South Korea Forklift Rental Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

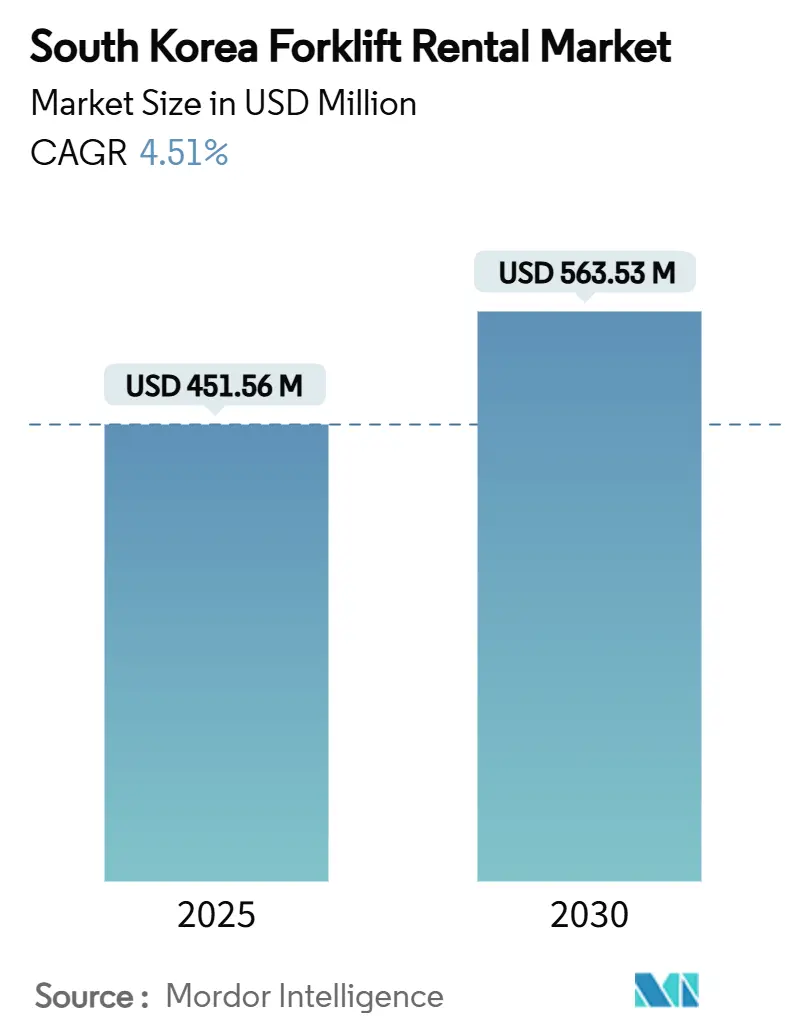

| Market Size (2025) | USD 451.56 Million |

| Market Size (2030) | USD 563.53 Million |

| Growth Rate (2025 - 2030) | 4.51% CAGR |

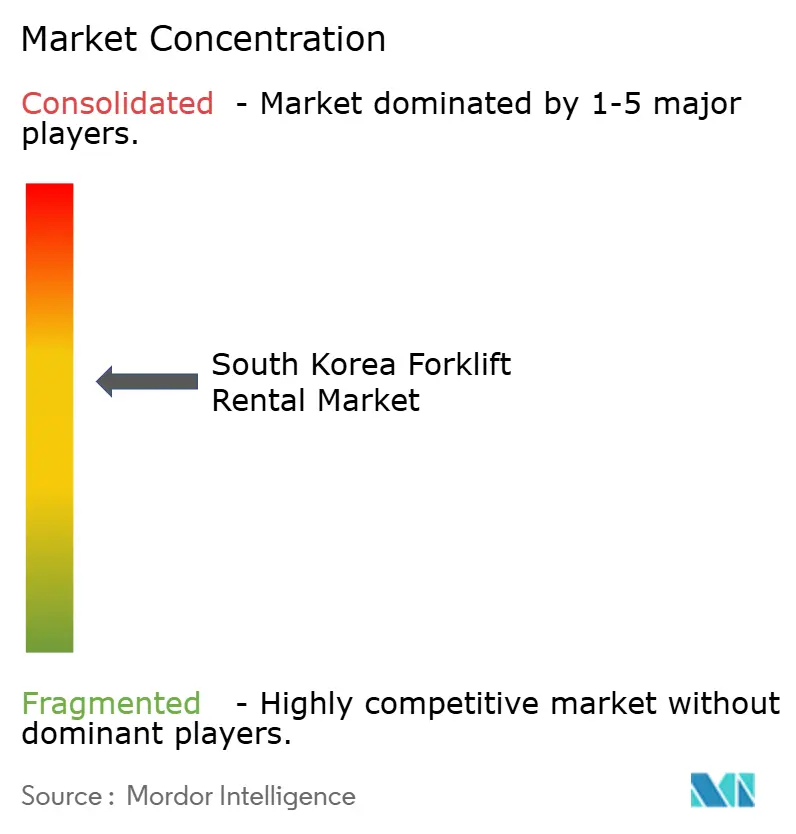

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Korea Forklift Rental Market Analysis by Mordor Intelligence

The South Korea forklift rental market size stands at USD 451.56 million in 2025 and is forecast to expand at a CAGR of 4.51% to reach USD 563.53 million by 2030. Robust demand stems from e-commerce warehousing upgrades, government incentives for zero-emission logistics equipment, and the build-out of smart industrial complexes. Electricity tariffs jumped 70% between 2022 and 2024, prompting manufacturers to shift toward rental contracts that avoid large upfront purchases. The national plan to quadruple renewable-energy capacity to 121.9 GW by 2038 is reshaping the electric-versus-internal-combustion mix, while OEM-backed leasing programs improve fleet utilisation through predictive maintenance and automation features[1]Institute for Energy Economics and Financial Analysis, "South Korea's 11th Power Plan Makes Partial Progress Towards Decarbonization." ieefa.org. Market competition remains moderate, yet rising automation intensity and supply-chain constraints are pushing operators to secure technology partnerships and diversified equipment sources.

Key Report Takeaways

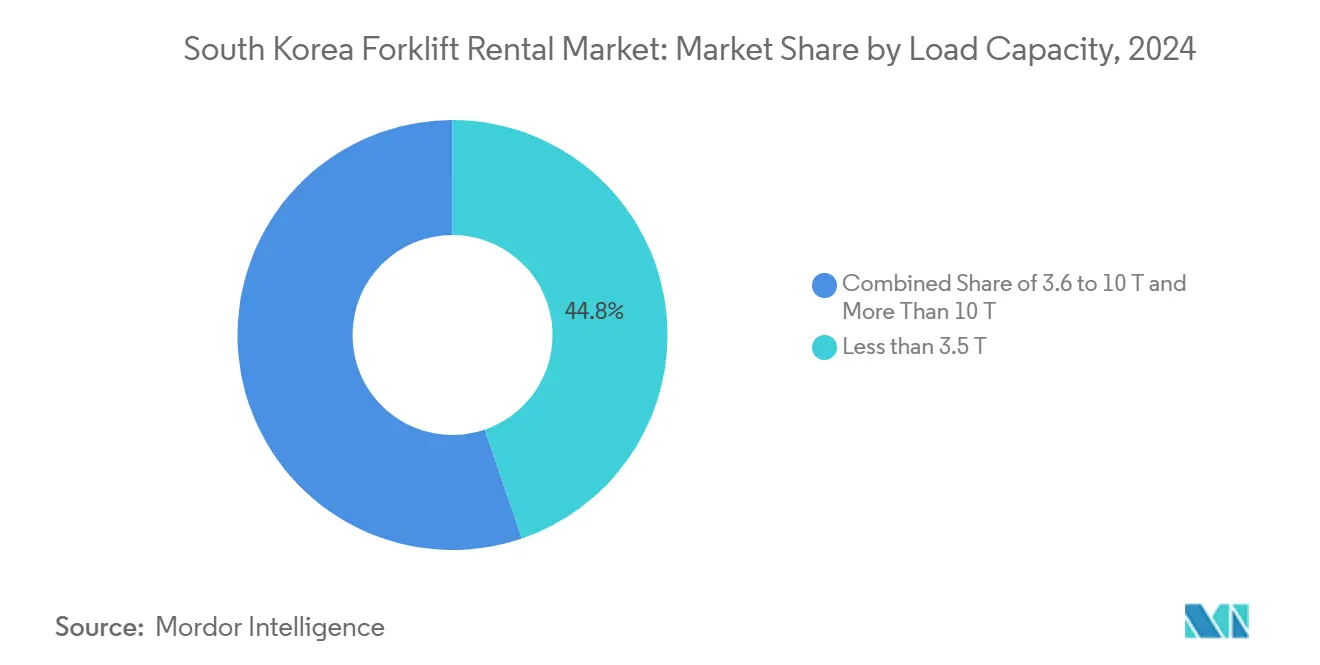

- By load capacity, units under 3.5 T led with 44.77% share in 2024 and are advancing at a 6.39% CAGR to 2030.

- By rental duration, short-term contracts held 50.61% of the South Korean forklift rental market share in 2024, while long-term leases posted the highest 6.82% CAGR through 2030.

- By power source, electric forklifts accounted for 56.44% of the South Korean forklift rental market size in 2024 and are expanding at a 9.46% CAGR to 2030.

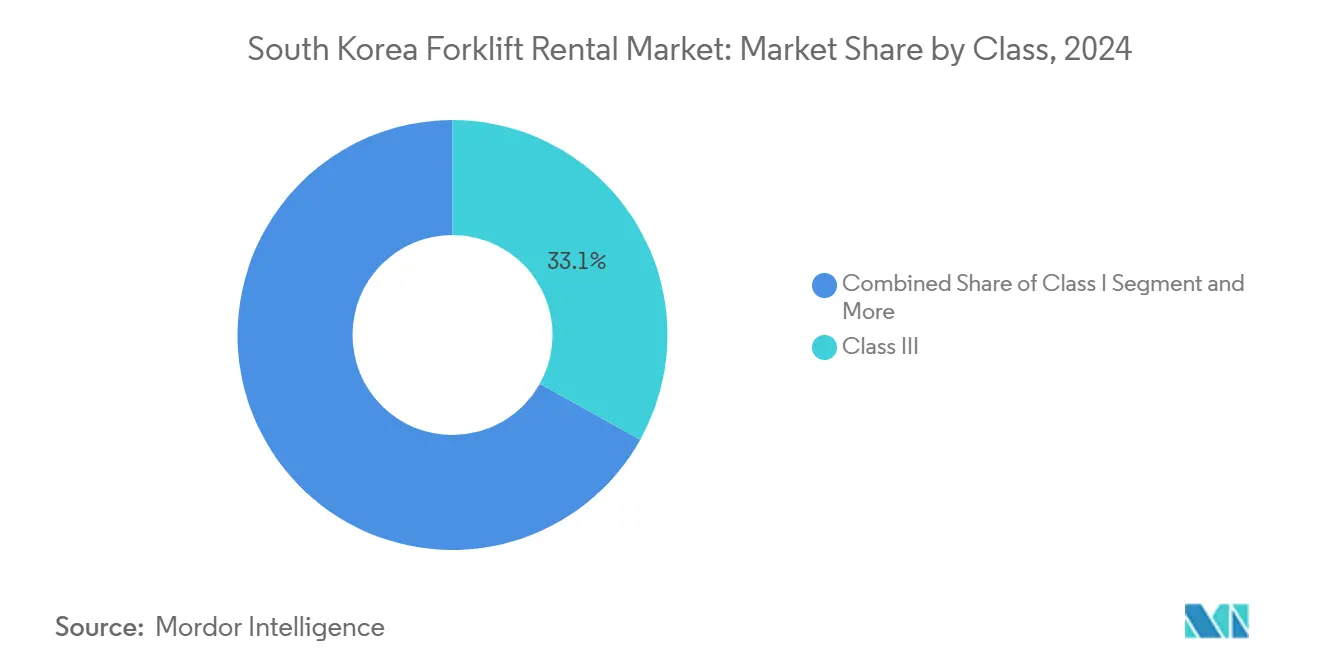

- By class, Class III vehicles captured a 33.09% share in 2024; Class I trucks registered the fastest 7.33% CAGR to 2030.

- By end-use, warehousing and logistics commanded 38.93% revenue share in 2024, buoyed by e-commerce facilities growing at a 9.05% CAGR.

- By region, the Seoul Capital Area contributed 59.36% market share in 2024, while the Gyeongsang Region records the quickest 6.04% CAGR through 2030.

Competitive positioning in South korea includes both locally based firms and those operating across multiple regions. The market landscape in the global forklift rental industry research shows how these players are arranged internationally.

South Korea Forklift Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce Warehousing Expansion | +1.2% | Seoul Capital Area, Gyeongsang Region | Short term (≤ 2 years) |

| Incentives for Zero-Emission Logistics Equipment | +0.8% | National, concentrated in industrial complexes | Medium term (2-4 years) |

| Construction of Smart Logistics Centres | +0.9% | National, with focus on Gyeonggi, Gyeongnam, Busan | Medium term (2-4 years) |

| Long-Term Leasing Programs | +0.6% | National, stronger in Seoul-Incheon corridor | Long term (≥ 4 years) |

| After-Sales Analytics Platforms | +0.4% | National, early adoption in Seoul Capital Area | Long term (≥ 4 years) |

| Ageing Workforce Acceleration | +0.7% | National, pronounced in manufacturing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-commerce Warehousing Expansion Boosts Peak-Period Rental Deman

South Korea’s e-commerce fulfilment facilities increasingly adopt automated storage systems that require nimble forklifts capable of handling narrow aisles and rapid order cycles. Up to 95% of existing warehouse stock still needs modernisation, and leading logistics firms are raising capital to fund smart logistics upgrades[2]Invest Korea, "Evolution of Korea's Logistics Industry: Rapid Advance into Smart Logistics.", investkorea.org. Third-party providers dominate peak-season capacity, favouring short-term rentals that avoid idle assets during off-peak months. AI-based demand-forecasting tools optimise pallet flows, sharpening the value proposition of flexible rental fleets. Cold-chain growth for fresh groceries calls for temperature-controlled forklifts, allowing rental operators to charge premium rates for specialised units. Overall, the warehousing upgrade positions rental companies as strategic partners rather than equipment suppliers.

Government Incentives for Zero-Emission Logistics Equipment

The Hydrogen Green Mobility Regulatory Free Zone in Ulsan waives refuelling restrictions, accelerating trials of fuel-cell forklifts. Doosan Bobcat commercialised a 3-ton hydrogen model equipped with a 20 kW cell stack in early 2024. Smart Logistics Center Certification rewards facilities that deploy clean-energy machines, indirectly subsidising rental operators that stock electric and hydrogen fleets. Although high electricity prices tighten operating margins, subsidies and ESG mandates preserve the shift toward low-emission solutions. Rental agreements mitigate technology risk for users while ensuring access to the newest drive systems.

Rising Construction of Smart Logistics Centres Under the Korean New Deal

The Korean New Deal earmarks KRW 4.0 trillion to build 15 smart industrial complexes by 2025, generating concentrated demand for advanced material-handling fleets[3]International Energy Agency, "Korean New Deal 10 key projects – Smart and green industrial complexes – Policies." iea.org. Early projects such as the Banwol-Sihwa complex integrate 5G-guided vehicles, setting performance benchmarks replicated nationwide. Provincial budgets, including a KRW 60.9 billion renovation in Gwangyang Bay, fuel regional order pipelines. Project-based construction schedules favour short-term rentals, while the tech-heavy operational phase favours long-term leases for automated forklifts. Rental firms that bundle telematics and analytics capture premium margins.

OEM-Backed Long-Term Leasing Programs Improve Fleet Utilisation

Manufacturers deepen vertical integration, lowering component costs and offering favourable lease terms with built-in service contracts. Mergers between robotics and machinery units enable bundled automation features that raise utilisation hours and lower downtime. Cross-selling agreements expand national coverage, giving OEM aligned rental divisions price flexibility that independent firms struggle to match. Customers value predictable budgeting, fueling the 6.82% CAGR in long-term leases

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-Chain Shortages | -0.9% | National, acute in specialized equipment segments | Short term (≤ 2 years) |

| High Electricity Prices | -0.6% | National, pronounced in energy-intensive operations | Medium term (2-4 years) |

| Fragmented Dealer Network | -0.5% | Regional, primarily Chungcheong, Jeolla, Gangwon-Jeju | Medium term (2-4 years) |

| Stricter Safety Regulations | -0.3% | National, disproportionate impact on smaller operators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Shortages Limit New Forklift Availability for Rental Fleets

Global component bottlenecks restrict battery cells, semiconductors, and hydraulic parts, delaying OEM deliveries and capping fleet expansion. Domestic raw-material inflation pushes up acquisition costs, compressing rental margins. Operators hedge by multibrand sourcing and redeploying idle assets yet still risk stockouts for popular electric or hydrogen models. Short-term substitution with diesel or LPG units meets urgent demand but complicates sustainability targets. Operators with robust supplier networks and refurbishment capabilities offset part of the shortfall but growth remains constrained until 2026.

High Electricity Prices Narrow TCO Gap vs IC Engine Rentals

Industrial power tariffs rose significantly from 2022 to 2024, eroding the running-cost advantage of electric forklifts. Energy-intensive facilities recalibrate lease budgets, occasionally reverting to LPG or diesel options for heavy-duty shifts. Pricing volatility complicates multi-year agreements, prompting rental firms to incorporate cost-pass-through clauses tied to electricity indices. Despite the squeeze, emission regulations and factory ESG targets continue to favour electrification, so operators balance tariff exposure with subsidy opportunities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Load Capacity: Compact Equipment Drives Adoption

Units under 3.5 T held 44.77% of the South Korean forklift rental market share in 2024 and expanded at a 6.39% CAGR. Their small turning radius and lightweight design align with automated storage systems common in e-commerce hubs. Mid-range 3.6-10 T models serve general manufacturing, while capacities above 10 T cater to steel and shipbuilding clusters in the Gyeongsang Region. Compact fleets benefit from rapid product cycles, making rental the preferred access mode for operators seeking the latest safety sensors and lithium-ion packs.

Second-generation narrow-aisle forklifts integrate 5G connectivity for real-time traffic control, further boosting rental appeal. Contracts typically bundle training and maintenance to ensure safe use in high-density rack environments. Larger industrial users rent compact units as secondary fleets for intra-plant movements, compensating for labour shortages on conventional routes.

By Rental Duration: Balancing Flexibility and Predictability

Short-term contracts kept a 50.61% share in 2024 by serving project peaks and seasonal retail surges. The South Korea forklift rental market size for long-term leases rises fastest at a 6.82% CAGR as smart-factory operators value uptime guarantees and technology upgrades. Mid-term deals bridge testing phases for hydrogen or lithium-ion prototypes before large-scale rollout.

Long-term packages increasingly embed performance-based KPIs, with penalties for downtime exceeding agreed thresholds. Operators benefit from steady cash flows and can finance higher-cost electric or fuel-cell units. Short-term rentals remain essential in construction sites and event setups, but their growth rate lags longer-tenure categories.

By Power Source: Electrification Outpaces Combustion

Electric models delivered 56.44% of 2024 revenue and posted a robust 9.46% CAGR, driven by subsidy programs and clean-air regulations. Diesel and LPG remain critical outdoors, yet face scrutiny within enclosed warehouses. Hydrogen fuel-cell pilots show promise for multi-shift operations with minimal refuel downtime, though infrastructure limits adoption for now.

Battery leasing arrangements minimise upfront costs and guarantee end-of-life recycling, a key value driver for sustainability-minded firms. The South Korea forklift rental market size for electric fleets receives additional lift from analytics platforms that optimise charge scheduling, offsetting high electricity tariffs during peak grid hours.

By Class: Automation Pushes Class I Leadership

Class I electric rider trucks gain momentum with a 7.33% CAGR through 2030 as warehouses automate pallet flow and pick-to-light systems. Class III pallet trucks still capture the largest share at 33.09% thanks to retail distribution ubiquity. Class II narrow-aisle trucks fill high-density storage, while Class IV and V combustion units sustain outdoor logistics and construction supply chains.

Integration between Class I forklifts and warehouse-management software triggers demand for rental packages, including telematics dashboards and operator-assist modules. The Gyeonggi Banwol-Sihwa Smart Green Industrial Complex's deployment of 5G-based automated guided vehicles demonstrates the integration between Class I forklifts and broader automation ecosystems. Advanced driver-assistance systems reduce collision risks, a major concern in high-throughput e-commerce hubs.

By End-Use Industry: Warehousing Commands Spend

Warehousing and logistics represented 38.93% of the 2024 value and exhibit a 9.05% CAGR as fulfilment centres proliferate. Construction follows, benefiting from the Korea New Deal infrastructure projects requiring project-based rentals. Automotive factories in Ulsan and Hwaseong expand electric-vehicle capacity, spurring specialised lift requirements for battery packs.

Cold-chain growth pushes the South Korea forklift rental market towards refrigerated-spec units with stainless-steel components. CJ Logistics' development of integrated robotic systems and cold chain solutions demonstrates how logistics providers drive specialized equipment demand. Aerospace and defence sectors rent precision-handling equipment for high-value components, utilising flexible contracts aligned with batch production schedules.

Geography Analysis

The Seoul Capital Area contributed 59.36% of 2024 revenue, leveraging dense industrial parks and world-class transport links. Gyeongsang Region records a 6.04% CAGR, anchored by hydrogen pilot zones and shipbuilding megasites. The Banwol-Sihwa Smart Green Industrial Complex exemplifies advanced 5G-enabled logistics platforms that demand connected electric forklifts. Elevated power tariffs squeeze warehouse margins, but capital-region operators offset costs through high utilisation and premium service tiers.

Gyeongsang Region achieves the fastest 6.04% CAGR, underpinned by heavy industries and the Ulsan Hydrogen Free Zone that accelerates fuel-cell equipment trials. Busan’s seaport automation projects and Daegu’s automotive supply chain further lift regional rentals. Fragmented dealer coverage outside metro areas grants national firms an edge if they invest in local service depots.

Chungcheong, Jeolla, and Gangwon-Jeju collectively present emerging growth pockets. Government-backed industrial sites near Chuncheon and the KRW 60.9 billion Gwangyang Bay renewal programme require specialised forklifts for steel and chemical logistics. Jeju’s renewable-energy installations create demand for maintenance lifts and rough-terrain models. Rental companies that tailor packages to provincial requirements stand to capture underserved segments.

Mordor Intelligence tracks the forklift rental market across other major regions such as North America, with additional country-level coverage spanning Indonesia, United States, Saudi Arabia, Brazil, and United Arab Emirates, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

The South Korean forklift rental arena shows moderate concentration around a core group of diversified equipment lessors. AJ Networks sets the benchmark for national fleet size and multi-industry reach. Doosan Bobcat leverages its machinery heritage and recent merger with Doosan Robotics to infuse smart functions into rental offerings. Hyundai Material Handling draws on automotive supply links to secure sales channels inside large manufacturing hubs.

Technology adoption is the key battleground as leading firms embed IoT sensors and cloud dashboards that predict maintenance events before downtime occurs. Hydrogen and lithium battery pilots create differentiation because only a few operators invest in the specialist service skills these powertrains require. Partnerships with software start-ups give rental providers access to warehouse-management data that supports performance-based billing. Competitors unable to match these digital capabilities focus on price discounts and fast replacement guarantees to defend accounts.

Regional coverage matters because service gaps outside Seoul can trigger costly delays for users. Larger companies respond by acquiring provincial agencies and adding mobile service vans that reach remote industrial parks. Safety regulation changes push all fleets toward real-time operator monitoring, raising compliance costs that smaller firms struggle to absorb. Vertical integration into components such as hydraulics and batteries shields the big players from global supply shocks that have lengthened delivery lead times. As automation intensity climbs, customers increasingly select rental partners on technical knowledge rather than asset count.

South Korea Forklift Rental Industry Leaders

-

AJ Networks

-

KION Group

-

Doosan Bobcat

-

Lotte Rental

-

Hyundai Material Handling

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Doosan Bobcat, Gwangyang City and Korea Logis Pool signed an MOU to supply hydrogen forklifts, with rental services embedded in the rollout plan.

- October 2024: Doosan Bobcat acquired Doosan Mottrol, bolstering vertical integration of hydraulic components for its forklift and construction-equipment lines.

South Korea Forklift Rental Market Report Scope

| Less Than 3.5 T |

| 3.6 to 10 T |

| More Than 10 T |

| Short-term / Spot (Less than 1 month) |

| Mid-term (1 to 12 months) |

| Long-term Lease (3 to 5 years) |

| Electric |

| Internal Combustion (Diesel/LPG) |

| Hybrid / Hydrogen Fuel-cell |

| Class I |

| Class II |

| Class III |

| Class IV |

| Class V |

| Warehousing and Logistics |

| Construction |

| Automotive |

| Food and Beverage |

| Aerospace and Defense |

| Others (Retail, Pharma, etc.) |

| Seoul Capital Area |

| Gyeongsang Region (Busan, Ulsan, Daegu) |

| Chungcheong Region |

| Jeolla Region |

| Gangwon and Jeju |

| By Load Capacity | Less Than 3.5 T |

| 3.6 to 10 T | |

| More Than 10 T | |

| By Rental Duration | Short-term / Spot (Less than 1 month) |

| Mid-term (1 to 12 months) | |

| Long-term Lease (3 to 5 years) | |

| By Power Source | Electric |

| Internal Combustion (Diesel/LPG) | |

| Hybrid / Hydrogen Fuel-cell | |

| By Class | Class I |

| Class II | |

| Class III | |

| Class IV | |

| Class V | |

| By End-use Industry | Warehousing and Logistics |

| Construction | |

| Automotive | |

| Food and Beverage | |

| Aerospace and Defense | |

| Others (Retail, Pharma, etc.) | |

| By Region | Seoul Capital Area |

| Gyeongsang Region (Busan, Ulsan, Daegu) | |

| Chungcheong Region | |

| Jeolla Region | |

| Gangwon and Jeju |

Key Questions Answered in the Report

What is the 2025 value of the South Korea forklift rental market?

The South Korea forklift rental market size is USD 451.56 million in 2025.

Which segment leads market share by power source?

Electric forklifts command 56.44% share in 2024 and are growing at a 9.46% CAGR.

Why are long-term leases growing faster than spot rentals?

Long-term contracts offer predictable costs and guaranteed availability, crucial amid supply-chain disruptions and rapid tech change.

How do high electricity prices affect electric forklift rentals?

Tariff increases narrow running-cost advantages, prompting rental firms to adjust pricing and incorporate subsidy mechanisms.

Which region is the fastest growing?

The Gyeongsang Region posts the highest 6.04% CAGR through 2030, supported by hydrogen-economy initiatives and heavy-industry demand.

What impact will hydrogen technology have on rental fleets?

Fuel-cell models lower refuel time and emissions, and rental agreements let users trial the technology without capital risk.

Page last updated on: