Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 13.58 Billion |

| Market Size (2026) | USD 14.29 Billion |

| Market Size (2031) | USD 18.94 Billion |

| Growth Rate (2026 - 2031) | 5.80% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Waste Management Market Analysis by Mordor Intelligence

The India Waste Management Market size was valued at USD 13.58 billion in 2025 and is estimated to grow from USD 14.29 billion in 2026 to reach USD 18.94 billion by 2031, at a CAGR of 5.80% during the forecast period (2026-2031).

Strong regulatory pressure, sizable fiscal transfers to municipalities, and widening producer-responsibility mandates underpin this growth trajectory. Capital-expenditure grants released under the 15th Finance Commission are helping city governments mechanize collection fleets, while the Plastic Waste Management Amendment Rules 2024 and the National Circular Economy Framework 2025 oblige brand owners to hit hard recycling quotas[1]"15th Finance Commission Grants Boost Urban Infrastructure." Economic Times, accessed January 2, 2026. https://economictimes.indiatimes.com.. Private operators are responding by shifting toward technology-enabled resource-recovery models that command higher gate fees and offtake prices. However, low source-segregation rates, litigation against waste-to-energy (WtE) plants, and volatile carbon-credit prices continue to squeeze margins and delay large-scale projects. The ability to lock in long-term municipal contracts, deploy automation at scale, and monetize secondary materials through extended-producer-responsibility (EPR) credits will ultimately decide winners across the India waste management market.

Key Report Takeaways

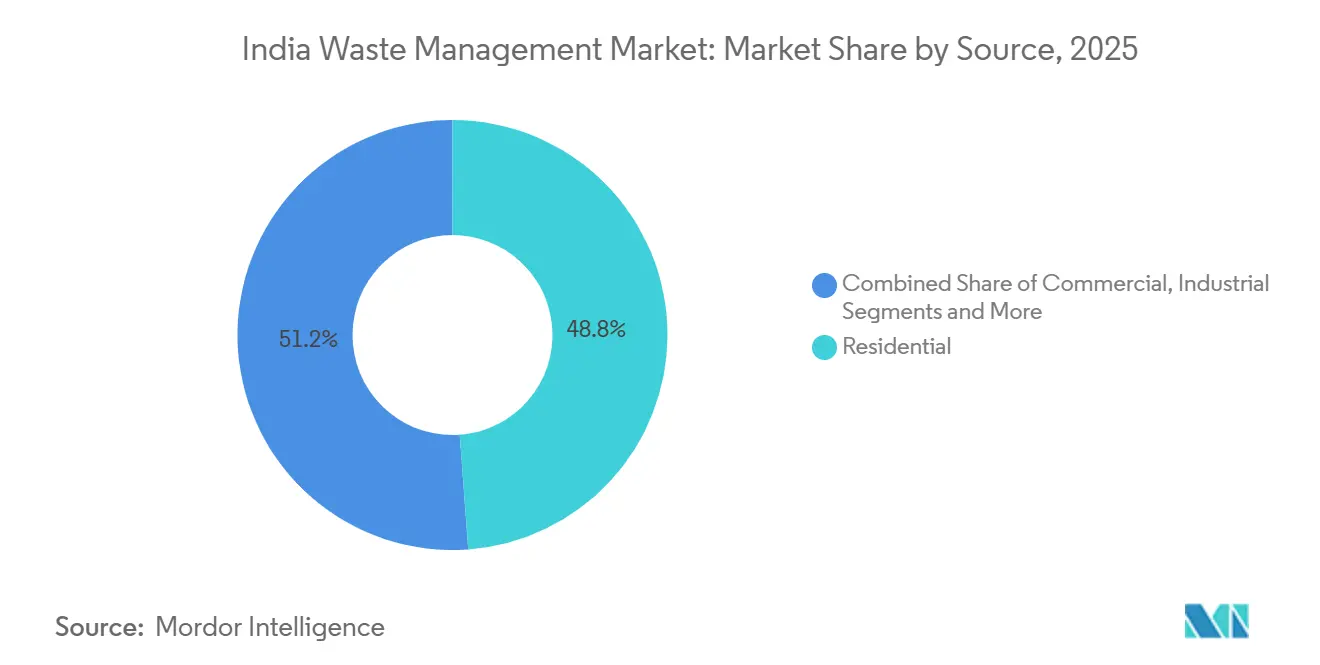

- By sources, the waste management market in India was led by residential waste, which accounted for 48.83% of 2025 revenue, while the commercial segment is projected to expand at an 8.6% CAGR through 2031.

- By service type, collection, transportation, sorting, and segregation held a 38.76% share in 2025; recycling and resource recovery are expected to rise at an 8.5% CAGR to 2031.

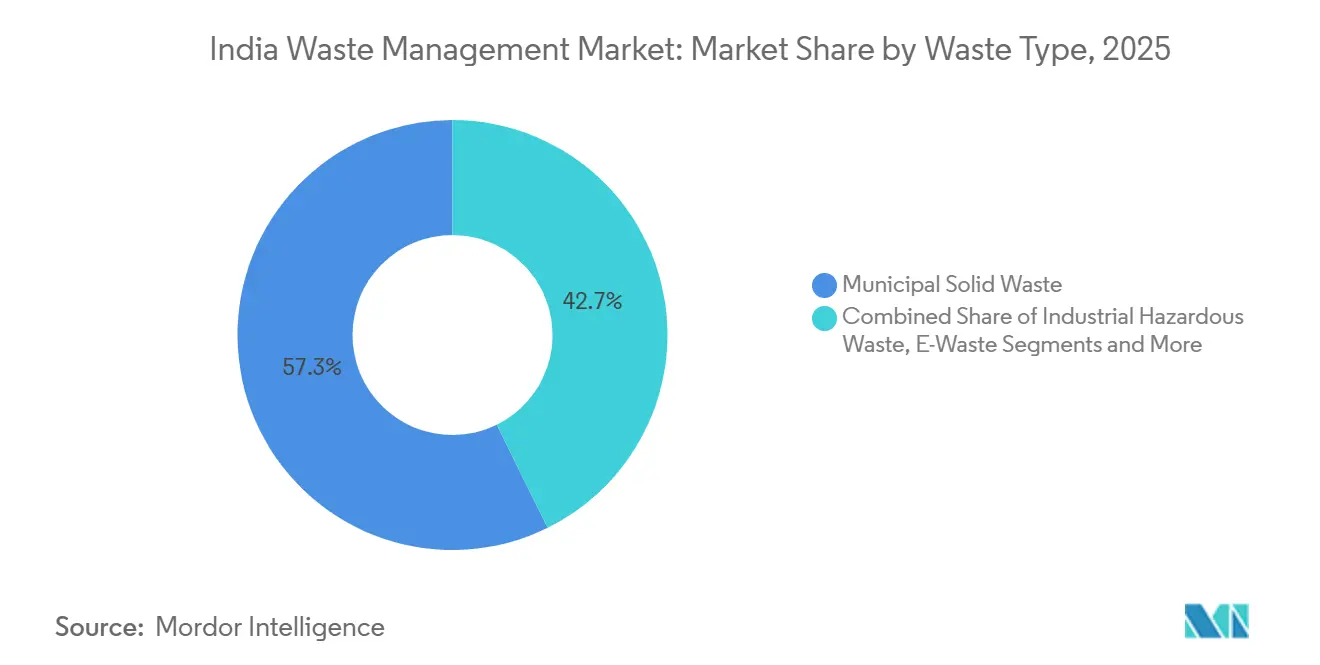

- By waste type, the waste management market in India was led by municipal solid waste, which held a 57.3% share in 2025, whereas e-waste is forecast to grow at a 7.4% CAGR during 2026-2031.

- By region, West India contributed 26.76% of 2025 revenue, and North India is set to register the fastest 6.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Waste Management Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 15th Finance Commission grants unlock INR 1.5 trn ULB capex for SWM 2025-26 | +1.3% | National, with higher disbursement in tier-1 and tier-2 cities | Short term (≤2 years) |

| National Circular Economy Framework 2025 mandates corporate recycling targets | +1.1% | National, with higher compliance in metros and industrial clusters | Long term (≥4 years) |

| Enforcement of Plastic Waste Management Amendment Rules 2024 & single-use plastic ban | +0.9% | National, with early enforcement in Maharashtra, Karnataka, Tamil Nadu | Medium term (2-4 years) |

| FAME-III battery EPR rules bring ~50 GWh end-of-life Li-ion by 2026 | +0.7% | National, concentrated in automotive hubs (Gujarat, Tamil Nadu, Haryana) | Short term (≤2 years) |

| Agri-biomass-to-bioCNG subsidies (SATAT 2.0) spur rural organic-waste valorization | +0.6% | North India (Punjab, Haryana, Uttar Pradesh), Maharashtra | Medium term (2-4 years) |

| Zero-e-waste commitments from hyperscale data-centers drive premium recycling contracts | +0.5% | National, with concentration in Hyderabad, Mumbai, Chennai, Bengaluru | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

15th Finance Commission Grants Unlock USD 18 billion for Municipal SWM

Disbursements covering collection vehicles, mechanized sweepers, and materials-recovery facilities are accelerating PPP bids in cities such as Mumbai, Delhi, and Indore[2]Ecogreen-Hindustan Unilever Recycled Polyethylene. Financial Express, accessed January 2, 2026. https://www.financialexpress.com.. Performance-linked conditions tied to segregation and landfill diversion are forcing municipalities to adopt digital monitoring. Land-acquisition delays capped first-year utilization at 58%, yet the grant program still contributes +1.3% to overall CAGR in the short term.

National Circular Economy Framework 2025 Mandates Corporate Recycling Targets

Companies with annual turnover above INR 500 crore must recycle at least 30% of packaging waste and 50% of electronic products by 2028, with even stricter 95% battery-mass recovery targets for vehicle manufacturers. Brand owners are increasingly entering multi-year offtake contracts with organized recyclers to hedge against virgin-resin price swings and to secure auditable compliance. Implementation success depends on certified capacity and timely penalties; nevertheless, the framework sets a clear compliance pathway and adds roughly +1.1% to sector CAGR over the forecast horizon.

Enforcement of Plastic Waste Management Amendment Rules 2024 & Single-Use-Plastic Ban

State pollution-control boards in Maharashtra, Karnataka, and Tamil Nadu began levying monetary penalties on non-compliant brand owners in 2025, funneling larger volumes of post-consumer plastic into formal channels. Recycled-content thresholds on PET bottles and polyolefin films have improved feedstock predictability for both mechanical and chemical recyclers. A standardized, quarterly EPR credit audit overseen by the Central Pollution Control Board is stimulating a secondary market for plastic-recycling certificates. Robust enforcement in metro areas is already nudging recycling rates upward, though rural districts still lag because of thin collection infrastructure. Over the medium term, more consistent policing and wider civic-awareness campaigns are expected to lift national recovery rates and support the +0.9% uplift to forecast CAGR.

FAME-III Battery EPR Rules Bring 50 GWh End-of-Life Li-ion by 2026

From April 2025, EV manufacturers must collect 90% of battery capacity within seven years of sale. Approximately 50 GWh of lithium-ion cells will retire by 2026, giving licensed recyclers such as Attero Recycling a large, high-value stream of nickel, cobalt, and lithium[3]Battery EPR Rules FAME-III Implementation. Economic Times, accessed January 2, 2026. https://economictimes.indiatimes.com.. Vehicle OEMs have begun pilot take-back networks via dealerships. Fire-safety protocols and the absence of standardized pack design pose near-term bottlenecks, but the high intrinsic metal value supports profit margins and adds +0.7% to CAGR.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Source-segregation average stuck below 35% | −0.8% | Nationwide, especially in tier-3 cities and rural areas | Long term (≥ 4 years) |

| NIMBY litigation halts 280 MW WtE capacity | −0.6% | Delhi NCR, Mumbai, Bengaluru | Medium term (2–4 years) |

| Ammonia-rich mixed food waste corrodes AD assets | −0.5% | Metro cities with high organic volumes | Medium term (2–4 years) |

| Carbon-credit slump (< INR 600/tCO₂e) | −0.4% | Cement corridors of Rajasthan, Madhya Pradesh, and Andhra Pradesh | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Source-Segregation Plateau

Mandatory household segregation into wet, dry, and hazardous waste categories remains largely aspirational, with the national rate stuck below 35% in 2025. Poor civic awareness, weak enforcement, and patchy door-to-door coverage degrade feedstock quality, slashing resale value for recyclables and raising contamination costs for composters. Pilot incentives such as property-tax rebates in Karnataka show localized success but have yet to scale nationally. Unless municipalities adopt real-time monitoring and levy penalties, the sub-optimal segregation will shave -0.8% off forecast CAGR.

NIMBY Litigation Against WtE Plants

Community lawsuits citing air-quality and siting concerns paused about 280 MW of proposed WtE capacity in 2025. Legal challenges extend project gestation by up to two years and elevate financing costs. A transparent emissions-monitoring regime and benefit-sharing with host communities are essential to close the policy-implementation gap; until then, the sector forfeits roughly -0.6% of growth potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Commercial Waste Gains Momentum

Residential sources accounted for 48.83% of India's waste management market revenue in 2025, although commercial volumes can eclipse residential volumes in many tier-1 business districts. Rising organized retail floor space and office complex densification in tier-2 cities are producing larger, more predictable waste streams. Commercial clients typically lock in multiyear service contracts at gate fees of USD 27 - 46 per tonne, compared with USD 10–15 for household waste, making this customer segment attractive to private operators. Collection routing is further optimized through RFID-tagged bins and GPS-enabled compactor trucks, cutting fuel cost and improving turnaround time. Aided by these dynamics, commercial waste volumes are estimated to grow at an 8.6% CAGR to 2031, outpacing the baseline expansion of residential streams.

Developers of shopping malls and business parks increasingly integrate on-site segregation rooms and balers, enhancing feedstock quality for downstream recyclers. Quick-commerce “dark stores” and last-mile delivery hubs are adopting closed-loop packaging, adding additional recyclable cardboard and plastics to formal networks. Operators such as Antony Waste Handling Cell expanded their commercial footprint by 28% in 2025, acquiring new contracts from large retail chains and corporate campuses, reinforcing revenue visibility. On balance, the commercial segment’s higher margin profile and contractual stickiness position it as the prime growth engine within the India waste management market.

By Service Type: Recycling & Resource Recovery Accelerates

In the waste management market in India, collection, transportation, sorting, and segregation held the largest revenue share at 38.76% in 2025, confirming the sector’s traditional focus on hauling fees. Yet recycling and resource recovery are forecast to clock an 8.5% CAGR, the fastest among service lines, driven by EPR credit monetization and higher commodity prices for recovered metals and plastics. Declining landfill availability is forcing municipalities to raise disposal tariffs, making diversion strategies financially compelling. At the same time, organized recyclers benefit from upgraded technology, such as AI-enabled optical sorters and robotic dismantlers, that elevate material purity and selling prices.

The India waste management market size generated by recycling and resource recovery for lithium-ion batteries alone is projected to more than triple between 2026 and 2031 as FAME-III EPR rules mature. Licensed recyclers like Attero have already demonstrated 98% metal-recovery yields, underscoring the value capture potential. Although incineration and WtE additions remain slow due to litigation, mechanical recycling and composting capacities are scaling across major states. Over the forecast horizon, operators able to blend high-quality aggregation with advanced processing are set to capture the steepest value uplift relative to purely hauling-focused peers.

By Waste Type: E-Waste Leads Future Upside

In the waste management industry in India, municipal solid waste dominated at 57.3% of 2025 revenues, yet e-waste represents the most rapid expansion path with a 7.4% CAGR forecast through 2031. India generated roughly 3.2 million tonnes of electronic scrap in 2025, but only 22% reached authorized recyclers, highlighting a vast untapped reservoir. Hyperscale data centers alone produced about 12,000 tonnes of server-grade scrap, which commands gate fees of USD 250–330 per tonne thanks to high precious-metal yields. Formal recyclers have begun installing automated shredders and pyrometallurgical lines to process these high-value streams at an industrial scale.

In parallel, the Plastic Waste Management Amendment Rules 2024 have shifted investor attention to polyolefin and PET recycling. State enforcement squads collected more than USD 5.6 million in penalties during 2025, further encouraging brands to source recycled resin. Construction-and-demolition waste remains underpenetrated, with less than 15% entering formal recycling channels despite regulatory mandates. However, ongoing urban infrastructure build-out is expected to tighten compliance, slowly bridging that gap. Overall, e-waste’s premium margins and regulatory tailwinds place it at the vanguard of future diversification within the India waste management market.

Geography Analysis

West India maintained the lead with 26.76% revenue in 2025, buoyed by Maharashtra and Gujarat’s mature public-private-partnership ecosystems and dense industrial clusters. Municipalities in Mumbai, Pune, and Nagpur awarded more than USD 287 million worth of design-build-operate contracts in 2025, accelerating the modernization of fleet and materials-recovery infrastructure. Source-segregation rates in Maharashtra’s tier-1 cities average 42%, compared with the 35% national benchmark, thanks to proactive civic campaigns and the early rollout of GPS-enabled collection vehicles. However, further growth is tempered by land scarcity for new processing sites.

North India is on track to register the fastest regional CAGR at 6.5% through 2031, energized by Delhi, Uttar Pradesh, and Punjab’s rapid build-out of composting plants and bio-CNG facilities under SATAT 2.0. Uttar Pradesh municipalities drew down USD 50 million in 2025 to procure compactor trucks and establish eight new materials-recovery centers. Punjab and Haryana account for a disproportionate share of new compressed-biogas registrations as rice-straw and wheat-residue valorization gains momentum. Although WtE projects in Delhi remain stuck at 58 MW due to litigation, three approved anaerobic-digestion plants totaling 300 tonnes per day are slated to be commissioned in 2027.

South India mirrors the national growth tempo, with Bengaluru and Hyderabad spearheading technology pilots such as AI-driven waste-segregation kiosks and blockchain-enabled EPR credit exchanges. Chennai’s expanded e-waste processing capacity is tapping into the region’s burgeoning data-center corridor. Conversely, East and Central India lag because of weak private-sector participation and sub-25% segregation rates. Carbon-credit volatility has also curbed refuse-derived-fuel uptake by cement producers in Madhya Pradesh and Chhattisgarh, limiting demand for thermal-treatment infrastructure.

Competitive Landscape

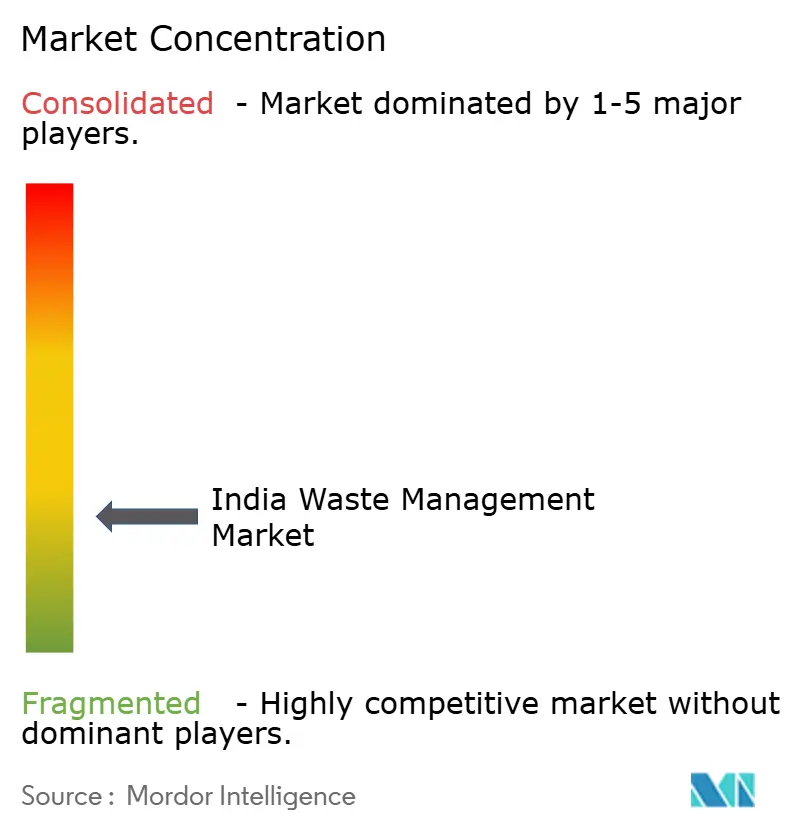

Competition remains fragmented; the top five operators controlled under 18% of total revenue in 2025. Listed incumbents such as Antony Waste Handling Cell and A2Z Green Waste Management leverage municipal concessions, public-market funding, and mechanized fleets to expand geographic reach. Meanwhile, specialized players like Attero and Exigo focus on high-margin verticals battery and e-waste recycling where technical barriers to entry and stringent licensing favor scale players. Digital-first aggregators, including Recykal and Saahas Zero Waste, differentiate through AI-powered sorting, real-time traceability, and EPR credit trading platforms that appeal to sustainability-oriented corporates.

Strategically, incumbents are bidding aggressively for long-duration design-build-operate contracts that ensure stable cash flow, while newcomers target niche streams such as hyperscale-data-center hardware, lithium-ion batteries, and agri-biomass bio-CNG. Intellectual-property filings are rising: Antony Waste applied for an RFID-based bin-tracking patent in 2025, and Recykal is scaling an AI recognition engine that boosts mixed-plastic sorting accuracy to 92%. Private-equity capital continues to flow, with Recykal closing a USD 22 million Series B round in 2025 to extend its digital marketplace to 180 cities.

White-space opportunities persist in construction-and-demolition recycling and rural organic-waste aggregation, both still dominated by informal handlers. Execution risks - land acquisition, regulatory approvals, and skilled labor - remain the major differentiators. Operators capable of combining concession management expertise with advanced processing technology are best positioned to consolidate share as regulatory scrutiny intensifies across the India waste management market.

India Waste Management Industry Leaders

-

A2Z Green Waste Management Ltd

-

Antony Waste Handling Cell Ltd

-

Attero Recycling Pvt Ltd

-

BVG India Ltd

-

Cerebra Integrated Technologies Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Attero Recycling and Tata Motors agreed to open 50 lithium-ion battery collection centers across three states, targeting 20,000 tonnes annual throughput by 2028.

- November 2025: Antony Waste Handling Cell bagged a 15-year USD 100 million contract from Greater Noida to manage a 400 TPD materials-recovery facility and citywide collection.

- September 2025: Ramky Enviro Engineers commissioned a 150-TPD anaerobic-digestion plant in Visakhapatnam, securing a decade-long offtake with Bharat Petroleum at USD 0.54 per kg of bio-CNG.

- August 2024: BVG India won a USD 74 million design-build-operate deal with Indore, including a 600-TPD composting unit tied to landfill-diversion KPIs.

India Waste Management Market Report Scope

Waste management involves collecting, transporting, processing, recycling, and disposing of waste from homes, businesses, and industries. This market handles diverse waste types, including municipal solid waste, hazardous materials, e-waste, and medical refuse. Environmental regulations, sustainability efforts, and technological advancements fuel the market's growth. Notable trends include the adoption of circular economy practices, the rise of smart waste management solutions, and the implementation of waste-to-energy technologies.

The India Waste Management market is segmented by waste type (industrial waste, municipal solid waste, hazardous waste, e-waste, plastic waste, and bio-medical waste), by disposal methods (collection, landfills, incineration, and recycling). The report offers market size and market forecasts for India Waste Management market in value (USD).

By Source

| Residential |

| Commercial (retail, office, etc.) |

| Industrial |

| Medical (Health and Pharmaceutical) |

| Construction & Demolition |

| Others (institutional, agricultural, etc) |

By Service Type

| Collection, Transportation, Sorting & Segregation | |

| Disposal / Treatment | Landfill |

| Recycling & Resource Recovery | |

| Incineration & Waste-to-Energy | |

| Others (Chemical Treatment, Composting, etc.) | |

| Others (Consulting, Audit & Training, etc.) |

By Waste Type

| Municipal Solid Waste |

| Industrial Hazardous Waste |

| E-waste |

| Plastic Waste |

| Biomedical Waste |

| Construction & Demolition Waste |

| Agricultural Waste |

| Other Specialized Waste (radio active, etc) |

By Region

| North India |

| South India |

| West India |

| East India |

| Central India |

| By Source | Residential | |

| Commercial (retail, office, etc.) | ||

| Industrial | ||

| Medical (Health and Pharmaceutical) | ||

| Construction & Demolition | ||

| Others (institutional, agricultural, etc) | ||

| By Service Type | Collection, Transportation, Sorting & Segregation | |

| Disposal / Treatment | Landfill | |

| Recycling & Resource Recovery | ||

| Incineration & Waste-to-Energy | ||

| Others (Chemical Treatment, Composting, etc.) | ||

| Others (Consulting, Audit & Training, etc.) | ||

| By Waste Type | Municipal Solid Waste | |

| Industrial Hazardous Waste | ||

| E-waste | ||

| Plastic Waste | ||

| Biomedical Waste | ||

| Construction & Demolition Waste | ||

| Agricultural Waste | ||

| Other Specialized Waste (radio active, etc) | ||

| By Region | North India | |

| South India | ||

| West India | ||

| East India | ||

| Central India | ||

Key Questions Answered in the Report

What is the current value of India’s waste management market?

The market is valued at USD 14.29 billion in 2026 and is set to reach USD 18.94 billion by 2031.

Which waste stream is growing the fastest?

E-waste is forecast to expand at a 7.4% CAGR through 2031, driven by data-center and consumer electronics disposal.

Why are recycling and resource-recovery services gaining momentum?

Higher margins from EPR credits and valuable recovered materials, combined with rising landfill costs, are steering investment toward recycling.

Which region offers the strongest growth outlook?

North India is projected to rise at a 6.5% CAGR, supported by new composting and bio-CNG plants under SATAT 2.0.

How fragmented is the competitive landscape?

The top five players account for under 18% of revenue, indicating a highly fragmented market with ample room for consolidation.

Page last updated on: