Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 48.58 Billion |

| Market Size (2026) | USD 50.25 Billion |

| Market Size (2031) | USD 59.52 Billion |

| Growth Rate (2026 - 2031) | 3.44% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Countertop Market Analysis by Mordor Intelligence

The North America countertop market size is projected to expand from USD 48.58 billion in 2025 and USD 50.25 billion in 2026 to USD 59.52 billion by 2031, registering a CAGR of 3.44% between 2026 and 2031. Homeowners are choosing to improve rather than move, which channels spend toward kitchen-centric replacements and lifts mid-cycle upgrades across the North America countertop market. Ongoing silica safety rules reshape fabrication practices and speed the shift from legacy high-silica quartz toward low-silica and porcelain alternatives that reduce exposure risk while meeting performance targets in residential and commercial settings across the North America countertop market. Trade measures on quartz surface imports and domestic capacity additions are redefining sourcing strategies and project pricing dynamics in the North America countertop market. Canada’s elevated housing-starts base supports retrofit activity, though new construction shows signs of slower momentum into 2026, which keeps replacement-led demand central to the North America countertop market. Company moves to lower silica content and expand porcelain also reflect stronger compliance and specification preference trends that will persist through the forecast horizon in the North America countertop market.

Key Report Takeaways

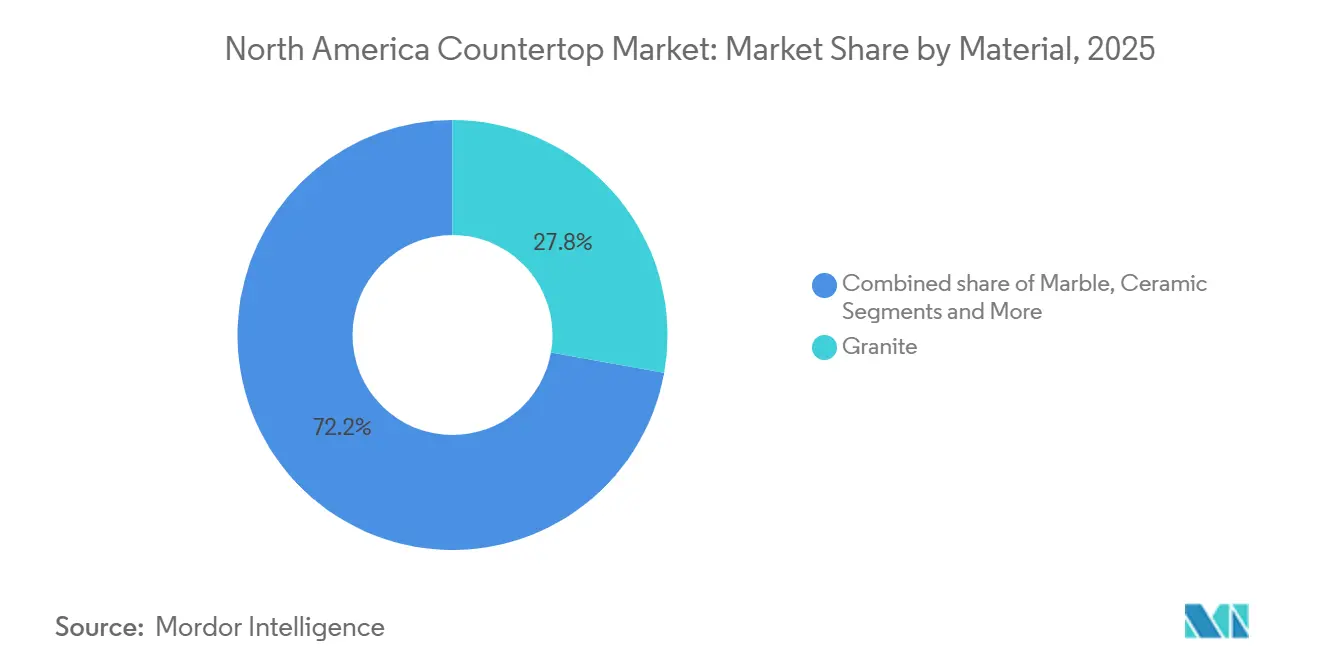

- By material, granite led with 27.81% revenue share of the North America countertop market in 2025, while ceramic surfaces are projected to expand at a 4.3% CAGR through 2031.

- By end-use sector, residential accounted for 71.13% share of the North America countertop market in 2025 and is projected to grow at a 4.1% CAGR to 2031.

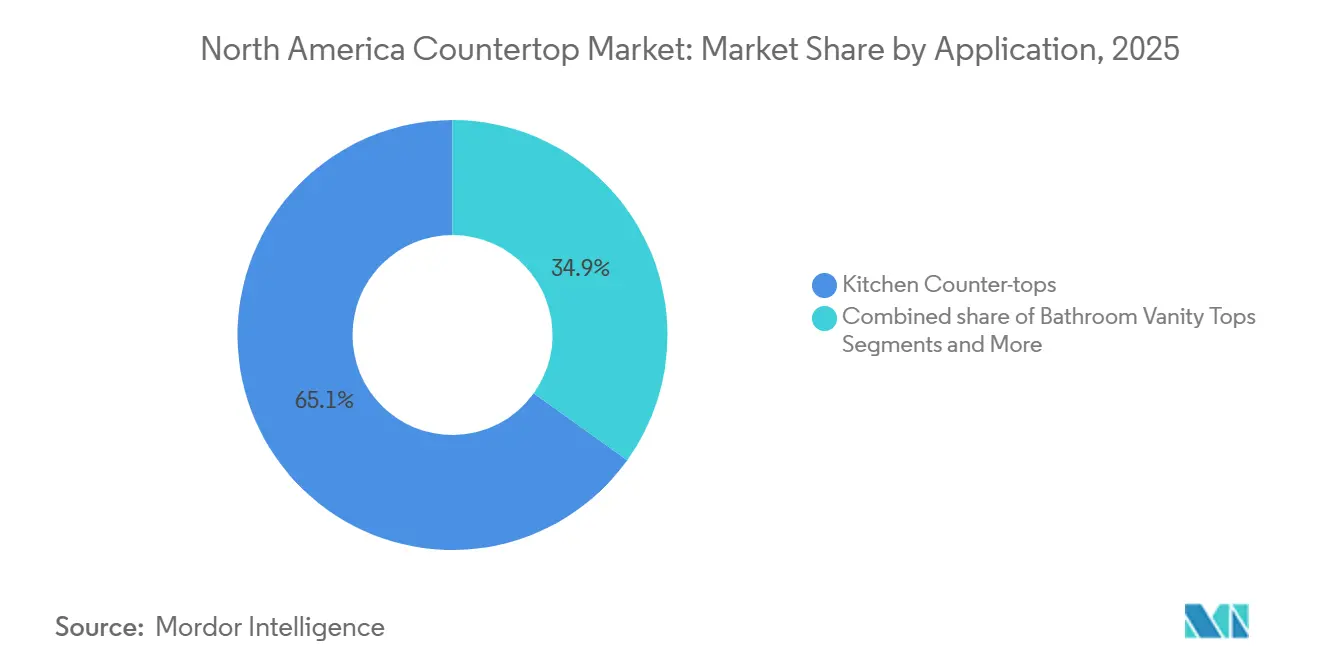

- By application, kitchen countertops accounted for a 65.18% share of the North America countertop market in 2025, while Others, including outdoor kitchens and hospitality bars, are the fastest-growing application at a 3.9% CAGR through 2031.

- By geography, the United States held an 84.24% share in 2025, while Mexico is projected to be the fastest-growing geography at a 4.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Countertop Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Remodeling Tailwind Amid Mortgage Lock-In and Deferred Moves | +1.2% | United States (California, Northeast), Canada (Ontario, Quebec) | Medium term (2-4 years) |

| Kitchen-Centric Replacements Dominate Installations | +0.8% | Global, with early gains in the US metropolitan areas and Canada | Short term (≤ 2 years) |

| Shift to Engineered Surfaces For Performance and Design | +0.6% | North America core, spill-over to Mexico (CDMX, Monterrey) | Medium term (2-4 years) |

| Fast-Rising Porcelain Slab For Outdoor And Commercial Use | +0.5% | US Sunbelt (Arizona, Texas, Florida), Mexico coastal zones | Long term (≥ 4 years) |

| Supply Reshoring and Trade Protection Reshape Sourcing | +0.3% | United States, secondary Canada | Medium term (2-4 years) |

| Low-Silica and Silica-Free Formulations Expand Addressable Market | +0.4% | California, with a national US follow-on | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Remodeling Tailwind Amid Mortgage Lock-In and Deferred Moves

Elevated borrowing costs reduce mobility and keep owners in place, which redirects household budgets toward updates that improve daily use and resale value across the North America countertop market. Remodeling spending indicators point to continued increases into 2026, aligning with a steady pipeline for countertop replacements in kitchens and baths that deliver high visual impact and durability benefits. This environment favors mid-ticket surfaces such as engineered quartz and porcelain, where uniform looks and non-porous performance reduce maintenance. It also creates an opening for upgraded natural stone in islands and high-heat zones where aesthetics and thermal resilience matter. Canada’s housing ecosystem supports similar improvement-first behavior after a strong base of 2025 housing starts, which helps smooth order volumes for fabricators and retailers that serve retrofit demand in the North America countertop market[1]Canada Mortgage and Housing Corporation, “Housing starts up 5.6% in 2025 from 2024,” CMHC, cmhc-schl.gc.ca. These factors collectively reinforce kitchen-centric replacement cycles as a structural pillar of growth.

Kitchen-Centric Replacements Dominate Installations

Countertops remain the most visible plane in kitchen projects, and upgrades often deliver the look-and-feel reset that homeowners want without the disruption of full cabinetry changes, keeping this category central to the North America countertop market. Engineered quartz continues to anchor mainstream demand where non-porous performance and consistent patterning support daily use. Premium brands have broadened colorways to emulate natural stone, bringing marble-like veining to price points suitable for mid-range renovations. Designers also specify porcelain more frequently for integrated indoor-outdoor aesthetics, which supports unified palettes across kitchens, patios, and entertainment spaces. That trend has gathered momentum alongside outdoor living investments, where resilient, low-care worktops suit multi-season use. As a result, fabrication shops continue to optimize cutting, edge profiles, and handling for both thickness extremes, from 2 mm large-format cladding to 12–20 mm kitchen-ready slabs, reflecting evolving material mixes in the North America countertop market.

Shift to Engineered Surfaces For Performance and Design

Engineered quartz remains a workhorse where stain resistance, predictable color, and minimal upkeep are the priority, while porcelain serves heat- and UV-exposed areas that challenge polymer-binder systems. Producers are updating collections with nature-inspired patterns and warm neutrals that connect to broader interior trends, helping sustain premium and mid-market demand in the North America countertop market. Silica safety rules have also accelerated product reformulation, with leading brands introducing lower-silica quartz lines to address fabrication exposure risk and to align with state-level enforcement, especially in California. These product shifts sit alongside investments in porcelain capabilities for indoor and outdoor areas, where UV stability and thermal resilience can outperform traditional engineered stone. Sustainability continues to influence selection, with recycled content and lower operational emissions now part of supplier value propositions that appeal to commercial and residential specifiers. The result is a balanced portfolio approach, where quartz, porcelain, and select natural stones fill distinct roles across budgets and performance needs in the North America countertop market.

Fast-Rising Porcelain Slab for Outdoor and Commercial Use

Porcelain’s technical profile, including near-zero water absorption and UV colorfastness, has made it a preferred outdoor surface in sun-exposed and freeze-thaw climates, which increases its share across the North America countertop market. In commercial hospitality and food-service, heat, scratch, and hygiene requirements align well with porcelain’s dense body, while easy cleaning supports fast turnover in restaurants and bars. Homeowners and designers also value porcelain’s continuous look in island waterfalls and feature walls, enabled by thin, large-format panels that minimize grout lines and reduce slab weight, which eases transport and installation in vertical applications. Outdoor living priorities have risen across North America, and owners want low-maintenance worktops that stand up to sun, temperature swings, and spills without sealing, which strengthens porcelain’s positioning in the North America countertop market. Total installed cost can sit above mid-tier quartz depending on region and fabricator specialization, but durability and lower upkeep often offset the upfront price for outdoor and heavy-use commercial settings. Combined, these attributes make porcelain a structural growth engine through the forecast, especially in the US Sunbelt and Mexico’s coastal metros.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Silica Exposure Regulation Raises Compliance Costs and Limits ES Adoption | -0.7% | California, with national US implications | Short term (≤ 2 years) |

| High Rates Dampen New Construction Budgets and Big-Ticket Upgrades | -0.5% | United States, Canada (Ontario, BC) | Short term (≤ 2 years) |

| Trade Actions And Safeguard Risks Create Supply/Price Volatility in Quartz | -0.4% | United States (import-dependent markets) | Short term (≤ 2 years) |

| Fabricator Labor Shortages And Compliance Burdens Constrain Capacity | -0.6% | North America-wide, acute in skilled-trade regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Silica Exposure Regulation Raises Compliance Costs and Limits ES Adoption

Cal/OSHA’s permanent standard and OSHA’s existing federal silica rules mandate wet methods, enhanced respiratory protection, exposure monitoring, and medical surveillance, which increase operating costs for fabricators and drive careful material selection in the North America countertop market. These requirements add complexity to engineered-stone processing and reduce tolerance for non-compliance, shifting demand toward low-silica formulations and porcelain that can reduce respirable crystalline silica exposure during cutting, shaping, and polishing. Industry associations and medical experts have elevated awareness, with 2026 initiatives that emphasize research and training to improve protection programs, align enforcement, and encourage best practices. Some manufacturers have adjusted operating footprints and product strategies in response to compliance and litigation risk, including transitions away from in-house quartz production and into diversified portfolios such as porcelain. Over time, these rules reshape supplier roadmaps, training investments, and equipment upgrades, which influence price and lead times across the North America countertop market.

High Rates Dampen New Construction Budgets and Big-Ticket Upgrades

Elevated interest rates have cooled certain new-home pipelines and stretched project budgets, which trim first-install countertop volumes and put emphasis on resilient remodeling channels within the North America countertop market. In Canada, housing starts remained high in 2025, yet momentum softened into late 2025 and early 2026, which reinforces the importance of replacement spend and steady retrofit activity for fabricators and retailers. Price-sensitive consumers continue to weigh premium quartz and porcelain installed costs against mid-tier options, creating a need for tiered product strategies and transparent value propositions. Where budgets tighten, owners often stage projects by prioritizing countertops and backsplashes, then sequencing cabinets or appliances later, which supports a healthy flow of small-to-mid scope jobs across the North America countertop market. These dynamics will continue to shape channel mix and margin management through the forecast period as borrowing costs normalize on a lag.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Ceramic Gains Ground as Silica and UV Concerns Redirect Budgets

Granite retained a 27.81% share in 2025, while ceramic surfaces, especially porcelain slabs, are the fastest-growing material with a 4.3% CAGR through 2031, reflecting a shift toward UV-stable, low-maintenance options in the North America countertop market. Porcelain’s dense body and near-zero water absorption suit outdoor kitchens and commercial hospitality tops where sun, rain, and temperature swings challenge other surfaces. Designers value the ability to wrap islands, walls, and furniture in continuous looks using thin, large-format panels, which reduces grout lines and achieves a seamless effect. Engineered quartz continues to set the benchmark for non-porous, stain-resistant daily use with updated designs that emulate marble and warm neutrals, keeping it central to mid-market renovations. Heightened silica safety enforcement in California and broader OSHA compliance requirements nudge specifiers toward low-silica quartz families and porcelain, aligning project choices with safer fabrication methods in the North America countertop market. Solid surface remains a viable option where seamless joints, repairability, and hygiene are the priority, and improvements in sustainability credentials add appeal for environmentally focused projects.

The North America countertop industry now blends these attributes into tiered material strategies by room and exposure conditions. Porcelain leads where direct sun, grills, and variable weather are factors, while engineered quartz dominates interior worktops requiring uniform colors and minimal upkeep. Granite preserves a loyal base in high-heat areas and statement islands, often as part of mixed-material kitchens that combine contrasting surfaces. Manufacturers continue to refresh quartz and solid-surface lines with new colors and recycled content, which addresses Look Sustainability briefs in residential and commercial specifications. With silica regulations raising the compliance bar for engineered stone, low-silica formulations reduce exposure risks and can simplify respiratory requirements at the fabrication stage, which helps shops manage training and equipment investments. Together, these dynamics explain why ceramic’s growth outpaces the category average while granite and quartz maintain scale positions that continue to anchor the North America countertop market.

By End-Use Sector: Residential Upgrades Drive Growth, Yet Commercial Hospitality Spots Porcelain’s Edge

Residential applications commanded 71.13% in 2025 and are projected to grow at a 4.1% CAGR through 2031, reflecting the improve-in-place cycle that underpins the North America countertop market size across the forecast. Owners favor high-impact, moderate-cost replacements that refresh daily spaces, and countertops lead that short list due to visible transformation and practical durability. With remodeling spend expected to remain firm into 2026, residential specifications continue to favor engineered quartz for non-porous, easy-clean use, complemented by porcelain for heat and UV-exposed zones in connected indoor-outdoor. Brands keep designs fresh with marble-inspired options, vein-rich neutrals, and warmer palettes that match cabinet and flooring trends. Meanwhile, safety-focused shifts in quartz composition and processing support contractor acceptance and align with state and federal silica rules, which influence bid strategies and timeline planning in the North America countertop market.

Commercial projects place a premium on lifecycle cost and hygiene. Porcelain’s UV stability, heat resistance, and dense body make it attractive for hospitality bars, quick-serve counters, and hotel bathroom surfaces that must stand up to heavy daily use. Seamless large-format cladding on bars and reception desks is easier to achieve with thin porcelain panels, which shortens install time and reduces joints relative to tile. Solid surface remains relevant in commercial healthcare and office breakrooms where seamless seams and thermosetting fabrication allow integrated sinks and coves, while sustainability gains support spec goals. As material costs, trade policies, and compliance spending evolve, commercial specifiers spread risk across quartz, porcelain, and solid surface based on performance-in-use, lead time, and maintenance profile across the North America countertop industry. These preferences stabilize demand in retrofit-heavy segments while enabling resilient design options for high-traffic environments.

By Application: Outdoor/Hospitality Installations Surge as Porcelain Sidesteps UV and Heat Constraints

Kitchen countertops held 65.18% in 2025, while Others, including outdoor kitchens and hospitality bars, are projected to grow at a 3.9% CAGR through 2031, supported by rising outdoor living investment and high-traffic commercial needs in the North America countertop market. Porcelain leads outdoors where direct sun, rain, and temperature swings require UV-stable, low-absorption, and heat-resistant worktops that do not require sealing or special cleaners. Large-format panels also deliver seamless aesthetic lines on islands and backsplashes, with thickness profiles that allow designers to manage weight and edge treatments across vertical and horizontal applications. In hospitality, porcelain’s dense body supports sanitation and rapid turnover, while heat and scratch resistance fit bar tops and service counters that experience heavy wear. Installed cost can be higher than mid-tier engineered stone, but it is often defended by durability and reduced upkeep in these use cases.

Bathroom vanity tops remain an important runner-up application, where engineered quartz and solid surface dominate for seamless looks, integrated sinks, and easy-clean performance. Brands have refreshed these lines with nature-inspired colors and recycled content that align with sustainability targets and occupant wellness narratives. Outdoor living is also an area where owners increasingly seek appliance integration, which raises the bar for worktops around grills, pizza ovens, and refrigeration, and further supports porcelain’s growth trajectory in the North America countertop market. These use-case distinctions ensure all three core materials remain relevant, with porcelain taking the lead in sun and heat, quartz in general-purpose kitchens and vanities, and solid surface in seamless, hygiene-sensitive environments.

Geography Analysis

The United States anchored the region with 84.24% of the North America countertop market share in 2025, while Mexico is projected to be the fastest-growing geography at a 4.45% CAGR through 2031, which reflects differing cycles and adoption curves across the region. In the US, remodeling outlays are set to remain firm into 2026, which supports countertop replacement projects that emphasize visual renewal and non-porous performance for daily use. Silica regulations have elevated compliance investments, so specifiers are leaning into low-silica quartz and porcelain where the fabrication approach and exposure controls align with state-level rules. Trade actions, including continued antidumping and countervailing measures on India, Türkiye, and China for quartz surfaces, also influence landed cost and design availability, which in turn affect product mix by channel and region. Domestic manufacturing expansions and investments in porcelain distribution and finishing capacity aim to improve supply resilience and shorten lead times as the North America countertop market advances.

Canada’s base of 2025 housing starts remained among the highest on record, which underpins steady retrofit volumes and countertop demand into 2026, even as momentum cooled later in the year. Fabricators continue to manage project pipelines that skew to kitchens and baths, with engineered quartz dominant for non-porous performance and porcelain rising in outdoor and hospitality specifications. Compliance with silica regulations is a shared focus with the United States, and training, wet-cutting setups, and ventilation upgrades remain priorities for shops that process engineered stone. Commercial projects track to resilient sectors like hospitality and healthcare, where porcelain and solid surface address hygiene and durability requirements, supporting a balanced mix within the North America countertop market. Tiered material strategies are common, pairing granite or porcelain island tops with engineered quartz perimeter runs, which stretches budgets while keeping maintenance low.

Mexico shows rising interest in modular kitchens and contemporary stone-forward designs in major metros such as Mexico City, Monterrey, and Guadalajara, which supports premium looks at tailored price points in the North America countertop market. Local suppliers highlight quartz, granite, and marble for residential kitchens, with a growing share of buyers seeking financing or staged installations to align with household budgets. Porcelain is also gaining traction for outdoor and hospitality spaces due to its resistance to heat, UV, and stains, a fit for coastal climates and year-round entertaining. With design content from local fabricators and retailers influencing choices, consumers often weigh aesthetics, durability, maintenance, and cost over pure brand position, which leads to a diversified mix of quartz, porcelain, granite, and marble purchases in the North America countertop market.

Competitive Landscape

The North America countertop market features a balanced mix of vertically integrated brands, global producers using third-party manufacturing, large distributors, and regional fabrication specialists, with no single company controlling a dominant share. Cosentino has announced a multi-year investment cycle that includes a Jacksonville, Florida, facility to improve service levels and support scale demand near key US markets, while maintaining a broad portfolio spanning engineered quartz and ultra-compact surfaces[2]Cosentino Group, “Cosentino Achieves a Consolidated Turnover of 1,464 Million Euros and Will Invest More Than 430 Million in the Period 2025–2027,” Cosentino Group, cosentino.com. Cambria continues to emphasize American manufacturing and premium design, expanding colors and showcasing fabrication-friendly formats across kitchen and bath use cases in the North America countertop market[3]Cambria, “Press Room: KBIS 2026,” Cambria Company LLC, cambriausa.com. MSI Surfaces is investing in design development and distribution capacity, highlighting domestic production in select categories and a diversified portfolio that includes quartz, porcelain slabs, and complementary surfaces.

Caesarstone completed the closure of its Bar-Lev facility in Israel in December 2025 and transitioned quartz production to global third-party partners, targeting annualized savings and a portfolio that includes porcelain growth initiatives. LX Hausys added new Viatera quartz colors manufactured in Georgia, which advances US-made offerings for residential and commercial specs. DuPont’s Corian business continues to evolve with lower operational emissions and refreshed solid-surface collections that support seamless, hygienic installations in healthcare, hospitality, and multi-family.

Strategic patterns point to three durable themes across the North America countertop market. First, silica risk mitigation through product reformulation and compliance-forward fabrication practices is now a core capability, with California’s permanent standard shaping national playbooks for engineered-stone shops. Second, portfolio diversification into porcelain slabs supports heat and UV-exposed applications and deepens participation in commercial hospitality and outdoor living. Third, sourcing resilience through domestic production, multiple country origins, and trade compliance has become a differentiator as AD/CVD continuations and related measures influence quartz availability and cost. These moves collectively reinforce a steady cadence of design refreshes, broader material choice, and risk-aware project delivery across the North America counter-top market.

North America Countertop Industry Leaders

MSI Surfaces

Cosentino

LX Hausys

Caesarstone

Cambria

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: MasterBrand announced an all-stock merger with American Woodmark, targeting USD 90 million in annual cost savings and bolstering integrated kitchen-solution offerings.

- April 2025: Lowe’s completed its USD 1.325 billion purchase of Artisan Design Group, adding 132 distribution centers and more than 3,200 installers to deepen its Pro builder network.

- January 2025: California’s OSHA adopted permanent respirable crystalline-silica rules for engineered-stone fabrication, mandating engineering controls and medical surveillance for exposed workers.

- January 2025: Vadara Quartz, a prominent player in the quartz industry, has set its sights on the United Kingdom, marking a significant step in its international expansion. This move not only underscores Vadara's ambition to extend its footprint beyond North America but also hints at potential shifts in supply chain dynamics and competitive positioning in the market.

North America Countertop Market Report Scope

This report aims to provide a detailed analysis of the North American countertops market. It focuses on the market dynamics, emerging trends in the segments and regional markets, and insights on various product and application types. Also, it analyzes the key players and the competitive landscape in the North American countertops market.

By Material

| Marble |

| Granite |

| Engineering Stone (quartz) |

| Ceramic |

| Cast Polymer/Solid Surface Countertops |

| Other Materials |

By End-Use Sector

| Residential |

| Commercial |

By Application

| Kitchen Counter-tops |

| Bathroom Vanity Tops |

| Others (Outdoor Kitchens, Hospitality Bars, etc.) |

By Country

| United States |

| Canada |

| Mexico |

| By Material | Marble |

| Granite | |

| Engineering Stone (quartz) | |

| Ceramic | |

| Cast Polymer/Solid Surface Countertops | |

| Other Materials | |

| By End-Use Sector | Residential |

| Commercial | |

| By Application | Kitchen Counter-tops |

| Bathroom Vanity Tops | |

| Others (Outdoor Kitchens, Hospitality Bars, etc.) | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the size and growth outlook for the North America countertop market through 2031?

The North America countertop market is projected at USD 50.25 billion in 2026 and expected to reach USD 59.52 billion by 2031, reflecting a 3.44% CAGR from 2026 to 2031.

Which materials are gaining the most traction in North America countertops?

Engineered quartz remains the mainstream choice for non-porous performance, while porcelain is the fastest riser for outdoor and commercial settings due to UV and heat resistance.

How are silica safety regulations affecting product and fabrication choices?

Cal/OSHA’s permanent rules and OSHA standards increase compliance needs, steering demand toward low-silica quartz and porcelain, and prompting investments in wet methods and respiratory protection programs.

Which end-use segments are leading demand in North America?

Residential leads with 71.13% share in 2025 and is projected to grow at a 4.1% CAGR to 2031, driven by improve-in-place remodeling cycles that prioritize kitchens and baths.

What applications are growing fastest within countertops?

Others, including outdoor kitchens and hospitality bars, are the fastest-growing application at a 3.9% CAGR through 2031, supported by porcelain’s strong outdoor and high-traffic performance.

How are trade measures shaping the North America countertop market?

Continued antidumping and countervailing orders on select quartz imports impact cost and design availability, while domestic investments and sourcing diversification improve resilience across the region.

Page last updated on: