Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

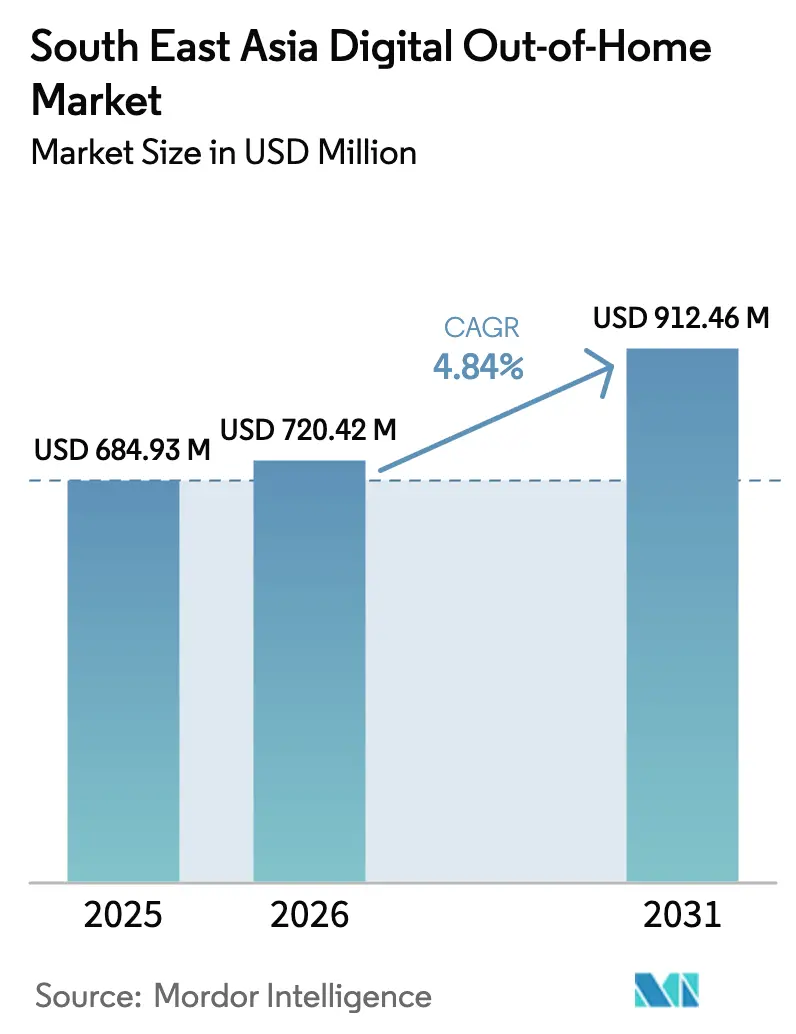

| Base Year Market Size (2025) | USD 684.93 Million |

| Market Size (2026) | USD 720.42 Million |

| Market Size (2031) | USD 912.46 Million |

| Growth Rate (2026 - 2031) | 4.84% CAGR |

| Market Concentration | Medium |

Major Players_Market__company_logog.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South East Asia Digital Out-of-Home Market Analysis by Mordor Intelligence

The Southeast Asia digital out-of-home market size was valued at USD 684.93 million in 2025 and is estimated to grow from USD 720.42 million in 2026 to reach USD 912.46 million by 2031, at a CAGR of 4.84% during the forecast period (2026-2031). Advertisers are shifting away from static billboards toward data-driven formats that allow real-time creative rotation, while airports and transit hubs absorb a larger share of regional budgets. Programmatic pipes shorten activation cycles from weeks to hours, enabling brands to trigger messages when weather changes or foot-traffic surges. Indonesia contributes the largest slice of revenue because Jakarta’s dense corridors host thousands of newly digitized panels, yet Vietnam is on a faster growth curve as elevator and transit screens proliferate in Hanoi and Ho Chi Minh City. Operators that integrate super-app purchase data can now link outdoor exposures to actual transactions, converting what was once a pure awareness channel into a performance engine.

Key Report Takeaways

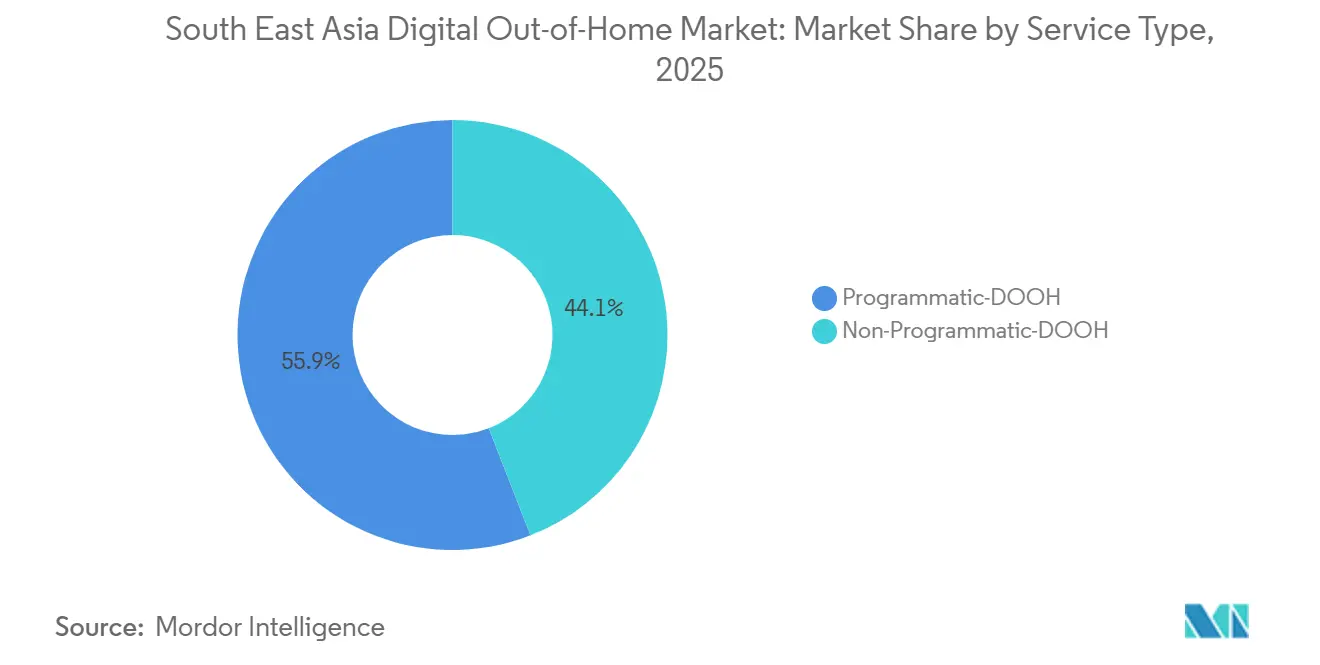

- By service type, non-programmatic formats held 55.91% of 2025 revenue, while programmatic inventory is forecast to post a 5.32% CAGR through 2031.

- By application, billboards accounted for 37.98% of the Southeast Asia digital out-of-home market share in 2025, whereas transit screens are projected to expand at a 5.67% CAGR to 2031.

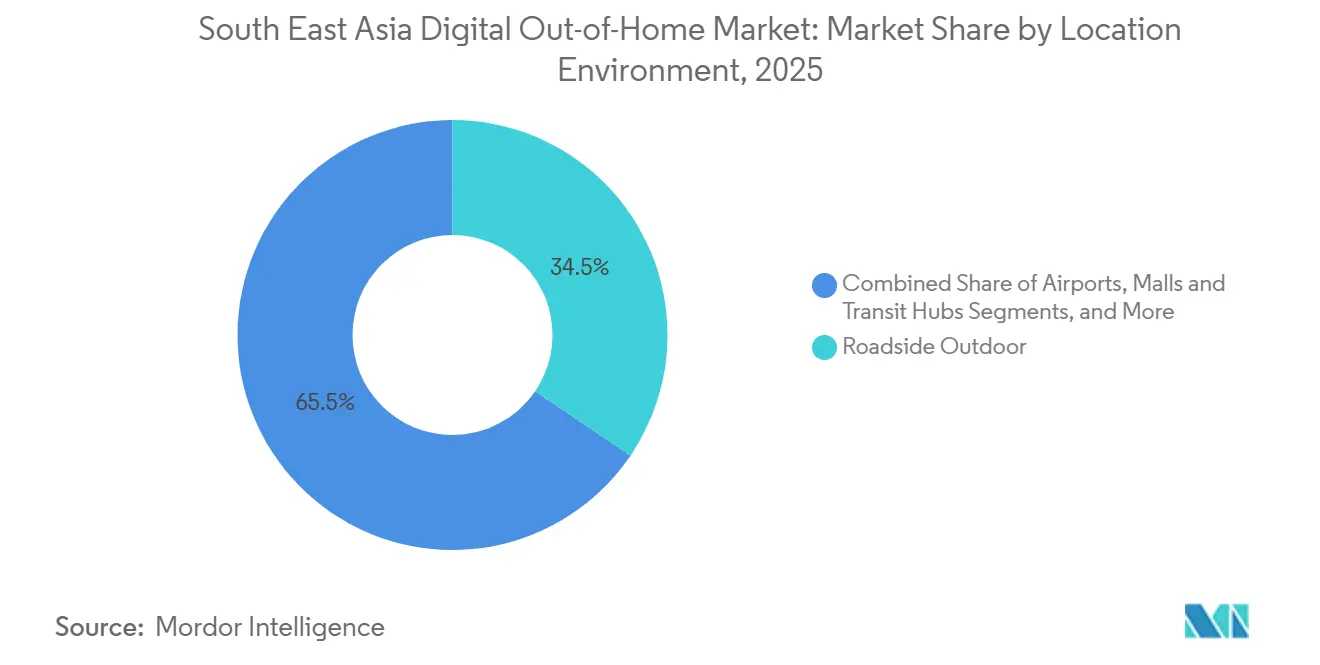

- By location environment, roadside placements captured 34.49% of spend in 2025, yet airport inventory is projected to grow at a 6.41% CAGR over the forecast window.

- By end-user, retail advertisers led with 21.04% of spend in 2025, while healthcare is on track for the fastest 5.23% CAGR through 2031.

- By Region, Indonesia retained 27.17% of regional revenue in 2025, whereas Vietnam is set to record the highest 6.11% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South East Asia Digital Out-of-Home Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Urbanisation and Transit-Hub Footfall Surge | +1.2% | Indonesia, Vietnam, Thailand, Philippines | Medium term (2-4 years) |

| Government Smart-City Investments in Digital Signage | +0.9% | Singapore, Malaysia, Thailand | Long term (≥ 4 years) |

| Explosion of Programmatic DOOH Buying Platforms | +1.0% | Singapore, Indonesia, Thailand | Short term (≤ 2 years) |

| Omnichannel Retail and Consumer-Brand Ad-Spend Uptick | +0.8% | High e-commerce markets across region | Medium term (2-4 years) |

| 3D Anamorphic Billboards Driving Premium Inventory | +0.5% | Singapore, Malaysia, Thailand | Short term (≤ 2 years) |

| Super-App Retail-Media Integration with DOOH | +0.6% | Entire region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization And Transit-Hub Footfall Surge

City populations are growing faster than infrastructure, funneling commuters into rail stations and bus interchanges that deliver long dwell times and clear sight lines for screens. In Jakarta, more than 30 million daily digital impressions originate from corridors such as Sudirman and Gatot Subroto, where inventory has been expanding above 60% annually. Vietnam’s economic boom raises both personal mobility and elevator-screen deployments, with one network reaching roughly 40 million users every day.[1]Chicilon Media, “Vietnam Elevator Screen Network Overview,” chicilon.com Bangkok’s upcoming Pink and Purple lines will add fresh captive audiences to VGI’s existing 4.5 billion annual transactions. Singapore’s Stellar Ace links platform walls, in-train screens, and exit gates across 95 stations to enable sequential storytelling. Because regional GDP momentum is set to hold above 6% in Vietnam and more than 5% in Indonesia through 2026, transit investments will keep widening the pool of addressable impressions.

Government Smart-City Investments In Digital Signage

Smart-city blueprints push digital signage into streetscapes by earmarking it for passenger-information kiosks and public Wi-Fi nodes that rely on ad support to cover costs. Singapore awarded a SGD 150 million (USD 118 million) contract for dynamic bus screens that rotate messages based on route data.[2]The Asian Banker, “Land Transport Authority Awards Dynamic Bus Contract,” theasianbanker.com Kuala Lumpur and provincial Thai capitals gain similar backing through national digital-economy funds. Standardized brightness caps, resolution rules, and content-management protocols lower creative production costs across cities, encouraging multi-market buys. Jakarta’s stricter rules on traditional banners, adopted in 2015, effectively nudged operators toward digital formats that meet compliance thresholds. Because concession tenures span 10-15 years, the resulting inventory pipeline gives the Southeast Asia digital out-of-home market a stable growth floor.

Explosion Of Programmatic DOOH Buying Platforms

Demand-side platforms such as Vistar Media, Hivestack, and VIOOH compress campaign lead times and let brands swap artwork when weather, traffic, or purchase-intent signals change. Vistar logged a 182% sales jump in Southeast Asia during 2023 as advertisers embraced cost-per-thousand bidding tied to third-party verification.[3]Vistar Media, “Southeast Asia Market Growth Report,” vistarmedia.com A Plan B-Vistar tie-up plugged more than 500 screens in 7-Eleven stores into programmatic pipes that trigger offers at foot-traffic spikes. Although the latest State of Nation study shows half of all campaigns already contain a programmatic element, two-thirds still run on guaranteed deals, underscoring buyer appetite for inventory certainty during the transition phase. Middleware like Moving Walls’ LMX platform normalizes audience data across disparate owners, helping close measurement gaps that once deterred large advertisers. Global giant JCDecaux reported 45.6% programmatic revenue growth in 2024, confirming that automated trading is shifting from test budgets to mainstream allocations.

Omnichannel Retail And Consumer-Brand Ad-Spend Uptick

Retailers now combine outdoor priming with mobile retargeting and in-store promotions because evidence shows connected campaigns drive higher return on ad spend. A Trade Desk survey found omnichannel plans are 1.5 times more persuasive and 2.2 times less fatiguing than single-channel efforts, while adding a fifth channel produced a 30% cost-per-acquisition drop. Tiger Beer’s Singapore push blended programmatic DOOH, display ads, and grocery data to lift sales 1.32 times and achieve a 1,873% return. Brands can already purchase super-app Grab ad units that join ride-hail, food delivery, and retail media signals, while Jaya Grocer now links GrabAds exposures to scanned in-store purchases. Because e-commerce penetration sits between 59% and 68% in key markets, retail-media integration positions the Southeast Asia digital out-of-home market to absorb budgets that used to belong solely to search and social.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex and Ongoing Maintenance Costs | -0.7% | Indonesia, Vietnam, Philippines | Short term (≤ 2 years) |

| Fragmented Supply Limiting Unified Measurement | -0.5% | Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines | Medium term (2-4 years) |

| Country-Specific Brightness and Content Limits | -0.3% | Singapore, Malaysia, Thailand | Long term (≥ 4 years) |

| Shortage of Skilled LED or IoT Technicians | -0.3% | Indonesia, Vietnam, Philippines, Thailand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex And Ongoing Maintenance Costs

Fine-pitch indoor LEDs cost as much as USD 2,500 per square meter, while outdoor panels run USD 800-1,200 and still require another 20%-40% for installation. Supply-chain snags stretch driver-IC lead times past 20 weeks, forcing operators to lock working capital months before revenue flows. Kuala Lumpur International Airport’s recent 14 ft × 81 ft screen needed structural reinforcement and custom CMS integration, showing why premium sites remain the domain of deep-pocket incumbents. Humid tropical climates accelerate module degradation, adding quarterly service costs that can consume up to 15% of annual revenue. Singapore pads budgets further through mandatory professional-engineer certification for any structure above 4 m in height. Until financing costs fall or hardware prices decline, capital intensity will slow network rollouts in emerging cities.

Fragmented Supply Limiting Unified Measurement

Advertisers still juggle incompatible reach metrics, raising planning costs for cross-country flights. Only half of campaigns use any form of programmatic buying, and those that do mostly rely on guaranteed deals because real-time bidding lacks common impression standards.[4]VIOOH, “State of Nation 2024,” viooh.com Operators sometimes pay for manual head-count studies to secure buyer trust, as Plan B did in February 2024, underscoring the absence of turnkey data feeds. JCDecaux’s AI-driven metro analytics remain confined to Hong Kong, leaving Southeast Asian networks dependent on survey panels or mobile-location extrapolations that lack granularity. The open-source OMIG framework promises relief, yet adoption is voluntary and still competes with proprietary stacks from Hivestack and Vistar. Privacy statutes across the region further restrict device identifiers, hampering closed-loop attribution without explicit consent.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Programmatic Momentum Outpaces Direct Sales

Non-programmatic formats still delivered 55.91% of revenue in 2025, but automated pipes are forecast to grow faster as agencies migrate display and video workflows into outdoor. Vistar’s 182% jump in Southeast Asian billings and the steady rise of programmatic-guaranteed deals underline early demand for inventory certainty. Yet long-term contracts remain attractive for auto or tourism launches that require unbroken share-of-voice along marquee roadways. The Southeast Asia digital out-of-home market size for programmatic inventory is set for a 5.32% CAGR, drawing on first-party retail data links that fuel outcome-based buying.

Direct deals will keep a presence because premium airport façades and landmark billboards often bundle site exclusivity, content audits, and creative-approval windows that are hard to replicate inside open exchanges. Integration costs, APIs, CMS upgrades, data layers, still deter smaller owners, slowing the shift in secondary cities. As supply-side fragmentation recedes and verification widens, the Southeast Asia digital out-of-home market will likely mirror display advertising’s earlier swing from reservations to auctions.

By Application: Transit Screens Ride Commuter Wave

Billboards captured 37.98% of 2025 spend, yet many prime corridors are already saturated, and new permits face visual-pollution caps. Transit concessions offer untapped dwell time at gates, concourses, and train cars, which explains the application’s projected 5.67% CAGR through 2031. Operators such as VGI lock in multi-year rights that carve defensive moats around Bangkok’s BTS and Malaysia’s commuter rail.

The Southeast Asia digital out-of-home market share lead held by billboards will erode gradually as rail, bus, and convenience-store screens compound in volume and add programmatic triggers tied to passenger peaks. Street furniture and in-store kiosks provide hyperlocal reach for neighborhood retailers, although their fragmented ownership lengthens the path to unified measurement. Creative formats such as forced-perspective 3D enrich both billboards and transit walls, but commuter environments deliver predictable foot-traffic that brand planners prize for frequency control.

By Location Environment: Airports Lift Premium Yields

Roadside panels still amassed 34.49% of 2025 revenue because motorists traverse ring roads and arterials daily. Yet airport networks post the strongest 6.41% CAGR forecast as cross-border travel rebounds. Changi Airport alone handled 67.7 million passengers last year, giving JCDecaux screens cost-per-thousand rates that top USD 45 in high-traffic zones. Kuala Lumpur International and Bangkok Suvarnabhumi offer similar premium tiers, and advertisers willingly pay because traveler demographics skew toward affluent decision-makers.

The Southeast Asia digital out-of-home market size held by airport media is small today but expands faster than other environments thanks to duty-free, luxury retail, and tourism boards that crave reach in a single high-value venue. Malls and transit hubs add blended foot-traffic indoors, securing mid-tier rates while weather-proofing screens. Secondary environments such as campuses or stadiums remain tactical, yet operators eye them for incremental inventory once measurement harmonizes.

By End-User Industry: Healthcare Advertising Accelerates

Retail still commands 21.04% of spend, driven by store traffic campaigns and seasonal promotions. However, healthcare and wellness brands are allocating larger budgets at a 5.23% CAGR, aiming at commuters during morning peaks when message recall is high. Pharmaceutical players appreciate DOOH’s strict brand-safety context compared with social feeds, while fitness apps sponsor multi-screen bursts that coincide with health-check reminders.

Automotive, banking, and entertainment continue to underwrite marquee billboards and 3D anamorphic showcases but face plateauing growth. The Southeast Asia digital out-of-home market share held by healthcare will climb as ageing populations and preventive-care messaging gain urgency. Advertisers from telecom, consumer packaged goods, and education remain consistent but use data-driven buying to stretch budgets instead of boosting absolute spend.

Geography Analysis

Indonesia contributes 27.17% of regional revenue thanks to Jakarta’s 30 million daily impressions and swift static-to-digital conversions guided by supportive regulations. City Vision and Broadsign digitized more than 2,000 city-center panels, while super-apps Grab and Gojek enrich targeting with ride-hail data. E-commerce growth and rising smartphone adoption feed advertiser appetite, ensuring the Southeast Asia digital out-of-home market maintains Indonesia as its largest base.

Vietnam registers the highest 6.11% CAGR outlook, buoyed by 8% GDP expansion and elevator networks that now dominate commercial towers. Chicilon Media’s near-total share of high-rise lifts amplifies reach in Hanoi and Ho Chi Minh City, while government infrastructure drives more transit concessions. Strong electronics exports and fast-growing e-commerce volumes sustain media budgets, positioning Vietnam as the breakout market in the region.

Thailand, Singapore, and Malaysia round out the core. Thailand rebounded with 13% value growth last year, and VGI’s BTS exclusivity offers an unrivaled commuter footprint. Singapore’s mature regulations invite high CPM but also impose strict content codes that favor experienced operators. Malaysia’s 50 million-passenger airport volumes plus Big Tree Outdoor’s 7,500-panel network keep it a mid-scale yet strategically important market. The Philippines and the remainder of Southeast Asia stay smaller today but attract investment as mobile use and retail media networks widen.

Competitive Landscape

Global incumbents JCDecaux and Clear Channel defend airport and luxury roadside sites, yet regional champions such as VGI, Plan B Media, and Big Tree Outdoor leverage exclusive concessions to cement local moats. JCDecaux logged 6.1% year-over-year DOOH revenue growth in Q3 2025, and its VIOOH exchange now funnels automated demand into Singapore and Malaysia screens. Clear Channel integrates Broadsign to modernize its Singapore footprint and teamed with Scoot Airlines for branded transit flows.

Regional specialists scale through technology and data. Moving Walls’ AI-enabled LMX platform pairs post-campaign attribution with supply aggregation, winning group-agency alignments. Hivestack partners with oOh!media to expose AUD 635.6 million (USD 422 million) in Australasian inventory to Southeast Asian buyers, blending cross-border reach with local relevance. Big Tree Outdoor and Vistar opened more than 7,500 panels to cost-per-thousand bidding, underscoring how programmatic alliances redraw competitive lines.

Disruptors exploit retail-media data. GroupM and GrabAds combine transaction signals with ride-hail and delivery impressions, while Gojek’s GoScreen offers hyperlocal targeting that met 130% of impression goals during pandemic periods. Hardware vendors Daktronics and Shenzhen-based suppliers embed forced-perspective 3D features into façades, differentiating owners who can finance marquee upgrades. As the OMIG framework diffuses, measurement parity should shift rivalry toward creative quality, data access, and speed of activation rather than purely on screen count.

South East Asia Digital Out-of-Home Industry Leaders

JCDecaux Singapore Pte Ltd

Clear Channel Singapore Pte Ltd

Ooh!Media Digital PTY Limited

Hivestack Inc.

Moove Media Pte Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Moove Media began rolling out dynamic bus screens under its seven-year Land Transport Authority contract, bringing live route data and audience-triggered creative to Singapore’s entire public-bus fleet.

- October 2025: Maybank Singapore launched a 100% bus-wrap campaign across 65 vehicles, the first fully wrapped fleet approved in a decade, marking regulatory softening toward large-format mobile ads.

- January 2025: T-Mobile agreed to acquire Vistar Media for about USD 600 million in cash to fuse 1.1 million connected screens with telecom customer data for improved addressable advertising precision.

South East Asia Digital Out-of-Home Market Report Scope

Advertising that is shown dynamically and digitally in indoor and outdoor public spaces is known as digital out-of-home (DOOH) advertising. In other words, it involves combining traditional out-of-home advertising with digital components. The trend toward digital OOH now dominates traditional offline out-of-home advertising.

The Southeast Asia Digital Out-of-Home Market Report is Segmented by Service Type (Programmatic-DOOH, Non-Programmatic-DOOH), Application (Billboard, Transit, Street Furniture, Other Applications), Location Environment (Roadside Outdoor, Airports, Malls and Transit Hubs, In-Store and Indoor Venues, Other Location Environments), End-User Industry (Automotive, Retail, Healthcare, Banking and Financial Services, Media and Entertainment, Other End-User Industries), and Geography (Singapore, Malaysia, Thailand, Indonesia, Philippines, Vietnam, Rest of South-East Asia). The Market Forecasts are Provided in Terms of Value (USD).

By Service Type

| Programmatic-DOOH |

| Non-Programmatic-DOOH |

By Application

| Billboard |

| Transit |

| Street Furniture |

| Other Applications |

By Location Environment

| Roadside Outdoor |

| Airports |

| Malls and Transit Hubs |

| In-Store and Indoor Venues |

| Other Location Environments |

By End-User Industry

| Automotive |

| Retail |

| Healthcare |

| Banking and Financial Services (BFSI) |

| Media and Entertainment |

| Other End-User Industries |

By Geography

| Singapore |

| Malaysia |

| Thailand |

| Indonesia |

| Philippines |

| Vietnam |

| Rest of South-East Asia |

| By Service Type | Programmatic-DOOH |

| Non-Programmatic-DOOH | |

| By Application | Billboard |

| Transit | |

| Street Furniture | |

| Other Applications | |

| By Location Environment | Roadside Outdoor |

| Airports | |

| Malls and Transit Hubs | |

| In-Store and Indoor Venues | |

| Other Location Environments | |

| By End-User Industry | Automotive |

| Retail | |

| Healthcare | |

| Banking and Financial Services (BFSI) | |

| Media and Entertainment | |

| Other End-User Industries | |

| By Geography | Singapore |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Philippines | |

| Vietnam | |

| Rest of South-East Asia |

Key Questions Answered in the Report

What is the projected value of the Southeast Asia digital out-of-home market in 2031?

The market is forecast to reach USD 912.46 million by 2031.

Which country contributes the largest revenue today?

Indonesia leads with 27.17% of 2025 regional spending thanks to Jakarta's dense screen network.

Which environment will grow fastest over the next five years?

Airport screens are expected to post the highest 6.41% CAGR as passenger volumes recover and advertisers seek affluent traveler audiences.

How quickly is programmatic inventory expanding?

Programmatic formats are projected to grow at a 5.32% CAGR through 2031 as automated pipes and data integrations mature.

Why are healthcare brands increasing spend on outdoor screens?

Wellness and pharmaceutical advertisers value high commuter reach and strict brand-safety controls, lifting healthcares forecast CAGR to 5.23% through 2031.

What are the main obstacles to faster market expansion?

High upfront hardware costs and fragmented measurement standards slow new deployments and deter multi-country campaign buys.

Page last updated on: