UAE Forklift Rental Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

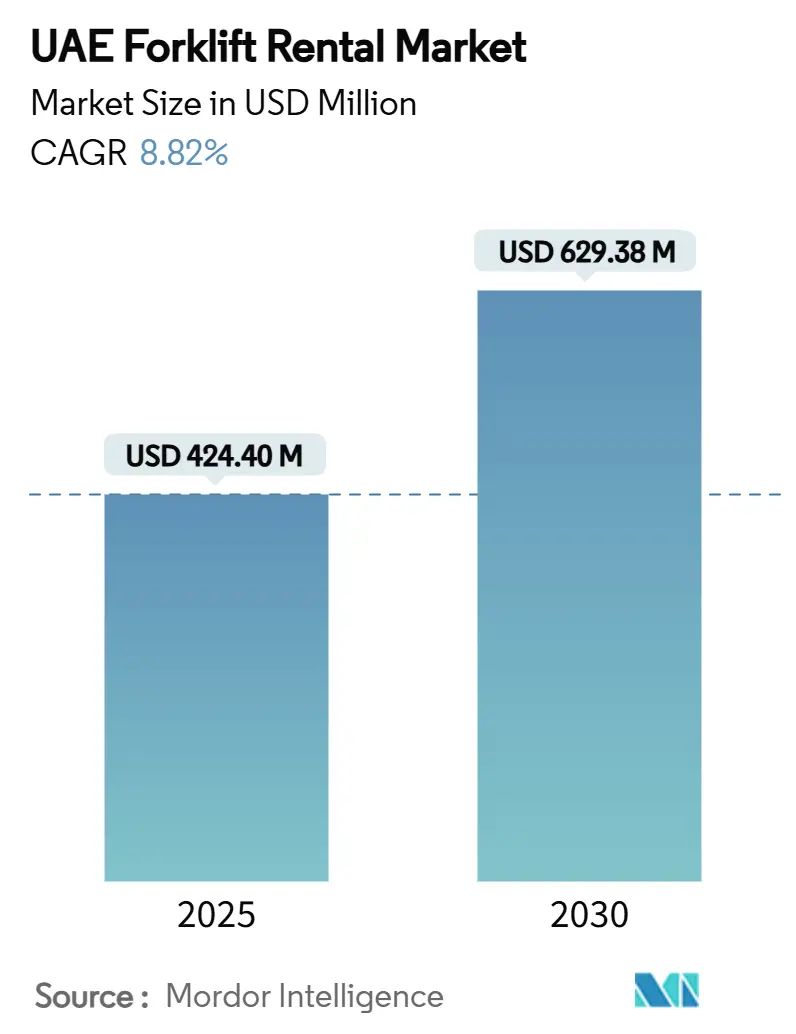

| Market Size (2025) | USD 424.40 Million |

| Market Size (2030) | USD 629.38 Million |

| Growth Rate (2025 - 2030) | 8.82% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Forklift Rental Market Analysis by Mordor Intelligence

The UAE forklift rental market stands at USD 424.4 million in 2025 and is forecast to reach USD 629.38 million by 2030, registering an 8.82% CAGR. The upward trajectory reflects the Emirates’ role as a logistics gateway linking Asia, Europe, and Africa, where the broader logistics sector already contributes to national GDP. A rise in industrial output further catalyzes growth, sizeable infrastructure outlays, and free-trade-zone incentives that compress import-export lead times. Rental demand also benefits from rising warehouse automation, the Net Zero 2050 framework incentivizing electric equipment uptake, and banking packages that lower entry barriers for small and medium enterprises. Competitive intensity remains moderate, with international manufacturers promoting technology-rich fleets while local distributors leverage entrenched customer relationships.

Key Report Takeaways

- By rental duration, short-term contracts led with 43.73% revenue share in 2024; long-term leases are projected to expand at a 9.56% CAGR through 2030.

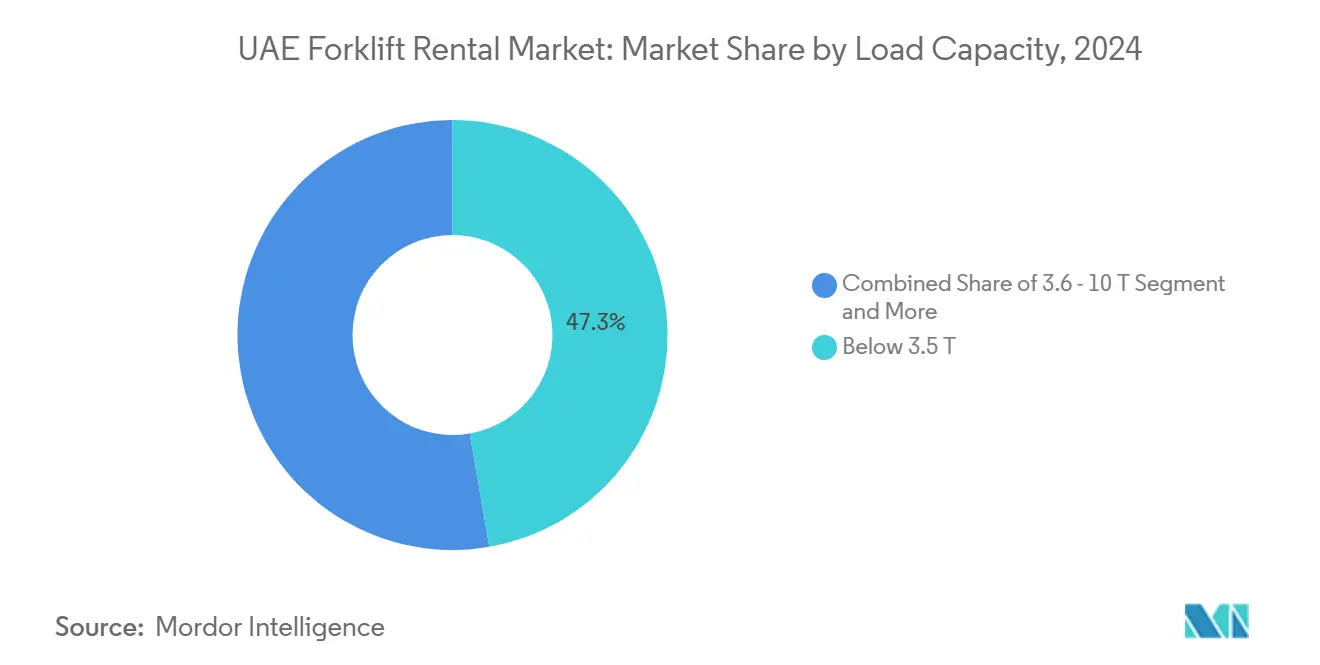

- By load capacity, units below 3.5 tons captured 47.26% of the UAE forklift rental market share in 2024, while 3.6-10 ton models are set to grow at a 9.89% CAGR to 2030.

- By power source, internal-combustion forklifts accounted for 66.87% of the UAE forklift rental market size in 2024; electric models will advance at an 11.28% CAGR over 2025-2030.

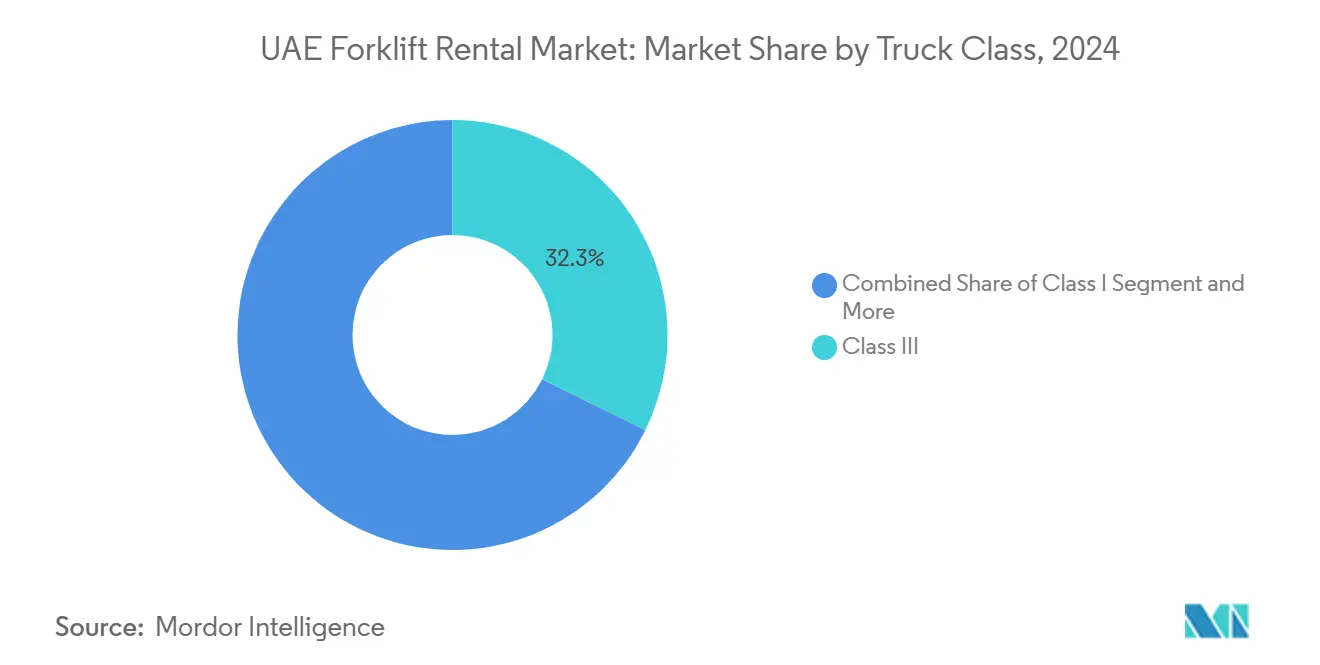

- By truck class, Class III held a 32.28% share of the UAE forklift rental market size in 2024, whereas Class I electric forklifts will register an 11.33% CAGR during the outlook period.

- By end-use, warehousing and logistics commanded 46.75% revenue in 2024 and are forecast to rise at an 11.65% CAGR to 2030, maintaining their position as the sector’s principal growth engine.

United arab emirates operates as part of an interconnected international environment rather than as a self-contained country level unit. The forklift rental market research by Mordor Intelligence places together all major developments across the globe within that wider frame.

UAE Forklift Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Logistics-Hub Expansion | +2.1% | Dubai, Abu Dhabi, nationwide corridors | Medium term (2-4 years) |

| Mega-Project Infrastructure | +1.8% | UAE-wide | Long term (≥ 4 years) |

| SME Capex-Light Rentals | +1.6% | All seven emirates | Short term (≤ 2 years) |

| Electric Forklift Shift | +1.4% | Dubai & Abu Dhabi leadership | Medium term (2-4 years) |

| Labor-Cost Automation | +1.3% | High-wage emirates | Medium term (2-4 years) |

| Mega-Event Spot Rentals | +0.9% | Dubai & Abu Dhabi | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Logistics-hub Expansion Fueled by E-commerce and Free-trade Zones

Dubai South’s new 23,200 m² facility, which will be online in 2025, exemplifies ongoing warehouse build-outs that enlarge the UAE forklift rental market[1]“Dubai South Announces Expeditors Facility,”, Zawya, zawya.com. Free-trade-zone operators seek material-handling flexibility to match seasonal peaks, prompting rental firms to bulk up mid-range fleets. The logistics sector is projected to expand, signalling sustained throughput that underpins rental utilization. Blockchain-enabled inventory tracking and automated sortation systems require precise, sensor-rich forklifts, pushing providers toward higher-specification, data-ready equipment. These dynamics collectively raise baseline demand across short-term and multi-year contracts.

Infrastructure Push for Mega-Projects and Smart Cities

The Dubai 2040 Urban Master Plan, which targets 5.8 million residents and doubles green space, sustains construction demand for forklifts on mixed-use developments. Parallel investments include the USD 3.5 billion Al Mafraq–Al Ghuwaifat artery and KEZAD Group’s 550 km² economic zone in Abu Dhabi, requiring continuous materials handling. The National Strategy for Industry and Advanced Technology adds industrial plants that need steady in-house transport solutions. As project scopes lengthen, contractors switch from spot rentals to long-term leases for cost certainty, fuelling the UAE forklift rental market’s recurring-revenue profile

Rising Labor Costs Spurring Warehouse Automation Demand

Average industrial wages in Dubai and Abu Dhabi have outpaced inflation since 2024, raising the payback for automation investments. Forklifts equipped with telematics, collision avoidance, and semi-autonomous guidance systems reduce operator hours per pallet moved. Rental providers offering connected fleets gain preference because warehouses benefit from utilization analytics without capital risk. The growing complexity of omnichannel logistics amplifies the need for agile material-handling assets that seamlessly integrate into warehouse-management software.

Mega-Event and Exhibition Cycles Driving Spot Rentals

Recurring international exhibitions at Dubai World Trade Centre and Abu Dhabi National Exhibition Centre create short-duration spikes in equipment demand. Venue operators and stand builders often rent forklifts for a few days to manage time-critical loads, supporting a vibrant spot-rental sub-segment. Event clustering around tourism peaks smooths seasonal gaps for rental companies, raising fleet turnover and ancillary revenue from transport and operator services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Charging Gaps & Tariffs | -1.2% | Industrial zones in all emirates | Medium term (2-4 years) |

| Oil- & Gas-Timeline Volatility | -0.8% | Abu Dhabi onshore & offshore corridors | Short term (≤ 2 years) |

| Grey-Market Imports | -0.7% | Price-sensitive segments nationwide | Short term (≤ 2 years) |

| Certification Cost Burden | -0.5% | Regulatory variations across seven emirates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Public Charging and High Electricity Tariffs for E-forklifts

Industrial-grade chargers are still sparse outside major logistics hubs, constraining electric penetration in remote construction sites[2]“Tariff Schedule 2025,”, Dubai Electricity and Water Authority, dewa.gov.ae. Electricity tariffs for commercial users remain higher than petroleum equivalents, diluting lifecycle savings. Rental companies must over-specify fleet counts to cover battery downtime, elevating capital exposure and dampening near-term ROI. The imbalance narrows as Dubai Electricity and Water Authority introduces tariff reform, yet the headwind persists into the medium term.

Volatile Oil-and-Gas Project Timelines Creating Demand Swings

ADNOC project schedules, which hinge on crude price signals, dictate forklift demand for hazardous-area certified units. Delays or scope cuts strand specialised inventory, eroding utilisation rates and pressuring margins. Although national diversification strategies lower oil dependency, energy construction still swings enough weight to jolt quarterly rental revenue patterns[3]“Project Pipeline Status 2025,”, Abu Dhabi National Oil Company, adnoc.ae.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Load Capacity: Mid-range units drive growth

Below-3.5-ton forklifts held 47.26% of UAE forklift rental market share in 2024 as e-commerce fulfillment centres favoured nimble equipment for rapid aisle turns. The 3.6-10-ton bracket is on track for a 9.89% CAGR, aided by KEZAD’s heavy-industry build-outs. These mid-range models bridge construction and manufacturing use-cases, improving fleet versatility.

Process-manufacturing plants stemming from import-substitution programs prefer mid-range electric units for cleanroom compatibility, gradually lifting the UAE forklift rental market size for this capacity segment. Above-10-ton units remain niche but stable, tied to port container yards and steel fabrication works.

By Rental Duration: Long-term leases gain momentum

Short-term hires led with 43.73% revenue in 2024 on the back of project-based construction flows. However, multi-year contracts are accelerating at 9.56% CAGR as contractors lock-in availability across prolonged gigaproject timelines such as the Al Maktoum International Airport expansion.

Asset-light SME manufacturers also lean toward 24- to 60-month agreements that bundle maintenance and operator training, thereby expanding the UAE forklift rental market size tied to long-term leases. Mid-term rentals preserve relevance for seasonal retail peaks and exhibition turnovers

By Power Source: Electric transition accelerates

Internal-combustion engines retained 66.87% of fleet count in 2024 due to refuelling speed and range advantages in heavy-duty shifts. Electric forklifts nonetheless post an 11.28% CAGR, reflecting ESG scorecard pressures and government infrastructure grants.

Hybrid units serve as a bridge technology in facilities where charger installations lag, ensuring dual-fuel reliability. As battery densities improve, electric models are expected to erode diesel dominance, lifting their share of UAE forklift rental market size past 2030.

By Truck Class: Class I leads innovation

Class III pallet trucks dominated 32.28% revenue in 2024 because of their versatility across produce distribution and general merchandising. Class I counterbalanced electrics are forecast for an 11.33% CAGR through to 2030, propelled by high-bay automation that rewards zero-emission indoor operations.

Class V internal-combustion models continue to anchor port and steel-yard tasks, but growth is tempered by sustainability mandates. Technology add-ons such as fleet telematics proliferate across classes, reinforcing differentiation within an otherwise commoditised UAE forklift rental market.

By End-Use Industry: Warehousing dominates growth

Warehousing and logistics captured 46.75% of the UAE forklift rental market share in 2024, riding e-commerce parcel volume and trans-shipment flows through Jebel Ali Port. The segment is set for an 11.65% CAGR as operators automate pallet movements and pursue 24/7 uptime via rented fleets.

Construction remains a cyclical but sizeable outlet, especially where mega-projects require mid-range forklifts for handling rebar, block, and façade. The automotive, food-and-beverage, and aerospace segments require specialised units, creating high-margin niches for rental firms.

Geography Analysis

Dubai and Abu Dhabi anchor most of the demand for the UAE forklift rental market, leveraging multimodal corridors that funnel goods through Jebel Ali Port and Khalifa Port. Dubai’s 2040 master plan, foreseeing a 75% population jump, guarantees continuous residential and infrastructure builds that underpin rental utilisation. Abu Dhabi’s KEZAD cluster adds heavy-industry pull, aided by AED 197 billion in statewide industrial value added in 2023.

Northern emirates such as Sharjah contribute through export-oriented manufacturing parks, while Fujairah’s Indian-Ocean outlet drives hazardous-goods forklift demand in oil-storage depots. Inter-emirate road upgrades, notably the USD 3.5 billion Al Mafraq–Al Ghuwaifat link, shave transit times, helping rental companies reposition fleets quickly between projects.

Regulatory diversity persists: Dubai mandates annual forklift inspections, whereas some emirates accept biennial checks, influencing fleet certification schedules and operating costs. Nonetheless, unified federal targets for emissions and digitalisation encourage national harmonisation of rental standards, benefiting providers with cross-emirate footprints.

The forklift rental market is assessed by Mordor Intelligence through a multi-layered geographic lens, covering other regions such as North America, along with detailed country-level analysis for Saudi Arabia, United States, Indonesia, South Korea, and Brazil.

Competitive Landscape

Local distributors such as Al-Futtaim Auto & Machinery and Khalifa Kanoo Machinery compete head-to-head with global names like Toyota Material Handling and Linde, creating a moderately fragmented UAE forklift rental market. International entrants emphasise telematics, lithium-ion options and global service protocols, while domestic firms bank on rapid response times and long-standing client ties.

White-space potential emerges in all-electric rental fleets, where current penetration lags stated sustainability goals. Providers that pair forklifts with charger installation and usage analytics stand to win enterprise contracts. Digital booking platforms are in pilot stages, promising dynamic pricing and automated maintenance scheduling.

Financial engineering becomes a differentiator: Some lessors co-design financing bundles with local banks under the Make-it-in-the-Emirates umbrella, effectively lowering customers' cost of capital. This service layering shields margins against grey-market unit imports that have recently pressured spot rental rates.

UAE Forklift Rental Industry Leaders

Byrne Equipment Rental

Al-Futtaim Auto & Machinery Co. (FAMCO)

Johnson Arabia

Kanoo Machinery

Mohamed Abdulrahman Al-Bahar (CAT)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Dayim Equipment Rental has marked a significant milestone in its expansion strategy with the arrival of its first batch of advanced forklifts in the UAE. These units are part of a strategic USD 15 million order placed with Hangcha Forklift. This delivery initiates a large-scale deployment, set to bolster Dayim’s long-term, multi-year rental contracts not just in the UAE, but also in Saudi Arabia, Kuwait, and other pivotal markets.

- February 2025: Dubai South and Expeditors International confirmed a 23,200 m² logistics facility slated for 2025 operations, likely boosting forklift rental volumes in the Logistics District.

UAE Forklift Rental Market Report Scope

| Less Than 3.5 T |

| 3.6 - 10 T |

| More Than 10 T |

| Short-term / Spot ( Less Than 1 month) |

| Mid-term (1 - 12 months) |

| Long-term Lease (3 - 5 years) |

| Electric |

| Internal Combustion (Diesel/LPG) |

| Hybrid |

| Class I |

| Class II |

| Class III |

| Class IV |

| Class V |

| Warehousing & Logistics |

| Construction |

| Automotive |

| Food & Beverage |

| Aerospace & Defense |

| Others (Retail, Pharma, etc.) |

| By Load Capacity | Less Than 3.5 T |

| 3.6 - 10 T | |

| More Than 10 T | |

| By Rental Duration | Short-term / Spot ( Less Than 1 month) |

| Mid-term (1 - 12 months) | |

| Long-term Lease (3 - 5 years) | |

| By Power Source | Electric |

| Internal Combustion (Diesel/LPG) | |

| Hybrid | |

| By Truck Class | Class I |

| Class II | |

| Class III | |

| Class IV | |

| Class V | |

| By End-use Industry | Warehousing & Logistics |

| Construction | |

| Automotive | |

| Food & Beverage | |

| Aerospace & Defense | |

| Others (Retail, Pharma, etc.) |

Key Questions Answered in the Report

What is the current value of the UAE forklift rental market?

The market is valued at USD 424.4 million in 2025 and is projected to grow at an 8.82% CAGR to USD 629.38 million by 2030.

Which segment delivers the highest UAE forklift rental market share?

Warehousing and logistics lead with 46.75% revenue in 2024 and are expected to maintain dominance through 2030

How fast are electric forklifts expected to grow?

Electric models are forecast to register an 11.28% CAGR between 2025 and 2030, faster than any other power class.

Why are long-term rental contracts gaining popularity?

Multi-year infrastructure projects and SME cash-flow strategies favour predictable equipment costs, driving a 9.56% CAGR for long-term leases.

What factors restrain electric forklift uptake?

Limited industrial charging infrastructure and higher commercial electricity tariffs currently dampen large-scale adoption.

Page last updated on: