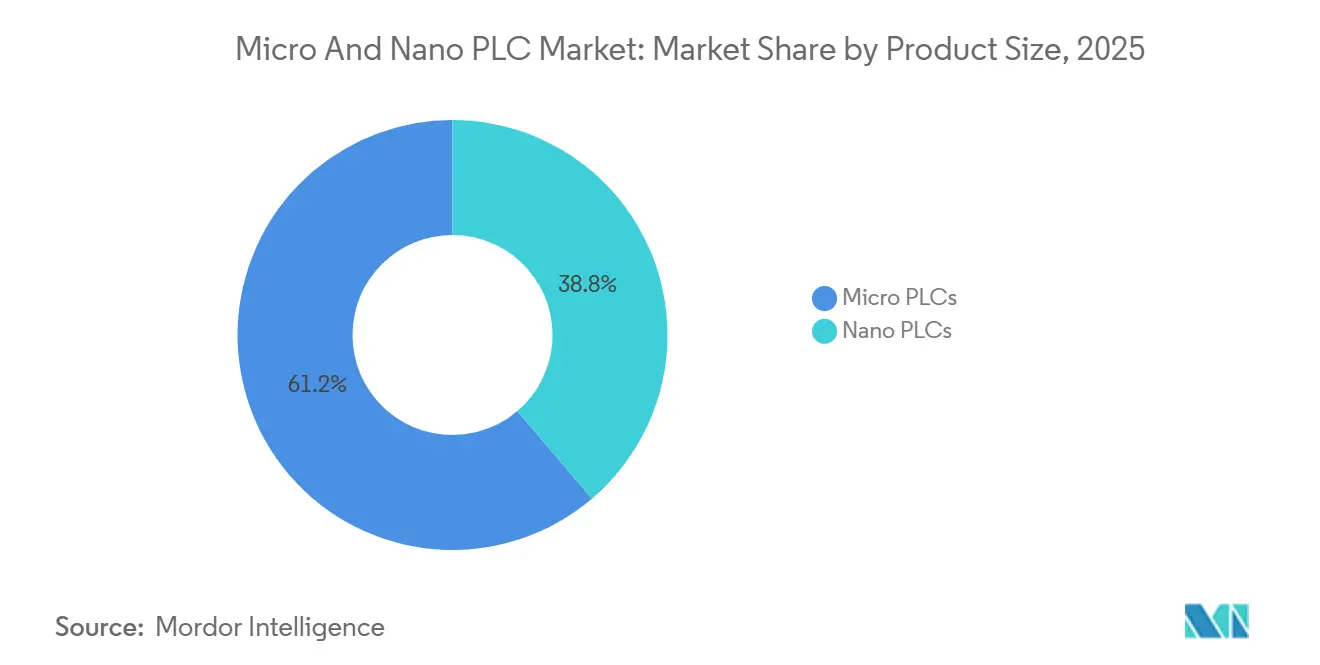

- By product size, micro PLCs led with a 61.23% revenue share of the micro and nano PLC market in 2025, while nano PLCs are projected to record the fastest growth at a 7.91% CAGR through 2031.

- By offering, hardware remained the largest segment with 69.38% share of the micro and nano PLC market in 2025, while software is forecast to grow at a 7.87% CAGR through 2031.

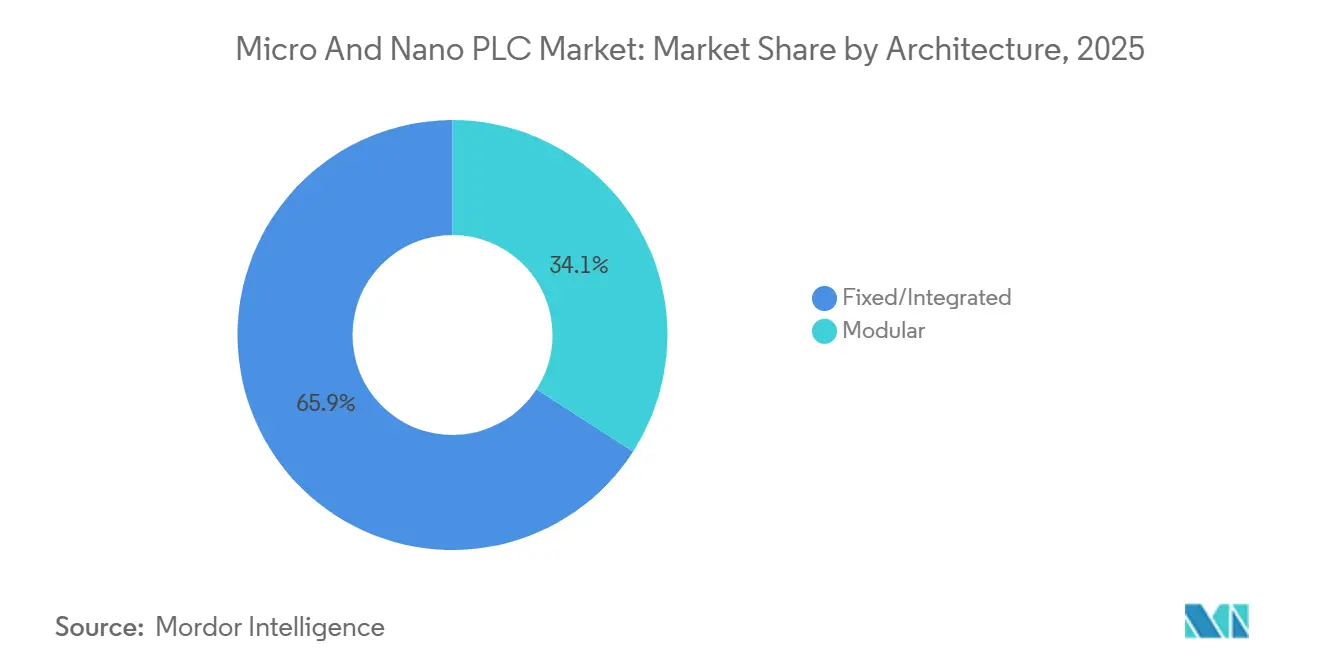

- By architecture, fixed/integrated platforms held 65.89% share of the micro and nano PLC market in 2025, while modular architectures are forecast to expand at an 8.12% CAGR through 2031.

- By end-user industry, automotive and transportation accounted for 22.78% of revenues in 2025, while the semiconductors and electronics segment is projected to grow the fastest at a 7.96% CAGR through 2031.

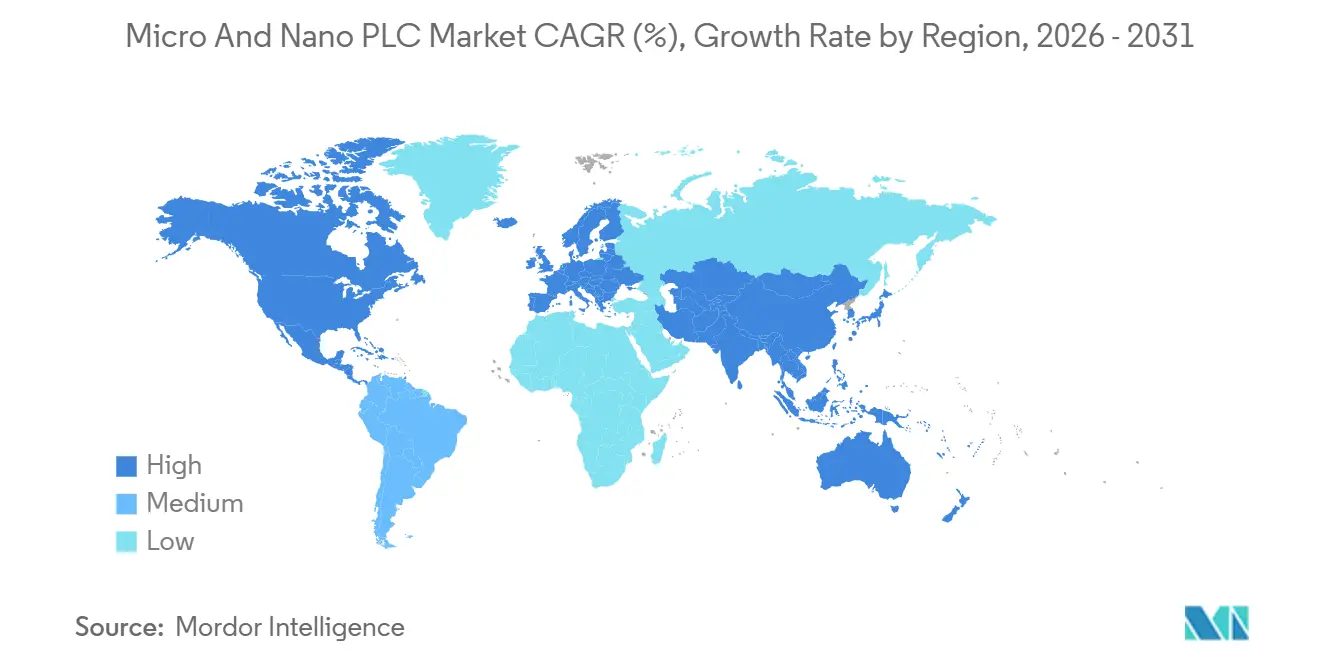

- By geography, Asia-Pacific accounted for 46.34% of total micro and nano PLC market revenues in 2025 and is also expected to post the fastest regional growth at a 7.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Micro And Nano PLC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SME Factory Automation in Asia-Pacific | +1.8% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| IIoT and Edge Connectivity in Compact Controllers | +1.5% | North America, EU, APAC | Long term (≥ 4 years) |

| Demand for Space-Saving Integrated Control in OEM Machines | +1.2% | Global | Short term (≤ 2 years) |

| Semiconductor and Electronics Capacity Additions | +0.9% | APAC, North America | Medium term (2-4 years) |

| Cyber-Ready Controller Replacement Cycle in Europe | +0.7% | EU, North America | Medium term (2-4 years) |

| Electrified Mobile and Off-Highway Equipment Controls | +0.6% | North America, EU, APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

SME Factory Automation in Asia-Pacific

Asia-Pacific remains the strongest volume engine for the micro and nano PLC market because automation demand is spreading deeper into smaller factories rather than staying concentrated in large industrial sites. A visible part of this shift is the wider use of compact controllers by small and mid-sized machine builders that need low-cost logic, faster commissioning, and easier operator training. In Japan, established compact controller lines such as Keyence KV Nano and JTEKT TOYOPUC-Nano show how tightly packaged products are being built for high-cycle and precision-oriented OEM environments, which continues to influence neighboring Asian integrators and equipment suppliers.[1]Keyence Corporation, “KV Nano Series Programmable Controller,” Keyence Corporation, keyence.co.jp. JEMA’s 2025 user survey also points to durable PLC adoption across precision machining and electronics equipment OEM applications in Japan, which supports the broader regional case for compact control investment. As a result, the micro and nano PLC market in Asia-Pacific is becoming more competitive on software familiarity, service support, and ecosystem fit, not only on upfront hardware pricing.

IIoT and Edge Connectivity in Compact Controllers

The micro and nano PLC market is gaining from controllers that now handle deterministic machine logic and local data movement in the same compact unit. This reduces the bill of materials, simplifies cabinet design, and shortens installation time for operators who want basic analytics without adding a separate edge gateway. Omron’s Sysmac-Edge DX1 Data Flow Controller, launched globally in September 2025, illustrates this direction because it enables no-code data collection from multiple PLC brands on the shop floor without stopping production.[2]Omron Corporation, “OMRON to Launch Sysmac-Edge DX1 Data Flow Controller, an Edge Controller That Accelerates On-Site Data Utilization,” Omron Corporation, omron.com. NTT and Toshiba also demonstrated a cloud PLC configuration over IOWN APN that achieved a 20 ms control cycle across 300 km in a manufacturing test, which supports the view that local compact nodes and remote software functions will increasingly work together. That shift is raising the baseline feature set in the micro and nano PLC market because Ethernet connectivity, protocol flexibility, and programmable edge logic are no longer limited to premium configurations.

Demand for Space-Saving Integrated Control in OEM Machines

Space pressure inside machine cabinets continues to support the micro and nano PLC market, especially where builders want to add functionality without expanding enclosure size. Fixed and integrated platforms remain attractive because they reduce inter-module wiring, keep installation simple, and help OEMs standardize faster across repeated machine designs. Siemens presented LOGO! 9 in March 2026 with 800 function blocks, a color touchscreen, Secure Boot, and backward compatibility within a compact DIN-rail design, which shows how much capability is moving into the base controller itself.[3]Siemens AG, “Siemens Presents LOGO! 9, the New Generation of Logic Controller,” Siemens AG, siemens.com. When HMI visualization, secure firmware, and broader I/O capability sit inside the same compact platform, the historical distinction between a nano controller and a separate entry-level panel starts to narrow. That trend supports the micro and nano PLC market because more machine builders can justify higher-feature compact units in place of multiple low-cost control components.

Semiconductor and Electronics Capacity Additions

The micro and nano PLC market is also supported by semiconductor and electronics manufacturing, where compact deterministic control is needed in tightly engineered production environments. Demand in these settings is different from general factory automation because equipment must fit limited spaces, support consistent cycle timing, and operate within strict contamination and uptime requirements. JEMA’s 2025 survey confirms continued PLC use across electronics equipment applications, which aligns with the stronger growth outlook for semiconductor and electronics as an end-user group. NTT and Toshiba’s cloud PLC demonstration also matters here because electronics production environments are among the most likely to adopt architectures that split local control from higher-level digital functions. This keeps the micro and nano PLC market exposed to one of the most investment-oriented industrial verticals through the forecast period, even as technical requirements remain demanding.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Performance Ceiling Versus Mid-Range PLCs | -1.5% | Global | Short term (≤ 2 years) |

| Brownfield Integration and Commissioning Costs | -1.2% | Global | Medium term (2-4 years) |

| Edge Controller and Industrial MCU Substitution | -0.9% | North America, EU, APAC | Long term (≥ 4 years) |

| CRA and IEC 62443 Compliance Burden on Smaller Vendors | -0.8% | EU, EU-adjacent export markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Performance Ceiling Versus Mid-Range PLCs

The clearest structural limit on the micro and nano PLC market is the processing ceiling that appears when applications move into high-density I/O, synchronized motion, or more complex batch environments. Compact controllers work well in many standalone machines, but they still lose ground when users need a larger control scope, deeper motion capability, or broader native process functions. Rockwell Automation’s Vreugdenhil Dairy Foods case shows the kind of large-scale, integrated production setting where higher-tier control platforms remain necessary because plant complexity extends beyond the practical headroom of compact devices.[4]Rockwell Automation, Inc., “Vreugdenhil Dairy Foods Automates and Controls Entire Milk Powder Plant With Rockwell Automation Integrated Architecture,” Rockwell Automation, rockwellautomation.com. This matters in the micro and nano PLC market because entry-level mid-range controllers are becoming more capable while also moving closer in price to upper micro-tier products. As vendors add safety, motion, or advanced software functions to defend against substitution, they risk raising cost and weakening the size advantage that made compact controllers attractive in the first place.

Brownfield Integration and Commissioning Costs

Brownfield migration continues to slow the micro and nano PLC market because much of the global factory equipment still runs on older networks and controller logic structures. Replacing a compact controller in these settings often requires converters, address remapping, testing cycles, and planned downtime that can cost more than the device itself. Contec IAS documented a PLC migration project in food production where engineering effort around legacy integration formed a significant part of the work scope, which reflects how sticky installed-base complexity can be. Rockwell Automation addressed part of this problem by adding PCCC functionality for MicroLogix migration support in its controller and software updates, showing that vendors are trying to reduce re-engineering friction for installed users. Even so, the micro and nano PLC market still faces a durable adoption barrier in multi-vendor plants where specialist commissioning knowledge is limited and downtime costs are hard to absorb.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Size: Nano PLC Growth Challenges Micro PLC Supremacy

Micro PLCs held 61.23% of the global micro and nano PLC market share in 2025, which kept them in the leading position across compact industrial control. Their advantage came from a balanced feature set that fits packaging machinery, conveyors, HVAC panels, pump systems, and small machine tools without pushing buyers into higher-cost modular platforms. In the micro and nano PLC market, this middle ground remains valuable because many OEMs need more logic and connectivity than a smart relay can provide, but they do not need full mid-range PLC architecture. Rockwell Automation’s Allen-Bradley Micro820 L20E, launched in October 2025, reflects that direction with EtherNet/IP Class 1 messaging, a USB-C commissioning interface, and compatibility with FactoryTalk Design Workbench. The micro PLC position is also supported by practical application depth, including Rockwell’s plant-protein microdosing case, where compact control helped maintain dosing accuracy in servo-driven food processing equipment.

Nano PLCs are projected to grow at a 7.91% CAGR through 2031, making them the fastest-moving part of the micro and nano PLC market. Their momentum is strongest where cabinet space is extremely limited and where users still need deterministic logic in embedded or highly localized control tasks. Keyence’s KV Nano line shows how that value proposition is broadening, because the platform combines ultra-fast processing with built-in networking in a very small form factor. JTEKT’s TOYOPUC-Nano series further supports the case for compact, machine-specific control designs that can serve precision-oriented OEM requirements without oversized hardware. This means the micro and nano PLC market is seeing a real narrowing of the historical capability gap between small-form-factor controllers and larger compact PLCs, even though micro PLCs still hold the broader installed base.

By Offering: Software Monetization Reshapes the Hardware-Led Revenue Mix

Hardware captured 69.38% of the global micro and nano PLC market size in 2025, which shows that controller sales still anchor the revenue base. That position reflects the capital-heavy nature of factory automation, where physical devices, I/O, and related control hardware remain the first purchase decision. The hardware layer also remains central in the micro and nano PLC market because buyers still weigh durability, communication support, and installed compatibility before they commit to a brand ecosystem. Rockwell Automation reinforced that hardware-led model in October 2025 with the Micro820 L20E launch, which added stronger connectivity and simpler commissioning to a compact controller platform. Even so, the hardware lead is gradually being pressured as software and services become more important in ongoing machine lifecycle decisions.

Software is forecast to grow at a 7.87% CAGR through 2031, making it the faster-expanding offering layer within the micro and nano PLC market. The driver is not only licensing revenue, but also the role of programming tools, troubleshooting platforms, visualization functions, and engineering workflows in locking users into a vendor ecosystem. Rockwell Automation’s FactoryTalk Design Workbench launch in October 2025 is a strong example because the company positioned a free programming and troubleshooting environment for Micro800 users as a retention and ease-of-use tool rather than a direct monetization product. Beckhoff’s TwinCAT PLC++ recognition in 2026 also highlights how development speed, continuity, and modern software workflow alignment are shaping buying decisions beyond controller hardware alone. As this pattern deepens, the micro and nano PLC industry will increasingly reward suppliers that can make compact control easier to engineer, update, and maintain over time.

By Architecture: Modular Expansion Driven by Scalability and Retrofit Demand

Fixed/Integrated platforms held 65.89% of the global micro and nano PLC market share in 2025, which kept them firmly ahead of modular designs. Their lead came from applications where the machine scope is already known at the design stage and where builders want to reduce wiring, cabinet depth, and installation time. In the micro and nano PLC market, what matters most is for repeated OEM platforms where simplicity, lower material cost, and faster build cycles outweigh future expansion needs. WAGO’s Compact Controller 100 illustrates how capable this format has become, with real-time Linux, CODESYS, and Node-RED support, and protocol coverage that reaches both industrial and building applications. That combination explains why fixed architectures still dominate much of the entry-level and mid-tier compact control base.

Modular architectures are projected to advance at an 8.12% CAGR through 2031, which gives them the fastest growth rate in the micro and nano PLC market. Their appeal is strongest in brownfield projects and scalable machine layouts where I/O needs can change after initial installation. Beckhoff expanded that argument in February 2026 with its ED series EtherCAT Terminals, which added tool-free wiring and broader analog functionality while maintaining compatibility with existing hardware. Beckhoff also released new high-density analog terminals in January 2026 with up to 8 channels and 16-bit resolution, giving users a more efficient upgrade path in space-constrained modular control setups. The result is a micro and nano PLC market where modular growth is increasingly tied to phased modernization and precision signal requirements, not only to large-scale automation architectures.

By End-User Industry: Automotive Anchors Revenue While Semiconductor Accelerates

Automotive and transportation accounted for 22.78% of the global micro and nano PLC market size in 2025, making it the largest end-user segment. The segment benefits from recurring demand in assembly control, conveyor management, paint shop monitoring, and battery-related process equipment. In the micro and nano PLC market, automotive remains important because production lines need deterministic performance, high uptime, and flexible machine-level changes without full system redesign. Rockwell Automation documented an EV production line upgrade where its Micro-series controllers helped compress engineering time through a common EtherNet/IP approach, showing how compact control fits line rebalancing needs in fast-moving vehicle programs. That application depth gives automotive a durable revenue base even as other verticals gain growth momentum.

Semiconductors and electronics are forecast to grow at a 7.96% CAGR through 2031, making them the fastest-growing end-user group in the micro and nano PLC market. Growth is linked to equipment expansion, cleaner production environments, and the need for compact control inside precision handling and process support systems. JEMA’s 2025 survey supports the strength of electronics-related OEM demand, particularly in applications where controller integration with precision motion and machine subsystems matters. The same vertical also aligns well with evolving edge-control models, as shown by NTT and Toshiba’s cloud PLC demonstration for manufacturing environments. Food and beverage, pharmaceuticals, water and wastewater, chemicals, and metals and mining remain important to the micro and nano PLC market, but their usage patterns are more mature and often shaped by regulatory, environmental, or site-condition constraints rather than rapid redesign cycles.

Geography Analysis

Asia-Pacific accounted for 46.34% of the global micro and nano PLC market size in 2025 and is expected to post a 7.71% CAGR through 2031, which gives it both the largest and fastest-growing regional position. This dual role is unusual in industrial automation and reflects a combination of dense manufacturing activity, rising SME automation, and broad demand across electronics, automotive, and machinery production. The micro and nano PLC market in Asia-Pacific also benefits from a wide range of local and international supplier options, which helps buyers match price, features, and service needs more closely. Japan remains an important reference market because JEMA’s 2025 PLC user survey shows continued adoption in precision machining and electronics equipment segments, where compact controllers integrate closely with motion and vision systems. The region is also well positioned for the next stage of software-linked compact automation because NTT and Toshiba’s 2025 cloud PLC test pointed to practical pathways for combining local control and remote digital functions.

North America and Europe form the second major demand base for the micro and nano PLC market, but their growth pattern is shaped more by replacement, compliance, and modernization than by greenfield volume alone. North America continues to rely on compact control in food processing, automotive, and electronics manufacturing, where machine-level reliability and easier integration carry a high value. Europe is becoming especially important in secure controller replacement because the Cyber Resilience Act entered into force in December 2024, with vulnerability reporting obligations applying from September 2026 and broader product requirements applying from December 2027. That regulatory calendar supports the micro and nano PLC market by encouraging upgrades away from legacy devices that lack Secure Boot, secure update paths, or documented security processes. European procurement is also placing greater weight on IEC 62443-aligned component security, which raises the qualification threshold for vendors serving industrial accounts.

South America, the Middle East, and Africa remain smaller in revenue terms, but they offer an important expansion path for the micro and nano PLC market. In South America, food processing, agribusiness, and mining create demand for compact control that can operate reliably in remote or network-limited environments. The Middle East is adding greenfield automation demand through industrial diversification and infrastructure-linked manufacturing activity, while Africa is seeing earlier-stage compact automation adoption in mining, food processing, and light manufacturing. These regions are especially relevant to the micro and nano PLC market because fixed and integrated platforms can often deliver useful automation without the engineering overhead that more complex architectures require.

Competitive Landscape

The global micro and nano PLC market shows moderate fragmentation, with a clear group of premium global vendors at the top and a broad field of regional suppliers underneath. Siemens AG, Rockwell Automation, Omron Corporation, Mitsubishi Electric Corporation, and Schneider Electric shape much of the premium roadmap, while Delta Electronics, LS Electric, Fuji Electric, and other local players apply price and channel pressure in the entry range. This structure keeps the micro and nano PLC market competitive across both performance tiers and customer types, especially where OEMs compare software usability as closely as hardware specifications. Rockwell Automation’s 2025 combination of the Micro820 L20E hardware launch and the FactoryTalk Design Workbench software rollout shows how suppliers are tightening the link between the physical controller and the engineering environment around it.

A second competitive theme in the micro and nano PLC market is the move from feature competition to ecosystem retention. Vendors that can make commissioning easier, enable simpler updates, and shorten engineering cycles are creating stronger long-term account stickiness than vendors that only add isolated hardware functions. Siemens’ LOGO! 9 launch is relevant here because it packages secure boot, greater function capacity, and backward compatibility into an entry-level logic controller that is easier to keep inside an installed Siemens environment. Beckhoff’s TwinCAT PLC++ recognition in 2026 also shows that development continuity and software workflow sophistication are now part of the competitive baseline in compact automation.

Cybersecurity and edge connectivity create the most visible white space in the micro and nano PLC market. Demand is rising for controllers that can meet stricter security expectations while also connecting natively to broader plant data environments. Omron’s Sysmac-Edge DX1 launch further shows how vendors are trying to widen relevance across mixed-brand factories by reducing the effort needed to collect and visualize data from multiple PLC families. Competition is therefore likely to stay intense in the micro and nano PLC market because price pressure at the low end is now matched by faster software and compliance investment at the upper end.

Micro And Nano PLC Industry Leaders

Rockwell Automation, Inc.

Siemens AG

Omron Corporation

Schneider Electric SE

ABB Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Beckhoff Automation's TwinCAT PLC++ was awarded first place in the Control and Regulation category at Computer and Automation magazine's Products of the Year 2026 awards, recognizing its DevOps-aligned architecture, CI/CD framework integration, and seamless backward compatibility with existing TwinCAT PLC code.

- April 2026: Siemens presented LOGO! 9, the new generation of its logic controller platform, at the Light and Building trade fair, making it available from April 1, 2026, the product delivers doubled function block capacity, up to 800, a color touchscreen display, 320 x 240 px, Secure Boot, and encrypted firmware update capability, its first generational change in 11 years.

- February 2026: Beckhoff Automation launched the ED series EtherCAT Terminals featuring tool-free push-in wiring connections and expanded analog I/O functionality, retaining full compatibility with all existing Beckhoff EtherCAT hardware while introducing a modernized housing standard with app-based diagnostics via scannable product data matrix.

- January 2026: Beckhoff Automation released a new generation of high-density analog EtherCAT I/O Terminals, EL3072, EL3074, EL3078, EL4072, EL4074, EL4078, with up to 8 channels and 16-bit resolution, a significant upgrade from the prior 12-bit specification, in compact high-density housings for space-constrained modular control architectures.

Global Micro And Nano PLC Market Report Scope

The Micro and Nano PLC Market Report is Segmented by Product Size (Nano PLC and Micro PLC), Offering (Hardware, Software, and Services), Architecture (Fixed/Integrated and Modular), End-User Industry (Automotive and Transportation, Food and Beverage, Oil and Gas, Power and Energy, Chemicals, Pharmaceuticals, Metals and Mining, Water and Wastewater, Semiconductors and Electronics, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Nano PLC |

| Micro PLC |

| Hardware |

| Software |

| Services |

| Fixed / Integrated |

| Modular |

| Automotive and Transportation |

| Food and Beverage |

| Oil and Gas |

| Power and Energy |

| Chemicals |

| Pharmaceuticals |

| Metals and Mining |

| Water and Wastewater |

| Semiconductors and Electronics |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Size | Nano PLC | ||

| Micro PLC | |||

| By Offering | Hardware | ||

| Software | |||

| Services | |||

| By Architecture | Fixed / Integrated | ||

| Modular | |||

| By End-User Industry | Automotive and Transportation | ||

| Food and Beverage | |||

| Oil and Gas | |||

| Power and Energy | |||

| Chemicals | |||

| Pharmaceuticals | |||

| Metals and Mining | |||

| Water and Wastewater | |||

| Semiconductors and Electronics | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the global micro and nano PLC market size in 2026 and what is the outlook to 2031?

The global micro and nano PLC market stood at USD 6.78 billion in 2026 and is projected to reach USD 9.57 billion by 2031 at a 7.14% CAGR.

Which region leads demand for compact PLCs worldwide?

Asia-Pacific led with 46.34% of revenue in 2025 and is also the fastest-growing region, with a projected 7.71% CAGR through 2031.

Which product type is larger, micro PLCs or nano PLCs?

Micro PLCs remained larger in 2025 with a 61.23% share, while nano PLCs are growing faster at a 7.91% CAGR through 2031.

Why are fixed and integrated controllers still dominant?

Fixed and integrated platforms held 65.89% share in 2025 because they reduce wiring, save cabinet space, and simplify OEM machine design.

Which end-user segment is creating the strongest revenue base?

Automotive and transportation led with 22.78% of revenue in 2025 because compact controllers are widely used in assembly, conveyors, and EV line automation.

What is changing competition among leading suppliers?

Competition is shifting from hardware-only differentiation to software ecosystems, cybersecurity readiness, and easier edge connectivity across mixed-brand factory environments.

Page last updated on: