Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

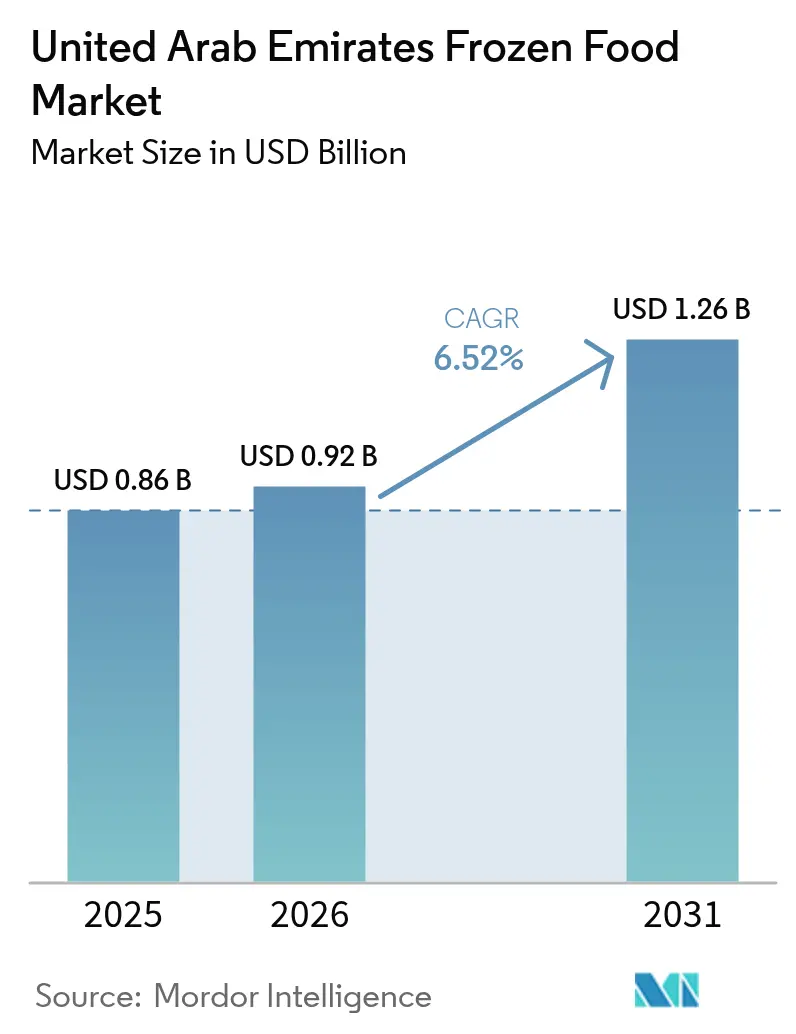

| Base Year Market Size (2025) | USD 0.86 Billion |

| Market Size (2026) | USD 0.92 Billion |

| Market Size (2031) | USD 1.26 Billion |

| Growth Rate (2026 - 2031) | 6.52% CAGR |

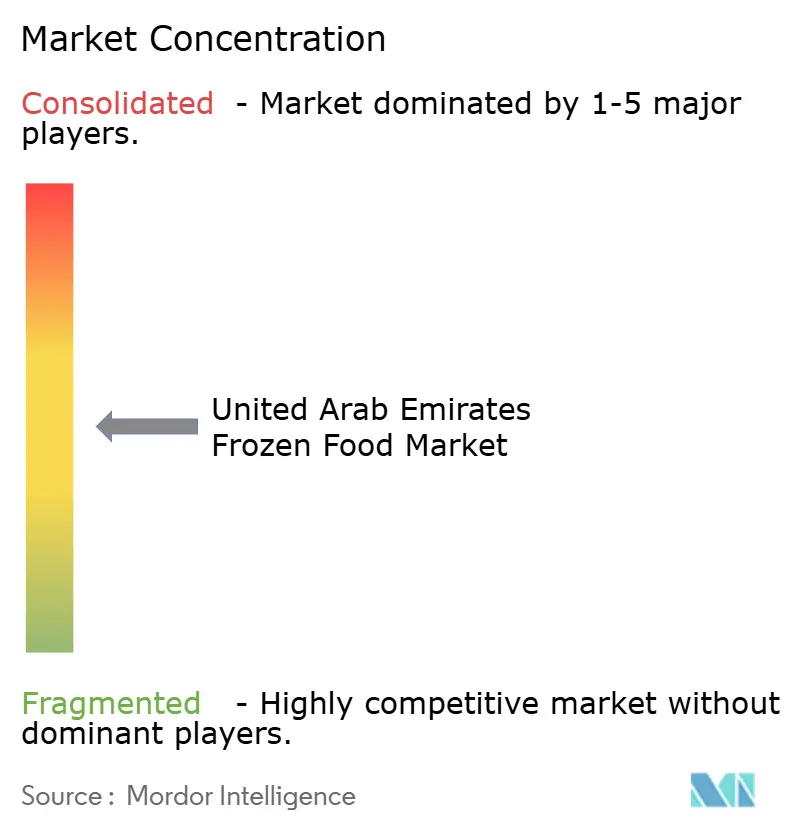

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Arab Emirates Frozen Food Market Analysis by Mordor Intelligence

The United Arab Emirates frozen food market size was valued at USD 0.86 billion in 2025 and estimated to grow from USD 0.92 billion in 2026 to reach USD 1.26 billion by 2031, at a CAGR of 6.52% during the forecast period (2026-2031). Dubai’s dominant consumer base, Sharjah’s logistics-linked expansion, and heavy reliance on halal-certified imports anchor growth. Supermarket penetration, robust e-grocery adoption, and resumed tourism fuel broad-based demand, while cold-chain investments exceeding USD 35 million safeguard temperature integrity and widen national distribution capacity. Food security policies encourage local processing, yet 90% import dependency keeps global sourcing pivotal. Regulatory tightening around ESMA inspections and Dubai’s 2025 single-use plastic ban adds compliance costs. Competitive intensity is moderate as regional leaders Al Islami Foods and IFFCO defend their share against new foreign entrants benefiting from 100% ownership rules.

Key Report Takeaways

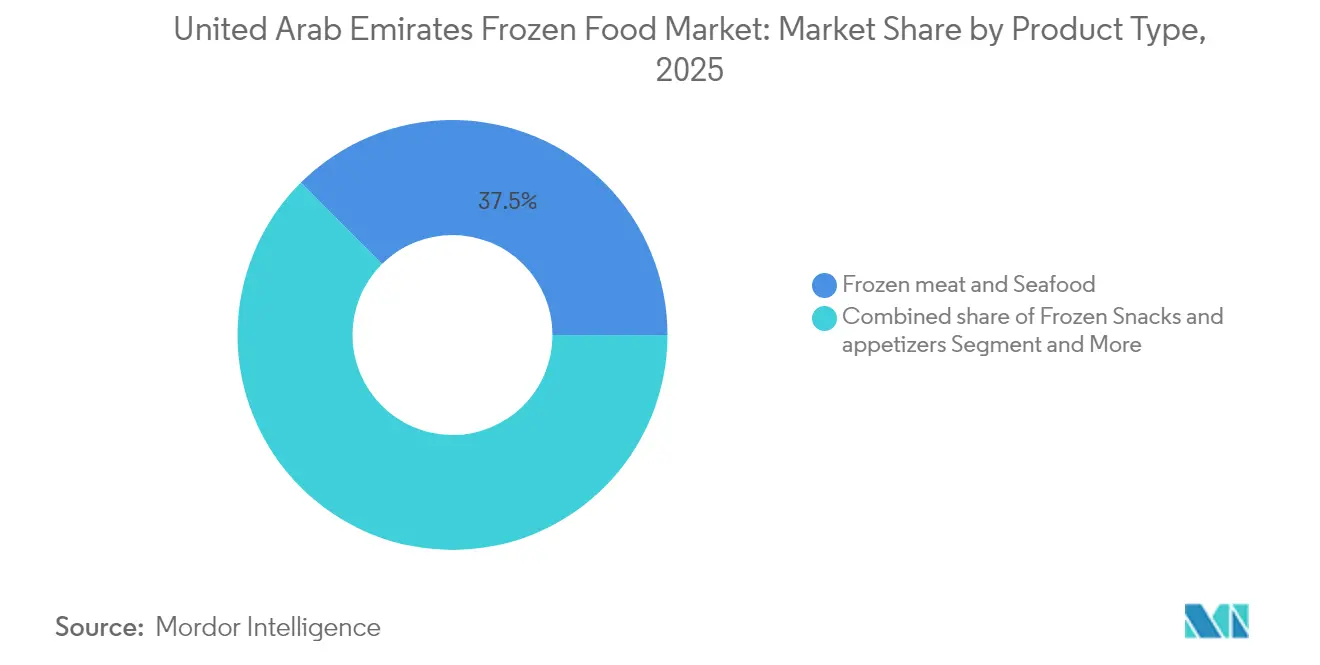

- By product type, frozen meat and seafood led with 37.46% revenue share of the United Arab Emirates frozen food market in 2025; frozen snacks and appetizers are forecast to expand at a 10.95% CAGR through 2031.

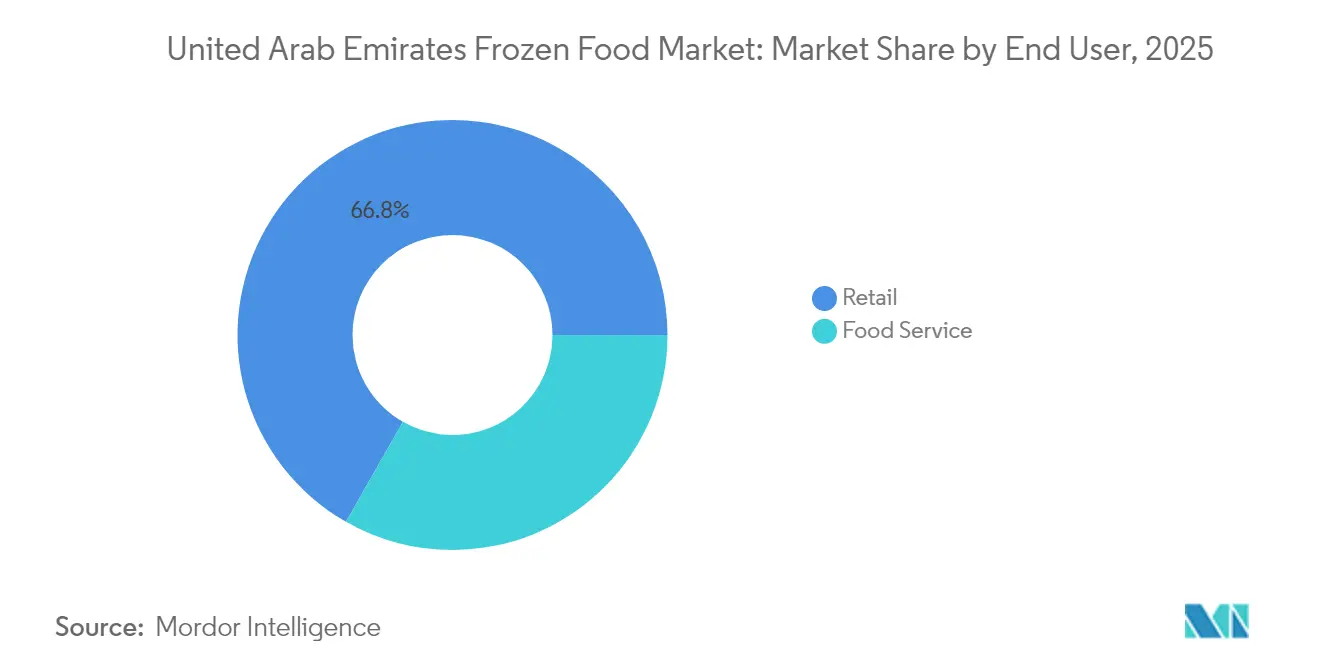

- By end-user, the retail segment accounted for 66.75% of the United Arab Emirates frozen food market share in 2025, while foodservice is advancing at a 9.36% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Frozen Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing expatriate and tourist population fuelling demand for convenient halal-certified frozen meals | +1.2% | Dubai, Abu Dhabi with spillover to Northern Emirates | Medium term (2-4 years) |

| Rapid e-grocery and quick-commerce adoption boosting at-home consumption | +1.8% | Dubai-centric with expansion to Sharjah, Abu Dhabi | Short term (≤ 2 years) |

| Continuous government investment in GDP-linked cold-chain infrastructure (KIZAD, Dubai CommerCity) | +1.5% | Abu Dhabi (KIZAD), Dubai (CommerCity, Jebel Ali) | Long term (≥ 4 years) |

| HoReCa rebound linked to mega events (COP-28 legacy, Dubai Expo spill-over) | +0.9% | Dubai-focused with tourism spillover effects | Medium term (2-4 years) |

| Energy-efficient refrigeration retrofits subsidised by Emirates Water and Electricity Authority | +0.7% | National, with concentrated benefits in Dubai, Abu Dhabi | Medium term (2-4 years) |

| Rising demand for plant-based frozen products from health-conscious residents | +0.6% | Dubai, Abu Dhabi urban centers with expatriate populations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing expatriate and tourist population boosting demand for convenient halal-certified frozen meals

Dubai and Abu Dhabi host dense expatriate communities that prioritize convenience over fresh preparation, driving a steady pull for ready-to-cook frozen products that carry trusted halal stamps. In 2024, the Ministry of Industry and Advanced Technology certified 6,581 halal items, creating a reliable compliance framework that producers leverage for both domestic sales and re-exports.[1]Source: Ministry of Industry and Advanced Technology, "Halal - MOIAT." moiat.gov.ae More than 13,000 food-service outlets in Dubai alone standardize procurement around portion-controlled frozen proteins to match diverse culinary preferences. The Emirates’ 4% GDP growth outlook for 2025 sustains labor inflows that reinforce freezer-aisle demand. As tourist arrivals rebound, hotels increasingly adopt frozen ingredients to guarantee menu consistency, bolstering volumes across meat, bakery, and dessert lines.

Rapid e-grocery and quick-commerce adoption boosting at-home consumption

Online grocery penetration has accelerated as platforms such as Noon and Talabat scale same-day fulfilment networks that preserve cold-chain integrity. Lulu Retail reported a 70% e-commerce revenue surge in 2024, with frozen food one of the fastest-moving categories thanks to packaging formats suited for last-mile ice-box delivery[2]Source: "Lulu Retail reports preliminary FY 2024 results.", gcc.luluhypermarket.com. Hybrid shopping habits, 56% of consumers shop both online and in-store, broaden category visibility and encourage trial of new SKUs. Quick-commerce dark-store models dispatch frozen items within 15 minutes in urban cores, lowering barriers to impulse purchases. These digital channels also generate granular consumption data that suppliers use for targeted assortment planning, improving inventory turns, and reducing wastage.

Government-backed cold-chain investments (KIZAD, Dubai CommerCity)

Capital-intensive projects at Khalifa Industrial Zone, Abu Dhabi, have attracted over AED 173.5 million in logistics spending, including multi-temperature warehouses designed for frozen throughput. In Dubai, DP World and partners added more than 70,000 pallet positions by 2025, underpinning the emirate’s role as a regional re-export hub[3]Source: "Americold Partners with RSA Cold Chain and DP World to Bring a New State-of-the-Art Cold Chain Logistics Platform to Dubai." dpworld.com. IFFCO’s AED 1 billion integrated facility in Dubai Industrial City reduces GCC import reliance and embeds value-added processing close to consumption. Enhanced multimodal connectivity cuts dwell times and freight costs, which vendors pass on via sharper retail pricing. These efficiency gains cushion the United Arab Emirates' frozen food market against global freight volatility.

HoReCa rebound linked to mega-events legacy

The COP-28 legacy and Dubai Expo spill-over have restored hotel occupancy and restaurant footfall, reviving wholesale demand for standardized frozen inputs. Climate-conscious catering pledges push outlets toward plant-based and portion-controlled frozen items, creating niche growth arenas. Quick-service brands such as ALBAIK rely on frozen supply for menu uniformity across new emirate locations. Tourism-led meal volumes flow through central kitchens that favor extended shelf-life inventories, buffering them from fresh-produce price swings. Consequently, the foodservice channel’s growth in the market widens its contribution to the overall United Arab Emirates frozen food market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Emirates Authority for Standardization and Metrology (ESMA) inspections delaying clearance | -0.8% | National, with concentrated impact in Dubai, Abu Dhabi ports | Short term (≤ 2 years) |

| High electricity tariffs for non-efficient legacy cold stores | -0.5% | National, with higher impact in Dubai, Abu Dhabi | Medium term (2-4 years) |

| Consumer perception of lower nutritional value vs. fresh produce | -0.6% | Urban centers with health-conscious demographics | Medium term (2-4 years) |

| Limited domestic agricultural output raises import-price volatility risk | -0.4% | National, with supply chain impacts across all emirates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent ESMA inspections delaying clearance

Enhanced ESMA oversight now requires exhaustive documentation, Arabic-English labeling, and batch traceability, extending port dwell times for temperature-sensitive consignments. Dubai Municipality’s food import portal mandates SKU-level registration, creating administrative burdens for brands with frequent recipe tweaks. Federal Law 10-2015 further obligates risk-assessment records that small importers often find resource-intensive. Clearance delays escalate demurrage and jeopardize product integrity, compelling firms to invest in bonded cold storage or premium freight options. While such controls elevate consumer safety, they temporarily erode margins and can discourage portfolio diversification.

Consumer perception of lower nutritional value versus fresh produce

United Arab Emirates shoppers worry that ultra-processed foods lead some to view frozen options as less wholesome, particularly among high-income expatriates. Retailers have reacted by expanding plant-based and fortified frozen lines, with Spinneys citing a 600% increase in such SKUs. Vertical-farm initiatives like Bustanica supply pesticide-free greens that compete directly with frozen vegetables. Brands respond through transparent provenance storytelling and flash-freezing claims to reassure nutrient retention. Nevertheless, perception gaps persist, requiring sustained education and recipe innovation to protect category share.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Protein Dominance Drives Market Leadership

The frozen meat and seafood category generated 37.46% of the United Arab Emirates frozen food market revenue in 2025, benefiting from established halal supply chains that secure religious compliance for the predominantly expatriate consumer base. Imports fulfill more than 80% of meat demand, making cold-chain reliability essential to preserve quality from source to shelf. Local investment is on the rise. Al Ghurair’s USD 272 million poultry complex is designed to process 10,000 metric tons annually, thereby shortening lead times. Frozen bakery, desserts, and ready meals remain staples for hospitality operators seeking menu consistency during seasonal tourism peaks.

Frozen snacks and appetizers, although smaller in value, are advancing at a 10.95% CAGR, the fastest within the United Arab Emirates frozen food market. Lifestyle shifts among millennials and Gen Z fuel home entertaining and quick-service restaurant patronage, both of which rely on bite-sized, fry-and-serve products. Retail freezers increasingly allocate space to international street-food SKUs, mirroring the Emirates’ multicultural demographic mix. Manufacturers innovate with cleaner labels and plant-based proteins to counter health skepticism. Collectively, these trends reinforce product differentiation and volume uplift across the portfolio.

By End-User: Retail Supremacy with Foodservice Acceleration

Hypermarket and supermarket chains captured 66.75% of the United Arab Emirates's frozen food market share in 2025, as centrally located outlets and attractive private-label pricing shape shopper routines. Lulu Retail’s private labels already contribute 29.6% of banner sales, demonstrating the retailer's bargaining power and margin leverage. Digital integration, scan-and-go lanes, curbside pickup, and smart vending enhance the visibility of freezer aisles and spur impulse buys of premium SKUs.

The foodservice segment is projected to grow at a 9.36% CAGR, powered by Dubai’s hotel pipeline and the rapid scaling of international fast-food franchises. Central kitchens prefer frozen items for portion accuracy and waste reduction, a priority under rising labor and utility costs. Quick-service operators collaborate with suppliers to co-develop proprietary marinades and breadings, locking in demand. As tourist arrivals recover to pre-pandemic levels, banquet and catering functions once again require bulk frozen proteins, vegetables, and pastries, lifting sales volumes across distributors.

Geography Analysis

Dubai’s leadership rests on extensive infrastructure and a cosmopolitan consumer mix that keeps freezers stocked with global cuisines. The emirate’s cold-storage additions exceeded USD 35 million by 2025, pushing capacity past 70,000 pallet positions and enabling same-day redistribution to neighboring states. Government ambitions to create the world’s largest fresh-food hub complement frozen food flow by consolidating inspection, warehousing, and bonded services. Retailers adapt to Dubai’s single-use plastic ban with recyclable trays and mono-material films, protecting shelf visibility while meeting compliance.

Sharjah’s logistics corridors parallel the E311 highway, offering rapid truck lanes into Dubai and Abu Dhabi. Recent municipal incentives encourage SMEs to install tunnel freezers and blast chillers in industrial parks, expanding local value-addition capacity. Demand is spurred by population growth and a youthful demographic profile that leans toward convenience meals. Abu Dhabi continues to inject capital into KIZAD, which now hosts dedicated multi-temperature terminals integrated with Khalifa Port’s deepwater berths. These assets align with the National Food Security Strategy 2051, positioning the capital as both an import gateway and an emerging manufacturing base.

The Northern Emirates maintain modest but stable consumption. Ras Al Khaimah’s port handles specialty seafood imports for re-processing, while Fujairah leverages bunkering services to attract container feeders carrying frozen staples. Umm Al Quwain Free Trade Zone offers duty exemptions and ready utilities, enticing niche processors targeting East African re-export channels. Collectively, the geography mosaic ensures balanced contribution to the United Arab Emirates frozen food market, hedging supply risks and distributing employment benefits nationwide.

Competitive Landscape

Competition is intense in the market. Al Islami Foods and IFFCO capitalize on long-standing halal certification and proprietary distribution fleets to defend share, while global majors such as BRF and Unilever exploit integrated sourcing to secure volume deals with retailers. IFFCO’s AED 1 billion Dubai facility exemplifies vertical integration, from slaughtering to value-added processing, reducing lead times and customs exposure. Technology adoption is accelerating; firms deploy IoT sensors for real-time temperature surveillance and AI-driven demand forecasting to minimize spoilage.

E-commerce disruptors Noon and Talabat extend reach through micro-fulfilment centers that guarantee sub-one-hour frozen delivery. Traditional wholesalers respond by forging alliances with cold-chain specialists to shorten last-mile gaps. Plant-based frozen lines represent a white-space opportunity; Spinneys’ six-fold SKU expansion indicates latent demand among flexitarian consumers. Packaging innovation is another battleground: compostable trays and mono-material pouches replace multilayer plastics to satisfy Dubai’s regulatory shift.

Foreign ownership liberalization enacted in 2021 invites mid-tier European and Asian brands to set up local subsidiaries, intensifying shelf competition. Nonetheless, the requirement for halal accreditation and ESMA conformity preserves an advantage for incumbents conversant with local norms. Merger and acquisiton prospects center on bolt-on acquisitions of refrigerated logistics firms to secure distribution control.

United Arab Emirates Frozen Food Industry Leaders

-

Al Islami Foods

-

IFFCO Group

-

Americana Restaurants International PLC

-

Unilever PLC

-

BRF S.A

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Al Islami launched a new Heat and Eat product, ‘Original Tempura Nuggets.’ Crafted from pure, halal-certified chicken breasts, these nuggets are free from added hormones.

- June 2024: Savola acquired the remaining 1.13% stake in Panda Retail for USD 16 million, gaining full ownership.

- December 2023: IFFCO partnered with Tetra Pak, a food processing and packaging provider. The partnership aims to enhance the sustainability initiatives of the company.

United Arab Emirates Frozen Food Market Report Scope

Frozen food is preserved through rapid freezing, ensuring its safety until consumption. This process not only extends the shelf life of food but also maintains its nutritional value.

The United Arab Emirates frozen food market is segmented by product type and distribution channel. Based on product type, the market is segmented into frozen meat and fish, frozen fruits and vegetables, frozen ready meals, frozen desserts, frozen snacks, and other product types. Based on the distribution channel, the market studied is segmented into supermarkets/hypermarkets, convenience stores, specialty stores, and online retail stores.

For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Product Type

| Frozen Meat and Seafood |

| Frozen Fruits and Vegetables |

| Frozen Ready Meals |

| Frozen Bakery and Desserts |

| Frozen Snacks and Appetizers |

| Other Product Types |

By End-User

| Foodservice/HoReCa | Full-service Restaurants |

| Quick-service Restaurants | |

| Hotels and Resorts | |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Independent Groceries and Baqalas | |

| Specialty and Gourmet Stores | |

| Online and Quick-Commerce Platforms |

| By Product Type | Frozen Meat and Seafood | |

| Frozen Fruits and Vegetables | ||

| Frozen Ready Meals | ||

| Frozen Bakery and Desserts | ||

| Frozen Snacks and Appetizers | ||

| Other Product Types | ||

| By End-User | Foodservice/HoReCa | Full-service Restaurants |

| Quick-service Restaurants | ||

| Hotels and Resorts | ||

| Retail | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Independent Groceries and Baqalas | ||

| Specialty and Gourmet Stores | ||

| Online and Quick-Commerce Platforms | ||

Key Questions Answered in the Report

How large is the United Arab Emirates frozen food market in 2026?

The UAE frozen food market size is USD 0.92 billion in 2026 and is set to rise to USD 1.26 billion by 2031.

Which product category leads sales?

Frozen meat and seafood leads with 37.46% share, reflecting high protein imports and robust halal certification systems.

Which channel is growing fastest?

Foodservice demand is advancing at a 9.36% CAGR to 2031 as tourism and hospitality rebound.

What regulation impacts packaging from 2025?

Dubai’s single-use plastic ban effective January 2025 forces brands to adopt recyclable or compostable frozen food packaging.

Page last updated on: