Train HVAC Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 15.61 Billion |

| Market Size (2031) | USD 18.45 Billion |

| Growth Rate (2026 - 2031) | 3.40% CAGR |

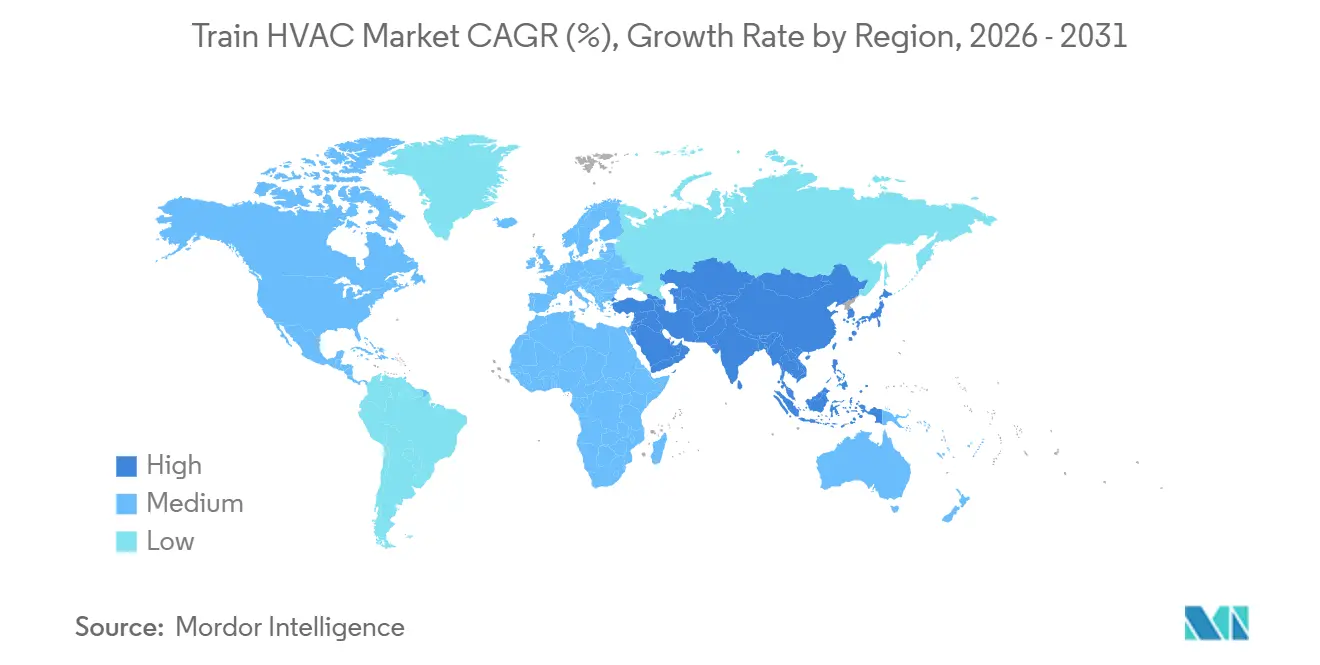

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Train HVAC Market Analysis by Mordor Intelligence

The train HVAC market was valued at USD 15.10 billion in 2025 and estimated to grow from USD 15.61 billion in 2026 to reach USD 18.45 billion by 2031, at a CAGR of 3.40% during the forecast period (2026-2031). This progression underscores a maturing phase in which value stems less from sheer unit additions and more from technology shifts—especially low-GWP refrigerants, IoT-enabled predictive maintenance, and energy-storage-assisted heat-pump architectures that significantly trim energy use compared with legacy R134a systems. Operators focus on regulatory readiness ahead of the 2027 F-Gas caps, real-time diagnostic uptime, and modular retrofits that maintain weight balance. Component demand patterns favor intelligent controls and inverters, even as vapor-cycle platforms dominate installed fleets. Competitive dynamics remain mid-tier concentrated: large thermal-management suppliers leverage cross-industry know-how, while specialist entrants differentiate through refrigerant expertise and secured semiconductor pipelines.

Key Report Takeaways

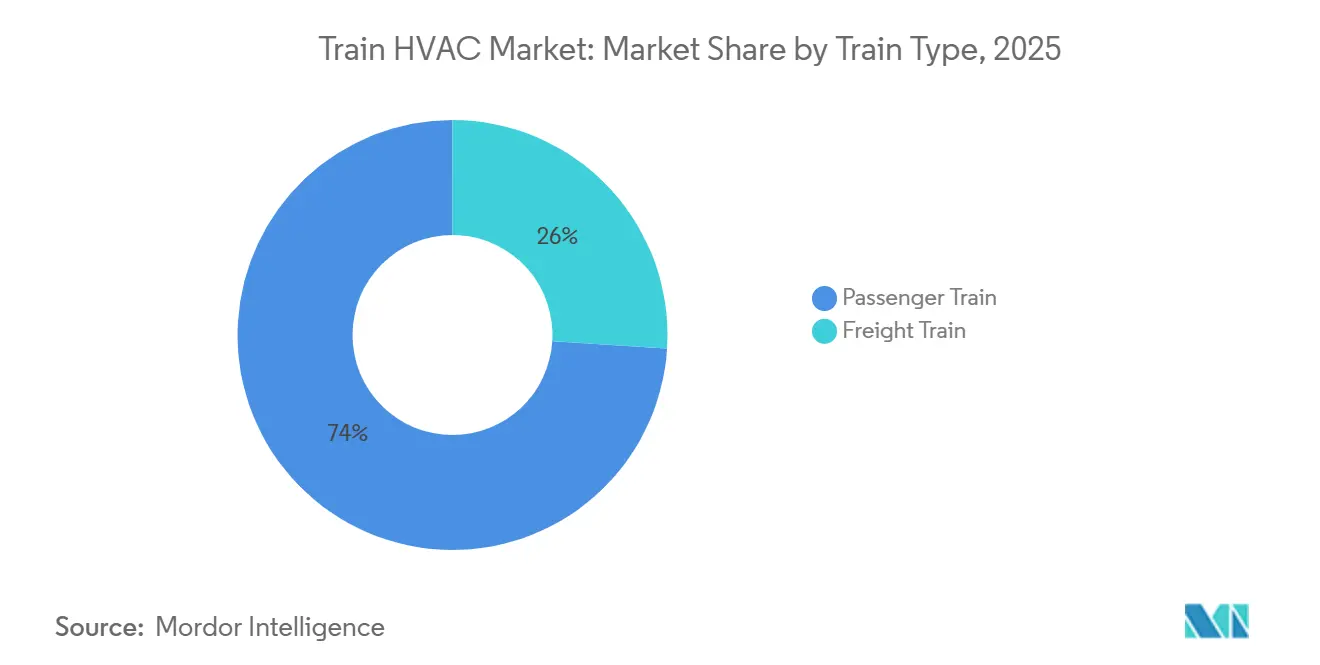

- By train type, passenger services led with 74.01% revenue share in 2025, whereas freight applications are projected to expand at a 4.75% CAGR to 2031.

- By installation type, roof-mounted systems accounted for 60.12% of the train HVAC market size in 2025, while split/car-body designs record the highest projected CAGR at 6.13% through 2031.

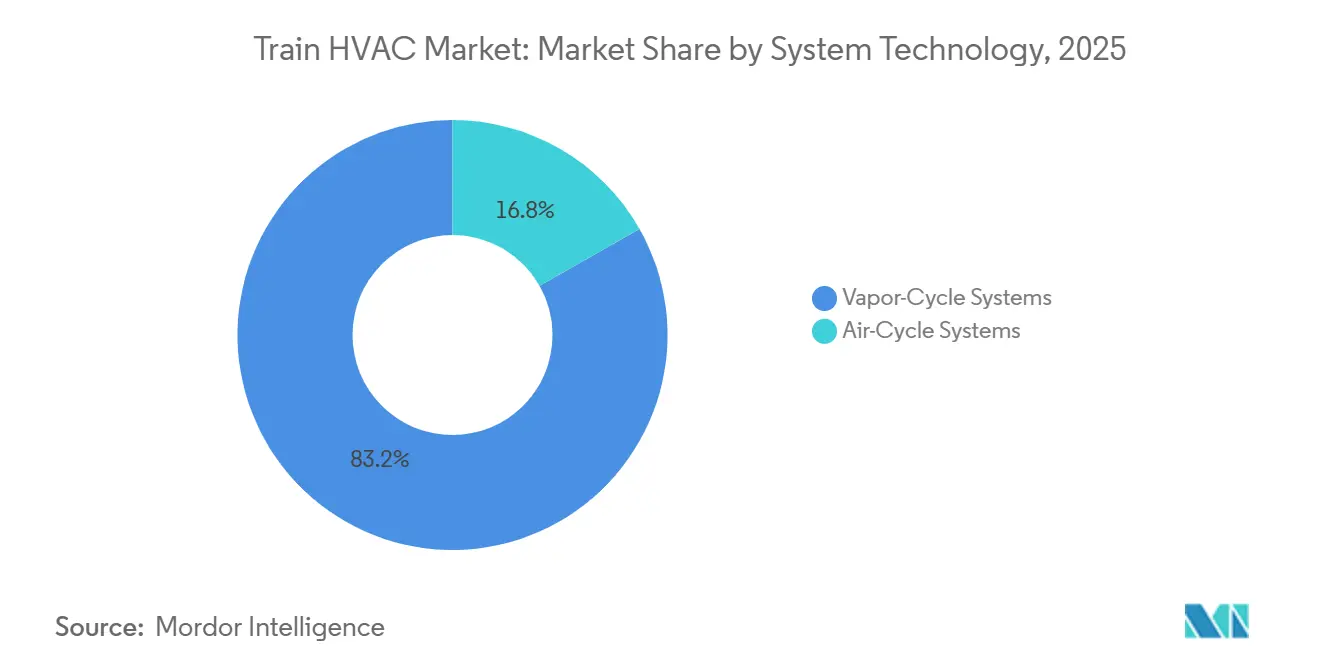

- By system type, vapor-cycle platforms accounted for 83.15% of the train HVAC market in 2025; air-cycle solutions are advancing at a 5.72% CAGR through 2031.

- By component, compressors accounted for 29.33% of revenue in 2025, but controls and inverters are forecast to register the fastest 6.85% CAGR from 2026-2031.

- By geography, Asia-Pacific held 49.25% of the train HVAC market share in 2025 and is expected to post the fastest regional CAGR at 5.01% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Train HVAC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-Funded Rail Network Expansion | +0.8% | Asia-Pacific, Middle East, and Africa | Medium term (2-4 years) |

| Growth in Passenger-Experience Standards | +0.6% | North America, EU, Asia-Pacific | Short term (≤ 2 years) |

| IoT-Enabled Predictive-Maintenance Retrofits | +0.5% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Thermal-Comfort and IAQ Regulations | +0.4% | EU core, North America, developed Asia-Pacific | Long term (≥ 4 years) |

| On-Board Energy-Storage Integration | +0.4% | Asia-Pacific and EU leading deployment, North America following | Short term (≤ 2 years) |

| Shift to Low-GWP Refrigerants | +0.3% | EU first, voluntary in North America and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-Funded Rail-Network Expansion

Massive public outlays unlock rolling-stock orders that explicitly budget for advanced HVAC. India earmarked significant investments for coach modernization, with HVAC absorbing a significant portion of each carriage’s budget. Sovereign programs in the UAE likewise bundled HVAC units into Etihad Rail’s 2030 fleet plan, elevating climate control from an optional amenity to mandated infrastructure. EU funding under the Connecting Europe Facility further accelerates orders by linking grant eligibility to HVAC interoperability. These capital flows spur predictable multiyear demand and reward suppliers possessing multi-regional certification portfolios.

Rapid Growth in Passenger-Experience Standards

Operators now monetize micro-climate precision. JR East’s E8 rolling stock introduced zone-based cooling that adapts to occupancy shifts, driving premium ticket surcharges on long-distance routes. European carriers validate a similar pricing uplift, confirming that thermal consistency—not absolute temperature—is the top determinant of customer satisfaction. Intelligent zoning algorithms trim energy by up to 35%, closing the payback gap for premium HVAC hardware.

Stricter Thermal-Comfort and IAQ Regulations

Regulators embed air-quality metrics into rolling-stock standards. EN 14750 now stipulates six fresh-air exchanges per hour and CO₂ below 1,000 ppm at peak loads. Deutsche Bahn recorded a notable drop in passenger complaints after upgrading to compliant units despite a one-time cost uptick. Conformance requires integrated particulate, humidity, and gas sensors, creating entry barriers for firms lacking multi-variable control IP.

Shift to Low-GWP Refrigerants to Meet 2027 F-Gas Caps

Liebherr and Stadler validated R290 passenger-car installations slated for Nordic Express deliveries in early 2025, demonstrating the viability of natural refrigerants in harsh climates. EU HFC phase-downs raise input prices significantly, incentivizing early migration. CO₂ transcritical prototypes demonstrate energy savings but hinge on scarce integration expertise. Vendors mastering propane safety protocols secure a head start in upcoming tenders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and OPEX | -0.7% | Global, cost-sensitive markets | Short term (≤ 2 years) |

| Space and Weight Limits | -0.5% | North America, EU | Medium term (2-4 years) |

| Global Shortage of Rail Technicians | -0.4% | Global, severe shortages in North America and developed EU markets | Long term (≥ 4 years) |

| Semiconductor Supply Volatility | -0.3% | Global, supply chain concentration in APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High CAPEX and OPEX of Advanced HVAC Units

Sophisticated rail-grade systems command price premiums, pushing life-cycle costs per passenger car toward high levels. Retrofit budgets continue to inflate as structural rewiring and downtime add a significant share to hardware costs. Smaller regional operators lack the analytic models to monetize downstream fuel and maintenance savings, delaying adoption even when payback horizons fall below six years.

Space / Weight Limits in Legacy Rolling-Stock Retrofits

Before 2010, EU passenger cars had a limited roof load capacity. In contrast, modern heat-pump packages, including batteries, are significantly heavier. Reinforcing these cars can be a substantial expense, often exceeding the cost of the HVAC hardware. Freight locomotives face cab-volume limits that cap cooling output, forcing performance trade-offs unless operators fund costly frame modifications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Train Type: Freight Growth Gains Momentum

Passenger fleets dominated the train HVAC market, accounting for 74.01% in 2025, reflecting decades-old comfort mandates. The freight segment’s 4.75% CAGR through 2031 outpaces the aggregate as labor rules now compel 8-hour cab-comfort compliance. Improvements reduce fatigue incidents, while shutting down idling main engines saves notable gallons of diesel per hour, encouraging railroads to retrofit cabs despite tight capital budgets.

Modern freight tenders increasingly specify integrated HVAC-APU modules that operate off-engine, cutting annual fuel use per locomotive. Vendors market these savings alongside crew-retention benefits in a labor-scarce environment. As intermodal corridors elongate travel windows, HVAC uptime becomes mission-critical, propelling unit sales beyond historical fleet-replacement cycles.

By Installation Type: Split Systems Unlock Retrofit Flexibility

Roof-mounted units accounted for 60.12% of 2025 revenue, as OEM-delivered rolling stock adheres to a familiar architecture. Yet split/car-body rigs surge at a 6.13% CAGR because they bypass roof load limits and enable staged maintenance. European refurbishments reveal lower life-cycle service expense when compressors and condensers slide out individually for overhaul.

Projects on 1990s-era EMUs are especially receptive; avoiding roof reinforcement can reduce high per-car retrofit costs. Split adoption aligns with predictive-maintenance rollouts, allowing technicians to swap condition-flagged modules without sidelining entire coaches and injecting additional savings into operators’ total-cost models.

By System Technology: Air-Cycle Options Target High-Speed Rail

Vapor-cycle designs maintained an 83.15% slice of the train HVAC market in 2025, anchored by mature tooling and parts networks. Air-cycle platforms are accelerating at a 5.72% CAGR, appealing to operators running at speeds above 300 km/h, where vibration stresses refrigerant loops. JR Central reports significant maintenance savings thanks to the absence of compressors and HFC leak points in air-cycle units.

Energy efficiency remains weaker than best-in-class vapor-cycle heat pumps, limiting uptake to premium corridors where downtime penalties dwarf electricity bills. Suppliers with aerospace pedigrees leverage existing turbomachinery IP to refine these niche systems and command premium pricing.

By Component: Intelligence Migrates to Controls and Inverters

Compressors still represented 29.33% of revenue in 2025, but the fastest value pool—forecast at 6.85% CAGR—lies in inverter drives and control electronics that orchestrate variable-speed cooling. Machine-learning algorithms inside modern inverters adjust fan curves, compressor RPM, and damper positions to cut energy draw without compromising cabin conditions [1]“Digital Inverter Drive White Paper,” Siemens Mobility, mobility.siemens.com.

Semiconductor scarcity challenges scale-up. Rail-grade SiC devices survive -40 °C to +85 °C ranges yet originate from a narrow supplier base, stretching component lead times to 12-16 weeks and inflating working capital. Makers able to lock multiyear chip allocations defend margins and delivery reliability—a differentiator in tender scoring.

Geography Analysis

Asia-Pacific retained 49.25% of global revenue in 2025 and is projected to post a 5.01% CAGR to 2031 as India outfits 40,000 AC coaches, and China extends high-speed mileage past 45,000 km [2]“AC Coach Deployment Program,” Indian Railways, indianrailways.gov.in. Thermal comfort is especially market-making in equatorial zones; Indian tenders assign a notable share of carriage budgets to HVAC, recognizing comfort as a ridership lever against low-cost airlines.

Europe contributes a steady volume as regulatory triggers—chiefly the 2027 F-Gas quota shrink—pull forward replacement demand. German S-Bahn orders totaling 1,350 R290 systems underscore early compliance moves. EU grants stipulate interoperability, nudging operators toward network-wide standardization that amplifies supplier scale effects.

North America focuses on freight locomotive upgrades, anchored in crew-retention economics and emissions mandates. The Federal Railroad Administration pilots waste-heat HVAC recovery prototypes to slash diesel use, an early sign of future subsidies. The Middle East fast-tracks high-capacity lines through desert climates—Etihad Rail’s order evidences the need for robust HVAC sealing against sand ingress. Africa and South America remain smaller but are targeted by vendors offering ruggedized, cost-optimized units for mining, rail, and premium intercity services.

Competitive Landscape

The train HVAC market shows moderate consolidation. Thermo King, Liebherr, and Mitsubishi Electric translate automotive and commercial-cooling pedigree into rail-grade reliability, giving them first call on multiyear fleet contracts. Their depth in refrigerant R&D helps operators navigate propane and CO₂ transitions faster than niche competitors.

Contracts are increasingly performance-based; Liebherr’s 550-unit Kazakhstan deal bundles ten-year maintenance alongside hardware, locking in after-sales revenue[3]“Kazakhstan 550-Unit Contract,” Liebherr Transportation Systems, liebherr-transportation.com. IoT connectivity becomes table stakes; suppliers pair hardware with analytics portals that predict filter clogs and compressor wear, monetizing software subscriptions. Those lacking semiconductor procurement leverage face project delays, amplifying buyer preference for vertically integrated incumbents.

White-space innovation clusters around battery-supported heat-pump HVAC. Companies combining traction-battery modules with climate systems capture synergies that few pure HVAC houses can duplicate. As rolling-stock builders adopt turnkey electrification, control of these hybrid blocks will shape competitive pecking orders through 2030.

Train HVAC Industry Leaders

Thermo King Corporation (Trane Technologies)

Liebherr-Transportation Systems

Mitsubishi Electric Power Products, Inc.

MERAK (Knorr-Bremse AG)

Siemens Mobility

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Alstom inaugurated a cutting-edge facility for the overhaul and repair of train components at its Crewe Works. This facility boasts a modern area dedicated to refurbishing heating, ventilation, and air conditioning (HVAC) units, along with a suite of new offices, marking a significant enhancement to Cheshire town's historic site.

- September 2025: Subros Ltd clinched an INR 52.18 crore (~USD 6.11 million) deal with Indian Railways’ Banaras Locomotive Works (BLW) in Varanasi. The contract, spanning three years, focuses on the annual maintenance of air-conditioning systems in locomotive driver cabins.

- August 2025: Stadler and Liebherr finalized delivery of 80 saloon, 80 heat-recovery, and 40 cab R290 units for 20 Finnish FLIRT trains, with shipments running from Sept 2024 to Dec 2026.

- July 2025: Liebherr China shipped the first of 550 HVAC systems for KTZ sleeper and couchette coaches under a five-year supply pact.

Global Train HVAC Market Report Scope

The scope includes segmentation by train type (passenger train and freight train), installation type (roof-mounted systems, under-floor systems, and split/car-body systems), system technology (vapor-cycle systems, and air-cycle systems), and component (compressors, condensers, evaporators, blowers and fans, inverters and controls, and air dampers and others). The analysis also covers regional-level segmentation, including North America, South America, Europe, Asia-Pacific, and the Middle East and Africa. Market size and growth forecasts are presented by value in USD.

| Passenger Train |

| Freight Train |

| Roof-Mounted Systems |

| Under-Floor Systems |

| Split / Car-Body Systems |

| Vapor-Cycle Systems |

| Air-Cycle Systems |

| Compressors |

| Condensers |

| Evaporators |

| Blowers and Fans |

| Inverters and Controls |

| Air Dampers and Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By Train Type | Passenger Train | |

| Freight Train | ||

| By Installation Type | Roof-Mounted Systems | |

| Under-Floor Systems | ||

| Split / Car-Body Systems | ||

| By System Technology | Vapor-Cycle Systems | |

| Air-Cycle Systems | ||

| By Component | Compressors | |

| Condensers | ||

| Evaporators | ||

| Blowers and Fans | ||

| Inverters and Controls | ||

| Air Dampers and Others | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the train HVAC market in 2031?

The train HVAC market is forecast to reach USD 18.45 billion by 2031.

Which region contributes the largest share of global revenue?

Asia-Pacific led with a 49.25% share in 2025, driven by large-scale rail expansion projects.

How fast is the freight segment growing compared with passenger applications?

Freight HVAC demand is expected to register a 4.75% CAGR through 2031, outpacing the overall market growth.

Which component category shows the fastest value growth?

Controls and inverters are projected to expand at a 6.85% CAGR thanks to IoT-driven efficiency gains.

Page last updated on: