Spain Mobile Virtual Network Operator (MVNO) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

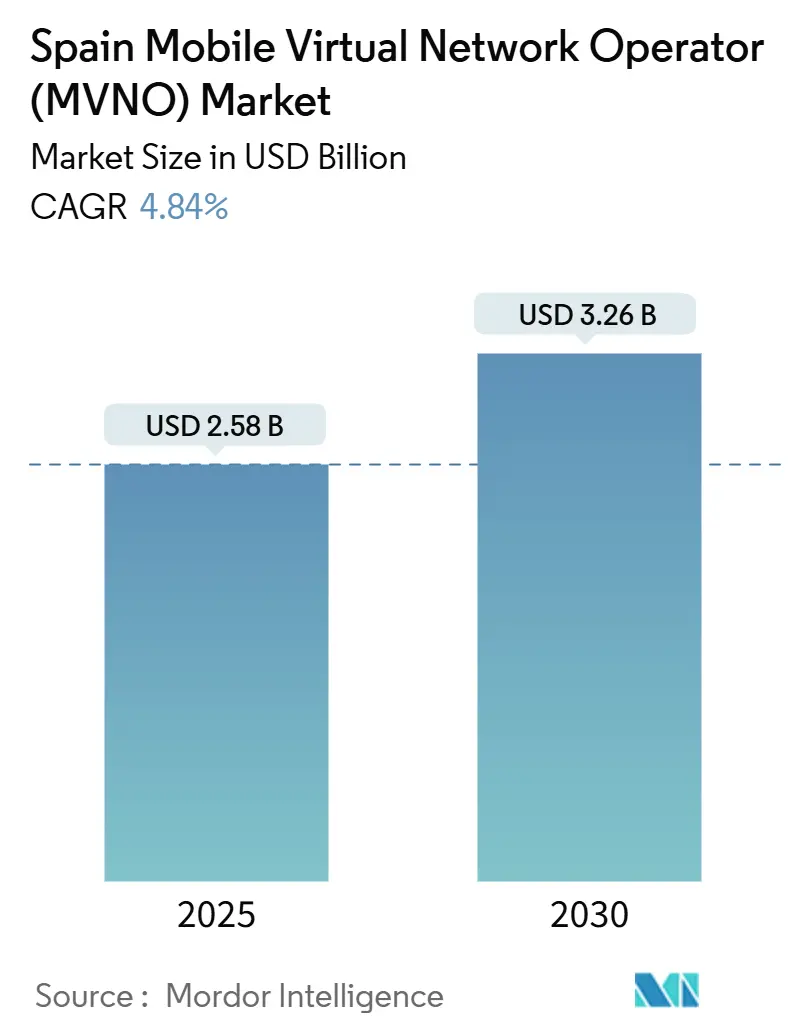

| Market Size (2025) | USD 2.58 Billion |

| Market Size (2030) | USD 3.26 Billion |

| Growth Rate (2025 - 2030) | 4.84% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Mobile Virtual Network Operator (MVNO) Market Analysis by Mordor Intelligence

The Spain Mobile Virtual Network Operator Market size is estimated at USD 2.58 billion in 2025, and is expected to reach USD 3.26 billion by 2030, at a CAGR of 4.84% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 8.32 million Subscribers in 2025 to 10.42 million Subscribers by 2030, at a CAGR of 4.61% during the forecast period (2025-2030).

Heightened demand for low-cost, digital-first mobile plans, the CNMC’s mandated 5G wholesale access, and nationwide 3G network sunsets are reshaping competitive dynamics. Operators are compressing time-to-market by migrating from on-premise cores to cloud-native stacks, while the accelerated rollout of eSIM services reduces acquisition costs and supports frictionless onboarding. Spectrum-sharing agreements forged after the Orange-MásMóvil merger improve rural coverage, enabling MVNOs to market nationwide footprints without building radio access networks. At the same time, industrial exporters are driving a surge in multi-IMSI IoT subscriptions that leverage both terrestrial 5G and satellite/NTN connectivity.

Key Report Takeaways

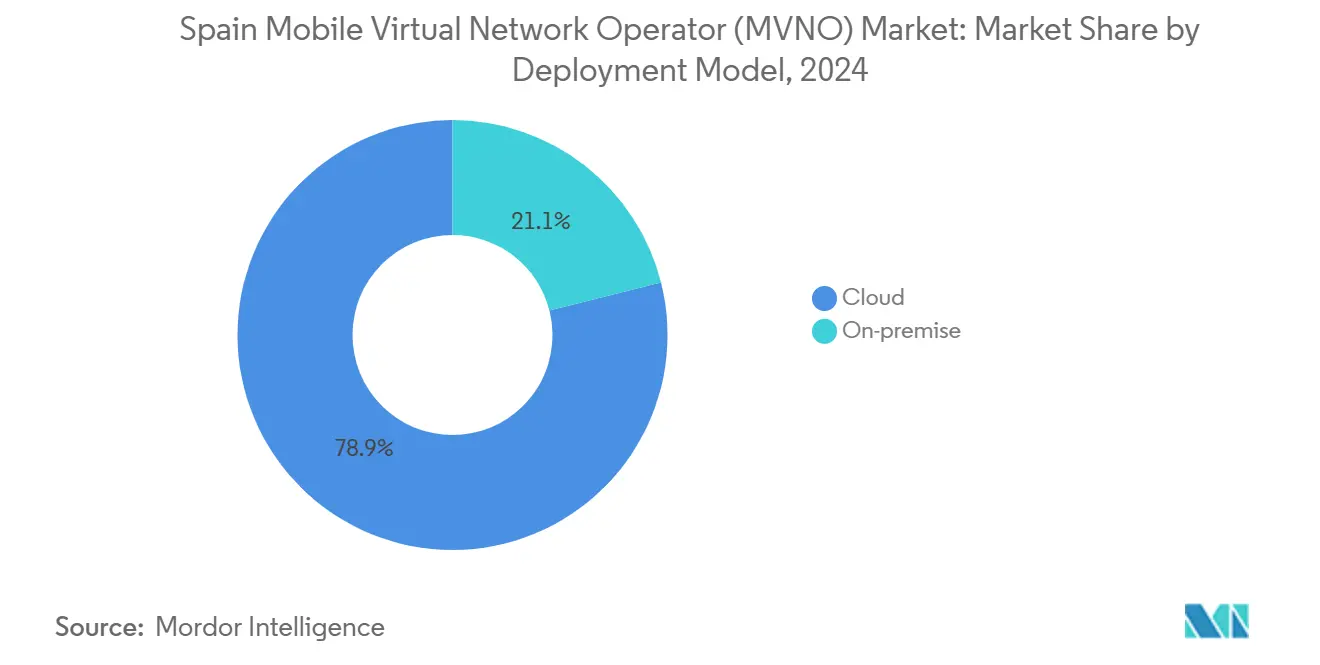

- By deployment model, cloud platforms captured 78.93% revenue share of the Spain MVNO market in 2024 and are on track for a 7.55% CAGR to 2030.

- By operational mode, Full MVNOs are expanding at 13.62% to 2030, outpacing the Reseller segment that held 52.31% Spain MVNO market share in 2024.

- By subscriber type, consumer lines dominated with a 77.58% share in 2024, while IoT-specific lines are forecast to rise at a 16.55% CAGR.

- By application, Cellular M2M lines are growing at 14.33% and will erode the 33.11% share held by the Others segment by 2030.

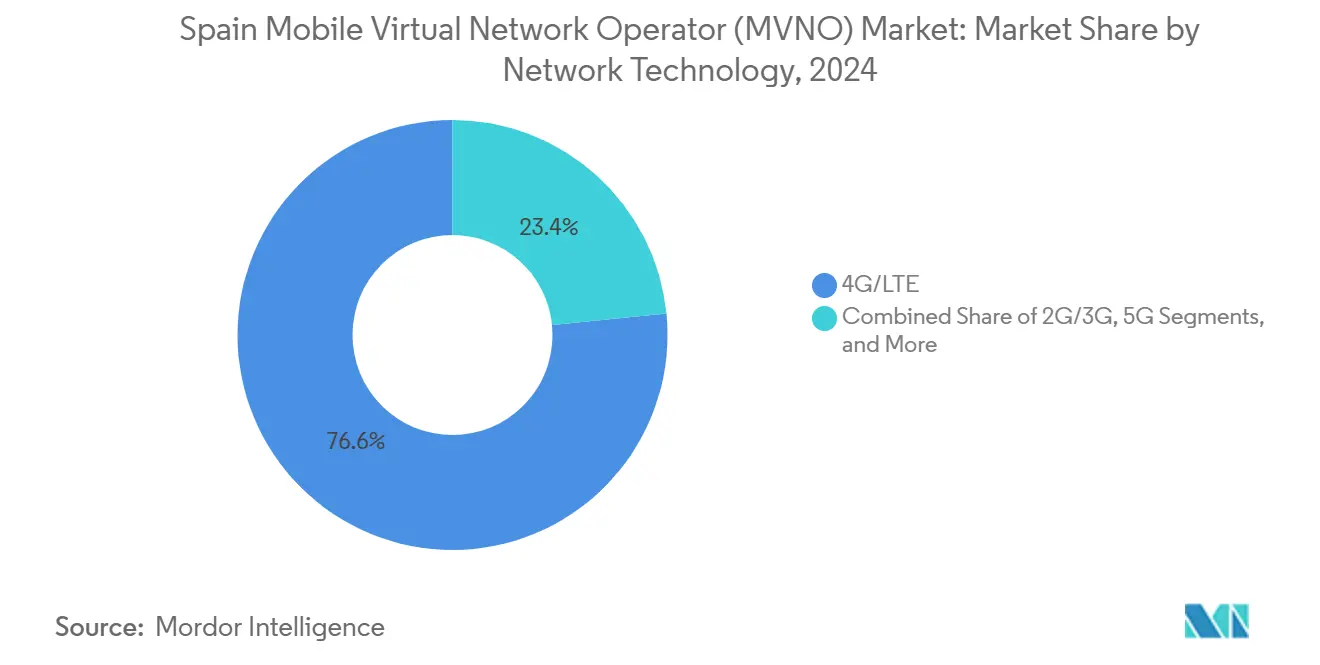

- By network technology, 4G/LTE retained 76.59% share in 2024, whereas Satellite/NTN is advancing at 119.25% CAGR through 2030.

- By distribution channel, online–digital outlets controlled 58.15% of 2024 revenue and are rising at a 7.95% CAGR, eclipsing traditional retail stores.

Spain Mobile Virtual Network Operator (MVNO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of low-cost, flexible plans among price-sensitive consumers | +1.2% | National, concentrated in urban centers | Short term (≤ 2 years) |

| CNMC-mandated 5G wholesale access accelerating MVNO launch cycles | +0.8% | National, with priority in major metropolitan areas | Medium term (2-4 years) |

| Expansion of eSIM and fully-digital onboarding models | +0.6% | National, early adoption in Madrid, Barcelona, Valencia | Medium term (2-4 years) |

| EU "Roam-Like-at-Home" extension unlocking cross-border propositions | +0.4% | National, enhanced value in border regions | Long term (≥ 4 years) |

| Industrial exporters' need for multi-IMSI IoT connectivity | +0.7% | National, concentrated in industrial corridors | Long term (≥ 4 years) |

| Rising Latin-American migrant population seeking international bundles | +0.3% | National, concentrated in Madrid, Catalonia, Valencia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid adoption of low-cost, flexible plans among price-sensitive consumers

Inflationary headwinds are squeezing household budgets, compelling subscribers to hunt for inexpensive bundles that do not impose multi-year contracts. When MasOrange raised tariffs in early 2025, challengers such as Simyo countered by adding 39-50% more data to existing plans without raising prices, thereby reinforcing the value narrative that distinguishes MVNO offerings [1]Cristina Charle, “Simyo inflates data allowances in latest tariff overhaul,” Xataka Móvil, xatakamovil.com. Lebara’s switch from a EUR 3.99 voice plan to new XXL bundles that offer up to 150 GB targets heavy data users who feel restricted by incumbent data caps[2]José M. Insa, “Lebara retires EUR 3.99 plan and debuts XXL bundles,” DigitalWeek, digitalweek.de. Churn remains elevated, March 2025 recorded over 530,000 number portings, demonstrating consumer willingness to migrate in search of favorable pricing [3]CNMC Statistical Bulletin March 2025, CNMC, cnmc.es . As leading MNOs pursue higher average revenue per user, MVNOs become the natural refuge for price-sensitive segments, fueling subscriber inflows that sustain Spain's MVNO market growth. Competitive elasticity, therefore, remains a central strategic lever for agile brands.

CNMC-mandated 5G wholesale access accelerating MVNO launch cycles

The CNMC requires host networks to extend 5G access on fair and non-discriminatory terms, cutting the average MVNO launch cycle from nearly two years to under 12 months. Digi’s 16-year national-roaming and RAN-sharing pact with Telefónica illustrates how new entrants can leverage regulated wholesale to evolve into full MNOs while maintaining competitive tariffs. Shorter incubation windows lower capital risk and help niche brands validate go-to-market propositions quickly, catalyzing the proliferation of over 100 active MVNOs. However, greater accessibility also inflates competition, obliging operators to differentiate on user experience, localized content, or bundled services rather than solely on price. Overall, the rule change lifts Spain's MVNO market capacity by widening the pipeline of potential entrants.

Expansion of eSIM and fully digital onboarding models

MVNOs are rolling out eSIM activation flows that eliminate physical distribution, slash logistics costs, and enable near-instant service provisioning. Simyo made eSIM downloads free for its users in 2024, a move quickly mirrored by Lowi early in 2025. Digital activation caters to travelers, digital nomads, and tech-savvy urbanites who favor seamless device switching and immediate connectivity. Reduced acquisition costs enhance margin resilience in a low-ARPU climate while shrinking carbon footprints associated with plastic SIM cards. As Spain MVNO market operators strengthen app-based self-care and identity verification workflows, they unlock new monetization playbooks, including micro-subscriptions and trial plans that were commercially impractical under legacy SIM fulfillment.

EU “Roam-Like-at-Home” extension unlocking cross-border propositions

The EU’s decision to prolong wholesale roaming caps, EUR 7.7 per GB in 2025, allows MVNOs to craft unified European bundles that feel domestic to end users. Spain’s 2.3 million Latin-American residents often travel or send remittances abroad; MVNOs such as Lycamobile already tailor offers that combine generous EU data with discounted Latin-American voice add-ons. Cross-border features strengthen customer retention by reducing bill shock in neighboring Portugal and France and by enabling frictionless connectivity for truckers and seasonal workers. Over time, bundled European-Latin American roaming could become a distinctive revenue pillar that sets Spain's MVNO market plans apart from incumbent triple-play strategies.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated wholesale access fees versus EU peers | -0.9% | National, affecting all MVNO operations | Short term (≤ 2 years) |

| Market saturation and declining ARPU compress margins | -0.7% | National, intensified in urban markets | Medium term (2-4 years) |

| 3G sunset and spectrum re-farming risk legacy MVNO contracts | -0.5% | National, critical for rural coverage | Short term (≤ 2 years) |

| Draft Digital-ID decree raises KYC onboarding costs | -0.3% | National, compliance framework pending | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Elevated wholesale access fees versus EU peers

Despite regulatory oversight, Spanish wholesale rates outstrip many European benchmarks, eroding MVNO margins. Recent CNMC revisions allowed Telefónica to push through 11% monthly and 14.6% one-time increases, moves the incumbent contends are necessary to recover infrastructure costs[4]“Telefónica denounces CNMC-set losses on duct pricing,” El Economista, eleconomista.es. Smaller players without bargaining heft, such as Finetwork, have entered pre-bankruptcy amid payment disputes with Vodafone that underscore financial fragility. Forced to absorb higher costs, several MVNOs have trimmed marketing budgets or narrowed geographic focus, potentially limiting the overall addressable footprint of the Spanish MVNO market. Unless a new cost baseline emerges, aggressive pricing strategies could become unsustainable for thinly capitalized brands.

Market saturation and declining ARPU compress margins

More than 100 active MVNOs produce intense deal-making that drags down ARPU even as subscriber counts rise. March 2025’s 530,000 portings evidence a consumer base trained to chase the best bargain. Simultaneously, MasOrange’s EUR 583 million loss across its first nine months as a consolidated entity shows that even scaled operators struggle to monetize traffic in Spain’s hyper-competitive arena. As price wars intensify, differentiation through service quality, content bundling, or multi-device offers becomes critical. Without new value-added revenue streams, profitability pressure may push some operators to exit, merge, or pivot toward niche enterprise and IoT domains, tempering the Spain MVNO market CAGR in later forecast years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Infrastructure Drives Digital Transformation

Cloud-based cores delivered 78.93% of 2024 revenue and maintain a 7.55% CAGR, underlining their role in streamlining network evolution and reducing fixed-asset exposure. That scale translates into lower operating costs, allowing providers to enter the Spain MVNO market faster than on-premise peers while matching feature velocity with customer demand. Telefónica’s cloud-hosted Kite Platform illustrates how virtualized control functions accelerate IoT onboarding while facilitating coverage across multiple radio technologies. Hybrid cloud designs also enable geographic redundancy, an attribute prized by MVNOs targeting critical M2M workloads.

Traditional on-premise deployments persist where data residency or bespoke security controls supersede cost advantages. Certain enterprise-focused MVNOs, particularly those integrating private network slices for manufacturing clients, retain on-site packet core gateways to meet audit standards. However, total cost-of-ownership analyses increasingly favor elastic, pay-as-you-scale clouds even for regulated workloads once encryption and sovereign-cloud options are configured. As hyperscale providers set up Spanish availability zones, latency gaps narrow and tilt the cost-performance equation further toward off-premise models.

By Operational Mode: Full MVNOs Gain Infrastructure Independence

Reseller constructs still hold 52.31% Spain MVNO market share, yet the full MVNO model’s 13.62% CAGR marks a decisive pivot toward infrastructure ownership. Digi epitomizes this migration: after purchasing spectrum for USD 120 million and signing a 16-year roaming deal, the operator is phasing in its own RAN to elevate gross margins and product control. Full MVNOs seize complete brand custody, manage their IMSIs, and exert price agility that resellers cede to hosts.

Service-operator hybrids sit mid-spectrum, hosting HLR/HSS elements while leasing RAN capacity. They balance capital exposure with quality-of-service stewardship, an approach popular among enterprise-centric players that need granular policy control but lack nationwide spectrum. As 5G standalone and network slicing mature, owning packet-core and policy layers becomes vital for differentiated latency guarantees, further nudging operators up the autonomy curve.

By Subscriber Type: Consumer Dominance Faces IoT Disruption

Consumer accounts represented 77.58% of active lines in 2024, cementing their historical weight in the Spain MVNO market. Unlimited-style bundles and youth-targeted sub-brands prove effective in minimizing churn among gig-hungry users. Yet the 16.55% CAGR in IoT connections signals a material realignment toward machine-centric revenues. Vodafone already manages 7.5 million Spanish IoT lines, adding nearly 1 million in nine months of 2024 and illustrating demand momentum.

Enterprise-human connections, while smaller in number, deliver superior ARPU, especially where bundled UCaaS or VPN add-ons raise value per line. For MVNOs, the growth formula increasingly blends consumer volume stability with targeted IoT solutions for logistics, agriculture, and smart-city deployments. Industrial clients require global eUICC profiles, multi-IMSI capabilities, and real-time diagnostics, features that cloud-based full MVNO stacks are positioned to supply.

By Application: M2M Growth Reshapes Service Portfolios

The other applications segment controlled 33.11% of 2024 billing but stands to cede share as Cellular M2M climbs at 14.33% CAGR through 2030. Smart meters, asset-tracking tags, and agricultural sensors rely on low-power, wide-area NB-IoT services that MVNOs can source at favorable wholesale rates. The Spain MVNO market size for Cellular M2M is projected to expand rapidly as industrial policy emphasizes digital twins and real-time supply-chain visibility.

Discount voice-data bundles remain the cash cow for price-led brands, yet falling termination rates and data-unit pricing squeeze margins. Business-grade applications, particularly SD-WAN and managed mobility, offer upsell leverage. Nevertheless, pure consumer discount plays are likely to plateau, ushering a portfolio pivot toward M2M and sector-specific service layers that insulate revenues from commodity pricing cycles.

By Network Technology: 5G Transition Accelerates Innovation

Spain’s operators completed 700 MHz coverage obligations in 2025, putting nationwide 5G NSA layers within reach of most urban subscribers. 4G/LTE, however, still carried 76.59% of active lines in 2024 and is expected to remain the primary traffic bearer until mid-decade. Satellite/NTN, powered by Barcelona-based Sateliot’s NB-IoT constellation, is surging at 119.25% CAGR by 2030.

For MVNOs, 5G SA and NTN present dual opportunities: differentiated quality-of-service tiers for high-value users and ubiquitous M2M coverage that transcends terrestrial dead zones. Yet legacy 2G/3G sunsets, Vodafone completed its 3G shutdown in September 2024 and Telefónica targets 2025, forcing rapid device migrations and renegotiation of older wholesale contracts. The result is a compressed technology refresh cycle that rewards operators with agile procurement and device certification processes.

By Distribution Channel: Digital-First Strategies Gain Momentum

Digital-only storefronts yielded 58.15% of revenue in 2024 and remain the Spain MVNO market’s fastest-growing distribution path at 7.95% CAGR. Lowi’s April 2025 rollout of a long-requested usage-monitoring feature epitomizes the feedback loop agility enabled by app-centric channels. E-commerce-driven acquisition trims SIM logistics, accelerates onboarding, and unlocks data-driven targeting models.

Carrier sub-brand kiosks and multi-operator shops preserve value for demographics desiring personal assistance or device financing, but their relative share is waning as post-pandemic behavior normalizes around contactless transactions. Third-party wholesalers still matter for rural shelves and migrant-heavy neighborhoods, although margin splits curb their scalability. Ultimately, omnichannel orchestration, online first, augmented by selective physical presence, emerges as the winning playbook.

Geography Analysis

Madrid, Catalonia, and Valencia together account for an estimated 60% of Spain's MVNO market subscriptions, correlating with dense populations, high purchasing power, and elevated smartphone penetration. Aggressive digital-only campaigns fuel urban churn and short contract tenures that simplify switching. The Unico Redes Activas program injects EUR 544 million in 90%-subsidized funding to extend 5G into towns under 10,000 inhabitants, turning historically loss-making zones into viable targets for virtual operators that lease 700 MHz capacity from MasOrange, Telefónica, or Vodafone.

Cross-border corridors adjacent to France and Portugal amplify the appeal of roam-like-at-home bundles that treat neighboring traffic as domestic. MVNOs offering such plans minimize bill shock for daily commuters and freight operators, cultivating loyalty in regions where alternative MNO coverage fluctuates. At the same time, 2.3 million Latin-American immigrants cluster largely in Madrid and Barcelona, enabling hyper-localized campaigns that package cheap calls to Colombia, Peru, or Venezuela with domestic data allowances.

Industrial clusters along the Mediterranean, Valencia, Murcia, and the Basque Country generate outsized IoT connectivity demand. Automotive and logistics majors there procure multi-IMSI SIMs that roam seamlessly across European supply chains, pushing MVNOs to interoperate with foreign networks. Homogeneous CNMC regulation simplifies nationwide compliance, yet local business licenses and consumer-protection norms necessitate minor tweaks in marketing and support operations. Taken together, geographic heterogeneity rewards operators that tailor propositions to urban affordability, cross-border mobility, and industrial digitization.

Competitive Landscape

Post-merger MasOrange controls 42.5% of mobile lines, while Telefónica and Vodafone hold 26.7% and 21.3%, respectively, concentrating wholesale power in three entities. This triopoly elevates the strategic importance of long-term capacity deals for MVNO sustainability. Finetwork’s May 2025 pre-insolvency filing after a billing dispute with Vodafone dramatizes execution risk when wholesale terms sour.

Competition stratifies into three tiers. First, infrastructure-owning challengers like Digi invest in spectrum and tower leases to migrate into full MNO status, aiming to compress network-cost curves over time. Second, mature sub-brands such as Lowi, Simyo, and Pepephone fight on agility, curation, and responsive pricing. Third, niche entrants exploit whitespace. Lebara pursues migrant international calling; Sateliot partners with industrial integrators for satellite IoT backhaul.

Strategic levers increasingly revolve around technology speed and customer-experience excellence. Simyo’s free eSIM rollout and Lowi’s real-time usage widgets show how digital-first cultures translate into tangible differentiation. Meanwhile, cross-industry alliances, mobile plus remittance, or satellite IoT plus sensor analytics, create moats that pure-play connectivity lacks. Rising compliance costs under Spain’s planned Digital-ID law could tilt the advantage to resource-rich brands able to absorb elevated onboarding outlays, potentially sparking another round of consolidation.

Spain Mobile Virtual Network Operator (MVNO) Industry Leaders

Lowi, S.L.U.

Simyo

Pepephone (Pepemobile, S.L.)

Finetwork Spain Telecom S.L.U.

Lycamobile SLU

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Simyo raised included data by up to 50% across multiple plans to reinforce its low-cost proposition against Digi, Lowi and O2.

- July 2024: Digi España activated its first proprietary mobile antenna as part of its transition from MVNO to MNO status, following its USD 120 million spectrum buy and 16-year Telefónica roaming pact.

- February 2024: The European Commission cleared the Orange-MásMóvil joint venture, prompting spectrum divestment to Digi and birthing Spain’s largest telecom operator with more than 37 million lines.

Spain Mobile Virtual Network Operator (MVNO) Market Report Scope

| Cloud |

| On-premise |

| Reseller / Light / Brand MVNO |

| Service Operator |

| Full MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online/Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party/Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller / Light / Brand MVNO |

| Service Operator | |

| Full MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online/Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party/Wholesale |

Key Questions Answered in the Report

How large is the Spain MVNO market in 2025?

The Spain MVNO market size stands at USD 2.58 billion in 2025 with a 4.84% CAGR outlook to 2030.

Which deployment model leads the virtual operator space?

Cloud platforms dominate with 78.93% revenue share and are expanding at 7.55% CAGR through 2030.

Which subscriber segment is growing fastest?

IoT-specific lines are rising at 16.55% CAGR, outpacing consumer and enterprise segments.

What technology shift is most disruptive?

Satellite/NTN connectivity is surging at 119.25% CAGR, enabling ubiquitous M2M coverage.

How does regulation influence new MVNO launches?

CNMC-mandated 5G wholesale access has cut launch cycles to 6-12 months, broadening entry paths for niche brands.

Why are wholesale fees a restraint for growth?

Access prices remain above EU averages, trimming MVNO margins and pushing smaller players toward consolidation.

Page last updated on: