United Arab Emirates Sugar Confectionery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

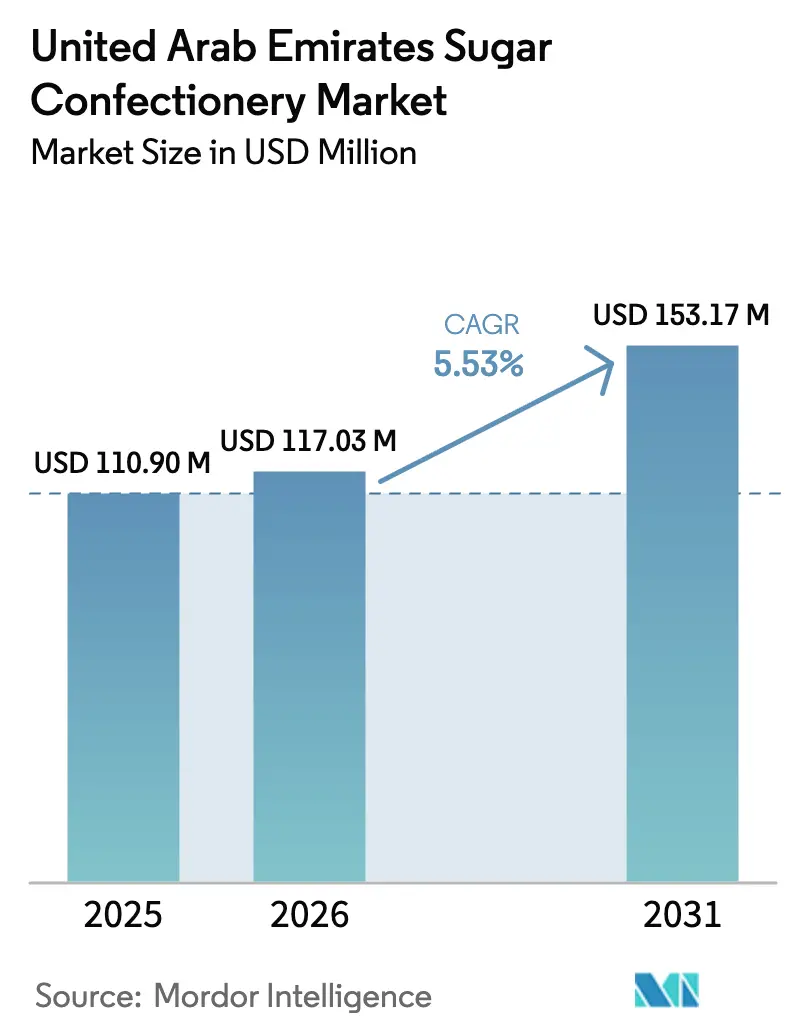

| Base Year Market Size (2025) | USD 110.90 Million |

| Market Size (2026) | USD 117.03 Million |

| Market Size (2031) | USD 153.17 Million |

| Growth Rate (2026 - 2031) | 5.53% CAGR |

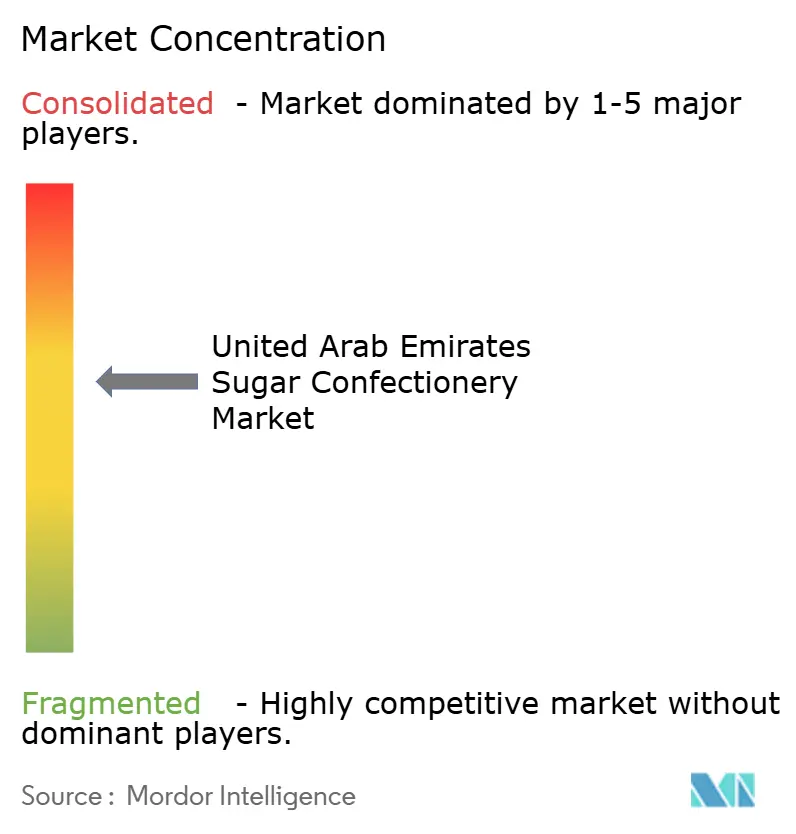

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Arab Emirates Sugar Confectionery Market Analysis by Mordor Intelligence

The United Arab Emirates sugar confectionery market size was valued at USD 110.90 million in 2025 and estimated to grow from USD 117.03 million in 2026 to reach USD 153.17 billion by 2031, at a CAGR of 5.53% during the forecast period (2026-2031). Three structural forces sustain this trajectory: an expatriate consumer base representing 88.52% of the total population, tourism flows that brought 18.72 million visitors to Dubai in 2024, and the rapid digitization of food retail channels. Discretionary purchases linked to gifting, duty-free impulse buys, and a cultural bias for premium imports elevate value growth above simple volume gains. Multinational incumbents such as Mars, Mondelēz, and Ferrero leverage regional manufacturing hubs for scale economies, while regional specialists like Patchi, Al Nassma, and Gandour protect share through localized flavors and Halal certification. Combined, these elements give the United Arab Emirates sugar confectionery market a balanced opportunity profile despite emerging health-policy headwinds.

Key Report Takeaways

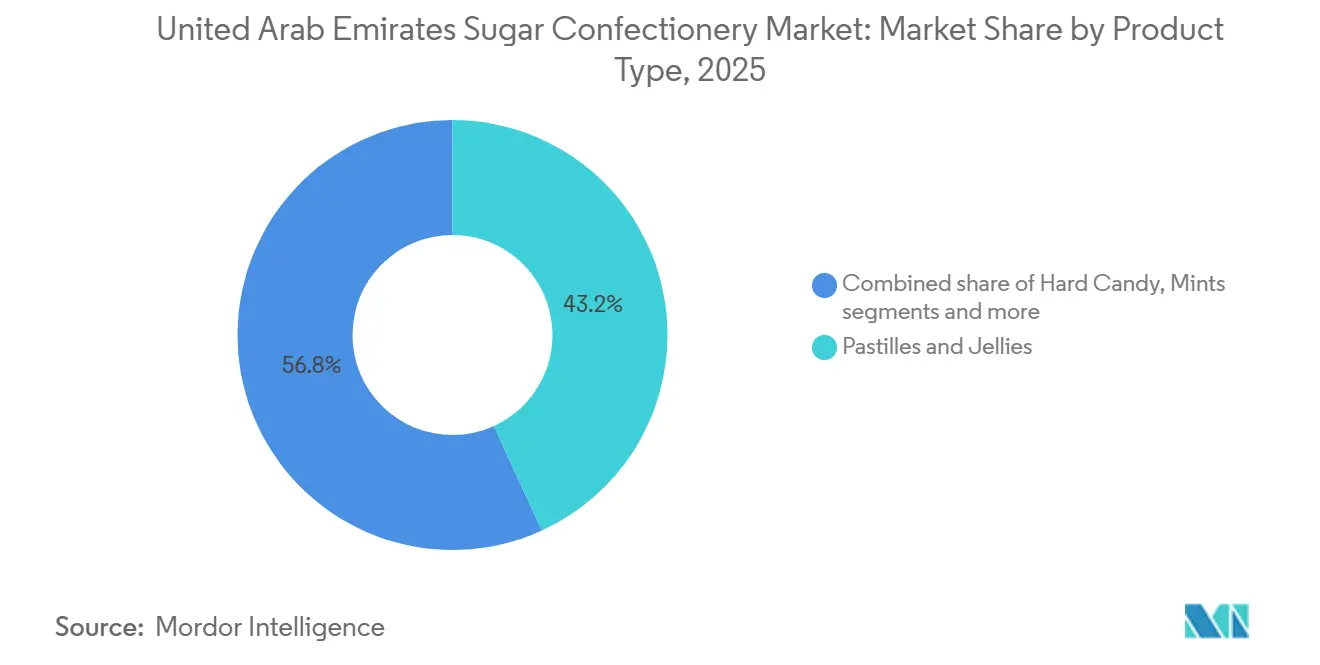

- By product type, pastilles and jellies led with 43.18% of 2025 revenue, while mints are projected to record the fastest 6.41% CAGR through 2031.

- By packaging type, sachets and pouches held the largest 40.76% share in 2025 and are forecast to advance at a 6.27% CAGR to 2031.

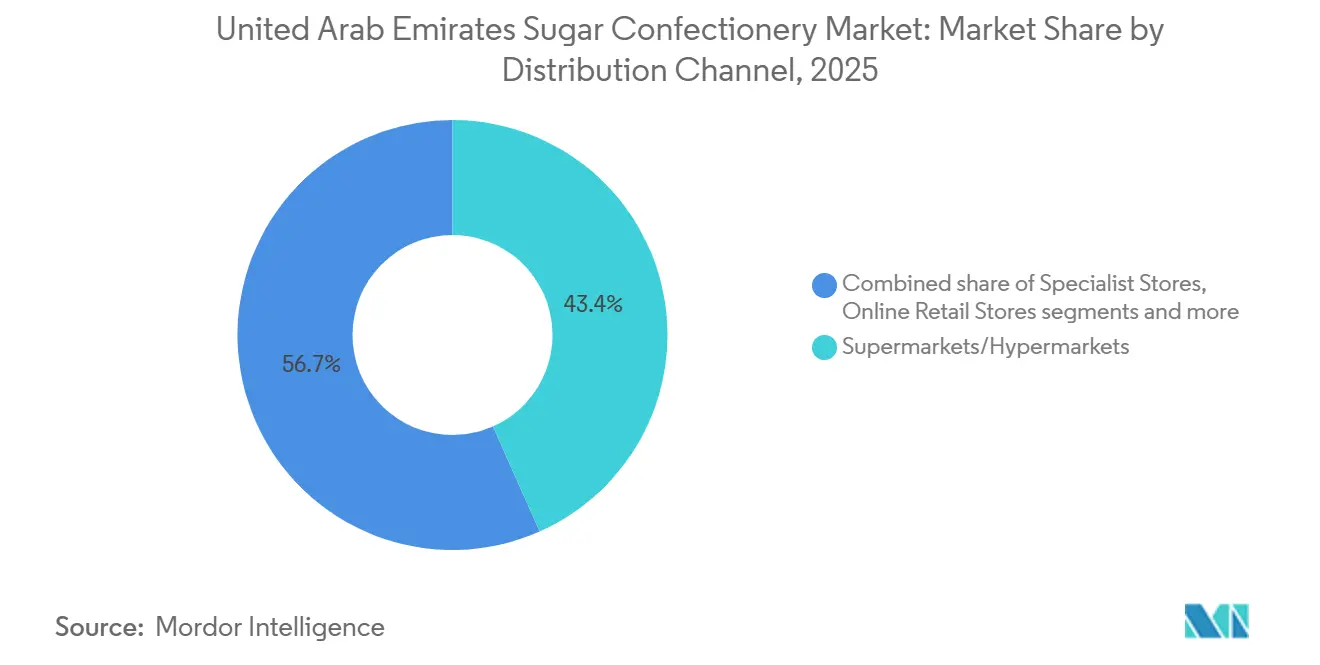

- By distribution channel, supermarkets and hypermarkets captured 43.35% of 2025 sales, whereas online retail stores are expected to grow at a 6.66% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Arab Emirates Sugar Confectionery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in expatriate population diversifies consumer demand for confectionery | +1.2% | Nationwide, concentrated in Dubai, Abu Dhabi, Sharjah | Long term (≥ 4 years) |

| Tourism expansion increases confectionery sales, especially at duty-free and travel retail locations | +0.9% | Dubai, Abu Dhabi airports and duty-free zones | Medium term (2-4 years) |

| Development of modern retail infrastructure enhances product accessibility and visibility | +0.8% | Urban centers: Dubai, Abu Dhabi, Sharjah, Ajman | Medium term (2-4 years) |

| Launch of innovative and limited-edition products attracts consumer interest | +0.6% | Nationwide, premium retail channels | Short term (≤ 2 years) |

| Strategic marketing and promotional campaigns by leading brands influence purchasing behavior | +0.5% | Nationwide, digital and physical retail | Short term (≤ 2 years) |

| Higher disposable incomes encourage spending on premium and imported confectionery items | +0.4% | Dubai, Abu Dhabi high-income zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in expatriate population diversifies consumer demand for confectionery

The growing expatriate population in the UAE is significantly influencing consumer preferences, prompting sugar confectionery companies to diversify their offerings in terms of flavors, formats, and price points. As per Emiratisation Gate, expatriates constituted nearly 88% of the UAE's population as of December 2025, totaling approximately 11.06 million out of 12.50 million [1]Source: Emiratisation Gate, "How Many Emiratis are in UAE? – Population Figures," emiratisationgate.org. This predominantly non-local demographic, shaped by origins in South Asia, Europe, and other MENA regions, has driven demand for both familiar "home-country" confectionery products and new global options. Global brands such as Haribo and Perfetti Van Melle have responded by introducing region-specific SKUs, including fruit gummies, chewy candies, and filled toffees, aligning with European and Asian flavor profiles while meeting local halal and labeling requirements. The diverse income levels within the expatriate workforce support a segmented market where mass-market brands compete with premium players like Patchi and Gandour, enabling retailers to offer assortments ranging from everyday impulse purchases to premium giftable options for occasions such as Diwali, Christmas, Eid, and corporate gifting. These multicultural celebrations foster innovation in packaging and flavor combinations, with brands leveraging formats such as assorted mixed bags or themed gift boxes to appeal to diverse ethnic groups. Additionally, local and regional manufacturers, such as Gandour and Al Seedawi, are exploring hybrid concepts by blending traditional Arabic flavors like pistachio, rose, or cardamom into formats familiar to Western and Asian consumers. The UAE’s role as a regional trade hub further allows global players like Mars and Mondelez to test and launch products for broader GCC and Middle Eastern markets, reshaping category dynamics and driving innovation to meet evolving multicultural preferences.

Tourism expansion increases confectionery sales, especially at duty-free and travel retail locations

The expansion of tourism is significantly influencing sugar confectionery sales in the United Arab Emirates by increasing foot traffic at airports, duty-free shops, and travel retail hubs, where impulse and gifting purchases are prevalent. According to the Dubai Department of Economy and Tourism, Dubai recorded 16.79 million overnight visitors between January and November 2024, reflecting a 9% growth compared to the same period in 2023 [2]Source: Dubai Department of Economy and Tourism, "Tourism Performance Report January - November 2024", dubaidet.gov.ae . This surge in tourist arrivals directly drives demand for travel-friendly confectionery products such as gift boxes, share packs, and souvenir-themed candies. Duty-free operators at Dubai and Abu Dhabi airports are leveraging this trend by strategically positioning global brands like Ferrero Rocher near checkout areas, encouraging tourists to purchase premium pralines and assortments as last-minute gifts. Concurrently, travel retailers are dedicating more space to regionally distinctive offerings, with brands like Al Nassma utilizing camel-milk chocolates and desert-inspired flavors to establish their products as uniquely UAE souvenirs, thereby strengthening the link between tourism, local identity, and confectionery demand. These curated assortments often combine international favorites with local flavors, catering to travelers from Western, Asian, and regional backgrounds who seek both familiarity and novelty. Additionally, the growing tourist base supports the introduction of limited-edition and travel-exclusive product lines, with brands such as Lindt launching special travel packs and destination-themed packaging to encourage trading up and repeat gifting. The strong performance of confectionery within Dubai Duty Free’s portfolio, where categories like "Dubai chocolate" and other premium sweets have achieved record monthly sales, underscores the critical role of travel retail as a channel for volume and value growth. Overall, the combination of rising tourist numbers, strategic brand activations, and differentiated product assortments highlights tourism as a structural driver of sugar confectionery growth in the UAE market.

Development of modern retail infrastructure enhances product accessibility and visibility

The development of modern retail infrastructure in the UAE is driving growth in the sugar confectionery market by improving product accessibility and visibility through the expansion of hypermarkets, convenience stores, and specialty outlets with strategic displays and impulse zones. Initiatives such as the Dubai 2040 Urban Master Plan are enhancing retail spaces, enabling brands to secure prime shelf positions in high-traffic locations like Carrefour and Lulu Hypermarkets [3]Source: Government of Dubai, "Dubai 2040 Urban Master Plan," dm.gov.ae. These advancements benefit products such as hard candy and toffees from brands like Ricola, whose herbal drops and butterscotch variants gain prominence in wellness aisles near checkout counters, encouraging impulse purchases. Similarly, caramels and nougat from Ferrero's premium lines capitalize on dedicated gifting sections in modern malls, where upgraded fixtures highlight their premium appeal alongside seasonal promotions. Pastilles and jellies from Rowntree's attract attention through vibrant end-cap displays in convenience chains like Zoom, ensuring accessibility for on-the-go shoppers seeking fruity, chewy options. Mints from brands such as Extra or Tic Tac thrive near tobacco and beverage counters, leveraging breath-freshening habits after meals. These interconnected placements across categories foster cross-purchases, as shoppers navigating enhanced store layouts encounter a variety of sugar confectionery options in a seamless shopping experience. The modernization of retail spaces under initiatives like Dubai 2040 is structurally elevating category visibility, linking brand-specific innovations to improved consumer convenience and driving sales growth.

Launch of innovative and limited-edition products attracts consumer interest

Innovative and limited-edition product launches are driving consumer interest in the sugar confectionery market by introducing unique flavors, textures, and packaging that differentiate them from standard offerings. These initiatives encourage product trials across diverse demographics. For instance, brands like CandyLand have introduced hard candies with spicy chili and tamarind variants, combining global trends with local taste preferences, generating social media engagement and repeat purchases. Toffees and caramels infused with Middle Eastern dates are positioned as premium treats for festive gifting and everyday indulgence. Regional players like Patchi have launched pistachio-filled nougat limited editions, blending traditional Arabic flavors with modern textures, appealing to both expatriates seeking familiar tastes and locals exploring new options. Pastilles and jellies from brands like Jelly Belly leverage vibrant colors and shareable packaging to drive impulse purchases in modern retail settings. Mints, such as Altoids' cinnamon editions, align with post-meal refreshment habits and wellness trends, particularly in hypermarkets. These innovations often include cross-promotional bundles, such as nougat-toffee duo packs or jelly-mint assortments, enhancing perceived value and encouraging trials across product categories. Limited-edition strategies tied to events like Ramadan or the Dubai Shopping Festival create urgency and exclusivity, increasing consumer demand and collector appeal. Brands sustain interest by regularly rotating these exclusive offerings, avoiding competition with core product lines, while collaborations with influencers further amplify visibility. These launches reinvigorate the category, fostering consumer loyalty through novelty and positioning sugar confectionery as a dynamic space for flavor exploration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened health concerns about sugar consumption are reducing the frequency of confectionery purchases | -0.7% | Nationwide, particularly urban health-conscious segments in Dubai and Abu Dhabi | Medium term (2-4 years) |

| Strict government regulations on food labeling and sugar content are constraining product development | -0.5% | Nationwide | Long term (≥ 4 years) |

| Increased competition from healthier snack options is weakening the market appeal of confectionery products | -0.4% | Nationwide, concentrated in premium retail channels and e-commerce platforms | Medium term (2-4 years) |

| Environmental concerns and issues related to packaging waste are driving the need for sustainable alternatives, leading to higher costs | -0.3% | Nationwide, particularly affecting multinational brands with global sustainability commitments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heightened health concerns about sugar consumption are reducing the frequency of confectionery purchases

Health concerns surrounding sugar consumption are significantly impacting consumer behavior in the United Arab Emirates, with rising diabetes risks and public awareness campaigns driving selective purchasing patterns. The adult diabetes prevalence in the UAE reached 20.7% in 2024, according to the International Diabetes Federation, spurring public health initiatives that emphasize the link between sugar and chronic conditions. This has led consumers to limit confectionery indulgences to occasional treats rather than daily consumption. The World Health Organization's guideline recommending sugar intake below 10% of daily energy, ideally below 5%, has been adopted by UAE health authorities as a public education standard, intensifying scrutiny on high-sugar products such as hard candies from brands like Fox's Glacier Fruits, which now face reduced demand despite their appeal in wellness-related categories. Social stigma around sugar consumption is particularly evident among health-conscious expatriates, who prioritize moderation and opt for smaller portions of toffees, caramels, and nougat from brands like Tom & Jenny's to align with family health goals during social gatherings. Even lighter alternatives, such as pastilles and jellies from Fox's Glacier Mints, are experiencing reduced basket sizes as consumers weigh their sugar content against perceived benefits like post-meal refreshment. Mints from brands like Smint, marketed as low-calorie breath fresheners, have performed relatively better but cannot offset the overall decline in category sales driven by diabetes-related warnings. These factors collectively reduce impulse purchases across modern retail and duty-free channels, favoring portion-controlled or premium buys over habitual consumption and compelling brands to navigate a market shaped by health-driven consumer preferences.

Strict government regulations on food labeling and sugar content are constraining product development

Strict government regulations on food labeling and sugar content are impacting product development in the sugar confectionery market in the United Arab Emirates (UAE). These regulations require detailed nutritional disclosures and Nutri-Mark front-of-pack grading, restricting high-sugar formulations. Under UAE Ministry rules, enforced by ESMA and the Abu Dhabi Nutri-Mark scheme, effective from June 2025, products must display an A-E grading based on sugar content per 100g. Products with sugar levels exceeding 15g/100g face scrutiny and reformulation demands, which hinder the launch of indulgent products such as Barlow's Originals fruit drops, now needing reduced portion sizes or lower-sugar variants to avoid unfavorable ratings. Additionally, claims such as "low sugar" are permitted only for products with less than 5g of sugar per 100g, compelling brands like Thorntons to reformulate toffees, caramels, and nougat using natural sweeteners or smaller servings, slowing innovation in rich-textured products often preferred for gifting. Rowntree's pastilles and jellies face similar challenges, as their vibrant fruit flavors frequently exceed sugar thresholds, necessitating recipe adjustments to maintain chewiness while meeting labeling requirements and avoiding penalties such as shelf removal. Mints from Fisherman's Friend, marketed for throat relief, benefit slightly from lower inherent sugar levels but still require precise declarations of any added sweeteners, linking compliance requirements across categories and delaying bold flavor innovations. Imported products must also provide FTA-accredited lab reports for sugar verification, increasing costs and timelines for multinational brands adapting to UAE-specific regulations. These stringent ESMA-enforced standards on labeling accuracy, sugar limits, and grading create a compliance bottleneck, forcing brands to prioritize restrained product development over broader confectionery innovation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mints Accelerate as Breath-Freshening Demand Rises

Pastilles and jellies represented 43.18% of sugar confectionery revenue in 2025, driven by consumer preference for fruit-flavored chews that align with tropical and Middle Eastern taste profiles. These products, inspired by regional fruits like mango and pineapple, appeal to multicultural households and encourage everyday snacking among families and youth in modern retail environments. Brands such as Rowntree's leverage this demand by offering assorted fruit jellies in shareable pouches, supported by visually appealing displays that boost impulse purchases. This category's revenue leadership is further strengthened by expatriate-driven diversification, as pastilles provide a chewy, nostalgic connection between Asian and European palates without excessive sweetness.

Meanwhile, mints are expected to achieve a 6.41% CAGR through 2031, fueled by rising demand for breath fresheners in corporate and hospitality settings. The UAE's service-oriented economy, characterized by face-to-face client interactions in finance, real estate, and tourism, creates a functional need for discreet breath fresheners. Sugar-free mint variants, incorporating ingredients like stevia and sorbitol, enable manufacturers such as Smint to position their products as health-conscious alternatives that address diabetes concerns and align with WHO sugar guidelines. Packaging innovations, including stick packs and rolls, enhance portability and convenience for professionals navigating fast-paced environments. Hard candy remains a popular choice among price-sensitive consumers, particularly blue-collar expatriate workers in construction and logistics, who favor bulk sachets for affordability and long-lasting sweetness during labor-intensive shifts. Brands like Fox's Glacier Fruits cater to this demand with fruit-infused drops in value packs, ensuring visibility in high-traffic outlets without premium pricing pressures. In the premium segment, toffees, caramels, and nougat target older consumers and gifting occasions, offering indulgent, shareable luxuries. Brands such as Werther's Original and Ferrero's Duplo lead this category, catering to tourism and festive demand with high-quality ingredients and limited-edition launches that appeal to expatriates seeking sophisticated alternatives to everyday chews.

By Packaging Type: Sachets and Pouches Sustain Leadership Through Impulse Convenience

Sachets and pouches accounted for 40.76% of sugar confectionery packaging revenue in the UAE in 2025 and are expected to maintain their leadership with a 6.27% CAGR through 2031. Their popularity stems from their suitability for single-serve impulse purchases at petrol stations, convenience stores, and supermarket checkout lanes. This format's dominance is closely linked to the UAE's car-centric urban environment, where consumers frequently make unplanned confectionery purchases during fuel stops or quick grocery visits. Additionally, sachets and pouches align with increasing health consciousness, offering portion-controlled options that address concerns about sugar intake. For example, brands like Rowntree's provide pastilles and jellies in compact fruit packs, satisfying cravings without overindulgence. The growing adoption of 30-minute delivery services from Carrefour UAE, Noon, and Amazon.ae further supports demand for small-format products, as online shoppers often add items like Fox's Glacier Fruits hard candies to meet free-delivery thresholds. Manufacturers enhance these products with metallized films for visual appeal under retail lighting and resealable closures to maintain freshness, increasing the tactile appeal of items such as Tic Tac mints in pocket-sized formats.

Boxes and tins remain the preferred choice for gifting occasions, including Eid celebrations, weddings, and corporate events, where presentation and perceived value justify premium pricing. These formats are particularly popular during tourism peaks and expatriate festivities, elevating products like toffees, caramels, and nougat from brands such as Toffifee and Cartwright & Butler. Ornate designs on boxes and tins convey luxury, making them a staple in duty-free shops and hypermarket gifting aisles. Meanwhile, stick packs and rolls cater to on-the-go consumption, with brands like Perfetti Van Melle's Mentos leveraging this format for cash-till placement in travel retail. Products like Extra mints in slim rolls address portability needs during corporate interactions, while hard candies in stick formats appeal to quick refreshment in hospitality settings. This segmentation sustains impulse purchases while addressing premium motivations across various retail channels.

By Distribution Channel: Online Retail Surges as E-Commerce Penetration Deepens

Supermarkets and hypermarkets captured 43.35% of sugar confectionery distribution revenue in the UAE in 2025. These outlets utilize extensive shelf facings, promotional end-caps, and checkout-lane impulse displays to attract both planned and unplanned purchases across diverse consumer segments. Their success is closely tied to modern retail infrastructure, where brands strategically position products like Rowntree's pastilles and jellies in vibrant end-caps near fruits, appealing to family shoppers with tropical taste preferences. Checkout lanes further drive sales of mints, such as Extra, through slim rolls designed for quick breath-freshening, catering to corporate consumers in high-traffic areas. Meanwhile, the shift to online retail, growing at a 6.66% CAGR through 2031, challenges the dominance of physical stores by leveraging algorithm-driven visibility. Platforms like Carrefour UAE, with over 10 million mobile app downloads and more than 3 million active digital customers, and Amazon.ae's same-day delivery services, have normalized e-commerce for confectionery. Products like Fox's Glacier Fruits hard candies rank prominently through sponsored searches, prompting manufacturers to focus on digital strategies to ensure products like Werther's Original toffees and caramels are included in online grocery baskets without requiring bulk purchases.

Convenience and grocery stores excel in driving impulse purchases, catering to immediate gratification. Sachet and pouch formats are particularly effective in petrol-station forecourts and quick-stop missions, aligning with the car-centric geography of the UAE. These channels also cater to expatriate mobility, with blue-collar workers often purchasing bulk sachets of hard candies for long shifts, reinforcing sachet formats as leaders in portion control. Specialist stores focus on premium gifting, offering products like Ferrero's Duplo nougat and caramels in boxed formats, which enhance perceived value for festive occasions. Online platforms also play a role here, as convenience apps replicate the speed of forecourt purchases, offering mints in stick packs and blending physical impulse buying with digital convenience. This approach sustains channel diversity, enabling health-oriented formats like sugar-free jellies to integrate into on-the-go routines without cannibalizing other channels. Together, these outlets contribute 56.65% of distribution revenue, maintaining segmented access alongside the growth of e-commerce.

Geography Analysis

Dubai drives sugar confectionery consumption in the UAE, supported by its large expatriate population, advanced tourism infrastructure, and extensive retail networks. The emirate welcomed 18.72 million visitors in 2024 and 13.95 million arrivals in the first nine months of 2025, according to the Dubai Department of Economy and Tourism. These visitors contribute to significant sales in duty-free zones, hotels, and attractions, where products like Jelly Belly pastilles and jellies in exotic fruit flavors inspired by local tropical profiles are popular. Expatriates from India, Pakistan, the Philippines, and Western countries sustain everyday purchases of mints such as Altoids in stick packs through convenience stores and e-commerce platforms. Hypermarkets prominently feature hard candies like Werther's Originals, catering to price-sensitive workers. Dubai's manufacturing infrastructure further strengthens its position as a production hub, supplying innovative sachets nationwide and driving category leadership through high-volume, diversified access.

Abu Dhabi supports premium gifting demand, driven by its affluent population and corporate events that favor luxury confectionery formats. Al Nassma's camel-milk chocolates, blending local heritage with indulgent nougat and caramel flavors, cater to upscale gifting in specialist stores and duty-free outlets. The emirate's retail landscape also supports products like Toffifee toffees in ornate boxes, which are popular for weddings and Eid celebrations, appealing to older demographics. Tourism infrastructure complements this premium focus, with visitors purchasing items like Fisherman's Friend mints for on-the-go refreshment. Expatriate professionals align with health trends by opting for sugar-free jellies in pouches from hypermarkets. Manufacturing logistics from Dubai ensure a steady supply of fresh premium stock, reinforcing Abu Dhabi's role in value-driven segments.

Sharjah and Ajman contribute to the market by catering to price-sensitive segments through Lulu Group's hypermarkets and convenience networks. Bulk sachets of hard candies like Fox's Glacier Mints are popular among blue-collar expatriates for long shifts in logistics. Pastilles from Rowntree's in value pouches perform well at petrol forecourts, appealing to car-centric consumers. While gifting remains secondary, it is growing through products like caramels in tins for modest celebrations, efficiently distributed from Dubai's production base. Retail expansion in these regions ensures broader category penetration, extending beyond urban centers and sustaining demand in lower-emirate markets.

Competitive Landscape

The sugar confectionery market in the UAE is characterized by moderate consolidation, with multinational corporations such as Mars, Mondelēz, and Perfetti Van Melle commanding significant shelf space in hypermarkets and duty-free zones. These companies utilize extensive global supply chains to distribute products like Haribo's pastilles and jellies, catering to expatriate preferences and encouraging impulse purchases at checkout counters. Their established brand equity supports offerings such as Mars, Incorporated's Orbit sugar-free mints, aligning with health-conscious trends amidst rising diabetes concerns. Meanwhile, regional players like Patchi, Al Nassma, and Gandour compete by offering localized flavors, Halal-certified products, and culturally relevant options tailored to Emirati and Arab expatriates.

Growth opportunities are evident in sugar-free and reduced-sugar product innovations, addressing the UAE's adult diabetes prevalence of 20.7% as reported by the International Diabetes Federation in 2024. These products aim to balance indulgent taste profiles with health-conscious attributes, appealing to consumers in corporate and tourist settings. Reformulating hard candies like Ricola's herbal drops with stevia could position them as wellness-compatible options in convenience stores, particularly for post-meal breath freshening. Similarly, low-sugar pastilles from brands such as Dr. Doolittle’s can attract health-conscious expatriates through e-commerce platforms and portion-controlled packaging. Regional players can also explore reduced-sugar toffees, aligning with WHO guidelines adopted locally to ensure family-friendly appeal without stigma.

Premium artisanal formats offer another avenue for differentiation, incorporating local ingredients like camel milk and dates to justify higher price points and stand out from mass-market offerings in Dubai and Abu Dhabi. Al Nassma exemplifies this approach with camel-milk caramels and nougat bars, targeting the gifting market for weddings and corporate events. These products also cater to tourism demand, offering experiential souvenirs that combine heritage with indulgence. Additionally, artisanal jellies infused with date syrup appeal to upscale shoppers in modern retail settings, resonating with expatriates seeking hybrid flavors that evoke nostalgia.

United Arab Emirates Sugar Confectionery Industry Leaders

-

Mondelez International Inc.

-

Perfetti Van Melle Group

-

Mars, Incorporated

-

HARIBO GmbH & Co. KG

-

Nestlé S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Haribo opened its first Haribo Happy World experiential attraction in Dubai, which integrated retail, entertainment, and brand engagement. This initiative was designed to enhance consumer interaction beyond transactional purchases, positioning the German confectionery manufacturer to strengthen its presence in the United Arab Emirates and the broader MENA region through location-based experiences.

- July 2025: Cloetta Global Travel Retail partnered with Dubai Duty Free and King of Reach by B&S to execute an experiential activation for The Jelly Bean Factory at Dubai International Airport (DXB). The initiative included a dedicated display for the travel retail-exclusive 175g Tube, a key SKU that was listed in over 50 locations worldwide.

- April 2024: Ferrero Travel Market announced the installation of dedicated platforms at Dubai International Airport and Abu Dhabi Airport, offering shoppers the opportunity to win a giant T96 pyramid dome. These platforms enabled shoppers to create and share personalized animated greeting cards. Accessible via a QR code at both airport locations, the platform provided a chance to win a pyramid consisting of 96 Ferrero Rocher pralines, designed for sharing with friends and family.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the UAE sugar confectionery market as retail and food-service sales of non-chocolate, sugar-based candies, including hard candy, pastilles, gummies, jellies, toffees, caramels, nougat, and breath-freshening mints, sold either packaged or loose. Products with added cocoa content above 5%, chewing gum, chocolate bars, and bakery snacks lie outside this scope.

Scope exclusion: Chocolate confectionery and chewing gum are not counted, nor are compound-coated bakery items.

Segmentation Overview

-

By Product Type

- Hard Candy

- Toffees, Caramels and Nougat

- Pastilles and Jellies

- Mints

- Other Product Types

-

By Packaging Type

- Sachets/Pouches

- Boxes/Tins

- Sticks Packs and Rolls

- Others

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience/Grocery Stores

- Specialist Stores

- Online Retail Stores

- Other Distribution Channels

Detailed Research Methodology and Data Validation

Primary Research

Interviews with distributors, supermarket category buyers, and plant managers across Dubai, Abu Dhabi, and Sharjah clarified channel margins, traveler-led duty-free pick-ups, and average selling prices. Follow-up surveys with urban consumers gauged gifting incidence and flavor trends, tightening the elasticity ranges used in volume-to-value conversions.

Desk Research

Analysts began with trade classification code 1704 shipment data from UAE Customs, COMTRADE, and Volza, then reviewed import and export trends (volume and value) to frame the demand pool. Retail scanner insights from Dubai Statistics Center, household expenditure data from UAE Federal Competitiveness and Statistics Centre, and tourism arrival tables from Dubai Tourism offered base consumption clues. We cross-checked category sales splits and packaging mixes in industry white papers by the International Confectionery Association and annual reports from large branded manufacturers. D&B Hoovers supplied company-level revenue that helped benchmark domestic production. The publicly quoted sources listed are illustrative only; many others fed into validation and clarification.

Market-Sizing & Forecasting

We constructed a top-down and bottom-up hybrid. Import-export reconciliations and domestic output formed the overarching volume, which was then sanity-checked through sampled retailer sell-out data (bottom-up) to capture informal kiosks and souq sales. Key variables like per capita disposable income, international visitor nights, supermarket footprint growth, white-sugar wholesale prices, and new product launch counts drive the model. A multivariate regression forecasts demand to 2030, with scenario analysis adjusting for sugar tax or health-label legislation. Where bottom-up audits missed small artisan makers, proportional lift factors (derived from mystery-shopping spends) filled gaps before final calibration.

Data Validation & Update Cycle

Every dataset runs through variance checks against historical three-year CAGR bands; outliers trigger re-contact with at least one primary respondent. Senior analysts review assumptions, and the model refreshes annually, with interim updates if import tariffs, VAT shifts, or major M&A events materially alter baselines.

Credibility Corner: Why Our UAE Sugar Confectionery Baseline Commands Confidence

Published estimates often differ because firms play with definitions, pricing bases, and refresh frequency.

Key gap drivers in this niche include whether chocolate and gum are blended into totals, how duty-free volumes are treated, and if informal bazaar trade is captured. Some publishers report retail-only revenue at consumer price levels, while Mordor Intelligence anchors on manufacturer-level value that nets out taxes and double counting. Our annual refresh and dual-channel interviews further narrow error bars.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 110.7 M (2025) | Mordor Intelligence | - |

| USD 991.0 M (2024) | Global Consultancy A | Bundles chocolate, gum, and healthy snacks; uses retail invoice prices without import-export reconciliation |

| USD 104.7 M (2025) | Regional Consultancy B | Omits duty-free and kiosk sales; relies mainly on packaged grocery audit panels |

The comparison shows that headline numbers swing widely when scope widens or key channels are skipped. Mordor's disciplined variable selection, balanced hybrid modeling, and yearly update give decision-makers a transparent, reproducible baseline they can trust.

Key Questions Answered in the Report

What is the current value of the United Arab Emirates sugar confectionery market?

The market is valued at USD 117.03 million in 2026.

Which product segment is growing the fastest?

Mints are projected to rise at a 6.41% CAGR through 2031.

How fast is online retail expanding for confectionery?

Online stores are expected to grow at a 6.66% CAGR over the forecast period.

What is the main packaging format for impulse purchases?

Sachets and pouches accounted for 40.76% of 2025 packaging revenue due to portability and single-serve convenience.

Page last updated on: