Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

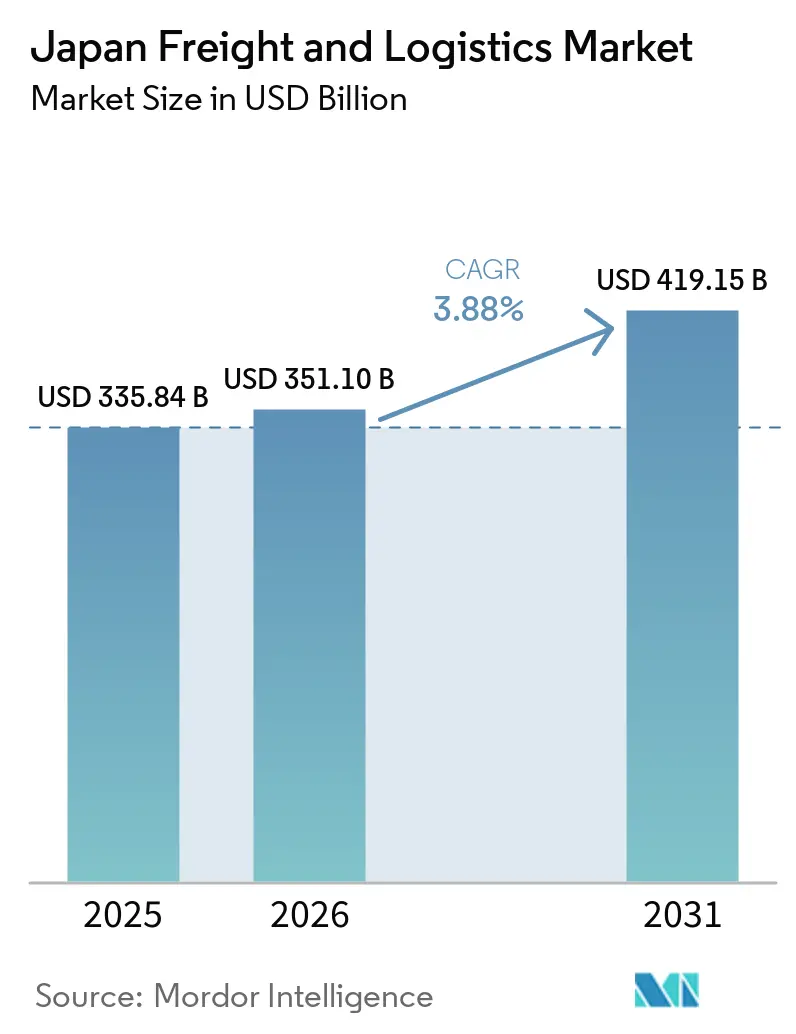

| Base Year Market Size (2025) | USD 335.84 Billion |

| Market Size (2026) | USD 351.10 Billion |

| Market Size (2031) | USD 419.15 Billion |

| Growth Rate (2026 - 2031) | 3.88% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Freight And Logistics Market Analysis by Mordor Intelligence

The Japan Freight and Logistics Market size was valued at USD 335.84 billion in 2025 and is estimated to grow from USD 351.10 billion in 2026 to reach USD 419.15 billion by 2031, at a CAGR of 3.88% during the forecast period (2026-2031). Robust near-shoring of critical supply chains, large-scale public infrastructure spending, and a national push for digital transformation are expanding volumes while changing the mix of services that shippers demand. Record investments in port automation and high-speed maglev freight corridors are shortening delivery windows, which in turn raise expectations for time-definite services. Cold-chain demand is climbing as biologics production and fresh-food e-commerce widen, creating premium opportunities for temperature-controlled storage and transport. Meanwhile, decarbonization rules and aging quay cranes squeeze operator margins, prompting carriers to prioritize fuel-efficient assets and to reroute vessels away from congested gateways. Competitive strategies now revolve around data integration, security clearances, and specialized handling capabilities that satisfy stricter government guidelines for economic security and pharmaceutical integrity.

Key Report Takeaways

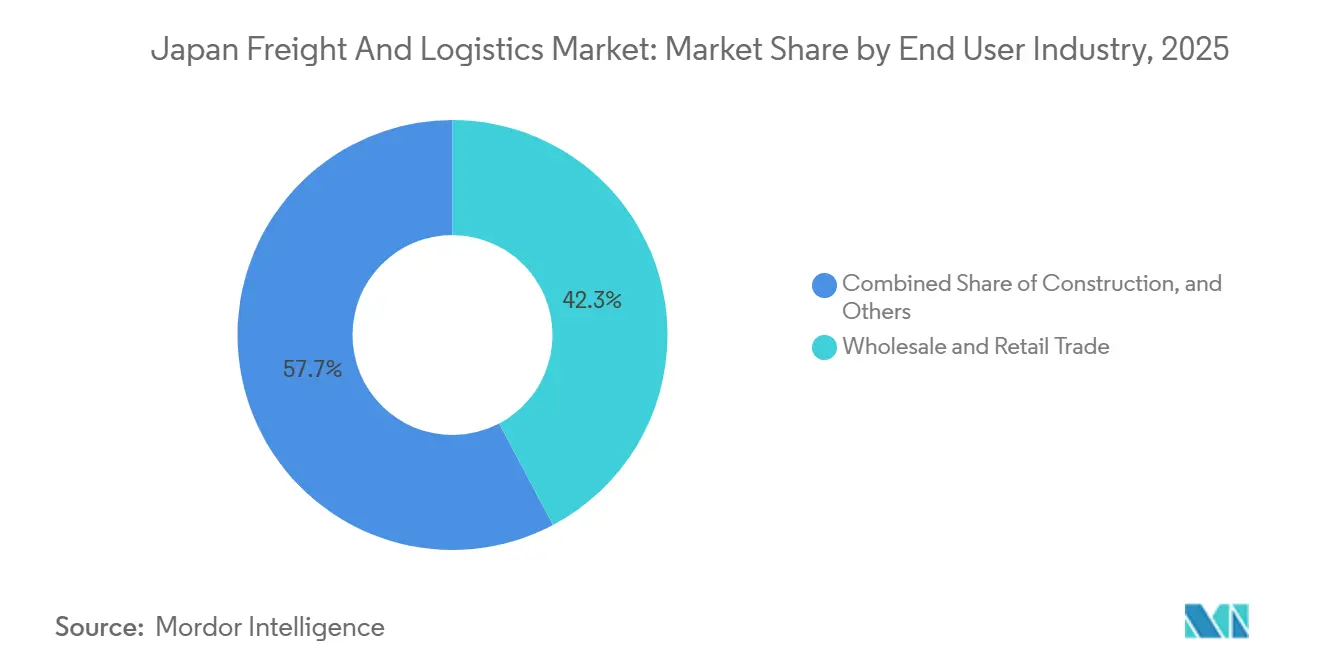

- By end-user, wholesale and retail trade led with 42.26% of the Japan freight and logistics market size in 2025, while the segment is forecast to expand at a 3.86% CAGR through 2031.

- By logistics function, freight transport accounted for 70.85% of the Japan freight and logistics market share in 2025, and courier, express, and parcel services are projected to grow at a 4.15% CAGR to 2031.

- By transport mode, road captured 80.85% of revenue share in 2025, whereas air freight is advancing at a 4.10% CAGR during 2026-2031.

- By CEP service, domestic operations held 64.05% of the revenue share in 2025, while international services are set to rise at a 4.29% CAGR through 2031.

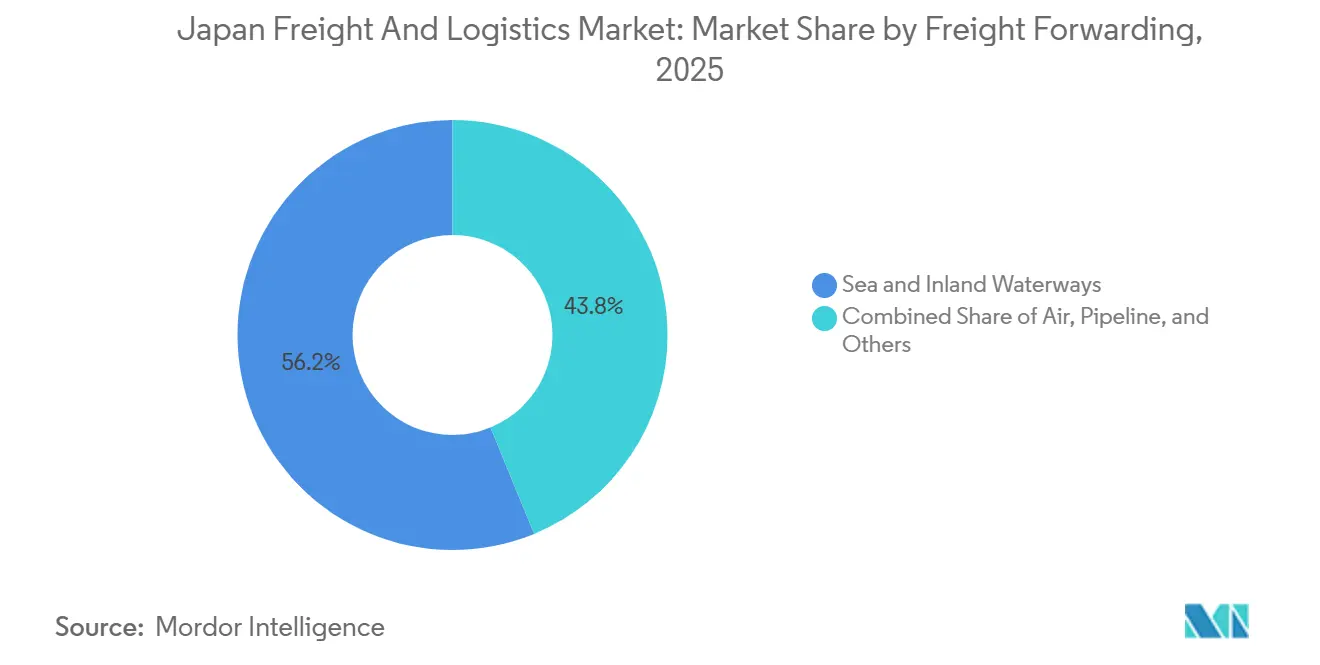

- By freight-forwarding mode, sea and inland waterways commanded 56.20% of the revenue share in 2025, and air forwarding is poised for a 3.67% CAGR by 2031.

- By warehousing, non-temperature-controlled facilities represented 92.01% in 2025, whereas temperature-controlled space is projected to climb at a 3.46% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Freight And Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Domestic near-shoring of critical supply chains | 1.1% | National, concentrated in Kyushu (semiconductors) and Tohoku (advanced materials) | Medium term (2-4 years) |

| National Logistics DX program & data-sharing mandates | 0.9% | National, pilot deployments in the Tokyo-Osaka corridor | Short term (≤ 2 years) |

| Record public spending on port, airport & Maglev freight corridors | 0.7% | National, priority investments in Osaka Bay, Haneda expansion, and Chuo Shinkansen | Long term (≥ 4 years) |

| Biologics & fresh-food cold-chain surge | 0.6% | Nationwide, the highest intensity is in metropolitan pharmaceutical hubs and agricultural regions. | Medium term (2-4 years) |

| Carbon-neutral freight incentives accelerating rail & coastal shift | 0.4% | National, modal shift is strongest on Tokyo-Osaka and Kanto-Kansai routes | Medium term (2-4 years) |

| Defence-industry logistics demand from the US-Japan security alignment | 0.3% | National, concentrated near defense manufacturing clusters and US military installations. | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Domestic Near-Shoring of Critical Supply Chains

Japan’s 2024 economic security law designates semiconductors, rare earths, and key APIs as strategic, so manufacturers are relocating production from overseas and building redundant plants inside the country. New fabs in Kyushu and advanced materials lines in Tohoku require frequent small-lot deliveries that lift shipment counts even when output volumes stay flat. Temperature-controlled, vibration-free trucks now serve lithography and chemical loads that cannot tolerate shock or heat. Government subsidies worth JPY 2.4 trillion (USD 15 billion) through 2026 reimburse up to one-third of relocation costs, locking in demand for industrial project logistics over the next three years. Logistics firms able to certify cleanroom trailers and GPS-linked humidity sensors command premium rates from semiconductor majors that must maintain sub-10 ppm contamination thresholds. Near-shoring also extends to battery materials, driving up movements of hazardous cathode powder that require ADR-compliant drivers and secure storage[1]Taiwan Semiconductor Manufacturing Company (TSMC), “Kumamoto Fab Overview,” tsmc.com.

National Logistics DX Program and Data-Sharing Mandates

MLIT’s Logistics DX Action Plan enforces common data formats for tracking, warehousing, and transport management by fiscal 2027. Large 3PLs that already run EDI and digital twins can match demand with real-time capacity, cutting empty-backhaul mileage by 10% and saving fuel. Smaller regional carriers face compliance spending that equals a year of net profit, which is pushing many toward M&A or white-label platform partnerships to maintain shipper visibility. The Personal Information Protection Commission issued 2025 guidance that clarifies data handling rules, calming customer concerns and enabling broader API integration. As interfaces normalize, shippers gain lane-level cost and delay forecasts, letting them shift freight to rail or coastal services when highways clog[2]Personal Information Protection Commission, “Guidelines on Data Utilization,” ppc.go.jp .

Record Public Spending on Ports, Airports, and Maglev Freight Corridors

Japan’s FY 2025 budget channels JPY 6.8 trillion (USD 43 billion) into transport projects, including automated quays at Yokohama that will lift crane productivity by 30%. Haneda’s 2025 cargo expansion added 150,000 m² of controlled-temperature space that meets GDP guidelines, unlocking new biologics exports. The Chuo Shinkansen maglev promises overnight freight at 500 km/h, trimming Tokyo-Osaka truck hauls from five hours to forty minutes. Together, these upgrades let distributors redesign networks around high-speed hubs, shrinking safety stocks and freeing working capital that can then fund further automation.

Biologics and Fresh-Food Cold-Chain Surge

Revised 2025 Good Distribution Practice rules demand continuous temperature validation from the loading dock to the pharmacy shelf. Pharmacies, hospitals, and online grocers, therefore, contract only with carriers that provide real-time monitoring and redundant power. Yamato installed automated cold stores with robotic pickers to cut worker exposure to sub-zero conditions and to raise pick accuracy above 99.7%. Fresh-food e-commerce now claims 8.5% of grocery sales, so parcel networks are adding insulated totes and two-hour delivery windows that mesh with elder-care meal plans. Insurance underwriters need verifiable sensor trails before covering biologics in transit, pushing operators to share excursion data and thereby deepening digital integration across partners.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing quay cranes & lock infrastructure bottlenecks | -0.6% | National, most severe at Tokyo, Osaka, Kobe, and Nagoya ports | Short term (≤ 2 years) |

| Rising decarbonization compliance costs (fuel EU ETS, IMO CII) | -0.5% | National, disproportionate impact on international shipping routes | Medium term (2-4 years) |

| Spike in catastrophe-driven cargo insurance premiums | -0.4% | Nationwide, the highest increases are in Pacific coastal zones and seismically active regions | Short term (≤ 2 years) |

| Heightened labor-action risk amid driver work-style reforms | -0.3% | National, concentrated in long-haul trucking and port operations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Quay Cranes and Lock Bottlenecks

Tokyo Port runs cranes averaging more than 25 years, so unplanned outages rose 15% in 2025 compared with 2024. Carriers diverted calls to Yokohama or Busan, adding two days to semiconductor export schedules. Replacing a single crane costs USD 12 million and cuts berth capacity during installation; port authorities stagger projects to avoid gridlock, yet still face peak-season congestion. Inland lock systems that link coastal ports to interior hubs are even older, with some gates exceeding 50-year design lives. Deferred maintenance constrains barge traffic, forcing cargo onto already scarce trucks[3] International Maritime Organization, “CII Regulatory Impact,” imo.org.

Rising Decarbonization Compliance Costs

CII mandates compel ocean carriers to spend USD 80 million to USD 120 million per vessel on retrofits, which translates into environmental surcharges of USD 150 to USD 200 per TEU on Europe lanes. High-value cargo owners then pay for air freight, inadvertently lifting aggregate carbon output when the weight is low relative to the value. Ammonia-ready new-builds lag behind bunker infrastructure, so carriers buy offsets in the interim at volatile ETS prices that complicate long-term service contracts. Smaller forwarders lack in-house carbon calculators and must rely on carrier data, making it hard to offer transparent quotes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Retail Ascendancy Reshapes Network Design

Wholesale and Retail Trade held 42.26% of the Japan freight and logistics market size in 2025 as e-commerce and omnichannel services increased shipment frequency and reduced average order size. The same segment is forecast to register a 3.86% CAGR, supported by fresh-food delivery that requires multi-temperature fleets and by loyalty-program free-return offers that double reverse-logistics volumes. Manufacturing, while large, is consolidating plants and deploying vendor-managed inventory, which tempers its relative share. Construction project cargo lifts demand for specialized trailers that move tunnel-boring machines, and pharmaceuticals boost GDP-compliant courier services that guarantee end-to-end visibility.

Retail growth forces network redesign away from single national DCs toward micro-fulfillment centers located within 10 km of urban households. Parcel lockers inside convenience stores reduce failed deliveries and trim last-mile emissions. Cross-docking remains dominant for fashion items that must reach stores within 24 hours to match fast-cycle promotions. As retailers blend online and in-store sales, they contract 3PLs that can merge inbound vendor freight with store replenishment and customer returns in a shared truck, cutting half-empty backhauls.

By Logistics Function: CEP Momentum Challenges Transport Dominance

Freight Transport controlled 70.85% of the Japan freight and logistics market share in 2025 due to automotive and machinery exports that need full-truck-load and container services. Yet Courier, Express, and Parcel volumes are rising at a 4.15% CAGR as small cross-border packages from Korea, China, and ASEAN flood gateways. CEP operators invest in optical sorters that process 20,000 parcels per hour, responding to flash-sale peaks that can triple daily volume.

Shippers now bundle CEP with freight forwarding so that a single provider manages inbound components and outbound consumer orders. Warehousing contracts increasingly include value-added kitting tasks such as packaging smartphone accessories with instruction leaflets, reducing touches at retailer sites. Other Services like supply-chain consulting grow as companies outsource planning to providers with AI route-optimization software.

By Freight Transport Mode: Air Gains Despite Road’s Lead

Road kept 80.85% of domestic values in 2025 because trucks offer door-to-door reach across Japan’s mountainous terrain. Driver shortages and toll hikes, however, raise costs and open a 4.10% CAGR opportunity for Air freight that serves semiconductor and biologic loads needing sub-24-hour transit. Maglev freight promises further share gains once commercial slots open in 2028.

Rail volume rises on eco-subsidies, with temperature-controlled wagons hauling strawberries from Hokkaido to Tokyo overnight while using 70% less CO₂ than trucks. Coastal feeders carry auto parts between Kyushu and Chubu plants, avoiding highway congestion and overtime constraints. Pipeline remains marginal yet stable, moving refinery output to industrial clusters.

By Courier, Express, and Parcel: International Segment Outpaces Domestic Growth

Domestic CEP, led by Yamato and Japan Post, managed 64.05% of parcels in 2025 through dense networks that reach every postal code. International CEP shows a 4.29% CAGR because Japanese consumers buy USD 25 billion in cross-border goods each year, and overseas shoppers order niche cosmetics directly from Tokyo boutiques. Customs pre-clearance APIs cut dwell times at Narita from 18 hours to under six, enabling next-day delivery to Seoul or Shanghai.

Domestic growth focuses on chilled parcels for meal-kit subscriptions that need 2-5 °C control. Locker networks inside train stations relieve last-mile stress during driver overtime caps. International operators add bonded mini-hubs inside airports so they can break bulk and inject final-mile parcels straight into domestic networks.

By Freight Forwarding Mode: Air Specialization Captures Premium Cargo

Sea and Inland Waterways held 56.20% forwarding share in 2025, benefiting from Japan’s export orientation and cost advantage for containers. Air forwarding, growing 3.67% CAGR, wins high-value loads whose unit price makes transport cost negligible. Forwarders charter freighters during peak chip demand, guaranteeing space that belly cargo cannot provide.

Multimodal services combine rail from Kyushu plants to Osaka Port, then ocean to Los Angeles, shaving one day off transit versus truck-ocean chains. Digitally native forwarders offer instant rate quotes with carbon footprints, meeting procurement rules that now score vendors on emissions as well as price.

By Warehousing and Storage: Temperature Control Commands Premium Positioning

Non-Temperature-Controlled facilities covered 92.01% of capacity in 2025, serving apparel, electronics, and machinery. Yet Temperature-Controlled space is climbing at 3.46% CAGR as vaccine and meal-kit volumes expand. Developers install multi-zone cooling so a single building can host frozen, chilled, and ambient goods, maximizing utilization.

Automated stacker-cranes cut labor costs where workers must wear heavy coats, and IoT sensors feed dashboards that alert operators to deviations within one-degree thresholds. Energy intensity is offset by rooftop solar and phase-change insulation, helping warehouses meet 2030 carbon targets. Pharmaceutical tenants sign leases up to 15 years, giving landlords stable income to justify higher upfront build costs[4]Prologis, “Multi-Temperature Warehouse Design,” prologis.com .

Geography Analysis

Tokyo’s metropolitan area anchors roughly two-thirds of national logistics value, leveraging Narita and Haneda airports plus contiguous highways that feed 38 million consumers. Road congestion and high rents, however, push distribution centers 40-60 km outward along the Ken-O Expressway, where land is cheaper, and trailers avoid downtown tolls. Kansai, centered on Osaka and Kobe, forms the secondary hub with container throughput that serves western Japan and provides redundancy when typhoons disrupt Kanto ports.

Chubu, around Nagoya, thrives on automotive exports; OEMs cluster suppliers within a 50 km radius, which limits stock levels and drives shuttle truck frequency. Kyushu is now the fastest-growing sub-region thanks to semiconductor fabs that require cleanroom logistics and high-security bonding stores. Government grants pay half the cost of cold warehouses in Hokkaido that funnel dairy and seafood southward, improving farmer margins.

Okinawa relies on air for perishables and e-commerce imports because ocean options are slow and infrequent. New integrated ferry-rail services in Shikoku aim to counter population decline by linking coastal factories to mainland buyers. Disaster-resilient warehouses in Tohoku use seismic isolation and dual-feed power to win tenants concerned about future quakes, setting a design template likely to spread nationwide.

Competitive Landscape

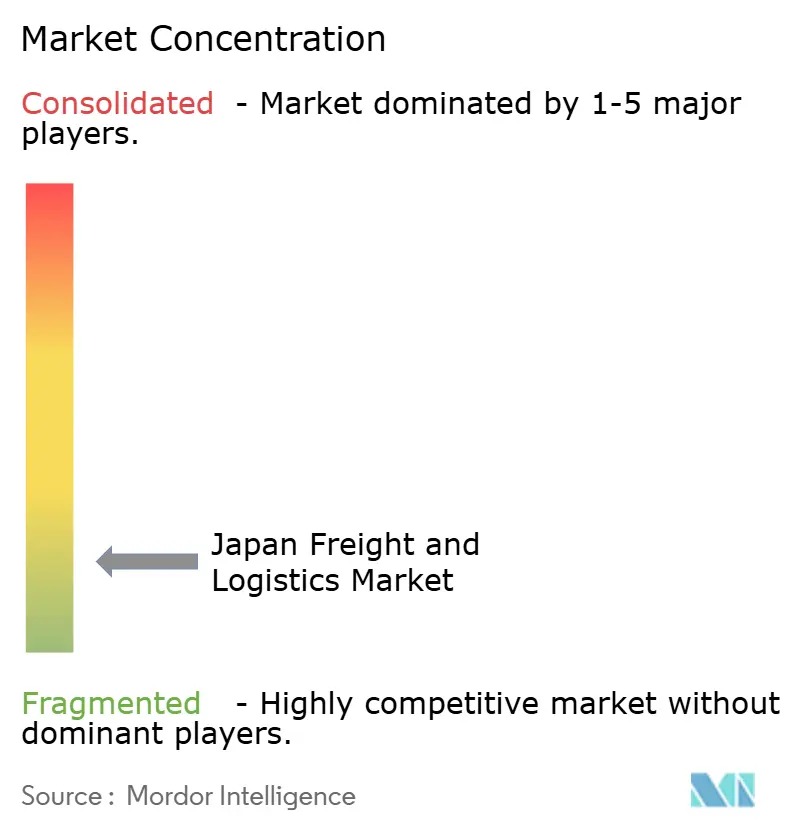

Nippon Express, Yamato, and SG Holdings together control a minor share of domestic revenue, giving the Japan freight and logistics market a fragmented landscape. Their nationwide terminals, proprietary IT, and long contracts with blue-chip shippers form high switching barriers. International integrators like DHL and FedEx specialize in cross-border express and value-added warehousing, where global networks are essential.

Digital capabilities now separate leaders from laggards. Nippon Express uses digital twins to predict lane congestion and to reroute trucks before bottlenecks form. Yamato pilots autonomous sorters that raise parcel throughput by one-third without adding headcount. SG Holdings embeds blockchain in defense shipments, generating immutable audit trails that satisfy security ministries.

Consolidation is likely as regional carriers struggle with DX compliance costs and aging drivers. Large 3PLs buy smaller firms to add rural coverage and driver pools. Joint ventures between Japanese incumbents and global tech firms accelerate warehouse robotics and hydrogen truck trials, creating ecosystems difficult for new entrants to replicate.

Japan Freight And Logistics Industry Leaders

Nippon Express Holdings

SG Holdings Co., Ltd.

Yamato Transport Co., Ltd.

Japan Post Holdings Co., Ltd.

Kuehne+Nagel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Nippon Express acquired a minority stake in TCS Logistics to strengthen connectivity in Central Asia and enhance end-to-end supply chain capabilities. The company gains a foothold in Central Asia to connect Japanese manufacturers shipping electronics, auto parts, and precision machinery to Eurasian markets.

- May 2025: DHL Express launched Japan's first use of locally produced SAF on international cargo flights from Central Japan International Airport. This positions DHL as a sustainability leader in Japan's freight market, meeting emission regulations while ensuring reliable air cargo for high-value exports.

- March 2025: Kuhene+Nagel Expanded sustainable logistics services in Asia-Pacific, including: Electric trucks, Carbon-neutral ocean freight, Infrastructure partnerships for EV logistics.

- March 2025: DHL absorbed Packfleet’s operations, customer base, and electric delivery fleet to strengthen its sustainable last-mile logistics capabilities, particularly in urban markets.

Japan Freight And Logistics Market Report Scope

End User Industry

| Agriculture, Fishing, and Forestry |

| Construction |

| Manufacturing |

| Oil and Gas, Mining and Quarrying |

| Wholesale and Retail Trade |

| Others |

Logistics Function

| Courier, Express, and Parcel (CEP) | By Destination Type | Domestic |

| International | ||

| Freight Forwarding | By Mode of Transport | Air |

| Sea and Inland Waterways | ||

| Others | ||

| Freight Transport | By Mode of Transport | Air |

| Pipelines | ||

| Rail | ||

| Road | ||

| Sea and Inland Waterways | ||

| Warehousing and Storage | By Temperature Control | Non-Temperature Controlled |

| Temperature Controlled | ||

| Other Services | ||

| End User Industry | Agriculture, Fishing, and Forestry | ||

| Construction | |||

| Manufacturing | |||

| Oil and Gas, Mining and Quarrying | |||

| Wholesale and Retail Trade | |||

| Others | |||

| Logistics Function | Courier, Express, and Parcel (CEP) | By Destination Type | Domestic |

| International | |||

| Freight Forwarding | By Mode of Transport | Air | |

| Sea and Inland Waterways | |||

| Others | |||

| Freight Transport | By Mode of Transport | Air | |

| Pipelines | |||

| Rail | |||

| Road | |||

| Sea and Inland Waterways | |||

| Warehousing and Storage | By Temperature Control | Non-Temperature Controlled | |

| Temperature Controlled | |||

| Other Services | |||

Market Definition

- Agriculture, Fishing, and Forestry (AFF) - This end user industry segment captures the external (outsourced) logistics expenditure incurred by the AFF industry players. The end user players considered are the establishments primarily engaged in growing crops, raising animals, harvesting timber, harvesting fish & other animals from their natural habitats and providing related support activities. Herein, Logistics Service Providers (LSPs) play a crucial role in acquisition, storage, handling, transportation, and distribution activities for the optimal & continuous flow of inputs (seeds, pesticides, fertilizers, equipment, and water) from manufacturers or suppliers to the producers and smooth flow of output (produce, agro-goods) to distributors/ consumers. This includes both termperature controlled and non-temperature controlled logistics, as and when required according to the shelf life of goods being transported or stored.

- Construction - This end user industry segment captures the external (outsourced) logistics expenditure incurred by the construction industry players. The end user players considered are the establishments primarily engaged in constructing, repairing and renovating residential & commercial buildings, infrastructure, engineering works, subdividing and developing land. Logistics Service Providers (LSPs) play a crucial role in increasing profitability of construction projects by maintaing the inventory of raw materials & equipment, time-critical supplies and by providing other value added services for effective project management.

- Courier, Express, and Parcel - The Courier, Express, and Parcel services, often called as CEP Market, refers to the logistics and postal service providers which specialize in moving small goods (parcels/packages). It captures the overall market size (USD) and market volume (number of parcels) of (1) the shipments/parcels/packages which are under 70kgs/ 154lbs weight, (2) Business Customer packages viz. Business-to-Business (B2B) & Business-to-Consumer (B2C) as well as private customer packages (C2C), (3) non-express parcel delivery services (Standard and Deferred) as well as express parcel delivery services (Day-Definite-Express and Time-Definite-Express), (4) domestic as well as international parcels.

- Demographics - To analyse total addressable market demand, population growth & forecasts have been studied and presented in this industry trend. It represents population distribution across categories like gender (male/female), development area (urban/rural), major cities among other key parameters like population density and final consumption expenditure (growth and share % of GDP). This data has been used for assessing the fluctations in demand & consumption expenditure, and the major hotspots (cities) of potential demand.

- Export Trends and Import Trends - Overall logistics performance of an economy is positively and significantly (statistically) correlated to its trade performance (exports and imports). Hence, in this industry trend, total value of trade, major commodities/ commodity groups and the major trade partners, for the studied geography (country or region as per the scope of report) have been analysed alongside the impact of major trade/logistics infrastructure investments & regulatory environment.

- Freight Forwarding - Freight forwarding which herein refers to the freight transportation arrangement (FTA) industry includes establishments primarily engaged in arranging & tracking transportation of freight between shippers and carriers. Logistics Service Providers (LSPs) considered are freight forwarders, NVOCCs, custom brokers and marine shipping agents. Others segment under Freight Forwarding captures the revenue earned through value added services of FTA like custom brokerage/clearance activities, preparation of freight related documentation, consolidation-deconsolidation of goods, cargo insurance & compliance, arrangement of warehousing & storage, liasing with shippers, and freight forwarding through other modes of transport viz. road and rail.

- Freight Pricing Trends - Freight pricing by mode of transport (USD/tonkm), over the review period, has been presented in this industry trend. The data has been used in assessing the inflationary environment, impact on trade, freight turnover (tonkm), freight and logistics market demand by mode of transport segments and hence the overall freight and logistics market size.

- Freight Tonnage Trends - Freight tonnage (weight of goods in tons) handled by mode of transport, over the review period, has been presented in this industry trend. The data has been used as one of the parameters apart from average distance per shipment (km), freight volume (tonkm), and freight pricing (USD/tonkm) to assess the freight transport market size.

- Freight Transport - Freight Transport refers to the hiring of a logistics service provider (outsourced logistics) for the transport of commodities (raw materials/final/intermediate/finished goods including both solids and fluids) from the origin to a destination within the country (domestic) or cross-border (international).

- Freight and Logistics - External expenditure on (or outsourced) facilitation of freight transport (freight transportation), arrangement of freight transport through an agent (freight forwarding), warehousing and storage (temperature controlled or non-temperature controlled), CEP (domestic or international courier, express and parcel) and other value-added logistics services involved in the transportation of commodities (raw materials or finished goods including both solids and fluids) from the origin to a destination within the country (domestic) or cross-border (international), through one or more modes of transportation viz. road, rail, sea, air and pipelines constitute freight and logistics market.

- Fuel Price - Fuel price spikes can cause delays and diruption for logistics service providers (LSPs), while drops in the same can result in higher short-term profitability and increased market rivalry to offer consumers with the best deals. Hence, the fuel price variations have been studied over the review period and presented along with the causes as well as market impacts.

- GDP Distribution by Economic Activity - Nominal Gross Domestic Product and distribution of the same, across major economic sectors in the geography studied (country or region as per scope of the report) have been studied and presented in this industry trend. As GDP is positively related to the profitability and growth of logistics industry, this data has been used in adjunction to the input-output tables/ supply-use tables for analyzing the potential major contributing sectors towards the logistics demand.

- GDP Growth by Economic Activity - Growth of Nominal Gross Domestic Product across major economic sectors, for the geography studied (country or region as per scope of the report) have been presented in this industry trend. This data has been utilized for assessing the growth of logistics demand from all the market end users (economic sectors considered here).

- Inflation - Variations in both Wholesale Price Inflation (YoY change in producer price index) and Consumer Price Inflation have been presented in this industry trend. This data has been used to assess the inflationary environment as it plays a vital role in smooth functioning of the supply chain, directly impacting the logistics operational cost components e.g., pricing of tyres, driver wages & benefits, energy/fuel prices, maintenace costs, toll charges, warehousing rents, custom brokerage, forwarding rates, courier rates etc. hence impacting the overall freight and logistics market.

- Infrastructure - As infrastructure plays a vital role in an economy's logistics performance, variables like length of roads, distribution of road length by surface category (paved v/s unpaved), distribution of road length by road classification (expressways v/s highways v/s other roads), rail length, volume of containers handled by major ports and tonnage handled by major airports have been analysed and presented in this industry trend.

- Key Industry Trends - The report section named "Key Industry Trends" include all the key variables/parameters studied to better analyze the market size estimates and forecasts. All the trends have been presented in the form of data points (time series or latest available data points) along with analysis of the paramter in the form of concise market relevant commentary, for the geography studied (country or region as per the scope of report).

- Key Strategic Moves - The action taken by a company to differentiate from its competitor or used as a general strategy is referred to as a key strategic move (KSM). This includes (1) Agreements (2) Expansions (3) Financial Restructuring (4) Mergers and Acquisitions (5) Partnerships, and (6) Product Innovations. Key players (Logistics Service Providers, LSPs) in the market have been shortlisted, their KSM have been studied and presented in this section.

- Liner Shipping Bilateral Connectivity Index - It indicates a country pair's integration level into global liner shipping networks and plays a crucial role in determining bilateral trade, which in turn potentially contributes toward the prosperity of a country and its surrounding region. Hence the major economies connected to the country/ region as per scope of the report, have been analyzed and presented in "Liner Shipping Connectivity" industry trend.

- Liner Shipping Connectivity - This industry trend analyses the state of connectivity to the global shipping networks based on the status of maritime transport sector. It includes the analysis of liner shipping connectivity, bilateral shipping connectivity, and port liner shipping connectivity indices for the geography (country/ region as per scope of the report) over the review period.

- Liner Shipping Connectivity Index - It indicates how well countries are connected to global shipping networks based on the status of their maritime transport sector. It is based on five components of the maritime transport sector: (1) The number of shipping lines servicing a country, (2) The size of the largest vessel used on these services (in TEUs), (3) The number of services connecting a country to the other countries, (4) The total number of vessels deployed in a country, (5) The total capacity of those vessels (in TEUs).

- Logistics Performance - Logistics Performance and Logistics Costs are the backbone of trade, and influences trade costs, making countries compete globally. Logistics performance is influenced by market wide adopted supply chain management strategies, government services, investments & policies, fuel/ energy costs, inflationary environment etc. Hence, in this industry trend, the logistics performance of the geography studied (country/ region as per the scope of report) has been analysed and presented over the review period.

- Major Truck Suppliers - Market share of truck brands is influenced by factors like geographical preferences, portfolio of truck types, truck prices, local production, truck repair & maintenance service peneteration, customer support, technological innovations (like electric vehicles, digitalization, autonomous trucks), fuel efficiency, financing options, annual maintenance costs, availability of substitutes, marketing startegies etc. Hence, the distribution (share % for base year of the study) of truck sales volume for leading truck brands and commentary on current market scenario & market anticipation over the forecast period have been presented in this industry trend.

- Manufacturing - This end user industry segment captures the external (outsourced) logistics expenditure incurred by the Manufacturing industry players. The end user players considered are the establishments primarily engaged in the chemical, mechanical or physical transformation of materials or substances into new products. Logistics Service Providers (LSPs) play a crucial role in maintaining a smooth flow of raw materials across the supply chain, enabling timely delivery of finished goods to distributors or end customers and storing & supplying the raw materials to clients for just-in-time manufacturing.

- Maritime Fleet Load Carrying Capacity - Maritime fleet load carrying capacity depicts the development state of an economy's maritime infrastructure & trade. It is influenced by factors like volume of production, international trade, major end user industries, maritime connectivity, environmental regulations, investments in port infrastructure development, port container cargo handling capacity etc. This industry trend represents the maritime fleet load carrying capacity by type of ship viz. container ships, oil tankers, bulk carriers, general cargo, among other types alongwith the influencing factors for the geography studied (country/ region as per scope of the report), over the review period.

- Modal Share - Freight Modal Share is influenced by factors like modal productivity, government regulations, containerization, distance of shipment, temperature control requirements, type of goods, international trade, terrain, speed of delivery, shipment weight, bulk shipments, etc. Also, modal share by tonnage (tons) and modal share by freight turnover (ton-km) differ as per average distance of shipments, weight of major commodity groups transported in the economy and number of trips. This industry trend represents the distribution of freight transported by mode of transport (tons as well as ton-km), for the study base year.

- Oil and Gas, Mining and Quarrying - This end user industry segment captures the external (outsourced) logistics expenditure incurred by the extraction industry players. The end user players considered are the establishments that extract naturally occurring mineral solids, such as coal and ores; liquid minerals, such as crude petroleum; and gases, such as natural gas. Logistics Service Providers (LSPs) covers entire phases from upstream to downstream and plays a crucial role in the transportation of machinery, drilling equipments, extracted minerals, crude oil & natural gas and refined/ processed products from one place to another.

- Other End Users - Other end user segment captures the external (outsourced) logistics expenditure incurred by the financial services (BFSI), real estate, educational services, healthcare, and professional services (administrative, waste management, legal, architectural, engineering, design, consulting, scientific R&D). Logistics Service Providers (LSPs) plays a crucial role in the reliable movement of supplies and documents to/from these industries such as transporting any equipment or resources required, shipping confidential documents and files, movement of medical goods & supplies (surgical supplies and instruments, including gloves, masks, syringes, equipment) to name a few.

- Other Services - Other Services segment captures revenue earned through (1) Value added services (VAS) for freight transportation by road, rail, air and sea & inland waterways, (2) VAS for marine cargo transportation (operation of terminal facilities such as harbours and piers, operation of waterway locks, navigation, pilotage and berthing activities, lighterage, salvage activities, lighthouse activities, among other miscellaneous support activities), (3) VAS for land freight transportation (operation of terminal facilities such as railway stations, stations for the handling of goods, operation of railroad infrastructure, switching and shunting, towing and road side assistance, liquefaction of gas for transportation purposes, among other miscellaneous support activities), (4) VAS for air cargo transportation (operation of terminal facilities such as airway terminals, airport and air-traffic-control activities, ground service activities on airfields, runway maintenance, inspection/ ferrying/ maintenance/ testing of aircrafts, aircraft fuelling services, among other miscellaneous support activities), (5) VAS for warehousing and storage service (operation of grain silos, general merchandise warehouses, refrigerated warehouses, storage tanks etc., storage of goods in foreign trade zones, blast freezing, crating goods for shipping, packing and preparing goods for shipping, labelling and/or imprinting the package, kit assembling and packaging services, among other miscellaneous support activities), and (6) VAS for courier, express and parcel service (pickup, sorting).

- Port Calls and Performance - The performance of ports is key to an economy's freight movement, trade, global connectivity, successful growth strategies, investment attractiveness for production & distribution systems, and thus affects GDP, employment, per capita income and industrial growth. Hence, the port perfomance parameters like median time spent by vessels in the ports; average age, size, cargo carrying capacity, container carrying capacity, of vessels entering the ports, port calls, and container port throughput have been analysed and presented in this industry trend.

- Port Liner Shipping Connectivity Index - It reflects a port's position in the global liner shipping network, wherein a higher value of index is associated with better connectivity. Efficient and well-connected ports (1) contribute towards minimizing transport costs, linking supply chains and supporting international trade, (2) pave the way for economies of scale and development of expertise by permitting producers to better exploit possibilities in domestic as well as foreign markets. Hence the major ports of strategic importance, in the country/ region as per scope of the report, have been analyzed and presented in "Liner Shipping Connectivity" industry trend.

- Port Throughput - It reflects the amount of cargo or number of vessels a port handles annually. It can be related to (1) cargo tonnage, (2) container TEU, and (3) vessel calls. Port throughput in terms of total containers handled (TEU's), has been presented in the "Port Calls and Performance" industry trend.

- Producer Price Inflation - It indicates inflation from viewpoint of the producers viz. the average selling price received for their output over a period of time. Annual change (YoY) of producer price index is reported as wholesale price inflation in the "Inflation" industry trend. As WPI captures dynamic price movements in most comprehensive way, it is widely used by governments, banks, industry, business circles and is deemed important in formulation of trade, fiscal and other economic policies. The data has been used in adjunction to consumer price inflation for better understanding the inflationary environment.

- Segmental Revenue - Segmental Revenue has been triangulated or computed and presented for all the major players in the market. It refers to the freight and logistics market specific revenue earned by the company, over the base year of study, in the geography studied (country or region as per the scope of report). It is computed through the study and analysis of major parameters like financials, service portfolio, employee strength, fleet size, investments, number of countries present in, major economies of concern, etc. that have been reported by the company in its annual reports, webpage. For companies having scarce financial disclosures, paid databases like D&B Hoovers, Dow Jones Factiva have been resorted to and verified through industry/expert interactions.

- Transport and Storage Sector GDP - Value and growth of Transport and Storage Sector GDP has a direct relation to the freight and logistics market size. Hence, this variable has been studied and presented over the review period, in value terms (USD) and as share % of total GDP, in this industry trend. The data has been supported by concise and relevant commentary around the investments, developments, and current market scenario.

- Trends in E-Commerce Industry - Enhanced internet connectivity and boom in smartphone penetration, coupled with increasing disposable incomes, has led to a phenomenal growth in the e-commerce market globally. Online shoppers require fast and efficient delivery of their orders leading to an increase in the demand for logistics services especially e-commerce fulfilment services. Hence, the Gross Merchandise Value (GMV), historial and projected growth, breakup of major commodity groups in e-commerce industry for the studied geography (country or region as per scope of the report) have been analysed and presented in this industry trend.

- Trends in Manufacturing Industry - Manufacturing industry involves the transformation of raw materials into finished products, while logistics industry ensures the efficient flow of raw materials to the factory, and the transport of manufactured products to the distributors & consumers. Demand-Supply of both industries are highly cross-linked and critical for a seamless supply chain. Hence, the Gross Value Added (GVA), breakup of GVA into major manufacturing sectors, and growth of manufacturing industry over the review period have been analysed and presented, in this industry trend.

- Trucking Fleet Size By Type - Market share of truck types is influenced by factors like geographical preferences, major end user industries, truck prices, local production, truck repair & maintenance service peneteration, customer support, technological disruptions (like electric vehicles, digitalization, autonomous trucks) etc. Hence, the distribution (share % for base year of study) of truck parc volume by type of truck, market disruptors, truck manufacturing investments, truck specifications, truck use & import regulations, and market anticipation over the forecast period have been presented in this industry trend.

- Trucking Operational Costs - The prime reasons for measuring/ benchmarking logistics performance of any trucking company are to reduce operational costs and increase profitability. On the other hand, measuring operational costs helps to identify whether and where to make operational changes to control expenses and identify areas for improved performance. Hence, in this industry trend, trucking operational costs and the variables involved viz. driver wages & benefits, fuel prices, repairs & maintenance costs, tyre costs etc. have been studied over the base year of study, and presented for the geography studied (country or region as per the scope of report).

- Warehousing and Storage - Warehousing and storage segment captures revenue earned through the operation of general merchandise, refrigerated and other types of warehousing & storage facilities. These establishments take responsibility for storing the goods and keeping them secure in lieu of charges. Value added services (VAS) they may provide are considered to be a part of the "other services" segment. Here VAS refer to a range of services, related to the distribution of a customer's goods and can include labelling, breaking bulk, inventory control & management, light assembly, order entry & fulfillment, packaging, pick & pack, price marking & ticketing and transportation arrangement.

- Wholesale and Retail Trade - This end user industry segment captures the external (outsourced) logistics expenditure incurred by the wholesalers and retailers. The end user players considered are the establishments primarily engaged in wholesaling or retailing merchandise, generally without transformation, and rendering services incidental to the sale of merchandise. Logistics Service Providers (LSPs) plays a crucial role in the reliable movement of supplies to and finished products from production houses to the distributors and finally to the end customer covering activites like material sourcing, transportation, order fulfillment, warehousing & storage, demand forecasting, inventory management etc.

| Keyword | Definition |

|---|---|

| Axle Load | The axle load of a wheeled vehicle is the total weight bearing on the roadway for all wheels connected to a given axle. |

| Back Haul | Backhaul is the return movement of a transport vehicle from its original destination to its original point of departure. |

| Bill of Lading | A bill of lading is a legal document issued by a carrier to a shipper that details the type, quantity, and destination of the goods being carried. |

| Bunkering | Bunkering is the process of supplying fuel and/or gasoil to be used to power the propulsion system of a ship (such fuel is referred to as bunker). It includes the logistics of loading and distributing the fuel among available shipboard tanks. A person dealing in trade of bunker (fuel) is called a bunker trader. |

| Bunkering Service | Bunkering service is the supply of a requested quality and quantity of bunkers to a ship. |

| C-commerce | C-commerce (Collaborative commerce) describes electronically enabled business interactions among an enterprise’s internal personnel, business partners and customers throughout a trading community. The trading community could be an industry, industry segment, supply chain or supply chain segment. |

| Cabotage | Transport by a vehicle registered in a country performed on the national territory of another country. |

| Cartage Agent | A ground transportation service that provides pickup and delivery of freight in locations not served directly by an air or ocean carrier. |

| Contract logistics | Contract logistics refers to the outsourcing of resource management tasks by one company to a third-party company specializing in logistical matters, such as transportation, warehousing, and order fulfillment. |

| Courier | A business that is used to send messages, packages, etc. Courier service refers to the fast or quick, door to door pickup and delivery service for goods or documents. It can be local or international. A company that provides such delivery services is called a courier company. A courier company hires people to provide their services. Such a person hired by the courier service company is called a courier. |

| Cross docking | Cross docking is a practice in logistics management that includes unloading incoming delivery vehicles and loading the materials directly into outbound delivery vehicles, omitting traditional warehouse logistical practices and saving time and money. |

| Cross Trade | International transport between two different countries performed by a vehicle registered in a third country. A third country is a country other than the country of loading/embarkation and than the country of unloading/disembarkation. |

| Customs Clearance | The procedures involved in getting cargo released by Customs through designated formalities such as presenting import license/permit, payment of import duties and other required documentations by the nature of the cargo such as FCC or FDA approval. |

| Customs seal | Customs seal means a seal, stamp or any other preventive means affixed by customs officials to ensure the inviolability of goods, commercial means of transport or warehouses. |

| Dangerous Goods | Dangerous goods (or hazardous materials or HAZMAT) include flammable liquids/solids, gases, compressed, liquified, dissolved under pressure, corrosives, oxidising substances, explosive substances and articles, substances, which on contact with water, emit flammable gasses, organic peroxides, toxic substances, infectious substances, radioactive materials, miscellaneous dangerous goods and articles. |

| Direct Shipment | Direct shipment is a method of delivering goods from the supplier or the product owner to the customer directly. In most cases, the customer orders the goods from the product owner. This delivery scheme reduces transportation and storage costs, but requires additional planning and administration. |

| Drayage | A drayage is a form of trucking service that connects the different modes of shipping (intermodal), such as ocean freight or air freight. It’s a short-haul trip that transports goods from one place to another, usually before or after its long-haul shipping process. Drayage trucks move cargo to and from various destinations, such as container ships, storage lots, order fulfillment warehouses, and rail yards. Typically, drayage only transports goods in short distances and operates only in one metropolitan area. It also requires only one trucker in a single shift. |

| Dry Docking | Dry docking is a term used for repairs or when a ship is taken to the service yard. During dry docking, the whole ship is brought to a dry land so that the submerged portions of the hull can be cleaned or inspected. |

| Dry van | A dry van is a type of semi-trailer that's fully enclosed to protect shipments from outside elements. Designed to carry palletized, boxed or loose freight, dry vans aren't temperature-controlled (unlike refrigerated “reefer” units) and can't carry oversized shipments (unlike flatbed trailers). |

| Feedering | Transport service whereby loaded or empty containers in a regional are transferred to a “mother ship” for a long-haul ocean voyage. |

| Final Demand | Final demand includes all types of commodities (goods as well as services) consumed as final use and might include personal consumption, or consumption by government, by businesses as capital investment, and as exports. includes all types of commodities (goods as well as services) consumed as final use and might include personal consumption, or consumption by government, by businesses as capital investment, and as exports. |

| First mile Delivery | First mile delivery refers to the first stage of the transportation. This is when the parcel leaves the seller’s warehouse and is taken by the courier pick up agent to process it or take it to the warehouse. Once the package reaches the post office or the courier’s hub, it is then sorted and transported further until it reaches the customer’s doorstep. |

| Fiscal storage services | It means a facility, clearly separated from other premises, where the excise goods are produced, processed, held, received or dispatched under a duty suspension arrangement by an authorized depositor, in the course of his business, under conditions laid down by the customs authorities. |

| Flat Bed | It has a back body that is flatly shaped for easy loading and unloading of goods. The flatbed truck is mostly used to transport heavy, oversized, wide and indelicate goods. |

| Flatbed Truck | A flatbed truck is a type of truck with rigid design. It has a back body that is flatly shaped for easy loading and unloading of goods. The flatbed truck is mostly used to transport heavy, oversized, wide and indelicate goods such as machinery, building supplies or equipment. Due to the truck open body, the goods transported with it must not be vulnerable to rain. By functionality, the flatbed truck is comparable to a flatbed trailer. |

| Freight Transit Time | Transit time is how long it takes for a shipment to be delivered to its final destination after being picked up from a designated pick up point. |

| Halal Logistics | It refers to the process of managing the logistics operations such as fleet management, storage/warehousing, and materials handling according to the principles of Shariah law in ensuring the integrity of the halal products at the point of consumption. |

| Haulage | The commercial transport of goods. |

| Inbound Logistics | Inbound logistics is the way materials and other goods are brought into a company. This process includes the steps to order, receive, store, transport and manage incoming supplies. Inbound logistics focuses on the supply part of the supply-demand equation. |

| Intermediate Demand | Intermediate demand includes goods, services, and maintenance and repair construction sold to businesses, excluding capital investment. |

| International Loaded | Place of loading of goods in reporting country (i.e., country in which the vehicle performing the transport is registered) and place of unloading in a different country. |

| International Unloaded | Place of unloading of goods in reporting country (i.e., country in which the vehicle performing the transport is registered) and place of loading in a different country. |

| Last Mile Delivery | Last mile delivery refers to the very last step of the delivery process when a parcel is moved from a transportation hub to its final destination—which, usually, is a personal residence or retail store. |

| Less than-Truck-Load (LTL) | Less-than-truckload, also known as less-than-load (LTL), is a shipping service for relatively small loads or quantities of freight. An LTL provider combines the loads and shipping requirements of several different companies on their trucks, using a hub-and-spoke system to get goods to their destinations. |

| Locomotives Haluage | The transport of coal, ore, workers, and materials underground by means of locomotive-hauled mine cars. The locomotive may be powered by battery, diesel, compressed air, trolley, or some combination such as battery-trolley or trolley-cable reel. |

| Milkrun | A Milk Run is a delivery method used to transport mixed loads from various suppliers to one customer. Instead of each supplier sending a truck every week to meet the needs of one customer, one truck (or vehicle) visits the suppliers to pick up the loads for that customer. This method of transport got its name from the dairy industry practice, where one tanker used to collect milk from several dairy farms for delivery to a milk processing company. |

| Multi country consolidation | Multi-Country Consolidation (MCC) is a cost-effective solution that consolidates ones cargo from different countries of origin to build Full Container Loads (FCL). MCC is most suitable for companies that import light volumes of goods from multiple countries but want to take advantage of the more economic FCL freight rates. |

| Multi-Modal Logistics | Multimodal transportation or multimodal shipping refers to logistics and freight processes that require multiple modes of transportation. |

| Omni Channel Logistics | Omnichannel distribution is a multichannel approach taken by companies to give customers a way to purchase and receive orders from several sales channels with one-touch seamless integration. Some of the ways include- 1. Buy online, then pick-up at the brick and mortar store; 2. Buy online, then have it delivered to the home or another location; 3.In store purchase, with the delivery either to the home or another location; 4. Drop ship from a warehouse or manufacturing center to store, home or other location; 5.Buy online, then return at store or online; 6. Buy online, then return online. |

| OOG cargo | Out of Gauge (OOG) cargo is any cargo that can not be loaded into six-sided shipping containers simply because it is too large. The term is a very loose classification of all cargo with dimensions beyond the maximum 40HC container dimensions. That is a length beyond 12.05 meters – a width beyond 2.33 meters – or a height beyond 2.59 meters. |

| Other ships | Other ships include: Liquefied petroleum gas carriers, liquefied natural gas carriers, parcel (chemical) tankers, specialized tankers, reefers, offshore supply vessels, tugboats, dredgers, cruise, ferries, other non-cargo ships |

| Other Specialised Cargo | Other specialised goods include pre-slung goods (Goods, one or more items, supplied with a sling or slings), mobile units (Mobile Self Propelled Units, Non Self Propelled Units, unrolled vehicles), oversized equipment load (light and heavy machinery that is often too big or too heavy), high value freight that needs extra protection like electronics, financial services road freight. |

| Outsourced Freight Transport | Transport for hire or reward; The carriage for remuneration of goods. |

| Pallets | Raised platform, intended to facilitate the lifting and stacking of goods. |

| Part load | A part load describes goods which only fills a truck partially. In essence, the quantity of the shipment is bigger than the Less Than Truckload (LTL) shipment. Also, the shipment cannot fully occupy a truck i.e. its capacity is much lower than a Full Truckload (FTL) shipment. |

| Paved Road | Road surfaced with crushed stone (macadam) with hydrocarbon binder or bituminized agents, with concrete or with cobblestone. |

| Q-commerce | Q-commerce, also referred to as quick commerce, is a type of e-commerce where emphasis is on quick deliveries, typically in less than an hour. |

| Quay | A stone or metal platform lying alongside or projecting into water for loading and unloading ships. |

| Recommerce | Recommerce is the selling of previously owned items through online marketplaces to buyers who reuse, recycle or resell them. |

| ReverseLogistics | Reverse logistics is a type of supply chain management that moves goods from customers back to the sellers or manufacturers. |

| Road Freight Transport Service | Hiring a trucking agency for transport of commodities (raw materials or manufactured goods including both solids and liquids) form the origin to a destination within the country (domestic) or cross-border (international) constitutes road freight transport market. The service might be Full-Truck-Load or Less than-Truck-Load, containerized or non-containerized, temperature controlled or non temperature controlled, short haul or long haul. |

| Roll-on/roll-off cargo | Roll-on/roll-off (RORO or ro-ro) ships are cargo ships designed to carry wheeled cargo, such as cars, motorcycles, trucks, semi-trailer trucks, buses, trailers, and railroad cars, that are driven on and off the ship on their own wheels or using a platform vehicle, such as a self-propelled modular transporter. |

| Swap bodies | A swap body, swop body, exchangeable container or interchangeable unit, is one of the types of standard freight containers for road and rail transport. |

| Tank Barge | A non-self-propelled vessel constructed or adapted primarily to carry liquid, solid or gaseous commodities or cargos in bulk in cargo spaces (or tanks) through rivers and inland waterways, and may occasionally carry commodities or cargos through oceans and seas when in transit from one inland waterway to another. The commodities or cargos transported are in direct contact with the tank interior. |

| Tautliner vehicle | Tautliner and curtainsider are used as generic names for curtain sided trucks/trailers. The curtains are permanently fixed to a runner at the top and detachable rails/poles at front and rear, allowing the curtains to be drawn open and forklifts used all along the sides for easy and efficient loading and unloading. When closed for travel, vertical load restraint straps are attached to a rope rail beneath the truck bed, connecting the truck bed and curtain along both sides. Winches at either end of the curtain tension it, hence the 'Tautliner' name. This stops the curtain from flapping or drumming in the wind and can also help retain light loads from slipping sideways. |

| Transloading | Transloading is a shipping term that refers to the transfer of goods from one mode of transportation to another en route to their ultimate destination. |

| Tsubo | A Japanese unit of area equal to 35.58 square feet. |

| Unpaved Road | Road with a stabilized base not surfaced with crushed stone, hydrocarbon binder or bituminized agents, concrete or cobblestone. |

| Vessel Husbandry Services | It includes ship maintenance, repairs, cleaning, upkeep of the hull and rigging and equipment. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms