Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Growth Rate | 6.00% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Metal Finishing Market Analysis by Mordor Intelligence

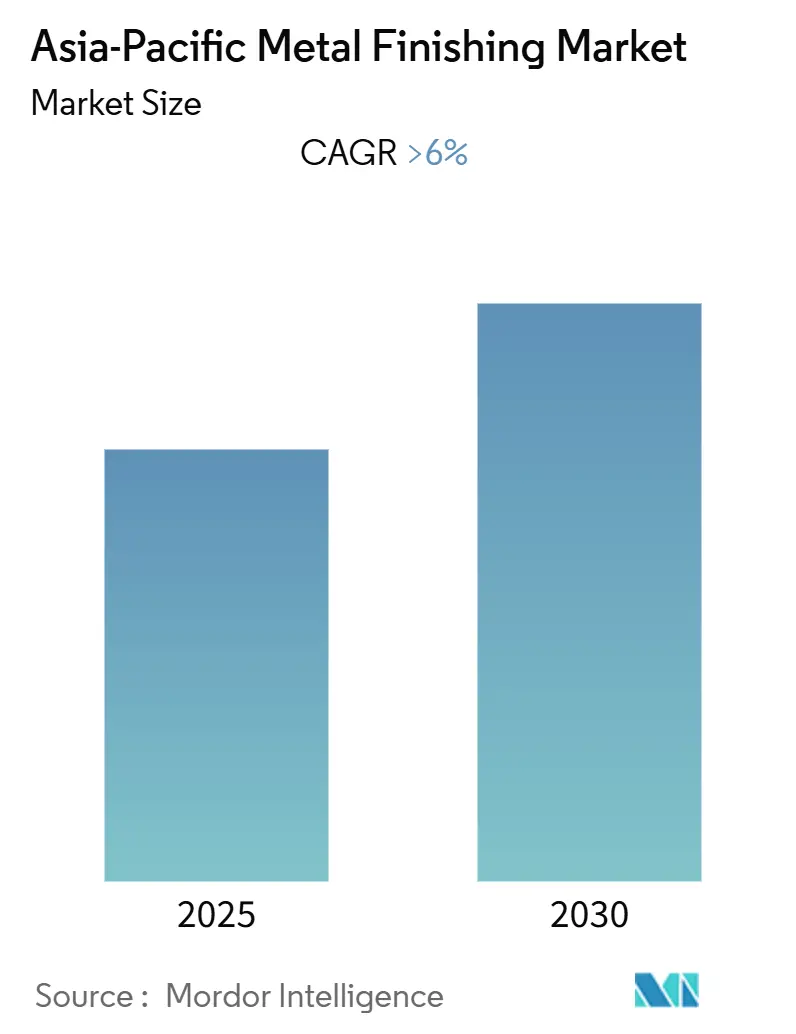

The Asia-Pacific Metal Finishing Market is expected to register a CAGR of greater than 6.5% during the forecast period.

- Environmental restrictions on some chemicals and increasing replacement of metal by plastics are likely to hinder the market's growth.

- Shift from traditional solvent-borne technologies to newer technologies are likely to create opportunities for the Asia-Pacific metal finishing market growth in the coming years.

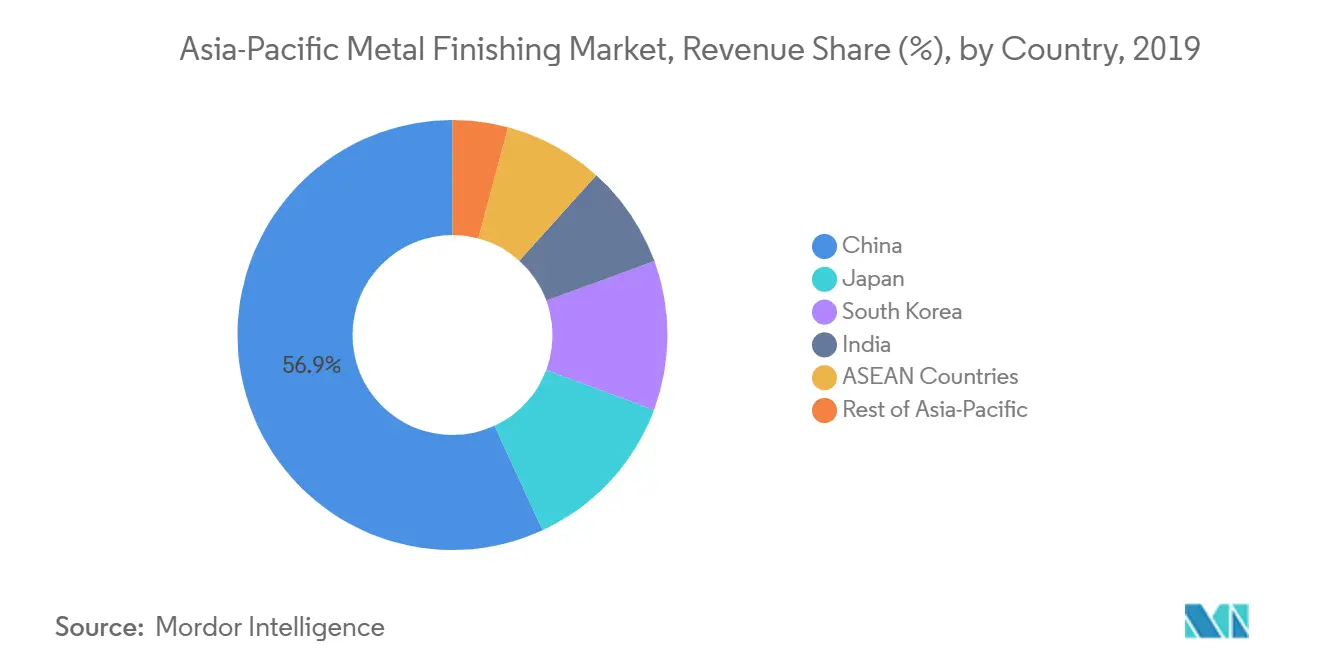

- China is expected to dominate the Asia-Pacific metal finishing market and is also expected to witness the fastest CAGR during the forecast period.

Asia-Pacific Metal Finishing Market Trends and Insights

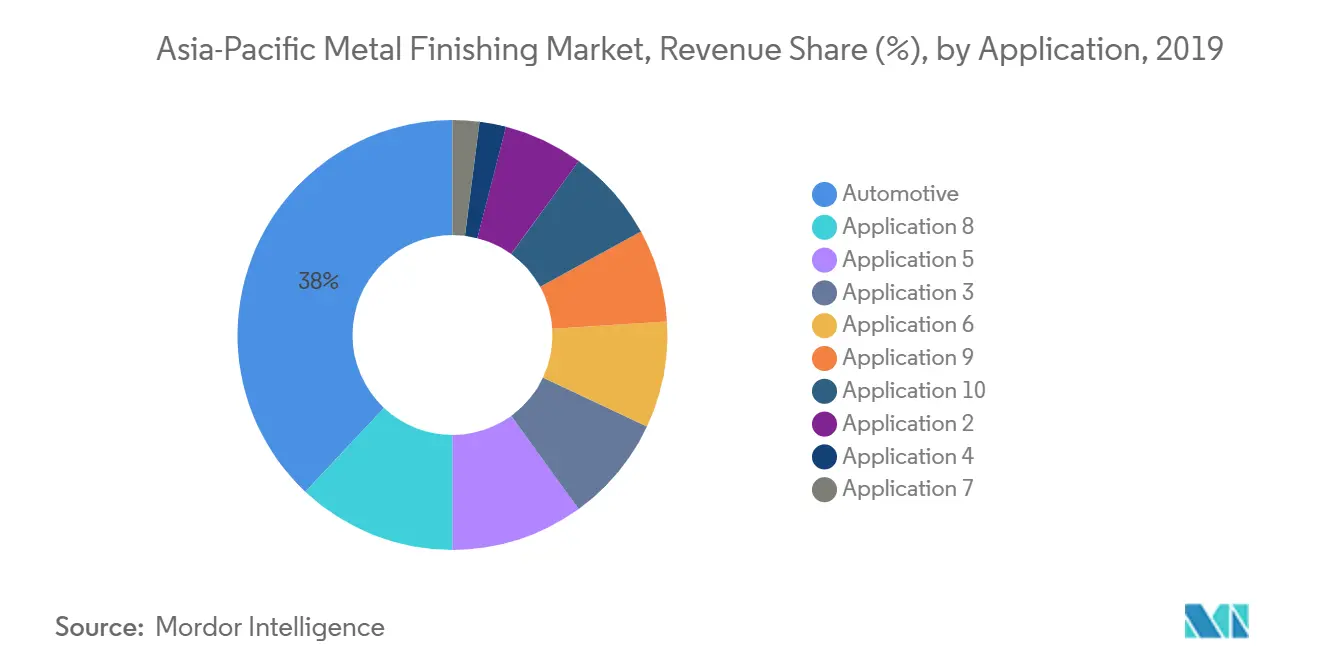

Automotive Segment to Dominate the Market

- Coatings are applied to various automotive components, majorly to provide aesthetics, corrosion resistance, wear resistance, and lubricity and smooth finish. They also increase the life span or durability of the metal component.

- Metal finishing is one of the prominent methods to provide a protective layer on metal automotive components; it involves applying one or more thin coats of a metal, such as gold, copper, silver, chromium or nickel, to a substrate.

- Automobile manufacturers are always in search of better technologies to protect their products from the relentless forces of corrosion. Vehicles are constantly exposed to the moisture from rain and snow, which can cause the premature demise of metal car parts. Metal finishing comprises the application of a metal coating via inorganic metal finishing, such as electroplating. This prevents automobiles from both red and white rust from reaching the underlying metal surface.

- Metal finishing also includes the application of paints or ceramics. Numerous small and large parts of the automobile require their contact surfaces to be smooth, stress relieved, and without burrs or defects. This enables the automotive engines to achieve a surface with less friction and heat, leading to generation of more horsepower and an overall better performance.

- The market, however, has potential for growth in the long term with the emergence of more technologically developed cars. If such a thing happens, the Asia-Pacific metal finishing market will benefit from it.

China to Dominate the Market

- In the Asia-Pacific region, China is the largest economy, in terms of GDP. China is one of the fastest emerging economies and has become one of the biggest production houses in the world, today. The country's manufacturing sector is one of the major contributors to the country's economy.

- The Chinese aircraft industry depicted significant growth over the years. According to Boeing, China is estimated to require around 7,600 new commercial aircraft, valued at USD 1.2 trillion, over the next two decades.

- Foreign investment in China has also been extended into the aviation sector, which is projected to register a CAGR of 6%, owing to China's geographical location, which provides easy access to the industrial goods markets in the neighboring countries, as well as, other countries globally, making it a major access point for manufacturers and suppliers.

- China is the largest manufacturer of automobiles in the world. The country's automotive sector has been shaping up for product evolution, with the country focusing on manufacturing products, in order to ensure fuel economy, and to minimize emissions (owing to the growing environmental concerns due to mounting pollution in the country).

- The production is expected to reach 30 million units by 2020, owing to the 'Made in China 2025' initiative support in upgrading the existing low-cost mass production to higher value-added advanced manufacturing. 'Automobile Mid and Long-Term Development Plan', was released in 2017, with an objective to make China a strong auto power in the next ten years.

- With the rising growing demand from various end-user industries, the Asia-Pacific metal finishing market is expected to grow during the forecast period.

Competitive Landscape

The Asia-Pacificmetal finishing market is partially consolidated in nature. Key players in the market include C. Uyemura & Co. Ltd, Honeywell International Inc., Linde plc, and OC Oerlikon Management AG, among others.

Asia-Pacific Metal Finishing Industry Leaders

C. Uyemura & Co. Ltd

Honeywell International Inc.

Linde plc

OC Oerlikon Management AG

- *Disclaimer: Major Players sorted in no particular order

Asia-Pacific Metal Finishing Market Report Scope

The Asia-Pacific metal finishing market report includes:

Type

| Inorganic Metal Finishing | Cladding |

| Pretreatment/Surface Preparation | |

| Consumables and Spares | |

| Electroplating | |

| Galvanization | |

| Electro Less Plating | |

| Conversion Coatings | |

| Anodizing | |

| Electro Polishing | |

| Organic Metal Finishing | |

| Hybrid Metal Finishing |

Application

| Automotive |

| Appliances |

| Hardware |

| Jewelry |

| Aerospace |

| Heavy Equipment |

| Medical Devices |

| Electronics |

| Construction |

| Other Applications |

Geography

| China |

| India |

| Japan |

| South Korea |

| ASEAN Countries |

| Rest of Asia-Pacific |

| Type | Inorganic Metal Finishing | Cladding |

| Pretreatment/Surface Preparation | ||

| Consumables and Spares | ||

| Electroplating | ||

| Galvanization | ||

| Electro Less Plating | ||

| Conversion Coatings | ||

| Anodizing | ||

| Electro Polishing | ||

| Organic Metal Finishing | ||

| Hybrid Metal Finishing | ||

| Application | Automotive | |

| Appliances | ||

| Hardware | ||

| Jewelry | ||

| Aerospace | ||

| Heavy Equipment | ||

| Medical Devices | ||

| Electronics | ||

| Construction | ||

| Other Applications | ||

| Geography | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current Asia-Pacific Metal Finishing Market size?

The Asia-Pacific Metal Finishing Market is projected to register a CAGR of greater than 6.5% during the forecast period (2025-2030)

Who are the key players in Asia-Pacific Metal Finishing Market?

C. Uyemura & Co. Ltd, Honeywell International Inc., Linde plc and OC Oerlikon Management AG are the major companies operating in the Asia-Pacific Metal Finishing Market.

What years does this Asia-Pacific Metal Finishing Market cover?

The report covers the Asia-Pacific Metal Finishing Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Asia-Pacific Metal Finishing Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: