Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

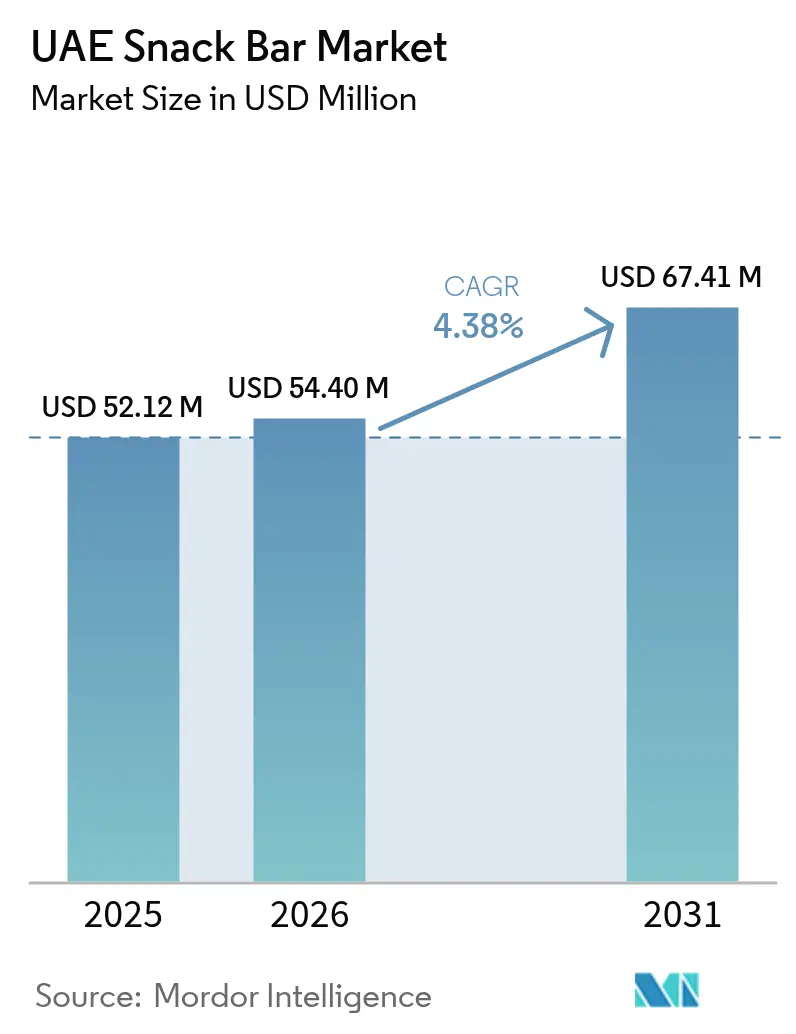

| Base Year Market Size (2025) | USD 52.12 Million |

| Market Size (2026) | USD 54.4 Million |

| Market Size (2031) | USD 67.41 Million |

| Growth Rate (2026 - 2031) | 4.38% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

UAE Snack Bar Market Analysis by Mordor Intelligence

UAE snack bar market size in 2026 is estimated at USD 54.4 million, growing from 2025 value of USD 52.12 million with 2031 projections showing USD 67.41 million, growing at 4.38% CAGR over 2026-2031. This growth is driven by supportive national nutrition policies, increasing disposable incomes, and a health-conscious population willing to invest more in wellness. For instance, as of September 2023, the Statistics Centre – Abu Dhabi reported approximately 1.15 million white-collar jobs in the emirate[1]Source: Statistics Centre – Abu Dhabi, "Employment in the emirate of Abu Dhabi", www.census.scad.gov.ae. Product development and retail assortments are being reshaped by clean-label claims, government-backed sugar-reduction targets, and corporate wellness programs. The expanding digital retail infrastructure in the UAE snack bar market is complemented by a consumer push for sustainable packaging, prompting brands to invest in recyclable and compostable materials. As fitness culture gains traction, there's a heightened demand for protein-enriched snacks and a surge in localized flavor innovations, blending Middle Eastern ingredients with Western bar formats. The market is fiercely competitive, with multinational, regional, and emerging local brands vying for dominance. While mass-market SKUs lead in volume, premium lines are witnessing faster value growth.

Key Report Takeaways

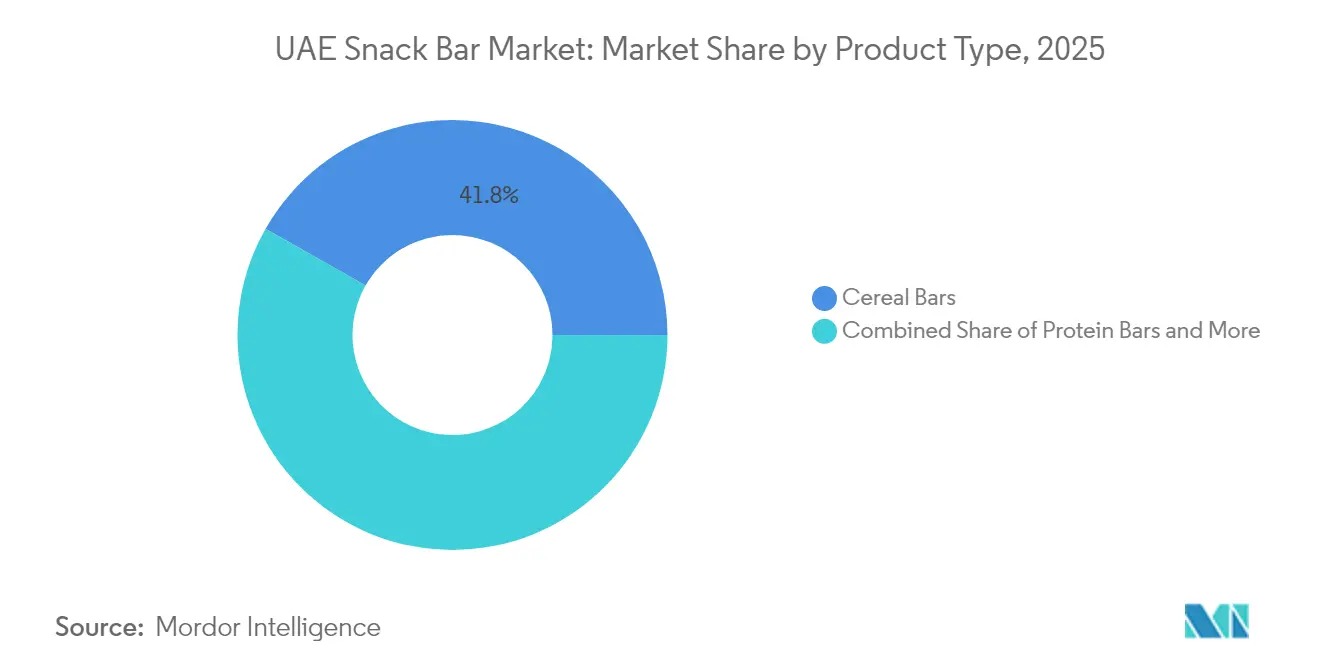

- By product type, cereal bars led with a 41.78% revenue share in 2025, while protein bars are projected to clock a 5.12% CAGR through 2031.

- By category, conventional offerings held 87.05% of the UAE snack bar market share in 2025; the organic segment is set to expand at a 5.55% CAGR to 2031.

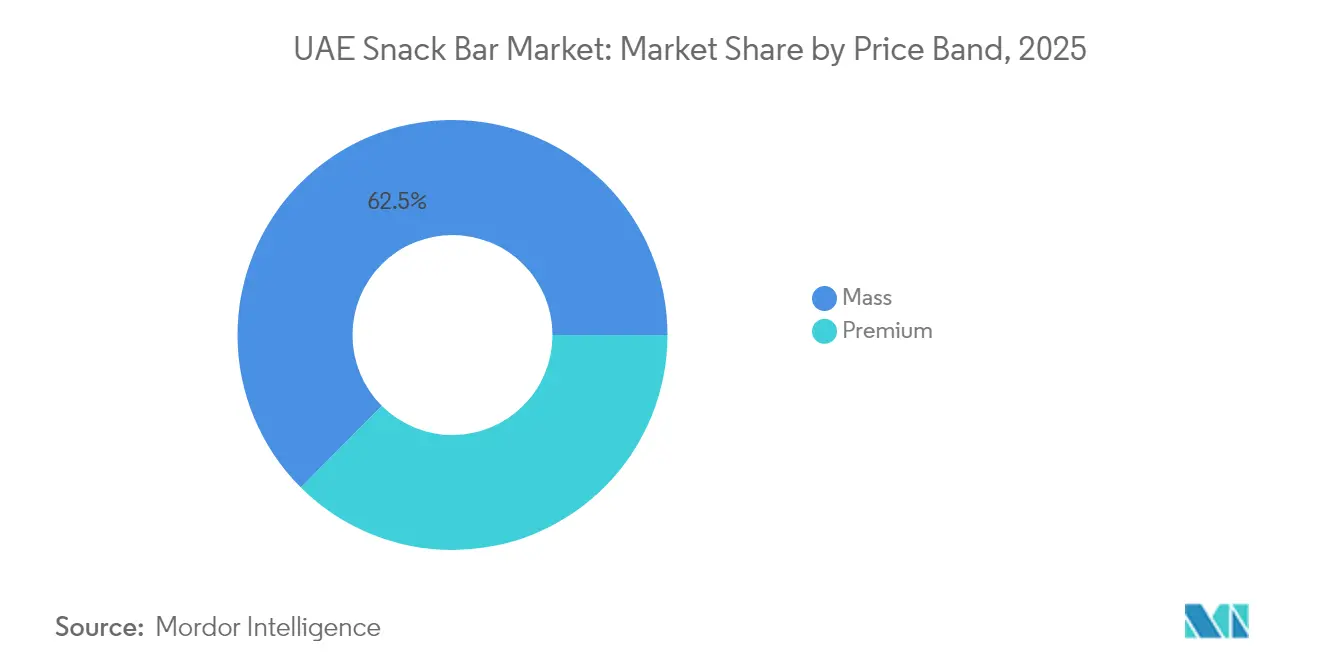

- By price band, mass-market lines accounted for 62.54% of the UAE snack bar market size in 2025, whereas premium products are advancing at a 5.92% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets captured 48.12% of 2025 sales; online channels are positioned for the highest growth at a 6.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Snack Bar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing health and wellness consciousness | +1.1% | UAE nationwide, concentrated in Dubai and Abu Dhabi | Medium term (2-4 years) |

| Expansion of fitness culture | +0.8% | UAE urban centers spill over to the Northern Emirates | Short term (≤ 2 years) |

| Product innovation and variety | +0.7% | UAE nationwide, with early adoption in metropolitan areas | Medium term (2-4 years) |

| Attractive and sustainable packaging | +0.6% | UAE nationwide, aligned with Vision 2071 sustainability goals | Long term (≥ 4 years) |

| Targeting of specific dietary needs | +0.5% | UAE expatriate communities and health-conscious nationals | Medium term (2-4 years) |

| Influence of Western snacking culture | +0.4% | UAE expatriate populations, urban millennials | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Health and Wellness Consciousness

In the UAE, a systematic public health transformation is reshaping snack consumption patterns, driven by government initiatives that are yielding measurable shifts in consumer behavior. The UAE Ministry of Health reports that the National Nutrition Strategy 2030 is pushing for reduced sugar content across various food categories[2]Source: UAE Ministry of Health, "National Nutrition Strategy 2030", www.u.ae. Concurrently, the National Policy to Promote Healthy Lifestyles is setting the stage for healthier product positioning. Notably, UAE consumers are now gravitating towards products that champion wellbeing, marking a shift from mere consumption to deliberate nutritional choices. This heightened awareness isn't limited to personal choices; it's influencing institutional procurement as well. Federal entities, through digital procurement platforms introduced in 2025, are increasingly leaning towards healthier snack options. Workplace wellness programs further amplify this trend, with employers promoting healthier eating habits as a strategy to cut healthcare costs and boost productivity.

Expansion of Fitness Culture

As gym memberships soar to unprecedented levels in urban centers, the UAE's expanding fitness infrastructure is fueling a growing demand for performance-oriented snack products. Strength training's rising popularity among UAE residents has led to a notable uptick in the consumption of protein bars and functional snacks. Bolstered by government investments in sports facilities and fitness programs, and a parallel expansion from the private sector, the UAE has cultivated a thriving ecosystem that champions active lifestyles. Take, for example, the Dubai Fitness Challenge (DFC) launched by His Highness Sheikh Hamdan bin Mohammed bin Rashid Al Maktoum. In October and November 2024, the DFC urged participants to engage in 30 minutes of exercise daily for 30 straight days, further embedding fitness into the UAE's cultural fabric. Corporate wellness programs are now marrying fitness tracking with nutritional advice, fostering a more informed consumer base that recognizes the significance of snack bars in their workout regimens. This cultural evolution is especially evident among the UAE's youthful expatriate community, where fitness engagement outpaces regional norms, leading to a penchant for premium products, even at a premium price.

Product Innovation and Variety

In the UAE, manufacturers are tapping into regional flavor preferences to craft products that resonate with the country's rich cultural tapestry. The meteoric rise of Dubai's chocolate flavor, which melds pistachio with kataifi pastry, has paved the way for snack bars that artfully combine Middle Eastern ingredients with Western styles. A case in point is Per4m's debut of Dubai Chocolate protein bars in February 2025, catering to those who crave familiar tastes in a functional format. But innovation isn't just about flavor; it's also about meeting dietary needs. This includes halal certifications, sugar-free options, and plant-based substitutes, all tailored for the UAE's religiously diverse populace. Furthermore, packaging now boasts Arabic labels and portion sizes that resonate with local habits, all while upholding international quality standards to attract expatriates.

Attractive and Sustainable Packaging

In the UAE snack bar market, a surge in environmental consciousness is reshaping packaging norms. Consumers are increasingly gravitating towards sustainable packaging, echoing the UAE's Vision 2071 sustainability goals. Highlighting this industry shift, Tetra Pak and Union Paper Mills unveiled a AED 2.5 million carton recycling initiative in November 2024, underscoring their commitment to circular economy principles. Further emphasizing this trend, Dubai Municipality's 2025 regulations demand heightened recyclability and a reduction in plastic content across food packaging[3]Source: Dubai Municipality, "Dubai Municipality issues guidance for businesses on single use plastics ban", www.dm.gov.ae. In response, brands are adopting compostable wrappers, minimalist designs to curtail material use, and bilingual recycling instructions in Arabic and English. This pivot towards sustainability not only sets brands apart in a competitive landscape but also resonates deeply with consumers, especially the younger demographic, who prioritize environmental responsibility in their purchasing choices.

Restrains Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from traditional snacks and fresh alternatives | -0.6% | UAE nationwide, stronger in culturally traditional areas | Short term (≤ 2 years) |

| High-cost barrier for niche and premium products | -0.5% | UAE price-sensitive segments, Northern Emirates | Medium term (2-4 years) |

| Market fragmentation and intense competition | -0.4% | UAE retail channels, concentrated in hypermarkets | Short term (≤ 2 years) |

| Shelf-life challenges for clean-label products | -0.3% | UAE supply chain, import-dependent segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from Traditional Snacks and Fresh Alternatives

In the UAE, cultural celebrations and social gatherings see a strong preference for traditional Arabic sweets and fresh alternatives, putting consistent pressure on packaged snack bars. Options like dates, nuts, and homemade sweets not only hold deep cultural significance but also often come with better price points and a perception of being more natural. While the GCC confectionery market sees growth in chocolate segments, it underscores a continued preference for familiar indulgences over functional alternatives. Retail channels in the UAE offer fresh fruits year-round, presenting a naturally nutritious choice that directly competes with health-focused snack bars. Furthermore, the food safety frameworks set by Dubai Municipality favor established traditional producers, who have adeptly navigated local certification processes, thus creating hurdles for new entrants in the snack bar market.

High-Cost Barrier for Niche and Premium Products

Despite rising health consciousness and increasing disposable incomes, UAE consumers remain price-sensitive, posing challenges for the adoption of premium and specialized snack bar products. The reliance on imported specialized ingredients and packaging materials drives up production costs. Furthermore, the limited market size hinders the realization of economies of scale, which could otherwise help in lowering retail prices. The UAE's diverse expatriate demographic includes segments that are particularly price-conscious, often valuing cost over premium offerings. This trend restricts the market penetration of higher-priced functional products. Additionally, currency fluctuations on ingredient imports from Europe and North America introduce pricing volatility. Retailers, often unable to absorb these fluctuations, frequently pass the increased costs onto consumers, resulting in elevated shelf prices. Moreover, the UAE's fragmented retail landscape amplifies distribution costs, exerting further margin pressure, especially on smaller brands that lack established relationships with major hypermarket chains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Protein Bars Drive Functional Innovation

In 2025, cereal bars command a dominant 41.78% market share, thanks to their familiar formats and widespread acceptance across diverse demographics. Meanwhile, protein bars are on a rapid ascent, projected to grow at a 5.12% CAGR through 2031, fueled by the rising fitness culture and its demand for performance-driven nutrition. This surge in the protein segment underscores the UAE's evolving consumer sophistication towards functional benefits, especially with the growing popularity of strength training and the consequent demand for post-workout recovery products. Fruit and nut bars find their niche in the market, catering to health-conscious consumers who prioritize natural ingredients but prefer to steer clear of overly complex functionalities.

Other snack bars, encompassing specialty and seasonal types, strategically position themselves to cater to specific occasions and dietary needs, thus securing the remaining market share. A notable trend is the introduction of Dubai chocolate flavoring in protein bars, highlighting how regional tastes can set products apart in established categories. Starting in 2025, Dubai Municipality's stringent food safety regulations will favor established manufacturers with solid quality systems. This could lead to a consolidation of market share among larger players, posing challenges for artisanal producers.

By Category: Organic Segment Accelerates Despite Conventional Dominance

In 2025, the conventional category holds a commanding 87.05% share of the market, underscoring a price-sensitive consumer base that leans towards familiar formulations rather than premium options. Yet, amidst this dominance, organic products are carving out a niche, growing at a robust 5.55% CAGR through 2031. This surge is fueled by a rising health consciousness and increasing disposable income among the affluent in the UAE. The growth of the organic segment resonates with the UAE's broader sustainability goals, notably the National Food Security Strategy 2051, which champions sustainable agriculture and clean-label products.

Despite its momentum, the organic segment grapples with challenges: limited local production and a reliance on imports drive up retail prices, making them less accessible to budget-conscious consumers. Yet, the UAE's strategic position as a regional trade nexus allows for the efficient sourcing of organic ingredients from certified suppliers in Europe and North America. Further bolstering the segment, the Emirates Authority for Standardization and Metrology (ESMA) has introduced streamlined organic certification processes, easing compliance costs for manufacturers. Major retailers, like Spinneys, are amplifying organic awareness through initiatives such as their annual Food Trend Report and dedicated organic merchandising, driving trial rates for organic snack bar alternatives.

By Price Band: Premium Growth Reflects Value Evolution

In 2025, mass-market products command a dominant 62.54% share, underscoring the UAE's diverse economic landscape and its consumers' price-sensitive shopping habits. The mass segment thrives on widespread availability in hypermarkets and convenience stores, where impulse buys significantly boost sales. Yet, premium products are on an upward trajectory, boasting a 5.92% CAGR through 2031. This trend signals a growing consumer readiness to invest more for enhanced quality, functional advantages, and brand prestige.

Notably, the premium surge is most pronounced among UAE nationals and affluent expatriates, who place a premium on quality over cost. This segment enjoys exclusive access via specialty health outlets and upscale retail channels, both of which emphasize superior shopping experiences and informed product choices. Lulu Group's 2024 rollout of 12 new stores, paired with bolstered e-commerce capabilities, is making premium products more accessible throughout the UAE. The rising premium segment mirrors a broader shift in UAE consumer behavior, leaning towards quality-centric purchases. This shift is further bolstered by government initiatives championing healthy lifestyles and sustainable consumption.

By Distribution Channel: Digital Transformation Accelerates Online Growth

In 2025, supermarkets and hypermarkets command a dominant 48.12% share of the distribution landscape, capitalizing on their vast footprints and ingrained consumer habits towards packaged goods. Retail giants like Carrefour, Lulu, and Spinneys are not just offering a diverse range of snack bars but are also employing competitive pricing and promotional strategies, fueling the category's growth. Yet, it's the online retail channels that are surging ahead, boasting a robust 6.72% CAGR expansion rate projected through 2031. This growth is buoyed by a remarkable 29% surge in FMCG e-commerce within the UAE and a shift in consumer preferences leaning towards the convenience of online shopping.

Convenience stores and specialty health outlets play distinct yet complementary roles in the retail ecosystem. While convenience stores adeptly capture those spontaneous impulse buys, specialty health stores offer informed guidance on functional products. The rapid growth of online channels can be attributed to advancements in delivery infrastructures. A prime example is Carrefour's newly established regional distribution center, which bolsters cold-chain capabilities for products sensitive to temperature fluctuations. Furthermore, digital procurement platforms, making their debut in 2025, are carving out fresh demand avenues for institutions. Major retailers are also tapping into mobile commerce, enhancing accessibility for younger consumers who value both shopping convenience and a diverse product range.

Geography Analysis

In the UAE, snack bar consumption and innovation are predominantly driven by the emirates of Dubai and Abu Dhabi, reflecting the country's concentrated growth patterns. These metropolitan hubs, bolstered by a diverse expatriate demographic, boast higher disposable incomes and a robust retail infrastructure. This environment not only supports the positioning of premium products but also welcomes the introduction of new categories. As a regional trade nexus, the UAE, particularly with Dubai's re-export center status, ensures competitive pricing for both imported ingredients and finished goods. Furthermore, government initiatives, such as the National Nutrition Strategy 2030, foster a regulatory landscape that champions healthier snacking choices across the nation.

Meanwhile, the northern emirates—Sharjah, Ajman, and Ras Al Khaimah—are emerging as hotspots for growth. Here, a burgeoning retail presence and a heightened health consciousness among residents are fueling the demand for convenient nutritional options. In a nod to these trends, Lulu Group has strategically rolled out 12 new stores in the first nine months of 2024, with a keen focus on these northern markets, enhancing both product accessibility and consumer awareness. The UAE's federal framework allows for synchronized policy execution. A case in point is Dubai Municipality's food safety regulations, set to kick in 2025, which are poised to serve as a benchmark for other emirates aiming to bolster consumer protection and elevate product quality standards.

On a broader scale, the GCC's regional integration unveils further growth avenues, positioning the UAE as a pivotal distribution hub for its neighbors, including Saudi Arabia, Oman, and Qatar. This strategic advantage is underscored by the robust demand for healthier snack alternatives in the wider GCC confectionery and snacks market—a demand that UAE manufacturers are well-placed to meet through astute positioning and streamlined logistics. Moreover, the region's cross-border e-commerce capabilities, coupled with unified food safety standards, pave the way for market expansion. Cultural affinities across the GCC mean that product formulations and marketing strategies tailored for UAE consumers can seamlessly resonate with a broader regional audience.

Competitive Landscape

The UAE snack bar market is moderately fragmented, with fierce competition among international giants, regional players, and emerging local manufacturers. These entities vie for a slice of a burgeoning yet price-sensitive market. Multinational behemoths like Kellogg's, Nestlé, and Mondelēz harness global supply chains and their established brand clout to cement their market foothold. In contrast, regional specialists carve out niches by emphasizing culturally resonant flavors and securing halal certifications. The competitive landscape is further intensified by the low switching costs and the fleeting brand loyalty of price-sensitive consumers. This dynamic paves the way for newcomers armed with enticing value propositions or innovative product strategies.

Strategic trends underscore a growing focus on functional benefits, sustainability, and digital outreach, especially to younger consumers who prioritize health and environmental stewardship. A testament to the market's consolidation trend is Mondelēz International's USD 2 billion takeover of Chipita in January 2025, underscoring a push for broader product portfolios and operational efficiencies.

On the tech front, AI-driven consumer insights are making waves, highlighted by Nestlé's February 2025 partnership with Dubai AI Campus. This collaboration promises sharper product development and pinpointed marketing strategies. Meanwhile, under the stringent food safety regulations of Dubai Municipality, companies boasting robust quality systems gain a competitive edge. In contrast, smaller players grapple with heightened compliance costs, potentially curtailing their market involvement.

UAE Snack Bar Industry Leaders

-

General Mills, Inc.

-

The Simply Good Foods Company

-

Mondelēz International, Inc.

-

Nestlé S.A.

-

The Kellogg's Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Finnforel, in partnership with Lulu Hypermarket, launched its premium LoHi rainbow trout brand in the UAE. This signified an expansion of product categories beyond traditional snack bars within retail settings, as it represented a new line of healthy, sustainable food offerings.

- October 2024: Spinneys signed a long term/landmark partnership to develop a food-processing facility in Dubai’s Food Tech Valley. The local processing/private-label production capacity makes it easier for retailers to develop UAE-made cereal/protein/fruit-and-nut bar SKUs, shorten lead times, lower costs and promote “Made in UAE” snack bars in-store.

- June 2024: Spinneys launched its Saudi expansion plan and opened its first store in Riyadh in June 2024. This regional footprint expansion increased scale and created broader distribution opportunities for Spinneys’ private-label snack bars (SpinneysFOOD) and other snack categories.

- April 2024: Nestlé introduced a "5+1 free" promotional multipack of its Chocapic cereal bar, which became available on Amazon.ae. This was not a new flavor but rather a retail packaging strategy designed to drive sales of an existing product through increased value offerings.

UAE Snack Bar Market Report Scope

Snack bars provide instant energy and nutrition and contain protein and flavoring ingredients. Snack bars are ready-to-eat baked products made with various ingredients such as granola, oats, chocolate, dried fruits, nuts, coconut oil, honey, peanut butter, and others.

The United Arab Emirates snack bar market is segmented into product types and distribution channels. By product type, the market includes cereal bars, energy bars, and other snack bars. Cereal bars are further sub-segmented into granola/muesli bars and other cereal bars. Based on distribution channels, the market is segmented into supermarkets/hypermarkets, convenience/grocery stores, specialty stores, online retail stores, and other distribution channels.

The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| Cereal Bars |

| Fruit & Nut Bars |

| Protein Bars |

| Other Snack Bars |

By Category

| Conventional |

| Organic |

By Price Band

| Mass |

| Premium |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialty Health Stores |

| Online Retail Stores |

| Other Distribution Channels |

| By Product Type | Cereal Bars |

| Fruit & Nut Bars | |

| Protein Bars | |

| Other Snack Bars | |

| By Category | Conventional |

| Organic | |

| By Price Band | Mass |

| Premium | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialty Health Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

How large is the UAE snack bar market today?

The UAE snack bar market size reached USD 54.4 million in 2026 and is projected to climb to USD 67.41 million by 2031.

What is the expected growth rate for UAE snack bars?

The market is forecast to register a 4.38% CAGR between 2026 and 2031 due to supportive health policies and rising fitness trends.

Which product type is growing fastest in UAE snack bars?

Protein bars are expanding at a 5.12% CAGR, propelled by strength-training popularity and demand for performance nutrition.

Are organic snack bars gaining ground in the UAE?

Yes, organic variants are forecast to post a 5.55% CAGR as consumers seek clean-label assurances and retailers widen organic assortments.

How important is e-commerce to snack bar sales in the UAE?

Online channels are the fastest-growing route, advancing at a 6.72% CAGR as FMCG e-commerce volumes jump and mobile shopping uptake rises.

What packaging features influence UAE snack bar purchases?

Eighty-six percent of shoppers prefer sustainable solutions, so compostable wraps and recyclable cartons increasingly sway brand choice.

Page last updated on: