Automotive Data Logger Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 4.73 Billion |

| Market Size (2031) | USD 6.82 Billion |

| Growth Rate (2026 - 2031) | 7.63% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Data Logger Market Analysis by Mordor Intelligence

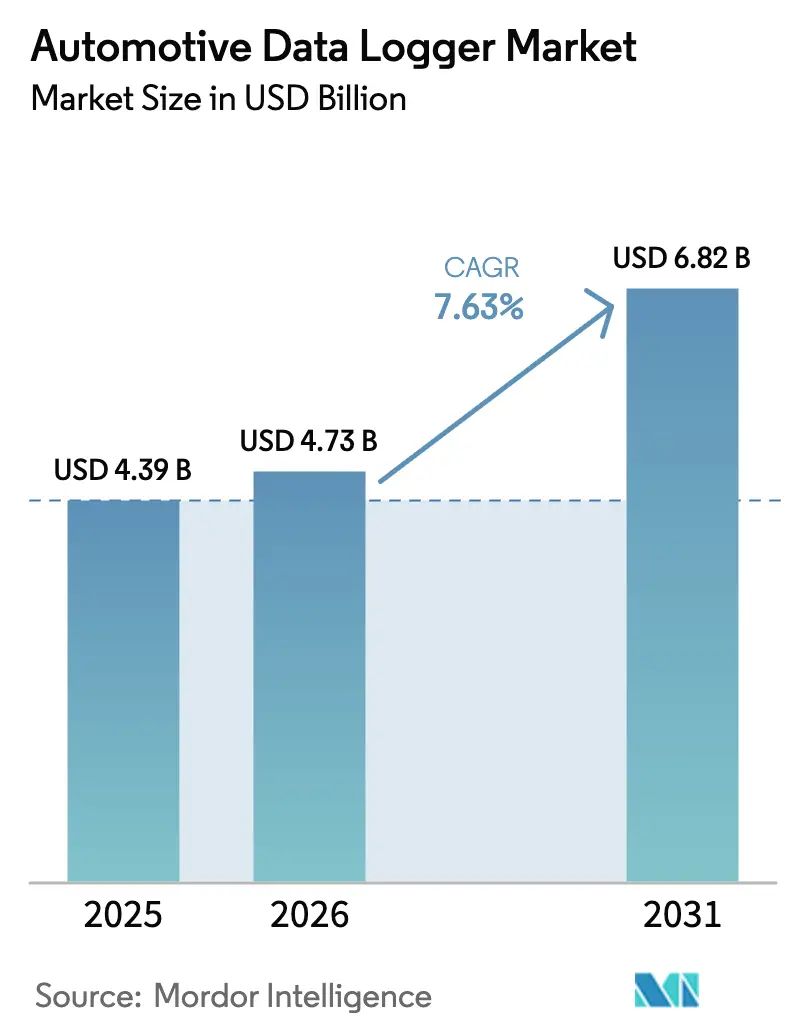

The Automotive Data Logger Market size is expected to grow from USD 4.39 billion in 2025 to USD 4.73 billion in 2026 and is forecast to reach USD 6.82 billion by 2031 at 7.63% CAGR over 2026-2031.

The expansion reflects a decisive industry shift toward predictive, data-centric vehicle management that enhances safety, efficiency, and lifecycle cost control. Regulatory mandates in the European Union, China, and other major regions are accelerating the adoption of event data recorders and broader data-logging capabilities. Growing sensor counts in advanced driver-assistance systems (ADAS) and the transition to centralized, software-defined vehicle architectures are increasing demand for high-bandwidth, secure logging platforms. Heightened fleet digitalization, usage-based insurance in emerging economies, and the need for real-time analytics across electrified fleets further reinforce growth opportunities. Competitive differentiation has begun to pivot from hardware alone toward integrated data-management ecosystems capable of over-the-air (OTA) updates, cybersecurity compliance, and advanced analytics.

Key Report Takeaways

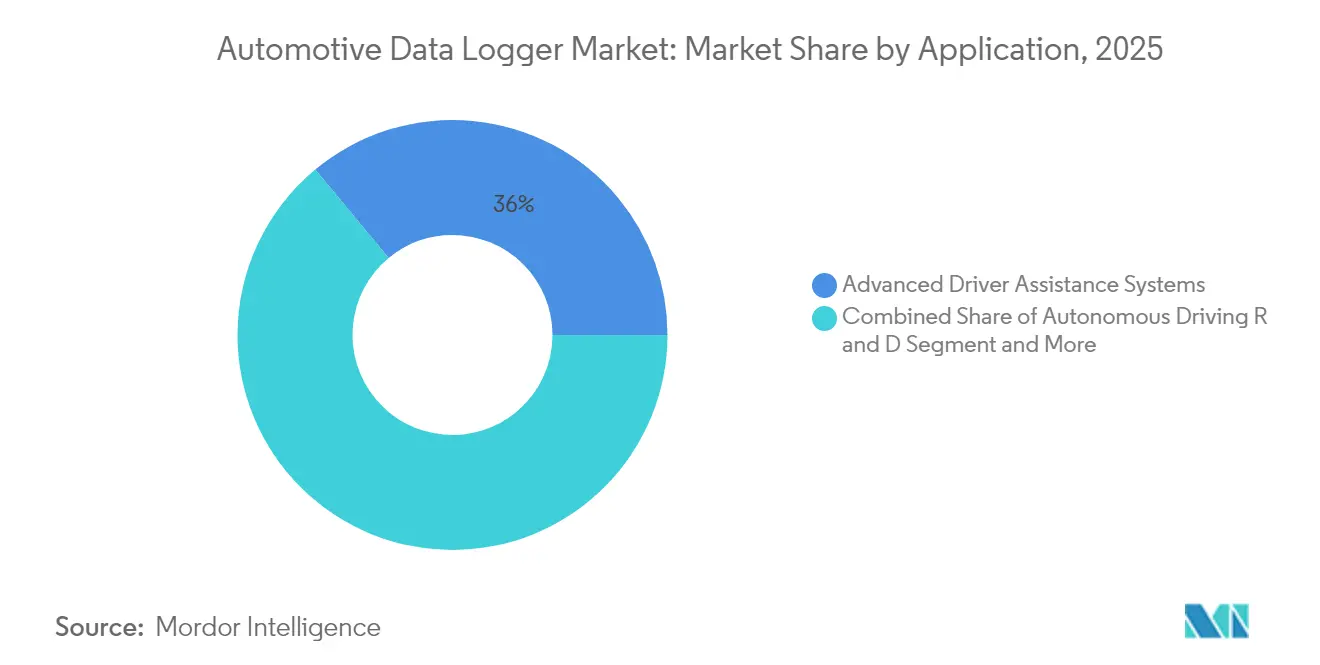

- By application, ADAS led with 36.02% revenue share in 2025; autonomous driving R&D is projected to expand at a 13.14% CAGR through 2031.

- By connection type, USB dominated the automotive data logger market, with 40.28% of the share in 2025, while automotive Ethernet is poised to grow at a 10.62% CAGR to 2031.

- By hardware type, stand-alone loggers dominated the automotive data logger market and captured 34.01% of the revenue share in the 2025 automotive data logger market size; cloud-based software agents represent the fastest-growing category at 9.11% CAGR.

- By memory capacity, the 32-128 GB tier dominated the automotive data logger market, accounting for a 31.74% share in 2025; capacities above 512 GB are forecast to rise at an 8.15% CAGR.

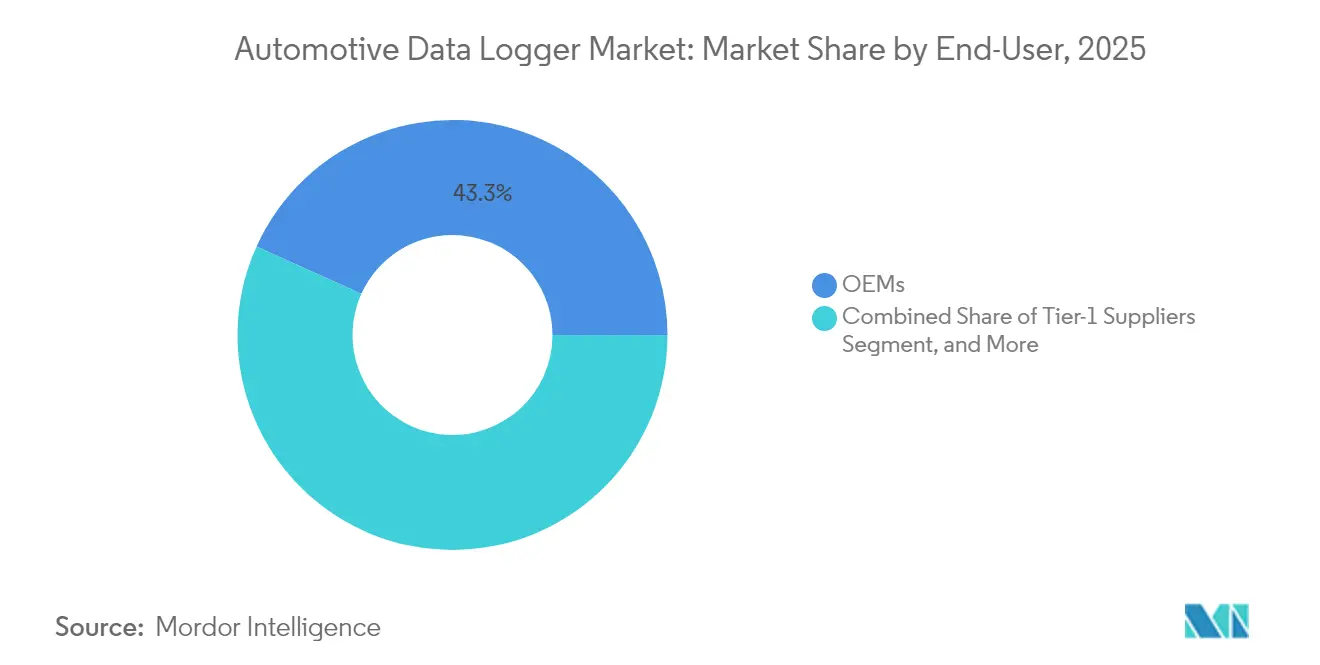

- By end user, OEMs held the highest market share in the dominated automotive data logger market, 43.25% in 2025; fleet operators are expected to advance at 10.31% CAGR.

- By channel, OEM-fitted solutions commanded the automotive data logger market with 56.62% share in 2025, while the aftermarket segment is set to grow at 9.32% CAGR.

- By vehicle type, passenger cars retained 66.88% share in the automotive data logger market in 2025; medium and heavy commercial vehicles show the highest growth at 9.63% CAGR.

- By propulsion, internal-combustion vehicles remain dominated the automotive data logger market with 65.72% share in 2025, yet battery-electric vehicles are projected to register a 12.08% CAGR.

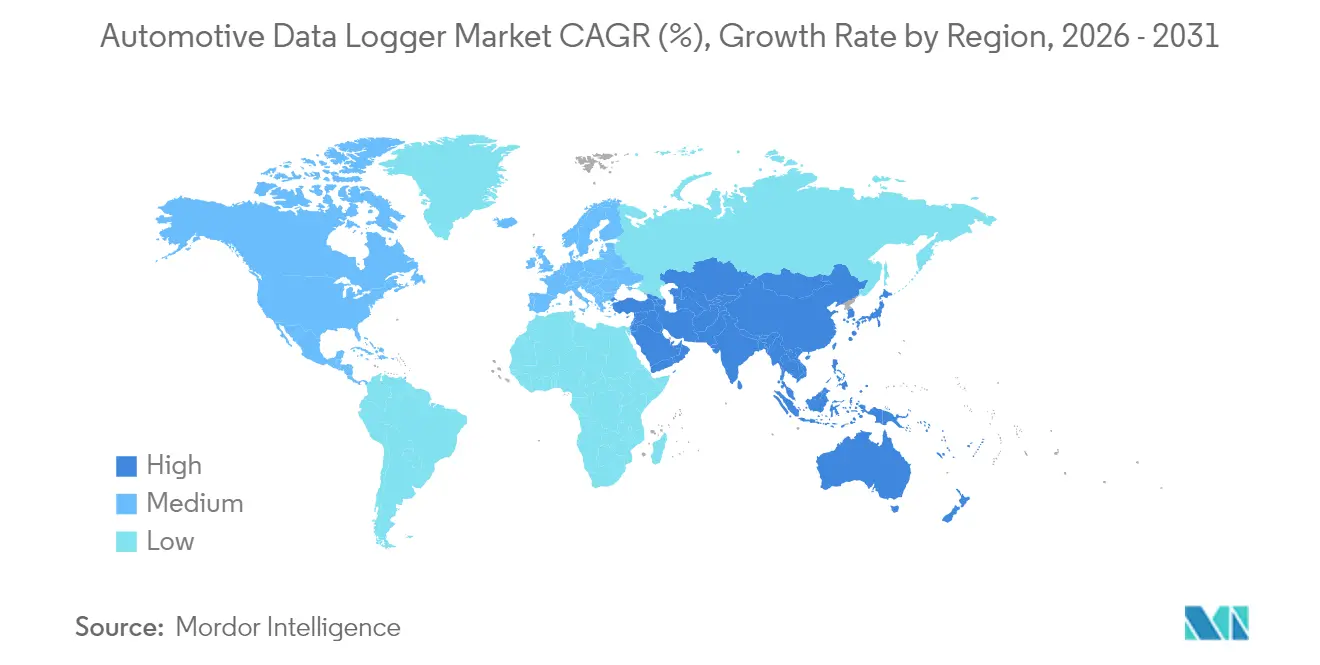

- Regionally, North America led the automotive data logger marketwith 30.92% share in 2025, whereas Asia-Pacific is the fastest-growing region at 10.09% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Data Logger Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Sensor Fusion Data in Level-3+ AD | +2.1% | North America and EU leading, Asia-Pacific following | Long term (≥ 4 years) |

| Regulatory Push for Autonomous-Ready E/E Systems | +1.8% | Global, with early adoption in EU and China | Medium term (2-4 years) |

| OEM Shift to Software-Defined Vehicles & Logging | +1.5% | Global, with premium segments first | Medium term (2-4 years) |

| Real-Time Fleet Analytics to Reduce EV TCO | +1.2% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Usage-Based Insurance Growth in Emerging Markets | +0.9% | Asia-Pacific core, spill-over to South America | Short term (≤ 2 years) |

| Mandated EDRs in Euro-NCAP & China NCAP 2026+ | +0.7% | EU and China, potential global harmonization | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Soaring Volume of Sensor-Fusion Data in Level 3+ AD Systems

Modern premium vehicles will need up to 278 GB of embedded memory in 2026 versus 90 GB in 2025, a threefold rise directly tied to multi-sensor ADAS suites[1]“Memory Trends for Advanced Driver-Assistance Systems,” Micron Technology, micron.com. BlackBerry IVY and NXP S32K5 MCUs showcase industry progress in secure multi-sensor data handling. Vehicles employing 60-400 sensors now generate petabyte-scale datasets over their lifetimes, stimulating long-term demand in the automotive data logger market for high-reliability storage and rapid offload capabilities.

Regulatory Push for Autonomous-Ready E/E Architectures

UN ECE Regulation 160 mandates event data recorders that capture discrete vehicle parameters for several seconds pre-incident, driving OEM demand for compliant, high-capacity logging subsystems[2]“Regulation No. 160: Event Data Recorders,” United Nations Economic Commission for Europe, unece.org. Suppliers like Continental respond with scalable software platforms integrating cybersecurity and OTA update readiness. Centralized computing architectures, now demonstrating 30-40% wiring reductions, intensify processing loads and elevate the automotive data logger market requirement for robust throughput and embedded security.

Usage-Based Insurance Adoption in Emerging Economies

Fleet and personal lines increasingly deploy telematics to refine risk models. Octo Telematics already supports 6 million connected policies across 20 countries, highlighting scalability potential in Asia and South America[3]“Connected Insurance Solutions Overview,” Octo Telematics, octotelematics.com. For data-logger suppliers, this presents immediate opportunities to package secure, insurer-grade data streams for underwriting and claims validation.

Real-Time Fleet Health Analytics to Cut TCO for Electrified Fleets

North American and European operators of battery-electric delivery and transit fleets rely on continuous logging of charge cycles, temperature profiles, and driving patterns to extend battery life and optimize routing. Continental’s VDO Fleet platform integrates tachograph data with predictive analytics that cut unplanned downtime, widening adoption across APAC as charging infrastructure matures.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity Risks Limiting Data Access | -1.3% | Global, with stricter enforcement in EU and China | Short term (≤ 2 years) |

| Raw Flash Price Volatility Raising BOM Costs | -0.8% | Global, affecting cost-sensitive segments most | Short term (≤ 2 years) |

| Lack of Unified Data Standards Across OEMs | -0.7% | Global, with fragmentation between US, EU, and Asia-Pacific standards | Medium term (2-4 years) |

| OEM Reluctance to Share Data with Insurers | -0.6% | North America and EU primarily, emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security Risks Driving Data-Access Restrictions

UNECE WP.29 R156 obliges manufacturers to maintain certified cybersecurity management systems, curtailing unauthorized third-party data tapping. China’s data-localization rules require on-shore storage and state security assessments for outbound transfers, complicating cross-border R&D collaboration. Providers are embedding Uptane-based secure-update frameworks and hardware root-of-trust elements to satisfy regulators while ensuring business continuity in the automotive data logger market.

High Raw-Flash Price Volatility Inflating BOM Cost

DRAM and NAND supply cannot keep pace with 30-35% annual demand growth for automotive-grade memory, leading to price swings that compress margins. Automotive specifications spanning –40 °C to +105 °C and AEC-Q100 qualification narrow the supplier pool, an issue highlighted by Western Digital’s automotive portfolio updates. Long-term supply agreements protect availability yet limit flexibility in adopting emerging, lower-cost technologies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: ADAS Dominance Faces Autonomous Disruption

ADAS accounted for the largest automotive data logger market slice in 2025 at 36.02%. The segment’s growth is anchored in regulatory calls for lane-keeping, automated braking, and driver-monitoring functions. In parallel, autonomous-driving R&D is charted to grow at 13.14% CAGR, underpinned by sensor-rich prototypes that create terabytes of daily data. Commercial fleet management continues steady adoption for predictive maintenance, while insurance telematics gains traction in Asia and Latin America. Emerging use cases, such as infotainment analytics and OTA validation, demand continuous logging of user interaction and software execution data. This application convergence positions data-management platforms as multipurpose hubs, enabling OEMs to monetize insights while reducing hardware redundancy.

Across these use cases, developers require deterministic storage, granular time-stamping, and open APIs. The automotive data logger market size for ADAS and infotainment combined commanded half of the total revenues 2025. As Level 3 trials progress, prototypes often employ more than 512 GB of onboard storage. Over the forecast period, the rising deployment of domain-controller architectures and edge analytics will further strengthen the value proposition for integrated logging and processing solutions.

By Connection Type: Ethernet Emerges as USB Alternative

USB dominated the automotive data logger market with a 40.28% share in 2025 because of its ubiquity in test benches and aftermarket retrofits. Yet the bandwidth ceiling of single-lane USB limits its future role in high-resolution sensor data offload. Automotive Ethernet, supported by single-pair variants such as 100BASE-T1, is forecast to post a 10.62% CAGR. Tier-1 suppliers bundle multi-protocol gateways that couple CAN-FD and Ethernet to balance legacy support and future scalability. The Ethernet products' automotive data logger market size is expected to double by 2031 as OEMs migrate to zonal architectures.

Other connection types, such as Cellular 5G connectivity, underpin real-time cloud backhaul for fleet use cases. At the same time, Wi-Fi Direct supports garage or depot offloads where bandwidth costs must be contained. Suppliers are increasingly packaging adaptable transceivers and software-defined radios that allow firmware-based switching between standards, mitigating obsolescence risk.

By Hardware Type: Cloud Migration Accelerates

Stand-alone loggers dominated the automotive data logger market with a 34.01% share in 2025 due to their ruggedness and independence. Cloud-native agents, however, will record the highest growth at 9.11% CAGR as OEMs virtualize electronic control units (ECUs). Continental’s vECU Creator exemplifies how developers compile and test software in the cloud before hardware is ready, compressing development cycles. The automotive data logger market share of embedded OEM modules is also rising because regulatory mandates encourage factory integration.

Hardware consolidation yields lower power draw, smaller harnesses, and easier OTA patching. Cloud-linked loggers provide lifecycle cost savings via remote diagnostics and dynamic storage allocation. Suppliers focusing on encryption, compression, and smart-stream selection stand to capture incremental value as data volumes expand.

By Memory Capacity: High-Capacity Demand Surges

The 32-128 GB band dominated the automotive data logger market with a 31.74% share in 2025, matching today’s Level 2 ADAS requirements. Vehicles under Level 3 development programs already test capacities above 512 GB, the fastest-growing bracket at 8.15% CAGR. As sensor counts scale, demand for error correction, power-loss protection, and extended temperature tolerance drives premium pricing. Automotive data logger market size for high-capacity tiers will reflect the shift to centralized storage pools managed by real-time controllers.

Micron’s projections indicate 4 TB per autonomous vehicle by 2030. Suppliers are therefore adopting mixed-memory architectures blending MRAM for instant-on logs, NOR for boot code, and NAND for bulk storage. Concurrently, software compression and intelligent sampling aim to slow physical capacity growth, balancing BOM costs against the relentless data-generation curve.

By End User: Fleet Operators Drive Growth

OEMs kept the largest stake in the automotive data logger market with 43.25% in 2025, leveraging in-house data for product engineering and regulatory compliance. Fleet operators will outpace other groups at 10.31% CAGR because predictive analytics lowers the total cost of ownership through reduced downtime. Tier-1 suppliers integrate component validation telemetry into broader service offerings, while insurers harness telematics to verify risk profiles.

Regulators and test agencies require traceable, tamper-proof logs for homologation and safety validation, creating a specialized niche demand. The automotive data logger market benefits from growing collaboration among OEMs, fleets, and insurers to pool anonymized data, accelerating model training for advanced analytics without compromising privacy mandates.

By Channel: Aftermarket Gains Momentum

OEM-fitted systems captured a 56.62% share in the automotive data logger market in 2025 under the influence of EDR regulations. Yet aftermarket providers are ramping up at 9.32% CAGR, capitalizing on the vast installed base of vehicles predating regulatory deadlines. The EU Data Act, effective September 2025, will require automakers to provide secure third-party data access interfaces, reducing historical barriers to aftermarket innovation.

OTA-deployable software agents blur channel distinctions by enabling subscription-based features post-sale. For the automotive data logger market, hybrid deployment models combining factory-installed gateways and dealer-installed expansion modules will become common, especially for mixed fleets spanning multiple model years.

By Vehicle Type: Commercial Vehicles Accelerate

Passenger cars dominated the automotive data logger market with 66.88% of sales in 2025, benefiting from scale economies. Heavy commercial vehicles, however, will log the highest CAGR at 9.63% as logistics firms embrace predictive powertrain maintenance and regulatory compliance (for example, tachograph mandates). Light commercial segments leverage telematics to optimize last-mile deliveries, while off-highway machinery adopts loggers for equipment health monitoring under harsh conditions.

Bosch’s Electronic Horizon has demonstrated measurable fuel savings in trucking by integrating topographic data with powertrain controls, highlighting value capture beyond raw data collection. The automotive data logger market is evolving from passive recorders to active enablers of operational efficiency across vehicle classes.

By Propulsion: Electric Vehicles Lead Innovation

Internal combustion models remain the volume bedrock, with a 65.72% share in the automotive data logger market in 2025. Battery-electric vehicles (BEVs) will expand fastest, at 12.08% CAGR, driven by battery state-of-health monitoring, charging analytics, and thermal-management logging. Hybrids require dual-powertrain data correlation, while fuel-cell models need hydrogen stack performance tracking.

Mahindra’s EV telematics platform, deployed in 24 countries, showcases how granular battery data improves range accuracy and residual-value forecasting. As electrification advances, standardized interfaces such as ISO 15118 for smart charging will feed additional telemetry to cloud analytics, reinforcing growth prospects in the automotive data logger market.

Geography Analysis

North America dominated the automotive data logger market with a 30.92% share in 2025 due to mature fleet telematics adoption and insurer telematics penetration. Regulatory focus centers on privacy and cybersecurity rather than prescriptive device standards, prompting OEM investment in consent management and encryption. Regional fleets increasingly deploy machine-learning-driven predictive maintenance to extend asset life and minimize roadside incidents.

Asia-Pacific is projected to grow at 10.09% CAGR through 2031. China mandates data localization and real-time uploads to government-approved servers for intelligent connected vehicles, reshaping global architecture decisions. Indian commercial fleets are integrating telematics quickly to meet new safety and tax compliance rules, while Japanese regulators emphasize driver-readiness monitoring for advanced autonomy trials. The region’s strong uptake of electric vehicles mirrors national industrial policies, amplifying demand for high-capacity loggers able to process battery and ADAS data in concert.

Europe maintains a leading regulatory influence. Regulation 2019/2144 obliges event data recorders in all new cars and vans, and the forthcoming Data Act will open manufacturer data silos to third parties under strict consent rules. German suppliers pioneer privacy-by-design principles, embedding on-device anonymization before transmission. Compliance costs spur collaboration across the value chain, with suppliers like Continental offering turnkey cybersecurity and logging stacks that comply with UN ECE and EU directives.

Competitive Landscape

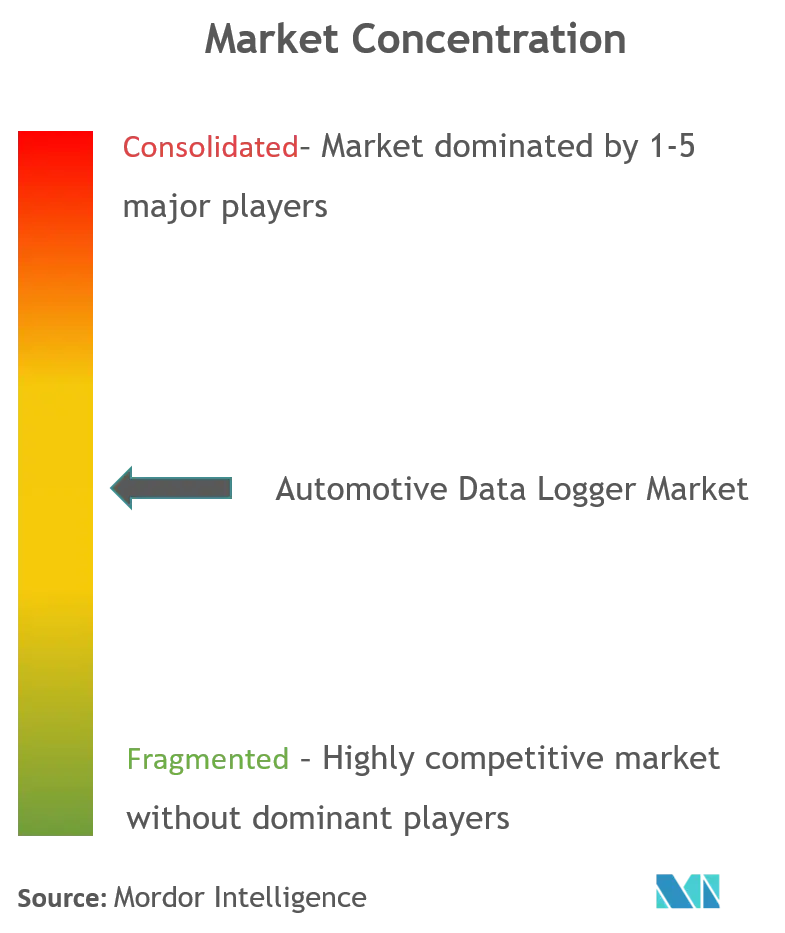

The automotive data logger market is moderately fragmented, featuring traditional Tier-1s (Bosch, Continental, HARMAN), semiconductor leaders (NXP, Renesas, Qualcomm), and cloud-native software entrants. Competitive advantage is shifting toward vertically integrated solutions that combine secure hardware, flexible middleware, and analytics platforms. NXP’s 2025 acquisition of TTTech Auto strengthens its ability to supply gateway controllers paired with deterministic Ethernet and OTA support. Bosch and Continental leverage deep OEM ties to embed logging functions into broader domain controllers, while software specialists emphasize rapid, OTA-deployable analytics.

Strategic themes include consolidating processing, networking, and power management into single platforms that reduce wiring by up to 40%. Providers compete to meet rigorous automotive cybersecurity standards without sacrificing data-sharing flexibility required by insurers and fleets. Emerging white spaces include off-highway machinery, micro-mobility, and developing-market fleets where incumbents have limited reach. Cloud scalability and subscription models redefine revenue streams, disadvantaging pure-hardware vendors unless they evolve toward service-oriented offerings.

Recent strategic moves illustrate the trend. NXP’s S32K5 MCU, launched March 2025, integrates embedded MRAM and AI accelerators calibrated for zonal architectures. TTTech Auto’s May 2025 logger targets software-defined vehicle validation with synchronized multi-gigabit capture. Bosch’s 2024 partnership with Amazon Web Services extends digital-logistics platforms into commercial vehicles. Together, these moves signal heightened race toward holistic, software-centric ecosystems.

Automotive Data Logger Industry Leaders

Robert Bosch Gmbh

Vector Informatik GmbH

Continental

National Instruments

Aptiv PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: TTTech Auto launched a next-generation data logger for software-defined vehicle verification. Advancing the latest evolution of PM-200, the PM-350 represents the latest innovation in capturing high-speed automotive.

- August 2024: NXP and TTTech Auto partnered on the N4 Network Controller, integrating S32G2 processors and Ethernet switching.

- March 2024: NXP introduced the S32 Core Ride platform to consolidate ECUs for production by 2027.

Global Automotive Data Logger Market Report Scope

The Automotive Data Logger market covers the latest trends and technological developments, as well as provides an analysis of the market demand on various segments like technology type and connection type. Regional and country-level analysis, as well as the market share of major automotive data logger across the globe, will be covered in the scope of the report.

| ADAS |

| Autonomous Driving R&D |

| Fleet Management |

| Others |

| USB |

| Automotive Ethernet |

| Others |

| Stand-alone Data Logger |

| Plug-in OBD Dongle |

| Embedded OEM Module |

| Cloud-based Software Agent |

| Less than 32 GB |

| 32 - 128 GB |

| 128 - 512 GB |

| More Than 512 GB |

| OEMs |

| Tier-1 Suppliers |

| Fleet Operators & Telematics Providers |

| Insurance Companies |

| Independent Service Providers |

| Regulatory & Testing Agencies |

| Research Institutions |

| OEM-Fitted |

| Aftermarket |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Off-Highway Vehicles |

| Two-Wheelers & Micromobility |

| ICE Vehicles |

| Hybrid Vehicles |

| Battery Electric Vehicles |

| Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | ADAS | |

| Autonomous Driving R&D | ||

| Fleet Management | ||

| Others | ||

| By Connection Type | USB | |

| Automotive Ethernet | ||

| Others | ||

| By Hardware Type | Stand-alone Data Logger | |

| Plug-in OBD Dongle | ||

| Embedded OEM Module | ||

| Cloud-based Software Agent | ||

| By Memory Capacity | Less than 32 GB | |

| 32 - 128 GB | ||

| 128 - 512 GB | ||

| More Than 512 GB | ||

| By End User | OEMs | |

| Tier-1 Suppliers | ||

| Fleet Operators & Telematics Providers | ||

| Insurance Companies | ||

| Independent Service Providers | ||

| Regulatory & Testing Agencies | ||

| Research Institutions | ||

| By Channel | OEM-Fitted | |

| Aftermarket | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| Off-Highway Vehicles | ||

| Two-Wheelers & Micromobility | ||

| By Propulsion | ICE Vehicles | |

| Hybrid Vehicles | ||

| Battery Electric Vehicles | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving growth in the Automotive Data Logger Market from 2026 to 2031?

Growth is propelled by regulatory mandates for event data recorders, rising sensor counts in advanced driver-assistance systems, adoption of software-defined vehicle architectures, and expanding fleet telematics in emerging economies.

Which application segment shows the fastest expansion?

Autonomous driving R&D is forecast to grow at 13.14% CAGR as OEMs log terabytes of multi-sensor data for Level 3+ validation.

Why is automotive Ethernet gaining traction over USB?

Ethernet offers higher bandwidth and deterministic communication needed for real-time sensor fusion, supporting a 10.62% CAGR compared with USB’s limited scalability.

How do cybersecurity regulations influence product design?

Rules such as UNECE WP.29 R156 require secure update infrastructures and strict data-access controls, leading suppliers to embed hardware roots of trust and encrypted OTA pipelines.

Which region presents the highest growth opportunity?

Asia-Pacific posts a 10.09% CAGR due to China’s intelligent-connected-vehicle regulations and India’s rapid fleet telematics adoption.

Page last updated on: