Market Overview

| Study Period | 2021 - 2031 |

|---|---|

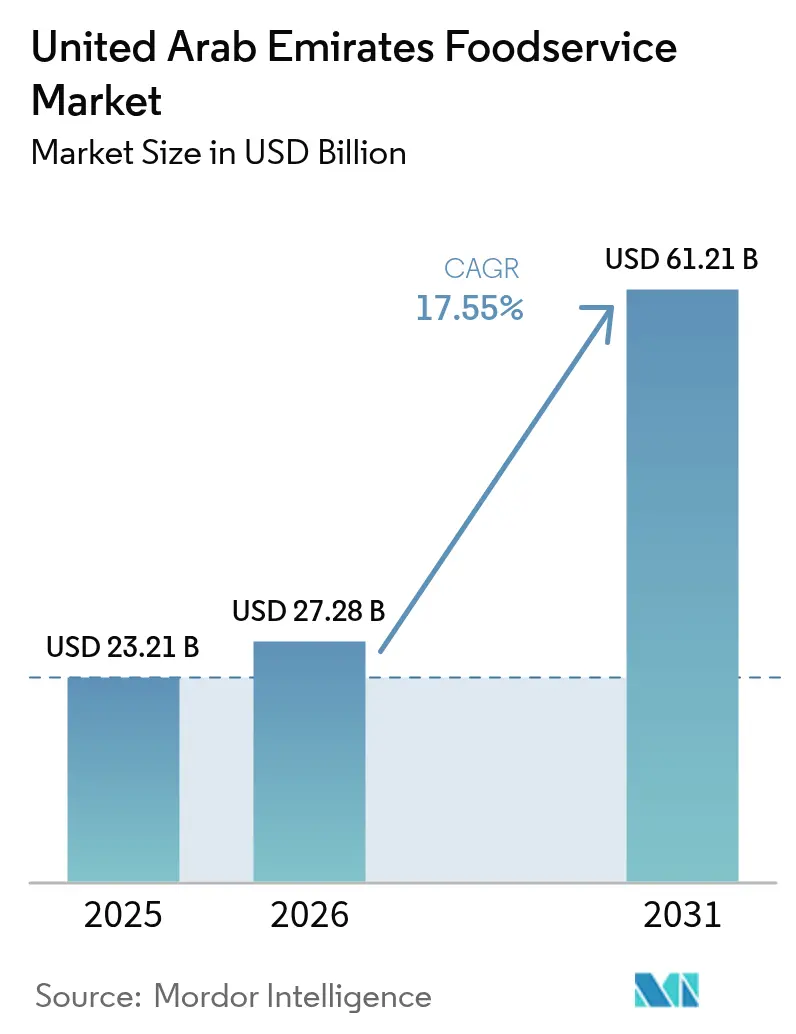

| Base Year Market Size (2025) | USD 23.21 Billion |

| Market Size (2026) | USD 27.28 Billion |

| Market Size (2031) | USD 61.21 Billion |

| Growth Rate (2026 - 2031) | 17.55% CAGR |

| Fastest Growing Market | Full Service Restaurants |

| Largest Market | Quick Service Restaurants |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Arab Emirates Foodservice Market Analysis by Mordor Intelligence

The United Arab Emirates foodservice market size is expected to grow from USD 23.21 billion in 2025 to USD 27.28 billion in 2026 and is forecast to reach USD 61.21 billion by 2031 at 17.55% CAGR over 2026-2031. Rising disposable income and changing consumer lifestyles have increased the frequency of dining out and spending on premium food experiences. The growing number of dual-income households and urban professionals has created a higher demand for convenient food options, including takeaway and delivery services. The adoption of digital technologies, such as online ordering platforms, contactless payments, and loyalty programs, has improved customer engagement and operational efficiency. Government initiatives focused on food security, sustainability, and innovation have created a supportive environment for market expansion. The development of luxury hotels and resorts has strengthened the full-service and lodging-based foodservice segments. Additionally, increasing health consciousness, demand for plant-based options, and social media influences continue to shape consumer preferences in the market.

Key Report Takeaways

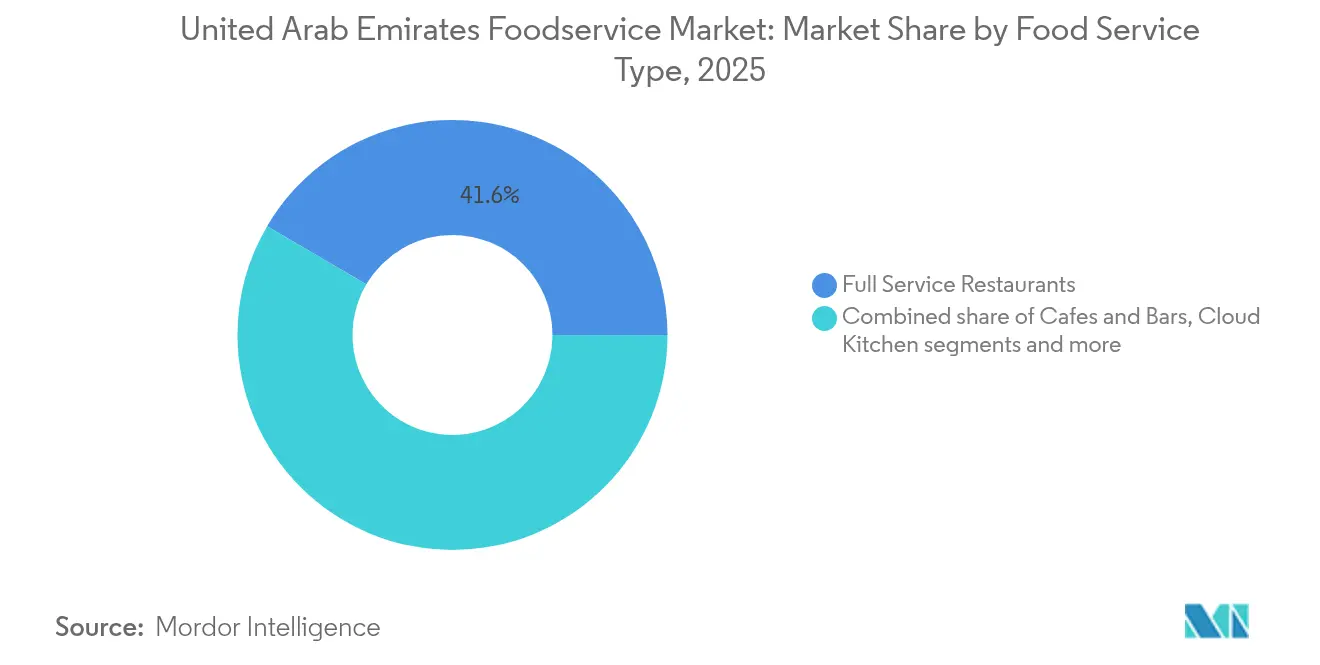

- By foodservice type, Full Service Restaurants led with 41.55% revenue share of the United Arab Emirates food service market in 2025, while Quick Service Restaurants are forecast to post a 19.55% CAGR through 2031.

- By outlet, Independent operators held 59.60% of the United Arab Emirates food service market share in 2025; Chained outlets recorded the fastest expansion at an 18.05% CAGR.

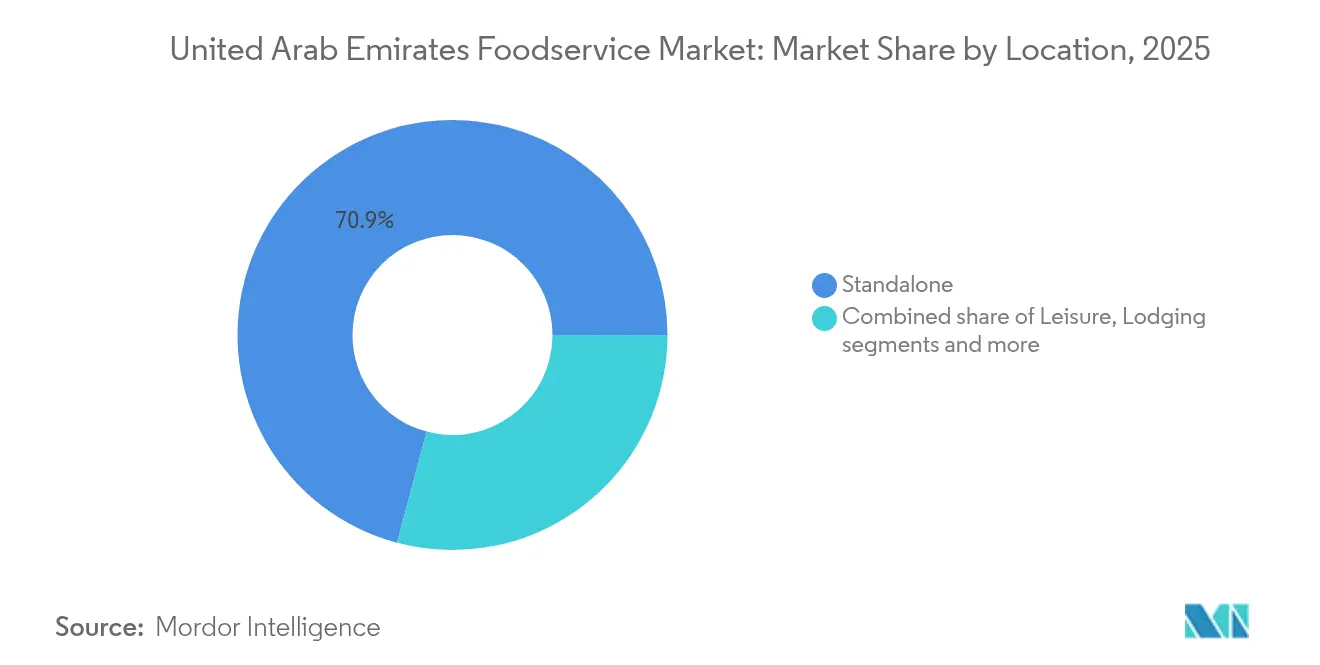

- By location, Standalone venues captured 70.85% share of the United Arab Emirates food service market size in 2025, whereas lodging-based outlets are advancing at a 20.10% CAGR.

- By service type, Dine-In accounted for 55.05% of the United Arab Emirates food service market in 2025, yet Delivery is increasing at 18.65% CAGR through 2031.\

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cultural diversity and expatriate population | +4.2% | United Arab Emirates - wide, concentrated in Dubai and Abu Dhabi | Long term (≥ 4 years) |

| Rise of cloud kitchens and virtual brands | +3.8% | Dubai, Abu Dhabi, Sharjah | Medium term (2-4 years) |

| Surge in plant-forward concepts targeting health-conscious consumers | +2.9% | United Arab Emirates - wide, premium segments | Medium term (2-4 years) |

| Social media and celebrity influence | +2.1% | United Arab Emirates - wide, youth demographics | Short term (≤ 2 years) |

| Strategic location and international connectivity | +1.7% | United Arab Emirates - wide, trade corridors | Long term (≥ 4 years) |

| Events, conferences, and business tourism | +1.5% | Dubai, Abu Dhabi | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cultural Diversity and Expatriate Population

The United Arab Emirates foodservice market is driven by its cultural diversity and large expatriate population, which influences demand across various segments. The country's diverse ethnic communities contribute distinct culinary preferences and dining habits. This multicultural environment creates opportunities for foodservice providers to serve various cuisines, including Middle Eastern, Asian, European, Latin American, and fusion offerings. The diverse consumer base generates demand for both authentic ethnic dining and international restaurant chains, prompting operators to adapt their menus and services. Foodservice outlets differentiate themselves by targeting specific expatriate groups with customized offerings and culturally appropriate atmospheres to build customer loyalty. As of 2024, the United Arab Emirates hosts over 3.5 million Indians, according to the Ministry of External Affairs [1]Source: Ministry of External Affairs, "Number of overseas Indians in United Arab Emirates", mea.gov.in. This significant Indian expatriate community influences foodservice demand through their preference for Indian cuisine, contributing to growth in full-service restaurants, quick-service outlets, and cloud kitchens specializing in Indian food.

Rise of Cloud Kitchens and Virtual Brands

Cloud kitchens and virtual brands are driving significant changes in the United Arab Emirates foodservice market by transforming food preparation, marketing, and delivery methods. Cloud kitchens operate without dine-in facilities and focus on online order fulfillment, which reduces real estate and staffing costs. This operational model enables businesses to scale operations efficiently and test new menu items while managing multiple brands from one kitchen location. Virtual brands use digital platforms and social media for direct customer engagement, meeting the needs of technology-oriented consumers who value convenience and diverse food options. These developments reflect evolving consumer preferences, particularly among younger customers who favor online ordering, home delivery, and contactless payment options. In March 2023, Talabat demonstrated this market evolution by launching Talabat Kitchen at its tech headquarters in City Walk, Dubai. The facility combines delivery operations with an experiential dine-in space, showcasing the integration of technology with food service while offering customers an interactive dining experience.

Surge in Plant-Forward Concepts Targeting Health-Conscious Consumers

The growth of plant-forward dining concepts targeting health-conscious consumers is transforming the United Arab Emirates foodservice market. The increasing awareness of health, environmental, and ethical benefits of plant-based diets has increased demand for vegetarian, vegan, and flexitarian options across foodservice segments. Consumers seek nutritious, sustainable menu options that align with their wellness goals and lifestyle choices. This trend requires foodservice providers to expand their menus with plant-based dishes that maintain taste and presentation quality, appealing to both plant-based eaters and those reducing meat consumption. Plant-forward concepts emphasize fresh, locally sourced, and organic ingredients, supporting sustainability initiatives that resonate with environmentally conscious United Arab Emirates customers. In August 2024, Veggie Mania introduced GALA, Abu Dhabi's first gourmet vegetarian dining experience. GALA's dishes feature distinctive plating techniques that position vegetarian cuisine in the fine dining category. This launch demonstrates the market potential for premium plant-based dining concepts that appeal to customers interested in health, wellness, and experiential dining.

Social Media and Celebrity Influence

Social media and celebrity influence have become significant drivers in the United Arab Emirates foodservice market, shaping consumer behavior and brand visibility. Foodservice brands engage with their audience through targeted marketing campaigns, influencer collaborations, and content that showcases new menu items, dining experiences, and brand stories. Celebrity endorsements generate media coverage and increase foot traffic while enhancing brand prestige. Restaurants now focus on creating visually appealing dishes and experiences suitable for social media sharing, recognizing that customers value this aspect of their dining experience. Brands that effectively utilize social media and celebrity partnerships strengthen their market position and customer loyalty in the United Arab Emirates foodservice landscape. For example, in October 2025, actress Kangana Ranaut attended the launch of Puranmal's new flagship restaurant in Dubai, demonstrating how celebrity involvement generates interest in new foodservice establishments through social media channels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply chain and import dependency | -2.8% | United Arab Emirates - wide, critical for specialized ingredients | Long term (≥ 4 years) |

| Skilled labor shortage | -2.1% | United Arab Emirates - wide, acute in Dubai and Abu Dhabi | Medium term (2-4 years) |

| High real estate and rental costs | -1.9% | Dubai, Abu Dhabi prime locations | Medium term (2-4 years) |

| Limited operating hours in certain areas | -0.7% | Specific municipal zones, heritage areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supply Chain and Import Dependency

The United Arab Emirates foodservice market faces constraints due to supply chain challenges and import dependency. The country's limited agricultural capacity and harsh climate necessitate heavy reliance on imported raw materials, ingredients, and food products. This dependence makes the foodservice sector susceptible to global supply chain disruptions, geopolitical tensions, and changes in international trade policies. Supply chain issues, including shipping delays and increased freight costs, raise operational expenses for foodservice operators, affecting their menu pricing and profit margins. The sector's reliance on imports also requires strict monitoring of quality control, food safety standards, and regulatory compliance to maintain consumer trust. These challenges limit market growth by increasing operational costs and creating supply uncertainties, compelling operators to develop backup plans and diversify their sourcing strategies to enhance operational resilience, market sustainability, long-term business continuity, and overall supply chain efficiency.

Skilled Labor Shortage

The United Arab Emirates food service sector faces significant labor challenges, with operators experiencing difficulties in hiring qualified staff due to rising wage expectations and competition from other hospitality sectors. The workforce shortage is particularly evident in specialized roles that require culinary expertise, language proficiency, and cultural understanding to serve the diverse customer base. The implementation of Emiratization policies presents additional challenges, requiring operators to balance local hiring mandates with available skill sets, resulting in extended training periods and increased onboarding costs. The competition from technology and finance sectors has increased salary expectations for customer-facing positions, while immigration policy changes and visa processing delays create recruitment challenges. In response, operators are investing in automation technologies and simplified service models to reduce staffing needs, though these solutions require substantial capital investment and may affect service quality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foodservice Type: QSR Acceleration Reshapes Dining Landscape

Full Service Restaurants (FSR) dominate the United Arab Emirates Food Service Market with a 41.55% market share in 2025. These establishments serve as the cornerstone of the country's foodservice market, delivering sophisticated dining experiences that cater to both residents and international tourists. The segment's robust expansion is propelled by rising disposable income levels, a rapidly growing expatriate community, and flourishing tourism activities. Full-service restaurants encompass an extensive range of dining options, from premium fine dining establishments to authentic traditional ethnic restaurants, solidifying the country's status as a premier global dining destination. The segment sustains its growth trajectory through innovative culinary offerings, exceptional service standards, and strategically positioned locations in prime commercial areas, particularly within the vibrant cities of Dubai and Abu Dhabi.

The Quick Service Restaurant (QSR) market in the United Arab Emirates is growing at a CAGR of 19.55% through 2031. This growth stems from changing consumer preferences and digital transformation in the food service industry. The demand for Quick Service Restaurant services is driven by urban consumers, including professionals, families, and expatriates, who seek convenient and affordable dining options. QSR operators are expanding their menus to include healthy alternatives and regional flavors while offering customization options to meet diverse consumer preferences. The market expansion is further supported by both international and local Quick Service Restaurant chains establishing new outlets across standalone locations and shopping malls to meet the increasing demand for quick dining solutions.

By Outlet: Chained Growth Challenges Independent Dominance

Independent outlets command a substantial 59.60% market share in 2025, demonstrating the country's robust entrepreneurial ecosystem and deeply embedded cultural preferences. Local operators maintain a competitive edge over international chains by delivering authentic, personalized dining experiences that resonate with diverse expatriate communities and local tastes. These independent establishments excel in crafting distinctive menus, incorporating regional flavors, and providing highly customized service offerings. Their exceptional ability to adapt swiftly to evolving consumer preferences and introduce innovative, specialized concepts for various demographic segments reinforces their market dominance. The country's business-friendly regulatory framework and passionate community of restaurant operators continue to drive the independent segment's growth and success.

Chained outlets in the United Arab Emirates foodservice market demonstrate remarkable expansion potential with a projected CAGR of 18.05% through 2031. International franchises are significantly intensifying their investments to capitalize on the country's sophisticated and high-income consumer base. These businesses implement comprehensive standardized operational systems that enable efficient scaling while maintaining exceptional service consistency. Their well-established business models, incorporating sophisticated supply chain networks, intensive staff training programs, and advanced technological solutions, facilitate successful expansion across premium malls, thriving business districts, and densely populated urban centers throughout the United Arab Emirates.

By Location: Lodging Surge Reflects Tourism Infrastructure Boom

Standalone locations dominate the United Arab Emirates foodservice market with a 70.85% market share in 2025. This dominance stems from their strategic advantages, including lower rental costs in suburban and less populated areas compared to urban shopping malls or commercial centers. The reduced rent expenses enable standalone operators to invest more in food quality, service, and customer experience. These locations also offer greater flexibility in layout design and space optimization, allowing for larger kitchens, dedicated delivery zones, and customized dining areas. This adaptability helps operators efficiently manage various business models, from casual eateries to specialized dining concepts.

Lodging-based foodservice outlets are experiencing the fastest growth in the sector, with a projected CAGR of 20.10% through 2031. This growth aligns with the expansion of the UAE hospitality industry, driven by increasing tourist arrivals and business travel. The United Arab Emirates Ministry of Economy & Tourism reported approximately 15.3 million hotel guests across the seven emirates during the first six months of 2024, showing a 10.5% increase from the previous year . This rise in hotel occupancy increases demand for diverse dining options within lodging establishments, from luxury restaurants to casual cafes and bars. Hotels and resorts have expanded their foodservice offerings through premium dining experiences, themed restaurants, and multi-cuisine venues to meet guest preferences.

By Service Type: Delivery Revolution Transforms Consumer Behavior

Dine-In experiences held a dominant 55.05% market share in the United Arab Emirates foodservice market in 2025, reflecting the country's vibrant social dining culture and consumer preference for experiential consumption. Dining out serves as a platform for socializing, networking, and celebrating special moments, driving consumers to pay premium prices for high-quality, immersive dining experiences. The segment thrives due to the country's multicultural population, where families, friends, and business professionals regularly visit restaurants, cafes, and bars to enjoy the atmosphere and hospitality. Premium full-service restaurants enhance this trend by offering curated menus, themed interiors, entertainment, and personalized services.

Delivery services are growing at a CAGR of 18.65% through 2031, indicating a significant shift in consumer behavior driven by technology adoption, urbanization, and lifestyle changes. The widespread adoption of smartphones and mobile apps, combined with digital payment solutions, has increased the accessibility of food delivery services, particularly among younger consumers. Urban lifestyles characterized by busy work schedules and preferences for at-home dining have increased delivery demand. The emergence of cloud kitchens and virtual restaurants has expanded delivery-only food options, enabling operators to serve urban centers efficiently without traditional dine-in spaces.

Geography Analysis

The United Arab Emirates food service market shows concentrated growth in Dubai and Abu Dhabi, driven by tourism infrastructure investments and economic diversification initiatives. Dubai's status as a global destination creates consistent demand for diverse dining options that balance international preferences with cultural authenticity. The emirate's events and conferences generate predictable demand patterns, enabling operators to optimize pricing and operations. Additionally, developments like Dubai Food Tech Valley provide supply chain benefits for food service businesses. Abu Dhabi's focus on luxury tourism and cultural experiences increases demand for premium dining, supported by the UAE National Food Security Strategy 2051, which aims to enhance local production and reduce import dependence .

Sharjah and the Northern Emirates offer expansion opportunities for operators seeking reduced real estate costs while maintaining access to Dubai's workforce and supply chain infrastructure. This geographic expansion aligns with consumer preferences for community-based dining and helps operators manage rising rental costs in Dubai and Abu Dhabi's prime locations. Operators must navigate distinct licensing requirements set by Dubai Municipality and the Abu Dhabi Tourism Authority when planning multi-emirate expansions.

The United Arab Emirates position as a regional hub benefits food service operators targeting GCC market expansion, with many using United Arab Emirates operations to test concepts for broader Middle East entry. Regional supply chain integration allows efficient ingredient sourcing while maintaining quality and cost effectiveness. However, the market's geographic concentration makes it susceptible to economic and tourism fluctuations, affecting demand across multiple locations simultaneously. This requires operators to implement diverse revenue strategies and adaptable operational models.

Competitive Landscape

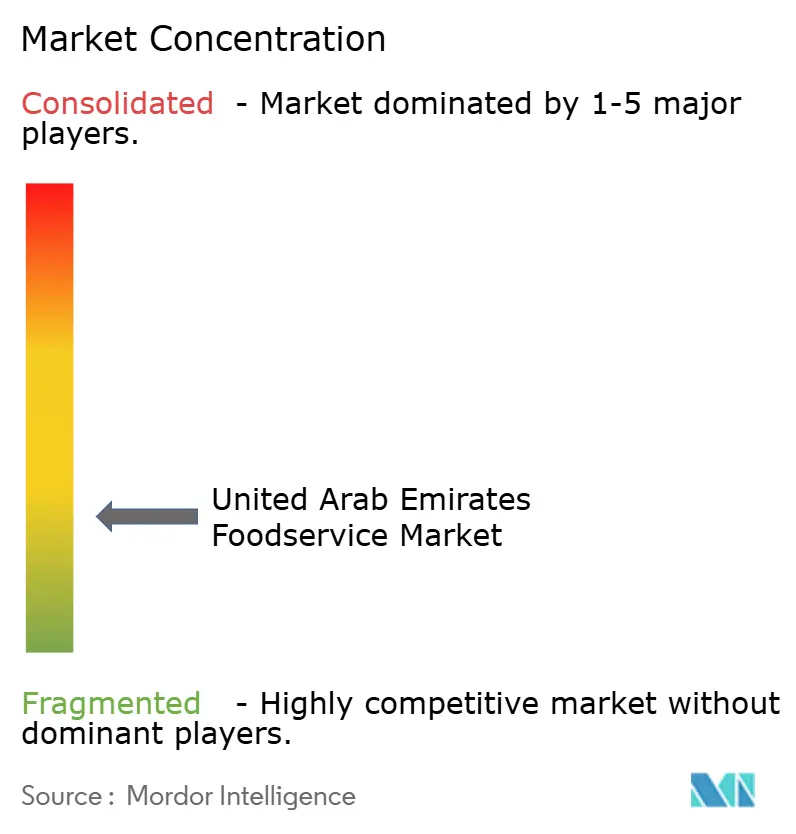

The United Arab Emirates food service market shows moderate fragmentation, characterized by regional players competing with international franchises and technology-driven new entrants. The market's limited concentration stems from cultural diversity, which creates multiple niche segments supporting specialized operators. Prime location scarcity acts as a significant entry barrier, benefiting established businesses. Companies like Americana Restaurants and Apparel Group maintain their competitive positions through extensive regional networks and established supply chains. However, they face competition from cloud kitchen operators who can launch new food concepts without substantial real estate investments.

The market's competitive dynamics increasingly focus on technology integration, with operators implementing AI-based ordering systems, delivery optimization tools, and customer data analytics to enhance operations and customer experience. These technological advancements enable businesses to streamline their operations, reduce costs, and provide personalized dining experiences. Successful operators leverage data-driven insights to optimize menu offerings, pricing strategies, and delivery routes, creating operational efficiencies across their service networks.

Growth opportunities exist in suburban areas and health-focused food concepts, as operators target underserved population segments while avoiding oversaturated premium markets. Virtual brand operators and delivery-focused businesses are disrupting traditional models through digital-first approaches and scalable expansion strategies that minimize physical infrastructure. This shift towards suburban markets and specialized concepts allows operators to capture new customer segments while maintaining profitable operations through optimized cost structures and targeted marketing initiatives.

United Arab Emirates Foodservice Industry Leaders

-

Americana Restaurants International PLC

-

Apparel Group

-

Al Khaja Group Of Companies

-

Alamar Foods Company

-

The Olayan Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Brunch & Cake, an all-day dining chain, opened its sixth location at Palm Jumeirah Mall. The 206-square-meter restaurant, situated on Level 01, serves the brand's signature menu featuring brunch dishes, all-day dining options, and fresh-baked pastries including croissants, cookies, and cakes.

- July 2025: Little Caesars opened its first restaurant in the United Arab Emirates, offering large classic pizzas including pepperoni, veggie, and cheese varieties. The Dubai opening represents a significant step in Little Caesars' international expansion.

- June 2025: Papa John's introduced a Croissant Pizza in the United Arab Emirates, featuring a flaky, buttery croissant-style dough base. The new product combines traditional pizza toppings with a pastry-like crust texture.

- March 2025: Vietnamese Foodies has opened their largest restaurant in Dubai. The menu features signature dishes, such as the 14-hour bone broth and Vit Nuong Hoisin grilled duck breast. The restaurant offers a variety of house-made drinks, including authentic Vietnamese coffees and teas.

United Arab Emirates Foodservice Market Report Scope

Cafes & Bars, Cloud Kitchen, Full Service Restaurants, Quick Service Restaurants are covered as segments by Foodservice Type. Chained Outlets, Independent Outlets are covered as segments by Outlet. Leisure, Lodging, Retail, Standalone, Travel are covered as segments by Location.

By Foodservice Type

| Cafes and Bars | By Cuisine | Bars and Pubs |

| Cafes | ||

| Juice/Smoothie/Dessert Bars | ||

| Specialist Coffee and Tea Shops | ||

| Cloud Kitchen | ||

| Full Service Restaurants | By Cuisine | Asian |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other FSR Cuisines | ||

| Quick Service Restaurants | By Cuisine | Bakeries |

| Burger | ||

| Ice Cream | ||

| Meat Based Cuisines | ||

| Pizza | ||

| Other QSR Cuisines |

By Outlet

| Chained Outlets |

| Independent Outlets |

By Location

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

By Service Type

| Dine-In |

| Takeaway |

| Delivery |

| By Foodservice Type | Cafes and Bars | By Cuisine | Bars and Pubs |

| Cafes | |||

| Juice/Smoothie/Dessert Bars | |||

| Specialist Coffee and Tea Shops | |||

| Cloud Kitchen | |||

| Full Service Restaurants | By Cuisine | Asian | |

| European | |||

| Latin American | |||

| Middle Eastern | |||

| North American | |||

| Other FSR Cuisines | |||

| Quick Service Restaurants | By Cuisine | Bakeries | |

| Burger | |||

| Ice Cream | |||

| Meat Based Cuisines | |||

| Pizza | |||

| Other QSR Cuisines | |||

| By Outlet | Chained Outlets | ||

| Independent Outlets | |||

| By Location | Leisure | ||

| Lodging | |||

| Retail | |||

| Standalone | |||

| Travel | |||

| By Service Type | Dine-In | ||

| Takeaway | |||

| Delivery | |||

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms