Market Overview

| Study Period | 2021 - 2031 |

|---|---|

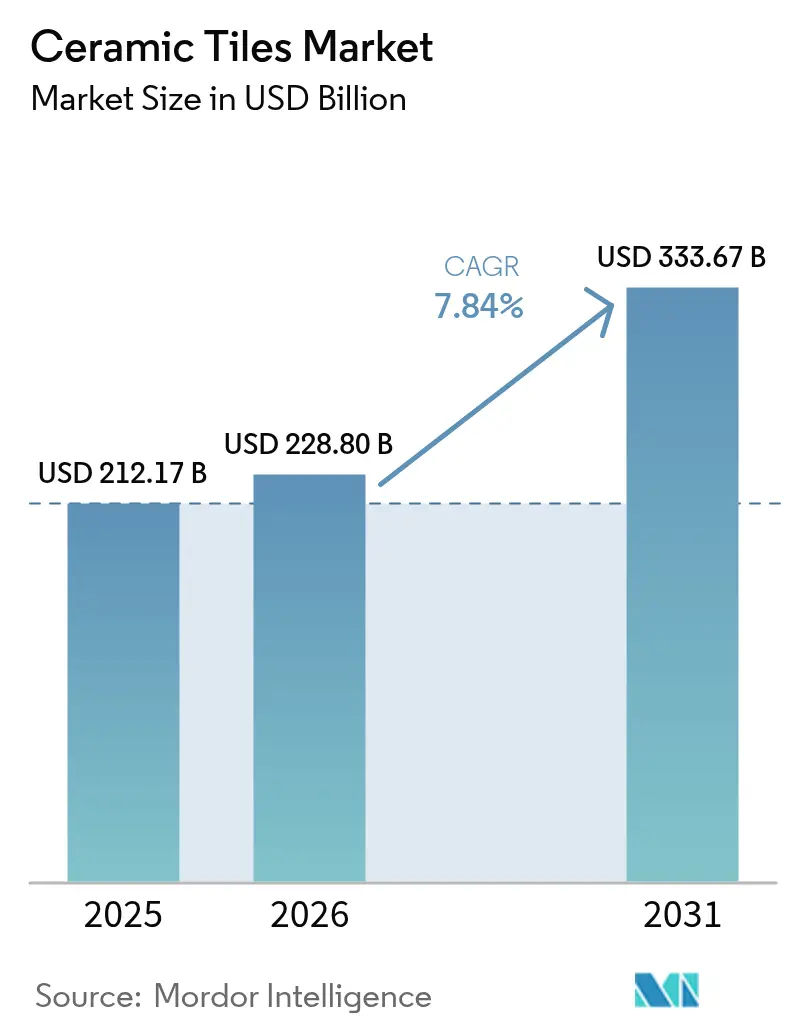

| Market Size (2026) | USD 228.8 Billion |

| Market Size (2031) | USD 333.67 Billion |

| Growth Rate (2026 - 2031) | 7.84% CAGR |

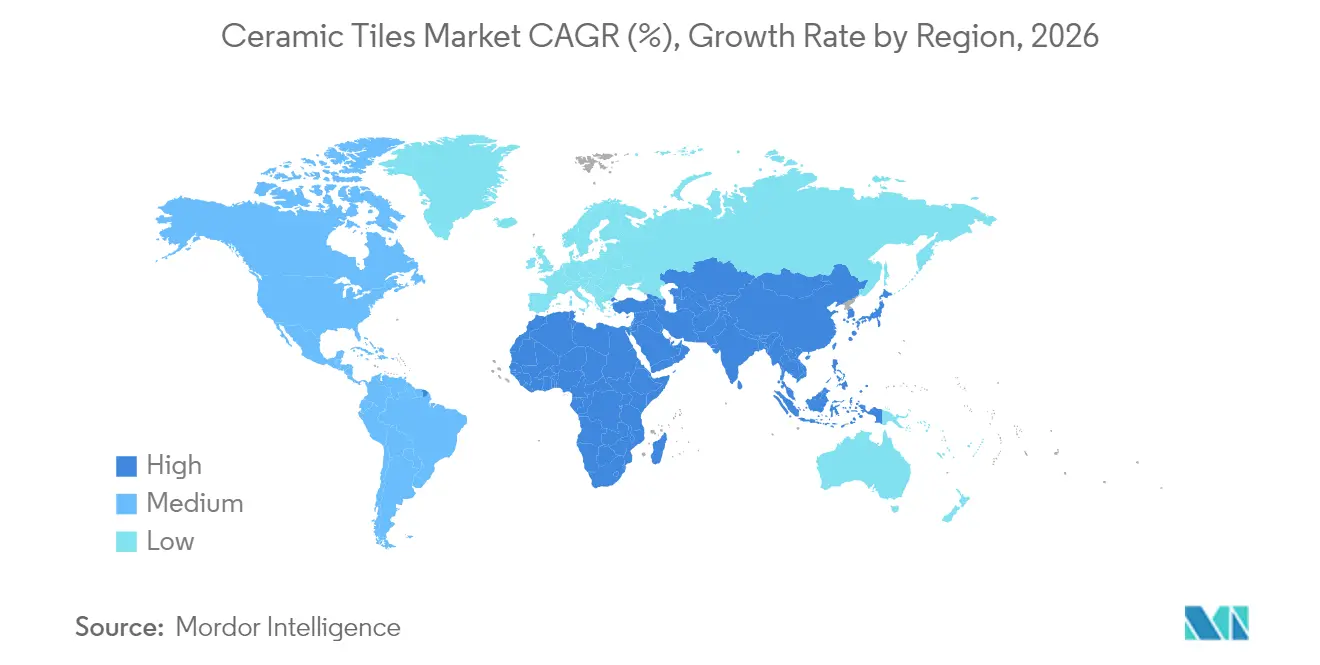

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

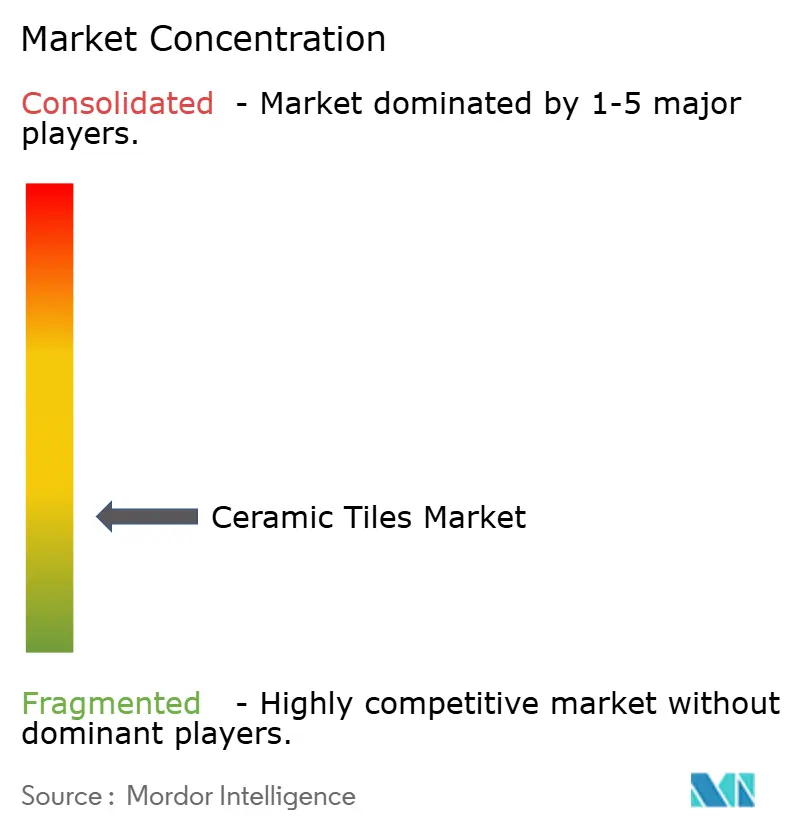

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ceramic Tiles Market Analysis by Mordor Intelligence

The ceramic tiles market size in 2026 is estimated at USD 228.8 billion, growing from 2025 value of USD 212.17 billion with 2031 projections showing USD 333.67 billion, growing at 7.84% CAGR over 2026-2031. Steady public-sector infrastructure outlays, rapid urban migration in Asia-Pacific, and consumers’ preference for durable, easy-to-clean surfaces anchor this expansion. New government spending packages in the United States and ongoing metro, airport, and smart-city developments in India and Southeast Asia are enlarging the addressable base for flooring and cladding products. Demand also benefits from technology that prints hyper-realistic stone, wood, and metallic effects on porcelain bodies, enabling premiumization without the price volatility of natural materials. Environmental regulations in Europe accelerate the rollout of low-carbon kilns and waste-based raw mixes, while online retail channels broaden product availability and price transparency worldwide.

Key Report Takeaways

- By product type, porcelain tiles led with 50.78% of the ceramic tiles market share in 2025; glazed porcelain is forecast to post the fastest 8.42% CAGR through 2031.

- By application, floor tiles accounted for 48.22% of the ceramic tiles market size in 2025, while wall tiles are advancing at the highest 8.16% CAGR to 2031.

- By end-user, the residential segment held 54.62% revenue share in 2025; the commercial segment records the swiftest 7.76% CAGR through 2031.

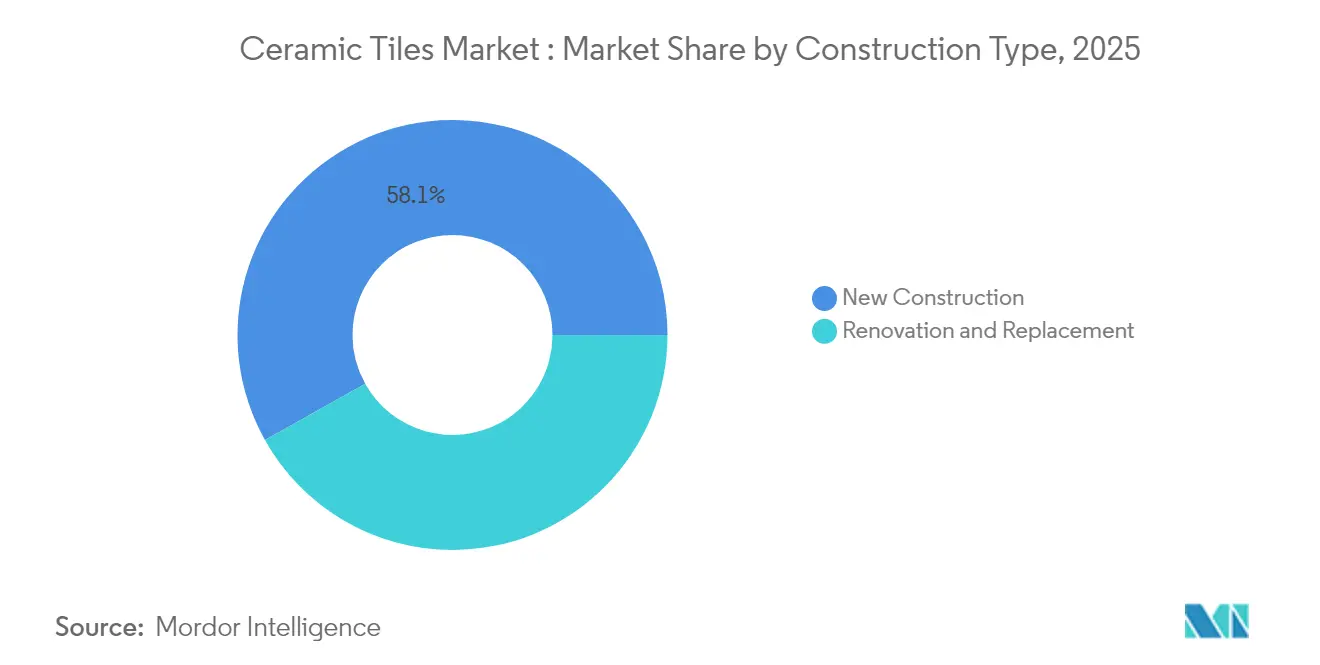

- By construction type, new construction captured 58.12% of the ceramic tiles market size in 2025, yet renovation and replacement are expanding faster at 7.52% CAGR.

- By distribution channel, independent retailers and home centers commanded a 41.75% share in 2025; online retail is growing at a 10.31% CAGR.

- By geography, Asia-Pacific dominated with 47.12% market share in 2025 and also posts the strongest 8.33% CAGR through 2031.

- The ceramic tiles market is moderately fragmented. The five largest players, Mohawk Industries, Grupo Lamosa, SCG Ceramics, Kajaria Ceramics, and RAK Ceramics, collectively hold major market share in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ceramic Tiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Construction and Infrastructure Development | +2.1% | Global, with concentration in Asia-Pacific and North America | Long term (≥ 4 years) |

| Increasing Demand for Aesthetic and Durable Flooring Solutions | +1.8% | Global, particularly Europe and North America premium segments | Medium term (2-4 years) |

| Growing Preference for Eco-Friendly and Sustainable Products | +1.3% | Europe and North America, spreading to Asia-Pacific | Medium term (2-4 years) |

| Advancements in Manufacturing Technology | +1.0% | Global, led by European and Asian manufacturers | Long term (≥ 4 years) |

| Rising Disposable Income and Changing Lifestyle | +0.9% | Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Increasing Ageing Building Infrastructure and Demand for Renovation Activities | +0.7% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Construction and infrastructure expansion

Global capital spending on transport corridors, energy plants, and mixed-use complexes is stimulating large-volume orders for the ceramic tiles market. In the United States, multiyear federal programmed collectively allocate USD 1.2 trillion to roads, bridges, semiconductor fabs, and clean-energy facilities, generating sustained demand for heavy-duty porcelain specified in factories and data centers. China’s Belt and Road Initiative drives tile-intensive rail stations and housing in partner economies, while ASEAN governments raise civil works budgets that favor flooring products with 30-year service lives. Suppliers of aggregates and cement report double-digit revenue growth, signaling robust downstream consumption of ceramic surfacing.

Demand for aesthetic, durable surfaces

Designers increasingly combine visual impact with performance, fuelling the uptake of large-format planks and marble-look slabs. Inkjet printers replicate veining and metallic highlights that rival quarried stone, but at lower weight and in repeatable colourways. Format growth—porcelain boards up to 1.8 m by 3.6 m—reduces grout lines and conveys seamless continuity valued in open-plan offices and luxury residences. Quick-fire glazes cut production cycles, enabling frequent style introductions that mirror fashion trends. The ceramic tiles market also gains share versus hardwood in kitchens and basements where moisture resistance is critical. Architects specify anti-static finishes for electronics assembly floors, widening functional appeal beyond décor.

Preference for eco-friendly products

Circular-economy targets push European producers to reclaim kiln heat, recycle sludge, and replace virgin clay with industrial by-products. Italian plants now recycle up to 100% of unfired scrap and operate high-efficiency burners that cut CO₂ per square meter by one-fifth compared with 2010 levels. Research in Poland proves that incorporating mining waste lowers raw-mix cost by up to 35% while retaining flexural strength above 40 MPa for stoneware bodies. Green certifications increasingly influence retail purchases, especially in Germany and the Nordic region. Government procurement guidelines that favor low-carbon building materials amplify this shift and open export opportunities for compliant Asian producers.

Manufacturing technology advances

Automation, vision systems, and AI-driven process control elevate yield and uniformity. Plant-wide execution platforms adjust kiln curves in real time, trimming energy and scrap. Next-generation piezoelectric printheads apply selective digital glazing, reducing overspray and pigment waste. Integrated pressing-firing lines shorten lead times, letting manufacturers switch designs within hours to meet online order patterns. Equipment vendors promote modular service contracts that spread capex and guarantee uptime, allowing mid-size firms to scale competitively and thereby expand the ceramic tiles market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Installation and Maintenance Costs | -1.4% | Global, particularly impacting price-sensitive segments | Short term (≤ 2 years) |

| Fragility and Risk of Cracking | -1.2% | Global, with higher impact in seismic zones and extreme climate regions | Medium term (2-4 years) |

| Raw Material Price Volatility | -1.1% | Global, with acute impact in import-dependent regions | Medium term (2-4 years) |

| Environmental Concerns in Manufacturing | -0.8% | Europe and North America leading, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High installation and maintenance costs

Skilled tile setters remain scarce in many developed markets, lifting labour rates and extending project timelines. Large-format porcelain slabs need specialised lifting rigs and epoxy grouts, adding 15-25% to installation budgets versus standard 60 cm products. Where homeowners can install floating vinyl planks themselves over a weekend, ceramic renovations require professional waterproofing and sub-floor preparation. Industry associations have stepped up certification schemes, yet supply of certified crews lags demand, tempering short-run volume growth, especially in refurbishments.

Raw material price volatility

Feldspar, zircon, and natural gas prices fluctuate with mining disruptions and geopolitical events, eroding producer margins. Mohawk Industries incurred USD 41 million in extra input costs in Q1 2025, underscoring exposure to upstream swings[1]Source: Mohawk Industries, “Q1 2025 Results,” mohawkindustries.com. Portuguese mineral studies confirm that Na-feldspar blends aid fast-firing but command premium prices, whereas K-feldspar enhances strength yet is geographically uneven in supply. European gas-price spikes prompt kiln fuel switching to LPG or hydrogen pilots, though adoption costs remain high for smaller plants. Hedging and multi-sourcing strategies alleviate but do not eliminate volatility risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Porcelain Dominance Drives Premium Shift

Porcelain tiles secured 50.78% of the ceramic tiles market share in 2025 owing to water-absorption rates below 0.5% and frost resistance that suits outdoor plazas and transit hubs. Glazed porcelain, aided by inkjet decoration, is projected to register an 8.42% CAGR through 2031, outpacing glazed ceramic and mosaic formats. Consumers perceive its colour-through body and abrasion class ≥ PEI IV as proof of longevity, encouraging substitution for marble in hotel lobbies and airports.

The segment’s momentum lifts the overall ceramic tiles market as manufacturers leverage continuous kilns to mass-produce large thin slabs for façades, reducing structural load yet retaining impact strength. Mosaic tiles, though niche, capture share in luxury spas were artisanal aesthetics command price premiums. Copper-glaze innovations offering antimicrobial action broaden use in food-handling zones and hospitals, illustrating how product diversification underpins sustained revenue growth.

By Application: Floor Tiles Lead While Wall Segments Accelerate

Floor installations represented 48.22% of the ceramic tiles market size in 2025 driven by mandatory specification in wet areas and heavy-traffic corridors. Slip-resistant porcelain and industrial-grade quarry tiles dominate commercial kitchens, warehouses, and transit stations, ensuring baseline volume stability.

Wall applications, posting an 8.16% CAGR to 2031, flourish as architects deploy textured and 3D surfaces for feature walls, hotel receptions, and retail backdrops. Expanded design palettes increase average selling prices, and easy-clean glazes meet hospitality hygiene codes. Roof and façade uses remain concentrated in Mediterranean and Andean regions where ceramic’s thermal mass and hail resistance are valued, while countertop, pool, and niche applications collectively extend total addressable demand.

By End-User: Residential Foundation Supports Commercial Growth

Homebuilding and do-it-yourself renovation kept the residential segment at 54.62% share in 2025: homeowners favor porcelain in kitchens and bathrooms to lift resale values and curb water damage risk. Developer-built multifamily housing in rapidly urbanizing economies ensures baseline demand and encourages distributors to stock value-priced SKUs.

Commercial projects, however, provide the fastest 7.76% CAGR as office landlords and retailers pivot to antimicrobial, low-VOC surfaces that reassure occupants. High-use arenas, schools, and healthcare facilities specify rectified porcelain planks for resilience and aesthetics. Industrial plants adopt acid-resistant tiles for clean rooms and chemical process floors, diversifying the ceramic tiles market revenue base.

By Construction Type: New Projects Lead Despite Renovation Momentum

New construction kept 58.12% of the ceramic tiles market size in 2025, buoyed by greenfield housing tracts and public-sector megaprojects that integrate flooring at the blueprint stage. Bulk purchases lower per-unit logistics cost, reinforcing price competitiveness versus luxury vinyl and engineered hardwood.

Renovations grow at 7.52% CAGR through 2031 as mid-life buildings in the United States, Europe, and Japan require interior refreshes to meet post-pandemic wellness norms. Thin-tile overlays allow upgrades without demolition, shortening downtime for hotels and malls. Government-funded retrofit schemes aimed at energy efficiency further propel replacement demand.

By Distribution Channel: Traditional Retail Faces Digital Disruption

Independent retail outlets and home-center chains together controlled 41.75% share in 2025, leveraging showroom vignettes and accredited installer referrals to convert walk-in traffic. Regional distributors consolidate to expand assortments and logistics reach.

E-commerce, advancing at 10.31% CAGR, reshapes purchase journeys: high-definition configurators let consumers visualize bathrooms in augmented reality, and sample-box services cut decision cycles. Manufacturers pilot direct-to-site fulfilment for contractors, bypassing intermediaries on large commercial orders. Hybrid click-and-collect models, therefore, emerge as the default omnichannel format for the ceramic tiles market.

Geography Analysis

Asia-Pacific accounted for 47.12% of global revenue in 2025 and is forecast to compound to 8.33% annually through 2031, anchored by mass urban housing, metro extensions, and export-oriented production clusters. China’s inland provinces add capacity close to clay deposits, while India scales smart-city and affordable-housing schemes that stipulate vitrified flooring. Vietnam’s 100-plus manufacturers, concentrated in the north, rely on imported chemicals for glazes but still achieved a combined output mix of 80% glazed and 20% porcelain tiles in 2024. ASEAN trade agreements allow duty-free flows, favouring regionally integrated supply chains.

North America presents a mature but strategically important arena where domestic producers hedge against future antidumping duties. US tile consumption eased to 264.5 million m² in 2024 amid high mortgage rates, yet federal outlays on semiconductor and battery plants underpin long-term volume. Mohawk Industries leverages vertically integrated Tennessee and Texas kilns to shorten lead times and secure public-project specifications. Canada funds hospital and transit refurbishments that increasingly stipulate low-carbon materials, while Mexico’s Grupo Lamosa operates plants across Latin America to diversify currency exposure.

Europe, while posting an 18% output drop in 2023 due to energy spikes, still accounts for 50% of global tile-machinery exports assopiastrelle.it. Italy’s closed-loop plants recycle 100% of unfired scrap, showcasing environmental leadership. Spain advances hydrogen-kiln pilots to meet EU Net-Zero targets, while Poland’s clay shortages force higher imports and spot-price volatility. In the Middle East and Africa, Egypt produces 200 million m² annually using low-cost shale resources, and the UAE’s Ras Al Khaimah cluster hosts 40,000 industrial registrants, fuelling related surface-finishing demand.

Competitive Landscape

The ceramic tiles market is moderately fragmented. The five largest players—Mohawk Industries, Grupo Lamosa, SCG Ceramics, Kajaria Ceramics, and RAK Ceramics—collectively hold an estimated mid-30% revenue share, leaving room for regional specialists. Scale advantages accrue from captive clay mines, in-house frit plants, and continent-wide distribution hubs.

Firms pursue vertical integration and geographic diversification. Mohawk expanded capacity by 30 million m² through a new Tennessee factory, while Grupo Lamosa bought Spain’s Baldocer unit to enter premium Mediterranean segments. SCG Ceramics merges Thai and Vietnamese networks to secure raw-material continuity and cut freight times to Australia.

Technological differentiation intensifies: KEDA Industrial’s “digital factory” suite bundles IoT sensors, machine-vision sorters, and predictive maintenance, enabling small plants to replicate best-in-class yield. Producers also develop antibacterial glazes and solar-reflective roof tiles to address evolving building codes. Private-equity interest in machinery suppliers—exemplified by One Equity Partners backing Gruppo Siti B&T—signals confidence in capital equipment cycles tied to broader ceramic tiles market growth.

Ceramic Tiles Industry Leaders

Mohawk Industries

Grupo Lamosa

SCG Ceramics PCL

Kajaria Ceramics

RAK Ceramic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: Transom Capital merged Virginia Tile with Galleher, forming a nationwide platform that integrates ceramics, hardwood, and installation supplies.

- June 2024: One Equity Partners invested in Gruppo Siti B&T, boosting R&D for high-speed presses and digital glaze lines that underpin next-wave capacity upgrades.

- May 2024: Eagle Materials committed USD 430 million to expand its Wyoming cement plant by 50% and cut per-tonne CO₂ by 20%, assuring a secure supply of tile-grade clinker for western US projects.

Global Ceramic Tiles Market Report Scope

Ceramic tiles comprise clay and natural materials like sand, quartz, and water. Ceramic tiles are used in houses, restaurants, offices, shops, and so on, as bathroom walls and kitchen floor surfaces. The ceramic tiles market is segmented by product type, application, construction, end user, and geography.

The market is segmented by product into glazed, porcelain, and scratch-free. By application, the market is segmented into floor tiles and wall tiles. By construction, the market is segmented into new construction and replacement and renovation. By end-user, the market is segmented into residential and commercial. The market is geographically segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report offers market size and forecasts in value (USD) for all the above segments.

By Product Type

| Porcelain Tiles |

| Glazed Ceramic Tiles |

| Unglazed Ceramic Tiles |

| Mosaic Tiles |

| Others |

By Application

| Floor |

| Wall |

| Roofing |

| Others |

By End-User

| Residential |

| Commercial |

| Industrial |

By Construction Type

| New Construction |

| Renovation and Replacement |

By Distribution Channel

| Independent Retailers |

| Large Home Centers |

| Online Retail |

| Direct Sales to Contractors |

By Geography

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Porcelain Tiles | |

| Glazed Ceramic Tiles | ||

| Unglazed Ceramic Tiles | ||

| Mosaic Tiles | ||

| Others | ||

| By Application | Floor | |

| Wall | ||

| Roofing | ||

| Others | ||

| By End-User | Residential | |

| Commercial | ||

| Industrial | ||

| By Construction Type | New Construction | |

| Renovation and Replacement | ||

| By Distribution Channel | Independent Retailers | |

| Large Home Centers | ||

| Online Retail | ||

| Direct Sales to Contractors | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the ceramic tiles market?

The ceramic tiles market generates USD 228.8 billion in 2026.

How fast is the ceramic tiles market expected to grow?

It is forecast to grow at a 7.84% CAGR and reach USD 333.67 billion by 2031.

Which is the fastest growing region in Ceramic Tiles Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region leads in ceramic tile consumption?

Asia-Pacific holds 47.12% of global revenue and posts the quickest 8.33% CAGR through 2031.

What years does this Ceramic Tiles Market cover?

The report covers the Ceramic Tiles Market historical market size for years: 2021, 2022, 2023, 2024 and 2025. The report also forecasts the Ceramic Tiles Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Why are porcelain tiles so dominant?

Porcelain’s low water absorption, high strength, and aesthetic versatility delivered 50.78% market share in 2025.

How is e-commerce changing tile distribution?

Online channels, expanding at 10.31% CAGR, let buyers visualize rooms, order samples, and schedule direct site delivery, prompting hybrid retail models.

Page last updated on: