Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.62 Billion |

| Market Size (2026) | USD 1.72 Billion |

| Market Size (2031) | USD 2.31 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turkey Ceramic Tiles Market Analysis by Mordor Intelligence

Turkey ceramic tiles market size in 2026 is estimated at USD 1.72 billion, growing from 2025 value of USD 1.62 billion with 2031 projections showing USD 2.31 billion, growing at 6.05% CAGR over 2026-2031. Demand rides on the country’s sweeping urban-renewal program, resilient export position, and the steady shift toward large-format slabs. Housing reconstruction after the February 2023 Kahramanmaraş earthquakes keeps domestic orders high, while competitive energy and raw-material costs spur exports to the USA and EU. Producers are accelerating digital printing, solar-powered kilns, and circular-economy practices to stay profitable under volatile natural-gas pricing. Tightening EU carbon rules and skilled-labor shortages temper momentum but have not derailed long-term growth expectations.

Key Report Takeaways

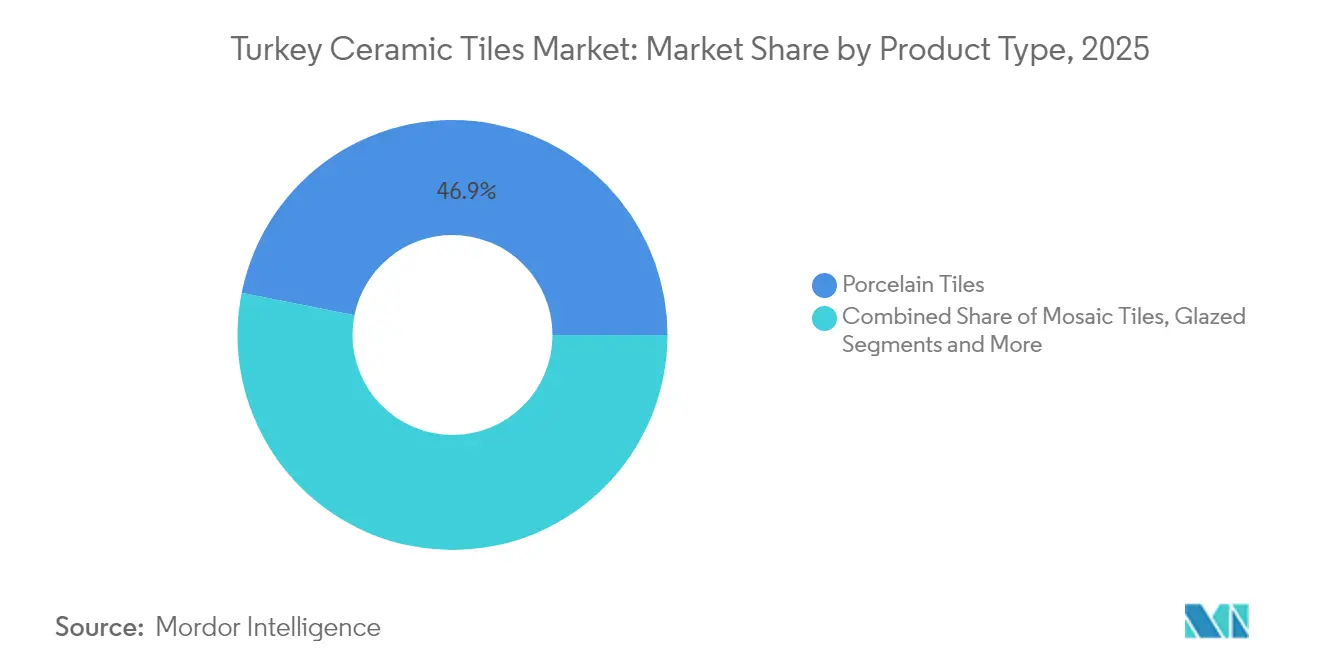

- By product type, porcelain led with 46.85% Turkey ceramic tiles market share in 2025; mosaic is projected to advance at a 6.08% CAGR to 2031.

- By application, floor installations captured 64.85% of the Turkey ceramic tiles market size in 2025; wall tiles are expanding at a 5.68% CAGR through 2031.

- By end-user, the residential segment held 52.75% of the Turkey ceramic tiles market size in 2025, while commercial projects are tracking the fastest CAGR at 6.74% through 2031.

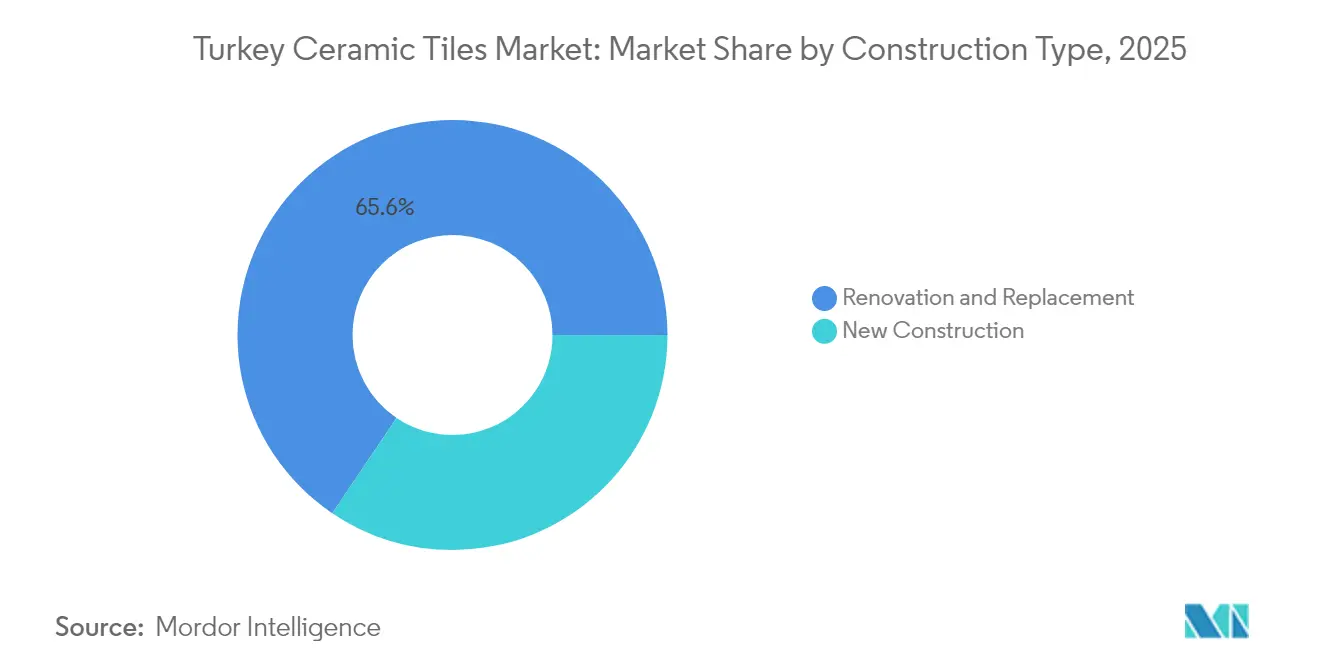

- By construction type, renovation commanded 65.55% of the Turkey ceramic tiles market share in 2025; new construction is set to grow at a 6.58% CAGR to 2031.

- By Distribution Channel, Specialty Tile & Stone Stores commanded 38.75% of the Turkey ceramic tiles market share in 2025; Online Retail is set to grow at a 7.12% CAGR to 2031.

- By geography, the Marmara region controlled 28.05% revenue in 2025; Southeastern & Eastern Anatolia registers the highest 6.66% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Turkey Ceramic Tiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban-renewal surge in seismic zones | +1.8% | Nationwide; strong in Marmara and Central Anatolia | Long term (≥ 4 years) |

| Credit incentives for earthquake-resilient floors | +1.2% | Nationwide; priority in high-risk provinces | Medium term (2-4 years) |

| Rising U.S. and EU demand for Turkish porcelain | +1.5% | North America and EU | Medium term (2-4 years) |

| Rapid take-up of digitally printed slabs | +0.8% | Marmara and Aegean urban centers | Short term (≤ 2 years) |

| Circular-economy use of industrial waste | +0.4% | Main manufacturing hubs | Long term (≥ 4 years) |

| Anti-slip mosaics in rail and metro projects | +0.6% | Major metropolitan corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Urban-renewal surge in seismic zones

Turkey’s USD 400-500 billion urban transformation mandate targets 6.7 million seismically vulnerable buildings, with 1.5 million units slated for renewal within five years[1]Source: Investment Office of Türkiye, “Urban Transformation Projects,” invest.gov.tr. Renovation uses 40-60% more ceramic flooring per square meter than new builds, boosting volumes through 2030. Expanded expropriation powers enable swift project starts, while zero-interest loans remove financing barriers. Continuous bidding cycles stabilize contractor pipelines, turning renovation into a predictable demand engine for the Turkey ceramic tiles market. The Ministry of Environment, Urbanization, and Climate Change's expanded expropriation powers facilitate rapid project initiation, ensuring consistent market demand through 2030. Zero-interest loan availability for severely damaged property owners eliminates traditional financing barriers that historically constrained renovation activity.

Credit incentives for earthquake-resilient floors

Interest-free loans attached to TOKİ’s 250,000-unit social-housing program reward certified seismic-grade ceramic tiles. Green public-procurement rules link flooring choices to renewable energy targets, nudging developers toward durable porcelain formats. Updated retrofitting codes simplify compliance and shorten permitting times, allowing project owners to upgrade finishes instead of opting for cheaper substitutes. The government's green cement mandate in public procurement extends to complementary materials, positioning ceramic tiles as preferred flooring solutions in government-funded projects. Interest-free financing mechanisms reduce project costs by 15-20%, enabling developers to allocate additional budget toward premium ceramic specifications that enhance structural resilience.

Rising U.S. and EU demand for Turkish porcelain

Turkish exports hit 116 million m² in 2024, with the USA alone absorbing 14.1% of shipments. This export momentum benefits from Turkey's strategic cost advantages, as manufacturers achieve production efficiencies through proximity to raw materials including feldspar (5.07 million metric tons produced in 2019) and boron compounds essential for ceramic glazes. Proximity to feldspar and boron deposits lowers input costs, delivering a 20–25% pricing edge over Spanish and Italian peers. Ongoing U.S. antidumping probes against Indian tiles divert purchase orders toward Turkish lines, while EU Customs Union membership keeps paperwork light for European buyers. Turkey's membership in the EU Customs Union facilitates seamless market access, though upcoming CBAM requirements necessitate carbon footprint optimization to maintain price competitiveness.

Rapid take-up of digitally printed slabs

Anatolia’s 250,000 m² facility pairs mold-free presses with 21.5 MW rooftop solar, cutting production time and emissions. Slabs up to 3,200 × 1,600 mm reduce grout lines, slicing installation hours by 40–50% and attracting high-end mixed-use projects in Istanbul and Izmir. Large-format ceramic slabs reduce installation time by 40-50% compared to traditional tiles, creating labor cost savings that offset premium material pricing. Local developers increasingly specify these products for high-end residential and commercial projects, driven by aesthetic preferences for seamless surfaces and reduced maintenance requirements. Kaleseramik's launch of new large porcelain tile production lines in 2023 demonstrates industry-wide commitment to meeting this emerging demand, with annual capacity reaching 56 million square meters across four facilities[2]Source: Kaleseramik Investor Relations, “IPO Prospectus 2023,” Kaleseramik, kaleseramik.com. .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile natural-gas prices | −1.4% | All production clusters | Short term (≤ 2 years) |

| Import competition from Spain & India | −0.9% | EU and North America | Medium term (2-4 years) |

| EU CBAM carbon-footprint compliance | −1.1% | 40% of exports going to EU | Medium term (2-4 years) |

| Skilled-labor shortage in manufacturing hubs | −0.7% | Central and Western Anatolia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Natural-Gas Prices Squeezing Kiln Margins

Natural gas price volatility significantly impacts Turkish ceramic manufacturers, as kiln operations consume 60-70% of total production energy requirements, with firing temperatures reaching 1200°C for porcelain tiles. Kilns consume 60-70% of energy costs, exposing producers when Turkish spot gas prices spike above European hubs. Cogeneration cuts dryer gas by 0.1115 m³/s yet demands upfront funding, delaying upgrades among mid-sized firms. Capacity utilization reached 74.3% in April 2025, so producers run full tilt despite thin margins. The challenge intensifies as Turkey's manufacturing sector capacity utilization reached 74.3% in April 2025, indicating strong demand that manufacturers struggle to meet cost-effectively under current energy pricing structures.

Tightening EU CBAM Carbon-Footprint Compliance for Exporters

The EU’s Carbon Border Adjustment Mechanism may levy EUR 777 million annually on Turkish exports starting in 2026. Transitional reporting through 2025 forces factories to audit kiln emissions; lacking verifiable data now triggers default values that inflate fees[3] Source: European Commission, “CBAM Transitional Rules,” ec.europa.eu. Ankara plans a national ETS in 2026 to soften shocks, but alignment with EU carbon prices remains uncertain. The mechanism's expansion to cover all goods under the EU ETS by 2030 threatens long-term export competitiveness unless Turkish manufacturers invest in carbon reduction technologies. Turkey's planned launch of its own emissions trading system in 2026 aims to mitigate these impacts, though the effectiveness depends on carbon price alignment with EU standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Porcelain Dominance Drives Innovation

Porcelain tiles held 46.85% of Turkey ceramic tile market share in 2025, reflecting high durability and style variety. Mosaic tiles post the swiftest 6.08% CAGR to 2031 as transport hubs specify anti-slip textures. Glazed and unglazed formats keep steady roles in homes and factories, while decorative “other” tiles gain from boutique architecture. Research into kiln-waste glazes underpins a circular push that trims costs and emissions. Digital printers now replicate marble and travertine veins, giving porcelain an edge over natural stone for budget-minded projects. Glazed ceramic tiles maintain steady demand in residential renovations, while unglazed ceramic tiles serve industrial and high-traffic commercial spaces. The "Others" category, encompassing decorative, patterned, and handmade tiles, benefits from architectural trends favoring customization and cultural authenticity.

Porcelain’s reach spans premium hotels to price-sensitive housing, enabling economies of scale that support aggressive export pricing. Mosaic growth aligns with metro expansion, each station installing roughly 2,500 m² of R11-rated flooring. Decorative lines leverage Anatolia’s “Aeterna” sintered stone slab, lifting perceived value in luxury villas. Glazed tiles retain popularity among DIY renovators who value broad color palettes. The category’s diversity cushions manufacturers from demand shocks in any single application, sustaining the Turkey ceramic tiles market.

By Application: Floor Segment Leads Infrastructure Demand

Floor applications dominate with 64.85% market share in 2025, supported by Turkey's construction sector growth of 9.3% and extensive infrastructure development programs. Wall applications demonstrate stronger growth potential at 5.68% CAGR through 2031, driven by architectural trends emphasizing vertical surface treatments and the integration of ceramic panels in facade systems. Roofing applications, while smaller in volume, benefit from traditional Turkish architectural restoration projects and earthquake-resilient construction requirements that favor ceramic materials' weather resistance and seismic performance.

High-speed rail stations and airports prefer durable porcelain floors that tolerate 15,000 footfalls per hour without visible wear. Wall panels now serve as ventilated façades, boosting thermal performance and adding tile square footage per project. Heritage roofing recovers Ottoman terracotta aesthetics while complying with seismic codes. Collectively, these shifts diversify demand and strengthen the Turkey ceramic tiles market against cyclical swings. Government mandates for green building materials in public procurement create a preference for ceramic applications that meet environmental performance criteria while delivering long-term durability.

By End-User: Commercial Sector Accelerates Growth

The residential segment maintains 52.75% market share in 2025, anchored by Turkey's urban transformation program targeting 1.5 million house renewals and TOKİ's 250,000 social housing initiative. Commercial applications emerge as the fastest-growing segment with 6.74% CAGR through 2031, driven by hospitality sector recovery, retail space expansion, and infrastructure development including airports, metro stations, and healthcare facilities. Transport hubs particularly favor ceramic solutions for their slip-resistance properties and ability to withstand high-traffic conditions while maintaining aesthetic appeal.

Tourism recovery adds upscale hotel refurbishments, often pairing large-format lobby slabs with mosaic wet-area flooring. Retail chains expand in secondary cities, embracing scratch-resistant porcelain to cut maintenance. Educational facilities benefit from ceramic tiles' durability and low maintenance requirements, aligning with government budget constraints while ensuring long-term performance. The hospitality subsegment, including hotels and resorts, drives demand for premium decorative tiles that enhance guest experiences while meeting operational durability requirements in high-use environments.

By Construction Type: Renovation Drives Market Momentum

Renovation and replacement activities account for 65.55% market share in 2025, reflecting Turkey's aging building stock and government-mandated seismic upgrades affecting 6.7 million structures nationwide. New construction demonstrates higher growth potential at 6.58% CAGR through 2031, supported by urban development projects and infrastructure expansion programs. The renovation segment benefits from regulatory changes that simplify retrofitting procedures while requiring compliance with modern safety standards, creating systematic demand for ceramic flooring systems that meet updated building codes

Zero-interest loans for damaged homeowners unlock premium finishes, nudging demand toward porcelain and large-format slabs. Contractors prefer factory-cut rectified edges that speed installation, vital when entire neighborhoods undergo simultaneous work. New builds leverage lightweight sintered stone façades to meet green-building ratings. The dual-track of rebuilding and expansion guarantees multi-year visibility for tile orders. The construction sector's capacity utilization at 74.3% indicates strong demand that renovation projects help sustain through consistent material requirements.

By Distribution Channel: Digital Transformation Reshapes Access

Specialty tile & stone stores maintain a 38.75% market share in 2025, leveraging expertise and product display capabilities that facilitate complex specification decisions. Online retail emerges as the fastest-growing channel with a 7.12% CAGR through 2031, reflecting digital transformation trends accelerated by pandemic-related shopping behavior changes and younger demographics' preference for e-commerce platforms. Home improvement & DIY stores serve the residential renovation market, while direct sales to contractors streamline commercial project procurement processes.

The digital shift enables manufacturers to showcase large-format tiles and complex patterns through virtual reality applications, overcoming traditional display limitations in physical showrooms. Kaleseramik’s public offering funds an omnichannel strategy with direct-to-consumer portals that bypass intermediaries. Virtual showrooms display full-size slab renders, solving physical space limits in urban boutiques. Contractors gain from project dashboards that sync inventory with site schedules, minimizing costly delays. Hybrid “click-and-collect” models blend e-commerce selection with local pickup and certified installation crews, catering to speed-driven urban customers.

Geography Analysis

The Marmara region commands 28.05% market share in 2025, driven by Istanbul's massive urban transformation requirements and proximity to major manufacturing facilities including Kaleseramik's operations. This region benefits from the highest concentration of renovation projects, with government estimates indicating 14,000 buildings in Istanbul requiring demolition and reconstruction due to seismic vulnerabilities. The region's economic activity, representing approximately 40% of Turkey's GDP, sustains premium ceramic tile demand in both residential and commercial applications. Manufacturing proximity reduces transportation costs and enables rapid project fulfillment, while the presence of major ports facilitates export operations to European markets.

Central Anatolia leverages its position as a traditional ceramic production hub, with Kütahya's historical ceramic heritage supporting modern manufacturing capabilities and skilled workforce availability. The region benefits from abundant raw material access, including feldspar and clay deposits essential for ceramic production, reducing input costs for local manufacturers. Aegean and Mediterranean regions demonstrate steady growth supported by tourism infrastructure development and coastal residential projects that favor ceramic tiles for their weather resistance and aesthetic appeal. These regions particularly benefit from export logistics advantages through Mediterranean ports, facilitating shipments to European and North African markets.

Southeastern Anatolia & Eastern Anatolia emerge as the fastest-growing geography with 6.66% CAGR through 2031, driven by post-earthquake reconstruction efforts and government infrastructure investments in previously underserved areas. The region's reconstruction program, supported by international development funding and government zero-interest loans, creates systematic ceramic tile demand as communities rebuild with modern safety standards. Transportation infrastructure improvements, including high-speed rail extensions, enhance market access while creating direct demand for anti-slip ceramic applications in stations and terminals. The region's lower labor costs attract manufacturing investment, though skilled workforce development remains a constraint requiring ongoing government and industry collaboration.

Competitive Landscape

The Turkish ceramic tiles market exhibits moderate fragmentation, with established domestic players maintaining strong positions through vertical integration and export capabilities. Kaleseramik leads with 56 million square meters of annual capacity across four facilities, achieving public listing in July 2023 and ranking 168th among Turkey's top 500 industrial companies. Competition intensifies through technology adoption, with Anatolia's USD 100+ million investment in a 250,000 square meter facility featuring digital printing capabilities and solar power generation, demonstrating the capital requirements for maintaining competitiveness. Strategic differentiation occurs through sustainability initiatives, export market development, and product innovation in large-format slabs and digitally-printed designs.

White-space opportunities emerge in circular economy applications, with research demonstrating successful incorporation of industrial waste, including borax waste and kiln roller materials, in ceramic production, potentially reducing costs by 25-35% while meeting environmental objectives. Digital transformation creates competitive advantages through AI-assisted design capabilities and predictive maintenance systems that optimize kiln operations and reduce energy consumption. Export market positioning benefits from Turkey's strategic location and EU Customs Union membership, though CBAM compliance requirements necessitate carbon footprint optimization investments that favor larger manufacturers with greater capital resources.

Turkey Ceramic Tiles Industry Leaders

Kaleseramik

Eczacıbaşı

Bien Seramik

NG Kütahya Seramik

Yurtbay Seramik

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Efesus Stone unveiled bespoke Turkish marble lines targeting architectural studios at Coverings 2025.

- February 2025: Anatolia debuted the Aeterna slab collection produced at its new 2.2 million-ft² Turkish facility, showcasing ultra-high-resolution imaging.

- April 2024: I4F partnered with Akgün Group-Duratiles to commercialize click-lock floating floor technology for ceramic tiles, naming Akgün the first global licensee.

Turkey Ceramic Tiles Market Report Scope

Ceramic tiles are made with clays mixed with other materials, e.g., sand, quartz, and water. This report aims to provide a detailed analysis of the Turkish ceramic tiles market. It focuses on the market dynamics, the emerging trends in the industry segments and regional markets, and insights into the various product and application types. It also analyzes the key players and the competitive landscape of the Turkish ceramic tiles market.

The Turkish ceramic tiles market is segmented by product (glazed, porcelain, scratch-free, and other products), application (floor tiles, wall tiles, and other applications), construction type (new construction, replacement, and renovation), and end user (residential and commercial). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Product Type

| Porcelain Tiles |

| Glazed Ceramic Tiles |

| Unglazed Ceramic Tiles |

| Mosaic Tiles |

| Others (Decorative, Patterned, Handmade) |

By Application

| Floor |

| Wall |

| Roofing |

By End-User

| Residential | |

| Commercial | Hospitality (Hotels, Resorts) |

| Retail Spaces | |

| Offices & Institutions | |

| Healthcare | |

| Educational Facilities | |

| Transport Hubs (Airports, Metro, Bus Terminals) | |

| Other Commercial Users |

By Construction Type

| New Construction |

| Renovation and Replacement |

By Distribution Channel

| Specialty Tile & Stone Stores |

| Home Improvement & DIY Stores |

| Online Retail |

| Direct Sales to Contractors |

By Geography

| Marmara Region |

| Central Anatolia |

| Aegean Region |

| Mediterranean Region |

| Southeastern Anatolia & Eastern Anatolia |

| By Product Type | Porcelain Tiles | |

| Glazed Ceramic Tiles | ||

| Unglazed Ceramic Tiles | ||

| Mosaic Tiles | ||

| Others (Decorative, Patterned, Handmade) | ||

| By Application | Floor | |

| Wall | ||

| Roofing | ||

| By End-User | Residential | |

| Commercial | Hospitality (Hotels, Resorts) | |

| Retail Spaces | ||

| Offices & Institutions | ||

| Healthcare | ||

| Educational Facilities | ||

| Transport Hubs (Airports, Metro, Bus Terminals) | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Renovation and Replacement | ||

| By Distribution Channel | Specialty Tile & Stone Stores | |

| Home Improvement & DIY Stores | ||

| Online Retail | ||

| Direct Sales to Contractors | ||

| By Geography | Marmara Region | |

| Central Anatolia | ||

| Aegean Region | ||

| Mediterranean Region | ||

| Southeastern Anatolia & Eastern Anatolia | ||

Key Questions Answered in the Report

What is the current value of the Turkey ceramic tiles market?

The market stands at USD 1.72 billion in 2026 and is forecast to reach USD 2.31 billion by 2031.

Which product category holds the highest share in Turkish ceramic tiles?

Porcelain tiles lead with 46.85% market share in 2025.

How will EU CBAM rules affect Turkish ceramic tile exporters?

CBAM could impose EUR 777 million in annual carbon fees starting 2026 unless factories cut embedded emissions.

Which Turkish region is growing fastest for ceramic tiles demand?

Southeastern & Eastern Anatolia shows the strongest 6.66% CAGR through 2031 due to post-earthquake reconstruction.

What distribution channels are gaining popularity for tile sales?

Online retail is the fastest-growing channel, logging a 7.12% CAGR as consumers embrace virtual showrooms.

Page last updated on: