United Arab Emirates DOOH Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

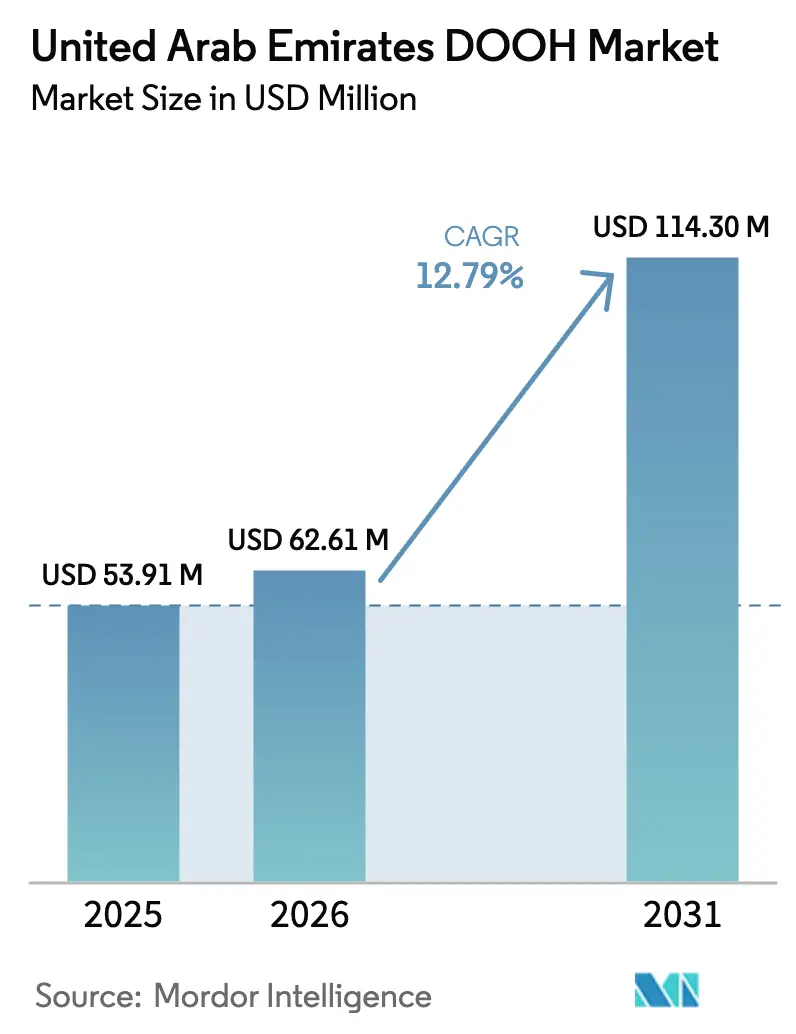

| Base Year Market Size (2025) | USD 53.91 Million |

| Market Size (2026) | USD 62.61 Million |

| Market Size (2031) | USD 114.30 Million |

| Growth Rate (2026 - 2031) | 12.79% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates DOOH Market Analysis by Mordor Intelligence

The United Arab Emirates DOOH market size was valued at USD 53.91 million in 2025 and estimated to grow from USD 62.61 million in 2026 to reach USD 114.3 million by 2031, at a CAGR of 12.79% during the forecast period (2026-2031). The expansion is propelled by advertisers’ pivot from static posters to data-fueled screens, rapid airport passenger recovery, and a nationwide smart-city agenda that embeds display networks into bus shelters, metro stations, and retail precincts. Programmatic buying platforms now allow brands to bid on impressions in real time, while 3D anamorphic content and high-brightness LED technology enable creative differentiation that commands premium prices. Municipal concessions along Sheikh Zayed Road, Dubai International Airport, and key malls remain the most sought-after assets, but rising lease costs are nudging smaller operators toward secondary corridors in Sharjah and the Northern Emirates. Privacy regulation enacted in 2021 has pushed media owners to adopt anonymized camera analytics, tempering public concerns without stalling deployment momentum.

Key Report Takeaways

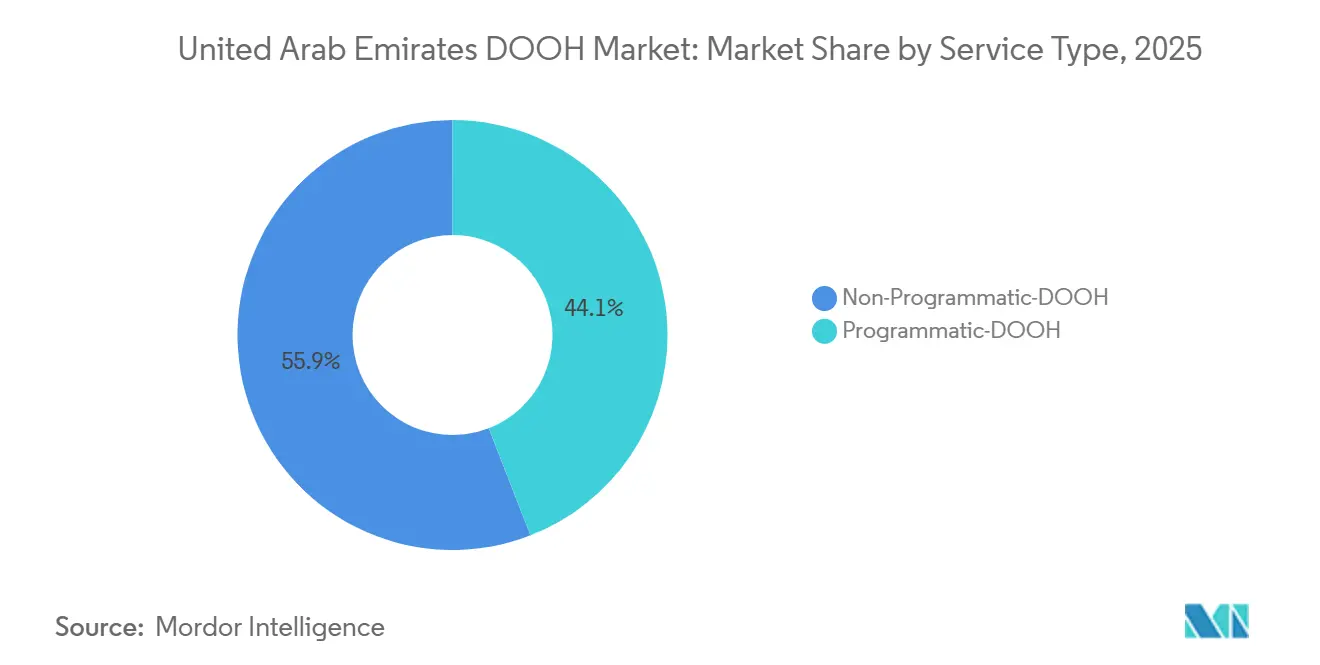

- By service type, non-programmatic screens led with 59.87% of United Arab Emirates digital out-of-home (DOOH) market share in 2025, while programmatic formats are advancing at a 16.03% CAGR through 2031.

- By application, billboards accounted for 37.89% of the United Arab Emirates DOOH market size in 2025, whereas transit screens are set to climb at a 15.27% CAGR to 2031.

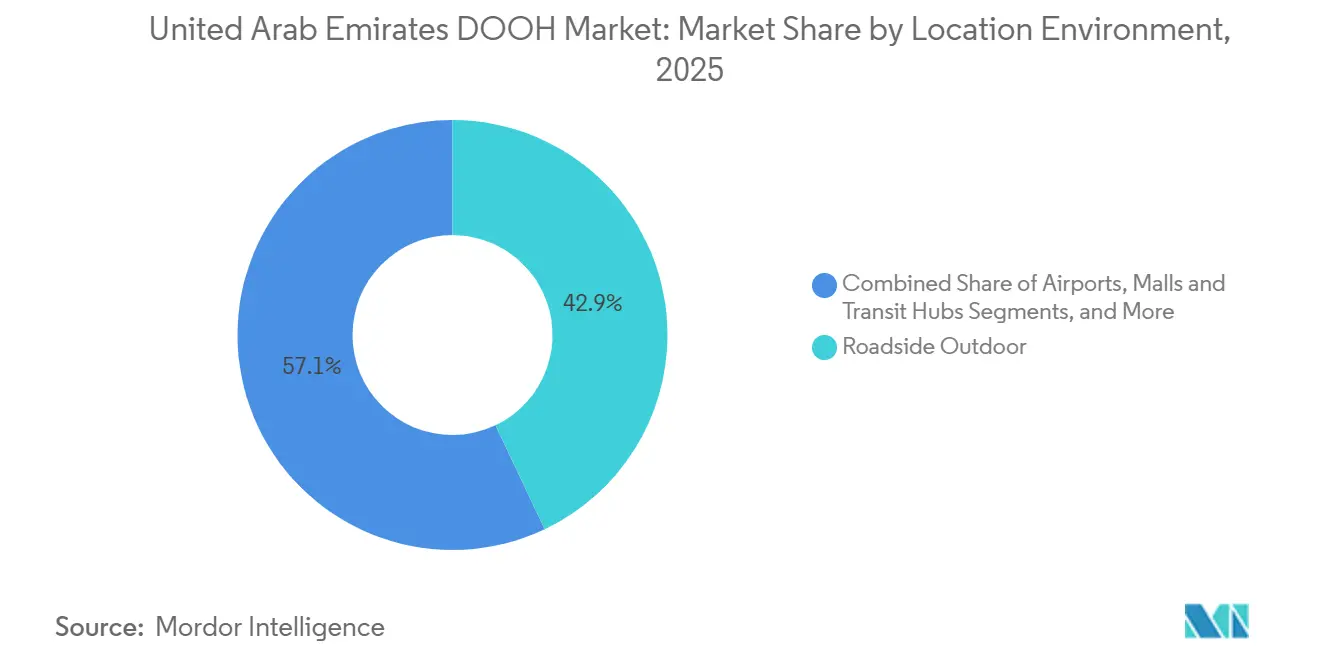

- By location environment, roadside displays dominated with 42.94% revenue share in 2025, yet airport inventory is projected to expand at a 15.42% CAGR over the forecast window.

- By end-user industry, retail topped spending at 27.06% in 2025, but automotive campaigns are forecast to post a 14.23% CAGR on the back of accelerating electric-vehicle launches.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates DOOH Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Brand-Led Shift from Static to Dynamic DOOH Formats | +3.2% | National, concentrated in Dubai and Abu Dhabi | Medium term (2-4 years) |

| Government Smart-City Initiatives Boosting Street Furniture Digitization | +2.8% | National, led by Dubai and Abu Dhabi municipalities | Long term (≥ 4 years) |

| Surge in Mall Footfalls by International Tourists Post-Expo 2020 | +2.1% | Dubai, Abu Dhabi, Sharjah | Short term (≤ 2 years) |

| Wider Programmatic Advertising Capabilities | +2.5% | National, early adoption in Dubai | Medium term (2-4 years) |

| Real-Time Data Integration with RTA Nol Card Ecosystem | +1.4% | Dubai and Northern Emirates served by RTA | Medium term (2-4 years) |

| Integration of 3D Anamorphic Content to Differentiate Premium Screens | +0.9% | Dubai premium corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Brand-Led Shift From Static to Dynamic DOOH Formats

Brands are diverting budgets away from printed billboards toward LED screens that enable day-part scheduling, rapid creative swaps, and campaign optimization within hours rather than weeks. BackLite Media reports eightfold revenue growth since digitizing its roadside network, underscoring the commercial upside of dynamic formats.[1]BackLite Media, “Digital Billboard Operations,” backlitemedia.com Luxury automakers launching electric models can update range claims and promotion details in near real time, aligning with evolving subsidy schemes. Eliminating print and installation costs frees funds for higher-visibility corridors, yet the upfront capital requirement for 4K LED panels and fiber connectivity favors well-financed incumbents. As a result, the United Arab Emirates digital out-of-home market continues to consolidate around operators with the balance sheet depth to retrofit entire networks at scale.

Government Smart-City Initiatives Boosting Street Furniture Digitization

The Roads and Transport Authority has rolled out 1,023 solar-powered smart bus shelters that stream transit data while doubling as high-dwell advertising nodes.[2]Roads and Transport Authority, “Smart Bus Shelters and Digital Infrastructure,” rta.ae Abu Dhabi’s Department of Municipalities and Transport is implementing comparable projects under Vision 2030, creating a consistent pipeline of municipal tenders for screen vendors. Solar mandates trim operating outlays and support the UAE’s net-zero-by-2050 pledge, strengthening the environmental credentials of outdoor campaigns. Digital street furniture also supports public-service broadcasts during emergencies, which eases permitting by demonstrating civic utility. Together, these smart-city programs embed advertising real estate into daily commuter journeys, underpinning long-run inventory growth across the United Arab Emirates digital out-of-home market.

Surge in Mall Footfalls by International Tourists Post-Expo 2020

Dubai hosted 24.3 million overnight visitors in 2024 and remains on track for further gains, funneling affluent tourists into The Dubai Mall and Mall of the Emirates. The Dubai Mall alone logged 105 million visits in 2023. Majid Al Futtaim’s Precision Media platform now pairs computer vision with programmatic buying to trigger context-aware ads inside its malls. Landlords are replacing static posters with interactive kiosks and LED walls, amplifying demand for premium indoor inventory. Abu Dhabi’s Yas Mall is mirroring this digital pivot to compete for spend from luxury houses and global electronics brands, adding further momentum to the United Arab Emirates digital out-of-home market.

Wider Programmatic Advertising Capabilities

JCDecaux’s Play+ integration across 378 airport screens enables advertisers to bid on impressions aligned with flight origin, destination, and passenger mix.[3]JCDecaux, “Play+ Programmatic Platform Launch,” jcdecaux.com Lemma Technologies advanced this automation with Lemma Phi, whose AI engine optimizes creative and day-parting based on real-time conditions.[4]Lemma Technologies, “Lemma Phi Launch,” lemmatechnologies.com Programmatic access lowers the friction of multi-city buys and attracts performance-oriented advertisers demanding measurable outcomes. Regional operators such as Elevision Media are onboarding exchanges like VIOOH to defend share against global platforms. As supply-side integrations mature, impression-level transparency will accelerate the scaling of programmatic spend across the United Arab Emirates digital out-of-home market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Location-Lease Costs along Sheikh Zayed Road | -1.8% | Dubai, particularly Sheikh Zayed Road and Downtown corridors | Short term (≤ 2 years) |

| Tight Municipal Content-Approval Lead Times | -1.3% | National, with stricter enforcement in Dubai and Abu Dhabi | Medium term (2-4 years) |

| Privacy Concerns over Camera-Enabled Audience Measurement | -0.9% | National, heightened in urban centers | Long term (≥ 4 years) |

| Limited Premium Location Availability | -0.7% | Dubai and Abu Dhabi CBDs, airport terminals | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Location-Lease Costs Along Sheikh Zayed Road

Annual leases for flagship LED sites range from AED 1.8 million to AED 2.5 million (USD 0.49-0.68 million), elevating total project budgets above USD 1 million after hardware, installation, and connectivity. Smaller entrants struggle to raise capital or secure finance terms long enough to amortize the outlays, reinforcing the dominance of established concessionaires in the United Arab Emirates digital out-of-home market. Long-tenor contracts also curb agility, as operators cannot readily exit or relocate inventory when new transit corridors emerge.

Tight Municipal Content-Approval Lead Times

Dubai Municipality requires creative submission at least 10 business days prior to flight, with Federal Decree-Law No. 55 of 2023 adding a national media-content layer that can extend reviews to three weeks for sensitive sectors.[5]Dubai Municipality, “Outdoor Advertising Regulations,” dm.gov.ae These windows clash with the on-demand promises of programmatic buying, forcing brands to pre-clear multiple ad variants or risk launch delays. The bottleneck is most disruptive for event-driven and limited-time promotions, nudging advertisers toward media channels with faster turnaround. Although Dubai’s new DANA permit portal applies automated checks, full harmonization across emirates remains a work in progress, tempering growth across the United Arab Emirates digital out-of-home market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Programmatic Builds Momentum Inside a Non-Programmatic Stronghold

Non-programmatic placements captured 59.87% of United Arab Emirates digital out-of-home market share in 2025, a lead sustained by long-standing roadside contracts with luxury and automotive advertisers. Programmatic formats, however, are scaling at a 16.03% CAGR as demand-side platforms standardize impression trading and attribution. JCDecaux’s airport rollout and Elevision’s VIOOH partnership demonstrate how real-time bidding is moving from proof of concept to operational norm in large-format environments. Because airport and mall landlords can verify dwell time and demographic profiles, they are accelerating supply-side integrations that support dynamic creative rotation and third-party data overlays.

The coexistence of both sales models is reshaping operational priorities. Media owners are retraining account executives to handle audience-based packages while IT teams upgrade content-management systems to support OpenRTB protocols. Non-programmatic deals remain appealing where brand safety and exclusive positioning are paramount, notably for four-year automotive launches or government awareness drives. Over the forecast horizon, programmatic’s share gains will lift inventory liquidity and broaden advertiser participation, reinforcing the long-term competitiveness of the United Arab Emirates digital out-of-home market.

By Application: Transit Screens Accelerate on Ridership Data, While Billboards Retain Brand-Building Clout

Billboards accounted for 37.89% of United Arab Emirates digital out-of-home market size in 2025, owing to spectacular LED walls along Sheikh Zayed Road and Emirates Road that reach millions of motorists weekly. Transit formats, fueled by Dubai Metro’s 230 million annual riders and 1,023 smart bus shelters, are predicted to surge at 15.27% CAGR. Transit’s advantage lies in longer dwell windows, often three to five minutes, during which commuters absorb multi-frame storytelling and interactive prompts.

Advertisers now tap Nol card datasets to cluster screens by rider demographics, boosting targeting precision compared with vehicular audiences that blur socio-economic segments. Nevertheless, roadside billboards remain unrivaled for blockbuster visibility, as illustrated by BackLite Media’s 3D Whoop campaign that generated viral social buzz. Going forward, a balanced inventory mix will persist: billboards safeguard upper-funnel objectives and global launches, while transit deployments court performance budgets from retail, banking, and telecom brands across the United Arab Emirates digital out-of-home market.

By Location Environment: Passenger Rebound Steers Spend Toward Airports Without Displacing Roadside Dominance

Roadside displays led revenue with 42.94% in 2025, anchored by Dubai’s arterial grid that accommodates dense vehicular flows. Airport environments are set to expand at a 15.42% CAGR, underpinned by 91.6 million travelers at Dubai International and 16.1 million at Abu Dhabi International in 2024. Average exposure time above 20 minutes amplifies recall and allows luxury retailers to tailor messages by flight origin or cabin class through platforms such as Play+.

LED integrations now stretch into mixed-use promenades, evidenced by Daktronics’ 2025 Yas Bay Waterfront installation that courts leisure tourists with immersive content. While roadside tenure remains secure for mass-reach vehicle launches and public-service campaigns, airports, malls, and entertainment districts will command accelerating budget share as advertisers chase affluent and experience-seeking audiences across the United Arab Emirates digital out-of-home market.

By End-User Industry: Automotive Adoption Quickens Amid Electric-Vehicle Surge

Retail held 27.06% of spend in 2025, reflecting weekly mall promotions and seasonal sale cycles. Automotive outlays are projected to climb at a 14.23% CAGR as electric-vehicle stocks rise toward 19,000 units by 2025, with incentives such as free parking and toll waivers fanning consumer interest. Brands exploit 3D content and dynamic range updates on LED megastructures to differentiate in a crowded launch calendar.

Healthcare providers are scaling transit placements to reach expatriate professionals, while banks deploy screens near CBDs to push digital-banking adoption. Media and entertainment firms activate burst campaigns around concerts and film releases, using impression pacing tools to match ticket sales curves. Together, these shifts diversify vertical exposure, making the United Arab Emirates digital out-of-home market less cyclical and more resilient to single-sector slowdowns.

Geography Analysis

Dubai and Abu Dhabi dominate spending, undergirded by dense transit systems, record tourist arrivals, and well-defined regulatory frameworks. Dubai’s 230 million metro trips, 1 billion Nol card swipes, and triple-digit mall visitation provide unrivaled frequency layers for campaign planning. The emirate’s DANA permit portal, launched October 2025, automates compliance and cuts approval cycles, accelerating screen rollouts.

Abu Dhabi aligns DOOH investments with Vision 2030, channeling funds into upgraded street furniture and terminal extensions targeting 40 million passengers by 2030. Prestige leisure enclaves on Yas and Saadiyat Islands attract high-spend audiences that command premium CPMs. Sharjah, Ajman, Umm Al Quwain, Ras Al Khaimah, and Fujairah collectively form a growth frontier, offering lower lease rates that appeal to price-sensitive advertisers priced out of Dubai arterials.

The UAE’s role as a Europe-Asia-Africa hub multiplies airport screen impact because a single placement reaches travelers from myriad origin markets within hours. However, such geographic concentration also concentrates risk; regulatory changes or economic shifts in Dubai could ripple through nationwide demand. Continued infrastructure expansion in the Northern Emirates may gradually balance exposure across the wider United Arab Emirates digital out-of-home market.

Competitive Landscape

The competitive field is moderately fragmented. Global majors like JCDecaux leverage cross-market scale and proprietary data stacks to secure airport and metro concessions. Regional champions, BackLite Media, Hypermedia, Next Level Media, anchor premium roadside corridors via long-run RTA contracts, exemplified by BackLite’s AED 1 billion Sheikh Zayed Road mandate. Technology vendors LG Electronics, Samsung Electronics, and Daktronics supply LED modules, CMS platforms, and remote diagnostics, often in partnership with venue operators such as Expo City Dubai.

Smaller operators exploit niches in mall atriums, pedestrian bridges, and experiential pop-ups where capex is lower and creative experimentation is welcomed. Programmatic exchanges including VIOOH and Lemma aggregate multivendor supply, giving advertisers unified reach across the United Arab Emirates digital out-of-home market. Regulatory exclusivity clauses limit operator count per emirate, making concession renewals and municipal relationships pivotal to strategic positioning. Consolidation is anticipated as capital requirements escalate and data-driven buying standards rise.

United Arab Emirates DOOH Industry Leaders

JCDecaux Group

Next Level

Eyemedia

ELAN Group

Backlite Media (Multiply Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Lemma Technologies expanded its Lemma Phi AI CMS to enable dynamic creative optimization on UAE networks, using machine learning to recommend day-part mixes.

- January 2026: Dubai Municipality began Phase 2 of the DANA permit platform, adding automated compliance checks that shorten approval cycles for digital billboards.

- February 2025: Multiply Group posted AED 1.04 billion net profit and 56% revenue growth in 2024 on the back of BackLite Media integration.

- December 2025: INFiLED delivered high-brightness LED panels for a flagship roadside unit in Dubai, supporting 4K playback with weather-sealed housing.

- November 2025: LG Electronics Gulf partnered with Expo City Dubai to deploy advanced LED signage across exhibition halls and retail zones

United Arab Emirates DOOH Market Report Scope

DOOH, which stands for digital out-of-home, is an innovative media known as outdoor or out-of-home (OOH) advertising. Unlike online and other device-based digital advertising, where people are already frequenting out of their homes, DOOH advertising is found on LED screens, billboards, and digital signs placed in high-traffic areas.

The United Arab Emirates DOOH Report is Segmented by Service Type (Programmatic-OOH, Non-Programmatic-OOH), Application (Billboard, Transit, Street Furniture, Other Applications), Location Environment (Roadside Outdoor, Airports, Malls and Transit Hubs, In-Store and Indoor Venues, Other Location Environments), End-User Industry (Automotive, Retail, Healthcare, Banking and Financial Services, Media and Entertainment, Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Programmatic-DOOH |

| Non-Programmatic-DOOH |

| Billboard |

| Transit |

| Street Furniture |

| Other Applications |

| Roadside Outdoor |

| Airports |

| Malls and Transit Hubs |

| In-Store and Indoor Venues |

| Other Location Environments |

| Automotive |

| Retail |

| Healthcare |

| Banking and Financial Services |

| Media and Entertainment |

| Other End-User Industries |

| By Service Type | Programmatic-DOOH |

| Non-Programmatic-DOOH | |

| By Application | Billboard |

| Transit | |

| Street Furniture | |

| Other Applications | |

| By Location Environment | Roadside Outdoor |

| Airports | |

| Malls and Transit Hubs | |

| In-Store and Indoor Venues | |

| Other Location Environments | |

| By End-User Industry | Automotive |

| Retail | |

| Healthcare | |

| Banking and Financial Services | |

| Media and Entertainment | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current value of the United Arab Emirates digital out-of-home market?

The United Arab Emirates digital out-of-home market size stood at USD 62.61 million in 2026.

How fast is programmatic buying growing in UAE outdoor advertising?

Programmatic formats are expanding at a 16.03% CAGR between 2026 and 2031, making them the fastest-growing service type.

Which application is forecast to grow quickest within UAE DOOH?

Transit screens are projected to rise at a 15.27% CAGR, driven by metro and bus-shelter digitization.

Why are airports critical for DOOH advertisers in the Emirates?

Dubai and Abu Dhabi airports deliver dwell times exceeding 20 minutes to 100-plus million high-income passengers, providing premium reach and advanced data targeting.

What factor limits rapid creative changes despite programmatic capability?

Municipal content-approval cycles, which may stretch up to three weeks, constrain last-minute campaign adjustments.

Which industry vertical is set to increase its DOOH spending fastest?

Automotive advertisers are expected to grow at a 14.23% CAGR as electric-vehicle launches multiply.

Page last updated on: