Polypropylene Fibers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

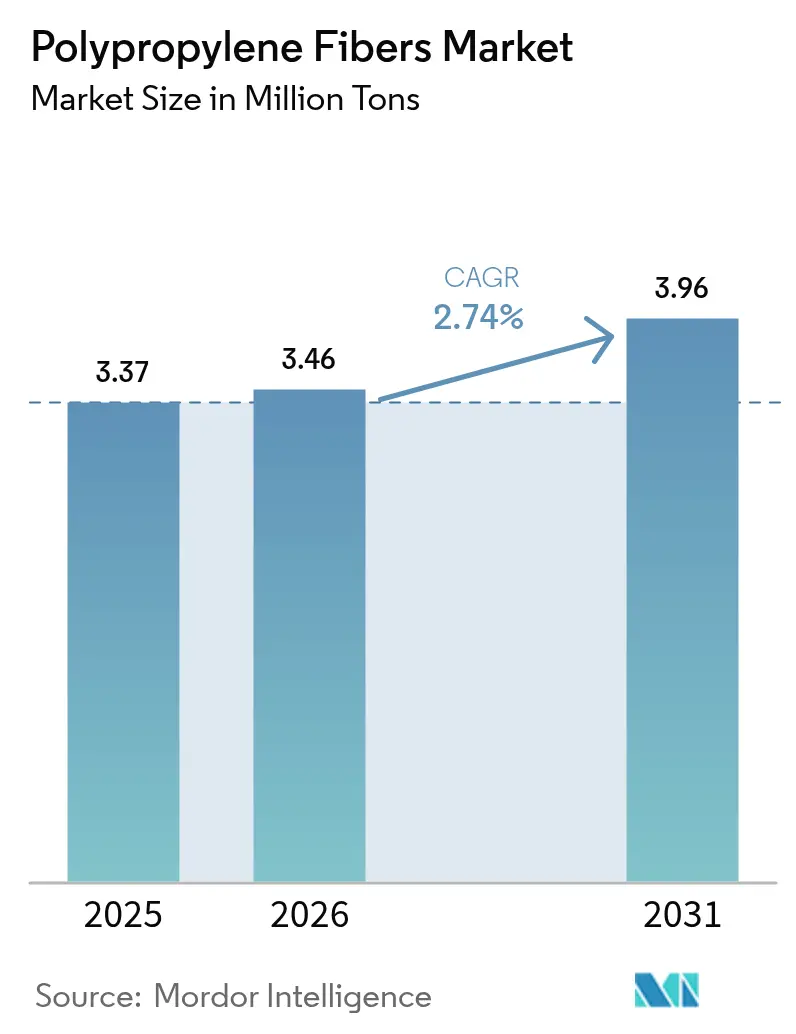

| Market Volume (2026) | 3.46 Million tons |

| Market Volume (2031) | 3.96 Million tons |

| Growth Rate (2026 - 2031) | 2.74% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polypropylene Fibers Market Analysis by Mordor Intelligence

The Polypropylene Fibers Market size is projected to be 3.37 Million tons in 2025, 3.46 Million tons in 2026, and reach 3.96 Million tons by 2031, growing at a CAGR of 2.74% from 2026 to 2031. Infrastructure agencies are replacing welded-wire mesh with macro-synthetic reinforcement, trimming rebar costs and accelerating pour cycles, while electric-vehicle (EV) assemblers specify recycled polypropylene (PP) compounds to shed 15-20 kg per car and add 8-12 km of range. Continuous-filament extrusion keeps yarn configurations at 84.51% of 2025 volume because the process synchronizes with 400-600 m/min textile and spunbond lines. Healthcare and hygiene converters lead end-user growth as hospitals worldwide adopt melt-blown nonwovens that repel fluids and block 98% of 0.5-micron aerosols. Asia-Pacific commands 51.12% of 2025 tonnage and expands at 3.37% CAGR thanks to China’s Belt and Road geotextile deployments and India’s USD 1.4 trillion National Infrastructure Pipeline that mandates synthetic erosion control fabrics.

Key Report Takeaways

- By type, yarn captured 84.51% of the polypropylene fibers market share in 2025 and is projected to advance at a CAGR of 2.78% through 2031.

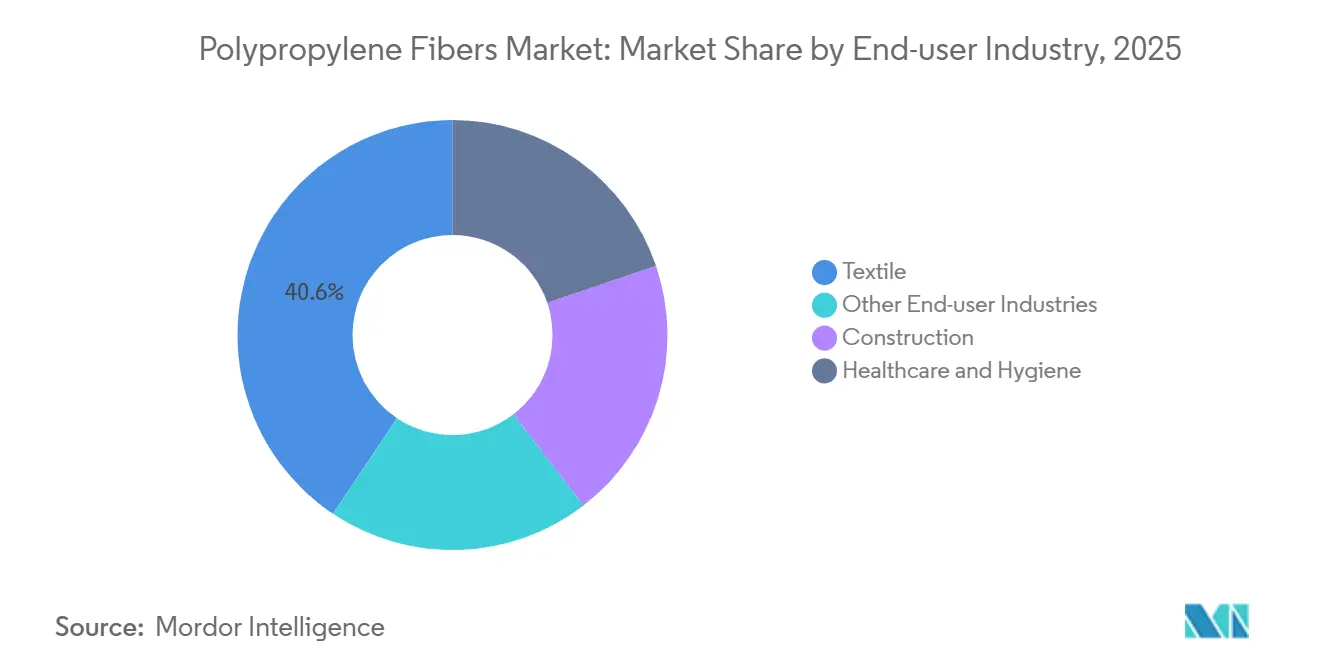

- By end-user industry, textiles captured 40.62% of the polypropylene fibers market share in 2025, while healthcare and hygiene is advancing at a 3.22% CAGR through 2031.

- By geography, Asia-Pacific led with 51.12% of the polypropylene fibers market share in 2025 and remains the fastest-growing region at 3.37% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polypropylene Fibers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure shift toward macro-synthetic concrete reinforcement | +0.8% | Global, with early gains in India, Indonesia, Brazil | Medium term (2-4 years) |

| Accelerating geotextile penetration in road and coastal engineering | +0.6% | APAC core, spill-over to Middle-East and Africa | Medium term (2-4 years) |

| Lightweight automotive interior adoption (EV range extension) | +0.5% | North America, Europe, China | Short term (≤ 2 years) |

| 3-D printing of PP-fiber reinforced composites (mass-customization) | +0.3% | North America, Germany, Japan | Long term (≥ 4 years) |

| Circular-grade recycled PP fibers enabled by chemical recycling | +0.4% | Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Infrastructure Shift Toward Macro-Synthetic Concrete Reinforcement

Transport ministries in India, Indonesia, and Brazil now allow 3-6 kg/m³ polypropylene macro-fibers to replace welded-wire mesh, cutting rebar by 20-35% and slashing corrosion-related repairs. India’s clause 509 specifications alone create 42,000 tons of captive demand by 2028. São Paulo field trials show 60% crack-width reduction after 90 freeze-thaw cycles, unlocking federal resurfacing funds. Contractors value single-pour placement that trims labor by almost one-quarter in congested urban corridors.

Accelerating Geotextile Penetration in Road and Coastal Engineering

Monsoon-sensitive soils across Southeast Asia settle 15-20 cm within two years without separation layers, so Vietnam’s USD 15 billion North-South Expressway specifies 200 g/m² needle-punched PP nonwovens, consuming 9,200 tons through 2027. Indonesian and Filipino municipalities install geotextile tubes that require 18-22 tons per shoreline kilometre, financed by an Asian Development Bank USD 340 million loan package. Laboratory tests confirm 85% flow retention after 10,000 hours in aggressive leachate, meeting EU landfill rules. The resulting infrastructure pull lifts regional demand. Government tender rules that score life-cycle cost now favor geotextiles because they halve maintenance dredging over a road’s service life, reinforcing adoption momentum.

Lightweight Automotive Interior Adoption (EV Range Extension)

Electric-vehicle platforms gain roughly 1.5-2.0 km of range for every 10 kg trimmed, so automakers target interior mass after battery optimization. Glass-fiber-reinforced PP compounds captured 38% of instrument-panel substrates in 2025 model launches, replacing ABS grades that weigh up to 2.2 kg more per vehicle and demand higher molding pressures. Stellantis reported that switching door panels and seat backs in the Peugeot e-3008 to 30% long-fiber PP composites saved 18 kg per car, extended range 14 km, and shaved EUR 22 off the bill of materials. EU rules effective 2027 impose EUR 95 per g/km CO₂ exceedance, so each kilogram of weight reduction is worth about EUR 6 in avoided penalties across a model’s compliance life.

Circular-Grade Recycled PP Fibers Enabled by Chemical Recycling

BASF and LyondellBasell commissioned pilot pyrolysis units that crack mixed-plastic waste into naphtha, yielding propylene identical to virgin monomer and allowing fiber spinners to market circular-grade yarn with 30-50% recycled content at no tensile-strength penalty. Indorama Ventures signed a five-year offtake deal for 18,000 tons per year of pyrolysis-derived PP from Plastic Energy’s Seville plant to supply apparel brands pledging 25% recycled synthetics by 2028. Although circular resin costs 28-35% more than prime, EU Packaging rules mandate 30% recycled content by 2030, narrowing the price gap as capacity scales from 120,000 tons in 2025 to 850,000 tons by 2031. Mass-balance certification lets converters claim recycled content without segregating supply chains, simplifying brand adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low melting-point limits in high-temperature uses | -0.5% | Global, acute in automotive under-hood and industrial filtration | Short term (≤ 2 years) |

| ESG scrutiny on micro-plastics leakage from non-woven disposables | -0.3% | Europe, North America | Medium term (2-4 years) |

| Ultrafine PP dust flagged in occupational-health regulations | -0.2% | Global, stringent enforcement in EU and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Low Melting-Point Limits in High-Temperature Uses

Polypropylene melts at 160-165 °C, ruling it out for diesel particulate filters that regenerate at 180-220 °C and for cement-kiln baghouse filters now required to capture 99.5% particulates under the U.S. EPA’s 2025 standards[1]U.S. Environmental Protection Agency, “Portland Cement NSPS 2025,” epa.gov . OEMs therefore choose polyamide, aramid, or PTFE fibers that cost 40-80% more per square meter yet survive higher temperatures, diverting an estimated 14,000 tons of annual demand from PP fibers. Attempts to raise the service ceiling by grafting maleic anhydride or blending HDPE add USD 0.18-0.25 per kilogram and still fail to meet 180 °C thresholds. Continued R&D may improve heat resistance, but commercial impact is unlikely within the next two years.

ESG Scrutiny on Micro-Plastics Leakage from Non-Woven Disposables

Single-use hygiene items shed 4-9 mg of PP microfibers per unit, and wastewater plants detect 1.2-3.8 particles per liter in treated effluent, raising public-health alarms. The European Chemicals Agency’s draft REACH restriction on intentionally added microplastics, published in 2024, forces brand owners to label disposable nonwovens with “releases microplastics,” causing a 6-8% sales dip in premium diapers during 1H 2025. Procter & Gamble and Kimberly-Clark aim to replace 30% of PP spunbond with wood-pulp or lyocell by 2028, but pilot runs show 12-18% higher scrap and new bonding chemistries that raise costs. Wastewater utilities in California and the Netherlands are adding 20-micron tertiary screens at USD 4-7 million per plant and 15-20% energy penalties, slowing global roll-out to fewer than 40 installations as of early 2026.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Continuous-Filament Yarn Outruns Staple

Continuous-filament yarn controlled 84.51% of the 2025 polypropylene fibers market size and is set to expand at a 2.78% CAGR through 2031, supported by 400-600 m/min weaving and spunbond lines that deliver 98% first-pass yield. Staple fiber is used in concrete reinforcement and needle-punched automotive carpets, but it incurs an additional conversion cost of USD 0.12-0.18/kg due to cutting and carding processes. U.S. and Turkish carpet mills migrated to bulked continuous filament because it eliminates carding, slashing labor 30-40% and ensuring just-in-time deliveries within 48 hours.

Staple fibers remain relevant in geotextile and shotcrete applications requiring 50-75 mm fibers. Tunnel constructors typically use 0.9-1.1 kg/m³ of fibers in shotcrete. Additionally, the demand for yarn is rising, particularly in hygiene spunbond and woven geotextiles.

By End-user Industry: Hygiene Converts Drive Volume Upswing

Textile absorbed 40.62% of the 2025 polypropylene fibers market size but will cede share as healthcare and hygiene advance at 3.22% CAGR through 2031, the quickest among end-users. Disposable spunbond-meltblown-spunbond drapes weighing 35-50 g/m² now block 98% of aerosols, prompting hospitals to abandon reusable cotton. Construction is buoyed by macro-synthetic concrete reinforcement and road geotextiles specified in India, Indonesia, and the Middle-East.

In the hygiene segment, diaper and feminine-care manufacturers reported increased consumption, driven by lower penetration rates in sub-Saharan and Southeast Asian regions compared to developed markets. Demand for surgical masks has stabilized but is projected to grow steadily as hospitals implement standardized respiratory protection protocols. Textile applications are facing challenges from polyester competition, with polyester staple prices ranging between USD 1,350-1,450 and offering superior dyeing properties. This has prompted polypropylene fiber producers to focus on cost-sensitive market niches.

Geography Analysis

Asia-Pacific dominates the polypropylene fibers market, holding 51.12% of 2025 volume and growing at a 3.37% CAGR through 2031 on infrastructure megaprojects. China's production was led by Sinopec and PetroChina, supplying domestic converters at prices below import parity. In India, consumption increased following a mandate by the Ministry of Road Transport requiring geotextile layers on all national highways exceeding 10 km. Meanwhile, Japan and South Korea focused on producing ultra-fine electret melt-blown material for N95 respirators, a high-margin niche market with retail prices ranging from USD 3,200 to USD 3,800 per ton.

In North America, the U.S. Bipartisan Infrastructure Law is expected to generate additional demand for polypropylene (PP) macro-fiber across multiple states[2]U.S. Department of Transportation, “Bipartisan Infrastructure Law,” transportation.gov . In Canada, Ontario’s electric vehicle (EV) assembly lines have seen increased utilization of glass-fiber-reinforced PP compounds for interior modules. Meanwhile, Mexico’s maquiladoras imported yarn under USMCA regulations, which allow duty-free re-export when a significant portion of the value originates within North America.

Europe's demand is influenced by Extended Producer Responsibility fees that are impacting hygiene product margins. Germany, the regional leader, has seen reusable diaper lines capture a growing share of the retail market. France and Italy collectively consumed PP for applications such as Alpine road-stabilization geotextiles and carpet backing, driven by a rebound in housing construction.

South America and the Middle-East and Africa each account for a smaller portion of global market volume. In South America, Brazil’s highway upgrades are expected to require separation fabrics. In the Middle-East, Saudi Arabia’s NEOM and Qiddiya projects are projected to demand woven PP for desert stabilization. In South Africa, spinners imported PP resin for carpet yarn and baler twine, marking a notable increase compared to the previous year.

Regulatory Landscape

Regulation affecting polypropylene (PP) fibers is tightening around microplastics release, product labeling, and chemical-management duties for polymer-based supply chains. In the European Union, Regulation (EU) 2026/1168 (published June 2, 2026) adjusted elements of the REACH microplastics restriction framework, including specific exemptions such as R&D quantities (up to 1 ton per year) and medicinal products used in clinical trials. These changes shape how fiber and nonwoven developers document uses and qualify exemptions.

In the United States, air-emissions compliance requirements for upstream polymer-related manufacturing continue to evolve. The US Environmental Protection Agency finalized amendments to the NESHAP for Polyether Polyols Production on March 18, 2026, revising criteria tied to storage capacity thresholds. The update reinforces a broader trend toward more granular control of emission points, including storage vessels and process vents, which can increase compliance attention across chemically intensive materials value chains supporting fiber production.

Value Chain Analysis

The polypropylene fibers value chain starts upstream with hydrocarbon feedstocks (naphtha or natural gas liquids) converted to propylene and polymerized into PP resin, then compounded with additives such as stabilizers and color masterbatches. Midstream, resin is melt-spun into filaments and then drawn and heat-set to target tenacity and shrinkage, feeding either continuous-filament yarn routes (dominant for high-speed woven and spunbond lines) or staple-fiber routes (cutting and carding for applications such as concrete reinforcement and needle-punched products). Quality sensitivity to resin melt-flow consistency and energy intensity at extrusion and drawing stages creates a structural advantage for integrated resin-to-fiber producers versus toll spinners when feedstock or power costs swing.

Downstream conversion includes nonwovens (spunbond and meltblown), geotextiles, ropes, carpet backing, and macro- and micro synthetic fibers for construction, sold through direct OEM supply, converters, and distributors. Standards and qualification act as gating nodes: BISFA guides fiber classification and test practices, and ISO 1346:2021 specifies polypropylene fiber rope requirements. Construction applications often require approval and performance validation, commonly aligned with ASTM/ICC acceptance criteria for fiber-reinforced concrete. Certification, documentation (including EPD-type disclosures in some buyer programs), and application engineering increasingly differentiate suppliers beyond commodity pricing, particularly for infrastructure and automotive programs that require traceable performance.

Competitive Landscape

The polypropylene fibers market remains moderately fragmented: the top five suppliers hold less than 40% combined share, sustaining price competition that caps commodity-grade EBITDA margins below 10%. Integrated resin-to-fiber producers, Indorama Ventures, Mitsubishi Chemical, and China National Petroleum, enjoy USD 80-120 per-ton feedstock advantages yet struggle to widen spreads because regional tollers in Southeast Asia accept 6-8% returns to keep lines full. Radici Partecipazioni’s 2024 investment in a Lombardy recycling consortium secures post-consumer flake for carpet yarns with certified circular content.

Technology is a key differentiator. BASF and Sika market pre-blended macro-fiber concrete packages that automate dosing and command 12-15% price premiums. Beaulieu Fibres partners with Eastman to validate methanolysis-derived propylene, pursuing apparel brands that demand third-party recycled-content certificates. Disruptive chemical recyclers Plastic Energy and Agilyx supply pyrolysis oils that give fiber makers circular claims without mechanical-recycling strength loss, but their joint capacity of 95,000 tons in 2025 equals less than 3% of resin demand.

Product development funnels toward higher-value niches. Toray and Kuraray commercialize ultra-fine melt-blown under 2 microns for HEPA-grade filters, while continuous-fiber-reinforced PP tapes emerge in aerospace interiors where 40% weight savings cut fuel burn 0.3% on narrow-body jets. Price sensitivity persists: Southeast Asian tollers undercut majors by 12-18% on spot contracts, forcing integrated players to emphasize sustainability and tailored formulations over cost leadership.

Polypropylene Fibers Industry Leaders

Freudenberg Group

DuPont

Radici Partecipazioni SpA

Indorama Ventures Public Company Limited

Beaulieu Fibres International NV

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Capacity additions and product upgrades are increasingly centered on differentiated PP fiber grades rather than purely commodity outputs. Borealis announced a EUR 49 million investment (January 2026) at its Burghausen, Germany site to scale up Borstar Nextension polypropylene for applications including fibers, supporting higher-performance and design-for-circularity requirements in downstream yarn and nonwoven portfolios.

China and India-linked infrastructure and industrial programs continue to translate into application-specific whitespace for PP fibers, where suppliers increasingly bundle technical validation and compliance support. In June 2026, Jiangsu Haibang New Material commenced development of a functional modified PP fiber facility in Taizhou, Jiangsu province (500 million yuan investment, 60,000 metric tons capacity). On the demand side, project-led adoption in geotextiles and fiber-reinforced concrete, along with circular-grade initiatives (including mass-balance and recycled-content claims used by brands and converters), supports room for suppliers that can deliver consistent properties, documented recycled content, and lower-shedding nonwoven structures aligned with tightening microplastics scrutiny.

Recent Industry Developments

- June 2026: Freudenberg Performance Materials introduced fine denier spunbond nonwoven technology for liquid filtration and technical textile applications, compatible with polymers including polypropylene (PP). The launch supports higher-efficiency filtration media design where fiber diameter and uniformity are key. It positions PP nonwovens for more technical, specification-driven segments beyond commodity hygiene grades.

- February 2026: Beaulieu International Group signed a Memorandum of Understanding with Alujain Corporation to establish a joint venture in Saudi Arabia focused on synthetic fibers and nonwovens. The agreement broadens regional manufacturing optionality. It also aligns PP fiber and nonwoven supply with Middle East project and conversion hubs.

- January 2026: Beaulieu International Group signed a share purchase agreement to acquire all shares of IFG Asota GmbH, an Austria-based synthetic staple fiber producer. This strengthens staple-fiber capabilities and integration across the group. It improves access to engineered fiber formats used in construction, automotive textiles, and technical nonwovens.

Research Methodology Framework and Report Scope

Market Definition and Coverage

In this methodology, the polypropylene fibers market is defined as the global demand and supply of polypropylene-based fibers counted in physical volume (tons), across major producing and consuming regions, for industrial and consumer end uses.

Scope exclusions: We exclude downstream finished goods value (for example, packaged hygiene articles or completed geotextile installations) and count only the fiber volume.

Segmentation Overview

- By Type

- Yarn

- Staple

- By End-user Industry

- Textile

- Construction

- Healthcare and Hygiene

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the market and to anchor the model to polymer and fiber activity that can be observed in official datasets. We leaned on public and official sources such as UN Comtrade trade statistics, World Bank macro indicators, national statistics offices, and customs and tariff schedules that help interpret fiber-related trade flows. We also reviewed technical and application context from peer-reviewed polymer and textile journals, plus standards and guidance from relevant industry associations.

To cross-check the direction of supply, we used company annual reports, investor presentations, and plant or capacity announcements covered by reputable press, which helps separate an announced plan from an operational supply change. In a few places, subscription datasets were used only for company financials and patent lookups to confirm timelines for new grades and processing improvements. The desk sources listed here are illustrative, and many other public references were also used during data collection and validation.

Primary Interviews and Surveys

Primary work focused on validating how polypropylene fiber volumes move by application and region, and on stress-testing assumptions that desk sources do not resolve well, such as substitution with other synthetic fibers and typical yield losses during processing. We spoke with manufacturers, distributors, converters, and large end users. For a global market, the discussion reflected demand signals across APAC, EMEA, and the Americas before we locked the final ranges.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 12% | APAC: 46% |

| Mid tier: 54% | Functional/Unit leaders: 35% | EMEA: 34% |

| Smaller Players: 15% | Managers: 53% | Americas: 20% |

Market-Sizing & Forecasting

Sizing was built mainly through a top-down approach where polymer and fiber activity indicators are used to reconstruct the addressable demand pool in tons, and then allocated across regions and end uses using validated shares. After forming the first cut, we checked the totals with selective bottom-up approximations, including sampled producer shipment ranges, distributor channel checks, and application-level volume math, and then adjusted the model only when the checks pointed to a consistent gap.

Inputs that mattered in this market included polypropylene resin availability and pricing direction, nonwoven and staple fiber consumption cues tied to hygiene and construction demand, trade movement of fiber and related intermediates, capacity additions or shutdowns for fiber lines, and substitution trends between polypropylene, polyester, and other synthetics. For forecasting, scenario analysis was used to reflect different demand paths in hygiene, geotextiles, and industrial textiles, and then the selected scenario was aligned with expert views gathered during interviews. Where bottom-up details were missing for smaller countries, we filled gaps through region peer benchmarking using import dependence, construction activity, and textile production indicators, and then rechecked the implied per-capita usage for reasonableness.

Data Validation & Update Cycle

Validation was done through multiple passes so the final totals do not rely on one single data point. Model outputs were compared with independent signals, such as trade direction, known capacity moves, and application demand markers, and any sharp jumps were reviewed to confirm they were supported by more than one input. If a variance could not be explained, assumptions were revisited and, where needed, follow-up calls were conducted to clarify changes in pricing, mix, or utilization.

Before sign-off, the work is reviewed by another analyst who checks calculation logic, units, and region splits, followed by a final consistency check against the full time series. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major capacity additions, policy changes affecting textiles, or sudden feedstock disruptions. Right before delivery, a fresh scan is performed so clients receive an updated view rather than an older snapshot.

Mordor Intelligence's Polypropylene Fibers Maket Market Size Measured Against Other Published Estimates

It is normal to see different published market sizes for polypropylene fibers because the underlying measuring unit and the boundary of what is counted are not the same across sources. Some publishers report revenue in USD, some report volume in tons, and even within volume-based work, the application mapping and trade treatment can shift totals.

In this study, the checks that matter most are capacity and operating rate signals, trade movement patterns, and application-level consumption logic, which are then tied back to the 2026 volume estimate used by Mordor Intelligence. When these signals are handled differently, especially around whether downstream nonwovens are treated as fiber-equivalent volume or as finished product value, the reported market size can move a lot even if the real demand trend is similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.46 M (2026) | |

| Global Consultancy A | USD 4.36 B (2025) | Uses revenue in USD with its own price and mix assumptions across fiber forms, which is not directly comparable to a volume-in-tons market total. |

| Industry Research Group B | USD 6.10 B (2024) | Publishes a revenue number and may include a wider set of polypropylene fiber-derived products under the same label, which can inflate the addressable scope versus fiber volume only. |

The table indicates that the widest spread comes from unit choice and the scope boundary, not from a disagreement on demand direction. By keeping the model traceable to tons and then validating it with supply and trade signals, the estimate remains easier to reproduce and to use for planning across regions and end uses.

Key Questions Answered in the Report

What is the size of the polypropylene fibers market?

The polypropylene fibers market stands at 3.46 million tons in 2026 and is expected to reach 3.96 million tons by 2031, growing at a 2.74% CAGR from 2026 to 2031.

Which region leads demand growth for polypropylene fibers?

Asia-Pacific holds 51.12% of 2025 volume and posts the fastest regional CAGR of 3.37% through 2031, driven by road, coastal, and infrastructure projects.

Why are polypropylene fibers gaining share in healthcare disposables?

Hospitals prefer lightweight, fluid-repellent spunbond-meltblown laminates that block 98% of aerosols, pushing healthcare and hygiene to the fastest end-user CAGR at 3.22% through 2031.

What technological trend could open new PP fiber niches?

Continuous-fiber-reinforced PP tapes and 3-D printed PP composites enable lighter automotive, aerospace, and tooling parts while preserving recyclability.

Page last updated on: