Automotive Printed Circuit Board (PCB) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.9 Billion |

| Market Size (2031) | USD 16.91 Billion |

| Growth Rate (2026 - 2031) | 5.56% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Printed Circuit Board (PCB) Market Analysis by Mordor Intelligence

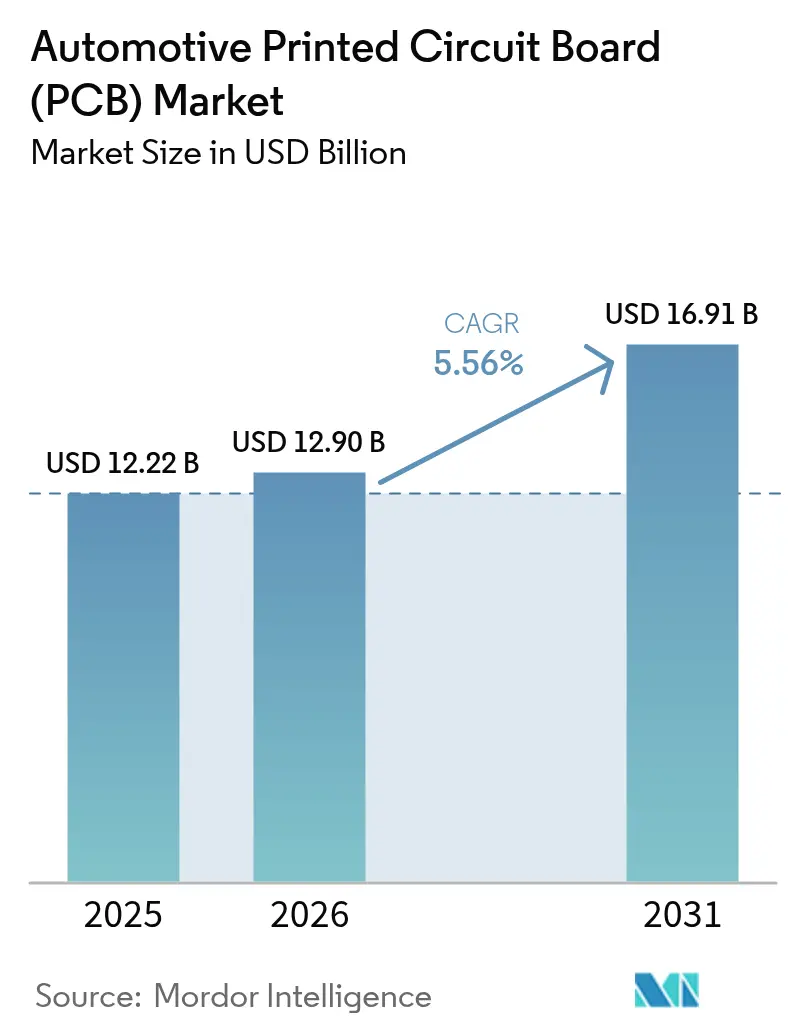

The automotive printed circuit board market size is expected to grow from USD 12.22 billion in 2025 to USD 12.9 billion in 2026 and is forecast to reach USD 16.91 billion by 2031 at 5.56% CAGR over 2026-2031. Growth stems from the rapid shift toward software-defined vehicles that depend on increasingly sophisticated boards to connect high-performance compute, safety sensors, and electrified drivetrains. Mandatory advanced driver-assistance standards, the proliferation of battery-electric platforms, migration to 48 V power nets, and always-connected infotainment expand the addressable automotive printed circuit board market opportunity. Silicon-carbide traction inverters and domain controllers now operate beyond 175 °C, pushing designers toward high-density interconnect and rigid-flex architectures that enhance thermal spreading and signal integrity.

Key Report Takeaways

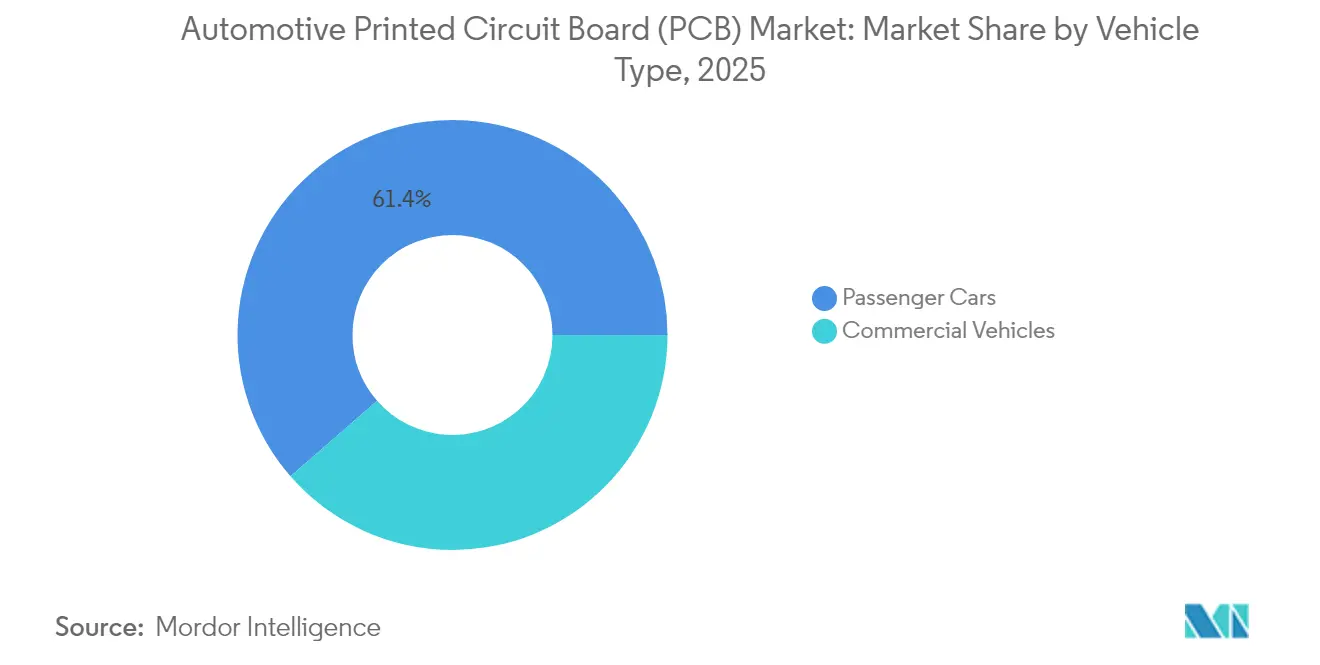

- By vehicle type, passenger cars held 61.42% of the automotive printed circuit board market share in 2025, carrying the fastest CAGR from 6.74% to 2031.

- By propulsion type, internal-combustion powertrains retained 54.96% of the automotive printed circuit board market size in 2025, while battery electric vehicles advance at an 18.29% CAGR through 2031.

- By PCB type, single-layer boards led with 37.92% of the automotive printed circuit board market share in 2025, whereas high-density interconnect solutions are on track for an 11.07% CAGR through 2031.

- By substrate, rigid materials dominated with 69.55% automotive printed board market share in 2025; rigid-flex options post the highest 13.18% CAGR.

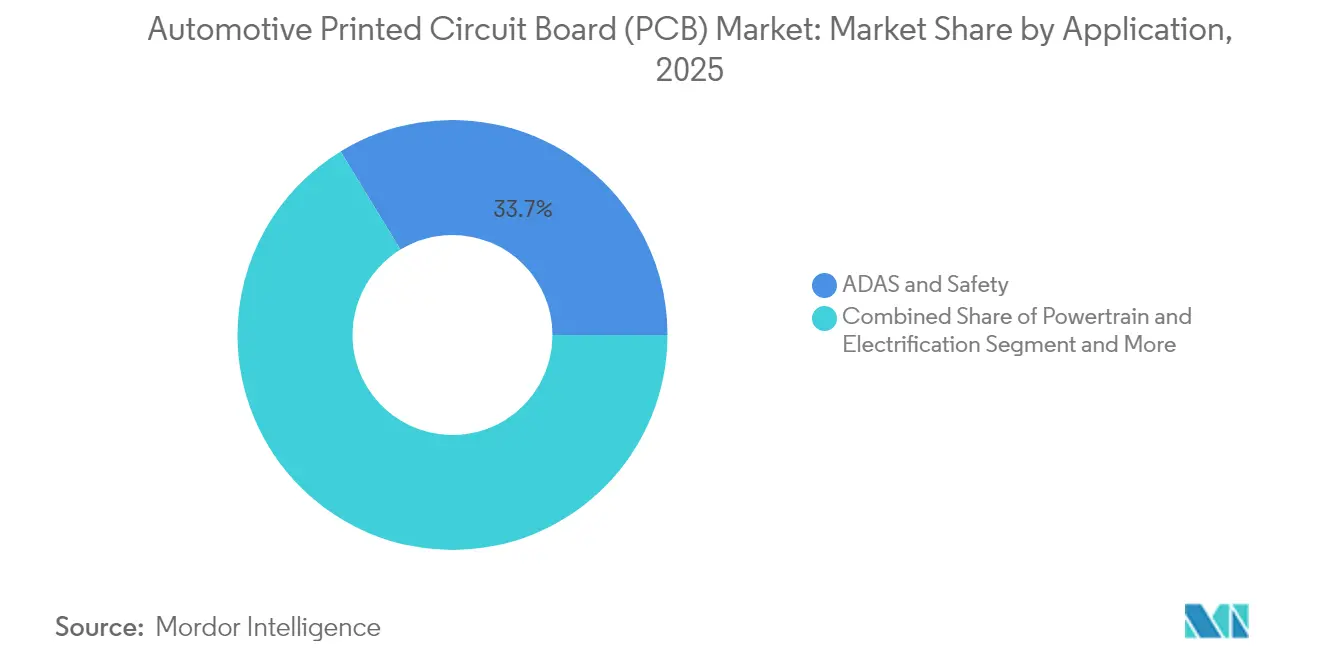

- By application, ADAS and safety systems accounted for 33.71% of the automotive printed circuit board market size in 2025; autonomous-driving compute is projected to grow at 13.86% CAGR.

- By level of automation, SAE Level 0-2 systems controlled 82.12% of the automotive printed board market size in 2025, while Level 4-5 solutions log a 14.78% CAGR through 2031.

- By geography, Asia-Pacific commanded 60.05% share of the automotive printed board market size in 2025 and is set for an 8.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Printed Circuit Board (PCB) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising EV Sales to Fuel PCB Demand | +1.8% | Global, with Asia-Pacific and North America leading adoption | Medium term (2-4 years) |

| ADAS And Safety Regulations | +1.2% | EU and North America primary, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Connected-Infotainment Proliferation | +0.9% | Global, with premium segment leadership in North America and EU | Medium term (2-4 years) |

| Transition to 48V Vehicle Architectures | +0.7% | North America and EU early adoption, Asia-Pacific following | Long term (≥ 4 years) |

| HDI And Flex Board Need | +0.6% | Global, with premium OEMs driving initial deployment | Long term (≥ 4 years) |

| OTA-Upgradable ECUs | +0.5% | Global, with software-defined vehicle leaders prioritizing | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising EV Sales to Fuel PCB Demand

Electric vehicles embed three to four times more board area than combustion cars, swelling volumes across the automotive printed circuit board market. Battery-management systems cycle between –40 °C and 85 °C and still uphold sub-millivolt measurement accuracy, forcing the adoption of thermally conductive laminates rated above 160 °C glass-transition. Copper-heavy layouts tackle inverter currents yet intensify material spend, particularly as spot copper prices increase. Programs that migrate to 800 V architectures impose wider creepage gaps, accelerating demand for advanced dielectrics to maintain insulation without expanding board footprint.

Mandatory ADAS and Safety Regulations

The EU’s General Safety Regulation II makes automatic emergency braking, lane-keeping, and driver monitoring compulsory from July 2024. Parallel rulemaking in the United States requires AEB on light vehicles by 2029[1]“Federal Motor Vehicle Safety Standards; Automatic Emergency Braking Systems for Light Vehicles,” Federal Register, federalregister.gov. Radar and lidar assemblies must sustain tight impedance at 77 GHz, driving high-density interconnect uptake. ISO 26262 Automotive Safety Integrity Level D raises documentation and validation thresholds, effectively rewarding incumbent suppliers within the automotive printed circuit board market that already operate qualified lines.

Connected-Infotainment Proliferation

Digital cockpits integrate multiple 4K displays, Wi-Fi 6E, 5G, and premium audio in one head unit. Boards must support PCIe Gen 4, automotive Ethernet, and MIPI interfaces inside cramped packaging while isolating from 48 V transient spikes. Secure boot, dual-bank flash, and hardware root-of-trust add layers and power draws. Flexible and rigid-flex boards enable curved OLED dash panels, a design lever that elevates differentiation for OEMs courting Gen-Z buyers. These additions swell the layer count and the average selling price in the automotive printed circuit board market.

Transition to 48 V Vehicle Architectures

Migrating to 48 V cuts harness mass up to 85% and slashes I²R losses by 75%, yet raises creepage requirements on power boards. Dual-voltage topologies persist because legacy 12 V devices remain; this forces designers to partition high- and low-voltage domains inside single substrates without cost-prohibitive spacers. Plants that refine etch uniformity on thick-copper lanes and certify against 48 V arcing secure long-term contracts across the automotive printed circuit board market[2]Christian Cruz, "The Power of 48 V: Relevance, Benefits, and Essentials in System-Level Applications", Analog Devices, analog.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex Design and Integration Challenges | -0.8% | Global, with higher impact in emerging automotive markets | Medium term (2-4 years) |

| Copper-Price Volatility | -0.6% | Global, with particular pressure on high-volume manufacturers | Short term (≤ 2 years) |

| Sic Power Modules' Thermal-Reliability Issues | -0.4% | Global, affecting premium EV segment primarily | Long term (≥ 4 years) |

| Lengthy ISO 26262 Safety-Audit Cycles | -0.3% | Global, with stricter enforcement in EU and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Complex Design and Integration Challenges

Modern vehicles juggle RF, power, and digital subsystems in centimeters of board real estate. Silicon-carbide modules sustain over 175 °C, so materials need low-expansion coefficients. Shortages of engineers versed in automotive functional-safety layout slow time-to-market. Incumbents that automate design-for-reliability cut-and-try loops enlarge their hold on the automotive printed circuit board market.

Copper-Price Volatility Squeezing Margins

Every multilayer board rides copper pricing. High-density interconnect stack-ups with heavy copper pours see cost spikes when metal markets tighten. Large vendors hedge, but smaller fabs lack bargaining weight and retreat from capital-intensive automotive bids, nudging consolidation within the automotive printed circuit board market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger Cars Drive Market Expansion

Passenger cars accounted for 61.42% of the automotive printed circuit board market size in 2025 and are expanding at a 6.74% CAGR to 2031. Feature-rich cabins, advanced parking assistance, and 48 V networks multiply the board area to more than 5 m² in premium trims. Commercial fleets emphasise durability, adopting metal-core or thick-copper FR-4 for brake and suspension controllers exposed to vibration. Passenger-car electrification and connectivity motives thus anchor volume growth that reinforces the scale economics of the automotive printed circuit board market.

Commercial vans remain a strategic subsector as e-commerce logistics pivot toward zero-emission zones. Predictive maintenance telematics sparks demand for ruggedised telematics PCBs. The bus and truck segments take longer to shift because of infrastructure gaps. However, when they adopt electric drivelines, board power densities climb sharply, underpinning fresh revenue streams for the automotive printed circuit board market.

By Propulsion Type: Electric Powertrains Reshape PCB Requirements

ICE vehicles dominated the automotive printed circuit board market size with a 54.96% share in 2025, while battery electric vehicles recorded an 18.29% CAGR, becoming the high-growth engine of the automotive printed circuit board industry. Battery-management, inverter, and on-board-charger boards now require dielectric breakdown strengths above 40 kV/mm to satisfy 800 V systems. Hybrid modules overlay combustion and electric domains, doubling thermal zones and complicating ground isolation. Internal-combustion vehicles remain the majority volume but shift toward turbo-48V mild hybrids, ensuring baseline demand.

In BEVs, thermally conductive yet electrically insulating fillers in prepregs cool power MOSFETs, extending range. Hybrid designs embed isolated gate drivers on the same board as engine controllers, shrinking wiring harnesses. The propulsion mix divergence across regions shapes localised design centre specialisations, all fuelling diversification in the automotive printed circuit board market.

By PCB Type: HDI Technology Drives Innovation

Single-layer panels kept 37.92% of the automotive printed circuit board market share in 2025, servicing lighting and simple sensor tasks. High-density interconnect formats post an 11.07% CAGR through 2031, as radar front ends stipulate stacked vias and laser-drilled microvias under 75 µm. Automotive printed circuit board market suppliers with sequential lamination and resin plugging dominate premium ADAS bids.

Rigid-flex deployments marry inflexible compute sections to tail flexes that remove connectors, raising reliability. These architectures reduce assembly time by up to 30%, an attractive lever for OEM cost control. Entry-level cars stick with double-layer FR-4 where density needs lag, sustaining volume for cost-optimised board shops and balancing product mix across the automotive printed circuit board market.

By Substrate: Rigid Substrates Dominate Current Applications

Rigid FR-4 and metal-core formats capture 69.55% of the automotive printed circuit board market size in 2025. They withstand moisture ingress, vibration, and thermal cycles repeated millions of times. Rigid-flex combinations deliver the fastest 13.18% CAGR to 2031, slashing harness weight in steering-wheel controls and door modules. Metal-core boards migrate from LED headlights into DC-DC converters, their aluminium backplanes doubling as heat sinks.

Thermally conductive polymeric substrates pop up in 2027-plus BEV inverters, promising mass cuts critical for range. Flexible polyimide remains the go-to for bend zones and rotating parts. Material choice thus hinges on application thermal and mechanical stress rather than price alone, a trend lifting value capture per unit within the automotive printed circuit board market.

By Application: ADAS Systems Lead Electronic Content Growth

ADAS and safety boards accounted for a share of 33.71% in the automotive printed circuit board market size in 2025 as regulations tightened. Millimeter-wave radar arrays use eight-layer HDI with in-plane phase-matched nets that require ±2% impedance control. Autonomous compute, though small today, houses stacked high-bandwidth memory on interposers, chasing a 13.86% CAGR that will upscale volumes for high-layer-count shops in the automotive printed circuit board market.

Power-train electrification pushes thick-copper planes and buried busbars. Body comfort stays cost-sensitive yet still upgrades to CAN-FD or automotive Ethernet, adding layers incrementally. Infotainment drives the adoption of flexible OLED backing boards. These diverse applications create a balanced portfolio that shields the automotive printed circuit board market from swings in any single vehicle subsystem.

By Level of Automation: Higher Autonomy Drives PCB Complexity

SAE Level 0-2 vehicles dominate 82.12% of the automotive printed circuit board market share, but Level 4-5 prototypes deliver a 14.78% CAGR. Level 3 boards gracefully transfer control between driver and machine by juggling redundant CPUs, dual power regulators, and safety monitors. Full autonomy boards exceed 1 TB/h data throughput and embed liquid-cooling cold plates into multilayer stack-ups.

Lockstep micro-controllers, watchdogs, and instantaneous checksum comparators trigger more complexity than consumer electronics of similar compute power. Suppliers who co-design board and cooling hardware position themselves as strategic partners to autonomy program leaders, securing higher-margin contracts inside the automotive printed circuit board market.

Geography Analysis

Asia-Pacific captured 60.05% of the automotive printed circuit board market size in 2025 and is forecast to post an 8.18% CAGR to 2031, cementing its status as the volume bedrock of the automotive printed circuit board market. China leads with scaled factories and seasoned operators; yet rising wages and geopolitical tensions drive “China + 1” sourcing. Thailand, Malaysia, and Vietnam roll out incentives and modern fabs capable of HDI and rigid-flex builds, granting OEMs supply-chain resilience.

North America holds a moderate share but owns high-value niches, such as silicon-carbide inverters, radar arrays, and cybersecurity-hardened telematics. Design-service boutiques around Detroit and Austin shorten prototype iterations, which is crucial for start-ups launching electric pickups. Policy incentives that foster domestic substrate and chip output may gradually close the cost gap versus Asia and lift on-shore board bookings, enriching the regional slice of the automotive printed circuit board market.

Europe, on the other hand, remains an engineering powerhouse. Premium German and Swedish marques enforce ISO 26262 traceability and zero-ppm contracts, favouring supply chains with automated optical inspection and X-ray via-fill validation. The continent pioneers 48 V and zonal architectures, keeping domestic design consultancies pivotal to advancing the automotive printed circuit board market. South America and the Middle East/Africa contribute modestly today, but local assembly plants in Brazil and Morocco seek regional board sources to dodge import tariffs.

Competitive Landscape

The automotive printed circuit board market is moderately consolidated, with the top five companies controlling a substantial global revenue share. Consolidation accelerates as automakers prefer fewer partners able to deliver design, simulation, fabrication, and assembly under a single quality-management system. Thermally enhanced HDI capability forms a moat that deters commoditised rivals.

Suppliers differentiate through process technology. Via-fill and back-drill accuracy at sub-100 µm, resin-coated copper for flex stiffeners, and embedded-component techniques reduce board count and harness length. Plants that run AEC-Q200 screening on laminates and employ automotive statistical-process control secure multiyear awards. Vendors acquiring EDA toolchains, as seen when Renesas bought Altium, integrate schematic capture and manufacturing knowledge, enabling “shift-left” validation and tighter collaboration with OEM E/E architects.

Strategic moves include metal-core innovation for traction inverters, dielectric formulations for 48 V boards, and pre-certified reference layouts that cut six months of development time. Partnerships between board fabricators and semiconductor houses create turnkey modules encompassing substrate, driver ICs, and thermal interface. Such vertical integration boosts entry barriers and tilts bargaining power toward established players, strengthening their foothold in the automotive printed circuit board market.

Automotive Printed Circuit Board (PCB) Industry Leaders

-

Samsung Electro-Mechanics

-

Unimicron Technology Corp.

-

Meiko Electronics Co. Ltd

-

TTM Technologies Inc.

-

Amitron Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Empyrean Technology acquired Xpeedic Technology, boosting domestic EDA ecosystems for automotive board simulation.

- December 2024: Ventec International Group unveiled Thailand's USD 17 million automotive PCB materials manufacturing facility, which aims to produce 150,000 sheets monthly by Q1 2026.

- August 2024: Bain Capital assumed control of Somacis, widening the latter’s reach in high-mix, mission-critical automotive boards.

- June 2024: Amber Enterprises announced an INR 2,000 crore (USD ~235 million) investment to develop an Indian PCB plant serving the automotive and IT sectors.

Global Automotive Printed Circuit Board (PCB) Market Report Scope

An automotive PCB is a complex circuit used to control all the electronics present in a vehicle. Automotive PCBs are used for common functions like deploying airbags and controlling other safety aids like the Electronic Stability Program (ESP) and Hill Assist Descent. They also control ADAS features like adaptive cruise control and parking sensors in a vehicle. An automotive PCB consists of a board made up of non-conductive material on which all other electronic components like sensors and microcontrollers are mounted.

The automotive PCB market has been segmented by vehicle type, propulsion type, and geography. By vehicle type, the market is segmented into Passenger Vehicles and Commercial Vehicles. By propulsion type, the market is segmented into IC Engine and Electric. By geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the World. For each segment, market sizing and forecasting were done based on value (in USD).

| Passenger Cars |

| Commercial Vehicles |

| ICE Vehicles |

| Battery Electric Vehicles (BEV) |

| Hybrid and Plug-in Hybrid Vehicles |

| Single-Layer |

| Double-Layer |

| Multi-Layer |

| High-Density Interconnect (HDI) |

| Rigid-Flex / Flexible |

| Rigid (FR-4 and metal-core) |

| Flexible Polyimide |

| Rigid-Flex |

| ADAS and Safety |

| Powertrain and Electrification |

| Body and Comfort |

| Infotainment and Connectivity |

| Autonomous Driving Compute |

| SAE Level 0 - 2 |

| SAE Level 3 |

| SAE Level 4 - 5 |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Arzentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Cars | |

| Commercial Vehicles | ||

| By Propulsion Type | ICE Vehicles | |

| Battery Electric Vehicles (BEV) | ||

| Hybrid and Plug-in Hybrid Vehicles | ||

| By PCB Type | Single-Layer | |

| Double-Layer | ||

| Multi-Layer | ||

| High-Density Interconnect (HDI) | ||

| Rigid-Flex / Flexible | ||

| By Substrate | Rigid (FR-4 and metal-core) | |

| Flexible Polyimide | ||

| Rigid-Flex | ||

| By Application | ADAS and Safety | |

| Powertrain and Electrification | ||

| Body and Comfort | ||

| Infotainment and Connectivity | ||

| Autonomous Driving Compute | ||

| By Level of Automation | SAE Level 0 - 2 | |

| SAE Level 3 | ||

| SAE Level 4 - 5 | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Arzentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected size of the automotive printed circuit board market by 2031?

The automotive printed circuit board market size is projected to reach USD 16.91 billion by 2031 on a 5.56% CAGR trajectory.

Which vehicle category contributes the largest revenue share?

Passenger cars represent 61.42% of the automotive printed circuit board market due to high electronics content.

Why is high-density interconnect technology growing quickly?

HDI boards enable compact routing for radar, camera, and zonal controllers, driving an 11.07% CAGR within the automotive printed circuit board market.

How does copper-price volatility influence board suppliers?

Spikes increase material costs, pressuring margins; larger suppliers hedge, but smaller fabs face consolidation risks in the automotive printed circuit board market.

Which region shows the fastest growth outlook?

Asia-Pacific leads growth with an 8.18% CAGR, anchored by China’s capacity and Southeast Asia’s new fabs.

What capabilities do automakers value most in board partners?

Integrated design-to-manufacture services, ISO 26262 compliance, and advanced thermal-management know-how are paramount inside the automotive printed circuit board market.

Page last updated on: