Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.74 Billion |

| Market Size (2031) | USD 3.86 Billion |

| Growth Rate (2026 - 2031) | 7.09% CAGR |

| Fastest Growing Market | North America |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chromatography Resins Market Analysis by Mordor Intelligence

The Chromatography Resins Market size was valued at USD 2.56 billion in 2025 and estimated to grow from USD 2.74 billion in 2026 to reach USD 3.86 billion by 2031, at a CAGR of 7.09% during the forecast period (2026-2031). Steady growth reflects the segment’s integral role in biopharmaceutical purification, where downstream steps still consume close to 60% of total drug-manufacturing costs Avantor. Heightened regulatory focus on product purity, rising adoption of continuous bioprocessing that needs high-flow resins, and widening therapeutic pipelines together lift demand. Capacity investments—such as Cytiva and Pall’s USD 1.5 billion multiphase expansion—are shortening regional supply gaps and reinforcing secure sourcing strategies. At the same time, developers are moving toward synthetic matrices to gain reproducibility, while natural agarose grades gain niche momentum under sustainability mandates.

Key Report Takeaways

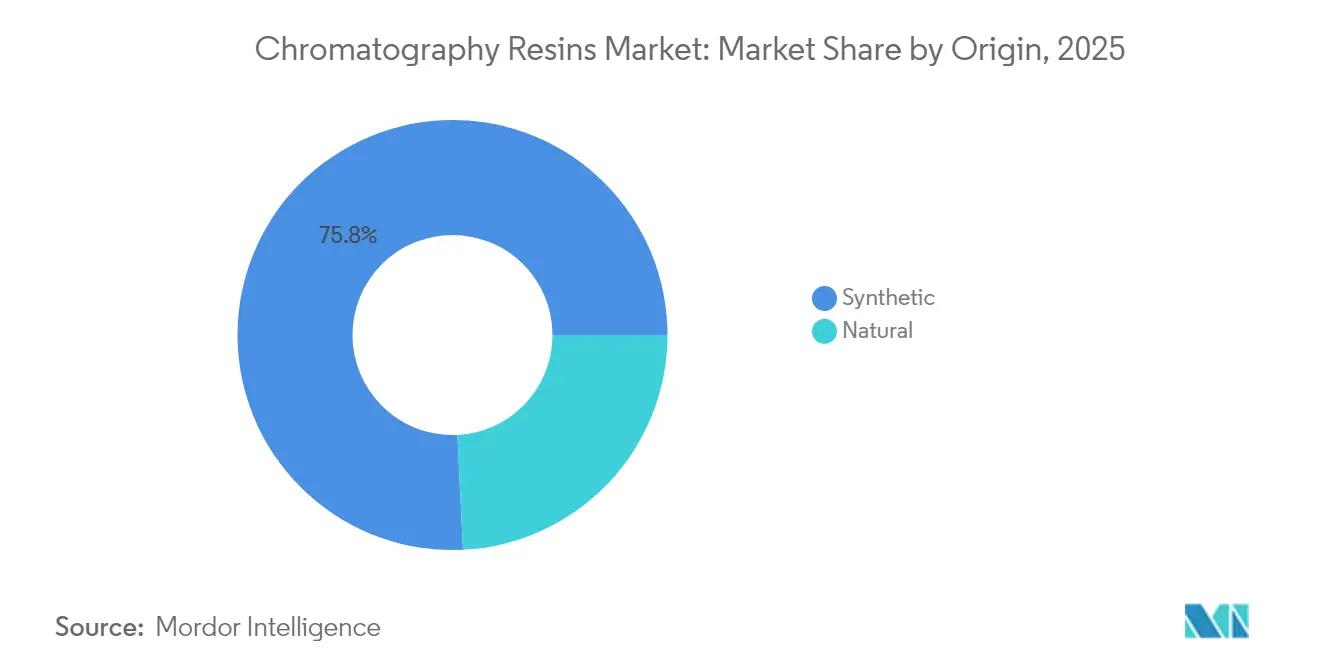

- By origin, synthetic-based resins held 75.78% of chromatography resins market share in 2025; natural-based grades post the quickest 8.48% CAGR to 2031.

- By product type, ion-exchange commanded 38.92% revenue share in 2025, whereas mixed-mode and multimodal formats expand fastest at 8.14% CAGR through 2031.

- By technology, affinity chromatography captured 46.74% share in 2025, while size-exclusion leads growth at 7.99% CAGR.

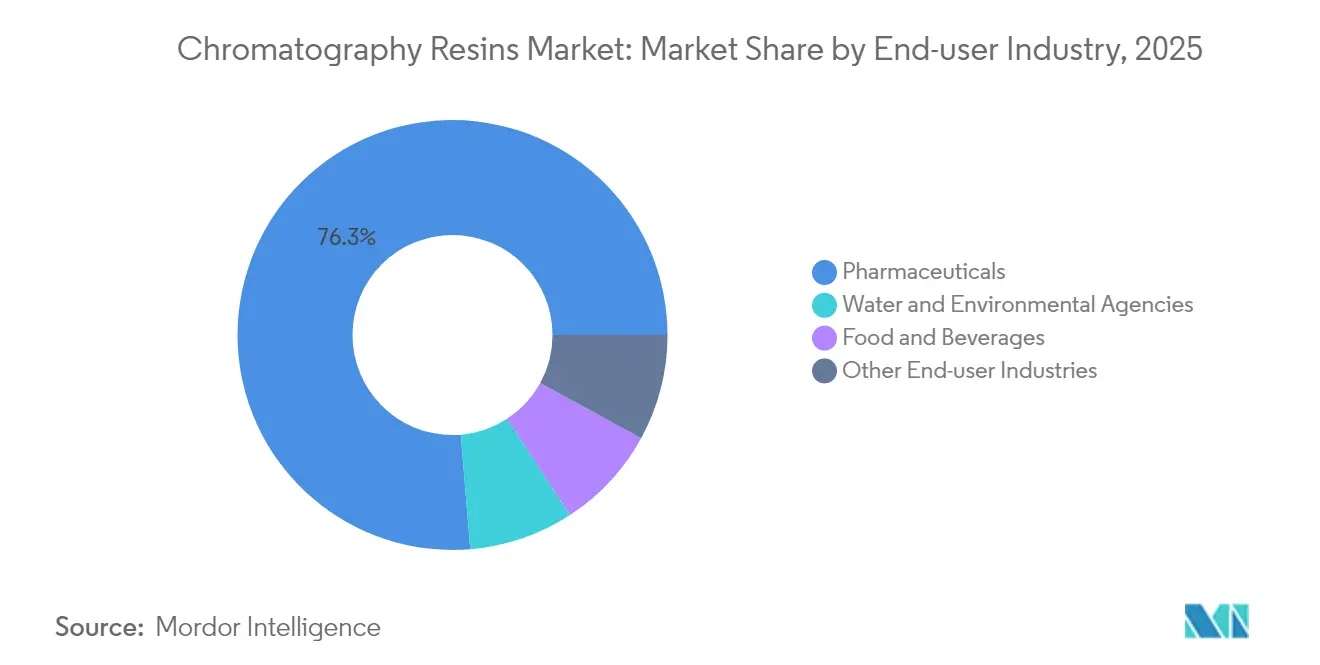

- By end-user, the pharmaceutical sector accounted for 76.32% of the chromatography resins market size in 2025 and is projected to grow at 8.41% CAGR.

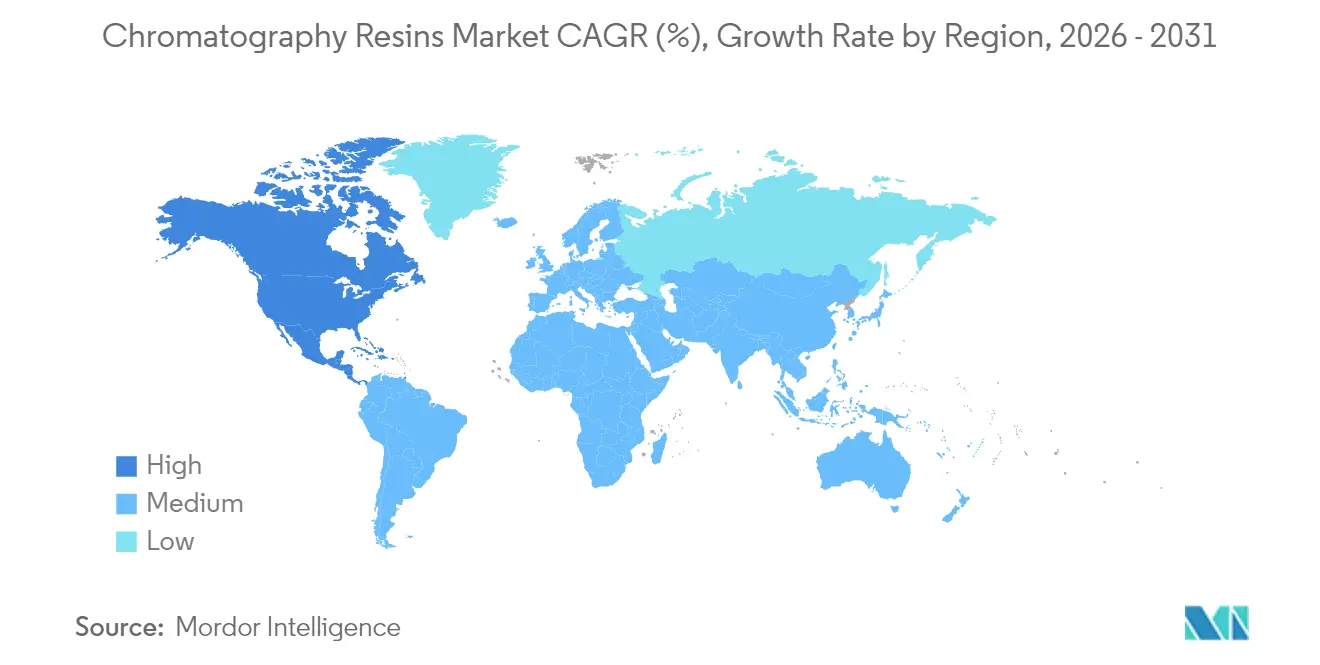

- By geography, North America dominated with 42.21% share in 2025 and is also the fastest-growing region at 8.37% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Chromatography Resins Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for monoclonal-antibody production | +2.1% | North America and Europe focus; global influence | Medium term (2-4 years) |

| Expanding vaccine pipelines in emerging markets | +1.8% | APAC core, spill-over to Latin America and MEA | Long term (≥ 4 years) |

| Transition toward single-use downstream systems | +1.4% | North America and EU; uptake in APAC | Short term (≤ 2 years) |

| Regulatory push for higher-purity biologics | +1.2% | Global, led by FDA and EMA | Medium term (2-4 years) |

| Need for high-flow resins in continuous bioprocessing | +0.9% | North America and EU manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Monoclonal-Antibody Production

Global mAb volumes keep climbing at a projected 13.23% CAGR to 2030, and resin consumption rises in parallel as antibody titers top 10 g/L, pushing Protein A beds to capacity limits. High-capacity alternatives such as Toyopearl GigaCap S-650M deliver dynamic binding above 90 g/L, more than doubling traditional media. Oncology indications account for 51% of therapeutic value, with autoimmune pipelines expanding fastest and broadening purification needs. North America retains 41.04% share of antibody output, yet Asia-Pacific advances at 13.24% CAGR, diversifying resin demand centers. In-vitro production now holds 78% of mAb supply, underscoring how downstream resin technology underwrites global access to biologics.

Expanding Vaccine Pipelines Across Emerging Markets

Post-pandemic capacity build-outs in India, China, Brazil and Indonesia keep vaccine demand buoyant, elevating need for resins that efficiently clear viral and plasmid impurities. Bio-Rad’s CHT Ceramic Hydroxyapatite captures more than 75% of influenza and dengue viral particles while trimming host proteins by 90%[1]Bio-Rad Laboratories, “CHT Ceramic Hydroxyapatite Performance Summary,” bio-rad.com. New ligands such as Repligen/Navigo’s spike-protein affinity resin exemplify purpose-built solutions for mRNA and viral-vector vaccines. Regulatory agencies from EMA to WHO now stipulate robust viral clearance studies, driving resin developers to validate higher selectivity and flow robustness for large-scale vaccine platforms.

Transition Toward Single-Use Downstream Systems

Demand for disposable chromatography hardware is rising as companies eliminate clean-in-place steps. GORE Protein Capture Devices show ten-fold higher productivity over packed columns without wash-down downtime. FDA guidance on disposable equipment, released in July 2022, clarifies qualification steps and accelerates adoption. Membrane adsorbers, in turn, reduce buffer use and fit seamlessly with continuous operations, while gamma-irradiated columns now sustain bioburden-free runs beyond 40 days. Although resin costs rise inside single-use cartridges, rapid turnaround and lower contamination risk offset expenses in multi-product plants.

Regulatory Push for Higher-Purity Biologics

Updated Q2(R2) analytical guidelines issued in March 2024 require deeper impurity profiling, thereby setting higher thresholds for chromatographic resolution FDA. EMA’s draft on solid-phase peptide synthesis spells out ligand cross-link density and extractables limits that directly govern resin qualification. WHO technical reports reinforce global alignment on raw-material quality, and ISPE guidance formalizes supplier audits—all of which heighten data-package requirements for every new resin lot. Consequently, suppliers invest in tighter process controls and extended CoAs to help users pass regulatory scrutiny.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High resin procurement and validation cost | -1.8% | Global, acute in emerging markets | Medium term (2-4 years) |

| Scarcity of skilled downstream-processing professionals | -1.2% | North America and EU, spreading to APAC | Long term (≥ 4 years) |

| Competition from disposable membrane chromatography | -0.9% | North America and EU manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Resin Procurement and Validation Cost

Protein A resin prices have climbed to USD 9,000-12,000 per liter, yet most products bind under 40 g/L, stressing budgets for both clinical and commercial runs. Lengthy lead times—often beyond 15 weeks—force firms to raise safety stocks and tie up working capital. Each supplier or lot change triggers comparability testing, extending timelines and requiring extensive documentation that inflates overall validation expenses. Smaller firms and emerging-market plants find it harder to absorb these costs, slowing domestic production scale-up.

Scarcity of Skilled Downstream-Processing Professionals

Manufacturing expansions have outpaced the talent pipeline, leaving a deficit of chromatography specialists able to develop robust methods and manage continuous systems. Automation and AI tools accelerate routine data review, yet process design, resin packing, and troubleshooting still demand experiential knowledge. Academic curricula are only gradually incorporating continuous bioprocessing modules, setting up a persistent skills gap that heightens operational risk and complicates tech-transfer timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Origin: Synthetic Dominance Drives Scalability

Synthetic-based materials represented 75.78% of 2025 revenue, reflecting manufacturers’ preference for lot-to-lot consistency and high mechanical strength. Such characteristics enable taller columns, faster flow, and straightforward scale-up, vital to the chromatography resins market where production cycles continue to shorten. In contrast, natural media—chiefly agarose—retain gentler chemistries that safeguard labile proteins, positioning them for niche vaccines and gene-therapy vectors. The natural segment’s 8.48% forecast CAGR signals renewed interest in renewable feedstocks and lower environmental footprints, especially in Europe where green- manufacturing incentives exist.

Adoption patterns illustrate a two-tier structure: multinationals install synthetic polymethacrylate beds for continuous antibody capture, whereas regional contract manufacturers expand capacity with agarose or cellulose for multi-product suites. The regulatory spotlight on adventitious-agent risk further pivots enterprise preference toward synthetics, yet biocompatibility concerns still pull natural grades into pediatric and cell-therapy pipelines. With both formats strengthening advanced ligand chemistries, competition will revolve less around base matrix and more around performance attributes such as dynamic capacity and alkaline stability in the chromatography resins market.

By Product Type: Ion-Exchange Leadership Faces Multimodal Challenge

Ion-exchange resins accounted for 38.92% of 2025 sales, cementing a decades-long role across capture, intermediate, and polishing stages. Their broad operating window, scalability, and relative affordability suit virtually every therapeutic protein. However, mixed-mode and multimodal media are projected to compound at 8.14% annually, because combined ionic, hydrophobic, and hydrogen-bond interactions allow single-step removal of aggregates and host-cell proteins, trimming buffer usage and skid footprint.

Protein A columns remain essential for IgG capture despite premium pricing, while hydrophobic-interaction units mitigate aggregation in continuous polishing. Size-exclusion devices fulfill buffer exchange or desalting without shear, an area where the chromatography resins market size for this niche is projected to widen steadily with a 7.99% CAGR. Ligand-coupled custom solutions are steadily entering pilot scale, driven by bispecific antibodies and viral vectors. Process-intensification roadmaps suggest multimodal beds will increasingly displace sequential ion-exchange-plus-HIC operations, underscoring shifting value pools inside the chromatography resins market

By Technology: Affinity Chromatography Maintains Capture Supremacy

Affinity platforms captured 46.74% of 2025 revenue, anchored by Protein A capture in mAb workflows. High flow-rate variants now exceed 65 g/L capacity while resisting NaOH cycles, reducing cost per gram processed. Ion-exchange technology keeps its multipurpose appeal, with newer giga-cap resins attaining 90 g/L dynamic capacities and fitting both bind-and-elute and flow-through modes. Size-exclusion is the quickest-expanding technology, mirroring the need for inline diafiltration and aggregate trimming ahead of final fill.

Hydrophobic-interaction chromatography remains critical for post-purification titer consolidation, and mixed-mode solutions blur traditional boundaries, adapting to hybrid batch-continuous operations. Custom affinity ligands advance most aggressively where standard Protein A cannot bind—such as Fc-free antibody fragments—illustrating how the chromatography resins market adapts to next-generation biologics. Automation integration across all technologies reduces operator-dependent variance and enables rapid resin-screening loops, shortening development timelines and enhancing reproducibility.

By End-user Industry: Pharmaceutical Sector Drives Dual Leadership

Pharmaceutical manufacturers consumed 76.32% of global volume in 2025 and are on track for an 8.41% CAGR, an alignment that uniquely positions the segment as both the largest and fastest-growing buyer cohort. Expanding pipelines of bispecific antibodies, ADCs, and gene-therapy payloads demand bespoke purification schemes, intensifying reliance on high-performance media within the chromatography resins market. Biotechnology labs invest in high-throughput resin-screening platforms to shave months off lead-candidate selection. Drug-production plants, in turn, scale resin pack formats to multi-column continuous capture, extracting efficiency gains across multisite networks.

Water and environmental agencies employ ion-exchange beds for nitrate and heavy-metal remediation, representing a small but stable slice of demand. Food and beverage processors use strong-acid cation resins for juice deacidification and whey purification, yet overall uptake remains secondary to pharmaceutical urgency. With vaccination and advanced therapy capacity building spreading to APAC and LATAM, pharmaceutical actors will continue dictating product specifications and delivery timelines across the chromatography resins market.

Geography Analysis

North America led with a 42.21% revenue contribution in 2025 and mirrors the fastest regional CAGR at 8.37% through 2031. Aggressive investments—Cytiva and Pall’s USD 1.5 billion program and Purolite’s new Pennsylvania agarose plant—aim to shorten lead times and insulate bioprocess supply chains. FDA analytical guidelines that tightened in 2024 cascade global expectations for resin consistency, anchoring North America’s status as regulatory reference hub.

Europe ranked second in value terms, combining long-standing GMP expertise with rising emphasis on sustainability. EMA process-validation rules force high-resolution separation and lean toward recyclable or lower-waste matrices. Investments such as Merck KGaA’s EUR 300 million research hub in Darmstadt and Tosoh Bioscience’s German expansion reinforce domestic supply. Green manufacturing incentives further nudge producers toward bio-based agarose and closed-loop solvent systems inside the chromatography resins market.

Asia-Pacific records the briskest structural expansion, spurred by Chinese, Japanese and Korean biologics programs as well as ASEAN vaccine initiatives. Tosoh’s new Yokkaichi plant exemplifies capacity alignment with regional demand. Policymakers funnel grants into local mAb and cell-therapy plants, raising consumption of high-capacity resins as multinationals localize production. India and Indonesia add volume in pandemic- readiness stockpiles, extending the customer base for continuous-flow compatible media.

South America sees gradual build-up in Brazil and Argentina, focusing on public-health vaccine needs that increasingly seek dual-ligand mixed-mode beds for viral clearance. The Middle East and Africa remain nascent but exhibit pockets of growth around Gulf state pharma clusters pursuing insulin, plasma, and vaccine self-sufficiency. Collectively, non-OECD regions contribute modest shares today yet represent double-digit growth prospects, underscoring the globalization of the chromatography resins market.

Competitive Landscape

The chromatography resins market remains moderately fragmented. Top multinationals—Cytiva, Merck KGaA, Thermo Fisher Scientific, Sartorius Stedim Biotech, and Bio-Rad Laboratories—combine synthesis, ligand design, and packed hardware, offering bundled platforms that lock in customers for multi-step processes. Danaher’s consolidation of Cytiva and Pall enables filter–resin bundles, eliciting antitrust scrutiny but also catalyzing integrated workflow innovation. Second-tier specialists such as Purolite and JSR Life Sciences cultivate high-capacity agarose or advanced polymethacrylate products, filling gaps in niche modalities like viral-vector purification.

Strategic moves lean toward capacity scale-up and technology acquisition. Repligen’s purchase of ligand innovator Tantti in July 2024 added bespoke affinity libraries to its OPUS column franchise[2]Repligen Corporation, “Acquisition of Tantti Enhances Chromatography Portfolio,” repligen.com . Avantor launched PROchievA to bolster supply flexibility for mAb capture workflows, addressing market bottlenecks. DuPont’s 2025 debut of AmberChrom TQ1 widened choices for oligonucleotide makers. Competitive intensity now centers on alkaline-stable ligands, flow-through multimodal designs, and columns pre-qualified for gamma irradiation.

Price pressure coexists with performance differentiation: while Protein A still commands premiums, alkaline stability and dynamic binding capacity gains are narrowing total-cost gaps. Automation-ready skids and RFID-tagged resin logistics add service layers. Smaller entrants find white spaces in cell-therapy unit operations, high-throughput ligand screening, and recyclable matrix chemistries aiming at circular-process credentials. Patent filings continue to rise around recombinant ligands and polymer grafting methods, signaling sustained R&D outlays and a vibrant innovation cycle across the chromatography resins market.

Chromatography Resins Industry Leaders

Cytiva

Merck KGaA

Thermo Fisher Scientific

Sartorius Stedim Biotech

Bio-Rad Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: DuPont has expanded its bioprocessing product range by introducing the AmberChrom TQ1 chromatography resin. This new resin is specifically designed to help purify oligonucleotides and peptide more efficiently.

- November 2024: Avantor has introduced PROchievA Protein A chromatography resin to support monoclonal-antibody production. This new chromatography resin helps solve capacity limitations in the manufacturing process.

Global Chromatography Resins Market Report Scope

The global chromatography resins market report includes:

By Origin

| Natural-based | Agarose |

| Cellulose | |

| Synthetic-based | Silica Gel |

| Aluminum Oxide | |

| Polystyrene | |

| Other Synthetic Based Resins |

By Product Type

| Protein-A |

| Ion-Exchange |

| Mixed-Mode and Multimodal |

| Hydrophobic-Interaction |

| Size-Exclusion |

| Ligand-Coupled Custom Resins |

By Technology

| Affinity Chromotography Resins |

| Ion-Exchange Chromotography Resins |

| Hydrophobic-Interaction Chromotography Resins |

| Size-Exclusion Chromotography Resins |

| Other Technologies |

By End-user Industry

| Pharmaceuticals | Biotechnology |

| Drug Discovery | |

| Drug Production | |

| Water and Environmental Agencies | |

| Food and Beverages | |

| Other End-user Industries |

By Geography

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

| By Origin | Natural-based | Agarose | |

| Cellulose | |||

| Synthetic-based | Silica Gel | ||

| Aluminum Oxide | |||

| Polystyrene | |||

| Other Synthetic Based Resins | |||

| By Product Type | Protein-A | ||

| Ion-Exchange | |||

| Mixed-Mode and Multimodal | |||

| Hydrophobic-Interaction | |||

| Size-Exclusion | |||

| Ligand-Coupled Custom Resins | |||

| By Technology | Affinity Chromotography Resins | ||

| Ion-Exchange Chromotography Resins | |||

| Hydrophobic-Interaction Chromotography Resins | |||

| Size-Exclusion Chromotography Resins | |||

| Other Technologies | |||

| By End-user Industry | Pharmaceuticals | Biotechnology | |

| Drug Discovery | |||

| Drug Production | |||

| Water and Environmental Agencies | |||

| Food and Beverages | |||

| Other End-user Industries | |||

| By Geography | By Geography | Asia-Pacific | China |

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN Countries | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| NORDIC Countries | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle-East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle-East and Africa | |||

Key Questions Answered in the Report

What is the 2026 value of the chromatography resins market?

The market stands at USD 2.74 billion in 2026, reflecting strong demand from biopharmaceutical manufacturing.

How fast will the chromatography resins market grow through 2031?

It is projected to expand at a 7.09% CAGR, reaching USD 3.86 billion by the end of the forecast period (2026-2031).

Which resin origin type dominates?

Synthetic-based resins hold 75.78% share owing to superior reproducibility and scalability.

Why is North America both the largest and fastest-growing region?

A high concentration of biologics plants, ongoing capacity investments, and stringent regulatory leadership propel an 8.37% regional CAGR.

What is the main cost restraint for manufacturers?

Protein A procurement and validation costs—often USD 9,000-12,000 per liter—remain the largest expense barrier.

Page last updated on: