Market Overview

| Study Period | 2020 - 2031 |

|---|---|

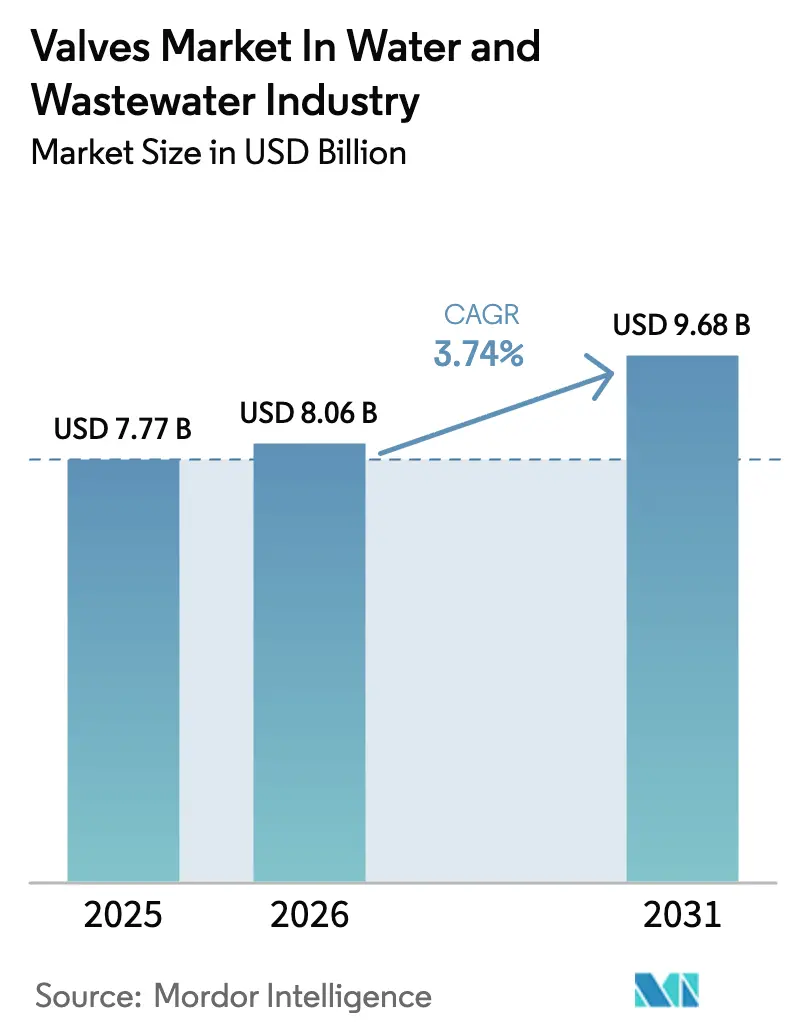

| Market Size (2026) | USD 8.06 Billion |

| Market Size (2031) | USD 9.68 Billion |

| Growth Rate (2026 - 2031) | 3.74% CAGR |

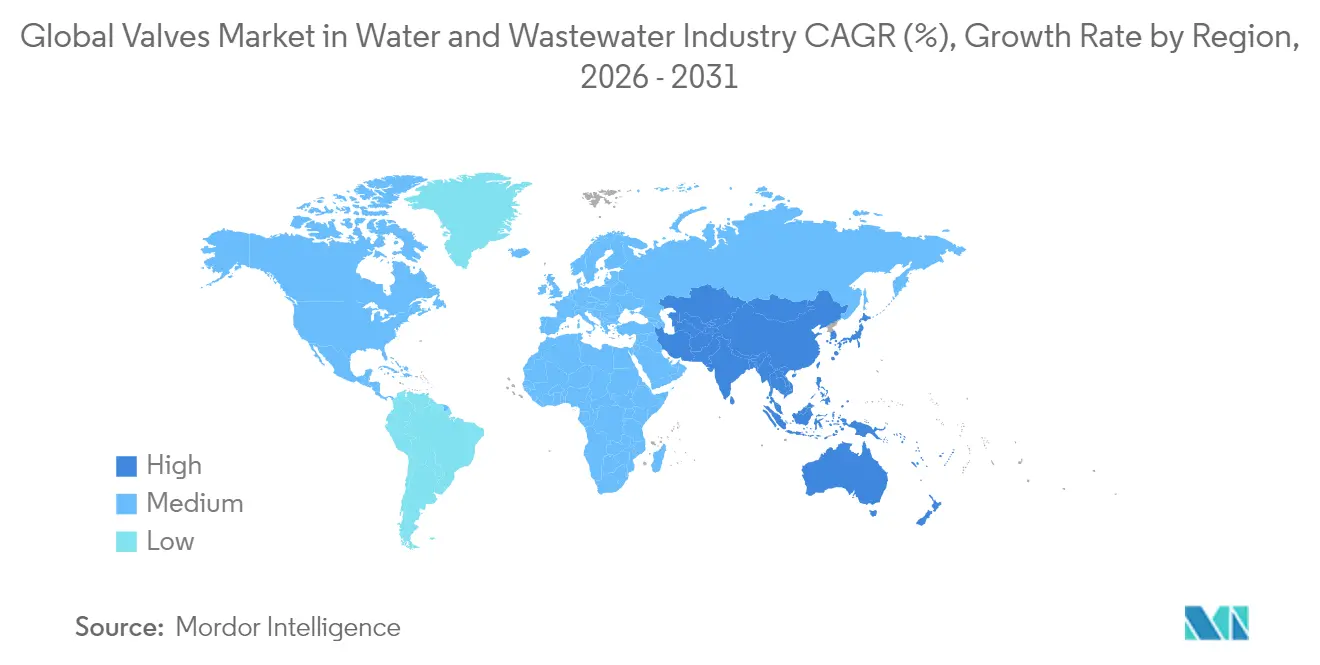

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Water and Wastewater Valves Market Analysis by Mordor Intelligence

The Valves market size in water and wastewater industry was valued at USD 7.77 billion in 2025 and estimated to grow from USD 8.06 billion in 2026 to reach USD 9.68 billion by 2031, at a CAGR of 3.74% during the forecast period (2026-2031). A measured expansion reflects steady infrastructure modernization, stricter discharge regulations and the rise of high-pressure desalination assets that collectively reshape procurement priorities for municipal and industrial operators. The combination of aging distribution networks, widening regulatory mandates such as emerging PFAS limits, and a growing appetite for IIoT-enabled remote monitoring is encouraging utilities to migrate from legacy gate valves toward automation-ready ball and butterfly formats. Consolidation among established manufacturers is gathering pace as Emerson, Flowserve and other majors acquire targeted specialists to secure digital capabilities and severe-service know-how, while regional producers expand Asian footprints to capture brisk public-sector spending.[1]World Pumps, “Pumps M&A Review 2024,” worldpumps.com Meanwhile, supply-chain volatility in nickel- and copper-based alloys keeps input costs unpredictable, nudging buyers toward thermoplastic and composite bodies that also satisfy circular-economy preferences.

Key Report Takeaways

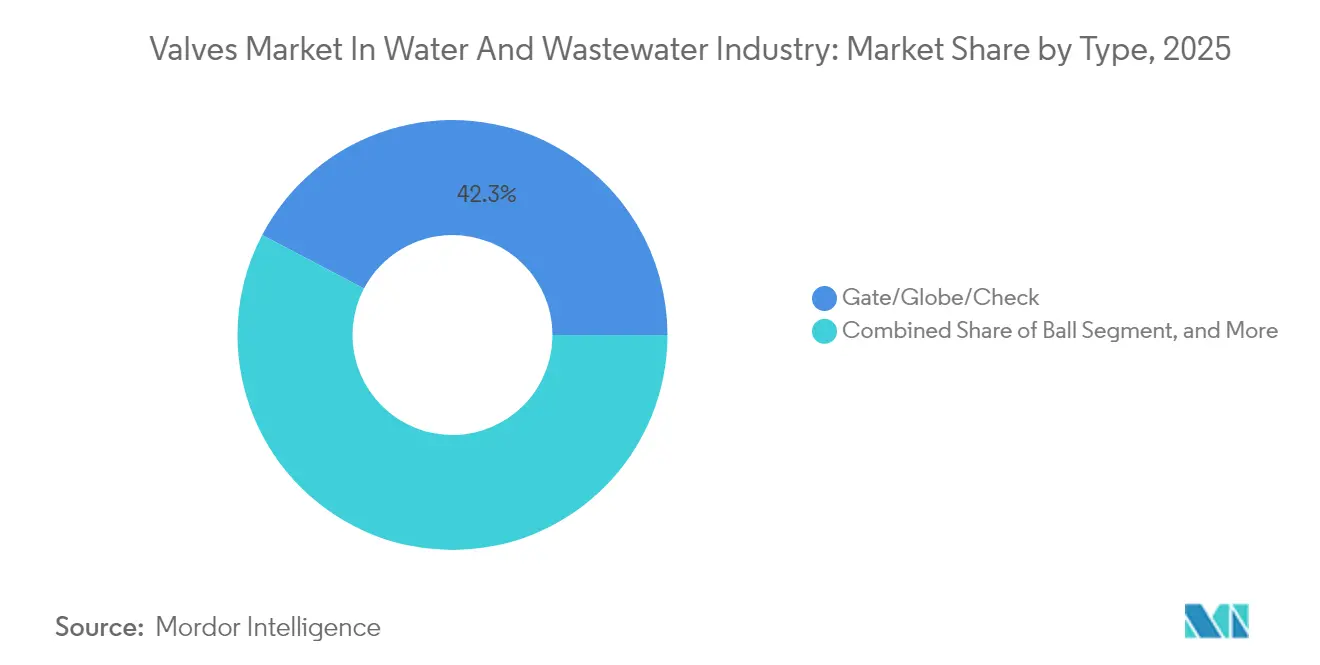

- By type, gate/globe/check valves led with 42.30% revenue share in 2025 in the Water and Wastewater Valves Market market in water and wastewater industry, whereas ball valves are poised for the fastest 4.79% CAGR through 2031.

- By material, cast and ductile iron retained 37.40% of the Water and Wastewater Valves Market in 2025, yet thermoplastics and composites are projected to expand at a 4.55% CAGR over the same horizon.

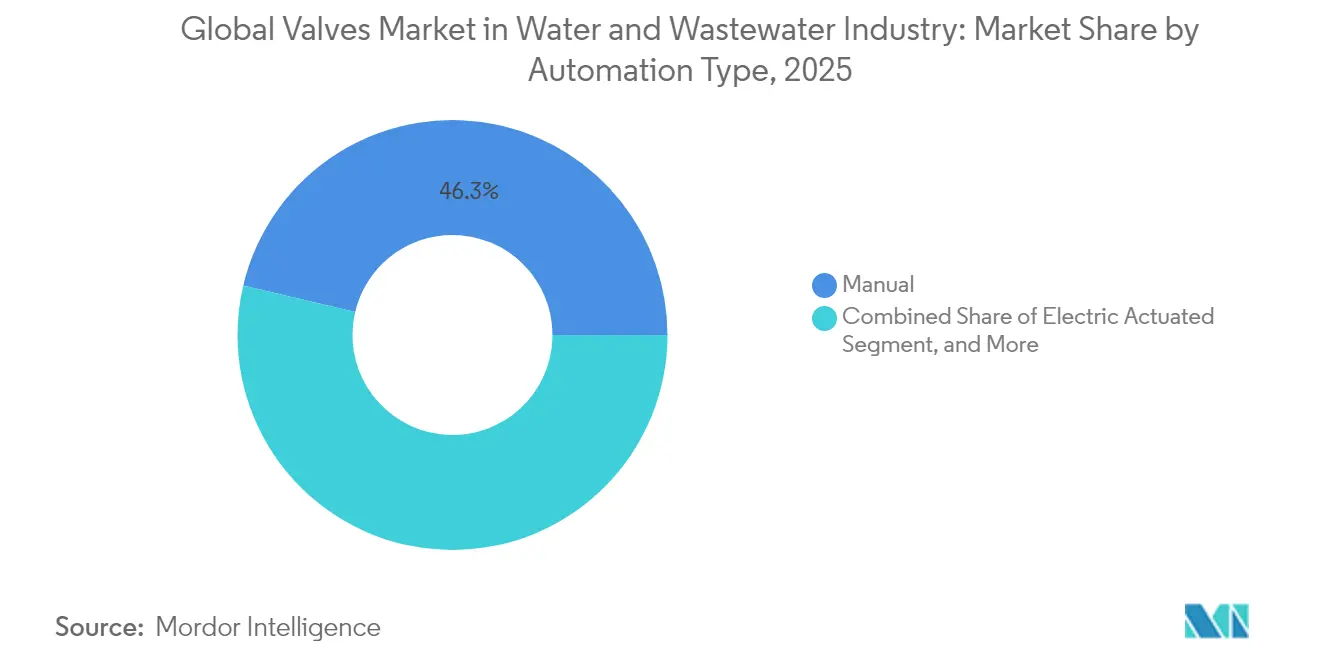

- By automation type, manual systems captured 46.30% of the Water and Wastewater Valves Market in 2025, while smart/IIoT-integrated solutions headline growth with a 4.88% CAGR to 2031.

- By application, municipal potable-water distribution held 38.40% of 2025 revenues in the Water and Wastewater Valves Market, but desalination plants are forecast to post the quickest 4.66% CAGR.

- By geography, Asia-Pacific commanded 34.40% of global sales in 2025 in the Water and Wastewater Valves Market and will compound at a 4.56% CAGR, underscoring its twin role as both scale leader and growth engine.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Water and Wastewater Valves Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising automation in water and wastewater facilities | +1.2% | Global, with APAC and North America leading adoption | Medium term (2-4 years) |

| Tightening discharge-quality limits drive upgrades | +0.8% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Ageing municipal infrastructure replacement cycle | +0.9% | North America and Europe core, emerging in APAC urban centers | Long term (≥ 4 years) |

| Surge in desalination CAPEX, esp. GCC and Australia | +0.7% | GCC, Australia, with spillover to Mediterranean and California | Medium term (2-4 years) |

| Low-power IIoT actuators cut OPEX | +0.4% | Global, concentrated in developed markets initially | Short term (≤ 2 years) |

| Circular-economy push for recyclable valve bodies | +0.3% | EU leading, North America following, APAC selective adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Automation in Water and Wastewater Facilities

Utilities are moving past basic SCADA toward distributed sensor networks and low-power IIoT actuators that enable condition-based maintenance and real-time pressure optimization.[2]ValvTechnologies, “ValvXpress Off-the-Shelf Actuator Packages,” valvtech.com Field trials report 15–20% declines in unplanned maintenance as smart valves flag seal wear or stem friction before failure. Quarter-turn ball designs gain favor because they couple easily with compact electric drives, reducing energy draw compared with multi-turn gate formats. The cybersecurity dimension grows more visible after a 300% jump in ransomware attacks on U.S. water systems between 2021–2023, compelling operators to insist on hardened controllers and segmented networks.[3]WaterWorld, “Mitigating PFAS Is Going to Be Expensive,” waterworld.comAutomation rollouts thus bundle mechanical upgrades with secure firmware and encrypted links, anchoring a durable uptick in the market.

Tightening Discharge-Quality Limits Drive Upgrades

Stricter effluent norms are another durable catalyst. The U.S. EPA’s impending PFAS rule imposes monitoring by 2027 and full-scale remediation by 2029, translating into USD 1.548 billion in annual compliance outlays, of which USD 1.506 billion is earmarked for treatment and disposal hardware. Granular activated carbon beds, anion-exchange skids and reverse-osmosis trains require fresh isolation, control and sampling valves made from stainless steel or fluorine-free polymers resistant to aggressive backwash chemicals. Higher pressures within nanofiltration loops also raise demand for finely machined control trims capable of throttling 60-bar feed streams without cavitation. Because non-compliance risks stiff penalties, utilities are fast-tracking procurement tenders, compressing delivery schedules and tightening bid specifications, stimulating premium-priced niches within the market.

Ageing Municipal Infrastructure Replacement Cycle

Across the United States and Western Europe, vast portions of post-war distribution pipe now approach systemic end-of-life. The American Water Works Association pegs national renewal needs at over USD 1 trillion through 2039, with valves commanding a sizeable slice of every network project budget. California American Water’s acquisition of Dublin San Ramon Services District unlocked immediate modernization workstreams that prioritize swap-outs of 1960s-vintage cast-iron gate valves for automation-ready ductile-iron or thermoplastic ball models. Such projects do more than like-for-like substitution; they typically bundle pressure management, flow metering and emergency-isolation upgrades, multiplying valve counts per kilometer. Because many mid-sized cities now confront similar asset-health curves, momentum behind this replacement wave will underpin the Water and Wastewater Valves Market throughout the decade.

Surge in Desalination CAPEX, especially GCC and Australia

Water-scarce Gulf states and Australia are scaling reverse-osmosis megaprojects that each deploy 5,000–10,000 valves across intake, pretreatment, high-pressure and product-water zones. Saudi Arabia’s Vision 2030 alone allocates multibillion-dollar budgets to seawater desalination, favoring duplex and super-duplex alloys as well as advanced thermoplastics with seawater corrosion resilience. Australia’s newest 160-billion-liter facility illustrates the product intensity: thousands of high-pressure check valves, corrosion-proof butterfly types for brine discharge and lined globe valves for chemical dosing. Because projects tend to be EPC-led and lumpy, manufacturers with specialized metallurgy and field-engineering services gain disproportionate order share. Together, these capital programs add a geographically concentrated but high-value layer to the Water and Wastewater Valves Market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain volatility in nickel and copper alloys | -0.6% | Global, with particular impact on stainless steel and duplex alloy valve production | Short term (≤ 2 years) |

| Skilled-labour shortage delays retrofits | -0.4% | North America and Europe primarily, emerging in APAC developed markets | Medium term (2-4 years) |

| Cyber-security concerns slow smart-valve adoption | -0.3% | Global, concentrated in developed markets with advanced infrastructure | Medium term (2-4 years) |

| Rising PFAS-focused regulations increase qualification costs | -0.2% | North America and EU leading, expanding to APAC regulatory frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Volatility in Nickel and Copper Alloys

Nickel supply disruptions and copper-price spikes squeeze margins on stainless and brass valves, prompting vendors to hedge metal costs or qualify alternate chemistries. Smaller manufacturers with lower purchasing leverage feel the sting most acutely, risking order backlogs when alloy bar stock runs short. Because duplex and super-duplex grades dominate desalination and corrosive-service bids, even brief commodity hiccups can delay EPC schedules, putting downward pressure on the Water and Wastewater Valves Market quarterly run rate.

Skilled-Labour Shortage Delays Retrofits

Valve installation and commissioning rely on a shrinking cohort of pipefitters and control-systems technicians. Utilities now report 20–30% longer project durations as experienced crews retire faster than apprentices enter the trade. Smart-valve retrofits, which require firmware uploads and encrypted network integration, amplify the skills gap. Higher labor premiums inflate total installed cost, convincing some municipalities to defer non-urgent replacements and thereby softening near-term demand in the Valves market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Ball Valves Drive Automation Adoption

Ball valves accounted for 4.79% CAGR through 2031, outpacing the broader Water and Wastewater Valves Market and eroding the long-held dominance of gate/globe/check units, which still held 42.30% revenue share in 2025. The swing stems from quarter-turn geometry that mates cleanly with compact electric actuators, minimizing torque demands and lowering power budgets. In distribution upgrades, utilities frequently specify ball designs when replacing seized gate models because the newer bodies reduce head loss and virtually eliminate stem-packing leaks. Manufacturers answer by offering modular ball platforms with ISO 5211 mounting pads, easing actuator retrofits and shortening outage windows. At the same time, emerging zero-emission plug varieties such as Mokveld’s seal-less concept are winning specification points where fugitive emissions clauses tighten. Control, pressure-relief and air-release categories maintain steady demand, especially inside treatment basins where flow modulation and surge protection remain paramount. Overall, product-mix evolution signals a gradual recalibration rather than abrupt displacement: by 2030, gate/globe/check assemblies will still form a large installed base but incremental growth favors ball and high-performance butterfly formats, an orientation that sustains the Water and Wastewater Valves Market market size expansion in both brownfield and greenfield jobs.

Ball momentum also intersects with automation trends. Quarter-turn cycles enable faster shutdown sequences critical for cybersecure remote isolation, a growing requirement in North American resilience planning. Developers of packaged desalination skids likewise choose ball bodies because corrosion-resistant internals survive aggressive RO cleaning chemicals. As digital monitoring gains mindshare, the Valves industry thus finds ball technology aligned with predictive-maintenance software, reinforcing a virtuous loop between mechanical design and IIoT rollout.

By Material: Thermoplastics Gain Amid PFAS Concerns

Cast and ductile iron preserved 37.40% share in 2025 on the back of cost-efficient municipal distribution grids, yet thermoplastics and composites are sprinting ahead at a 4.55% CAGR. Regulators scrutinizing PFAS leakage spur a pivot toward fluorine-free polymer seats such as UHMW-HDPE, exemplified by Hayward Flow Control’s newest true-union series. European procurement frameworks increasingly award circular-economy points for products documenting above 95% recyclability, pushing makers to redesign bodies for mono-material recovery. Stainless and duplex alloys still dominate seawater and chemically aggressive loops, particularly within GCC desalination lines where chloride pitting dictates premium metallurgy. Yet rising alloy quotations tilt lifecycle cost appraisals in favor of engineered plastics, especially on low-pressure irrigation or storm-water gates. As PFAS curbs strengthen, the Water and Wastewater Valves Market market size tied to non-fluorinated polymers will likely accelerate further, aided by drop-in designs that simplify operator qualification steps.

A second driver for composites is weight savings. In elevated reservoirs or rooftop booster sets, lightweight glass-reinforced nylon valves cut crane time and footing loads, allowing faster installs. Meanwhile, zero-lead brass mandates in several U.S. states open doors for plastic potable-water checks certified to NSF-61. The Valves industry therefore navigates a nuanced material matrix: iron remains cheap and familiar, stainless resists corrosion, but next-generation polymers are capturing growth lanes where sustainability, weight and tightening metal supply intersect.

By Automation Type: Manual Systems Persist Despite Smart Growth

Manual hand-wheel operation still governed 46.30% of sales in 2025 because tens of thousands of secondary mains, branch laterals and isolated rural sites cannot justify automation’s capex. However, smart/IIoT-integrated packages will post a 4.88% CAGR as utilities chase OPEX savings and regulatory bodies urge cyber-resilience. Suppliers bundle encrypted Bluetooth commissioning, edge analytics and solar back-up modules to allay hacking fears without burdening grid power budgets. Electric actuation maintains healthy uptake for precision dosing lines, while pneumatics carve a niche in plants already running compressed-air loops for instrumentation. Hydraulic drives endure within large-bore penstocks where stall torque soars but control cycle counts stay modest. entrenched manual stock coexists with digitally fluent newcomers, with labor shortages prodding fence-sitters toward automation once payback exceeds five years.

Vendor competitive tactics mirror this split. Tier-one producers monetize data portals tied to proprietary cloud dashboards, whereas regional outfits push low-cost stainless hand-wheels. Over time, predictive-maintenance outcomes, fewer truck rolls, fewer flooded vaults, will broaden smart adoption, especially after insurers price resilience credits into premiums. Still, a proportion of gravity-fed or intermittently used pipelines will likely remain manual well beyond 2030, ensuring product-line breadth remains a core requirement across the Valves industry.

By Application: Desalination Plants Accelerate Growth

Municipal potable-water distribution absorbed 38.40% of revenue in 2025, an anchor that stabilizes the broader Water and Wastewater Valves Market market through steady replacement cycles. Yet desalination plants will outstrip all other segments with a 4.66% CAGR as GCC states, Australia and parts of Southern Europe underwrite massive reverse-osmosis outlays. Each 500 million-liter-per-day installation demands rows of high-pressure, corrosion-proof valves for feed pumps, energy-recovery devices and brine discharge headers. Because downtime carries hefty cost penalties, EPCs demand extended 3-year warranties and on-site spares, raising average revenue per valve well above distribution-grid norms. Municipal wastewater, irrigation and storm-water continue to generate resilient, if slower, growth as urban intensification strains existing networks. Meanwhile, specialized industrial wastewater niches, from pulp and paper to food processing, sustain a modest premium segment driven by tailored metallurgy and sanitary design requirements.

The interplay between scarcity economics and technology specificity makes desalination a strategic high-ground. European and North American manufacturers with pedigree in titanium overlay or super-duplex castings hold a credibility edge, though rising localization in Saudi Arabia and the United Arab Emirates is spurring joint-venture fabrication shops. For the Water and Wastewater Valves Market market, that means a rising share of high-margin units despite only incremental volumetric tonnage increases.

Geography Analysis

Asia-Pacific captured 34.40% of 2025 turnover and will deliver a market-leading 4.56% CAGR through 2031. China drives a dominant slice via mega-projects like the Sichuan PPP water-supply overhaul and the Shanghai Qingcaosha intake expansion, each packing tens of thousands of isolation and control valves. India follows suit under sectoral reforms targeting USD 2.8 billion in annual water infrastructure spending by 2025, spurring domestic production hubs such as Bürkert’s new Pune plant that trims lead times for local tenders. Japan, South Korea and Australia contribute with renewal programs focusing on leakage reduction and desalination backup capacity.

North America and Europe log mature but sizeable replacement-driven outlays, with federal subsidies for lead-service-line removal and PFAS compliance keeping order books filled. The Middle East commands disproportionately high unit values stemming from super-duplex content in seawater systems. Africa and South America exhibit patchier spending, though Chile’s mining-backed desal initiatives inject pockets of high-spec demand. Taken together, Asia-Pacific’s volume leadership and the Middle East’s premium mix assure diversified revenue channels across the Water and Wastewater Valves Market market, cushioning suppliers against country-specific swings.

Competitive Landscape

The global supplier base is moderately fragmented, yet a discernible consolidation trend is elevating scale advantages. Emerson’s USD 3.15 billion take-over of Pentair’s Valves and Controls line vaults it into a top-tier position across municipal, industrial and energy verticals. Flowserve’s USD 290 million acquisition of Mogas Industries broadens severe-service credentials that dovetail with high-pressure desalination, while also adding extensive aftermarket field-service teams able to lock-in lifecycle contracts. These moves foreshadow deeper convergence between mechanical hardware and digital analytics, as larger entities bundle cloud diagnostics, cybersecurity modules and performance-based service models.

Mid-cap specialists respond by sharpening niche propositions. Hayward bets on PFAS-free thermoplastics, winning municipal bids anxious about future material bans. Mokveld exploits emissions-free designs to target utilities governed by new methane-leak protocols. In parallel, component makers form ecosystem alliances, actuator vendors with encryption houses, sensor firms with platform players, to deliver holistic packages compliant with water-sector reliability codes. Geographic expansion also stays active: Bürkert’s Pune factory positions it closer to Asia-Pacific growth corridors, while Metso’s Australian buyout increases exposure to slurry-rich mining water loops, hedging commodity cycles.

Competitive intensity remains moderate, with price wars checked by technical qualification hurdles and the bespoke nature of many treatment projects. Nevertheless, supply-chain strain around nickel and freight costs pressures margins, rewarding operators that leverage multi-region footprint to rebalance sourcing. Cyber-hardened products could emerge as the next battleground as insurance carriers begin to mandate certified secure valves for critical infrastructure, a shift likely to favor players with integrated OT-security stacks.

Water and Wastewater Valves Industry Leaders

Emerson Electric Co.

Schlumberger Limited

Alfa Laval Corporate AB

Flowserve Corporation

Crane Holdings

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Flowserve completed the acquisition of Mogas Industries for USD 290 million plus up to USD 15 million in earn-out payments, enlarging its severe-service valve line for high-pressure applications.

- December 2024: Xylem bought a majority position in Idrica to fold advanced analytics into the Xylem Vue platform, expanding digital-water offerings.

- November 2024: Emerson finalized its USD 3.15 billion purchase of Pentair’s Valves and Controls business, forming one of the broadest valve portfolios worldwide.

- October 2024: Metso took over Australia’s Jindex Pty Ltd to sharpen slurry-handling solutions across mining and water treatment.

Global Water and Wastewater Valves Market Report Scope

A valve acts as a passage for restricting or allowing fluid flow in pipelines and other devices. The valves are designed to help the customers to safely optimize the flow through pump control stations and assemblies requiring special surge equipment and safety shutoffs. It is used also to protect against reverse flow or prevent slamming problems.

The study tracks the market based on the revenues generated by different vendors operating in the Global Valves market. The scope is limited to the types of valves used in water and wastewater. The market study doesn't offer drilldown breakup of the regional shares for the countries.

By Type

| Ball |

| Butterfly |

| Gate/Globe/Check |

| Plug |

| Control |

| Pressure-relief and Air-release |

By Material

| Cast Iron and Ductile Iron |

| Carbon Steel |

| Stainless Steel |

| Alloy (Duplex, Nickel-based) |

| Thermoplastics and Composites |

By Automation Type

| Manual |

| Electric Actuated |

| Pneumatic Actuated |

| Hydraulic Actuated |

| Smart/IIoT-Integrated |

By Application

| Municipal Potable-Water Distribution |

| Municipal Wastewater Treatment |

| Desalination Plants |

| Irrigation and Storm-Water Networks |

| Industrial Wastewater (Food, Pulp and Paper, Chemicals) |

By Geography

| North America |

| South America |

| Europe |

| Asia-Pacific |

| Middle East and Africa |

| By Type | Ball |

| Butterfly | |

| Gate/Globe/Check | |

| Plug | |

| Control | |

| Pressure-relief and Air-release | |

| By Material | Cast Iron and Ductile Iron |

| Carbon Steel | |

| Stainless Steel | |

| Alloy (Duplex, Nickel-based) | |

| Thermoplastics and Composites | |

| By Automation Type | Manual |

| Electric Actuated | |

| Pneumatic Actuated | |

| Hydraulic Actuated | |

| Smart/IIoT-Integrated | |

| By Application | Municipal Potable-Water Distribution |

| Municipal Wastewater Treatment | |

| Desalination Plants | |

| Irrigation and Storm-Water Networks | |

| Industrial Wastewater (Food, Pulp and Paper, Chemicals) | |

| By Geography | North America |

| South America | |

| Europe | |

| Asia-Pacific | |

| Middle East and Africa |

Key Questions Answered in the Report

How large is the global Valves market in the water and wastewater sector today?

The Valves market size reached USD 8.06 billion in 2026 and is projected to climb to USD 9.68 billion by 2031 at a 3.74% CAGR.

Which valve type is expanding the fastest through 2031?

Ball valves lead growth at a 4.79% CAGR through 2031 thanks to easy automation readiness and lower maintenance demands.

Why is Asia-Pacific pivotal for future demand?

Asia-Pacific holds 34.40% share and will post the quickest 4.56% CAGR through 2031, fueled by large-scale Chinese and Indian water-infrastructure build-outs.

How will PFAS regulation influence material choices?

Tightening PFAS curbs are driving adoption of fluorine-free thermoplastics and composites, lifting their segment growth to 4.55% CAGR.

What cybersecurity measures are utilities seeking in smart valves?

Hardened controllers, encrypted protocols and segmented networks have become baseline requirements after a 300% jump in water-system ransomware attacks.

Page last updated on: