UAE Construction Equipment Rental Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

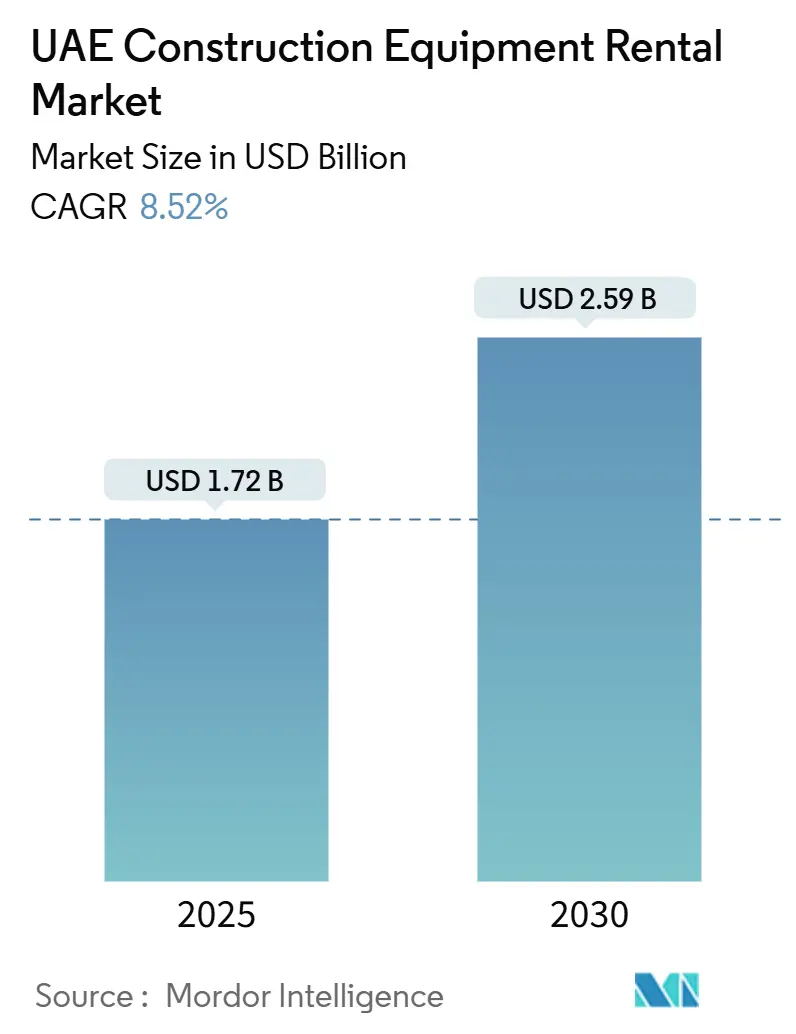

| Market Size (2025) | USD 1.72 Billion |

| Market Size (2030) | USD 2.59 Billion |

| Growth Rate (2025 - 2030) | 8.52% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Construction Equipment Rental Market Analysis by Mordor Intelligence

The UAE construction equipment rental market stands at USD 1.72 billion in 2025 and is projected to reach USD 2.59 billion by 2030, expanding at an 8.52% CAGR. The uptrend is fueled by the federal government’s multi-billion-dollar infrastructure pipeline, the sector’s preference for capital-light business models, and the country’s long-term net-zero roadmap. Mega projects such as Etihad Rail, the Abu Dhabi Integrated Transport system, and the USD 35 billion Al Maktoum International Airport expansion keep fleet utilization high while drawing new entrants into the UAE construction equipment rental market. Digital rental platforms that apply telematics for predictive maintenance boost uptime and trim idle time, reinforcing rental as the logical alternative to ownership. On the cost side, elevated interest rates and material inflation spur contractors to convert capital expenditure into operating expenditure, tilting demand toward flexible rental contracts. Finally, the national mandate for hydrogen-ready and electric machinery accelerates fleet renewal cycles, especially for equipment deployed in urban and renewable-energy projects.

Key Report Takeaways

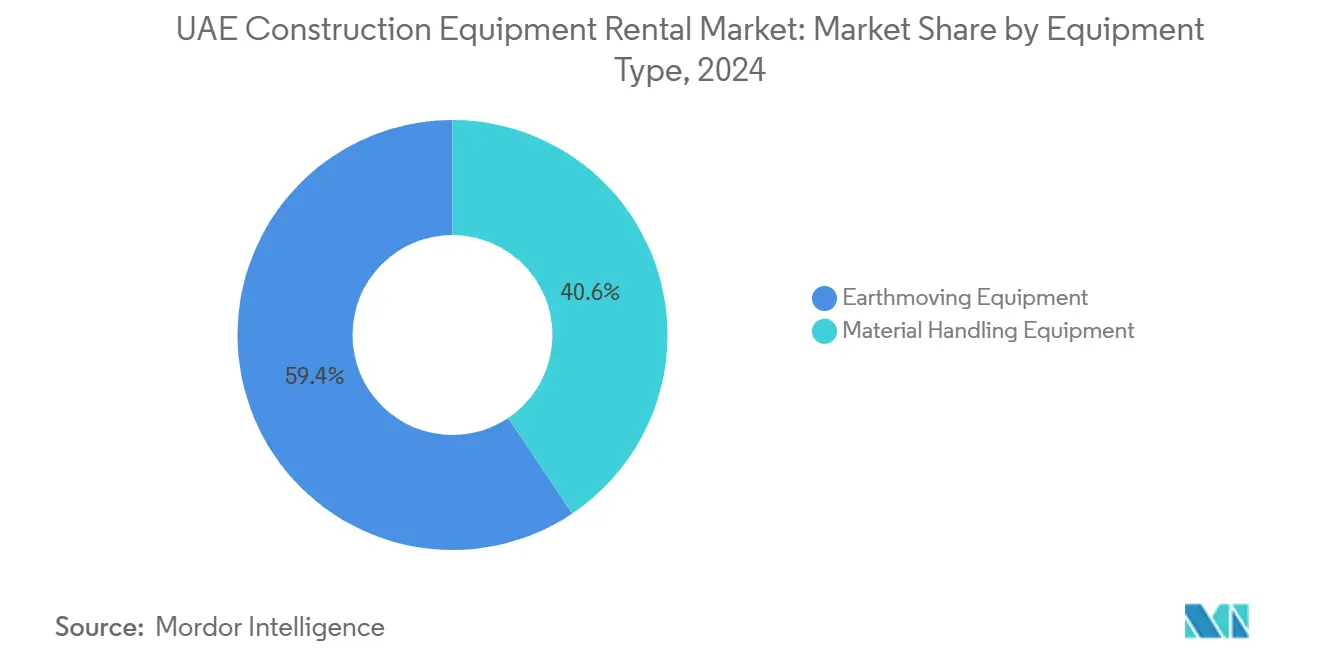

- By equipment type, earthmoving equipment held 59.41% of the UAE construction equipment rental market share in 2024, while material-handling equipment is advancing at a 9.32% CAGR to 2030.

- By propulsion, IC-engine models dominated 95.81% of the UAE construction equipment rental market share in 2024; hybrid and electric variants are rising at a 13.98% CAGR through 2030.

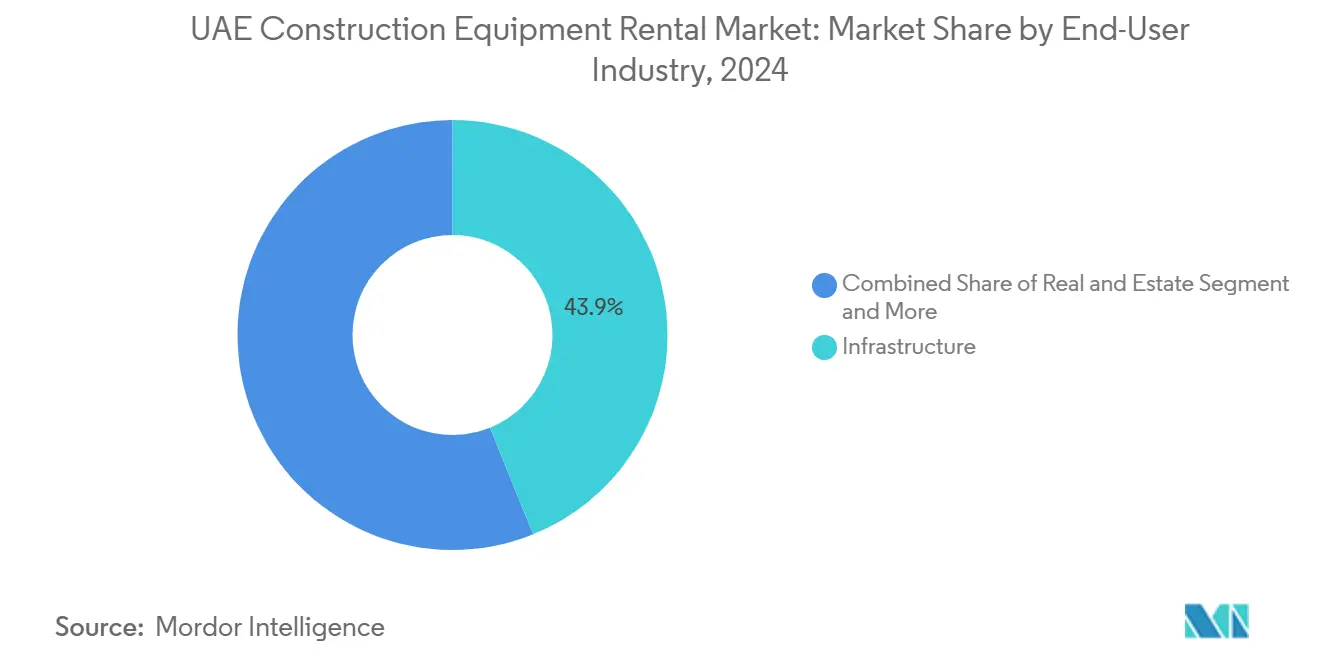

- By end-user industry, infrastructure accounted for a 43.87% slice of the UAE construction equipment rental market size in 2024. In contrast, mining and quarrying are forecast to expand at an 8.83% CAGR between 2025 and 2030.

- By power output, the 101-200 HP class captured 45.63% share of the UAE construction equipment rental market size in 2024; equipment above 400 HP is set to grow fastest at 9.54% CAGR to 2030.

- By region, Abu Dhabi and Al Ain led with 46.31% of the UAE construction equipment rental market share in 2024, while Sharjah and Northern Emirates recorded the highest projected CAGR at 8.59% through 2030.

UAE Construction Equipment Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mega Infrastructure Projects (Etihad Rail, Abu Dhabi Transport) | +2.1% | Abu Dhabi and Al Ain, Dubai, with spillover to Northern Emirates | Medium term (2-4 years) |

| CapEx-to-OpEx Shift Among EPCs | +1.8% | National, with early gains in Dubai, Abu Dhabi | Short term (≤ 2 years) |

| Renewables Driving Crane & Material-Handling Demand | +1.5% | National, concentrated in Abu Dhabi desert zones, Dubai South | Long term (≥ 4 years) |

| PPP Financing Unlocking Long-Term Rental Models | +1.3% | National, with concentration in Abu Dhabi government projects | Medium term (2-4 years) |

| Telematics-Enabled Platforms Boosting Fleet Uptime | +1.2% | National, with tech adoption leadership in Dubai, Abu Dhabi | Short term (≤ 2 years) |

| Hydrogen/Hybrid Fleets Aligning with Net-Zero 2050 Goals | +0.9% | National, pilot programs in Abu Dhabi, Dubai | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mega Infrastructure Pipeline Drives Equipment Demand Surge

Unprecedented megaproject activity anchors demand for large, versatile fleets across every emirate. Etihad Rail Phase 2 alone required machines during peak excavation, while the USD 4.9 billion Blue Line metro extension and USD 6.8 billion Strategic Sewerage Tunnel amplify multi-year equipment bookings [1]“Connecting the Emirates,”, Etihad Rail, etihadrail.ae. Contractors favor renting to match fleet size with phased workloads, avoiding the balance-sheet burden of owning specialized assets that may sit idle between contracts. Airports, ports, and logistics hubs add another sustained layer of demand, ensuring the UAE construction equipment rental market remains structurally tight.

Renewable-Energy Build-Out Amplifies Specialized Equipment Needs

Utility-scale solar parks, hydrogen electrolyzer farms, and battery storage plants demand precision lifting gear, desert-rated aerial platforms, and explosion-proof material-handling systems. Crane hours per megawatt installed at the Mohammed bin Rashid Solar Park exceed traditional building norms, driving a sharp uptick in high-tonnage crawler cranes. Because these projects lie in remote desert zones, contractors depend on rental providers that can deliver, maintain, and service equipment on-site, often bundling operator services under the same contract.

Digital Platforms Revolutionize Fleet Utilization Through Telematics

Leading platform operators say marketplace portals equipped with telematics have cut average idle time. Sensors transmit engine hours, fuel burn, and location data in real time, enabling predictive maintenance scheduling and automated billing tied to actual use. For contractors handling multiple sites across the Emirates, dashboards that consolidate fleet health and availability reduce logistical friction, reinforcing the shift toward the UAE construction equipment rental market [2]“Fleet Performance White Paper,”, Tenderd FZ-LLC, tenderd.com.

Hydrogen-Ready Fleets Align With Net-Zero Ambitions

Hydrogen fuel-cell trials on heavy trucks and excavators validate performance in the Gulf’s high-temperature conditions. Rental firms responding to customer ESG requirements import limited batches of hydrogen or battery-electric equipment, commanding premium daily rates to offset higher capex. The government plans to install more public chargers by 2035, creating a supportive ecosystem for broader adoption, even if on-site high-capacity charging remains a deployment constraint.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Material Costs Squeezing Project Budgets | -1.4% | National, with acute impact in Dubai, Abu Dhabi | Short term (≤ 2 years) |

| Skilled Operator Shortages and Tightening Visa Rules | -1.1% | National, with concentration in Northern Emirates, Dubai | Medium term (2-4 years) |

| Limited On-Site Charging Slowing Electric Equipment Adoption | -0.8% | National, with infrastructure gaps in remote project sites | Medium term (2-4 years) |

| Grey-Market Imports Diluting Rental Pricing | -0.6% | National, with concentration in free-zone areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Charging Infrastructure Gaps Limit Electric Equipment Adoption

Although the national EV policy supports public chargers, most units cater to passenger cars. High-duty construction machinery can require 50-150 kW chargers, which are rarely available on remote sites. Diesel gensets persist as backup, diluting the emissions advantage and dampening immediate demand for battery-electric excavators and loaders.

Grey-Market Imports Pressure Rental Rate Structures

Used machinery, circumventing full customs duties under free-zone exemptions, enters the country at a lower landed cost. Smaller contractors willing to trade reliability for upfront savings introduce low-price competition, compelling formal rental firms to defend value on service quality, safety certifications, and guaranteed uptime.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Earthmoving Dominance Amid Material-Handling Acceleration

Earthmoving equipment generated 59.41% of the UAE construction equipment rental market revenue in 2024, reflecting persistent demand from highways, airports, and rail corridors that require high-capacity excavation, grading, and paving. Excavators represent the workhorse subsegment, followed by bulldozers and motor graders that shape large-scale civil works. Contractors rent these machines to stay asset-light, using short-term leases during intensive groundwork phases and then off-renting as sites transition to vertical construction.

Material-handling equipment is the fastest-growing slice, projected at a 9.32% CAGR through 2030. Growth stems from logistics hub expansion, utility-scale solar plants, and data-center builds that demand precision lifts and aerial access. Telescopic handlers and spider cranes serve indoor fit-out and congested urban plots, while all-terrain cranes support panel installation across vast desert solar farms. This divergence in growth profiles illustrates how the UAE construction equipment rental market adapts to legacy infrastructure spending and emerging high-tech facilities.

By Propulsion: IC-Engine Leadership Challenged by Electric Transition

IC-powered models commanded 95.81% of the fleet in 2024 thanks to robust refueling infrastructure and proven reliability. Contractors favor diesel equipment for heavy, continuous duty cycles, especially where on-site power is scarce. Rental providers leverage established supply chains for consumables and spare parts, ensuring quick turnaround on maintenance and minimizing downtime.

Hybrid and electric machines are still in the niche and are expanding at a 13.98% CAGR. Early adoption is concentrated in material-handling categories such as forklifts, scissor lifts, and small loaders, whose duty cycles align with current battery capacities. Premium daily rates reflect higher capex, yet clients working under green-building mandates or urban emission caps accept the upcharge. The UAE construction equipment rental market size for electric variants is set to accelerate as the scale and battery density of charging solutions improve.

By End-User Industry: Infrastructure Leadership With Mining Momentum

Infrastructure contributed 43.87% of the UAE construction equipment rental market size in 2024, underpinned by rail, metro, airport, and port megaprojects that lock in multi-year equipment demand. Long project timelines favor rental over ownership, enabling EPC consortia to match fleet size with construction phases without straining balance sheets.

Mining and quarrying, aided by upstream commodity projects and domestic processing plants, is growing the fastest at an 8.83% CAGR. High-horsepower loaders, articulated dump trucks, and drilling rigs experience extended shift lengths, compelling operators to favor rental packages that include maintenance teams and parts inventory on site. As the scale of mineral extraction scales, the UAE construction equipment rental market share attached to this vertical is expected to expand materially.

By Power Output Rating: Mid-Range Dominance With High-Power Growth

Equipment rated 101-200 HP secured 45.63% of revenue in 2024 due to its versatility across general construction tasks. Mid-range excavators, wheel loaders, and telescopic handlers strike an optimal balance between productivity and fuel economy, making them staples in mixed-fleet packages offered by rental houses.

Machines above 400 HP are on the fastest growth path at 9.54% CAGR, driven by bulk earthworks, tunneling, and heavy-lift operations associated with rail embankments and deep-port dredging. These behemoths carry steep daily hire rates and often require specialized transport and certified operators, encouraging contractors to outsource ownership risks entirely. As megaproject scopes expand, demand for ultra-high-power classes will climb, lifting the UAE construction equipment rental market size attributable to heavy-duty segments.

Geography Analysis

Abu Dhabi and Al Ain held 46.31% of 2024 market revenue, buoyed by federal spending on Etihad Rail, industrial zones, and oil-and-gas capacity upgrades. EPC consortia place multi-year rental orders covering excavators, tunnel-boring support gear, and high-tonnage cranes, affording providers predictable utilization and favorable pricing. Vigorous regulatory enforcement around safety and emissions further tilts demand toward established rental firms able to supply certified fleets.

Given its commercial hub and innovation testbed status, Dubai remains a pivotal node. Projects such as the Blue Line metro, Al Maktoum Airport expansion, and high-rise clusters along Sheik Zayed Road call for advanced telematics-enabled machinery and low-emission variants suitable for dense urban environments. Rental companies that bundle equipment with BIM-compatible data feeds and operator training gain a competitive edge.

Sharjah and Northern Emirates post the fastest CAGR at 8.59% thanks to manufacturing diversification, port expansions, and cost-competitive industrial estates. The region’s proximity to primary logistics corridors and access to labor pools encourage small and mid-size contractors to tap rental fleets rather than import or purchase machinery, widening the footprint of the UAE construction equipment rental market. Fujairah’s deep-port dredging and Ras Al Khaimah’s quarrying activities additionally generate niche demand for specialized rock-handling and marine equipment.

Competitive Landscape

The UAE construction equipment rental market shows moderate concentration. Top national fleets, Al Faris Group, Kanoo, and Al-Bahar Cat Rental Store-leverage nationwide depots, certified operators, and 24/7 maintenance coverage. Their economies of scale support bulk buying of Tier 4-Final machines and early adoption of hybrid cranes, allowing them to meet strict project specifications quickly.

Digital disruptors like Tenderd integrate IoT sensors and AI-driven scheduling to elevate utilization and shrink idle capacity. By matching equipment owners to contractors on a real-time platform, they erode transactional friction and introduce dynamic pricing that can undercut traditional day-rate structures on commodity machines. Incumbents respond by embedding telematics across fleets and offering subscription-style packages that wrap equipment, service, and analytics into a single invoice.

Specialist providers focus on niche categories, Atlas Copco in compressed-air and power modules, or Liebherr with heavy-lift cranes, supplying turnkey solutions, including application engineering, operator certification, and compliance documentation[3]“Rental Solutions Middle East,”, Atlas Copco AB, atlascopco.com. Competitive advantage in these pockets rests less on fleet size and more on technical know-how and response time. As sustainability mandates sharpen, differentiation increasingly hinges on supplying hydrogen-ready or battery-electric options coupled with verified lifecycle emissions data.

UAE Construction Equipment Rental Industry Leaders

Byrne Equipment Rental

Al Marwan Machinery

Johnson Arabia LLC

Mohamed Abdulrahman Al-Bahar. (Cat Rental)

Dayim Equipment Rental

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Al Marwan Heavy Machinery has bolstered its dump truck rental fleet with the addition of 40 Ton Caterpillar Articulated Dump Trucks. This move not only strengthens the company's capabilities but also broadens its offerings, positioning it to better support the region's most intricate infrastructure projects. The strategic enhancement aims to provide clients with increased flexibility, efficiency, and power in construction.

- January 2025: In a strategic move to bolster its market leadership in the Middle East, Rapid Access has expanded its fleet with new machines sourced from Dingli. The newly added fleet boasts a versatile array of booms and scissor lifts, tailored to meet the diverse needs of various sectors.

UAE Construction Equipment Rental Market Report Scope

| Earthmoving Equipment | Backhoe Loaders | |

| Wheel Loaders | ||

| Excavators | ||

| Bulldozers | ||

| Asphalt Pavers | ||

| Motor Graders | ||

| Other Earthmoving Equipment | ||

| Material Handling Equipment | Cranes | |

| Dump Trucks | ||

| Forklifts | ||

| Telescopic Handlers | ||

| Aerial Platforms | Articulated Boom Lifts | |

| Telescopic Boom Lifts | ||

| Scissor Lifts | ||

| IC Engine |

| Hybrid and Electric |

| Infrastructure | Roads |

| Rail | |

| Airports | |

| Ports | |

| Real Estate | Residential |

| Commercial | |

| Mining & Quarrying | |

| Others |

| Less than 100 HP |

| 101 - 200 HP |

| 201 - 400 HP |

| Greater than 400 HP |

| Abu Dhabi and Al Ain |

| Dubai |

| Sharjah and Northern Emirates |

| Other Emirates (Ajman, Fujairah, Ras Al Khaimah, Umm Al Quwain) |

| By Vehicle Type | Earthmoving Equipment | Backhoe Loaders | |

| Wheel Loaders | |||

| Excavators | |||

| Bulldozers | |||

| Asphalt Pavers | |||

| Motor Graders | |||

| Other Earthmoving Equipment | |||

| Material Handling Equipment | Cranes | ||

| Dump Trucks | |||

| Forklifts | |||

| Telescopic Handlers | |||

| Aerial Platforms | Articulated Boom Lifts | ||

| Telescopic Boom Lifts | |||

| Scissor Lifts | |||

| By Propulsion | IC Engine | ||

| Hybrid and Electric | |||

| By End-User Industry | Infrastructure | Roads | |

| Rail | |||

| Airports | |||

| Ports | |||

| Real Estate | Residential | ||

| Commercial | |||

| Mining & Quarrying | |||

| Others | |||

| By Power Output Rating | Less than 100 HP | ||

| 101 - 200 HP | |||

| 201 - 400 HP | |||

| Greater than 400 HP | |||

| By Geography | Abu Dhabi and Al Ain | ||

| Dubai | |||

| Sharjah and Northern Emirates | |||

| Other Emirates (Ajman, Fujairah, Ras Al Khaimah, Umm Al Quwain) | |||

Key Questions Answered in the Report

What is the 2025 value of the UAE construction equipment rental market?

The market is valued at USD 1.72 billion in 2025, reflecting sustained demand across infrastructure and industrial projects.

How fast is the UAE construction equipment rental market expected to grow?

It is forecast to expand at an 8.52% CAGR, reaching USD 2.59 billion by 2030.

Which emirate leads rental demand?

Abu Dhabi & Al Ain account for the largest share at 46.31%, driven by federally backed megaprojects.

Which equipment category is growing the fastest?

Material-handling machinery, including cranes and aerial platforms, is projected to rise at a 9.32% CAGR through 2030.

What is the major challenge for rental providers in the near term?

Escalating material costs and skilled-operator shortages squeeze margins and could limit fleet deployment capacity over the next two years.

Page last updated on: