Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

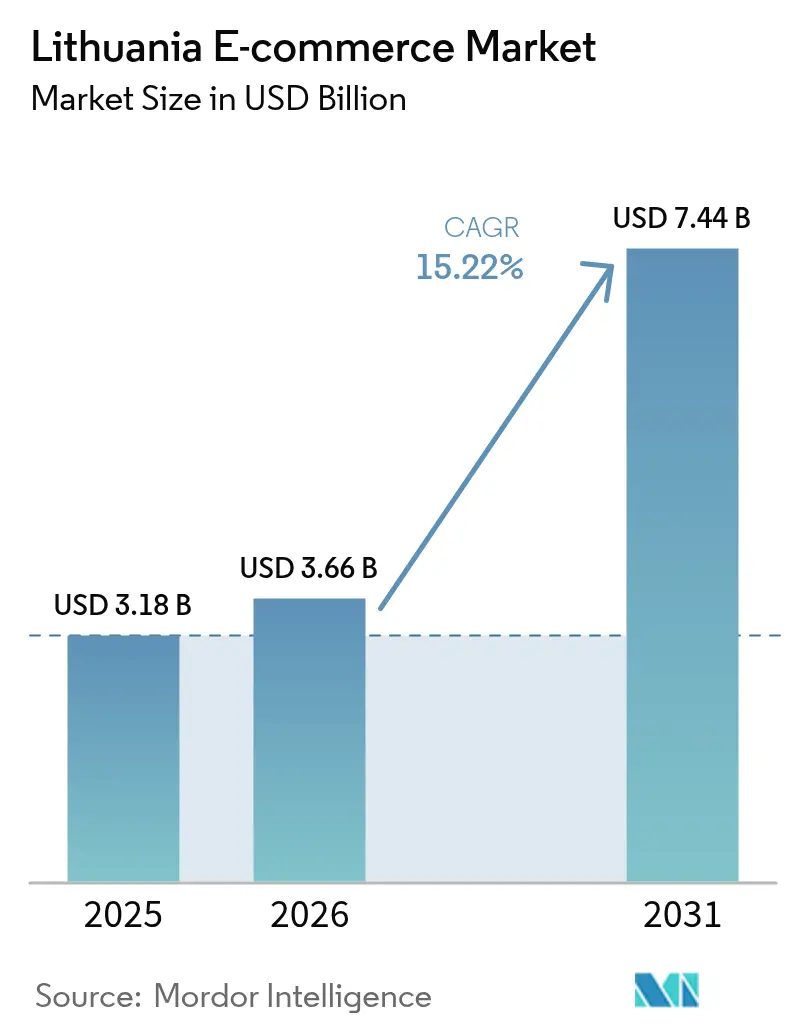

| Base Year Market Size (2025) | USD 3.18 Billion |

| Market Size (2026) | USD 3.66 Billion |

| Market Size (2031) | USD 7.44 Billion |

| Growth Rate (2026 - 2031) | 15.22% CAGR |

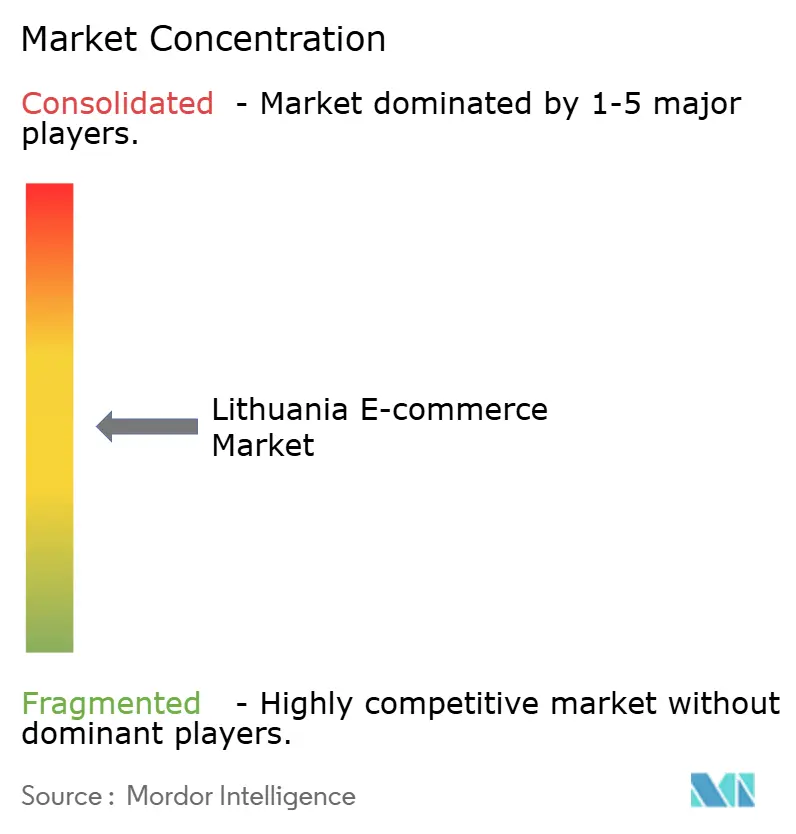

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lithuania E-commerce Market Analysis by Mordor Intelligence

The Lithuania e-commerce market size was valued at USD 3.18 billion in 2025 and estimated to grow from USD 3.66 billion in 2026 to reach USD 7.44 billion by 2031, at a CAGR of 15.22% during the forecast period (2026-2031). This growth stems from the nation’s 38.9% business e-sales penetration rate—the highest in the EU—and from regulatory alignment with the EU Digital Single Market, which simplifies cross-border trade. [1]European Commission, “E-commerce Statistics,” ec.europa.eu Mobile commerce dominates transactions, reflecting 63% of sales, while digital wallets accelerate payment conversion as consumers adopt online payments at a 29% penetration rate that outpaces the eurozone average. [2]European Central Bank, “Study on the Payment Attitudes of Consumers in the Euro Area (SPACE) 2024,” ecb.europa.eu Investments in parcel lockers, 5G coverage, and cold-chain logistics reduce delivery friction and extend service reach beyond Vilnius and Kaunas. Competitive intensity is rising as global platforms scale into Lithuania’s high-growth environment, yet data-privacy enforcement and elevated product-return rates can moderate momentum.

Key Report Takeaways

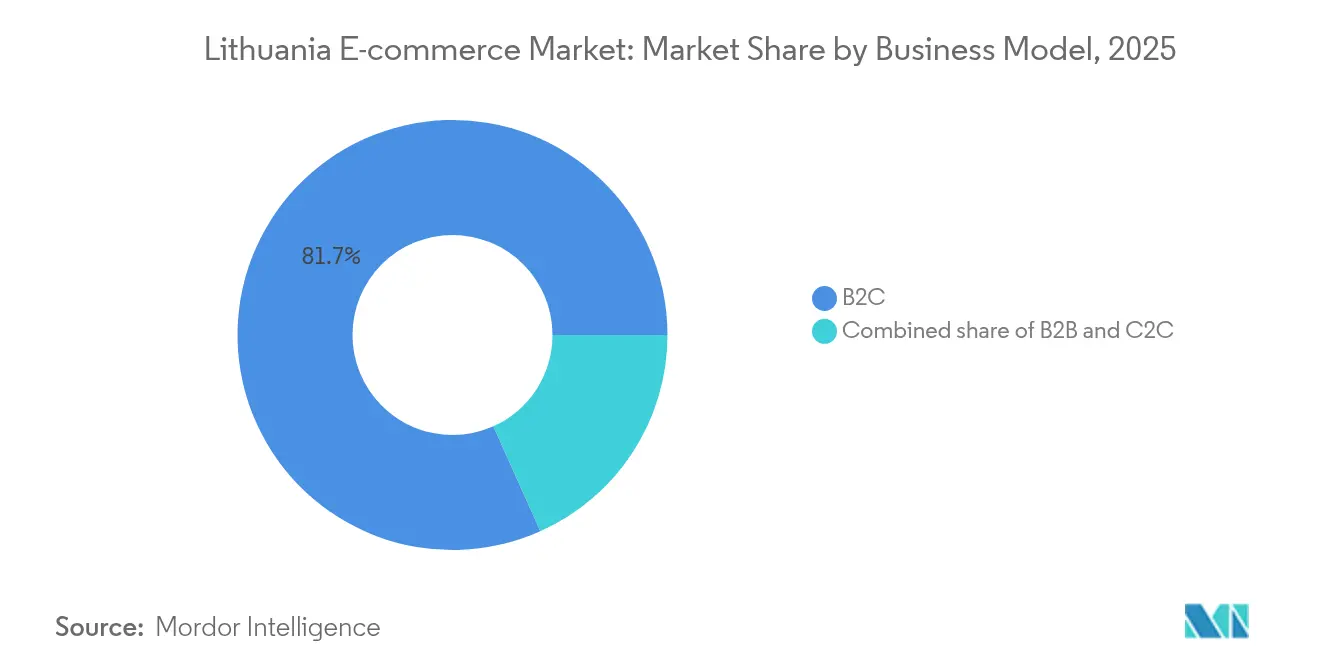

- By business model, the B2C segment held 81.70% of the Lithuania e-commerce market share in 2025, while C2C platforms are forecast to grow at an 18.35% CAGR through 2031.

- By device type, mobile commerce commanded 62.55% share of the Lithuania e-commerce market size in 2025 and is projected to expand at 16.85% CAGR to 2031.

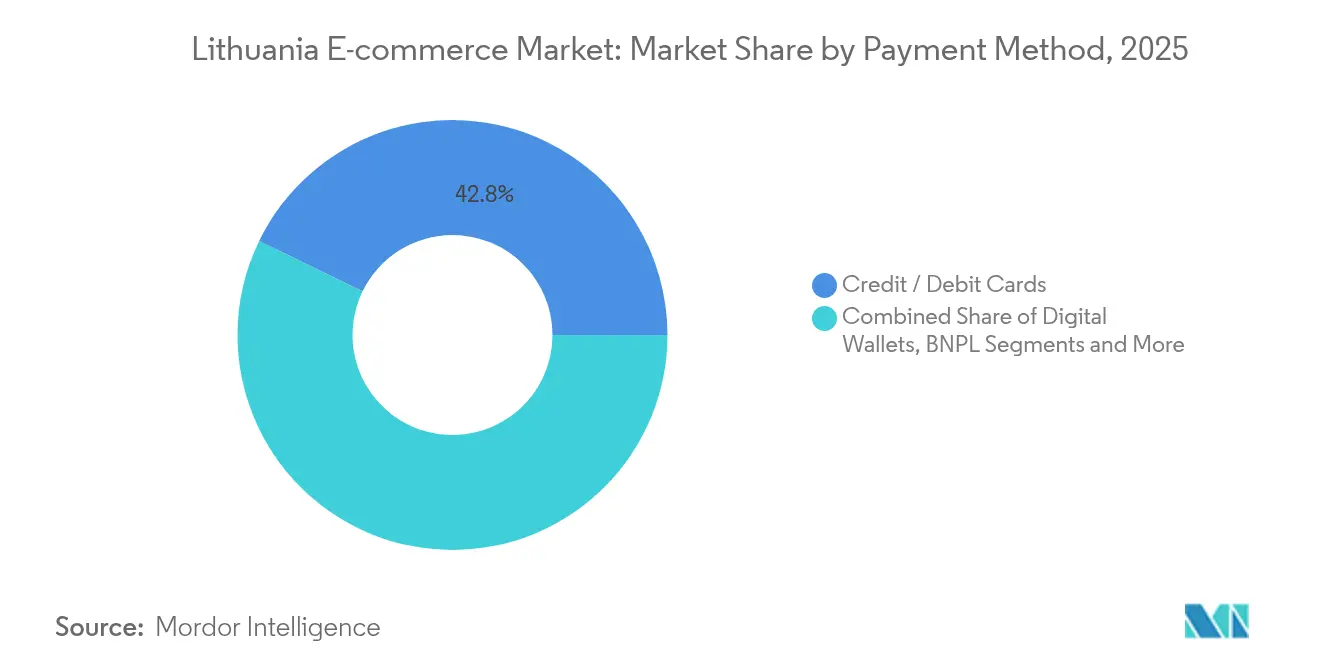

- By payment method, credit and debit cards led with 42.80% share of the Lithuania e-commerce market size in 2025, while digital wallets post the highest growth at 20.98% CAGR through 2031.

- By product category, fashion and apparel accounted for 26.40% of the Lithuania e-commerce market size in 2025; food and beverages are advancing at a 17.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Lithuania E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing smartphone penetration | +2.8% | National, concentrated in Vilnius and Kaunas urban areas | Medium term (2-4 years) |

| Expansion of mobile payments and wallets | +3.2% | National, with cross-border EU spillover effects | Short term (≤ 2 years) |

| Improved last-mile logistics infrastructure | +2.1% | National, rural area gains accelerating | Medium term (2-4 years) |

| EU Digital Single Market compliance gains | +1.9% | EU-wide, Lithuania benefiting from regulatory harmonization | Long term (≥ 4 years) |

| Parcel-locker network proliferation | +1.4% | Urban centers expanding to suburban areas | Short term (≤ 2 years) |

| Remittance-driven online gifting demand | +0.8% | National, diaspora-connected regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Smartphone Penetration

Lithuania’s mobile device share reached 63% in 2024 and is growing at 17.2% CAGR as 5G coverage broadens and banks refine mobile payment rails. Retailers leverage augmented-reality try-ons and push-notification campaigns that resonate with Gen Z audiences. Enterprise adoption still lags EU averages, suggesting catch-up potential for SMBs investing in responsive design. Vinted’s mobile-native model exemplifies monetization, supporting a 330% profit rise to EUR 76.7 million (USD 83.3 million) in 2024.

Expansion of Mobile Payments and Wallets

Digital wallets grow at 21.6% CAGR, aided by the Bank of Lithuania’s licensing of electronic money institutions such as Vinted’s subsidiary, which processes payments across EU markets. Wallet use boosts checkout conversion and lowers merchant fees compared with cards. Network effects intensify as more merchants adopt wallet acceptance, creating a virtuous cycle of consumer uptake. Regulatory clarity around strong customer authentication sustains trust, while buy-now-pay-later options diversify wallet functionality and attract millennial shoppers.

Improved Last-Mile Logistics Infrastructure

Lithuanian Post delivered 12 million parcels in 2024, a 20% jump, and targets 700 parcel lockers by 2029. Locker density reduces delivery times for rural consumers and supports temperature-controlled units for grocery e-commerce. Private couriers pursue route-optimization software to address customer complaints—28% concern improper delivery and 26% concern delays. Sustainability pilots such as reusable packaging, trialed with Vinted, reinforce brand equity while trimming waste.

EU Digital Single Market Compliance Gains

Harmonized digital-contract rules launched in 2022 streamline cross-border transactions and reduce legal costs for Lithuanian exporters. Although implementation gaps persist in VAT alignment, Lithuania’s early adoption provides first-mover advantage when selling into larger EU markets. The Digital Services Act adds compliance overhead for global platforms, potentially leveling the field for domestic firms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and cyber-security concerns | -2.4% | National, with EU-wide regulatory spillover | Short term (≤ 2 years) |

| High product-return rates | -1.8% | National, particularly affecting fashion and footwear categories | Medium term (2-4 years) |

| Limited Lithuanian-language coverage on global sites | -1.2% | National, affecting rural and older demographic segments | Medium term (2-4 years) |

| Warehouse and courier labour shortages | -1.6% | National, concentrated in logistics hubs and urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Cyber-Security Concerns

The State Data Protection Inspectorate issued EUR 2.38 million (USD 2.6 million) in fines to Vinted for GDPR breaches in 2024, heightening compliance risk perceptions. Authorities recorded 273 breach notifications affecting 1.47 million individuals, with human error causing 52% of incidents. Enhanced oversight raises operating costs for SMEs that lack in-house legal teams and may slow user acquisition if trust erodes.

High Product-Return Rates

Return rates reach 20% for clothing and 30% for footwear, inflating reverse-logistics expenses and hitting margins for fashion retailers. [3]European Environment Agency, “The Destruction of Returned and Unsold Textiles in Europe’s Circular Economy,” eea.europa.eu EU proposals forbidding destruction of unsold textiles will require companies to optimize demand planning and reuse programs. Lithuanian logistics providers also note that 21% of consumer complaints relate to damaged parcels, compounding profit leakage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: C2C Platforms Challenge B2C Dominance

The Lithuania e-commerce market size for business-to-consumer channels represented 81.70% of 2025 revenue, illustrating legacy strength of traditional online retail. Consumer-to-consumer platforms, however, outpace the overall Lithuania e-commerce market with an 18.35% CAGR, propelled by Vinted’s EUR 813.4 million (USD 885.5 million) turnover and EUR 5 billion (USD 5.4 billion) valuation. Circular-economy preferences and thrifty Gen Z shoppers favor C2C marketplaces, while B2C operators face price-matching pressure and higher customer-acquisition costs.

B2C incumbents respond by layering premium services, private labels, and rapid delivery. Maxima Group’s BARBORA logged EUR 171.3 million (USD 186.5 million) sales in 2024 by widening product range and scaling dark-store logistics. Meanwhile, Lithuania’s 38.9% enterprise digitization rate signals latent B2B marketplace expansion potential, especially for industrial supplies and export-oriented SMEs.

By Device Type: Mobile Commerce Drives Digital Transformation

Mobile channels accounted for 62.55% of Lithuania e-commerce market share in 2025 and are expected to post a 16.85% CAGR, dwarfing desktop growth. Faster 5G rollouts enable richer content, while biometric authentication reduces cart abandonment. Desktop remains favored for high-ticket B2B orders and complex product configurations.

App-centric strategies unlock geofenced promotions, social-commerce tie-ins, and push-based re-engagement tactics. Yet 39% of Lithuanian firms still lack advanced mobile optimization, underscoring a capability gap that the Lithuania e-commerce market participants can exploit through SaaS storefront templates and no-code app builders. Emerging device categories such as smart TVs and voice assistants offer incremental reach, but their transaction share remains sub-5%.

By Payment Method: Digital Wallets Accelerate Traditional Card Displacement

Credit and debit cards controlled 42.80% of Lithuania e-commerce market size in 2025, but wallet penetration is expanding at 20.98% CAGR, eroding card share. Wallet providers capitalize on instant settlement and tokenized security, lowering fraud risk for merchants. Fast-payment rails also underpin buy-now-pay-later solutions that attract under-banked segments.

Cost advantages and one-click checkout foster convergence around a handful of wallet brands, potentially compressing acquiring margins. Interoperability across SEPA countries furnishes an export channel for Lithuanian fintechs, reinforcing the Lithuania e-commerce industry’s ecosystem depth. Cards remain relevant for travel and corporate spend where chargeback rights are critical.

By B2C Product Category: Food and Beverages Outpace Fashion Growth

Fashion retained 26.40% of 2025 Lithuania e-commerce market size, but high returns and sustainability scrutiny limit margin upside. Food and beverages exhibit the strongest trajectory at 17.05% CAGR, aided by cold-chain advances and active lifestyles seeking convenience. Consumer electronics register steady demand, reflecting Lithuania’s tech-savvy users, while furniture sales rise on home-office upgrades.

Maxima’s BARBORA enhances grocery margins through own-brand lines and temperature-controlled lockers. Conversely, fashion sellers pilot virtual fitting rooms to curb returns and align with the EU’s anti-waste agenda. Category leaders in the Lithuania e-commerce market integrate inventory analytics and dynamic pricing to balance stock risk with fulfillment speed.

Geography Analysis

Urban hubs provide the nucleus of spending as Vilnius and Kaunas benefit from higher broadband penetration, 65.2% employment, and 4.9% unemployment, enabling stable discretionary outlays. The Sostinės region posted a 20.37% enterprise birth rate in 2021, nearly double the EU norm, underpinning startup-driven demand for cloud commerce tools.

Suburban and rural zones increasingly access parcel lockers as Lithuanian Post targets 700 units by 2029, shrinking service gaps and reinforcing customer expectations for two-day delivery. Cross-border parcel flows topped 600,000 shipments to Latvia and Estonia in 2024, illustrating Baltic-wide integration of the Lithuania e-commerce market.

EU-level regulatory harmonization facilitates outbound expansion, yet VAT reconciliation and language localization remain barriers that vendors must navigate. Strengthening regional logistics corridors and leveraging free-trade zones around Klaipėda port will further broaden market coverage as China-EU rail links reroute cargo through the Baltics.

Competitive Landscape

The Lithuania e-commerce market hosts a mixed structure of local champions and multinational entrants. Vinted, Pigu, Senukai, Varle, and Barbora anchor domestic traffic, while Amazon, AliExpress, and eBay skim discretionary spend from cross-border shoppers. Vinted commands scale advantages through a EUR 5 billion (USD 5.4 billion) valuation and integrated wallet licensing that supports lower clearing costs.

Local retailers differentiate with private labels, omnichannel click-and-collect, and Baltic-focused courier alliances. Pigu’s February 2025 restructuring reinstated founder Dainius Liulys to revive service standards and liquidity, signaling strategic emphasis on core assortment and fulfillment excellence. Maxima Group expands dark stores and last-mile fleets to defend grocery share against rapid-delivery newcomers.

Strategic plays include secondary equity rounds to fund infrastructure, as seen in Vinted’s EUR 340 million (USD 370 million) sale led by TPG, aimed at category diversification and AI-driven merchandising. Logistics operators pursue sustainability differentiation with reusable packaging and carbon-footprint tracking, gaining B2B contracts from eco-conscious merchants.

Start-ups cluster around payment orchestration, last-mile robotics, and reverse-logistics platforms, leveraging Lithuania’s favorable sandbox regulations. Global entrants monitor the market’s affluent digital users but must absorb GDPR compliance costs and navigate linguistic adaptations.

Lithuania E-commerce Industry Leaders

UAB Pigu (Pigu.lt)

Kesko Senukai Digital UAB (Senukai.lt)

UAB Varle (Varle.lt)

UAB Barbora (Barbora.lt)

Vinted UAB (Vinted)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Pigu undergoes restructuring as founder Dainius Liulys returns to steer operational turnaround and restore customer trust.

- December 2024: Lithuanian Post reports 12 million parcel deliveries, a 20% rise, plus 600,000 cross-border parcels to the Baltics, highlighting locker-network scale-up.

- December 2024: Lithuanian tech start-ups secure EUR 1.98 billion (USD 2.2 billion) aggregate funding across 309 deals since 2007, with e-commerce and fintech dominant.

- September 2024: Lithuanian Post wins Service Provider of the Year for its reusable locker-packaging pilot used by 10,000 customers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Lithuanian e-commerce market as the total gross merchandise value generated when buyers in Lithuania place orders for goods or fee-based services through internet-connected sites or mobile apps, whether those orders are fulfilled domestically or cross-border. Transactions span B2C, B2B, and C2C storefronts, and values are reported in USD at consumer checkout.

Scope exclusion: In-store card payments, online advertising spend, and purely digital content subscriptions are kept outside this scope.

Segmentation Overview

- By Business Model

- B2C

- B2B

- C2C

- By Device Type

- Smartphone / Mobile

- Desktop and Laptop

- Other Device Types

- By Payment Method

- Credit / Debit Cards

- Digital Wallets

- BNPL

- Other Payment Method

- By B2C Product Category

- Beauty and Personal Care

- Consumer Electronics

- Fashion and Apparel

- Food and Beverages

- Furniture and Home

- Toys, DIY and Media

- Other Product Categories

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts then held structured calls with executives from large marketplaces, SME web-store owners, parcel locker operators, and fintech gateways across Vilnius, Kaunas, and Klaipėda. Their insights on average ticket values, return rates, and holiday seasonality helped us tighten assumptions that secondary data alone could not resolve.

Desk Research

We began with Statistics Lithuania retail turnover series, Eurostat ICT usage surveys, Bank of Lithuania payment dashboards, and parcel-volume releases from Lietuvos Paštas. Trade publications such as Ecommerce Europe country notes and academic papers on Baltic digital adoption offered additional context. Company filings sourced through D&B Hoovers and news archives on Dow Jones Factiva supplied revenue clues for leading platforms. These publicly available inputs, while not exhaustive, built the factual spine of our model.

Market-Sizing & Forecasting

A top-down reconstruction converts national retail sales into an online pool using shopper penetration, mobile share, and average order value, which are then validated through sampled bottom-up roll-ups of leading platform GMV and courier parcel counts. Key variables like broadband penetration, smartphone usage, digital wallet adoption, inflation-adjusted consumer spending, and parcel throughput drive the multivariate regression plus ARIMA overlay that projects demand through 2030. Where platform level data were partial, gaps were bridged by respondent-confirmed load factors and conservative ASP proxies.

Data Validation & Update Cycle

Outputs pass a three-step check: intra-model consistency tests, variance benchmarking against independent indicators, and senior analyst review. Reports refresh annually, with interim updates triggered by material regulatory or macro events, ensuring clients always receive the latest view.

Why Mordor's Lithuania E-Commerce Baseline Earns Trust

Published estimates often diverge because studies slice the market differently, apply unlike inflation adjustments, or refresh at varied cadences.

Key gap drivers include: some studies confine scope to retail goods alone, others ignore C2C flows or mobile-app spending, and a few freeze exchange rates at survey year averages. Mordor's disciplined inclusion criteria, rolling currency conversions, and annual refresh help us present a dependable baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.18 B (2025) | Mordor Intelligence | - |

| USD 2.89 B (2024) | Global Consultancy A | Retail-only scope; excludes services and C2C GMV |

| USD 1.06 B (2024) | Industry Database B | Counts card-settled domestic sales; omits mobile app and B2B orders |

The comparison shows that when scope is narrowed or payment channels are missed, totals swing widely. By capturing every transaction pathway and validating each assumption in dialogue with market participants, Mordor delivers a balanced, transparent baseline that decision-makers can trace and replicate.

Key Questions Answered in the Report

What is the current size of the Lithuania e-commerce market?

The market stands at USD 3.66 billion in 2026 and is forecast to reach USD 7.44 billion by 2031.

Which business model is growing fastest in Lithuania’s online retail space?

Consumer-to-consumer platforms are expanding at an 18.35% CAGR, outpacing traditional B2C channels.

How dominant is mobile commerce in Lithuania?

Mobile devices captured 62.55% of transactions in 2025 and will maintain double-digit growth through 2031.

What payment method is gaining the most traction?

Digital wallets, growing at 20.98% CAGR, are rapidly displacing credit and debit cards.

Which product category is expanding fastest?

Online food and beverage sales are rising at a 17.05% CAGR due to improved cold-chain logistics and consumer demand for convenience.

How strict is data-privacy enforcement in Lithuanian e-commerce?

The State Data Protection Inspectorate’s EUR 2.38 million (USD 2.74 million) fine on Vinted highlights heightened GDPR oversight and the need for robust compliance frameworks.

Page last updated on: