Qatar Car Rental Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

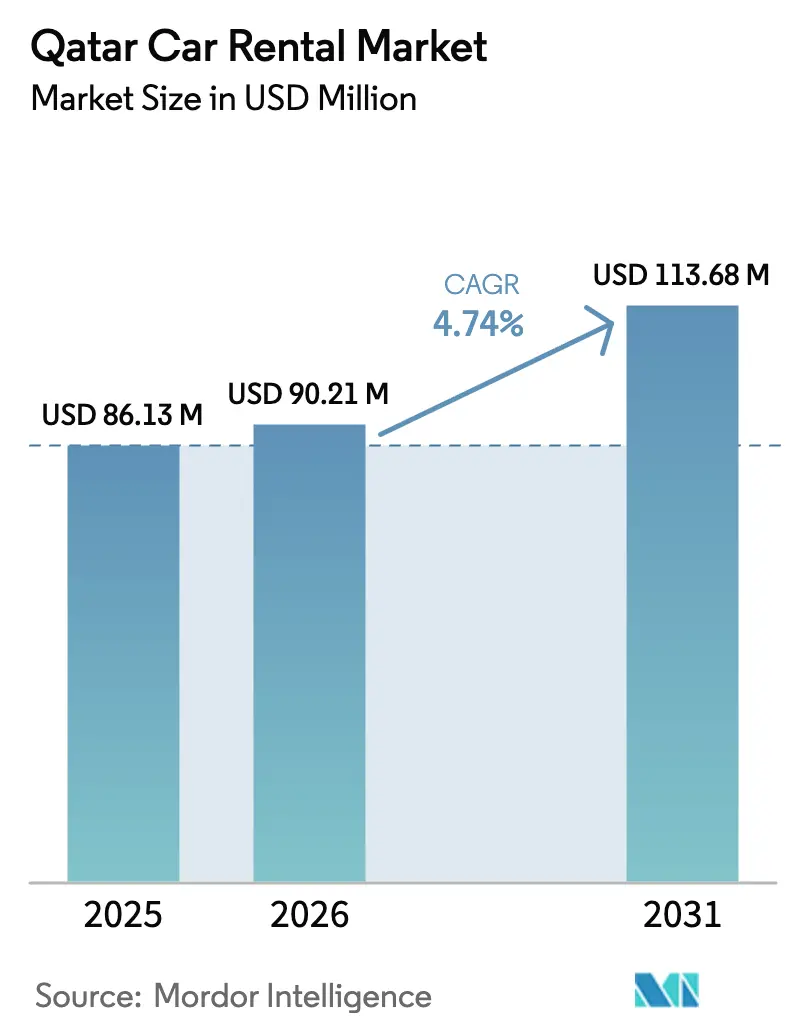

| Base Year Market Size (2025) | USD 86.13 Million |

| Market Size (2026) | USD 90.21 Million |

| Market Size (2031) | USD 113.68 Million |

| Growth Rate (2026 - 2031) | 4.74% CAGR |

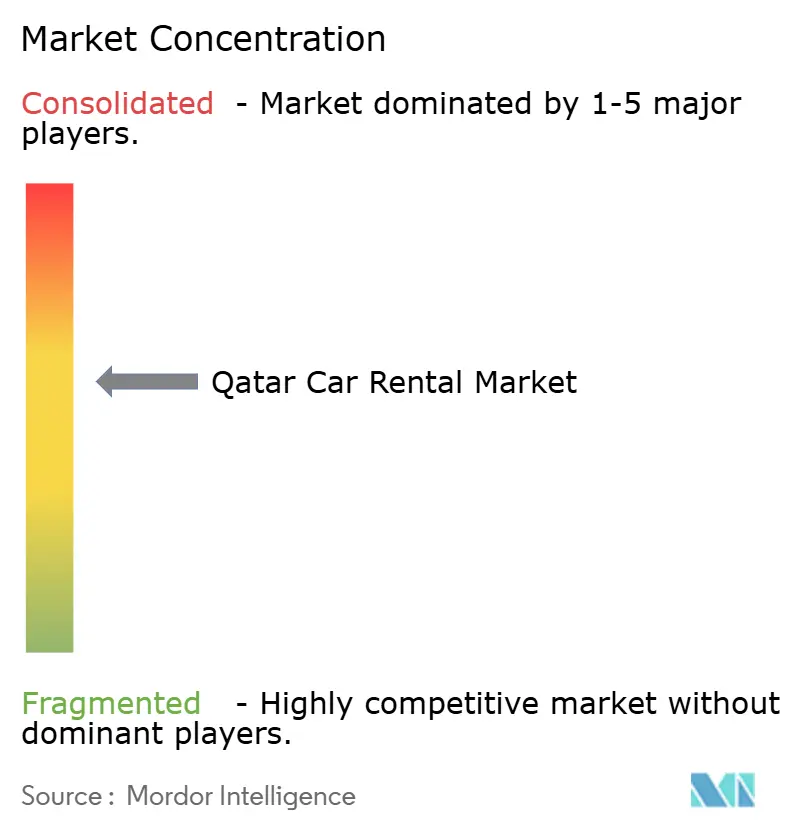

| Market Concentration | Medium |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Car Rental Market Analysis by Mordor Intelligence

The Qatar Car Rental Market size was valued at USD 86.13 million in 2025 and estimated to grow from USD 90.21 million in 2026 to reach USD 113.68 million by 2031, at a CAGR of 4.74% during the forecast period (2026-2031). Sustained post-FIFA visitor arrivals, LNG-linked corporate investments, and rapid smartphone-led digitalization are shaping the growth path. The country’s visa-free stopover incentives encourage transit passengers to prolong stays, while a high GDP per capita underpins steady discretionary spending on mobility. International brands and local operators share a moderately concentrated playing field; yet, differentiated fleet offerings, particularly in electric vehicles, provide room for competitive separation. Demand volatility during the extreme summer period and ride-hailing substitution add layers of operational complexity, compelling firms to refine fleet planning, pricing, and value-added service mixes.

Key Report Takeaways

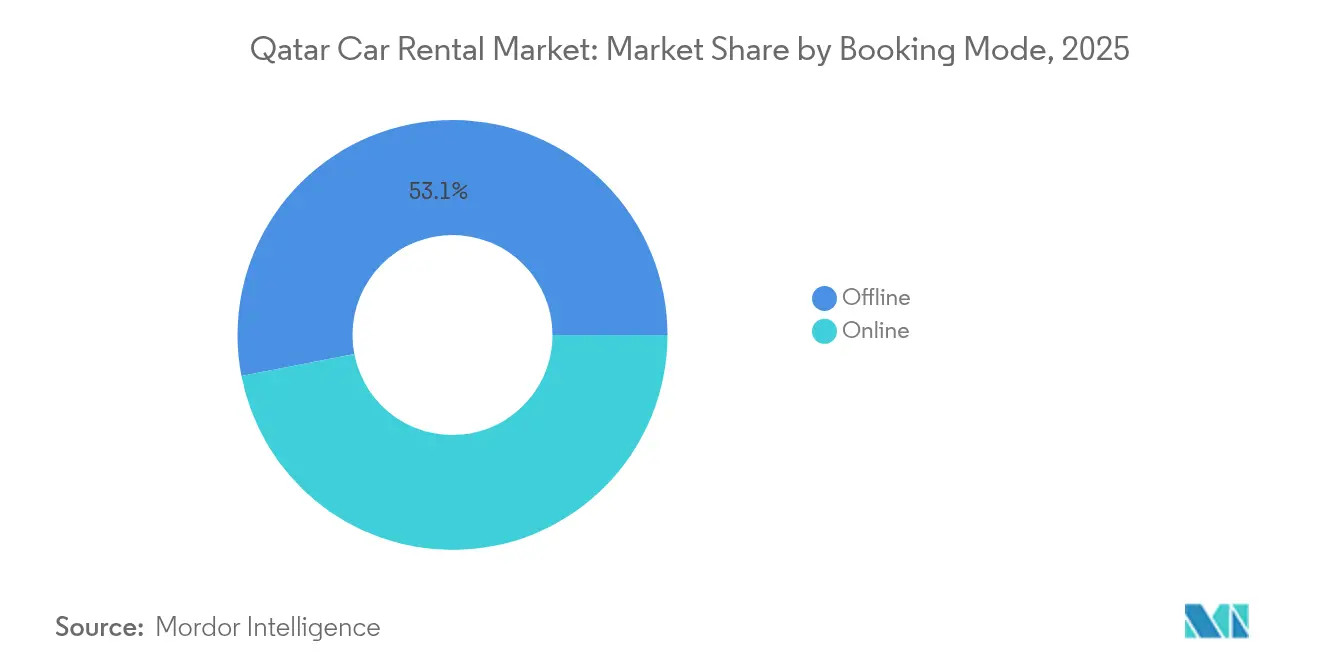

- By booking mode, online bookings led growth at a 4.75% CAGR between 2026 and 2031; yet, offline channels retained 53.05% of Qatar's car rental market share in 2025.

- By application, leisure applications captured 62.85% of Qatar's car rental market share in 2025, while business use is projected to post the highest growth at a 4.80% CAGR to 2031.

- By end-user, self-drive individual users held 47.60% of Qatar's car rental market share in 2025, whereas peer-to-peer rentals are forecast to expand at a 4.82% CAGR through 2031.

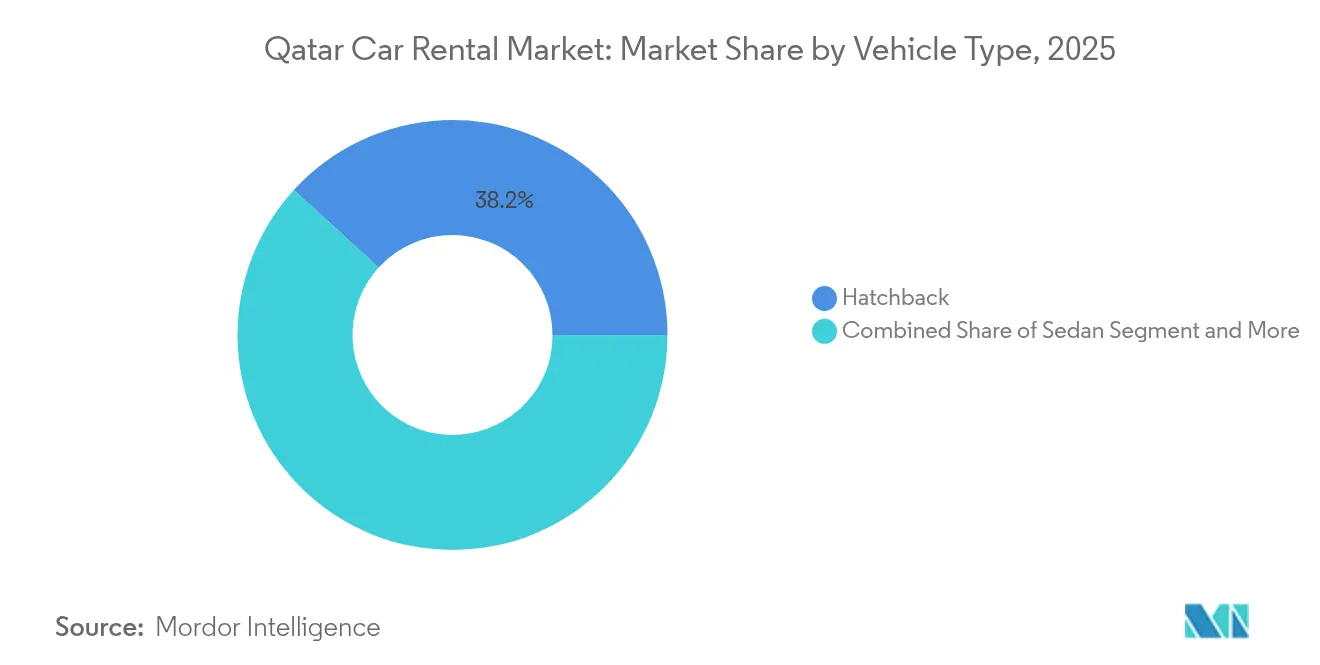

- By vehicle type, hatchbacks accounted for 38.21% of the Qatar car rental market size in 2025; however, SUVs exhibit the fastest trajectory, growing at a 4.78% CAGR over 2026-2031.

- By rental length, short-term rentals accounted for 57.10% of the Qatar car rental market size in 2025, and long-term rentals are projected to advance at a 4.79% CAGR during the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Qatar Car Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FIFA-2022 Legacy Tourism Momentum | +1.2% | National, with concentration in Doha and West Bay | Medium term (2-4 years) |

| Rapid Adoption of Digital Booking Apps | +0.9% | National, with urban concentration | Short term (≤ 2 years) |

| LNG-Sector Business-Travel Inflows | +0.8% | National, with focus on industrial zones and Doha | Long term (≥ 4 years) |

| Gig-Economy Demand Amid Expat Ownership CAPS | +0.7% | National, with expatriate community concentration | Long term (≥ 4 years) |

| Government Stop-Over Tourism Incentives | +0.6% | National, with Hamad International Airport focus | Medium term (2-4 years) |

| Fleet Electrification Push | +0.4% | National, with urban pilot programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

FIFA-2022 Legacy Tourism Momentum

The World Cup transformed perceptions of Qatar and anchored a recurring visitor base that counteracts the typical post-event slump. IMF data indicate that transportation services are expected to remain robust through 2024, signaling sustained demand for mobility. Rental companies benefit from a nationwide highway grid and multilingual signage that simplify self-driving. The compact land area encourages day-trip itineraries beyond Doha, further lifting car usage. High seasonal visitor peaks reduce off-hire risk, supporting steady fleet utilization. In turn, operators can refresh their fleets more frequently, thereby maintaining high vehicle quality and customer satisfaction.

Rapid Adoption of Digital Booking Apps

High smartphone penetration and the state’s Digital Agenda 2030 accelerate online migration. The 2025 QIC–Alfardan Automotive integration, featuring BMW, Mini, Land Rover, and Jaguar rentals within a mobile app, showcases the seamless bundling of insurance, booking, and maintenance services offered [1]“QIC App Wins Mobile App of the Year,” Qatar Insurance Company, qic.qa . Digital channels reduce counter wait times and enable contactless pickups, which have become a baseline consumer expectation following the COVID-19 pandemic. Dynamic pricing engines improve yield management, while real-time fleet visibility reduces idle ratios. Operators using app-based platforms capture cost efficiencies that fund service innovations, such as delivery and collection options.

LNG-Sector Business-Travel Inflows

Qatar’s status as the largest LNG exporter continues to attract engineers, executives, and consultants who require prolonged stays. The IMF projects real GDP growth of over one-tenth over the medium term, primarily driven by LNG expansions [2]“Qatar 2024 Article IV Consultation,” International Monetary Fund, imf.org . Corporate travelers typically rent premium sedans and SUVs for weeks, generating higher ticket values than leisure bookings. Predictable demand enables firms to invest in larger fleets and specialized services, such as chauffeur options. Business visitors also display lower seasonality than tourists, smoothing fleet utilization across summer troughs.

Government Stop-Over Tourism Incentives

Qatar Airways, leveraging its vast network, and Hamad International, with its hub status, channel transit passengers through Doha. A visa-free policy, coupled with subsidized hotel packages, transforms mere layovers into extended multi-day stays. These brief interludes boost rentals for city tours and desert adventures. Significant public investment in upgrading hospitality assets further enriches visitor experiences. Guests on stopovers usually opt for compact cars for short durations, balancing the long-stay corporate demand and softening seasonal lulls.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extreme-Summer Demand Volatility | -0.9% | National, with peak impact in inland areas | Short term (≤ 2 years) |

| Ride-Hailing Substitution | -0.6% | Urban areas, particularly Doha metropolitan | Medium term (2-4 years) |

| Spare-Parts Supply-Chain Inflation | -0.4% | National, with higher impact on fleet operators | Medium term (2-4 years) |

| Proposed Doha Congestion Pricing | -0.3% | Doha metropolitan area and central business district | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Extreme-Summer Demand Volatility

During the peak summer months, extremely high temperatures deter outdoor tourism and dampen leisure bookings. Rental firms, holding onto inflated winter fleets, find themselves with idle cars during the off-season. The combination of intense cabin-cooling demands and scorching asphalt not only accelerates tire wear but also strains air-conditioning components, leading to heightened maintenance costs. Smaller operators, constrained by limited credit lines, grapple with cash flow challenges during months of low occupancy. To counter these hurdles, some have turned to promotional summer rates and shifted vehicles towards corporate clients, who are less affected by weather fluctuations.

Ride-Hailing Substitution (Uber, Careem)

App-based rides compete for airport transfers and intra-city hops, eroding a lucrative slice of rental revenue. Careem’s regional acquisition of Swapp signals the convergence of ride-hailing and short-term rental on a single platform [3]“Careem invests in Swapp to broaden mobility services,” Careem, careem.com . However, multi-day self-drive journeys and desert tours remain less susceptible to substitution. To counter displacement, operators offer bundled fuel packages and loyalty points as incentives. Achieving parity with ride-hailing apps in terms of technology is now essential, including instant reservation confirmation and transparent pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Booking Mode: Digital Channels Drive Market Evolution

The online channel recorded a 4.75% CAGR over 2026-2031, while offline sales retained majority status with 53.05% of Qatar's car rental market share in 2025. Digital uptake mirrors rising e-commerce confidence and extensive 5G coverage. QIC’s tie-up with Alfardan enables premium renters to secure vehicles directly through an insurance app, underscoring the convergence of platforms. Dynamic discounting and push-notification promotions encourage direct bookings.

Offline counters still dominate because many travelers value face-to-face service, especially when arranging add-ons such as child seats or cross-border permissions. Airport kiosks offer immediate keys for late-booking visitors. Domestic users from markets with lower digital adoption also prefer walk-in interactions. Although the growth gap widens yearly, a blended channel approach remains prudent to capture the full demand spectrum.

By Application: Leisure Dominance with Business Growth Potential

Leisure trips accounted for 62.85% of Qatar's car rental market share in 2025 and are expected to expand at a 4.80% CAGR, driven by event tourism and government efforts to promote cultural assets. Packages that pair desert safaris with car rentals boost uptake of SUVs and MPVs. Short-stay tourists often opt for pay-per-day deals that include zero excess coverage for added peace of mind.

Business use, while smaller, promises steadier revenue through long-term contracts with oil and gas majors. Non-hydrocarbon grew significantly in the first three quarters of 2024, spurring cross-sector corporate travel, according to IMF.ORG. Multinational firms favor leased fleets and chauffeur services to ensure consistent transportation for executives and project personnel. This subset often insists on premium brands, which in turn lifts average daily rates.

By End-User: Self-Drive Individual Leads, P2P Rental Disrupts

Self-drive individuals held a 47.60% market share in 2025, reflecting travelers' growing desire for personal control over their itineraries. Competitive daily pricing and a wide variety of vehicles fuel adoption. Clear signage and English-Arabic navigation apps simplify driving for tourists, strengthening uptake.

Peer-to-peer rental, although nascent, is growing at the fastest rate of 4.82% CAGR. Expats and younger residents value access over ownership, using marketplace apps to secure vehicles for weekends. Regulatory gaps in insurance and liability remain a growth brake; yet, once resolved, traditional firms may need to launch in-house P2P platforms to stay relevant. Chauffeur-driven services meet premium expectations, especially during the summer when visitors prefer not to drive in peak heat.

By Vehicle Type: Hatchback Dominance Faces SUV Challenge

Hatchbacks accounted for 38.21% of the market share in 2025, driven by their affordability, maneuverability, and lower fuel consumption-attributes well-suited to Doha’s dense traffic. Rental companies buy hatchbacks in bulk to manage fleet-wide costs and offer entry-level price points.

SUVs are growing at a 4.78% CAGR due to family tourism and cultural preferences for larger vehicles. Elevated ride height, ample luggage space, and a perceived sense of safety resonate well with Gulf consumers. Desert excursions and multi-generational travel parties are driving the uptake of SUVs, prompting operators to expand their model choices from economy to luxury trims.

By Rental Length: Short-Term Dominance with Long-Term Growth

Short-term hires accounted for 57.10% of the Qatar car rental market size in 2025, reflecting visitor profiles with stays of three to seven days. Bundled GPS, unlimited mileage, and easy return policies help drive adoption. Seasonal demand peaks during winter encourage dynamic price spikes, maximizing margins.

Long-term rentals are expected to grow at a 4.79% CAGR, driven by expatriates who are restricted from car ownership under specific visa categories. Subscription models offering inclusive maintenance and insurance strike a chord with contract workers. Fleet managers mitigate seasonality by rotating vehicles between short-term and long-term pools based on demand forecasts.

Geography Analysis

Doha and the surrounding suburbs act as the nucleus of the Qatar car rental market, stimulated by Hamad International’s role as a global hub. Continuous flows of stopover tourists and LNG executives ensure steady counter traffic and online bookings. Industrial hubs at Ras Laffan and Mesaieed inject predictable demand tied to construction schedules and maintenance shutdowns. Towns on the Dukhan Highway attract leisure drivers visiting beaches and heritage sites, amplifying weekend peaks.

Infrastructure quality underpins seamless road trips; multilane highways link north–south corridors, enabling same-day excursions between markets and tourist spots. Stronger connections to GCC neighbors through highway upgrades foreshadow cross-border rental packages once regional insurance protocols align. Further afield, the north-eastern mangrove reserves spur niche eco-tourism rentals outfitted with roof racks and kayaking gear.

Centralized economic activity compresses competitive turf within Doha, raising real estate costs for airport kiosks and downtown branches. However, proximity lowers fleet relocation expenses, enabling same-day vehicle shuffling between depots. Government smart-city plans introduce connected-road pilots that could later feed data to rental platforms for real-time route optimization. As urban expansion continues toward Lusail, strategic branch openings along the Red Line metro create fresh touchpoints.

Competitive Landscape

International brands such as Hertz, Avis, Budget, and Sixt leverage global booking engines and loyalty programs to draw inbound travelers. Local champions like Al Muftah Rent A Car and Strong Rent A Car compete based on cultural familiarity, bilingual staff, and flexible negotiation. Moderate concentration allows both tiers to coexist while targeting different customer slices.

Technology adoption differentiates winners. International players deploy contactless kiosks and digital key-drop lockers, cutting queue times. Local firms invest in WhatsApp-based customer support to align with regional communication habits. The QIC–Alfardan partnership illustrates how insurers and dealership groups harness bundled mobility, spreading risk across underwriting and rental income streams.

Fleet electrification emerges as the next frontier, driven by national goals to achieve a 20% renewable energy capacity by 2030. Early movers experimenting with EV imports capitalize on environmentally conscious visitors and corporate sustainability mandates. Charging infrastructure remains limited; however, joint ventures with shopping malls and hotels help fill these gaps. Ride-hailing platforms’ expansion into short-term rental compels traditional firms to accelerate app development and modernize CRM systems.

Qatar Car Rental Industry Leaders

Al- Mulla

Al Saad Rent A Car Co.W.L.L

Al Sayer

Avis Corporation

Europcar

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Infinity Rent-A-Car received 50 new Mitsubishi Xpander vehicles from Qatar Automobiles Company to diversify its offerings.

- October 2024: The UK-based global car rental network Finalrentals announced its strategic expansion into Qatar through a partnership with local firm Safety Rent a Car. This move aims to provide digitally driven rental services across Doha, including at the airport.

- May 2024: CARWIZ International announced a significant expansion into 16 new countries, including Qatar, planning to offer a range of luxury vehicles to the Middle Eastern clientele.

Qatar Car Rental Market Report Scope

A car rental company, rental car, or car rental agency is a business that leases cars to the public for short periods of time, usually from a few hours to a few weeks.

The Qatar Car Rental Market is segmented on the basis of Booking Type, Application, Vehicle Type, End-User. By Booking Type, the market is segmented into, Online and Offline. By Application, the market is segmented into, Leisure/tourism and daily utility/business. By Vehicle Type, the market is segmented into, Economy Cars and Luxury Cars. By End-User, the market is segmented into, Self-driven and chauffer. The report offers market size and forecast in value (USD) for all the above segments.

| Offline |

| Online |

| Leisure |

| Business |

| Self-Drive Individual |

| Chauffeur-Drive |

| Corporate Fleet Subscription |

| Peer-to-Peer Rental |

| Hatchback |

| Sedan |

| Sports Utility Vehicles |

| Multi Purpose Vehicles |

| Short-Term |

| Medium-Term |

| Long-Term |

| By Booking Mode | Offline |

| Online | |

| By Application | Leisure |

| Business | |

| By End-User | Self-Drive Individual |

| Chauffeur-Drive | |

| Corporate Fleet Subscription | |

| Peer-to-Peer Rental | |

| By Vehicle Type | Hatchback |

| Sedan | |

| Sports Utility Vehicles | |

| Multi Purpose Vehicles | |

| By Rental Length | Short-Term |

| Medium-Term | |

| Long-Term |

Key Questions Answered in the Report

What is the expected growth rate of the Qatar car rental market through 2031?

The market is forecast to expand at a 4.74% CAGR, rising from USD 90.21 million in 2026 to USD 113.68 million by 2031.

Which booking channel is expanding the quickest in Qatar?

Online reservations are advancing at a 4.75% CAGR, outpacing offline sales, though counters still account for most bookings.

What factors stabilize demand outside the peak tourist season?

Long-term corporate rentals linked to LNG projects and expatriate workforce needs provide steady revenue during the hot summer months.

Which vehicle category is gaining ground on hatchbacks?

SUVs are the fastest-growing class with a 4.78% CAGR, driven by family tourism and cultural preferences for larger cars.

How are rental firms responding to ride-hailing competition?

Operators are deploying contactless booking apps, loyalty programs, and bundled fuel offers while exploring peer-to-peer and EV-based services.

What opportunity does the government’s stopover policy create?

Visa-free transit packages convert layovers into short city breaks, lifting short-term rental demand for compact cars and SUVs.

Page last updated on: