Market Overview

| Study Period | 2020 - 2031 |

|---|---|

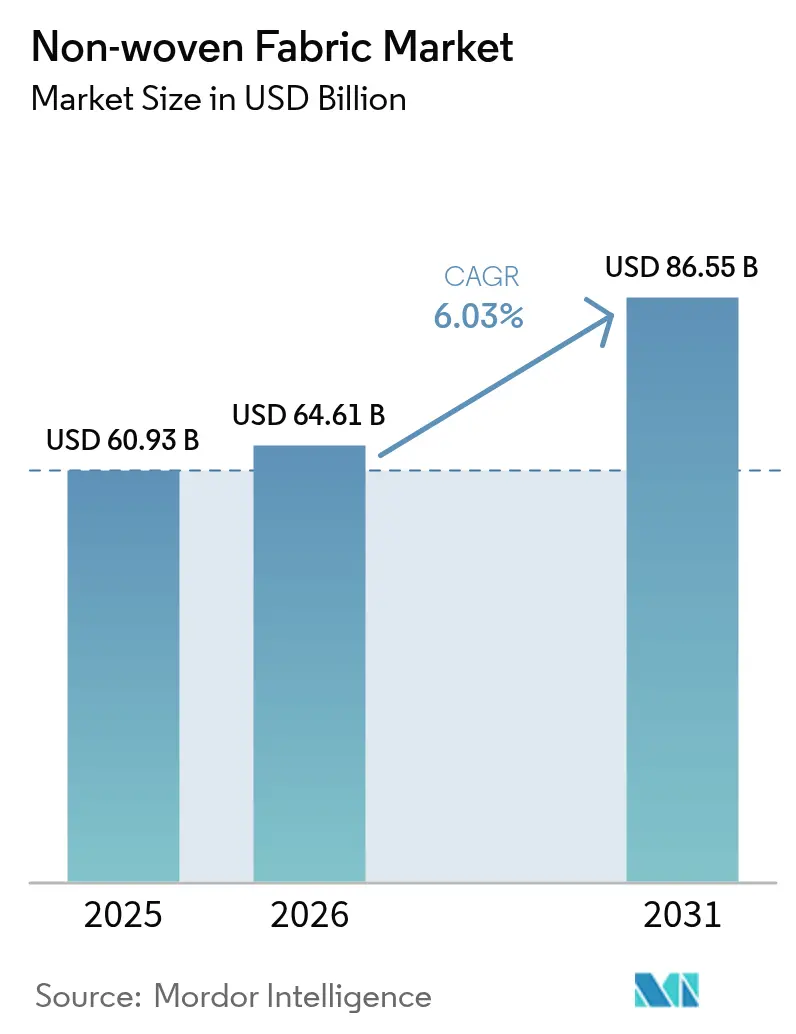

| Market Size (2026) | USD 64.61 Billion |

| Market Size (2031) | USD 86.55 Billion |

| Growth Rate (2026 - 2031) | 6.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Non-woven Fabric Market Analysis by Mordor Intelligence

The Non-woven Fabric Market size was valued at USD 60.93 billion in 2025 and estimated to grow from USD 64.61 billion in 2026 to reach USD 86.55 billion by 2031, at a CAGR of 6.03% during the forecast period (2026-2031). Sustained demand from healthcare, construction, and automotive applications continues to accelerate investment in spun-bond manufacturing lines, while electrospun nanofiber breakthroughs open premium niches in wound care, filtration, and solid-state battery separators. Polypropylene-based grades preserve a cost edge over woven fabrics even as propylene feedstock prices rise, helping converters defend margins. Regulatory momentum around microplastic leakage and recyclable packaging is reshaping product design toward biodegradable or circular solutions, pushing rayon, lyocell, and natural-fiber blends into mainstream specifications.

Key Report Takeaways

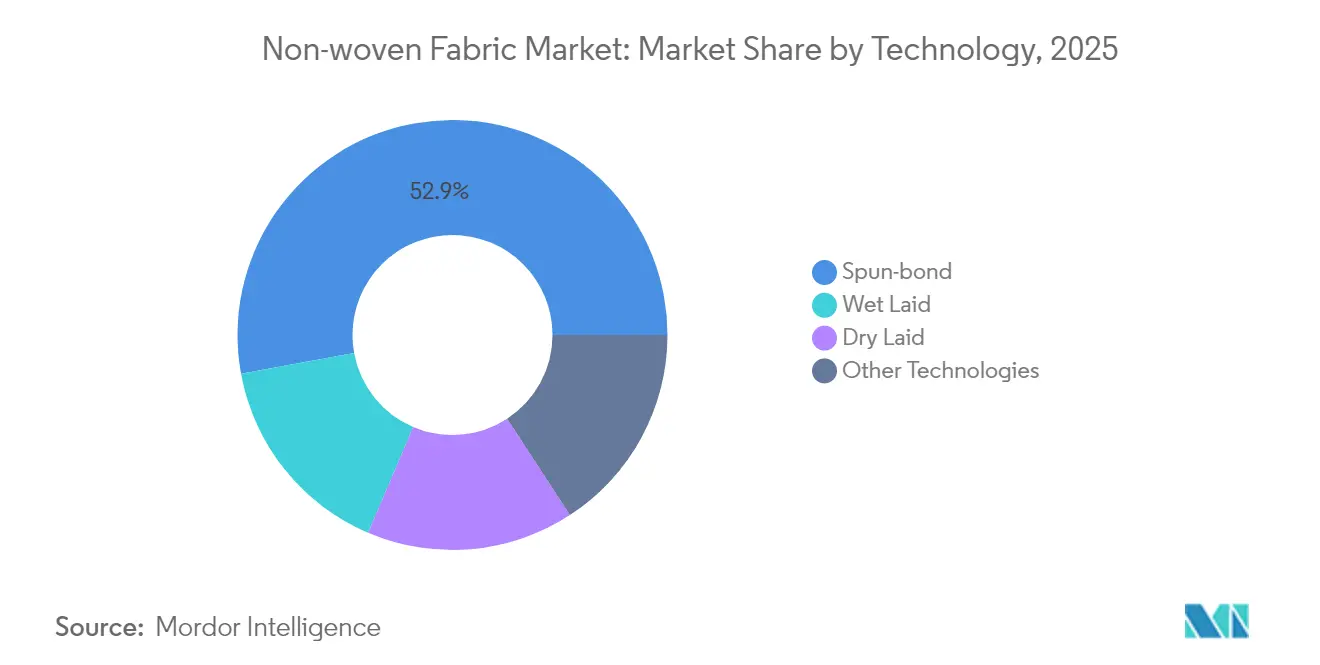

- By technology, spun-bond led with 52.88% of the non-woven fabric market share in 2025, whereas other technologies are projected to expand at an 8.74% CAGR through 2031.

- By material, polypropylene accounted for a 63.45% share of the non-woven fabric market size in 2025, while rayon is on track for the fastest 6.47% CAGR to 2031.

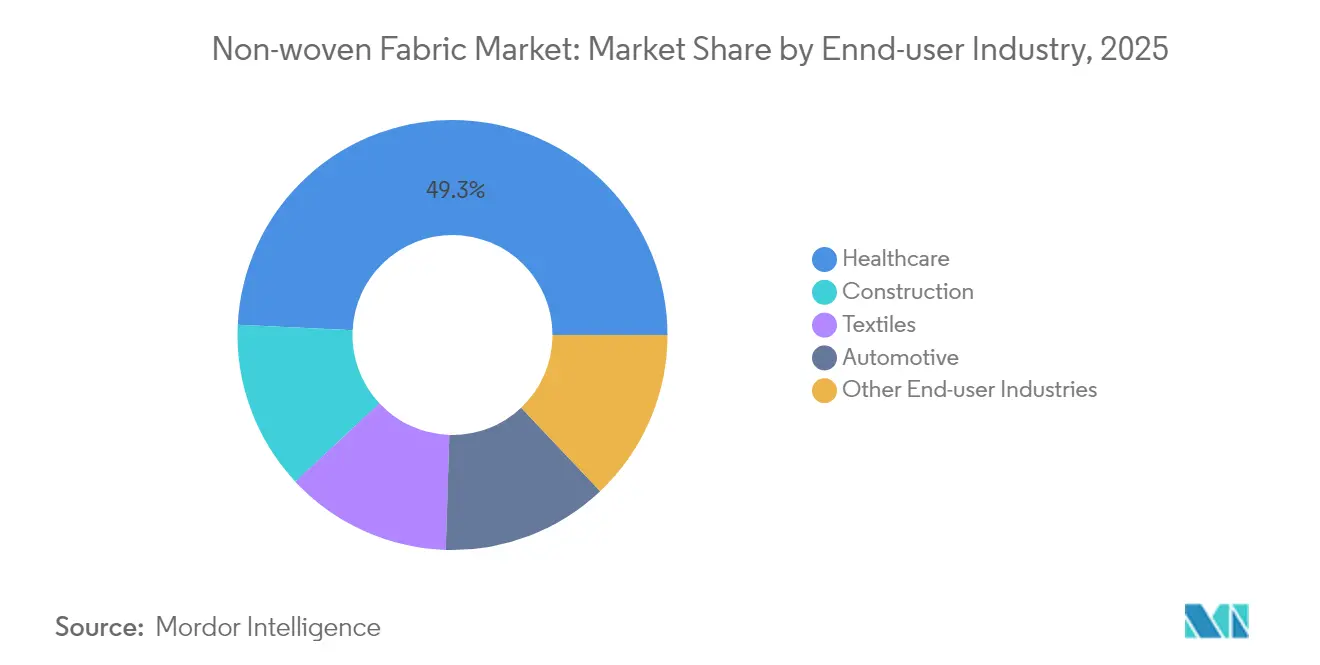

- By end-user industry, healthcare captured 49.25% revenue share in 2025 and is advancing at a 6.42% CAGR through 2031.

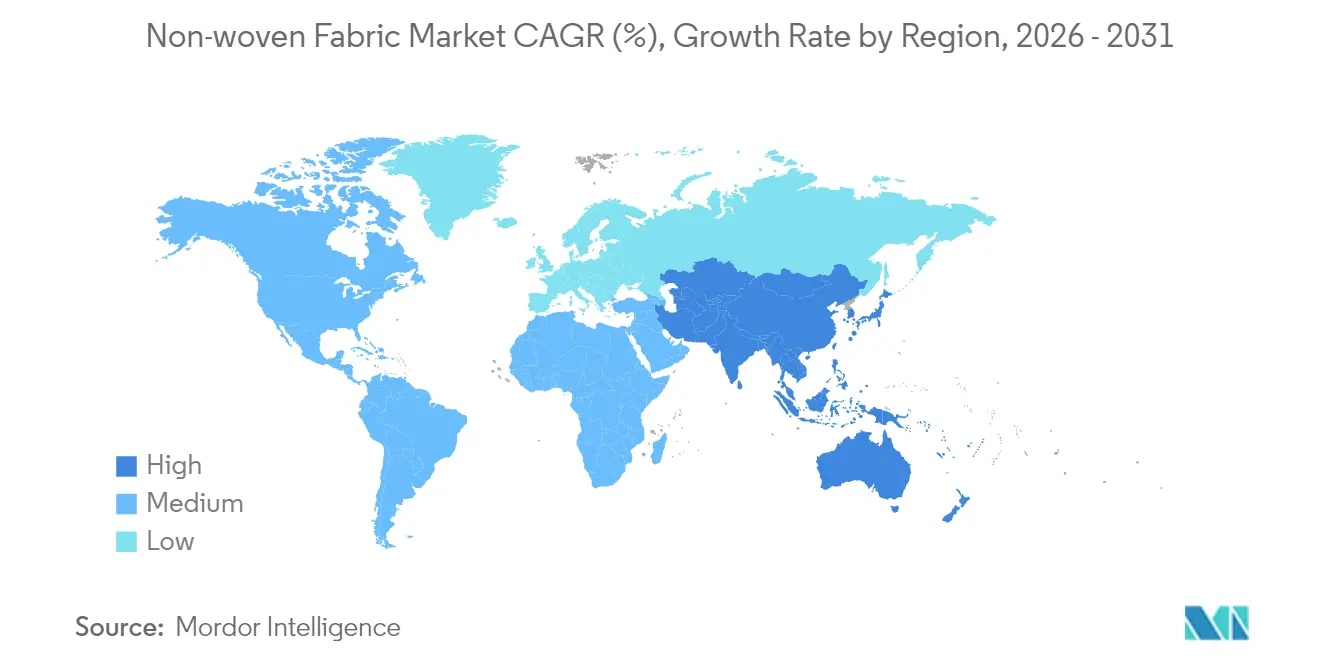

- By geography, Asia-Pacific dominated with 48.10% share of the non-woven fabric market in 2025, and the region is forecast to record a 7.50% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Non-woven Fabric Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding demand for disposable hygiene products | +1.8% | Global, with APAC and emerging markets leading | Medium term (2-4 years) |

| Rapid adoption in medical PPE and wound-care | +1.5% | Global, accelerated in developed markets post-pandemic | Short term (≤ 2 years) |

| Infrastructure boom driving geotextile uptake | +1.2% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Cost-advantage over woven and knitted fabrics | +0.9% | Global manufacturing regions | Medium term (2-4 years) |

| Solid-state EV battery separators | +0.7% | North America, Europe, China EV production hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Exploding Demand for Disposable Hygiene Products

Soaring birth rates in parts of Asia-Pacific and steadily aging populations in North America and Europe are lifting unit sales of diapers, adult incontinence pads, and feminine hygiene articles that rely on lightweight, absorbent non-wovens[1]EDANA, “Nonwovens in Medical and Healthcare,” edana.org. Smart wound-care substrates incorporating controlled vapor transmission films and super-absorbent cores are moving from pilot to high-volume production, improving healing environments and reducing dressing changes. Producers are pairing spun-bond and melt-blown layers to optimize fluid handling while keeping basis weight low, a configuration that helps converters meet price points without sacrificing performance. Brand owners also favor chlorine-free fluff pulps and bio-based binders to align with retailer sustainability scorecards. Together, these trends reinforce the non-woven fabric market trajectory in hygiene through mid-decade.

Rapid Adoption in Medical PPE and Wound-Care

Hospital supply chains that experienced shortages during the pandemic have expanded stocking requirements for masks, gowns, and drapes with certified barrier performance[2]CDC/NIOSH, “Healthcare Personal Protective Technology Targets,” cdc.gov. NIOSH targets for 2020-2030 emphasize domestic surge capacity, prompting investment in high-output spun-melt composites equipped with real-time quality monitoring. Electrospun nanofibers based on polyimide or PEEK deliver elevated heat resistance, allowing their use in powered air-purifying respirators and implantable devices. Multifunctional wound dressings integrating silver nanoparticles or growth factors show more than 99.99% bacterial reduction and faster epithelialization in pre-clinical trials. Reimbursement reforms that reward shorter hospital stays further support demand for advanced non-wovens that cut infection risk and healing time.

Infrastructure Boom Driving Geotextile Uptake

Mega-projects in road, rail, and coastal defense across India, Indonesia, and the Gulf Cooperation Council underpin rising consumption of non-woven geotextiles. Compared with woven alternatives, needle-punched polypropylene felts offer higher porosity and bidirectional water flow, preventing soil intermix while enabling drainage. Municipal landfill cells specify thicker non-woven layers to shield HDPE liners from puncture during waste compaction. Engineers also spray-coat geotextiles with bentonite clay or polymer barriers to contain contaminants and limit evaporation. As governments allocate stimulus budgets to climate-resilient infrastructure, demand for durable yet economical separation fabrics is set to climb steadily.

Cost Advantage Over Woven and Knitted Fabrics

Spun-bond lines convert polypropylene pellets directly into bonded webs in one continuous step, reducing labor and energy costs relative to weaving yarn into fabric. Melt-blown technology achieves fiber diameters under 2 µm with production speeds up to 1,000 kg per hour, a scale unmatched by electrospinning. Process innovations such as intense needling trim electricity use and permit low-basis-weight automotive insulators. Because non-wovens skip the carding and weaving stages, scrap rates stay below those of traditional textiles, delivering an attractive total cost of ownership to converters that face margin pressure from volatile resin prices.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PP and PET price volatility | -1.4% | Global, particularly Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Micro-plastic/landfill regulations tightening | -0.8% | Europe leading, expanding to North America | Medium term (2-4 years) |

| Inferior tensile and tear strength vs woven fabric | -0.5% | Global, affecting technical applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PP and PET Price Volatility

Unplanned refinery outages and delayed new propylene capacities have tightened supply, lifting polypropylene contract prices in South Asia by USD 10-20 per ton in early 2025. At the same time, freight surcharges tied to Red Sea rerouting inflate delivered costs into key converting hubs. PET markets mirror the pattern as producers in China and Europe shut older polymer lines amid negative spreads. Such swings compress margins for converters locked into fixed-price supply contracts with hygiene brand owners, prompting them to explore resin hedging or material substitution strategies.

Microplastic and Landfill Regulations Tightening

The European Union’s draft regulation on pellet loss introduces mandatory containment and quarterly reporting for any operator handling more than 5 tons of raw plastic annually, with fines that can reach 4% of turnover. France requires microfiber filters on new washing machines from 2025, a rule expected to cut fiber shedding by up to 80%. Studies confirm that functional polyester garments can release 173-672 mg of fibers per kilogram during home laundering, adding urgency to mitigation measures. Brands are therefore specifying biodegradable or recyclable non-wovens and pushing suppliers to certify cradle-to-grave impacts, which raises compliance costs and redesign effort.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Spun-bond Strength Anchors Diversification

The spun-bond segment accounted for 52.88% of the non-woven fabric market in 2025, reflecting its high throughput and proven suitability for hygiene laminates, medical gowns, and geotextiles. Generational upgrades now integrate weight-control scanners and closed-loop air recirculation to curb energy use. Growth opportunities emerge in ultra-soft topsheets and 3-layer SMX-based composites that enhance cloth-like feel without sacrificing barrier integrity.

Other technologies are set to expand at an 8.74% CAGR to 2031, lifting their contribution to the non-woven fabric market size through electrospinning, centrifugal spinning, and intense needling platforms that deliver nanofiber webs, gradient density mats, and 3D lofted felts. Electrospun separators using PAN/PS/PMMA blends achieve 75.87% porosity and less than 3% shrinkage at 150 °C, features valued in high-safety battery packs. Melt-blown producers combine electret charging with nanoparticle doping to maintain more than 97% capture of 0.3 µm aerosols, securing air-filtration and respirator contracts.

By Material: Polypropylene Leads Yet Rayon Gains Momentum

Polypropylene held a 63.45% share of the non-woven fabric market size in 2025, sustained by low density, chemical inertness, and compatibility with spun-melt processes that dominate high-volume applications. Converters are boosting post-consumer recycled PP usage to meet brand recycling targets, although supply purity remains a constraint.

Rayon, chiefly in lyocell form, is forecast to log the fastest 6.47% CAGR. Lenzing introduced fine 1.3 dtex and coarse 6.3 dtex variants that enhance softness or fluid permeability in wipes and wound dressings while remaining fully biodegradable. Wood-based fibers evade single-use plastics labeling in Europe, offering easy regulatory compliance. Hybrid webs blending rayon with kapok or agricultural-waste fibers further elevate sustainability credentials without major process changes.

By End-user Industry: Healthcare Extends Premium Edge

Healthcare generated 49.25% of the non-woven fabric market revenue in 2025 and is projected to grow at a 6.42% CAGR to 2031 as hospitals adopt single-patient-use drapes and devices to cut infection risk. Implantable scaffolds formed from resorbable electrospun fibers support tissue regeneration, and drug-eluting dressings deliver controlled therapeutic release.

Construction ranks second as governments prioritize resilient infrastructure. Non-woven geotextiles facilitate soil stabilization and drainage layers beneath paved surfaces, extending roadway life. Automotive manufacturers deploy lightweight PET or PP felts for acoustic panels and EV battery enclosures that slash vehicle mass by more than 50% relative to steel casings. The sectors of packaging, agriculture, and industrial filtration also accelerate uptake owing to performance and sustainability gains.

Geography Analysis

Asia-Pacific commanded 48.10% of non-woven fabric market share in 2025 and is on course for a 7.50% CAGR to 2031 as converters expand in China, India, and Indonesia to serve growing diaper and mask consumption. Regional supply chains integrate propylene crackers, fiber spinning, and end-product assembly within close proximity, minimizing logistics cost. Chinese lines add needlepunch capacity dedicated to acoustic and thermal insulation for domestic EV factories, while Indian producers scale spun-lace installations to supply wipes exporters.

North America benefits from reshoring of critical medical-PPE and battery-separator supply, supported by Kimberly-Clark’s USD 2 billion expansion across Ohio and South Carolina facilities that feature AI-enabled logistics. Canada’s forthcoming separator plant from Asahi Kasei will feed the U.S. EV ecosystem beginning in 2027. Tight labor markets push the adoption of high-automation spun-bond lines, creating opportunities for equipment vendors.

Europe’s stringent regulations spur investment in biodegradable fibers and closed-loop recycling pilots. Freudenberg’s acquisition of Heytex deepens exposure to coated technical textiles, while Lenzing’s lyocell upgrades secure long-term supply of bio-based inputs. Middle East and Africa show emerging demand linked to coastal protection and sanitary product localization, whereas Latin America leverages nearshoring to supply North American hygiene brands with competitively priced composites.

Competitive Landscape

The market is fragmented in nature. Freudenberg Performance Materials absorbed large parts of Heytex to broaden coated fabric capabilities for architecture and logistics applications. Strategic focus centers on cost leadership, sustainability promises, and application depth. UNIFI and Rudra Ecovation secure bottle-to-fiber closed loops processing more than 8.8 million PET bottles per day into recycled non-wovens. Innovation alliances flourish: spun-laid producers license nanofiber overlays to raise breathability and softness in hygiene laminates, and battery firms partner with separator specialists to tailor porosity and ceramic coatings for thermal runaway mitigation.

Non-woven Fabric Industry Leaders

Ahlstrom

Amcor plc

DuPont

Fitesa SA and Affiliates

Freudenberg Performance Materials

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Avgol, part of Indorama Ventures, started a high-capacity multiple-beam spun-bond line and a 3-layer lamination unit in North Carolina as part of a USD 100 million investment to boost non-woven composites output.

- May 2024: Mitsui Chemicals Asahi Life Materials introduced a spun-bond grade made from home-compostable resin aimed at beverage filtration, food-contact packaging, and agricultural films.

Global Non-woven Fabric Market Report Scope

Non-woven fabrics are broadly defined as sheet or web structures bonded together by entangling fiber or filaments mechanically, thermally, or chemically. They are flat, porous sheets made directly from separate fibers or molten plastic or plastic film.

The non-woven fabric market is segmented by technology, material, end-user industry, and region. By technology, the market is segmented into spun-bond, wet-laid, dry-laid, and other technologies. By material, the market is segmented into polyester, polypropylene, polyethylene, rayon, and other materials. By end-user industry, the market is segmented into construction, textile, healthcare, automotive, and other end-user industries. The report also covers the market size and forecasts for the market in 27 countries across the major regions.

For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Technology

| Spun-bond |

| Wet Laid |

| Dry Laid |

| Other Technologies |

By Material

| Polyester |

| Polypropylene |

| Polyethylene |

| Rayon (Viscose) |

| Others |

By End-user Industry

| Construction |

| Textiles |

| Healthcare |

| Automotive |

| Other End-user Industries |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Turkey | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Nigeria | |

| Egypt | |

| Qatar | |

| United Arab Emirates | |

| Rest of Middle-East and Africa |

| By Technology | Spun-bond | |

| Wet Laid | ||

| Dry Laid | ||

| Other Technologies | ||

| By Material | Polyester | |

| Polypropylene | ||

| Polyethylene | ||

| Rayon (Viscose) | ||

| Others | ||

| By End-user Industry | Construction | |

| Textiles | ||

| Healthcare | ||

| Automotive | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Turkey | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Qatar | ||

| United Arab Emirates | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the global non-woven fabric market in 2031?

The market is forecast to reach USD 86.55 billion by 2031.

Which end-user category currently generates the highest demand for non-woven fabrics?

Healthcare leads with 49.25% revenue share, reflecting strong uptake in medical PPE and advanced wound care.

Why are rayon-based non-wovens gaining popularity?

Rayon offers biodegradable performance that aligns with tightening microplastic and landfill regulations in Europe and North America.

How fast will the Asia-Pacific region grow through 2031?

Asia-Pacific is projected to register a 7.50% CAGR on the back of expanded production capacity and rising hygiene consumption.

What impact does polypropylene price volatility have on converters?

Rising propylene costs compress margins, prompting converters to consider recycled PP, material substitution, and resin hedging strategies.

Which technology segment is expected to grow the fastest during the forecast period?

Other technologies, led by electrospinning and centrifugal spinning, are set for an 8.74% CAGR thanks to applications in battery separators and medical devices.

Page last updated on: