Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

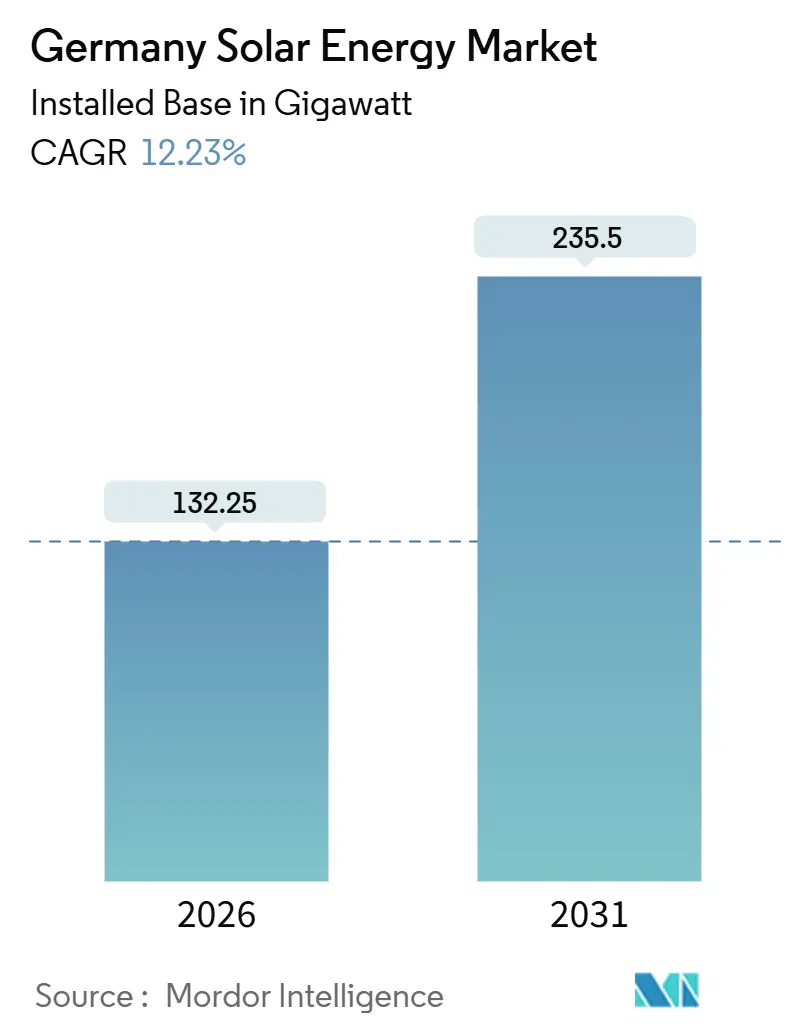

| Market Volume (2026) | 132.25 gigawatt |

| Market Volume (2031) | 235.5 gigawatt |

| Growth Rate (2026 - 2031) | 12.23% CAGR |

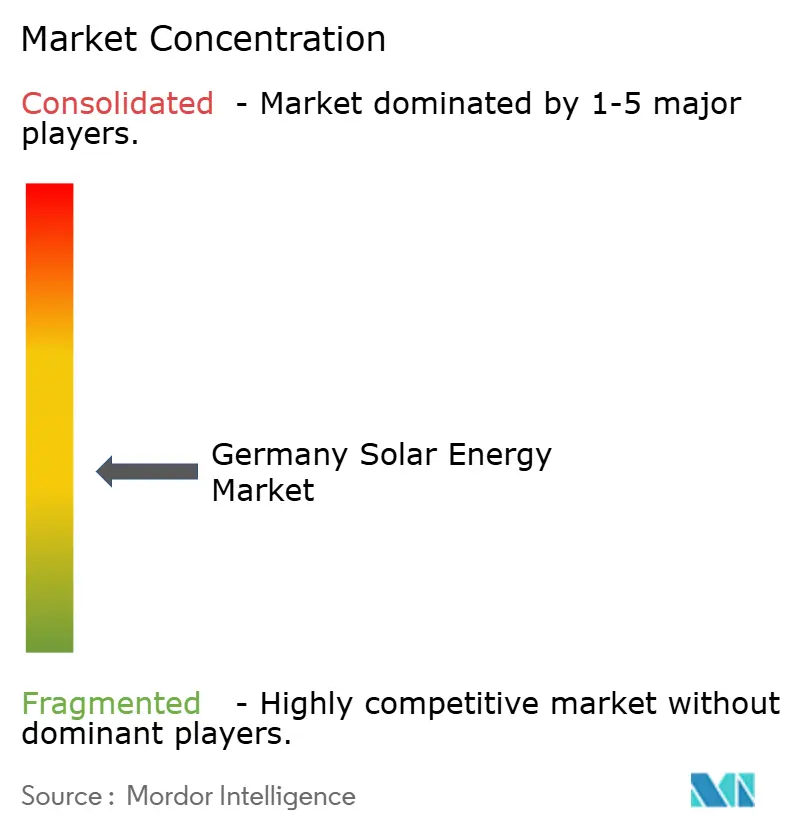

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Solar Energy Market Analysis by Mordor Intelligence

The Germany Solar Energy Market size in terms of installed base is expected to grow from 132.25 gigawatt in 2026 to 235.5 gigawatt by 2031, at a CAGR of 12.23% during the forecast period (2026-2031).

A federal permitting overhaul in 2024 spurred an 86% jump in approved projects, positioning the country to command roughly 60% of all solar capacity auctioned across Europe in the first half of 2025. Developers added 16.2 GW in 2024, and preliminary 2025 figures show another 15.9 GW, underscoring a rapid build-out that lifted solar generation to 63.3 TWh in 2024 and an expected 89 TWh in 2025. Utility-scale plants now compete head-to-head with wholesale power prices as module costs collapsed to about USD 0.11 per watt-DC in early 2024, enabling bids below 5 cents / kWh even after capture-rate discounts. Behind-the-meter PV plus storage adoption is surging because redispatch costs above EUR 4 billion flow through rising grid fees, cutting typical commercial payback periods to under eight years.

Key Report Takeaways

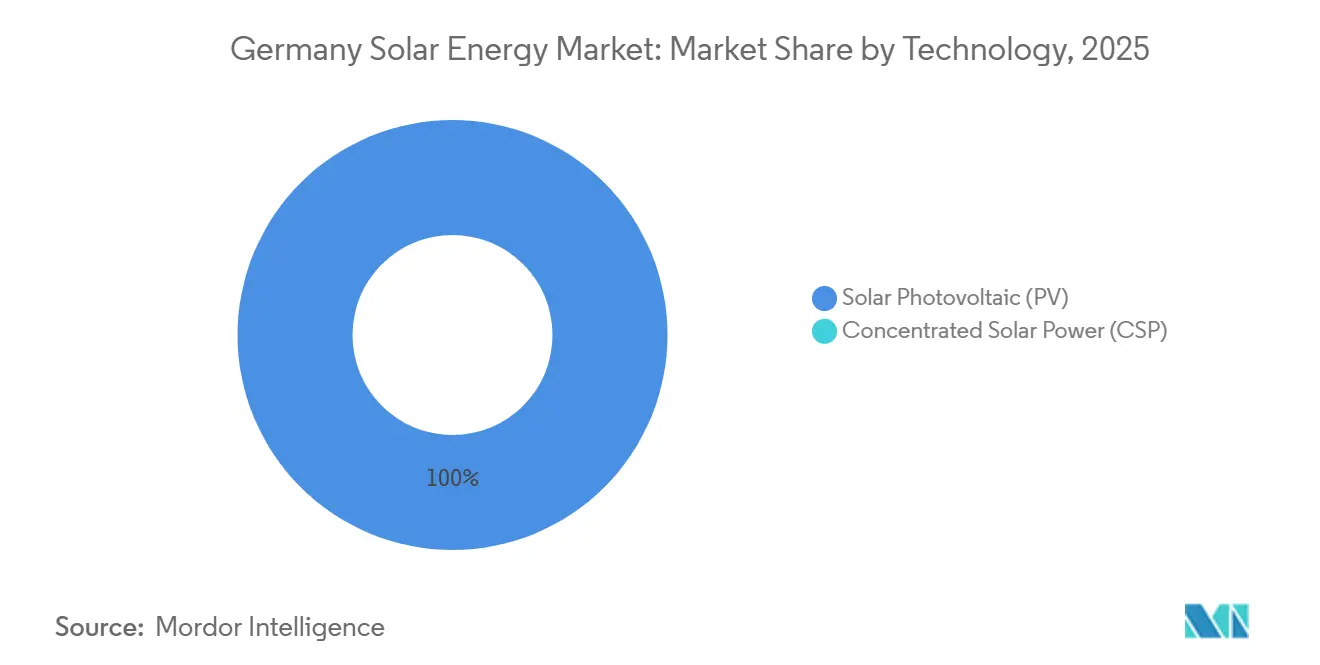

- By technology, solar PV held 100% of Germany's solar energy market share in 2025 and is forecast to grow at a 12.2% CAGR through 2031.

- By grid type, on-grid systems accounted for 94.1% of Germany's solar energy market size in 2025, while off-grid installations are expanding at a leading 16.4% CAGR to 2031.

- By end-user, utility-scale projects captured 50.5% of Germany's solar energy market share in 2025 and are projected to rise at 14.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Solar Package I & Rooftop Mandates Accelerating Approvals | +2.1% | National, with early gains in Bavaria, Baden-Württemberg | Short term (≤ 2 years) |

| Corporate PPA Boom Lifting Unsubsidised Utility Projects | +1.8% | National, concentrated in North Rhine-Westphalia, Lower Saxony | Medium term (2-4 years) |

| Rising Grid-Fee Inflation Driving Behind-the-Meter PV + Storage | +1.5% | National, urban commercial hubs | Medium term (2-4 years) |

| Mass Adoption of Balcony-Plug-in PV by Renters | +0.9% | National, urban centers (Berlin, Hamburg, Munich) | Short term (≤ 2 years) |

| 87% Module-Price Collapse Enables Cost-Parity vs. Wholesale | +2.4% | National | Short term (≤ 2 years) |

| Integrated BIPV Requirements in New-Build Codes (from 2026) | +1.2% | National, state-level enforcement in Baden-Württemberg, Bavaria | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Solar Package I & Rooftop Mandates Accelerating Approvals

The 2024 Solar Package I simplified registrations and raised the balcony-PV inverter limit to 800 W, allowing tenants to self-install systems without landlord consent. Registrations reached about 780,000 units by year-end 2024, adding 435,000 systems in a single year and equaling 2.6% of national solar additions. State-level mandates now require solar on new roofs in Baden-Württemberg and Bavaria, cutting average permitting times from 18 months to under six and adding roughly 2.1 percentage points to forecast growth. Rooftop auction volumes ticked up in October 2025, with 281 MW awarded at 9.66 cents/kWh, confirming early traction. The driver is strongest in southern states, but uptake is expected to broaden as other regions align with the revised Energy Performance of Buildings Directive.

Corporate PPA Boom Lifting Unsubsidised Utility Projects

Long-term corporate PPAs are increasingly displacing subsidy auctions. Energiekontor’s 2024 deal with Currenta to power a chemical park shows industrial buyers locking in fixed-price solar to hedge wholesale volatility. Unsubsidised projects already propel growth because developers can finance plants outside capped auction volumes. North Rhine-Westphalia and Lower Saxony lead activity thanks to large industrial loads, lower curtailment risk, and quicker grid connections. Falling module prices let developers offer PPA rates below 5 cents/kWh, supporting pipeline acceleration through 2028.

Rising Grid-Fee Inflation Driving Behind-the-Meter PV + Storage

Annual redispatch costs above EUR 4 billion inflate network charges, motivating businesses to cut imports with rooftop PV paired with batteries. Bundesnetzagentur logged 9,710 storage connection requests in 2024, equal to 400 GW of power and 661 GWh of energy, but only 921 plants were live, highlighting grid bottlenecks.[1]Bundesnetzagentur, “Aurora Photovoltaik Auktionen 2025,” bundesnetzagentur.de When batteries are added, commercial paybacks fall to under eight years compared with 12 years for PV alone. Urban commercial hubs feel the strongest pull as high demand coincides with expensive grid tariffs.

Mass Adoption of Balcony-Plug-in PV by Renters

Balcony systems give renters cheap self-generation. Official registrations hit 780,000 by end-2024, likely understating true adoption that may already top 1 million units. Each kit averages 0.5 kW, summing to about 0.4 GW or 2.6% of 2024 solar capacity growth. Uptake is heavily urban, notably in Berlin, Hamburg, and Munich.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Distribution-Grid Congestion & 24-Month Queue Times | -1.9% | National, acute in Bavaria, Baden-Württemberg | Medium term (2-4 years) |

| Skilled-Labour Shortages in Licensed Electricians & Installers | -1.3% | National | Medium term (2-4 years) |

| 60% Cost Gap on EU-vs-China Modules Creating Supply-Risk | -0.8% | National, EU-wide supply-chain exposure | Short term (≤ 2 years) |

| Declining FiTs & Sudden Subsidy Tweaks Eroding Residential ROI | -1.1% | National, residential segment | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Distribution-Grid Congestion & 24-Month Queue Times

Connection backlogs near 24 months in Bavaria and Baden-Württemberg delay project cashflow and shave 1.9 percentage points off the baseline CAGR. Redispatch costs above EUR 4 billion in 2022 and onshore solar curtailment topping 13% on peak 2024 days illustrate the grid’s limited headroom.[2]International Energy Agency, “Germany Energy Policies Review 2025,” iea.org Developers are redirecting pipelines toward Lower Saxony and North Rhine-Westphalia, yet even there, transformer slots fill fast, forcing bids to price in lower capture rates. Bundesnetzagentur still issued around 3,800 connection commitments in 2024, but the gap between commitment and energization widens every quarter. Unless accelerated cable upgrades materialize, the German solar energy market faces staggered commissioning schedules that dampen near-term additions.

Skilled-Labour Shortages in Licensed Electricians & Installers

More than half of installation firms reported critical hiring gaps in 2025, lifting wage bills and stretching lead times from six to nine months for residential rooftops. The overlap between heat-pump and PV skill sets intensifies competition for certified electricians, subtracting about 1.3 percentage points from forecast growth. Federal training schemes launched in 2024 aim to certify 10,000 new installers annually, but meaningful relief will not arrive before 2027. As a result, developers phase projects to match labor availability rather than capital access, and component stock often sits in warehouses awaiting crews. The constraint is national, but rural districts with the fastest build-outs feel the tightest pinch.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Solar PV Retains Total Share, Tandems Promise Density Gains

Solar PV held 100% of Germany's solar energy market share in 2025 and is forecast to expand at 12.2% annually through 2031. Efficiency leaps matter more than raw silicon volume now that Fraunhofer ISE and Hanwha Q CELLS certified a 30.8% perovskite-silicon tandem cell in 2024, hinting at commercial modules by 2028. Higher power density can cut racking and land costs up to 15%, a vital lever as permitting favors brownfield sites. Agrivoltaic pilots in Bavaria show crops and panels co-existing under elevated bifacial trackers, easing land-use opposition and broadening farmer income. Concentrated solar power remains absent because diffuse irradiation weakens its thermodynamic advantage.

Perovskite durability is the remaining hurdle, but German research spending represented 64% of EU private PV R&D during 2010-2020, positioning domestic labs to solve it. Once bankability proofs emerge, utility developers can fit more megawatts per kilometer of feeder line, alleviating some curtailment. The German solar energy market, therefore, embeds a technology upside optionality that could temper future grid constraints by delivering more output per site footprint.

By Grid Type: On-Grid Dominates, but Off-Grid Grows Quickest

On-grid arrays accounted for 94.1% of Germany's solar energy market size in 2025. They benefit from auction prices that fell to 4.84 cents /kWh in July 2025, below the 7.85 cents wholesale average, even after negative-price discounts. However, off-grid and microgrid systems are rising 16.4% per year as industrials chase energy security and tariff avoidance. Remote agrivoltaics powering irrigation pumps, plus containerized PV-battery-diesel hybrids at factories, headline this surge.

Developers quote four-year paybacks when batteries let factories shave peak-demand surcharges. Grid operators welcome the relief, yet still require permits for back-feed capability, extending paperwork cycles. Because off-grid avoids curtailment entirely, financiers see lower revenue volatility. Over the forecast, its share inches upward but remains single-digit, keeping on-grid the anchor of the German solar energy market.

By End-User: Utility-Scale Leads on PPAs, Residential Lags on Tariffs

Utility-scale plants captured 50.5% of Germany's solar energy market share in 2025 and will post the fastest 14.9% CAGR to 2031. Corporate PPAs let developers bypass auction caps; Energiekontor’s supply deal to Currenta’s chemical park is emblematic. Large arrays also secure dedicated transmission corridors, cutting queue risk. Commercial and industrial rooftops follow, thanks to grid-fee inflation that lowers eight-year payback thresholds.

Residential rooftops, once the growth engine, now face declining tariffs and policy uncertainty. Balcony-plug-in kits soften the slowdown but cannot offset the wattage gap versus full roofs. Overall, end-user dynamics skew toward players with creditworthy offtakers and balance-sheet strength, underscoring consolidation pressure in the German solar energy market.

Geography Analysis

Bavaria added 4 GW in 2024, maintaining the state lead, yet rising curtailment and 24-month queues push developers north. Lower Saxony and North Rhine-Westphalia now host the bulkiest utility-scale pipelines because stronger grids couple with industrial PPA demand. Saxony’s 162 MW plant, commissioned in 2024, signals eastern states’ ability to clear land quickly and tap spare transmission.

Southern rooftop strength endures due to high irradiance and strict building mandates that start in 2026. Baden-Württemberg and Bavaria require 0.06 kW per square meter on new roofs, adding roughly 1.2 GW a year once fully enforced. Meanwhile, Berlin, Hamburg, and Munich drive mass balcony-PV adoption, widening urban self-generation as grid fees bite renters.

Cross-border electricity flows sharpen regional urgency. Germany was a net importer in 2024, buying 67 TWh and exporting 35 TWh, so every new solar gigawatt cuts external dependence.[3]Bundesnetzagentur, “Netzanschlussmonitoring 2025,” bundesnetzagentur.de EU-wide REPowerEU goals place moral suasion on laggard states to accelerate permits. Consequently, the geography split of the German solar energy market is re-balancing: southern states still dominate rooftops, but northern and eastern regions now command the growth pulse in utility-scale capacity.

Competitive Landscape

The German solar energy market remains moderately fragmented, with no company controlling more than 10% of installed capacity, yet price-based rivalry is intense because Chinese modules account for 95% of European Union imports. BayWa r.e. entered insolvency in 2024, while Meyer Burger sought court protection in June 2025, underscoring how plunging panel prices to USD 0.11 /W-DC squeezed European manufacturers. Wacker Chemie continues to operate the bloc’s only polysilicon plant at 60,000 t/y, but downstream wafer and cell stages remain Asia-centric, forcing developers in the German solar energy market to rely on long-distance supply chains that amplify geopolitical risk.

Developers are reshaping strategy around long-term corporate PPAs that bypass capped auctions. Energiekontor’s 2024 deal with Currenta locked 50 MW of output for a chemical park in North Rhine-Westphalia, and RWE committed to building 7 GW of new renewables domestically by 2030, all outside subsidy support. SMA Solar, insulated from module price swings, recorded EUR 353.9 million in Q3-2024 sales and a 7.3% EBIT margin by focusing on inverter systems and digital fleet services.[4]SMA Solar Technology AG, “Q3 2024 Financial Report,” sma.de These plays illustrate how the German solar energy market rewards firms that pivot toward system integration and power-trading expertise rather than pure module throughput.

Technology leadership is a second battlefront. Hanwha Q CELLS expanded its Thalheim factory to 3.3 GW of module capacity and, together with Fraunhofer ISE, certified a 30.8% perovskite-silicon tandem cell in October 2024, pointing to a commercial launch before 2028. Start-ups such as 1KOMMA5° aggregate small installers on a digital platform to speed residential roll-outs, while Next2Sun pilots vertical bifacial arrays for agrivoltaic dual use. Altogether, competitive moves show that the German solar energy market favors vertically integrated developers, inverter specialists, and niche innovators that can capture value in financing, permitting, and advanced cell architectures.

Germany Solar Energy Industry Leaders

BayWa r.e. AG

Enerparc AG

Hanwha Q CELLS GmbH

SMA Solar Technology AG

EnBW Energie Baden-Württemberg AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: EnBW has inaugurated an 80 MW solar facility in Langenenslingen, Germany. The official opening was graced by Baden-Württemberg Premier Winfried Kretschmann, representing the German Green Party. Notably, this plant stands out as the largest photovoltaic installation in the Baden-Württemberg state.

- May 2025: RWE announced large-scale solar farms alongside a German motorway to optimise land use and reinforce its renewable expansion goals.

- May 2025: Octopus acquired a 2 GW solar portfolio in Germany, underscoring strong foreign capital inflows.

- February 2025: Energy Infrastructure Partners took a majority stake in BayWa r.e., continuing market consolidation.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the German solar energy market as the total grid-connected photovoltaic and concentrated solar power capacity physically installed within Germany's borders and ready to export electricity to the public grid. Capacity is expressed in direct-current gigawatts, mirroring how network operators report additions.

Scope Exclusion: off-grid pico-solar kits below 1 kW and imported power from neighboring countries' solar parks lie outside our boundary.

Segmentation Overview

- By Technology

- Solar Photovoltaic (PV)

- Concentrated Solar Power (CSP)

- By Grid Type

- On-Grid

- Off-Grid

- By End-User

- Utility-Scale

- Commercial and Industrial (C&I)

- Residential

- By Component (Qualitative Analysis)

- Solar Modules/Panels

- Inverters (String, Central, Micro)

- Mounting and Tracking Systems

- Balance-of-System and Electricals

- Energy Storage and Hybrid Integration

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured interviews with inverter makers, distribution-grid planners, and residential installers across Bavaria, Saxony, and North-Rhine Westphalia. These discussions verified average system sizes, storage attachment rates, and near-term permitting bottlenecks, giving us live inputs that desktop material alone cannot reveal.

Desk Research

We launched the desk phase with official operator statistics from Bundesnetzagentur, monthly capacity ledgers from the European Network of Transmission System Operators for Electricity, and policy dossiers published by the Federal Ministry for Economic Affairs and Climate Action. Trade bodies such as SolarPower Europe and BSW-Solar enriched trend signals on rooftop uptake, while peer-reviewed papers in journals like Renewable & Sustainable Energy Reviews helped benchmark module efficiency curves. Commercial filings downloaded through D&B Hoovers, plus news archives on Dow Jones Factiva, supplied financial context for leading EPC players and price evolution. This set of sources is illustrative, not exhaustive; many other publications supported cross-checks and clarifications along the way.

Market-Sizing & Forecasting

A top-down reconstruction begins with Bundesnetzagentur's quarterly installed-base file, which we align to calendar years, then adjust for unregistered balcony PV using survey-based penetration factors. Supplier roll-ups of module shipments and sampled ASP × volume checks provide a bottom-up reasonableness screen before totals are frozen. Key drivers carried into the capacity forecast include feed-in tariff step-downs, median residential payback periods, land-auction volumes, storage attachment ratios, and inverter replacement cycles. Our multivariate regression links these variables to annual net additions. Scenario bounds are stress-tested with experts for policy or cost shocks. Gap handling, where bottom-up evidence trails the regulator's headline figure, is resolved by weighting the higher-quality data stream.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated anomaly flags, peer analyst scrutiny, and a senior sign-off. Reports refresh each year, with interim edits if subsidy rules, currency swings, or force-majeure events move the market.

Credibility Anchor - Why Mordor's Germany Solar Energy Baseline Earns Trust

Published estimates rarely match because providers pick differing cut-off dates, treat balcony modules inconsistently, or fold in speculative project pipelines.

Key Gap Drivers: competitors often stop at certified grid registrations, convert alternating-current ratings 1:1 to DC, or freeze exchange rates that distort euro-to-watt calculations. Mordor's base uses real-time filings, supplements them with balcony PV surveys, and re-pegs historical data whenever currency or tariff revisions alter incentives.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 100.93 GW (2025) | Mordor Intelligence | - |

| 99.3 GW (2024) | Energy Regulator A | Omits unregistered plug-in systems and year-end retrofits |

| 99.8 GW (2024) | Industry Association B | Reports DC only, no forward estimate, excludes pilot agrivoltaics |

The comparison shows that while external figures cluster near 100 GW, each leans on a narrower scope.

By blending regulator feeds with field intelligence and a disciplined refresh cadence, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can replicate and defend.

Key Questions Answered in the Report

How large is Germany’s installed solar base in 2026?

Installed capacity reached 132.25 GW in 2026 and is projected to grow at a 12.23% CAGR to 235.5 GW by 2031.

What segments are expanding fastest within German solar?

Utility-scale plants grow the quickest at a 14.9% CAGR, propelled by corporate PPAs and merchant exposure.

Why are module prices so low in Germany now?

A global 87% price collapse from 2022 highs, driven by Chinese oversupply and cheaper polysilicon, pushed spot rates to about USD 0.11 /W-DC.

Which states attract the most new utility-scale projects?

Lower Saxony, North Rhine-Westphalia, and Saxony draw rising investment thanks to stronger grids and shorter connection queues.

How do rising grid fees influence commercial PV adoption?

Higher network charges make behind-the-meter PV plus batteries profitable in under eight years, spurring rapid uptake among businesses.

Page last updated on: