Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

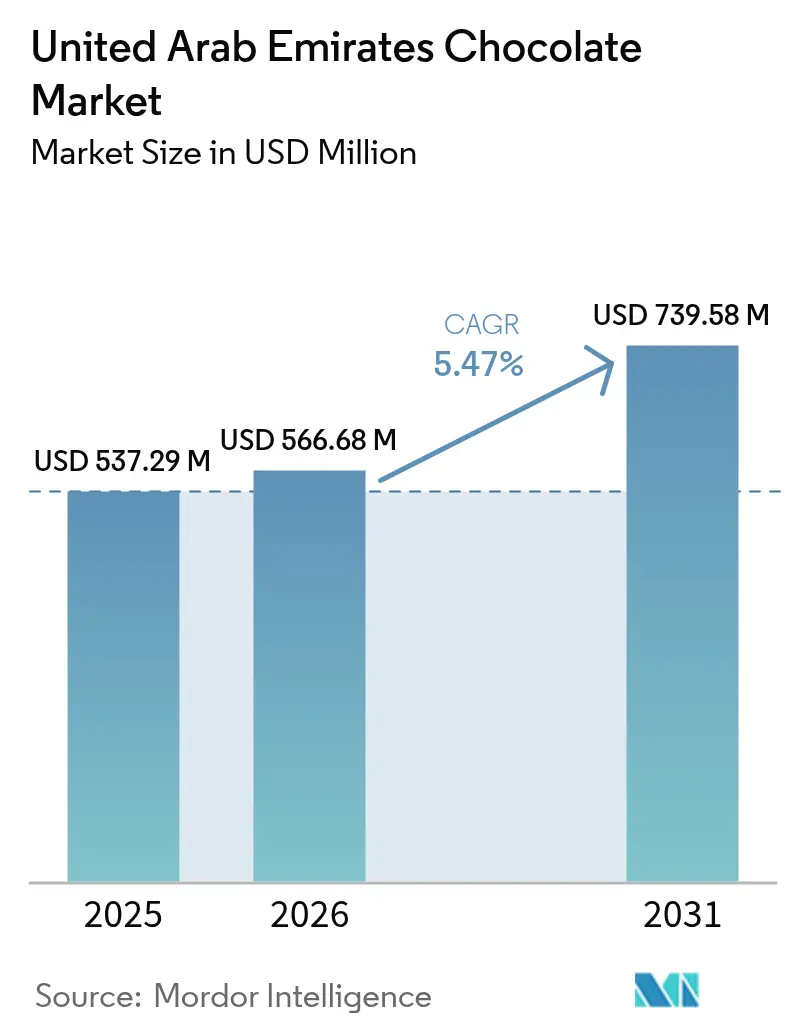

| Base Year Market Size (2025) | USD 537.29 Million |

| Market Size (2026) | USD 566.68 Million |

| Market Size (2031) | USD 739.58 Million |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Arab Emirates Chocolate Market Analysis by Mordor Intelligence

The United Arab Emirates chocolate market size is expected to grow from USD 537.29 billion in 2025 to USD 566.68 billion in 2026 and is forecast to reach USD 739.58 billion by 2031 at 5.47% CAGR over 2026-2031. The market is experiencing steady growth, driven by a strong gifting culture, a premium retail environment, and a multicultural consumer base that values both local and global brands. While supermarkets dominate with mass-market products, there is increasing demand for premium assortments, experiential retail formats, and online gifting solutions. This trend is further supported by tourism and duty-free sales, positioning the UAE as a strategic hub for regionally inspired chocolates with global appeal. Simultaneously, manufacturers face challenges such as stricter front-of-pack labeling regulations, upcoming sugar taxes, shifts toward sustainable packaging, and volatile cocoa prices. To address these pressures and sustain competitive margins, companies are focusing on reformulation, portion control, and premiumization strategies.

Key Report Takeaways

- By product type, milk and white chocolate held 56.12% of the United Arab Emirates chocolate market share in 2025, while dark chocolate is projected to grow at a 7.51% CAGR through 2031.

- By form, tablets and bars led with 39.05% revenue share in 2025; pralines and truffles are advancing at a 6.76% CAGR to 2031.

- By price form, the mass segment accounted for 77.10% of the United Arab Emirates chocolate market size in 2025, whereas premium products are forecast to expand at a 6.65% CAGR across the same horizon.

- By ingredient type, dairy-based items represented 75.70% of the United Arab Emirates chocolate market size in 2025, yet plant-based chocolate is climbing at a 6.92% CAGR

- By distribution channel, supermarkets and hypermarkets controlled 35.55% revenue in 2025, while online retail is set to accelerate at a 6.60% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for premium and artisanal chocolates | +1.2% | Dubai, Abu Dhabi (core); Sharjah (emerging) | Medium term (2-4 years) |

| Rise of gift-giving and luxury packaging during festivals | +0.9% | National, with peak intensity in Dubai, Abu Dhabi | Short term (≤ 2 years) |

| Strong tourism and hospitality sector supporting chocolate gifting/consumption | +0.7% | Dubai (primary); Abu Dhabi (secondary via cultural tourism) | Medium term (2-4 years) |

| Expansion of e-commerce and online retail channels | +0.8% | National, led by Dubai and Abu Dhabi metro areas | Short term (≤ 2 years) |

| Innovative flavors tailored to Middle Eastern tastes | +0.6% | National, with Dubai as innovation hub | Medium term (2-4 years) |

| Growing health consciousness boosting dark, vegan, and sugar-free chocolate | +1.0% | National, strongest in expatriate-heavy Dubai, Abu Dhabi | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing demand for premium and artisanal chocolates

The United Arab Emirates chocolate market is experiencing a notable shift driven by premiumization. Consumers are transitioning from standard offerings to artisanal and high-end products that highlight quality, origin, and gifting value. Luxury boutiques, bean-to-bar experiences, and locally tailored innovations, such as camel-milk chocolates and regionally inspired flavor profiles, are redefining chocolate as a lifestyle and experiential purchase rather than a routine indulgence. This trend is fueled by affluent residents, tourists, and seasonal gifting occasions, which prioritize visually appealing, handcrafted assortments with strong provenance narratives and European craftsmanship elements. While mass-market products continue to dominate overall consumption, the accelerated growth of premium chocolates is creating a distinct two-tier market. In this structure, value products sustain volume, while high-margin specialty formats drive growth and enhance brand differentiation. Companies are increasingly investing in product innovation and marketing strategies to capture the growing demand for premium offerings. Additionally, the rise of e-commerce platforms is further facilitating access to high-end chocolates, expanding their reach to a broader consumer base.

Rise of gift-giving and luxury packaging during festivals

In the United Arab Emirates, the chocolate market experiences pronounced spikes in demand, especially during the festive seasons of Ramadan and Eid. Seasonal gifting during Ramadan and Eid led to a significant 150% increase in sales and a remarkable 203.7% growth in gross merchandise value in 2025, with confectionery and pastries accounting for 20.4% of all gifting transactions on platforms such as Flowwow [1]Source: "Eid al-Fitr and Ramadan drive MENA e-commerce boom," samenacouncil.org. Shoppers are gravitating towards curated hampers and upscale assortments, often blending chocolates with traditional sweets and dates. This trend underscores the importance of premium packaging, larger sizes, and exclusive festive designs, all of which enhance brand visibility and elevate basket values. Such cultural buying habits not only compress inventory cycles but also necessitate meticulous pre-season stock planning, especially in modern retail and online platforms. Furthermore, these traditions provide brands with a strategic window to launch new products, innovate flavors, and roll out targeted promotions centered on gifting and hospitality. Businesses that effectively align their strategies with these seasonal dynamics can capitalize on the heightened consumer spending during these periods.

Expansion of E-commerce and online retail channels

In the United Arab Emirates, the surge of e-commerce is revolutionizing chocolate distribution. Factors like widespread smartphone adoption, sophisticated last-mile logistics, and a heightened demand for convenience, especially during Ramadan, are driving consumers to buy curated hampers and premium assortments online for direct delivery. Major hypermarket chains are bolstering their digital prowess with click-and-collect and home delivery options. Meanwhile, chocolatiers are rolling out subscription services, personalized offerings, and bespoke packaging to foster recurring demand and deepen customer ties. This online retail boom is not just about convenience; it's broadening access to artisanal and luxury brands, previously confined to flagship stores. As a result, consumers nationwide can now partake in premium gifting occasions, amplifying the reach of these high-margin products. Businesses are leveraging these trends to strengthen their competitive positioning and capture a larger share of the growing premium chocolate market.

Growing health consciousness boosting dark, vegan, and sugar-free chocolate

In the United Arab Emirates, a surge in health consciousness is driving consumers towards dark, vegan, organic, and sugar-free chocolates. These choices reflect a desire for indulgence that aligns with wellness, clean-label, and ethical sourcing values. In response, brands are introducing portion-controlled formats, crafting reduced-sugar recipes, sourcing cocoa sustainably, and offering premium products that balance taste with nutritional mindfulness. Furthermore, specialty collections and artisanal innovations bolster the perception of these chocolates as a “better-for-you” luxury. This industry shift is bolstered by front-of-pack nutrition labeling and the impending sugar tax, both of which are spurring reformulation efforts. As a result, low-sugar, high-cocoa, and plant-based variants are becoming increasingly competitive on retail shelves. Companies that adapt to these evolving consumer preferences are likely to gain a competitive edge in the market. Strategic partnerships with ethical cocoa suppliers, investments in product innovation, and targeted marketing campaigns are expected to further drive growth in this segment.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent food safety regulations and sugar limitations | -0.5% | National, with Abu Dhabi Nutri-Mark as pilot | Short term (≤ 2 years) |

| Seasonal sales spikes leading to demand fluctuations | -0.3% | National, concentrated in Ramadan/Eid periods | Short term (≤ 2 years) |

| Fluctuations in ingredient quality due to global supply issues | -0.7% | National, affecting importers and local manufacturers | Medium term (2-4 years) |

| Pressure on packaging sustainability and waste reduction | -0.4% | Dubai, Abu Dhabi (regulatory focus); national (consumer expectation) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent food safety regulations and sugar limitations

In the UAE, chocolate manufacturers are reshaping their product portfolios in response to stringent food safety regulations and sugar limitations. The Nutri-Mark law mandates clear nutrition scores on front-of-pack labels. Abu Dhabi's Nutri-Mark front-of-pack labeling, which will become mandatory from June 2025, assigns A-to-E grades based on the levels of sugar, sodium, and saturated fat in food products [2]Source: International Nut & Dried Fruit Council, “UAE: New Labeling Requirements Under Nutri-Mark Scheme,” inc.nutfruit.org. Additionally, forthcoming sugar-based excise taxes will penalize high-sugar formulations, pushing manufacturers towards healthier alternatives. The landscape is further complicated by regional labeling requirements, harmonization across the GCC, and a mandatory halal certification. School canteen restrictions on sugar and nut content add another layer of challenge. These overlapping mandates not only elevate entry costs but also favor established players, who possess the resources to navigate multi-jurisdictional compliance. In contrast, smaller artisans grapple with heightened challenges in maintaining their competitiveness. Companies must strategically innovate to align with these regulatory shifts while sustaining market share and profitability.

Fluctuations in ingredient quality due to global supply issues

Fluctuations in global cocoa supply are exerting significant cost and quality pressures on the United Arab Emirates chocolate market. Local manufacturers and importers, heavily reliant on international sourcing, face the dual challenge of mitigating price risks or absorbing margin compression. Supply shortages and inconsistent grind volumes are driving some producers to reformulate recipes or optimize cocoa usage, which may compromise product consistency. Additionally, the blending of lower-grade beans to meet contractual requirements poses a critical issue for premium and artisanal brands that depend on stable flavor profiles to maintain their competitive edge. In response, companies are increasingly adopting traceable and sustainability-certified sourcing strategies to secure long-term supply, protect brand equity, and address the escalating uncertainties associated with climate change and structural constraints in major cocoa-producing regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dark Chocolate Gains on Wellness Wave

In 2025, milk and white chocolate held a significant 56.12% share of the market, driven by their broad consumer appeal. Their strong positioning in festive gifting and family-oriented consumption established them as the preferred choice for traditional assortments, particularly among price-sensitive consumers. The sweeter flavor profile of these chocolates aligns with Ramadan and Eid celebrations, where they are commonly paired with dates, cookies, and pralines. This strategy enhances occasion-based spending and optimizes basket value, reinforcing the leadership of these variants across retail and hospitality channels.

Conversely, dark chocolate is projected to record a 7.51% CAGR through 2031, fueled by increasing demand from health-conscious consumers seeking lower-sugar, high-cocoa products. These offerings, often marketed as functional indulgences, cater to the growing preference for healthier lifestyles. Premium brand positioning, product innovation, and upcoming sugar regulations favoring reduced-sugar formulations are further driving this trend. As a result, the market is witnessing a bifurcation, with milk chocolate maintaining scale while dark and specialty variants drive value growth. Leading brands are responding by developing balanced portfolios that address both traditional gifting needs and health-driven consumption patterns.

By Form: Tablets and Bars Lead, but Pralines Capture Premiumization

In 2025, tablets and bars accounted for a significant 39.05% of the market share, driven by their convenience and widespread availability across modern trade and online channels. However, pralines and truffles are projected to achieve a 6.76% CAGR through 2031, reshaping the market through premiumization. This growth is primarily supported by the gifting culture during Ramadan and Eid, where curated assortments are perceived as symbols of sophistication and generosity. Premium brands such as Patchi and Forrey & Galland are elevating these offerings into lifestyle products, utilizing immersive retail experiences and artisanal packaging to reinforce their premium positioning.

While molded blocks and novelty forms address niche demands, the primary growth driver lies in pralines and truffles. These products deliver higher margins by emphasizing craftsmanship, provenance storytelling, and innovative packaging. This trend benefits both established players and local artisans. Experiential retail concepts and the bean-to-bar approach enable smaller brands like Mirzam to compete effectively by focusing on authenticity rather than scale. As a result, while tablets and bars continue to support everyday consumption, incremental market growth is concentrated in premium gifting assortments that combine cultural relevance with luxury appeal.

By Price Form: Mass Dominates, Premium Outpaces

In 2025, mass-market chocolate accounted for 77.10% of the market share. Its widespread availability, budget-friendly pricing, and robust presence in supermarkets, hypermarkets, and convenience stores made it the go-to choice for daily indulgence among a varied demographic. While this segment enjoys rapid product turnover and impulsive buys, it's grappling with shrinking margins. Volatile cocoa prices and looming sugar regulations pose challenges, making it tough to transfer costs to price-sensitive consumers. As a result, despite robust sales volumes, profitability remains constrained.

On the other hand, the premium segment is witnessing significant growth, with a compound annual growth rate (CAGR) of 6.65% projected through 2031. This surge is fueled by affluent locals, tourists, and festive shoppers gravitating towards artisanal and luxury chocolates. These offerings spotlight superior ingredients, compelling origin narratives, and upscale packaging. Premium brands, with their ability to adjust prices, are adept at weathering cost fluctuations. They're also reaping rewards from duty-free sales and special occasions, where chocolates often serve as status symbols or cherished gifts. This dynamic is carving a distinct divide in the market: while mass products maintain their scale, the real growth in value and margins is shifting towards premium offerings. This trend is prompting manufacturers to straddle both market tiers, yet with a keen focus on luxury-driven innovations and curated retail experiences.

By Distribution Channel: Supermarkets Lead, Online Gains

In 2025, Supermarkets and hypermarkets accounted for 35.55% of the market share, bolstered by their strong in-store visibility, diverse product assortments, and pivotal role in driving both impulse and routine purchases. Yet, as the retail landscape shifts, the online retail channel is witnessing significant growth, with a compound annual growth rate (CAGR) of 6.60% through 2031. This surge is largely attributed to the rapid adoption of mobile commerce and the evolution of last-mile delivery networks, ensuring swift and dependable fulfilment, especially for gifting occasions. Cultural events, notably Ramadan, have further catalyzed this trend, with consumers now favoring curated hampers sent directly to recipients over traditional store visits. Acknowledging this paradigm shift, major players in modern trade are pivoting, channeling investments into digital grocery platforms and enhancing delivery capabilities. This move is reshaping their operations into cohesive omnichannel ecosystems, moving away from a sole dependence on in-store sales.

While convenience stores, airport retail, hotel boutiques, and specialty chocolatiers cater to niche markets like travel retail, premium gifting, and impulse buys, their growth is hampered by location constraints and limited product assortments. E-commerce, on the other hand, boasts structural advantages, offering broader product ranges, tailored recommendations, and unique services like customized packaging and subscriptions. Moreover, digital platforms are bridging gaps, granting consumers in the Northern Emirates access to premium and artisanal brands, previously concentrated in Dubai and Abu Dhabi. This evolution underscores the necessity for a harmonious online-offline strategy: physical stores should focus on brand experience and discovery, while online platforms emphasize convenience, broader reach, and growth opportunities.

Geography Analysis

Dubai and Abu Dhabi act as pivotal hubs in the UAE's chocolate market, driving premium demand through luxury retail corridors, advanced tourism infrastructure, and affluent expatriate demographics. Dubai's status as a global tourism hub directly fuels chocolate sales, with duty-free outlets and experiential retail formats enhancing the market presence of local brands. This heightened visibility often extends internationally, as Dubai-originated flavors and artisanal concepts gain traction, solidifying the city's position as a leader in the confectionery industry.

Abu Dhabi reinforces the market through institutional demand, hospitality, and corporate gifting, while also influencing packaging strategies by implementing regulatory frameworks such as sustainability mandates. Conversely, Sharjah and the Northern Emirates operate as volume-driven markets, where supermarkets and hypermarkets dominate distribution channels to cater to price-sensitive households. The UAE's strategic role as a re-export hub further strengthens its market position, enabling local manufacturers to leverage advanced logistics infrastructure for regional expansion across the GCC and Middle East.

Regulatory harmonization across Gulf markets presents both challenges and opportunities, with the UAE often leading through initiatives such as front-of-pack labeling and upcoming sugar taxes. Geographic expansion within the country, including flagship experiential centers in Dubai and Abu Dhabi, demonstrates confidence in the premium segment. However, brands must strategically balance these investments with cost-efficient distribution models in Sharjah and the Northern Emirates to maximize market penetration and profitability.

Competitive Landscape

Top Companies in UAE Chocolate Market

The UAE chocolate market exhibits a moderately high level of concentration, with key players such as Mars, Ferrero, Mondelez, and Nestlé maintaining a significant market share through mass-market brands distributed via supermarkets, hypermarkets, and convenience stores. In contrast, the premium and gifting segments are led by brands like Patchi, Al Nassma, Mirzam, and Bateel, which operate through boutique outlets, e-commerce platforms, and strategic partnerships with hotels.

In February 2024, Ferrero established its new regional headquarters in Downtown Dubai, increasing its workforce from 12 to over 400 employees. The company has outlined plans to double its GCC business within five years by focusing on localized marketing strategies, seasonal product assortments, and B2B partnerships with hotels and airlines. Key market trends include a focus on seasonal gifting occasions such as Ramadan, Eid, and Diwali, the growing integration of e-commerce, and the introduction of Middle Eastern-inspired flavors like pistachio, kunafa, dates, saffron, and camel milk. Multinational corporations are increasingly licensing local flavors, while artisanal brands are leveraging social commerce and travel retail channels to scale their operations.

Emerging opportunities in the market include functional chocolates infused with probiotics, collagen, or adaptogens, as well as heat-stable formulations designed for outdoor consumption in the UAE's extreme summer temperatures, which often exceed 40 degrees Celsius. Additionally, subscription-based models targeting expatriates seeking European or artisanal chocolate brands unavailable in local retail channels present a promising growth opportunity.

United Arab Emirates Chocolate Industry Leaders

-

Mars, Incorporated

-

Ferrero International S.A.

-

Mondelez International, Inc.

-

Nestlé SA

-

Patchi Industrial Company S.A.L.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Fix Dessert Chocolatier introduced a new chocolate flavor in Dubai to align with shifting consumer preferences. This strategic initiative strengthens Fix's regional brand positioning and highlights its commitment to innovation within the competitive chocolate market of the United Arab Emirates.

- June 2025: FIX Dessert Chocolatier introduced its latest product, the "Time to Mango" chocolate bar, through a pop-up event at Mall of the Emirates, enhancing its focus on premium product innovation and strengthening consumer engagement within the UAE's chocolate market.

- November 2024: Careem partnered with Ebraheem El Samadi, the founder of Forever Rose, to launch a line of luxury Belgian chocolate bars. These products, featuring flavors inspired by local tastes, are exclusively distributed through Careem Groceries in Dubai and Abu Dhabi, enhancing the premium chocolate segment in the United Arab Emirates.

United Arab Emirates Chocolate Market Report Scope

Chocolate is a food product made from cocoa beans, which are fermented, dried, roasted, and ground to produce cocoa mass (cocoa solids and cocoa butter). It is typically combined with ingredients such as sugar, milk solids (in milk chocolate), and permitted emulsifiers or flavorings to create different chocolate varieties. The United Arab Emirates chocolate market (henceforth referred to as the market studied) is segmented by product type, form, price form, and distribution channel. By product type, the market is segmented into dark chocolate and milk & white chocolate. By form, the market is segmented into tablets and bars, molded blocks, pralines & truffles, and other forms. By price form, the market is segmented into mass and premium. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Product Type

| Dark Chocolate |

| Milk and White Chocolate |

By Form

| Tablets and Bars |

| Molded Blocks |

| Pralines and Truffles |

| Other Forms |

By Price Form

| Mass |

| Premium |

By Ingredient Type

| Dairy-based |

| Plant-based |

| Single Origin |

By Distribution Channel

| Supermarket/Hypermarket |

| Online Retail Store |

| Convenience Store |

| Other Distribution Channels |

| By Product Type | Dark Chocolate |

| Milk and White Chocolate | |

| By Form | Tablets and Bars |

| Molded Blocks | |

| Pralines and Truffles | |

| Other Forms | |

| By Price Form | Mass |

| Premium | |

| By Ingredient Type | Dairy-based |

| Plant-based | |

| Single Origin | |

| By Distribution Channel | Supermarket/Hypermarket |

| Online Retail Store | |

| Convenience Store | |

| Other Distribution Channels |

Market Definition

- Milk and White Chocolate - Milk chocolates is a solid chocolate made with milk (in the form of either milk powder, liquid milk, or condensed milk) and cocoa solids. White chocolate is made from cocoa butter and milk and contains no cocoa solids whatsoever. The scope includes regular chocolates, low-sugar, and sugar-free variants

- Toffees & Nougats - Toffees include hard, chewy, and small or one-bite candies marketed with labels as toffee or toffee-like confectionery. Nougat is a chewy confection with almond, sugar, and egg white as a basic ingredient; and it originated in Europe and Middle East countries.

- Cereals Bars - A snack composed of breakfast cereal that has been compressed into a bar shape and is held together with a form of edible adhesive. The scope includes snack bars made with cereals such as rice, oats, corn, etc. mixed with a binding syrup. These also include products labeled as cereal bars, cereal treat bars, or grain bars.

- Chewing Gum - This is a preparation for chewing, usually made of flavored and sweetened chicle or such substitutes as polyvinyl acetate. The types of chewing gums included in the scope are sugar-chewing gums and sugar-free chewing gums

| Keyword | Definition |

|---|---|

| Dark Chocolate | Dark chocolate is a form of chocolate containing cocoa solids and cocoa butter without the milk. |

| White Chocolate | White chocolate is the type of chocolate containing the highest percentage of milk solids, typically around or over 30 percent. |

| Milk Chocolate | Milk chocolate is made from dark chocolate that has a low cocoa solid content and higher sugar content, plus a milk product. |

| Hard Candy | A candy made of sugar and corn syrup boiled without crystallizing. |

| Toffees | A hard, chewy, often brown sweet that is made from sugar boiled with butter. |

| Nougats | A chewy or brittle candy containing almonds or other nuts and sometimes fruit. |

| Cereal bar | A cereal bar is a bar-shaped food product, made by pressing cereals and usually dried fruit or berries, which are in most cases held together by glucose syrup. |

| Protein bar | Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats. |

| Fruit & Nut bar | These are often based on dates with other dried fruit and nut additions and, in some cases, flavorings. |

| NCA | The National Confectioners Association is an American trade organization that promotes chocolate, candy, gum and mints, and the companies that make these treats. |

| CGMP | Current good manufacturing practices are those conforming to the guidelines recommended by relevant agencies. |

| Unstandardized foods | Unstandardized foods are those that do not have a standard of identity or that deviate from a prescribed standard in any manner. |

| GI | The glycemic index (GI) is a way of ranking carbohydrate-containing foods based on how slowly or quickly they are digested and increase blood glucose levels over a period of time |

| Skimmed milk powder | Skimmed milk powder is obtained by removing water from pasteurized skim milk by spray-drying. |

| Flavanols | Flavanols are a group of compounds found in cocoa, tea, apples, and many other plant-based foods and beverages. |

| WPC | Whey protein concentrate- the substance obtained by the removal of sufficient nonprotein constituents from pasteurized whey so that the finished dry product contains greater than 25% protein. |

| LDL | Low density Lipoprotein- the bad cholesterol |

| HDL | High density Lipoprotein- the good cholesterol |

| BHT | butylated Hydroxytoluene is a lab-made chemical that is added to foods as a preservative. |

| Carrageenan | Carrageenan is an additive used to thicken, emulsify, and preserve foods and drinks. |

| Free form | Not containing certain ingredients, such as gluten, dairy, or sugar. |

| Cocoa butter | It is a fatty substance obtained from cocoa beans, used in the manufacture of confectionery. |

| Pastellies | A type of of Brazilian candy made from sugar, eggs, and milk. |

| Draggees | Small, round candies that are coated with a hard sugar shell |

| CHOPRABISCO | Royal Belgian Association of the chocolate, pralines, biscuit, and confectionery industry- A trade association that represents the Belgian chocolate industry. |

| European Directive 2000/13 | A European Union directive that regulates the labeling of food products |

| Kakao-Verordnung | The German chocolate ordinance, a set of regulations that define what can be labeled as "chocolate" in Germany. |

| FASFC | Federal Agency for the Safety of the Food Chain |

| Pectin | A natural substance that is derived from fruits and vegetables. It is used in confectionery to create a gel-like texture. |

| Invert sugars | A type of sugar that is made up of glucose and fructose. |

| Emulsifier | A substance that helps to mix to liquids that does not mix together. |

| Anthocyanins | A type of flavonoid that is responsible for the red, purple, and blue colors of confectionery. |

| Functional Foods | Foods that have been modified to provide additional health benefits beyond basic nutrition. |

| Kosher certificate | This certification verifies that the ingredients, production process including all machinery, and/or food-service process complies with the standards of Jewish dietary law |

| Chicory root extract | A natural extract from the chicory root that is a good source of fiber, calcium, phosphorous, and folate |

| RDD | Recommended daily dose |

| Gummies | A chewy gelatin-based candy that is often flavored with fruit. |

| Nutraceuticals | Food or dietary supplements that are claimed to have health benefits. |

| Energy bars | Snack bars that are high in carbohydrates and calories are designed to provide energy on the go. |

| BFSO | Belgian Food Safety Organization for the food chain. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms