Viral Vector Manufacturing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.55 Billion |

| Market Size (2031) | USD 9.02 Billion |

| Growth Rate (2026 - 2031) | 20.49% CAGR |

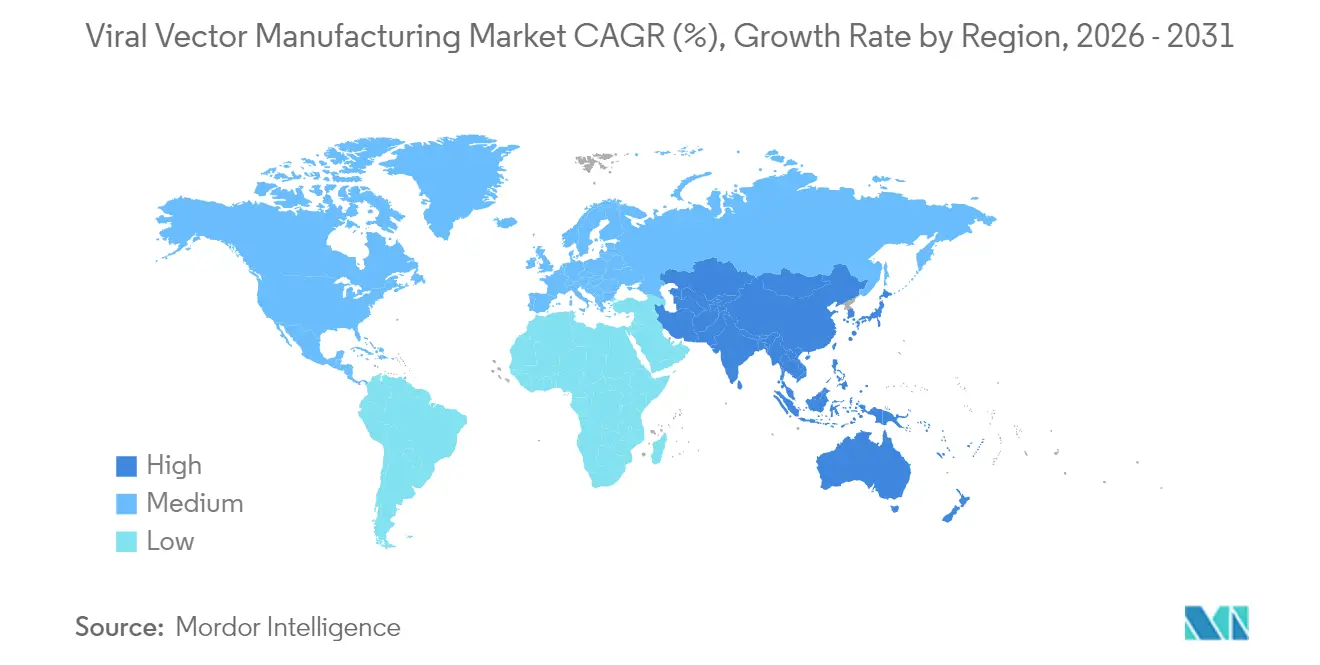

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

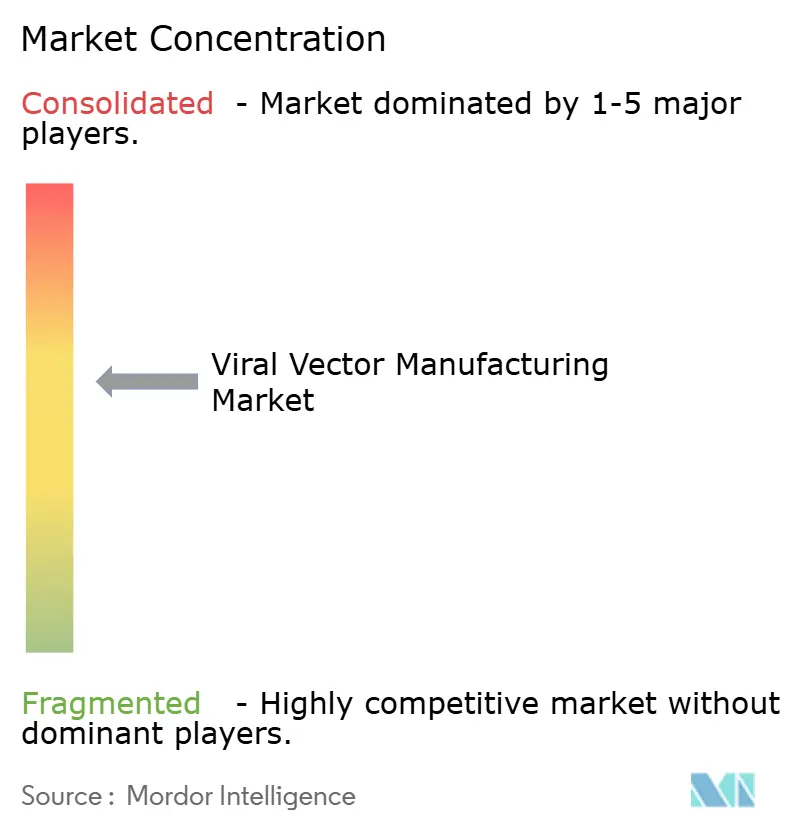

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Viral Vector Manufacturing Market Analysis by Mordor Intelligence

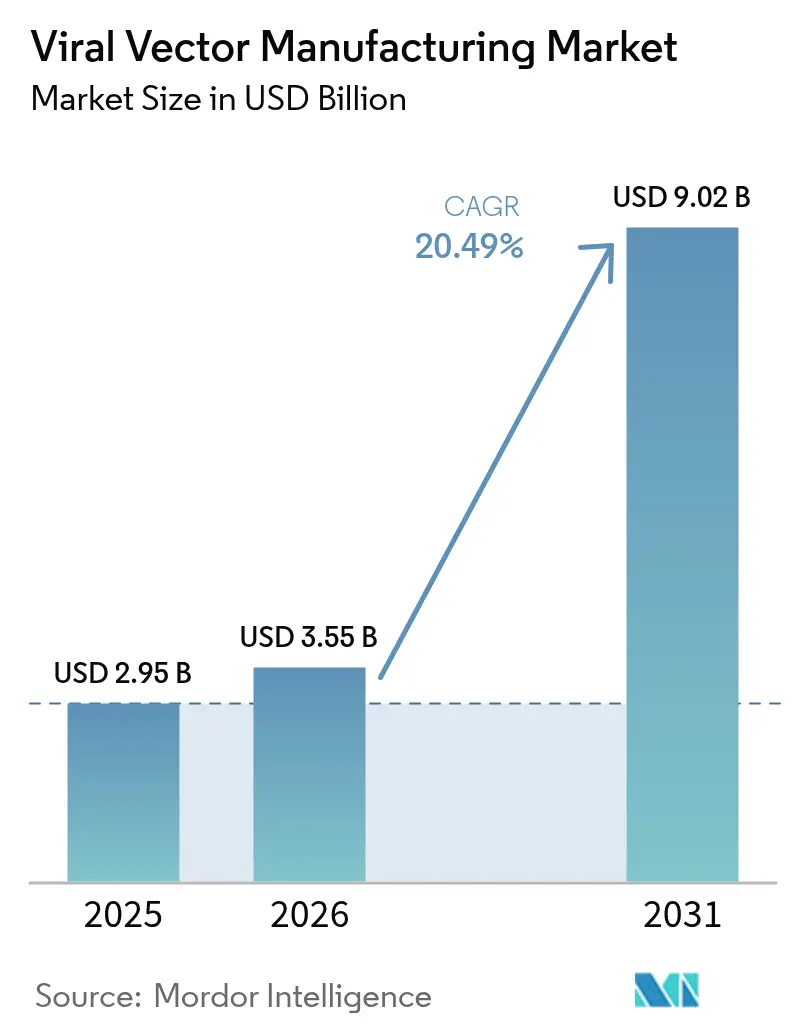

The Viral Vector Manufacturing market size is expected to grow from USD 2.95 billion in 2025 to USD 3.55 billion in 2026 and is forecast to reach USD 9.02 billion by 2031 at 20.49% CAGR over 2026-2031.

This trajectory mirrors the transformation of gene therapy from an experimental niche into a regulated treatment class as the tally of FDA-cleared products climbed to 14 in 2024. Breakthrough authorizations such as Casgevy for sickle cell disease and new indications for Elevidys in Duchenne muscular dystrophy validated commercial demand and accelerated funding for production infrastructure. More than USD 8 billion in green- and brown-field projects were announced by major CDMOs during 2024-2025, led by Fujifilm Diosynth and Lonza, yet many suites still run below 50% utilization because they were designed for early-phase work rather than sustained commercial output. Consolidation is intensifying as acquirers chase end-to-end capabilities, advanced analytics and regulatory know-how that shorten time to market.

Key Report Takeaways

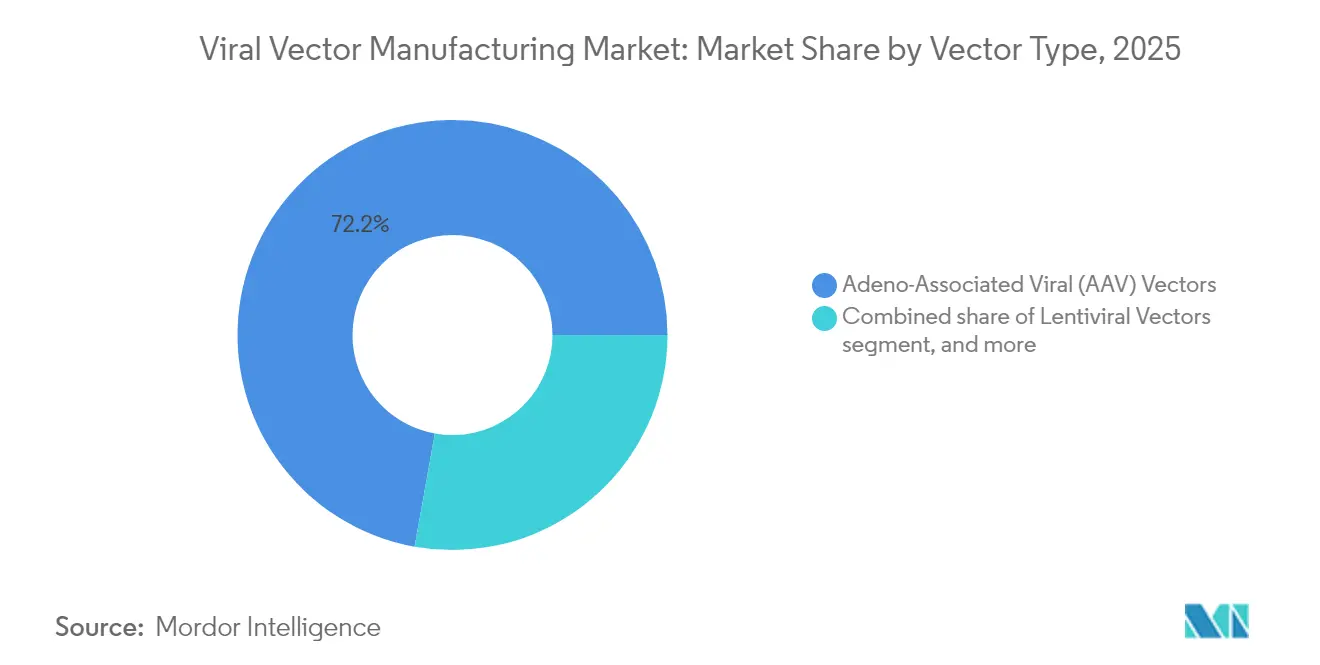

- By vector type, adeno-associated viral platforms accounted for 72.18% of 2025 revenue while adenoviral vectors are projected to grow at a 22.9% CAGR to 2031.

- By disease, genetic disorders represented 48.10% of the viral vector manufacturing market share in 2025; neurological disorders are set to expand at 23.6% CAGR through 2031.

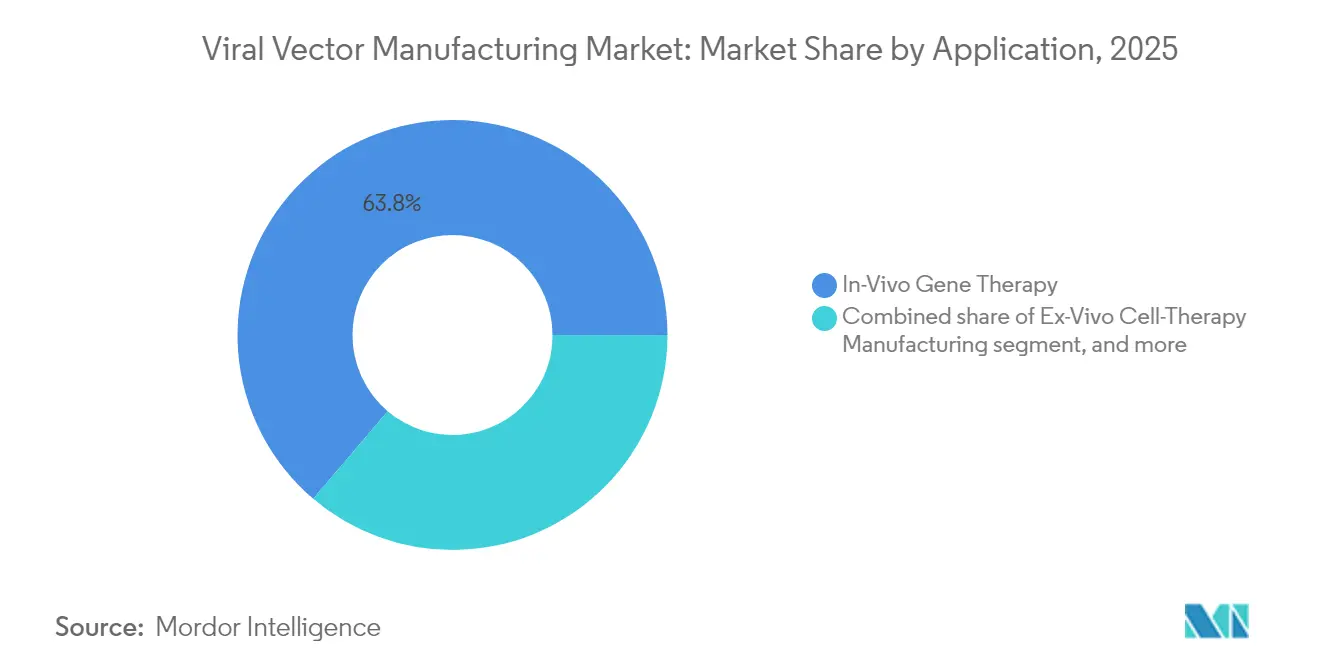

- By application, in-vivo therapies held 63.78% of the viral vector manufacturing market size in 2025 and ex-vivo cell therapies are advancing at a 22.9% CAGR to 2031.

- By mode of manufacturing, in-house production captured 61.70% of the viral vector manufacturing market revenue in 2025, whereas contract manufacturing is forecast to post a 23.4% CAGR to 2031.

- By geography, North America commanded 46.95% of 2025 revenue and Asia-Pacific is projected to grow at 21.8% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Viral Vector Manufacturing Market*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing gene therapy pipeline and clinical successes | +4.2% | North America, EU, Asia-Pacific | Medium term (2-4 years) |

| Increasing CDMO outsourcing and capacity expansions | +3.8% | North America, Asia-Pacific | Short term (≤ 2 years) |

| Strong venture capital and government funding | +3.1% | North America, EU, China, Singapore | Medium term (2-4 years) |

| Transition to suspension cell culture platforms | +2.9% | Global hubs | Long term (≥ 4 years) |

| Adoption of single-use bioreactors | +2.7% | Global | Short term (≤ 2 years) |

| Emerging AI-guided capsid engineering | +2.4% | North America, EU, select APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Gene Therapy Pipeline and Clinical Successes

More than 2,000 gene therapies were under development by 2024, underscoring the breadth of indications progressing toward commercialization[1]Food and Drug Administration, “Novel Gene Therapy Approvals and Guidance Documents,” fda.gov. Approval of Kebilidi for aromatic L-amino acid decarboxylase deficiency marked the first therapeutic option for this rare neurologic disorder and established a regulatory precedent for intraparenchymal AAV delivery. The BENEGENE-2 trial reported a 71% fall in bleeding episodes for hemophilia B, confirming durable factor IX expression. Such clinical milestones strengthen payer confidence and stimulate larger patient cohort studies, which in turn expand batch-volume requirements inside the viral vector manufacturing market. As process know-how improves, average AAV dose costs have dropped into the tens of thousands of dollars, enabling exploration of common diseases without sacrificing economic viability.

Increasing CDMO Outsourcing and Capacity Expansions

CDMOs and hybrid manufacturers are expected to own 54% of global biologics capacity by 2028—up from 43% in 2024—reflecting a decisive move toward asset-light models among therapy developers. Charles River’s partnership with the Gates Institute for lentiviral services and Takara Bio’s deployment of 5,000 L single-use reactors illustrate the specialized scale sponsors now rent instead of build. UniQure sold its Lexington plant and outsourced Hemgenix manufacturing to Genezen, demonstrating the economic calculus that favors external production for high-complexity vectors. Resilience invested USD 225 million to boost output beyond 200 million units by 2025, showing how fast demand is rising in the viral vector manufacturing market.

Strong Venture Capital and Government Funding in Cell & Gene Therapies

Despite a wider biotech funding cooldown, investors poured capital into manufacturable platforms. VectorBuilder secured USD 76 million for a 30-suite Guangzhou facility, while China earmarked USD 4.17 billion for biomanufacturing projects starting in 2025. Germany’s national strategy backed Roche’s EUR 90 million gene therapy center in Penzberg. Venture financing for gene-editing companies dipped to USD 280 million in 2024 but early-2025 rounds point to renewed confidence as programs reach pivotal trials. Capital allocation now favors ventures that demonstrate scalable, quality-assured production paths within the viral vector manufacturing market.

Emerging AI-Guided Capsid Engineering Strategies

Machine-learning frameworks such as CAP-PLM predict AAV capsid fitness with high accuracy, allowing developers to narrow experimental libraries and cut discovery cycle[2]Phys.org Editors, “Machine Learning Elevates AAV Capsid Design,” phys.org. Better-designed capsids can halve vector dose requirements, easing cost pressures and freeing fermenter space. Early adopters in the United States and Europe have integrated AI platforms into process development, signalling long-term efficiency gains for the viral vector manufacturing market.

Restraints Impact Analysis of Viral Vector Manufacturing Market*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of goods and therapy pricing concerns | –2.8% | Global, with emphasis on price-sensitive markets | Medium term (2-4 years) |

| Regulatory complexity and batch-release delays | –2.1% | Global, varying by regulatory jurisdiction | Short term (≤ 2 years) |

| Supply chain constraints for GMP-grade plasmids | –1.9% | North America, Europe, Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Competition from non-viral delivery technologies | –1.7% | Global, notably in advanced therapy innovation clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Goods and Therapy Pricing Concerns

AAV production still spans around three weeks and costs roughly USD 50,000 per construct, with empty capsids inflating volumes and complicating titer calculations[3]Form Bio Product Team, “AI-Enabled Vector Design Platform,” formbio.com. Commercial prices remain high—Casgevy lists at USD 2.2 million and Hemgenix at USD 3.5 million per patient—raising payer concerns about affordability. Ethical debates over equitable access limit market penetration in low-income regions. Platform manufacturing, higher cell densities and in-line analytics are reducing waste, yet major savings will appear only as late-stage portfolios mature and volumes rise inside the viral vector manufacturing market.

Regulatory Complexity and Batch-Release Delays

The FDA’s Q5A(R2) revision deepened viral safety requirements and lengthened validation packages. Distinguishing full from empty capsids demands analytical ultracentrifugation or mass photometry that many plants lack. Workforce shortages for these niche skills add further lags. The EMA is harmonizing guidelines, yet staggered national timelines force manufacturers to navigate parallel pathways. These hurdles slow product launches and dampen growth prospects for the viral vector manufacturing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Viral Vector Manufacturing Market Segment Analysis

By Vector Type:

AAV Dominance Drives Market ExpansionAAV vectors delivered 72.18% of the viral vector manufacturing market revenue in 2025 as favorable safety, tissue tropism and six FDA-approved therapies anchored demand. The viral vector manufacturing market size for AAV products is expected to increase sharply as hemophilia and muscular dystrophy treatments scale commercial volumes. More than 225 active trials rely on AAV backbones, cementing multiyear capacity needs. CDMOs are commissioning AAV-dedicated suites that leverage suspension bioreactors to lift productivity.

Adenoviral vectors hold the fastest growth outlook at 22.9% CAGR through 2031. Novel serotype engineering mitigates pre-existing immunity, opening repeat-dose vaccine and oncolytic applications. Lentiviral vectors remain essential for autologous CAR-T workflows; improved pH control and competitive inhibition now curb 62.1% functional-particle loss once common in manufacturing. Retroviral and oncolytic platforms serve niche oncology uses, often in combination with checkpoint inhibitors, and benefit from proprietary cell-line partnerships that enhance yield.

By Disease:

Genetic Disorders Lead Therapeutic ApplicationsGenetic disorders accounted for 48.10% of the viral vector manufacturing market revenue in 2025, among all indications as curative outcomes justified premium pricing structures. Long-term data in hemophilia A, hemophilia B and sickle cell disease incentivized payers to adopt outcome-based payment schemes. The viral vector manufacturing market size for these rare conditions remains sizable due to pent-up demand, newborn screening programs and expanded label use.

Neurological disorders are slated to record a 23.6% CAGR through 2031. Intrathecal and intraparenchymal delivery methods overcame earlier barriers posed by the blood-brain barrier. Positive safety and efficacy readouts in spinal muscular atrophy and inherited retinal diseases are driving new Parkinson’s and ALS candidates. Oncology retains a stable share via CAR-T therapies that depend on lentiviral backbones, while infectious disease projects pivot toward adenoviral vectors during outbreak scenarios.

By Application:

In-Vivo Therapies Drive Market GrowthIn-vivo therapies captured 63.78% of the viral vector manufacturing market revenue in 2025 because they require only vector manufacture instead of individualized cell manipulation. Recent capsid innovations raised transduction efficiency, allowing lower doses and shortening infusion times. Two intramuscular AAV candidates filed in 2025 highlight the widening substrate for direct administration.

Ex-vivo cell therapy programs hold the highest growth rate at 22.9% CAGR, propelled by edits for sickle cell disease and beta-thalassemia that validated manufacturing economics. Engineered producer lines such as NuPro-2S reduce DNA impurities by 89%, improving consistency. Preventive vaccinology leverages adenoviral vectors for pandemic preparedness but faces competitive pressure from rapidly adaptable mRNA platforms.

By Mode of Manufacturing:

Contract Manufacturing AcceleratesIn-house suites still generated 61.70% of 2025 revenue as firms safeguarded process knowledge. However, capacity limits and escalating CapEx have led numerous sponsors to shift toward external partners. The viral vector manufacturing market is therefore tilting toward CDMOs that supply turn-key analytics, process validation and regulatory support.

Contract services are expected to grow at 23.4% CAGR to 2031. Lonza’s USD 1.2 billion Vacaville acquisition and Fujifilm Diosynth’s USD 1.2 billion North Carolina expansion each added more than 300,000 L of bioreactor volume. Hybrid strategies are gaining favor as developers keep small-scale R&D internal while outsourcing commercial lots, giving flexibility without foregoing core intellectual property control.

Geography Analysis

North America Viral Vector Manufacturing Market

North America held 46.95% of 2025 revenue, driven by the FDA’s clear regulatory road map and dense biotechnology clusters in Boston, Research Triangle Park and the San Francisco Bay Area. Resilience’s USD 225 million capacity build in Ohio and GenScript ProBio’s 128,000 ft² New Jersey site underline investor faith in domestic infrastructure. The region also benefits from the deepest labor pool of vector-skilled specialists.

Europe Viral Vector Manufacturing Market

Europe ranked second and received a boost from Germany’s EUR 90 million Penzberg center and Novartis’ fully robotized USD 43 million facility in Slovenia. Harmonized EMA guidelines streamline filings, although Brexit still imposes dual-site quality reviews for products crossing the Channel. Environmental regulations in the EU encourage single-use systems that lower water usage and carbon footprints, influencing procurement policies across the viral vector manufacturing market.

APAC Viral Vector Manufacturing Market

Asia-Pacific is projected to register a 21.8% CAGR through 2031. China reserved USD 4.17 billion for biomanufacturing lines beginning in 2025, while Japan, India and South Korea upgrade regulatory frameworks to attract multinational trials. WuXi Biologics reported 2024 revenue growth that funds additional vector lines in Wuxi and Suzhou. Large treatment-naïve patient pools and competitive operating costs make the region a preferred launchpad for late-phase outsourcing.

Competitive Landscape

The viral vector manufacturing market shows moderate concentration as leading CDMOs acquire specialty firms to integrate cell-line development, analytical assays and fill-finish under one roof. Charles River’s USD 292.5 million purchase of Vigene Biosciences, Merck KGaA’s USD 600 million acquisition of Mirus Bio and Lonza’s USD 1.2 billion buyout of Genentech’s Vacaville plant illustrate the premiums paid for proven scalability.

Technology differentiation is now essential. Form Bio’s AI engine predicts optimal AAV capsids, reducing trial-and-error loops and shaving months off development timelines. Engineered cell lines that cut residual DNA below regulatory thresholds and AI-driven digital twins that forecast batch yields provide measurable performance gains. Operators without such toolsets risk competing on price rather than value-added science.

White-space prospects lie in emerging markets and niche vectors. VIVEbiotech raised fresh capital to expand lentiviral services for neuro-oncology programs. ViroCell Biologics completed oversubscribed financing to accelerate clinical-stage production in the United Kingdom. New entrants can still gain traction by specializing in rare serotypes, regional fill-finish, or next-generation analytics.

Viral Vector Manufacturing Industry Leaders

Lonza

Thermo Fisher Scientific, Inc.

Charles River Laboratories

Fujifilm Diosynth Biotechnologies

Catalent

- *Disclaimer: Major Players sorted in no particular order

Viral Vector Manufacturing Market Companies Covered in this Report

- Lonza Group

- Thermo Fisher Scientific

- Charles River

- FUJIFILM

- Catalent

- Kaneka

- Merck KGaA (MilliporeSigma)

- Oxford Biomedica

- UniQure

- Spark Therapeutics (Roche)

- Cytiva

- Yposkesi (Servier)

- Viralgen Vector Core

- Aldevron

- Vibalogics

- Waisman Biomanufacturing

- Novasep

- Genezen

- bluebird Bio

Recent Industry Developments in Viral Vector Manufacturing Market

- March 2025: WuXi Biologics reported solid 2024 results and forecast accelerated 2025 growth, citing fresh vector capacity in Asia-Pacific.

- February 2025: Takara Bio launched 50 L–5,000 L single-use bioreactors for large-scale vector production.

- February 2025: Novartis opened a EUR 40 million automated viral vector plant in Slovenia.

- January 2025: Fujifilm Diosynth said 2025 will be its biggest expansion year, tripling Holly Springs bioreactor volume.

- December 2024: VIVEbiotech secured growth investment from Ampersand Capital Partners.

Viral Vector Manufacturing Market Report Scope and Research Methodology

Market Definition and Coverage

Our study treats the viral vector manufacturing market as the value generated from current-good-manufacturing-practice (cGMP) production of adeno-associated, lentiviral, adenoviral, retroviral, and other engineered vectors that are supplied for clinical or commercial gene and cell therapies. The figures exclude revenue from non-GMP research-grade batches, plasmid DNA backbones, and single-use equipment.

Scope exclusion: platforms that only supply plasmid DNA or non-viral nanoparticles are left outside this assessment.

Segments Covered in This Report

- By Vector Type

- Adeno-Associated Viral (AAV) Vectors

- Lentiviral Vectors

- Adenoviral Vectors

- Retroviral & ?-Retroviral Vectors

- Oncolytic & Other Engineered Viruses

- By Disease

- Cancer

- Genetic Disorders

- Infectious Diseases

- Neurological Disorders

- Other Therapeutic Areas

- By Application

- In-Vivo Gene Therapy

- Ex-Vivo Cell-Therapy Manufacturing (CAR-T, TCR-T, Etc.)

- Preventive & Therapeutic Vaccinology

- By Mode Of Manufacturing

- In-House Manufacturing

- Contract Manufacturing (CDMOs)

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Discussions with bioprocess engineers at CDMOs, therapy developers across North America, Europe, and East Asia, as well as regulators and equipment vendors, helped validate average yields, failure rates, and price corridors. These conversations also clarified future batch size preferences and commissioning timelines that cannot be inferred from desk work alone.

Desk Research

Mordor analysts began with governmental and scientific sources such as the US Food & Drug Administration's CBER cell-gene approval database, European Medicines Agency advanced-therapy reports, ClinicalTrials.gov pipeline listings, and World Health Organization International Clinical Trials Registry. Capacity indicators were gathered from trade bodies like the Alliance for Regenerative Medicine, export shipment clues from UN Comtrade HS 3002 codes, and patent velocity trends using Questel. Public company filings, investor decks, and reputable news feeds via Dow Jones Factiva complemented the landscape view. The sources mentioned illustrate, but do not exhaust, the wider collection mined for datapoints and cross-checks.

Market-Sizing & Forecasting

A top-down build links treated-patient pools, clinical-trial attrition factors, and expected commercial launches, which are then converted into vector-liter demand via dose times patients norms. Selected bottom-up checks sampled CDMO revenues and average selling price times announced capacity anchor the totals.

Key variables inside the model include: 1. Phase II-III gene therapy count and success probability. 2. Typical vector dose per indication. 3. Average bioreactor titer and batch yield. 4. Installed GMP clean-room square footage that can run viral campaigns. 5. Venture and grant funding trends tied to novel capsid work.

Forecasts use multivariate regression blended with scenario analysis to test funding and titer shocks before finalizing the base case. Gaps in bottom-up coverage are adjusted through calibrated utilization assumptions reviewed with interviewees.

Data Validation & Update Cycle

Outputs pass two-layer peer review, anomaly sweeps against external capacity announcements, and currency consistency checks before sign-off. The model is refreshed every year, with interim updates triggered by major facility additions, pivotal approvals, or price resets.

How Mordor Intelligence's Viral Vector Manufacturing Market Size Compares to Other Published Estimates

Published numbers rarely converge because firms pick different inclusions, base years, and refresh cadences.

Variation typically stems from mixing plasmid DNA with vectors, counting research-grade batches, choosing distinct currency years, or applying single-scenario outlooks. Mordor's disciplined scope, annual refresh, and dual-path validation remove these distortions, giving decision-makers a dependable starting point.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.95 B (2025) | Mordor Intelligence | - |

| USD 5.50 B (2023) | Global Consultancy A | Combines plasmid DNA and vectors; older base year; limited cross-check with CDMO revenues |

| USD 5.33 B (2023) | Industry Journal B | Includes research-grade output and downstream consumables; single scenario forecast |

| USD 1.85 B (2024) | Regional Consultancy C | Excludes contract manufacturing outside North America; conservative uptake rates |

In sum, differences narrow once comparable scope and timing are applied, and this is where Mordor Intelligence provides the most transparent, traceable baseline for strategic planning.

Key Questions Answered in the Report

What is the current size of the viral vector manufacturing market?

The market is valued at USD 3.55 billion in 2026 and is projected to reach USD 9.02 billion by 2031 at a 20.49% CAGR.

Which vector type dominates the viral vector manufacturing market?

Adeno-associated viral platforms lead with a 72.18% revenue share thanks to favorable safety profiles and multiple FDA-approved therapies.

Why are CDMOs gaining importance in the viral vector manufacturing industry?

Developers prefer specialized CDMOs for their validated processes, advanced analytics and ready capacity, avoiding the high CapEx of building proprietary plants.

Which region is growing fastest in the viral vector manufacturing market?

Asia-Pacific is forecast to grow at a 21.8% CAGR through 2031, supported by China’s multi-billion-dollar biomanufacturing initiatives and expanding regional capabilities.

What is the main cost barrier for wider adoption of gene therapies?

High production expenses keep therapy prices in the USD 2 million–USD 3.5 million range, but process optimization is slowly reducing cost per dose.

How concentrated is competition in the viral vector manufacturing market?

The top five suppliers control about 60% of global commercial capacity, indicating moderate concentration that still allows new entrants to gain share.

Page last updated on: