Trivalent Chromium Finishing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 469.85 Million |

| Market Size (2031) | USD 605.22 Million |

| Growth Rate (2026 - 2031) | 5.19% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

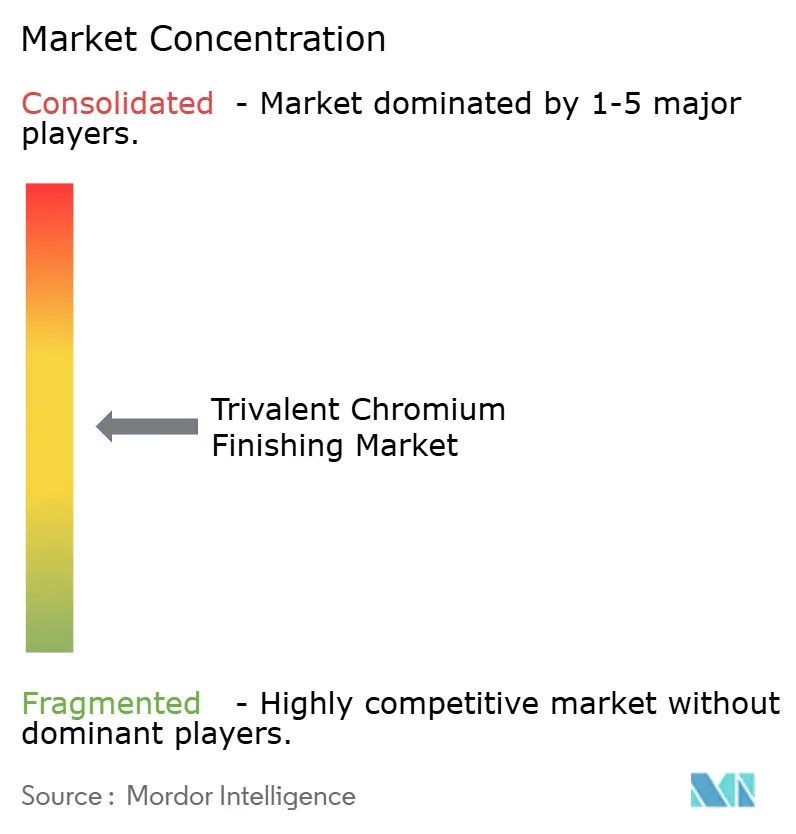

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Trivalent Chromium Finishing Market Analysis by Mordor Intelligence

The Trivalent Chromium Finishing Market size was valued at USD 447.65 million in 2025 and is estimated to grow from USD 469.85 million in 2026 to reach USD 605.22 million by 2031, at a CAGR of 5.19% during the forecast period (2026-2031). The trivalent chromium finishing market is expanding because regulatory agencies in Europe, North America, and Asia are phasing out hexavalent chromium, forcing OEMs (original equipment manufacturers) to redesign supply chains and co-locate compliant plating capacity. Rising demand from electric-vehicle (EV) connectors, magnesium-intensive lightweight structures, and additive-manufactured aerospace brackets adds structural volume, while closed-loop process lines and in-line electrowinning reduce operating costs and widen adoption. Capital spending on dual-chemistry lines is moderating competitive intensity because only well-capitalized suppliers can install trivalent modules next to legacy hexavalent tanks, and this concentration allows chemistry vendors to maintain price discipline. The trivalent chromium finishing market also benefits from its micro-throwing-power advantage that coats internal lattice geometries common in 3D-printed parts, giving it a functional edge that hard-chrome cannot match.

Key Report Takeaways

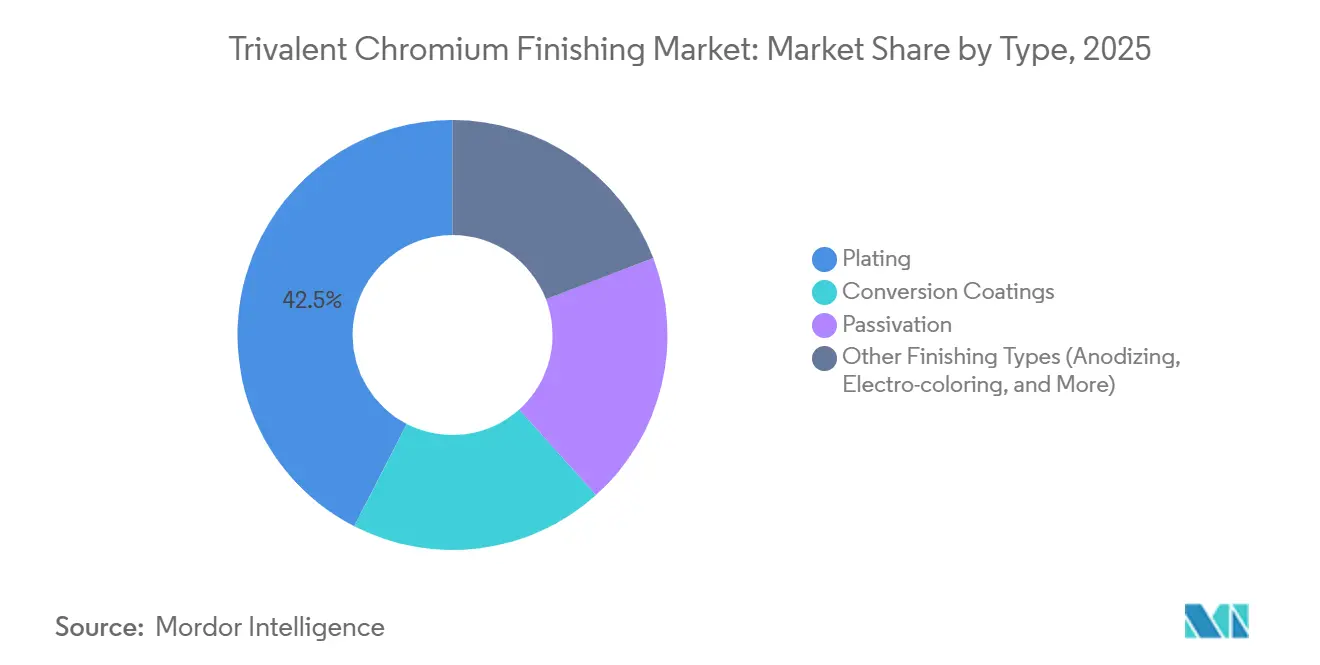

- By type, plating processes led with 42.45% of the trivalent chromium finishing market share in 2025, while passivation is projected to advance at a 6.12% CAGR during the forecast period (2026-2031).

- By base material, steel and stainless steel accounted for 34.17% of the trivalent chromium finishing market size in 2025, whereas magnesium is set to grow fastest at a 6.23% CAGR during the forecast period (2026-2031).

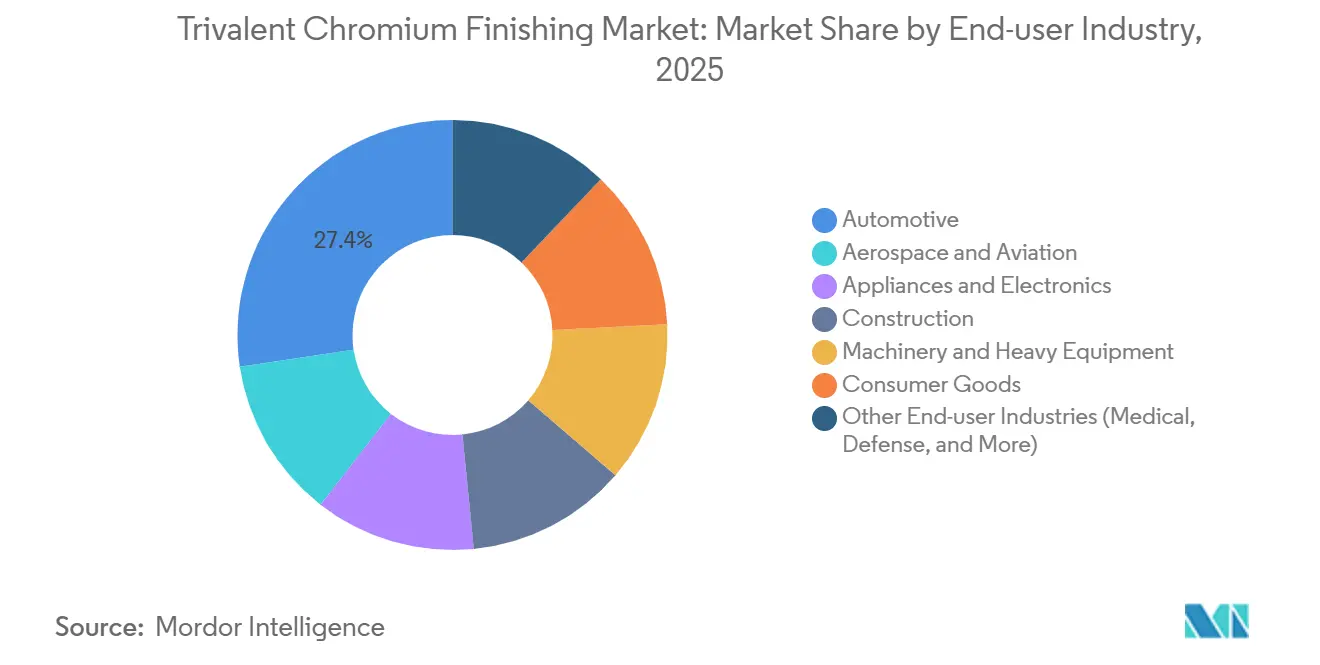

- By end-user industry, automotive commanded 27.36% revenue in 2024 and is forecast to rise at a 6.16% CAGR during the forecast period (2026-2031).

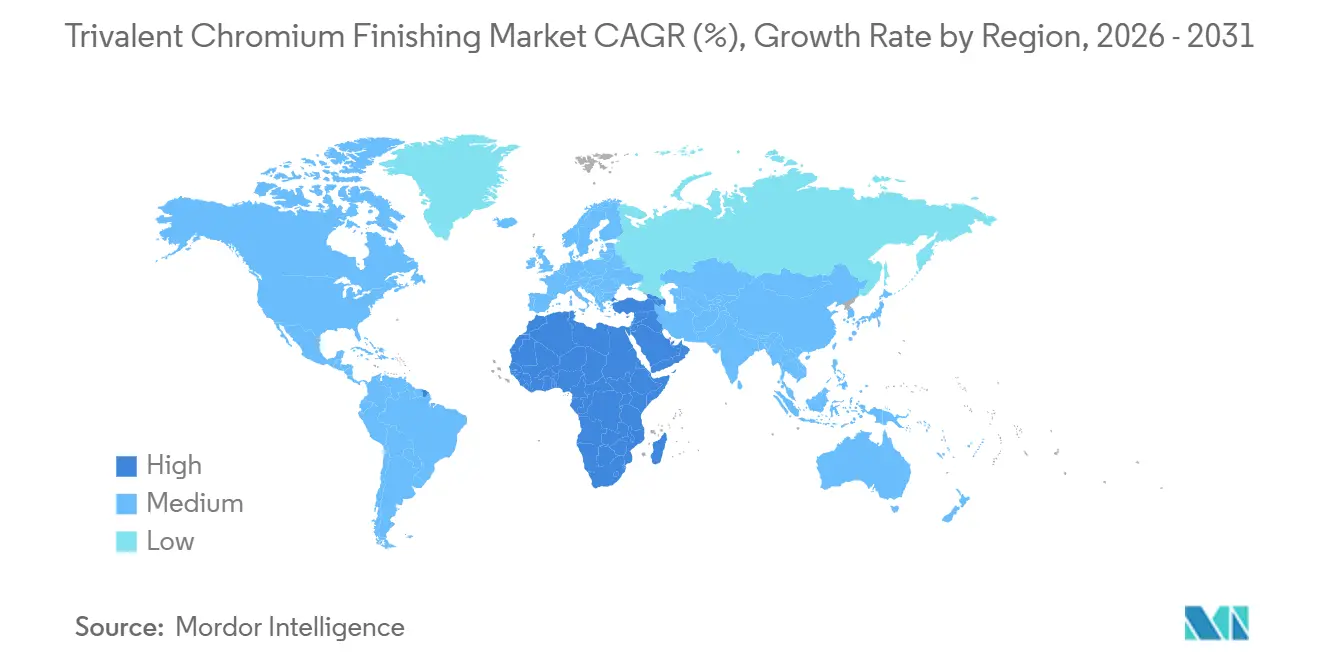

- By geography, Asia-Pacific captured 41.22% of 2025 revenue, and the market share of the Middle East and Africa is projected to post a 6.31% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Trivalent Chromium Finishing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict environmental regulations limiting Cr(VI) use | +1.8% | Global, led by EU and California | Short term (≤ 2 years) |

| EV battery-pack connectors require Cr(III) passivation | +1.2% | APAC core (China, South Korea), spill-over to North America | Medium term (2-4 years) |

| Automotive lightweighting demands corrosion-proof finishes | +0.9% | Global, concentrated in Germany, Japan, United States | Medium term (2-4 years) |

| Aerospace shift toward high-efficiency trivalent hard-chrome | +0.6% | North America & EU aerospace hubs | Long term (≥ 4 years) |

| Micro-throwing-power edge for complex 3D-printed metal parts | +0.5% | North America, Germany, Japan (additive manufacturing centers) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict Environmental Regulations Limiting Cr(VI) Use

Jurisdictions are compressing the compliance window for hexavalent chrome and propelling the trivalent chromium finishing market toward rapid substitution. The European Chemicals Agency proposed an 18-month transition in April 2025, intending entry into force during 2027-2028, while California’s Air Resources Board mandates decorative phase-outs by 2027 and hard-chrome elimination by 2039[1]European Chemicals Agency, “Restriction Proposal for Chromium Trioxide,” echa.europa.eu. OEMs serving both regions now engineer dual-chemistry lines, elevating capital intensity but deepening their commitment to trivalent chemistries. Japan’s Ministry of Economy, Trade, and Industry aligned export timelines with REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals), effectively globalizing the standard. South Coast Air Quality Management District Rule 1469 tightens emissions to 0.01 mg per amp-hour, making closed-loop trivalent systems with electrowinning the default in Southern California. Collectively, these statutes cement the trivalent chromium finishing market as the regulatory safe harbor for international suppliers.

EV Battery-Pack Connectors Require Cr(III) Passivation

China delivered more than 12 million new-energy vehicles in 2025, and connector salt-spray requirements doubled from 48 hours to 96 hours within 18 months, creating a surge in demand for trivalent passivation of copper busbars[2]Ministry of Industry and Information Technology, “China NEV Production Report 2025,” miit.gov.cn. Each vehicle houses 20-30 connectors, translating into over 120 million components annually needing RoHS-compliant coatings. Plating parks in Suzhou experienced a 50% order spike for copper connector finishing in H2-2025, and thermal stability thresholds rose to 150-200°C as fast-charging proliferated. Formulators such as SurTec have introduced hybrid zirconium-chromium layers that extend impedance tenfold when paired with sol-gel topcoats, hinting at future migration toward entirely chromium-free alternatives. For the medium term, however, the trivalent chromium finishing market retains the advantage of drop-in compatibility with existing copper cleaning and activation sequences.

Automotive Lightweighting Demands Corrosion-Proof Finishes

Corporate average fuel-economy rules and Electric Vehicle range targets are forcing OEMs to integrate aluminum and magnesium castings that must still survive decade-long corrosion tests. Plasma-electrolytic-oxidation on AZ91D magnesium, followed by trivalent chromium sealing, boosted coating resistance threefold in pilot lines, validating commercial scale-up. Atomic-layer-deposited chromium oxide on AA2024 aluminum cut corrosion current density by two orders of magnitude at only 50 nm thickness, enabling uniform coverage on gigacast megacastings without a weight penalty. As casting consolidates parts into larger monoliths, the square-meter surface area per vehicle increases, lifting the trivalent chromium finishing market volume even if unit vehicle sales plateau. German, Japanese, and U.S. OEMs are therefore budgeting multi-year tooling upgrades that bundle gigacasting with trivalent finishing cells located inside foundry footprints.

Aerospace Shift Toward High-Efficiency Trivalent Hard-Chrome

The International Aerospace Environmental Group confirmed in June 2025 that trivalent hard-chrome is not yet a one-to-one drop-in for critical wear surfaces, but Boeing, Henkel, and MacDermid lead a consortium targeting 90% substitution by 2036. Boeing’s Cr(III)-Fe alloy patent specifies hardness above 1,050 Vickers and Taber wear indices below 10, positioning it for non-critical hinges, seat tracks, and fasteners. High-velocity oxygen-fuel (HVOF) tungsten-carbide coatings can outpace electroplating by a factor of 50 on throughput, yet USD 300,000 equipment costs limit adoption to major MRO hubs. Over the long term, blended strategies, HVOF for struts, trivalent for interiors, mean every incremental gallon of chromium trioxide removed from landing-gear overhaul lines flows toward the trivalent chromium finishing market instead of legacy hexavalent baths.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capex for converting legacy Cr(VI) plating lines | -0.7% | Global, acute in North America & EU | Short term (≤ 2 years) |

| Limited high-temperature wear resistance vs. hard-chrome | -0.5% | Aerospace hubs (North America, EU) | Medium term (2-4 years) |

| Volatile supply and price of high-purity Cr(III) salts | -0.3% | Global, sourced from South Africa, Kazakhstan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Capex for Converting Legacy Cr(VI) Plating Lines

Typical conversion budgets range from USD 150,000 to USD 500,000 per line, including rectifiers, filtration, and wastewater upgrades, and payback exceeds five years for shops plating fewer than 1,000 parts yearly. The ADCR consortium estimates EUR 1.2 billion in capital across European aerospace players to meet REACH deadlines, and many SMEs lack access to low-cost financing. Consequently, the trivalent chromium finishing market is bifurcating: Tier-1 suppliers embed captive lines while small job shops shutter or consolidate.

Limited High-Temperature Wear Resistance vs. Hard-Chrome

Trivalent deposits average 600-800 Vickers and lose adhesion above 150°C unless supported by nickel underlayers, which add 20% cycle time and create thermal-expansion mismatch. HVOF tungsten-carbide passes accelerated wear tests yet commands higher capex and operator skill. Boeing’s alloyed trivalent chrome proposes post-plate baking to exceed 1,050 Vickers, though elevated heat raises hydrogen-embrittlement risk in high-strength steel. Until performance reaches parity, critical aerospace and hydraulic parts will keep limited Cr(VI) exemptions, slowing a full pivot to the trivalent chromium finishing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Passivation Gains as Chromium-Free Alternatives Mature

Plating delivered 42.45% of 2025 revenue, driven by decorative trim and functional wear coatings, but passivation is expanding fastest at 6.12% CAGR for the forecast period (2026-2031) as OEMs chase processes that skirt both hexavalent and trivalent reporting thresholds. Conversion coatings occupy a stable middle ground because they serve aluminum housings before powder paint, yet SurTec’s hybrid zirconium-chromium passivation recently demonstrated tenfold impedance gains, foreshadowing a future tilt toward zirconium dominance. The trivalent chromium finishing market size for plating remains large, yet its share is set to erode as nano-ceramic and sol-gel topcoats converge with low-temperature trivalent seals that run in 90-second cycles, improving takt time on high-volume automotive stampings.

Plating advocates counter that Boeing’s Cr(III)-Fe alloy patent specifies current densities of 100-500 mA cm-² and aims for 1,250 Vickers with minimal macro-crack formation, suggesting functional chrome will endure. Meanwhile, conversion coatings’ 30-90 second immersion windows and low capital needs resonate with consumer-electronics plants that must pivot between aluminum, zinc, and magnesium chassis weekly. These economics ensure the trivalent chromium finishing market remains diversified across finishing techniques rather than dominated by a single process.

By Base Material: Magnesium’s 6.23% CAGR Reflects Lightweighting Imperative

Steel and stainless steel supplied 34.17% of 2025 revenue because fasteners, appliance shells, and industrial valve bodies still value tensile strength over mass reduction. Magnesium’s 6.23% CAGR during the forecast period (2026-2031), however, mirrors its 35% density advantage over aluminum and the shift to gigacasting large structural pieces that push surface area per part higher. Trivalent-chromium sealed plasma-electrolytic-oxidation on AZ91D multiplied coating resistance threefold, making magnesium acceptable even in corrosive coastal markets. The trivalent chromium finishing market size for aluminum also increases because atomic-layer-deposited Cr₂O₃ films at only 50 nm satisfy aerospace corrosion tests without adding significant weight.

Nonetheless, magnesium’s galvanic mismatch with steel fasteners mandates isolation gaskets or duplex coatings, injecting added assembly cost. Steel retains niche growth in high-wear components as electrical-discharge chromium-copper overlays reach 1,230 Vickers hardness, extending duty life for hydraulic cylinder rods. These cross-currents keep the trivalent chromium finishing market balanced across multiple base metals.

By End-user Industry: Automotive’s 6.16% CAGR Outpaces Broader Market

Automotive consumed 27.36% of 2025 revenue and is forecast to grow 6.16% annually between 2026 and 2031, faster than the overall trivalent chromium finishing market. Each EV packs 20-30 copper connectors, and 10-year battery warranties elevated salt-spray targets to 96-120 hours, locking in demand for RoHS-compliant passivation. Aerospace represents smaller tonnage but higher value per square inch, and the ADCR consortium’s 12-year authorization extension means dual sourcing will persist: trivalent for interiors, HVOF for struts.

Appliances and electronics decelerate because PVD colors match chrome aesthetics without liquid effluent, shrinking their share of the trivalent chromium finishing market. Industrial machinery lags amid macroeconomic slowdowns, but medical devices adopt Armoloy’s ISO-10993-compliant chromium, commanding 30% price premiums. Collectively, these patterns ensure automotive remains the growth engine while aerospace safeguards premium margins.

Geography Analysis

Asia-Pacific held 41.22% of 2025 revenue for the trivalent chromium finishing market, with China’s 12 million EVs anchoring connector passivation demand and Japan’s precision engineering segments standardizing on trivalent to appease EU customers. South Korea protects its semiconductor lead frames with trivalent coatings despite the CHIPS Act omitting plating infrastructure funding. ASEAN economies gain from “China-plus-one” relocation, adding greenfield trivalent lines in Vietnam and Thailand.

North America’s market share is dominated by the U.S. aerospace and Mexican near-shored automotive parts. California’s ATCM forces West Coast shops to shift decorative chrome by 2027 and hard chrome by 2039, propelling regional investment in closed-loop trivalent cells. Canada’s aluminum heat-exchanger plating grows as OEMs push lightweighting.

Europe faces the tightest transition window: ECHA’s 18-month deadline starting in 2027 converges with the End-of-Life Vehicle Regulation’s 0.1 % Cr(VI) threshold, raising traceability costs. German OEMs piloting gigacasting need in-house trivalent lines, while the ADCR group’s EUR 1.2 billion capex estimate underlines the financial strain on smaller aerospace platers.

South America and the Middle East & Africa together command the least market share, but the latter is expected to grow at the fastest 6.31% CAGR to 2031. Saudi Arabia’s Vision 2030 funds captive plating for defense and construction, while South Africa’s chromite reserves anchor global Cr(III) salt supply despite labor disruptions that reverberate through the trivalent chromium finishing market worldwide.

Competitive Landscape

The Trivalent Chromium Finishing market is moderately fragmented. Aerospace primes patent in-house trivalent alloy plates to hedge against supply risk, embedding captive know-how. Independent job shops without capital for electrowinning modules face exit or consolidation, while vertically integrated players, Tesla, BYD, Volkswagen, install on-site trivalent cells to insource finishing and lock in quality. Zero-liquid-discharge lines that recover 90-95% chromium cut raw-material cost by up to 25%, offering margin ballast as salt prices gyrate.

Trivalent Chromium Finishing Industry Leaders

Atotech

MacDermid Enthone

SurTec Group

Nihon Parkerizing Co., Ltd.

Columbia Chemical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Quaker Houghton announced the acquisition of Dipsol Chemicals Co., Ltd. for approximately USD 153 million, expanding its advanced solutions portfolio in plating chemicals for automotive and industrial applications. The transaction strengthens Quaker Houghton's position in the Asian market and adds specialized trivalent chromium technologies to its product portfolio.

- February 2025: Integer Holdings acquired Precision Coating, a provider of surface functionality enhancement services for medical devices, strengthening capabilities in specialized surface treatments, including trivalent chromium applications for implants and surgical instruments.

Global Trivalent Chromium Finishing Market Report Scope

Trivalent Chromium (Cr3+) finishing is an eco-friendly, non-carcinogenic alternative to hexavalent chrome, offering superior corrosion resistance, improved plating coverage, and a similar aesthetic, often used in automotive, decorative, and functional applications.

The trivalent chromium finishing market is segmented by type, base material, end-user industry, and geography. By type, the market is segmented into plating, conversion coatings, passivation, and other finishing types (anodizing, electro-coloring, and more). By base material, the market is segmented into steel and stainless steel, aluminum and alloys, zinc and alloys, magnesium, and other metals (copper, nickel, and more). By end-user industry, the market is segmented into automotive, aerospace and aviation, appliances and electronics, construction, machinery and heavy equipment, consumer goods, and other end-user industries (medical, defense, and more). The report also covers the market size and forecasts for trivalent chromium finishing in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Plating |

| Conversion Coatings |

| Passivation |

| Other Finishing Types (Anodizing, Electro-coloring, etc.) |

| Steel and Stainless Steel |

| Aluminum and Alloys |

| Zinc and Alloys |

| Magnesium |

| Other Metals (Copper, Nickel, etc.) |

| Automotive |

| Aerospace and Aviation |

| Appliances and Electronics |

| Construction |

| Machinery and Heavy Equipment |

| Consumer Goods |

| Other End-user Industries (Medical, Defense, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Plating | |

| Conversion Coatings | ||

| Passivation | ||

| Other Finishing Types (Anodizing, Electro-coloring, etc.) | ||

| By Base Material | Steel and Stainless Steel | |

| Aluminum and Alloys | ||

| Zinc and Alloys | ||

| Magnesium | ||

| Other Metals (Copper, Nickel, etc.) | ||

| By End-user Industry | Automotive | |

| Aerospace and Aviation | ||

| Appliances and Electronics | ||

| Construction | ||

| Machinery and Heavy Equipment | ||

| Consumer Goods | ||

| Other End-user Industries (Medical, Defense, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How big is the trivalent chromium finishing market?

The Trivalent Chromium Finishing Market size was valued at USD 447.65 million in 2025 and is estimated to grow from USD 469.85 million in 2026 to reach USD 605.22 million by 2031, at a CAGR of 5.19% during the forecast period (2026-2031).

What is the forecast CAGR for trivalent chromium processes?

The market is projected to grow at a 5.19% CAGR between 2026 and 2031.

Which end-user segment is expected to grow the fastest through 2031?

Automotive leads with a 6.16% CAGR due to EV connector and lightweighting demand.

Why is Asia-Pacific dominant in market share?

China’s 12 million EV output and widespread electronics manufacturing give Asia-Pacific 41.22% of 2025 revenue.

Page last updated on: