Mexico Cold Chain Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

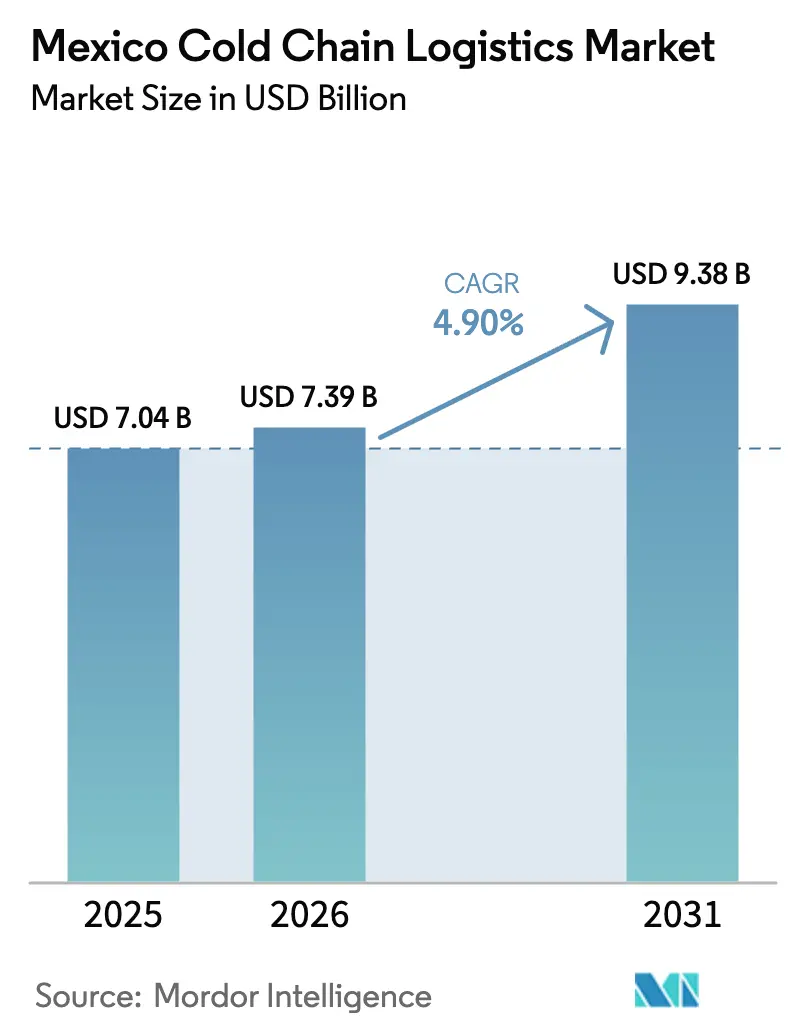

| Base Year Market Size (2025) | USD 7.04 Billion |

| Market Size (2026) | USD 7.39 Billion |

| Market Size (2031) | USD 9.38 Billion |

| Growth Rate (2026 - 2031) | 4.90% CAGR |

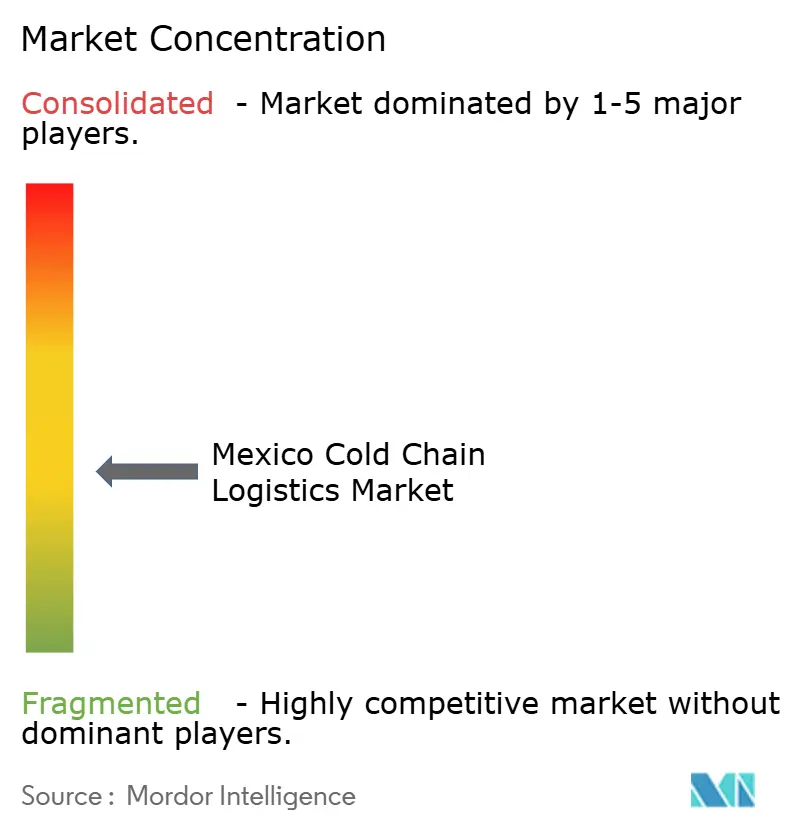

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Cold Chain Logistics Market Analysis by Mordor Intelligence

The Mexico cold chain logistics market size is expected to grow from USD 7.04 billion in 2025 to USD 7.39 billion in 2026 and is forecast to reach USD 9.38 billion by 2031 at a 4.90% CAGR over 2026-2031.

Robust nearshoring momentum under USMCA, the rollout of high-bay automated storage clusters along the northern border, and venture-capital infusions into tech-enabled 3PL start-ups are widening the capacity gap in the Mexico cold chain logistics market. Stricter NOM-251 and United States FSMA traceability rules are accelerating the adoption of IoT sensors and blockchain platforms that provide end-to-end shipment visibility, while a surge in biologics and vaccine exports is pushing operators to invest in −80 °C infrastructure. Power-grid instability in produce heartlands and escalating cargo-theft insurance premiums temper growth prospects, yet rising e-grocery penetration keeps last-mile micro-fulfillment build-outs on an upward trajectory, ensuring that the Mexico cold chain logistics market continues to attract long-term capital.

Key Report Takeaways

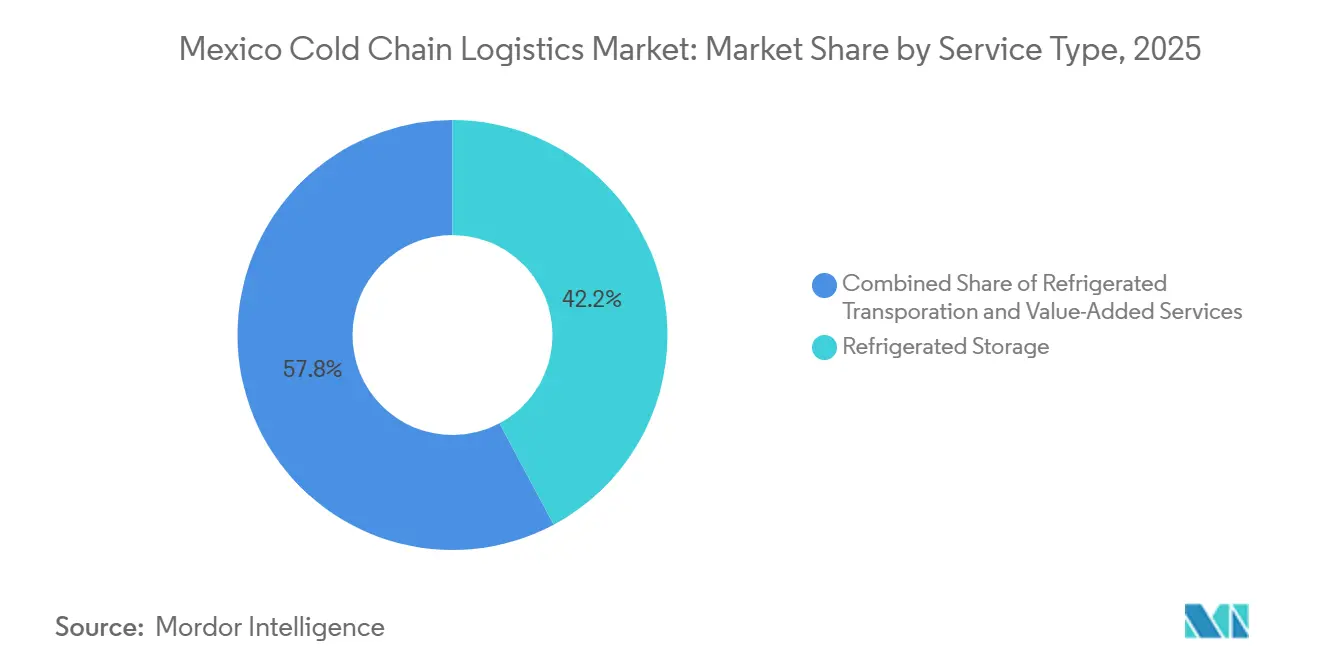

- By service type, refrigerated storage accounted for 42.20% of the Mexico cold chain logistics market share in 2025, whereas value-added services recorded the fastest 4.94% CAGR through 2031.

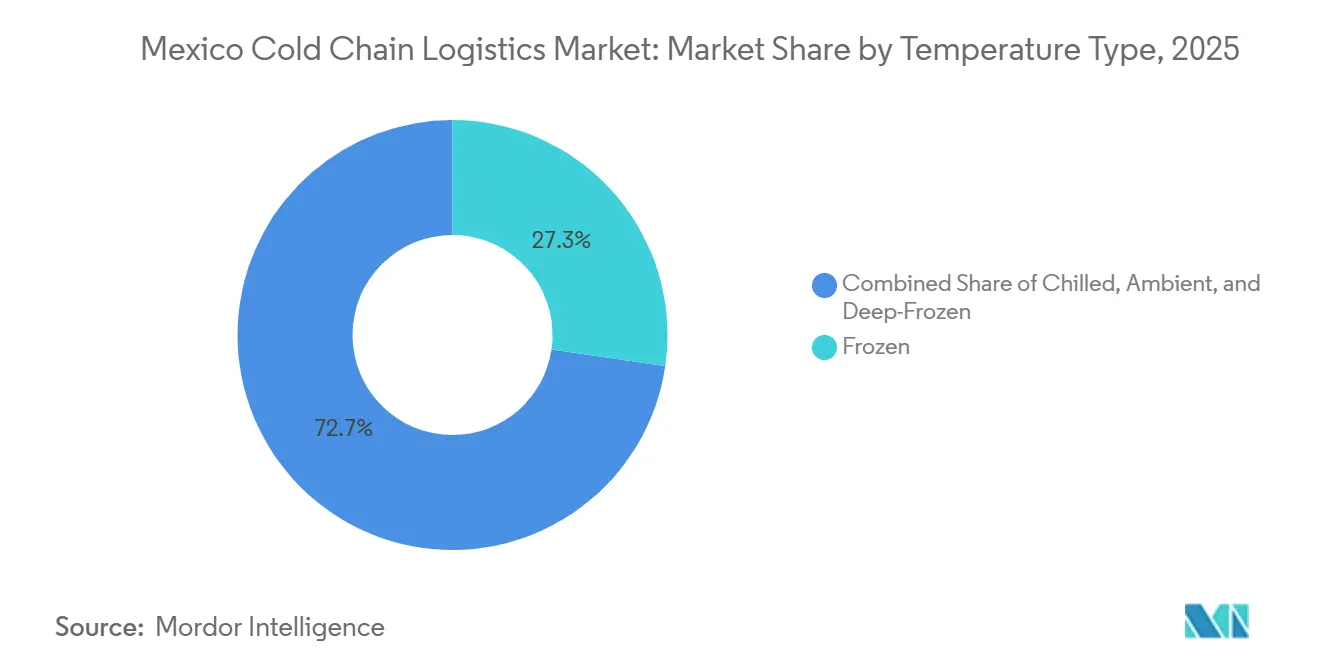

- By temperature type, the frozen temperature band held 27.30% of the overall Mexico cold chain logistics market share in 2025, while the deep-frozen segment is forecast to expand at a 5.10% CAGR between 2026 and 2031.

- By application, meat and poultry captured 21.50% of the Mexico cold chain logistics market size in application terms in 2025, but ready-to-eat meals are projected to post the highest 5.30% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with Mexico representing one among them. The global report on cold chain logistics market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

Mexico Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| USMCA-Driven Sanitary-Phytosanitary Harmonization | +1.1% | National export corridors | Medium term (2-4 years) |

| Automated High-Bay Cold-Storage Clusters Near Border | +0.9% | Northern states, Bajío | Long term (≥ 4 years) |

| VC-Backed Tech-Enabled 3PL Start-ups Scaling Nationwide | +0.7% | Urban hubs | Medium term (2-4 years) |

| Mandatory End-to-End Traceability Compliance | +0.8% | Export facilities | Short term (≤ 2 years) |

| Pharma Export Boom Requiring Ultra-Low-Temperature Logistics | +0.6% | Pharma zones | Medium term (2-4 years) |

| Retail Omnichannel Micro-Fulfillment Expansion | +0.5% | Mexico City, Monterrey, Guadalajara | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

USMCA-Driven Sanitary-Phytosanitary Harmonization

USMCA embedded a common rulebook for produce, meat, and dairy, lifting long-standing obstacles that once delayed perishable cargo at the border. Jalisco became the second state authorized to ship avocados to the United States, adding 100,000 tons of incremental fruit that now clears customs in 4-6 hours rather than 24-48 hours. Ninety percent of United States avocado imports originate in Mexico, and duty-free treatment keeps the bilateral value chain cost-competitive. Mutual-recognition audits let USDA inspectors validate orchards in advance, so carriers in the Mexico cold chain logistics market avoid spoilage losses tied to dwell times. Growers, packers, and 3PLs report improved labor scheduling because they can predict border transit windows within a two-hour variance[1]“México exportación oro verde aguacate,” Expansión, expansion.mx.

Automated High-Bay Cold-Storage Clusters Near Border

Vertical warehouses with 40-foot clear heights are proliferating around Laredo and El Paso. A single Kuehne + Nagel site in El Paso consolidates four legacy depots and pushes 50,000 pallets through fully automated cranes, shrinking pick-to-ship times by 70%. Robotics addresses a 56,000-driver shortfall by substituting labor with AS/RS units that lift, sort, and stage mixed-temperature SKUs inside the same building. Integrating rooftop solar and LED lighting lowers energy cost per cubic foot, creating a blueprint that other players in the Mexico cold chain logistics market are copying in the Bajio[2]“Foreign Supplier Verification Program,” U.S. FDA, fda.gov.

VC-Backed Tech-Enabled 3PL Start-ups Scaling Nationwide

Venture funding has birthed data-driven entrants that automate freight matching, IoT monitoring, and route optimization. Chile’s UNK deployed telematics that flag a 2 °C temperature drift within 60 seconds, slashing produce shrink by 20% for early adopters. Mexican beverage giant Arca Continental adopted Sensify’s AI-based cooling diagnostics, trimming compressor energy draw by 15% and setting a performance bar legacy providers must meet. These success stories underpin a flywheel that attracts new capital into the Mexico cold chain logistics industry, further digitalizing capacity.

Mandatory End-to-End Traceability Compliance

NOM-251 demands continuous temperature records and HACCP adherence, while FSMA’s FSVP extends accountability into Mexican farms shipping into the United States. Small operators spend USD 50,000 on cloud trackers, whereas multinationals invest USD 5 million to integrate ERP, WMS, and blockchain ledgers. Failure to comply can halt exports overnight, as seen when the USDA temporarily blocked certain avocado lots in 2024. Consequently, the Mexico cold chain logistics market treats audit readiness as a core selling point, bundling compliance dashboards with every service contract.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Power-Grid Instability in Key Produce Heartlands | −0.7% | Michoacan, Jalisco, Sinaloa | Short term (≤ 2 years) |

| Escalating Insurance Premiums for Excursion and Cargo Theft | −0.6% | National high-value lanes | Medium term (2-4 years) |

| Scarcity of Class-A Cold-Warehouse Real Estate in Tier-2 Cities | −0.5% | Queretaro, Aguascalientes, Guanajuato | Long term (≥ 4 years) |

| Port-Side Customs Bottlenecks Eroding Chilled-Cargo Shelf-Life | −0.4% | Manzanillo, Lazaro Cardenas, Veracruz | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Power-Grid Instability in Key Produce Heartlands

Average blackout duration climbed from 2 minutes to 11 minutes, forcing avocado packers in Michoacán and berry exporters in Jalisco to install diesel gensets that add USD 0.03 per kWh and 15% to total refrigeration. Beyond cost, voltage dips corrupt compressor cycles, cutting shelf life by 12 hours for some fruit. Operators in the Mexico cold chain logistics market now add UPS buffers and dual evaporator circuits to critical nodes, but redundant gear inflates capex and slows payback[3]“Electricity in Mexico,” The Mexico Political Economist, mxpe.org.

Escalating Insurance Premiums for Excursion and Cargo Theft Risk

More than 85,000 hijackings since 2019 have doubled premiums on reefer fleets traversing Puebla-Veracruz and Mexico-Queretaro corridors. Underwriters insist on GPS locks, armed escorts, and geofenced routing expenses that layer 8-12% on freight rates. Carriers must also ensure against temperature excursions; one spoiled biologics load can wipe out profits for a quarter, making risk mitigation paramount in the Mexico cold chain logistics market[4]“Meat Consumption in Mexico to Keep Rising,” USDA ERS, ers.usda.gov.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Value-Added Services Drive Differentiation

Refrigerated storage commanded 42.2% of the Mexico cold chain logistics market share in 2025 as Emergent Cold and Frialsa grew combined capacity to 282.7 million ft³. However, margin squeeze from volatile electricity prices is pushing operators toward services such as blast freezing, cross-docking, and kitting that earn 20-35% premiums. Value-added services are therefore projected to increase their slice of the Mexico cold chain logistics market size faster than any other service, expanding at a 4.94% CAGR through 2031.

Digital orchestration amplifies this pivot: AI demand-sensing from Blue Yonder’s 600-staff Monterrey hub feeds real-time slotting routines that cut order cycle time by 30%. Canadian Pacific Kansas City’s USD 240 million annual rail capex opens refrigerated blocks that bypass congested highways, enabling 3PLs to bundle door-to-door rail-road products. As compliance complexity deepens, clients reward providers that shoulder labeling, quality inspection, and customs data entry, reinforcing the ascendancy of value-added plays in the Mexico cold chain logistics market.

By Temperature Type: Deep-Frozen Capacity Expands Fastest

The frozen band retained a market share of 27.3% of 2025 revenue, thanks to Mexico’s 4.1 million-metric-ton poultry output. Yet deep-frozen and ultra-low zones, tethered to booming biologics exports, are set to notch a 5.1% CAGR, outpacing all other ranges in the Mexico cold chain logistics market. DHL’s ongoing hub roll-out, which embeds −80 °C cells within multi-temperature parks, exemplifies capex flowing into this niche.

Retail tastes also lift deep-frozen demand: premium ice cream and chef-crafted frozen entrées now occupy end-caps at urban mini-marts, a response to dual-income lifestyles. High-density locations employ multi-zone chambers so a single forklift circuit can service chilled berries, frozen poultry, and −80 °C trial vaccines without cross-contamination. Those hybrid builds require advanced insulation and smart air curtains, driving technology spend inside the Mexico cold chain logistics market.

By Application: Convenience Foods Spur Ready-To-Eat Surge

Meat and poultry retained a market share of 21.5% of the 2025 application value, anchored by rising per-capita poultry intake that the USDA sees hitting 43.8 kg by 2033. Nevertheless, ready-to-eat meals will clip a 5.3% CAGR because urban millennials swap home cooking for reheatable dishes. Amazon, Walmart, and MercadoLibre all specify mixed-temperature totes that land on doorsteps within 60 minutes, stretching the Mexico cold chain logistics market into neighborhood micro-hubs.

Fruits and vegetables benefit from avocado and berry export uprisings, while fish and seafood leverage longer shelf life gains from super-chill at −1 °C. Pharmaceuticals and biologics ride NIH and FDA cross-border trial pipelines, elevating the value per cubic foot handled. Each vertical imposes special handling and documentation, so operators diversify SOP libraries to secure wallet share across the Mexico cold chain logistics market size spectrum.

Geography Analysis

Northern border states dominate throughput as trucks carry 72.5% of United States–Mexico freight, and cross-border volumes climbed 52% year-on-year to September 2024. Kuehne + Nagel’s El Paso site and DSV’s 900,000 ft² Laredo project illustrate how automated depots knit Mexican supply nodes to United States consumer markets within a one-day drive. Canadian Pacific Kansas City’s refrigerated train sets, now linking Guanajuato agro-parks with Illinois distributors, insulate perishables from highway theft.

The Bajio Queretaro, Guanajuato, and Aguascalientes absorb automotive and aero OEMs that pull imported components through temperature-controlled cross-docks, broadening the addressable Mexico cold chain logistics market. Pacific hubs, led by Manzanillo, interface with Asia; a new seven-line Shanghai service cuts door-to-door avocado transit to 24 days, though customs lag still clips chilled margins.

Central megacities consume two-thirds of national convenience foods, prompting Amazon and MercadoLibre to ring Mexico City with micro-fulfillment nodes. Agricultural south-west regions shoulder blackout woes but remain indispensable, keeping investment channels open for grid-tied solar micro-grids that stabilize pack-house chillers.

Mordor Intelligence provides coverage of the cold chain logistics market across other key regional markets, including Africa and South America, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Indonesia, Sweden, Netherlands, and Thailand incorporating local coverage and market participation, as required.

Competitive Landscape

The Mexico cold chain logistics market exhibits moderate concentration, with the top five players controlling approximately 35-40% of the market share, while numerous local fleet services cater to regional crops. DHL is investing EUR 2 billion (USD 2.08 billion) in healthcare capital expenditures to strengthen its pharmaceutical segment. Simultaneously, CPKC-Americold plans to allocate USD 500 million to 1 billion for the development of cross-border rail-refrigerated corridors. Emergent Cold and Frialsa are competing to secure prime class-A sites before they become unavailable, while domestic conglomerate Traxion leverages its Less Than Truckload (LTL) network to consolidate ambient and cold Stock Keeping Units (SKUs) into a single invoice.

Digital differentiation is becoming a critical factor in the market. UNK's Software as a Service (SaaS) telemetry, Sensify's AI-powered compressors, and Blue Yonder's demand-sensing solutions are creating integrated ecosystems that shift the focus from rate-based competition to value-added data-service bundles. Compliance expertise serves as another competitive advantage, with facilities holding USDA, FDA, and Good Distribution Practice (GDP) certifications attracting export-focused tenants and commanding a 15% premium in rental rates.

Security innovation has also become a strategic priority. Features such as geofenced routes, panic buttons, and drone escorts are now key considerations in Request for Proposal (RFP) evaluations. This reflects the increasing importance of mitigating cargo theft risks in shaping strategies within Mexico's cold chain logistics industry.

Mexico Cold Chain Logistics Industry Leaders

AIT Worldwide Logistics

Emergent Cold LatAm

DHL Group

Frialsa Frigorificos

United Parcel Service of America, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: CPKC and Americold launched a cross-border refrigerated rail service that connected the US Midwest to Mexico. This initiative bolstered multimodal cold corridors, mitigated risks associated with border congestion, and upheld temperature integrity. Furthermore, it positioned rail transportation as a viable and scalable alternative to traditional long-haul reefer trucking.

- January 2026: Emergent Cold LatAm inaugurated a modern cold storage warehouse in the Guadalajara region. The facility had a capacity of 12,000 pallet positions across 81,000 cubic meters and was designed to store 12,000 tons of food. The site included land for future expansions to double its capacity.

- August 2025: DSV started a 900,000 ft² distribution center in Laredo to strengthen cross-border cold chain flows between Mexico and the United States.

- June 2025: We Store Frozen broke ground on a USD 40 million, 100,000 ft² frozen store in Laredo, expanding capacity for inbound produce and proteins.

Mexico Cold Chain Logistics Market Report Scope

| Refrigerated Storage | |

| Refrigerated Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Value-Added Services |

| Chilled (0-5°C) |

| Frozen (-18-0°C) |

| Ambient |

| Deep-Frozen/Ultra-Low (less than -20°C) |

| Fruits and Vegetables |

| Meat and Poultry |

| Fish and Seafood |

| Dairy and Frozen Desserts |

| Bakery and Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals and Biologics |

| Vaccines and Clinical Trial Materials |

| Chemicals and Specialty Materials |

| Other Perishables |

| By Service Type | Refrigerated Storage | |

| Refrigerated Transportation | Road | |

| Rail | ||

| Sea | ||

| Air | ||

| Value-Added Services | ||

| By Temperature Type | Chilled (0-5°C) | |

| Frozen (-18-0°C) | ||

| Ambient | ||

| Deep-Frozen/Ultra-Low (less than -20°C) | ||

| By Application | Fruits and Vegetables | |

| Meat and Poultry | ||

| Fish and Seafood | ||

| Dairy and Frozen Desserts | ||

| Bakery and Confectionery | ||

| Ready-to-Eat Meals | ||

| Pharmaceuticals and Biologics | ||

| Vaccines and Clinical Trial Materials | ||

| Chemicals and Specialty Materials | ||

| Other Perishables | ||

Key Questions Answered in the Report

How big will Mexico’s cold chain logistics sector be by 2031?

It is projected to reach USD 9.38 billion by 2031, up from USD 7.39 billion in 2026.

What compound annual growth rate is expected for the country’s temperature-controlled logistics through 2031?

A 4.90% CAGR is forecast for the 2026-2031 period.

Which service category is expanding the fastest across Mexico’s refrigerated supply chains?

Value-added services such as co-packing, blast freezing, and labeling are on track for the highest 4.94% CAGR through 2031.

Why is deep-frozen capacity scaling so rapidly in the nation’s logistics networks?

Rising exports of biologics, vaccines, and premium frozen foods require −80 °C infrastructure, driving a 5.10% CAGR in deep-frozen revenue.

How does USMCA shape cross-border refrigerated trade for Mexican exporters?

Harmonized sanitary-phytosanitary rules cut border clearance from up to 48 hours to as little as 4 hours, boosting avocado and berry throughput.

What security upgrades are logistics firms using to curb cargo theft on Mexican highways?

Operators deploy GPS-locked reefers, armed escorts, and geofenced routing, lowering theft incidents by 40-60% even as insurance premiums rise.

Page last updated on: