Graphite Electrode Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

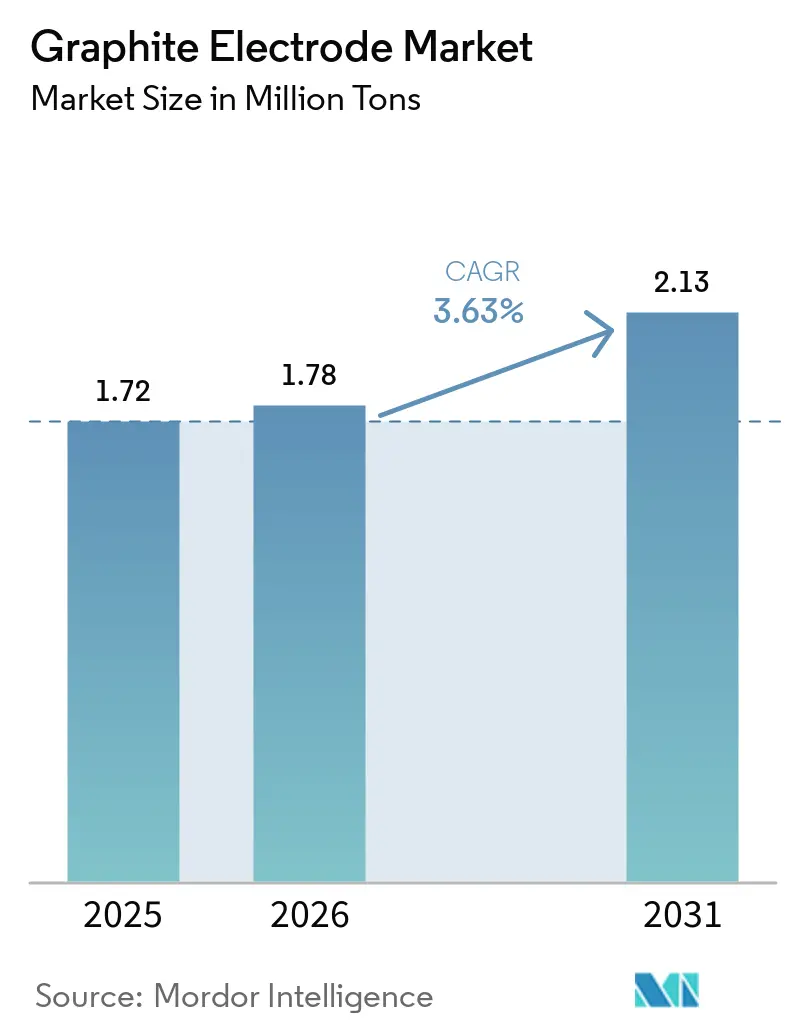

| Market Volume (2026) | 1.78 Million tons |

| Market Volume (2031) | 2.13 Million tons |

| Growth Rate (2026 - 2031) | 3.63% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Graphite Electrode Market Analysis by Mordor Intelligence

The Graphite Electrode Market size is projected to expand from 1.72 million tons in 2025 and 1.78 million tons in 2026 to 2.13 million tons by 2031, registering a CAGR of 3.63% between 2026 to 2031. Several structural changes are driving this consistent volume growth. Electric-arc-furnace (EAF) steelmakers are transitioning from traditional blast-furnace methods. Each EAF heat now incorporates larger-diameter ultra-high-power (UHP) columns, which help manage increased arc currents and enhance electrode intensity per ton of liquid steel. China's energy-quota policies are restricting domestic graphitization, leading mills in India, Vietnam, and Malaysia to import unfinished blanks from Chinese plants, complete the finishing locally, and supply them to regional EAF operators. In Europe, producers with low-carbon footprints are benefiting from price premiums due to the Carbon Border Adjustment Mechanism (CBAM), which requires embedded-emissions data for procurement.

Key Report Takeaways

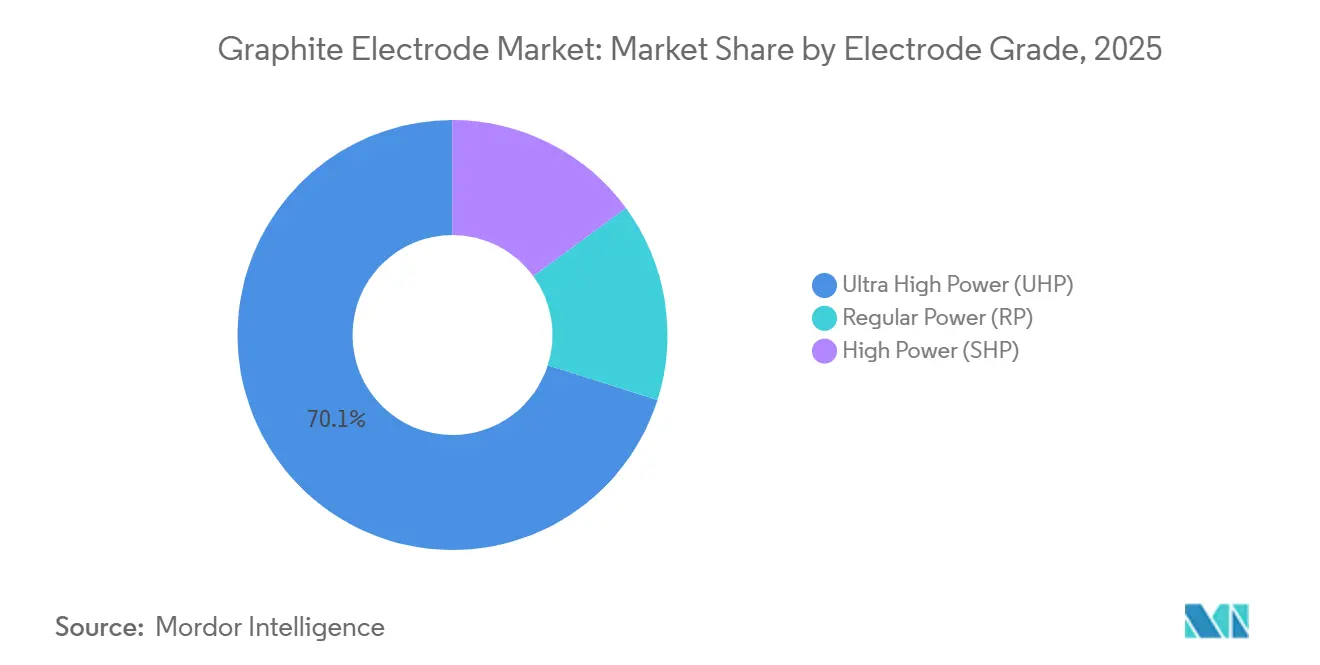

- By electrode grade, UHP products commanded 70.11% of the graphite electrode market share in 2025 and are forecast to expand at a 4.12% CAGR through 2031.

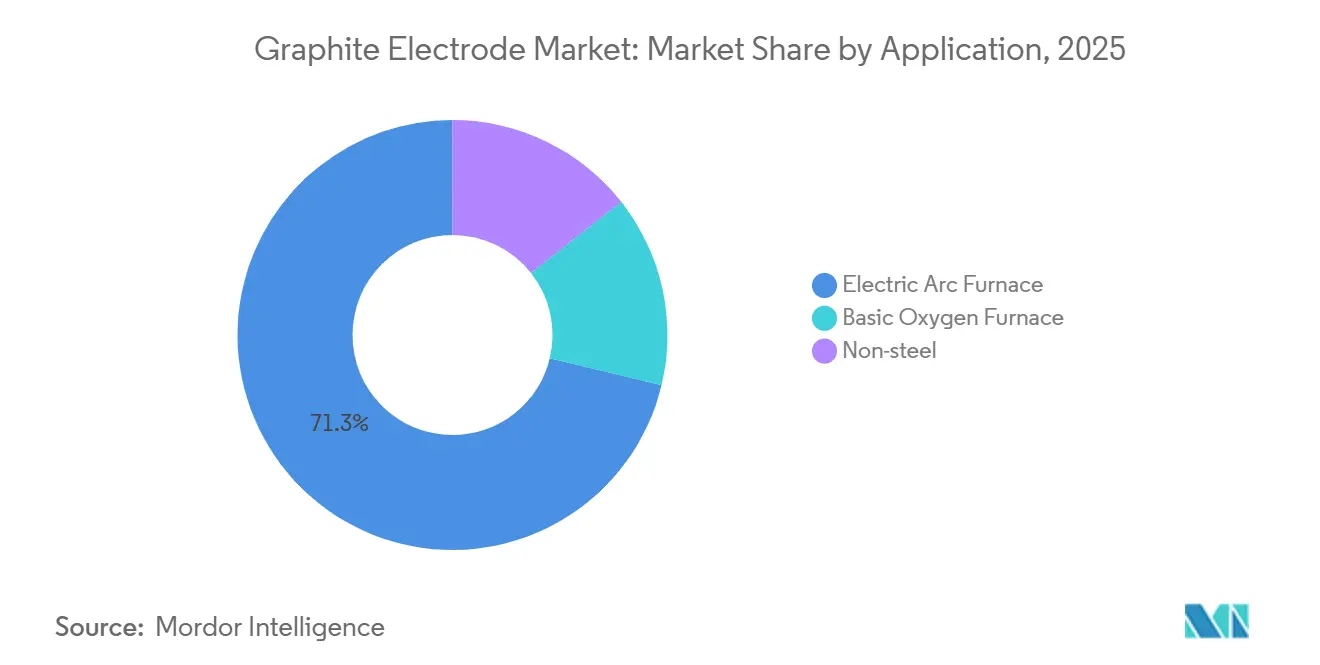

- By application, EAF steelmaking accounted for 71.25% of the graphite electrode market size in 2025 and is projected to grow at a 4.41% CAGR to 2031.

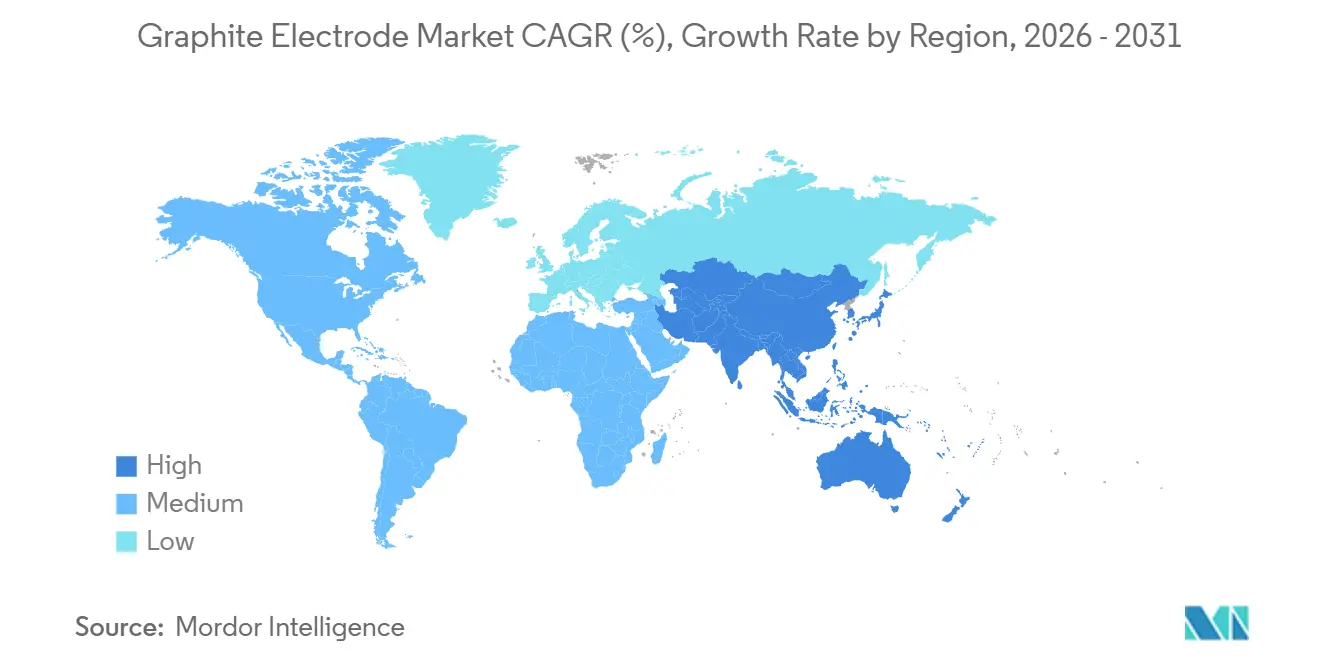

- By geography, Asia-Pacific held 60.34% of global demand in 2025 and is expected to increase at a 4.74% annual pace through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Graphite Electrode Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|---|

| Rising global steel-scrap availability | +0.90% | Global, with concentration in North America, Europe, and East Asia | Medium term (2-4 years) | |

| Accelerating demand for ultra-high-power (UHP) electrodes | +1.20% | Global, led by Asia-Pacific and Middle-East EAF expansions | Long term (≥ 4 years) | |

| Hydrogen DRI-EAF hybrids requiring larger-diameter electrodes | +0.60% | Europe, Middle-East, and select North American projects | Long term (≥ 4 years) | |

| Carbon-neutral silicon-metal smelters expanding UHP demand | +0.40% | Asia-Pacific (China, India, Malaysia) and North America | Medium term (2-4 years) | |

| Premium low-CO₂-footprint electrode traceability mandates | +0.50% | Europe (CBAM compliance), North America, with spillover to Asia-Pacific exporters | Short term (≤ 2 years) | |

| Source: Mordor Intelligence | ||||

Rising Global Steel-Scrap Availability

In North America and Europe, the retirement of end-of-life vehicles, coupled with China's demolition of outdated infrastructure, is driving a surge in steel-scrap generation. The global ferrous scrap supply has increased significantly in recent years[1]OECD Steel Committee, “Steel Market Developments Q4 2024,” oecd.org . However, the quality of scrap varies; obsolete scrap tends to have higher copper and tin contamination compared to prompt industrial scrap. As a result, Electric Arc Furnace (EAF) shops are increasingly mixing in direct-reduced iron (DRI) to achieve the desired automotive-grade chemistries. This practice not only extends melting times but also elevates amperage and increases electrode consumption per heat. Therefore, while the supply of scrap has risen annually, the intensity of electrode use has grown at a faster pace. Producers who can ensure a consistent current-carrying capacity stand to gain significantly from the ongoing scrap super-cycle.

Accelerating Demand for Ultra-High-Power Electrodes

UHP electrodes, with a bulk density greater than 1.68 g/cm³ and a resistivity less than 5.5 µΩ·m, are overtaking traditional high-power grades. Jiangsu Shagang launched a 6-million-ton EAF complex in 2024, exclusively utilizing 700-mm UHP columns to achieve significant tap weights. While UHP products are more expensive than their high-power counterparts, they offer an extended service life and reduced power consumption. This results in a decrease in total electrode costs per ton of steel, particularly when furnace utilization is high. Mid-tier producers, lacking access to premium needle coke, are witnessing a decline in market share. In response, several Chinese mills are shutting down high-power extrusion lines, reallocating funds to UHP machining centers. With an increasing number of furnaces transitioning to 150 MVA-plus transformers, the dominance of UHP in the graphite electrode market is expected to expand further.

Hydrogen DRI-EAF Hybrids Requiring Larger-Diameter Electrodes

Commercial trials of hydrogen-based Direct Reduced Iron (DRI) have progressed from pilot stages to demonstration scales. By 2024, ArcelorMittal’s Hamburg facility upgraded from 600-mm to 650-mm Ultra High Power (UHP) columns, starting to charge a hydrogen DRI[2]ArcelorMittal, “Hamburg Works Hydrogen-DRI Project Update,” arcelormittal.com . This shift was necessitated, as lower-density iron pellets demand a higher current to achieve the desired tap temperature. The HYBRIT consortium achieved an electrode intensity during heats using hydrogen DRI, which was higher than operations relying solely on scrap in Electric Arc Furnaces (EAF). Capitalizing on affordable solar electricity, Middle-Eastern steelmakers have preemptively chosen 700-mm electrodes for Qatar Steel's 1.5-million-ton line, set to commence in 2028. As a result, the demand landscape is splitting, traditional scrap-based EAFs are sticking with 500-mm-600-mm sets, whereas hydrogen hybrids are rapidly expanding into a 650-mm-800-mm segment, a niche currently catered to by only a select few suppliers.

Premium Low-CO₂-Footprint Electrode Traceability Mandates

In 2023, Europe introduced its Carbon Border Adjustment Mechanism (CBAM), requiring importers to purchase certificates that account for the emissions tied to every electrode entering the continent. The Acheson graphitization process, which typically uses 2,000 kWh per ton, emits over 2 tons of CO₂ equivalent for each ton of finished electrode, especially when powered by a coal-dominant grid. Producers who can document emissions below 1.5 tons of CO₂ equivalent are enjoying price premiums. SGL Carbon and GrafTech reported that contracts for these low-carbon premium batches constituted a substantial share of their sales in Europe. As steel and battery clients tighten their Scope 3 targets, the once-niche demand for traceable low-carbon electrodes has evolved into a standard procurement practice.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|---|

| Cyclicality of global steel production | -0.80% | Global, particularly acute in China and Europe | Short term (≤ 2 years) | |

| Emerging amorphous-graphite composite electrodes (substitution) | -0.30% | Experimental applications in Asia-Pacific and North America; limited commercial deployment | Long term (≥ 4 years) | |

| Emission-quota caps on graphitization capacity expansion | -0.50% | China (primary), with spillover to India and Southeast Asia | Medium term (2-4 years) | |

| Source: Mordor Intelligence | ||||

Cyclicality of Global Steel Production

In early 2025, global crude steel production saw a year-on-year decline, prominently driven by a downturn in China. This fluctuation was intensified by the demand for electrodes, as operators of Electric Arc Furnaces (EAF) opted to postpone restocking when their utilization dipped below a specific threshold. From Q4 2024 to Q1 2025, GrafTech noted a sequential dip in its average selling price, a change linked to mills shifting from term contracts to spot purchases. Historical trends show that a downturn in EAF steel output often results in a marked drop in electrode shipments, mainly because mills prioritize depleting their existing inventory. Moreover, the recovery is not instantaneous; buyers cautiously rebuild their stocks, leading to longer lead times and diminished capacity-planning clarity for manufacturers. Given the ongoing instability in global steel demand, this adverse operating leverage is poised to persistently burden the graphite electrode market during the forecast period of 2026–2031.

Emission-Quota Caps on Graphitization Capacity Expansion

China's dual-control policy, aimed at curbing both total energy consumption and energy intensity, has effectively put a stop to the establishment of new graphitization furnaces in Shandong, Hebei, and Inner Mongolia. These regions were once pivotal to the nation's capacity. After failing to secure an energy quota, Fangda Carbon scrapped its Shandong project, redirecting its investment to Gansu, where renewable power credits are more readily available. Current quota holders are running at full throttle, exporting semi-finished blanks to India and Vietnam for final processing. In contrast, new entrants face significant delays. India's HEG has clinched approvals for a graphitization line poised to process these blanks, underscoring the ripple effects of Chinese policy on regional supply chains. This bottleneck has stunted global capacity growth, even as demand for larger-diameter electrodes surges, tightening supplies during peak quarters and potentially driving up prices for buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Electrode Grade: UHP Dominance Reflects Furnace-Power Escalation

UHP electrodes captured 70.11% of global volume in 2025, and their share of the graphite electrode market size is projected to rise further on a 4.12% CAGR to 2031. Operators of furnaces exceeding 150 MVA favor UHP columns due to their finer grain structures and reduced thermal-expansion coefficients, which minimize breakage incidents. Data from Jilin Carbon indicates that in 2025, UHP consumption was lower per ton of EAF steel compared to high-power grades, resulting in a notable lifetime-cost advantage. High-power electrodes have seen their market share decline, now primarily used for ladle-furnace refining or furnaces with smaller tap weights. In contrast, regular-power grades are predominantly utilized in yellow-phosphorus and calcium carbide smelting, where cost considerations overshadow performance. Supply-side investments further bolster UHP adoption. In 2025, Liaoning Dantan invested significantly in a 700-mm UHP machining center, responding to UHP inquiries that constituted a large portion of its backlog. In India, similar shifts are evident, with HEG dedicating its new line's entire incremental capacity to 600-mm and 700-mm products. Producers reliant on legacy high-power tooling risk stranded assets unless they adapt extrusion presses for larger billets. With the rise of hydrogen-DRI hybrids, the demand for diameters exceeding 650 mm is expected to solidify UHP's dominance, potentially relegating the combined share of high-power and regular-power electrodes to a smaller portion of the graphite electrode market by 2031.

By Application: EAF Steel Anchors Growth, Non-Steel Niches Emerge

EAF steelmaking commanded 71.25% of the graphite electrode market share in 2025 and is set to grow at a 4.41% CAGR through 2031, sustained by China’s blast-furnace retirements and North America’s automotive supply-chain localization. Basic oxygen furnace (BOF) users, accounting for a small portion of the demand, utilize electrodes primarily for bottom stirring and ladle refining at low intensities. This limited usage restricts their growth potential. Meanwhile, the non-steel sector - which includes silicon-metal, ferroalloy, yellow-phosphorus, and calcium-carbide - has been expanding as photovoltaic-grade silicon smelters transition to using UHP electrodes with minimal ash content.

Multi-year sourcing models highlight distinctions between segments. U.S. EAF frontrunners secure volumes through long-term offtake agreements, with prices adjusting quarterly based on needle-coke indices. This strategy provides a buffer for producers during demand downturns, yet limits their ability to pass on costs when feedstock prices surge. In the diverse non-steel sector, price sensitivity remains high; for instance, Chinese calcium-carbide producers often shift suppliers for small discounts, squeezing profit margins. Looking ahead, EAF's dominance is expected to persist. Its consistent electrode intensity and stable contracting account for a significant portion of global tonnage. In contrast, while non-steel segments present cyclical opportunities, especially with the growth in solar-grade silicon, they remain more volatile.

Geography Analysis

Asia-Pacific accounted for 60.34% of global consumption in 2025 and is poised to expand at 4.74% annually through 2031, yet growth is uneven. In the first half of 2025, Chinese output experienced a notable contraction. This was largely due to provincial governments imposing operating-hour restrictions on graphitization furnaces. As a result, producers pivoted to exporting semi-finished blanks rather than their usual finished columns. Meanwhile, India capitalized on this gap. HEG, targeting buyers in the Middle-East and Southeast Asia who previously depended on Chinese supplies, is set to upgrade its capacity by 2027. In a strategic move, Japan's Tokai Carbon bolstered its presence in North America by acquiring two U.S. machining shops. This acquisition has notably reduced delivery lead times for clients. Additionally, Vietnam and Malaysia, taking advantage of reduced electricity tariffs, approved three finishing plants in 2025. These plants will process Chinese blanks, achieving lower landed costs, further diversifying regional trade dynamics.

In 2025, North America accounted for a notable portion of global demand and is on a growth trajectory. Nucor and Steel Dynamics announced new EAF capacity. This move is set to bolster electrode offtake, secured through multi-year contracts that benefit local machining hubs. GrafTech's Ohio facility, the sole integrated plant in the region, catered to most of its 2025 shipments domestically. This underscores the regional buyers' preference for resilient and traceable supply chains. In a strategic partnership, Canada’s Algoma Steel, which transitioned to EAF in 2024, signed a long-term deal to procure UHP columns from Tokai Carbon’s Pennsylvania facility. This ensures a steady supply of electrodes for Algoma's upcoming hydrogen-DRI trials. Meanwhile, Mexico stands out as a growth hotspot, with Ternium and ArcelorMittal boosting their EAF lines to cater to the auto-steel demand driven by USMCA.

Europe, accounting for a significant portion of global consumption in 2025, is witnessing steady growth, largely influenced by the Carbon Border Adjustment Mechanism (CBAM). Under CBAM, importers are mandated to present certificates corresponding to embedded carbon. This regulation imposes additional costs on shipments that lack the ISO 14067 carbon footprint certification. Capitalizing on its eco-friendly products, SGL Carbon, with a low carbon footprint, secured contracts at a premium over Asian competitors. Despite Turkey relying on imports for most of its electrodes, the rising CBAM costs are spurring domestic investments. A testament to this shift is the production line inaugurated by Karabük Demir Çelik in 2025. Meanwhile, Russia's market faces distortions due to sanctions limiting needle coke imports. While Chinese exports surged month-on-month in January 2025, ongoing logistical challenges have tempered this growth.

Competitive Landscape

The global graphite electrode market is moderately consolidated, but oversupply and numerous mid-tier Chinese firms have weakened pricing power. Industry leaders are differentiating through backward integration into calcined needle coke, regulatory arbitrage with semi-finished blanks, and carbon-footprint certification. For instance, Fangda Carbon's Gansu facility (operational since 2024) reduced feedstock costs, while Indian firms leverage lower power costs to re-export finished electrodes. SGL Carbon and GrafTech have tapped into European CBAM premiums with sub-1.5 tons CO₂ e certifications.

Technological advancements highlight a divide. Major producers use automation and infrared detection to cut scrap rates, while smaller Chinese mills face higher breakage costs due to manual processes. The industry is shifting to larger diameters (700 mm and above) and oxidation-resistant coatings for hydrogen-DRI furnaces. HEG and Graphite India, following Graphite India's 2025 equity stake in GrafTech, have jointly filed patents. Fewer than six players possess captive needle-coke, large-diameter machining, and ISO-certified low-carbon credentials, positioning them as market leaders.

Geographic shifts add complexity to supply chains. Resonac closed its Omuta plant in Japan in late 2025, moving production to a cost-efficient Malaysian joint venture. In Vietnam, three finishing plants set to launch in 2025 will expand machining capacity but exclude graphitization, reinforcing the semi-finished-blank trade. Shanghai Jiazhihua's Sichuan project will introduce UHP capabilities for 650 mm and above diameters, targeting hydrogen-DRI EAFs. Technically advanced, carbon-certified suppliers are gaining an edge as the steel industry focuses on decarbonization.

Graphite Electrode Industry Leaders

Fangda Carbon New Material Technology Co. Ltd

GrafTech International

HEG Limited

Resonac Holdings Corporation

Tokai Carbon Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Graphite India Limited has announced plans to expand the capacity of its Graphite Electrodes Division by 25,000 TPA, increasing the total capacity from 80,000 TPA to 105,000 TPA. This INR 600 crore expansion will be executed in two phases over a period of 36 months.

- August 2025: HEG Limited is enhancing its production capabilities with plans to increase its graphite electrode and related products capacity by 15,000 tonnes per annum (TPA). This strategic initiative aims to capitalize on a structural industry shift that is driving higher demand for electrodes.

Global Graphite Electrode Market Report Scope

Graphite electrodes are used to transfer electrical energy from the power supply to the steel melt in the EAF bath. They are normally manufactured using quality petroleum needle coke, coal tar pitch, and some additives.

The graphite electrodes market is segmented by electrode grade, application, and geography. By electrode grade, the market is segmented into ultra-high power (UHP), high power (SHP), and regular power (RP). By application, the market is segmented into electric arc furnaces, basic oxygen furnaces, and non-steel applications. The report also covers the market size and forecasts for 27 countries across major regions. For each segment, market sizing and forecasts have been done on the basis of volume (tons) and revenue (USD).

| Ultra High Power (UHP) |

| High Power (SHP) |

| Regular Power (RP) |

| Electric Arc Furnace |

| Basic Oxygen Furnace |

| Non-steel |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Russia | |

| Spain | |

| Turkey | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| Qatar | |

| United Arab Emirates | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Electrode Grade | Ultra High Power (UHP) | |

| High Power (SHP) | ||

| Regular Power (RP) | ||

| By Application | Electric Arc Furnace | |

| Basic Oxygen Furnace | ||

| Non-steel | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Russia | ||

| Spain | ||

| Turkey | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| Qatar | ||

| United Arab Emirates | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What volume growth is expected for the graphite electrode market by 2031?

The global graphite electrode market size stands at 1.78 million tons in 2026, and it is projected to reach 2.13 million tons by 2031 at a 3.63% CAGR.

Why are ultra-high-power electrodes gaining share?

UHP grades survive higher currents in modern EAFs, cut power use by about 18%, and last 25% longer than high-power alternatives, lowering total cost per ton of steel.

How is CBAM influencing electrode procurement in Europe?

Importers must buy carbon certificates, so mills increasingly pay 15%-20% premiums for ISO-14067-certified low-carbon electrodes to avoid surcharges.

Which regions will drive new capacity additions?

Asia-Pacific remains dominant, but India, Vietnam, and Malaysia are adding finishing lines, while North America is expanding demand via new EAF steel plants.

What feedstock risks face electrode producers?

Needle-coke price spikes, tied to delayed-coker refinery economics, can raise production costs by more than 20%, favoring producers with captive calcination assets.

How will hydrogen-based DRI affect electrode specifications?

Hydrogen-DRI hybrids need 650-mm–800-mm UHP columns and consume up to 2.1 kg of electrodes per steel ton, about one-third higher than scrap-only EAFs.

Page last updated on: