Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

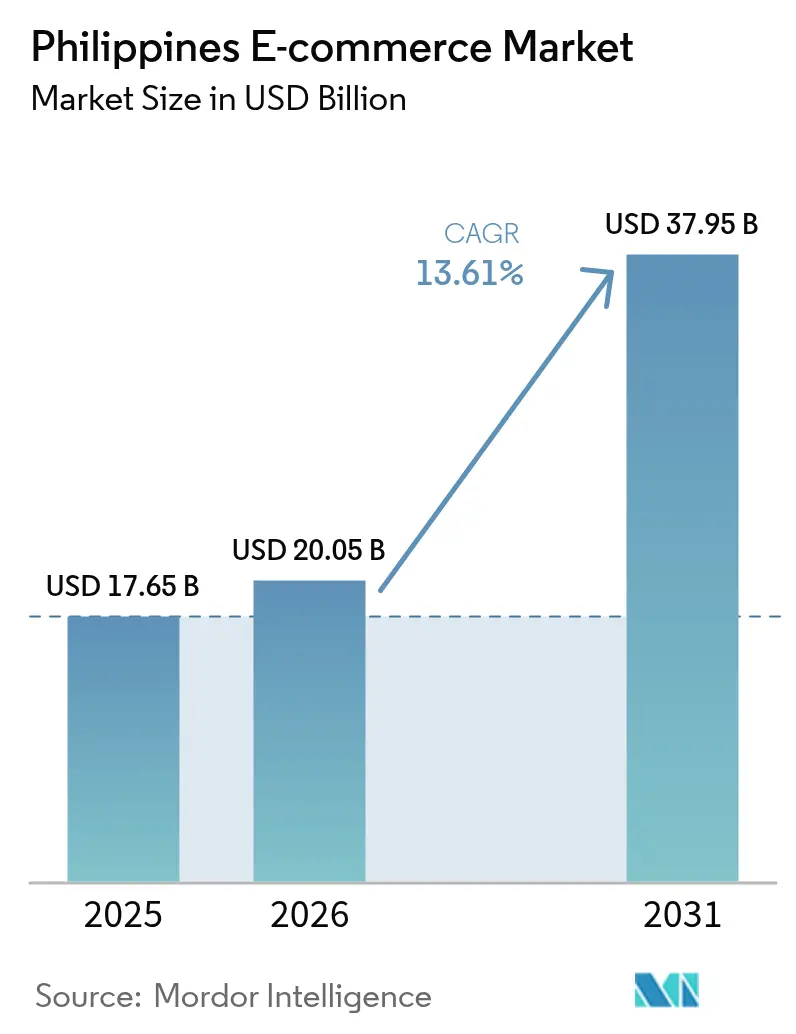

| Base Year Market Size (2025) | USD 17.65 Billion |

| Market Size (2026) | USD 20.05 Billion |

| Market Size (2031) | USD 37.95 Billion |

| Growth Rate (2026 - 2031) | 13.61% CAGR |

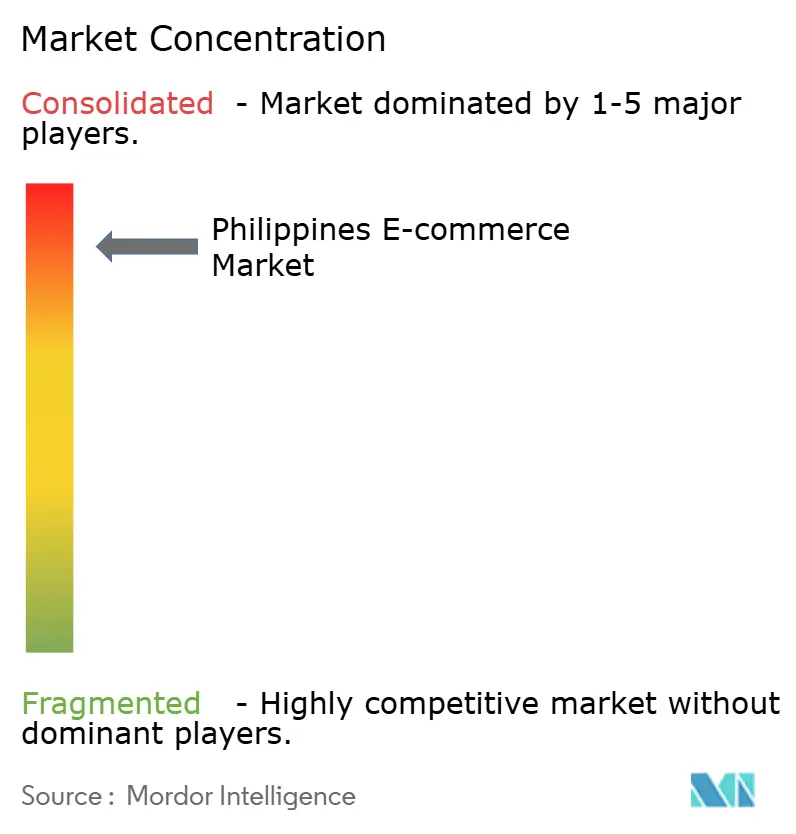

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines E-commerce Market Analysis by Mordor Intelligence

The Philippines e-commerce market size is expected to grow from USD 17.65 billion in 2025 to USD 20.05 billion in 2026 and is forecast to reach USD 37.95 billion by 2031 at 13.61% CAGR over 2026-2031. Its growth has been propelled by nationwide mobile-wallet penetration that exceeded 65% in 2024, the rollout of provincial logistics mini-hubs that shorten delivery routes across 7,641 islands, and policy targets that position digital trade as a core engine for the PHP 1.2 trillion e-commerce sector. Intensifying platform competition, the rapid uptake of Buy-Now-Pay-Later (BNPL) credit, and the concerted push to utilize the Regional Comprehensive Economic Partnership (RCEP) for tariff-free cross-border shipments have further expanded the Philippines e-commerce market’s addressable base. Merchant digitization programs led by the Department of Trade and Industry (DTI) accelerated SME onboarding, while AI-enhanced live-commerce tools raised conversion rates, especially in fashion and beauty streams.

Key Report Takeaways

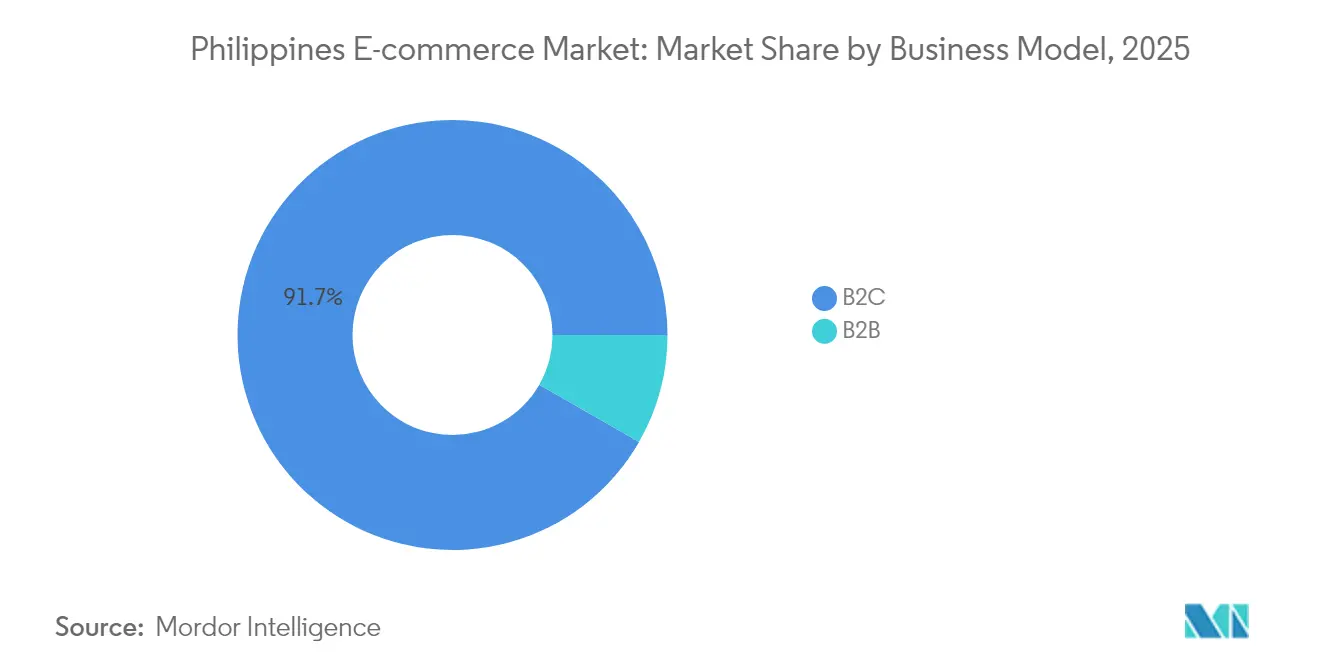

- By business model, B2C transactions captured 91.72% of the Philippines e-commerce market share in 2025, whereas B2B commerce is projected to expand at a 14.76% CAGR through 2031.

- By Payment Mode for B2C E-commerce, mobile wallets controlled 64.74% of 2025 value, but BNPL is expected to post 15.45% CAGR to 2031.

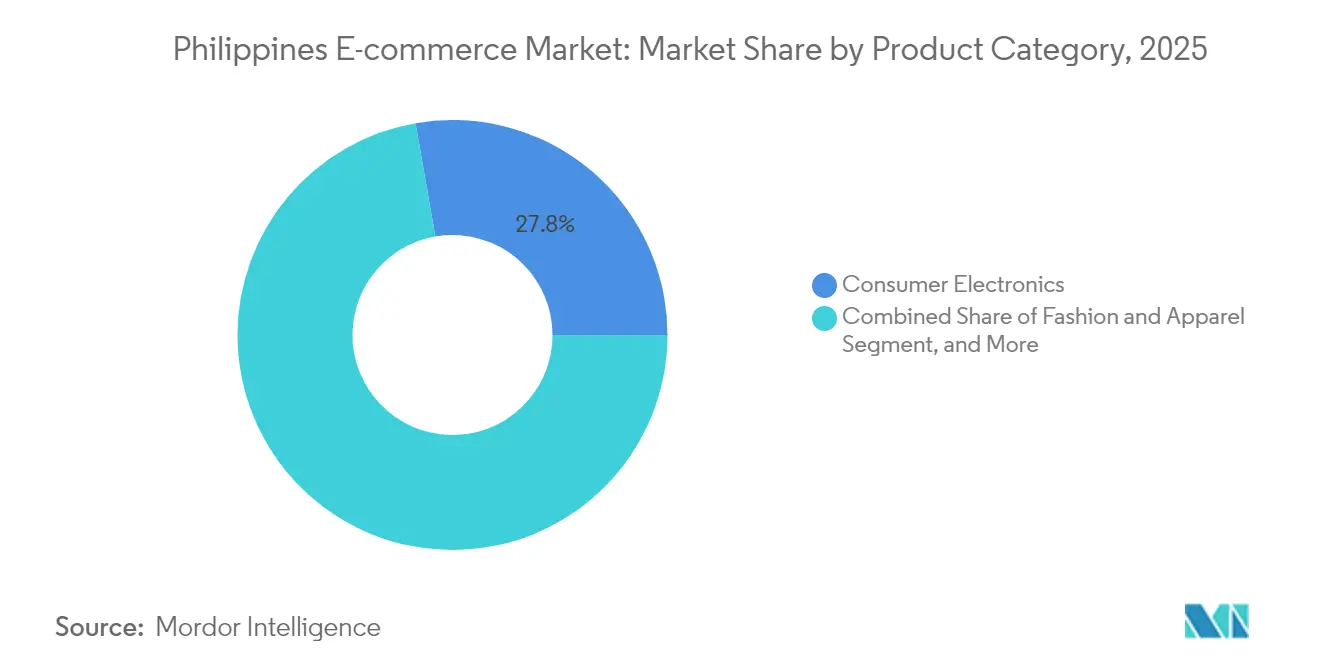

- By Product Category for B2C E-commerce, Consumer Electronics held 27.75% of 2025 revenue, while Food and Beverages are slated to grow at 14.41% CAGR to 2031.

- By device type, smartphones generated 78.52% of sales in 2025 and are also the fastest-growing device segment at 13.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Philippines E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring mobile-wallet penetration | +3.2% | National, strongest in NCR & Central Visayas | Short term (≤ 2 years) |

| Logistics mini-hubs in provincial cities | +2.8% | Luzon-Other, Visayas, Mindanao | Medium term (2-4 years) |

| Rapid cross-border social-commerce adoption | +2.1% | National; early gains in NCR, Cebu, Davao | Medium term (2-4 years) |

| Digital-payment mandates for government fees | +1.9% | National | Short term (≤ 2 years) |

| MSME onboarding incentives | +1.5% | National | Long term (≥ 4 years) |

| AI-powered live-commerce engagement | +1.8% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Soaring Mobile-Wallet Penetration Transforms Payment Infrastructure

GCash amassed 94 million users by early 2025, while Maya widened its wallet with credit extensions such as the Maya Black card, raising digital payments to 52.8% of retail transaction volume in 2023.[1]Bangko Sentral ng Pilipinas, “2023 Report on E-payments Measurement,” bsp.gov.ph Visa’s integrations let 87% of surveyed Filipinos fund wallets using cards, blurring lines between traditional banking and app-based finance. Seamless linkages between wallets and marketplaces have lowered merchant onboarding hurdles, pushed unbanked consumers into formal channels, and enlarged the Philippines e-commerce market’s daily active buyer pool. Super-app roadmaps now embed savings, credit, and insurance modules that tether users to commerce ecosystems. This payment ubiquity has shortened checkout flows and lifted repeat-purchase frequency.

Logistics Mini-Hubs Enable Provincial Commerce Expansion

Courier groups such as J&T Express and Ninja Van scaled fleet capacity and opened sub-depot networks in Cebu, Iloilo, and Davao, cutting delivery lead-times by up to 30% relative to Metro Manila fulfilment routes. Central Visayas, which logged 7.3% GRDP growth in 2024, now enjoys same-day delivery for high-velocity SKUs, unlocking pent-up provincial demand.[2]SunStar Publishing, “Central Visayas Still PH’s Fastest Growing Economy,” sunstar.com.ph Mini-hub economics also reduce failed-delivery rates in remote municipalities, boosting merchant margins. Enhanced route density improves asset utilization, persuading platforms to list bulky and perishable goods that previously faced prohibitive freight costs. The model is replicable across Mindanao’s secondary cities, indicating sustained upside for the Philippines e-commerce market.

Rapid Cross-Border Social-Commerce Adoption

TikTok Shop’s live-commerce tools and marketplace global seller programs offer tariff-free sourcing under RCEP, encouraging Filipino buyers to access Japanese beauty items and Korean gadgets at lower landed cost. DTI’s Philippine e-Commerce Platform (PEP Store) launched in July 2025 with 350 domestic brands to balance the import influx and link local MSMEs to overseas consumers. Early movers in cross-border beauty have mirrored Vietnamese sellers’ 50% export value surge, signaling untapped export upside. Younger demographics-responsible for 68.6% rise in peer-to-peer wallet transfers-drive livestream shopping, pushing the Philippines e-commerce market toward entertainment-centric retail formats. Platforms must now curate interactive feeds rather than static catalogs.

AI-Powered Live-Commerce Engagement

Sea Limited rolled out OpenAI-powered scripts that auto-generate product recommendations during Shopee live sessions, while Lazada tested dynamic pricing bots that adjust offers in real time. Conversion rates in AI-assisted streams run three to five times higher than on-site browsing, especially in fashion and cosmetics where real-time Q&A reduces purchase anxiety. GCash applies machine-learning fraud filters to transaction data, giving merchants granular risk scores and lowering charge-back ratios. Personalization engines tap browsing history to queue tailored vouchers, nudging basket size upward. These AI utilities differentiate platforms and cement the Philippines e-commerce market’s reputation as Southeast Asia’s live-commerce test lab.

Restraints Impact Analysis*

| Restraint | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High last-mile costs outside NCR | -2.4% | Luzon-Other, Visayas, Mindanao | Medium term (2-4 years) |

| Fragmented VAT compliance among merchants | -1.8% | National, acute in MSME segments | Short term (≤ 2 years) |

| Data-privacy skills gap in SMEs | -1.2% | National | Long term (≥ 4 years) |

| Port congestion and customs delays | -1.6% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Last-Mile Costs Outside NCR

Deliveries to far-flung islands often exceed 15% of order value, eroding margins on low-ticket grocery and FMCG items that are climbing at 14.67% CAGR. Multi-modal routes involving inter-island ferries and provincial roads remain vulnerable to typhoons, creating fulfillment unpredictability. Although mini-hubs narrow cost gaps, network density in Luzon-Other and Mindanao is still thin, compelling couriers to levy surcharges. Consumers outside NCR also show lower disposable income, compressing price ceilings for delivery fees. Without accelerated infrastructure spending under public-private logistics partnerships, last-mile friction will keep suppressing the Philippines e-commerce market’s rural penetration.

Fragmented VAT Compliance Among Merchants

DTI’s push for electronic invoicing aims to alleviate mosaic tax rules, yet many MSMEs lack accounting resources and avoid formal registration despite incentives such as BMBE exemptions. Cross-border sellers face overlapping value-added-tax and import duties, generating reconciliation headaches that discourage participation. Platforms must therefore build automated tax modules to retain small sellers. Until rule harmonization reaches local governments, compliance uncertainty will drag on Philippines e-commerce market onboarding velocity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: B2B Momentum Narrows the Gap

B2C held 91.72% of the Philippines e-commerce market share in 2025, translating into sizeable absolute GMV, yet the B2B vertical is expanding at 14.76% CAGR and is set to unlock larger basket values. The Philippines e-commerce market size associated with electronic procurement for manufacturers and distributors is rising as firms migrate away from fax and phone orders in favor of digital portals that consolidate spending and integrate credit terms.

Corporate buyers now demand embedded finance-UnionBank’s API partnerships allow invoice-based lending directly within procurement dashboards-signaling that payment rails will shape B2B platform selection. Investor appetite for wholesaler-centric marketplaces such as Growsari, which raised USD 17.8 million, underscores confidence that B2B service depth will compress B2C’s historical dominance in the Philippines e-commerce market.

By Device Type for B2C E-commerce: BNPL Scales Credit Access

Mobile wallets represented 64.74% of transaction value in 2025, but Other Payment Modes are forecast to log a 15.45% CAGR, expanding the Philippines e-commerce market size accessible to underbanked shoppers. BillEase, already profitable in 2023, embedded its installment option across 10,000 merchants, enabling small-ticket splits without card credentials.

Wallet operators like Maya now white-label BNPL plugins, merging credit scoring with wallet KYC data to mitigate default risk. Cash-on-delivery has shrunk as trust in digital refunds improves, while real-time bank transfers receive regulatory backing under the InstaPay rail. Payment providers that deliver holistic ecosystems-credit, savings, insurance-will capture the Philippines e-commerce market’s next growth wave.

By Product Category for B2C E-commerce: Grocery Digitization Accelerates

Consumer Electronics secured 27.75% of 2025 revenue, but food and beverages are on track for the fastest 14.41% CAGR, driven by social group-buy platforms such as SariSuki, whose gross merchandise value multiplied 36-fold between 2023 and 2025. Community leaders consolidate neighborhood orders, leveraging mini-hub drop-offs that sidestep traditional wet-market visits.

Cross-border beauty imports flourish under RCEP; Filipino livestream sellers bundle Korean skincare into flash deals that routinely sell out in minutes. AI sizing tools and virtual try-ons decrease return rates in fashion. Furniture remains logistics-constrained, though platform-managed line-haul agreements slowly improve fee transparency. Overall, diversified category depth makes the Philippines e-commerce market resilient against saturation in electronics.

By Device Type for B2C E-commerce: Smartphone-First Commerce Deepens

Smartphones generated 78.52% of GMV in 2025 and are climbing at 13.92% CAGR, reinforcing a mobile-only design ethos among platforms. Responsive web apps mimic native-app performance, while 5G rollout in 2025 boosted average download speed by 36%, encouraging video-rich live commerce that anchors the Philippines e-commerce market.

Desktops remain essential for enterprise sourcing and high-consideration purchases, but their share inches downward as smartphone screen sizes reach 6.7 inches and foldables proliferate. Tablets sit in a niche for content creators and home schooling. Platform roadmaps center on voice search, AR visualization, and geo-tagged vouchers, illustrating how mobile hardware capabilities steer service innovation.

Geography Analysis

NCR retained the largest slice of 2025 spend owing to dense logistics infrastructure, same-day fulfillment and a payments ecosystem that bundles SeaBank, ShopeePay and GCash super-app functions. However, NCR’s growth trajectory moderates as platform saturation sets in and user acquisition costs climb.

Central Visayas, led by Cebu’s significant asset base, has emerged as the fastest-growing regional market. Regional hubs reduce delivery times to nearby islands, encouraging FMCG sellers to experiment with same-day grocery deliveries. Government tourism initiatives and BPO inflows are boosting disposable income, driving the adoption of live-commerce entertainment tailored to mobile-centric lifestyles.

Luzon-Other and Mindanao still wrestle with logistics gaps and lower wallet adoption, but policy aid through programs like OTOP and Go Lokal has driven PHP 3.11 billion in artisanal sales since 2017. As mini-hubs proliferate and 5G coverage south of Metro Manila improves, these zones present the Philippines e-commerce market with white-space for category-specific expansion-especially agriproducts and regional delicacies that enjoy local supply-chain advantages.

Competitive Landscape

Shopee, Lazada and TikTok Shop dominate GMV and spend aggressively on integrated financial services that deepen user stickiness. Shopee’s linkage with SeaBank lets shoppers open savings accounts and secure microloans without leaving the app, a strategy that widens the Philippines e-commerce market funnel. Lazada leverages Alibaba’s Cainiao logistics stack and AI product-matching engine to raise seller conversion and lower delivery costs.

TikTok Shop pivots on creator-led livestreams where AI co-hosts moderate chats and suggest add-on bundles, generating click-through rates markedly higher than static listings. Etaily’s USD 17.8 million war chest illustrates demand for category specialists that manage end-to-end brand commerce from content to cross-border fulfillment.

Barriers to entry center on VAT compliance and data-privacy adherence, compelling new entrants to invest in automated regulatory modules. Embedded-finance newcomers such as UNO Digital Bank secured USD 32.1 million to offer white-label credit tools, signaling convergence between fintech and retail stacks. As live-commerce, AI and financial services intersect, future leadership will hinge on ecosystem breadth rather than price subsidy races.

Philippines E-commerce Industry Leaders

Sea Ltd.

Alibaba Group

ByteDance Ltd.

Global Fashion Group

Amazon.com Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The Department of Trade and Industry launched the Philippine e-Commerce Platform (PEP Store) featuring 350 local merchants, aiming to boost MSME digitization.

- June 2025: RCEP utilization became crucial for achieving the Philippines’ USD 240.5 billion export target by 2028.

- May 2025: President Ferdinand R. Marcos Jr. approved the Philippine Export Development Plan 2023-2028 with adjusted export targets of USD 105.3 billion.

- April 2025: DTI announced a five-point strategy emphasizing digitalization and AI to improve MSME competitiveness.

Philippines E-commerce Market Report Scope

E-commerce is the buying and selling of goods and services over the Internet through online shopping. However, this term is often used to describe all the seller's efforts in selling products directly to consumers. It begins when potential customers learn about a product, buy it, use it, and ideally maintain lasting customer loyalty.

The scope of the study is limited to tracking the revenue generated through the e-commerce market in the Philippines. The study also tracks key market metrics, underlying growth influencers, and significant industry vendors, providing support for market estimates and growth rates in the Philippines e-commerce market throughout the anticipated period. The study looks at Covid-19's overall influence on the ecosystem. The report's scope includes market size and forecasting for B2B and B2C segments, with the qualitative analysis of the B2C channel being further split by application.

The Philippines e-commerce market is Segmented into B2C e-commerce (application (beauty and personal care, consumer electronics, fashion and apparel, food and beverage, furniture and home)) and B2B e-commerce. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Business Model

| B2B |

| B2C |

By Payment Mode for B2C E-commerce

| Credit/Debit Cards |

| Mobile Wallets |

| Other Payment Modes for B2C E-commerce |

By Product Category

| Beauty and Personal Care |

| Consumer Electronics |

| Fashion and Apparel |

| Food and Beverages |

| Furniture and Home |

| Toys, DIY and Media |

| Other Product Categories for B2C E-commerce |

By Device Type for B2C E-commerce

| Smartphone |

| Desktop/Laptop |

| Other Device Types for B2C E-commerce |

| By Business Model | B2B |

| B2C | |

| By Payment Mode for B2C E-commerce | Credit/Debit Cards |

| Mobile Wallets | |

| Other Payment Modes for B2C E-commerce | |

| By Product Category | Beauty and Personal Care |

| Consumer Electronics | |

| Fashion and Apparel | |

| Food and Beverages | |

| Furniture and Home | |

| Toys, DIY and Media | |

| Other Product Categories for B2C E-commerce | |

| By Device Type for B2C E-commerce | Smartphone |

| Desktop/Laptop | |

| Other Device Types for B2C E-commerce |

Key Questions Answered in the Report

How large was online retail spending in the Philippines in 2026?

The Philippines e-commerce market size reached USD 20.05 billion in 2026.

What annual growth is expected for digital commerce through 2031?

Gross merchandise value is projected to rise at a 13.61% CAGR from 2026 to 2031.

Which payment method leads Philippine online check-outs today?

Mobile wallets held 64.74% of 2025 transaction value, the highest among all methods.

Which product line is expanding the fastest on Philippine platforms?

Food and Beverages items are forecast to grow at a 14.41% CAGR through 2031.

Which region outside Metro Manila shows the quickest e-commerce upswing?

Central Visayas is the fastest-growing, backed by Cebu’s strong economic base and logistics hubs.

Page last updated on: