Hybrid Train Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

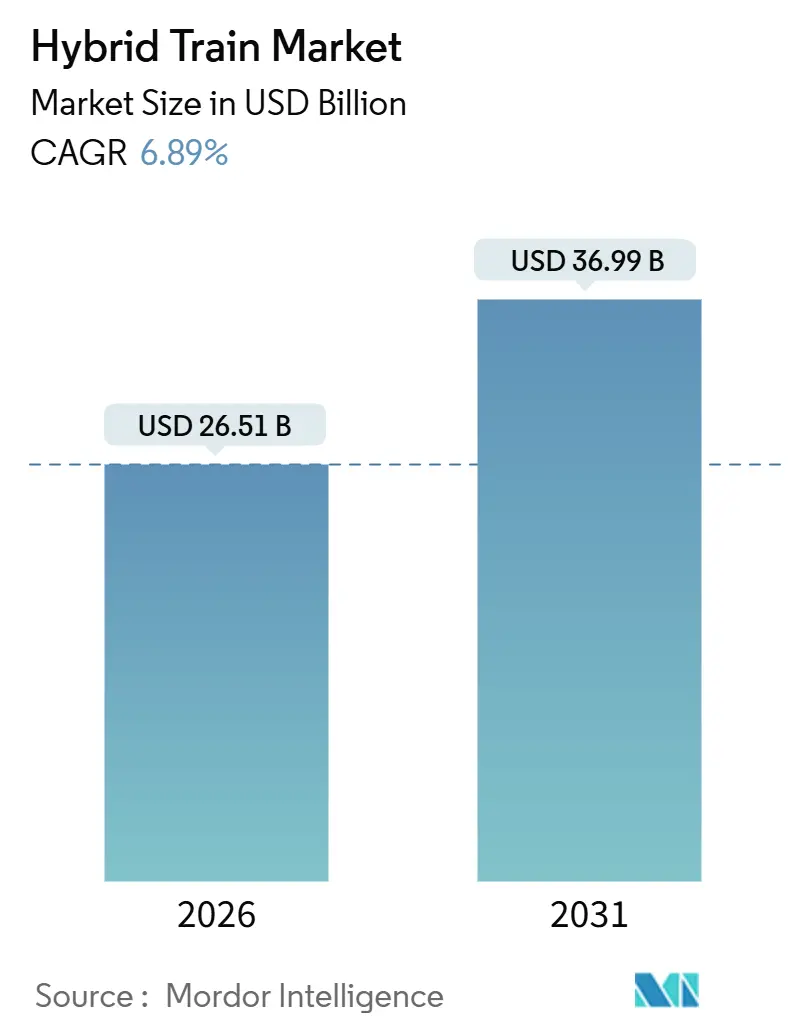

| Market Size (2026) | USD 26.51 Billion |

| Market Size (2031) | USD 36.99 Billion |

| Growth Rate (2026 - 2031) | 6.89% CAGR |

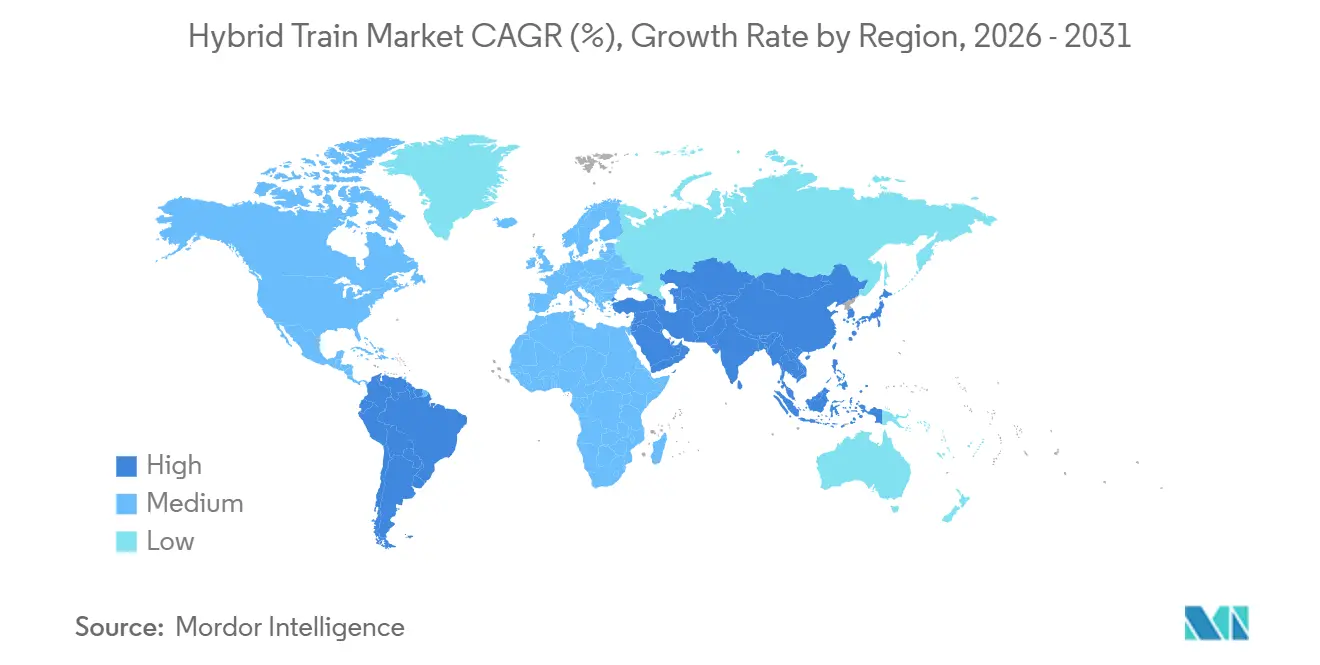

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

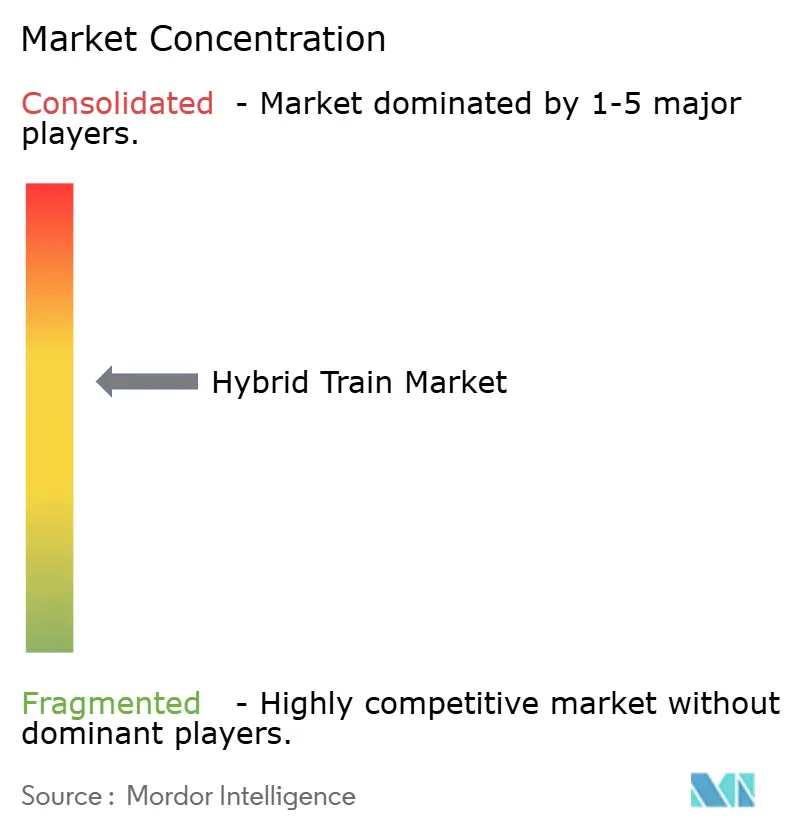

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hybrid Train Market Analysis by Mordor Intelligence

The hybrid train market is valued at USD 26.51 billion in 2026 and is projected to reach USD 36.99 billion by 2031, expanding at a 6.89% CAGR. The growth reflects a convergence of stricter emission rules, rapid public funding for low-carbon rail corridors, and declining battery costs that, together, improve the total cost of ownership for operators shifting from diesel fleets. Europe leads adoption thanks to aggressive decarbonization mandates and a supportive hydrogen infrastructure, while Asia-Pacific is the fastest-growing region as governments couple new rail builds with the clean-energy targets era. Passenger services currently dictate demand, yet freight operators are starting to retrofit large diesel fleets, signaling a broader market pivot.

Key Report Takeaways

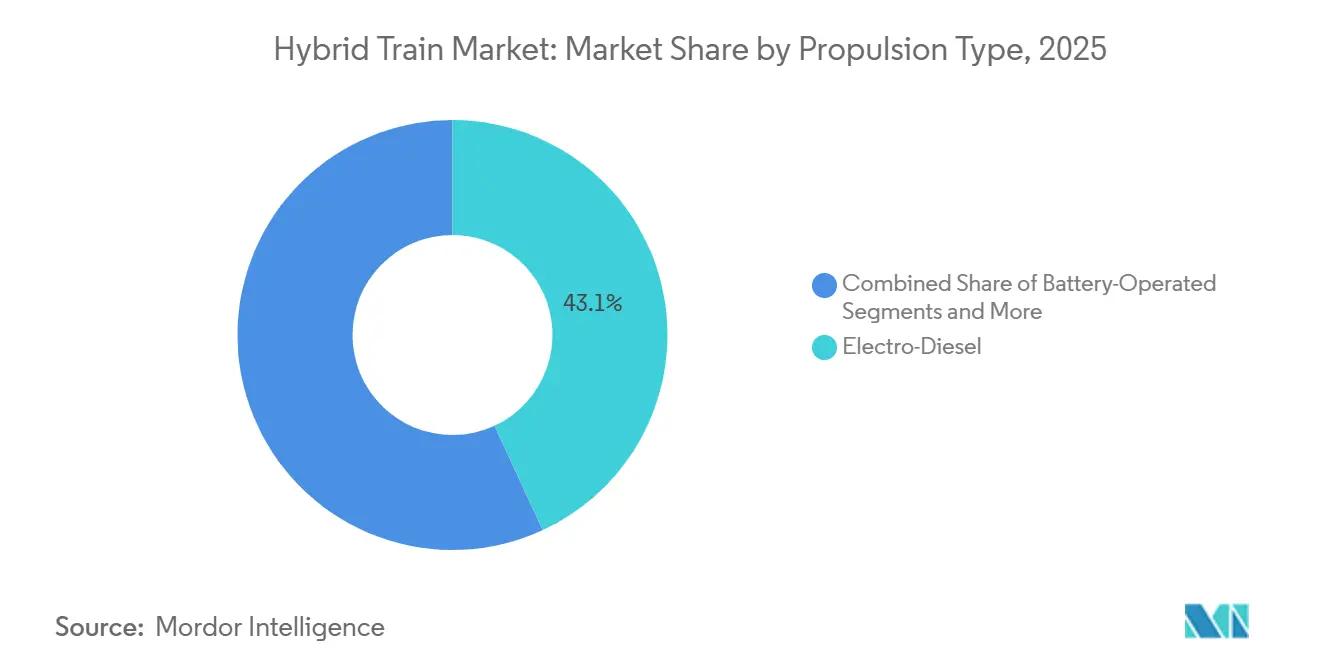

- By propulsion type, electro-diesel systems held 43.11% of the hybrid train market share in 2025, while hydrogen power is forecast to post an 17.45% CAGR through 2031.

- By operating speed, the 100–200 km/h segment captured 55.02% of the hybrid train market size in 2025; trains above 200 km/h are projected to expand at 12.34% CAGR to 2031.

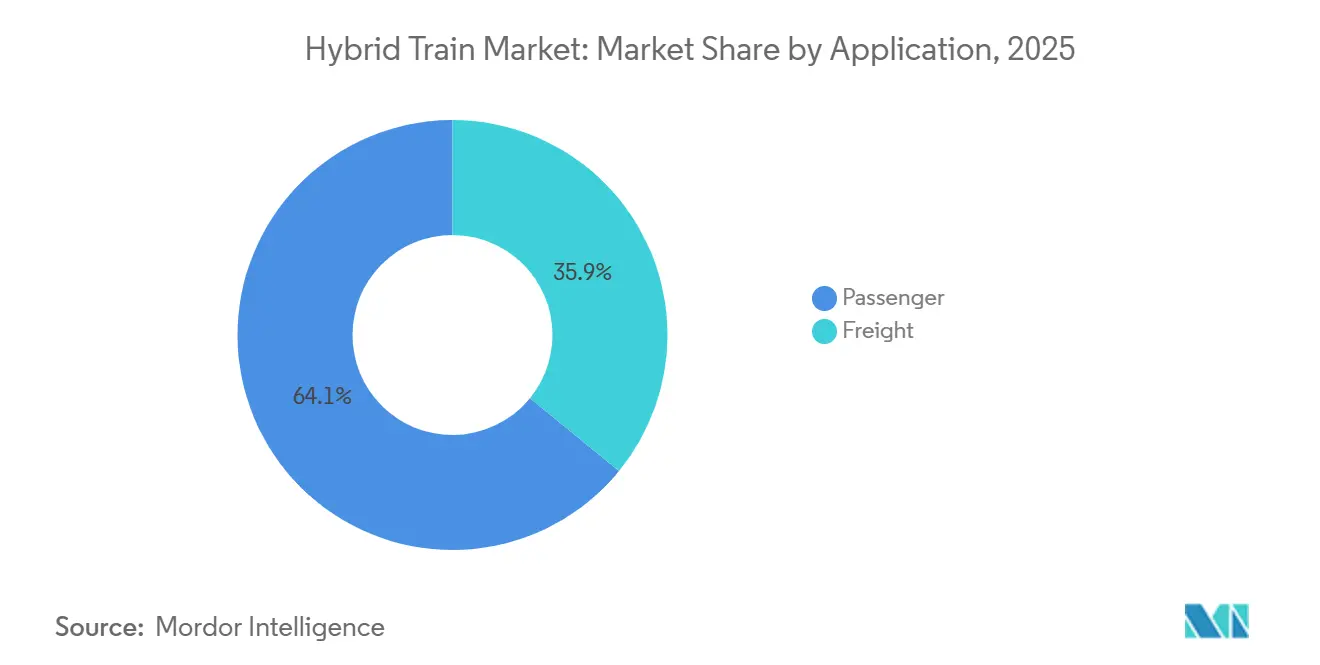

- By application, passenger services accounted for 64.13% of the hybrid train market size in 2025, whereas freight is the fastest-growing segment at 9.56% CAGR.

- By battery chemistry, lithium-ion technology commanded 67.35% of the hybrid train market share in 2025; sodium-ion and other alternatives are advancing at 11.24% CAGR.

- By geography, Europe led with 40.12% revenue share in 2025, while Asia-Pacific is forecast to grow at 10.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hybrid Train Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Emission Regulations | +1.8% | Europe, California, global spill-over | Short term (≤ 2 years) |

| Public Funding for Low-carbon Corridors | +1.5% | North America and European Union, expanding to Asia-Pacific | Medium term (2-4 years) |

| Falling Lithium-ion Battery Costs | +1.2% | Global, manufacturing centered in Asia-Pacific | Medium term (2-4 years) |

| Diesel-hybrid Retrofit Programs | +0.9% | North America and European Union freight networks | Short term (≤ 2 years) |

| Hydrogen Refueling Expansion on Freight Lines | +0.8% | European Union core, expanding to North America | Long term (≥ 4 years) |

| AI-driven Energy-Management TCO Reduction | +0.6% | Global, led by technology-advanced markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening Global Emission Regulations for Rail Transport

Regulators now embed stringent cut-off dates for diesel operations, accelerating hybrid procurement cycles. California’s In-Use Locomotive Regulation compels zero-emission switch engines by 2030, catalyzing immediate demand for bridge technologies [1]“Impact of California In-Use Locomotive Regulation,” Association of American Railroads, aar.org. The European Union’s target of a 90% cut in transport emissions by 2050 positions hybrids as pivotal for lines awaiting catenary investments. Noise caps in dense urban zones reinforce the appeal of battery-only arrival and departure modes. As compliance penalties rise, operators find that hybrid total cost of ownership outperforms refurbished diesel even without carbon pricing.

Rapid Public Funding for Low-Carbon Rail Corridors

National stimulus programs narrow the cost gap between hybrid and legacy powertrains. The United States Infrastructure Investment and Jobs Act assigns USD 66 billion to rail modernization, with hybrid eligibility baked into Federal Railroad Administration grants. Europe’s Clean Hydrogen Partnership investment in the FCH2RAIL bi-mode demonstration merges overhead power and hydrogen fuel cells. Funding extends beyond rolling stock to charging and H₂ refueling nodes, de-risking early adopter routes. Multilateral agencies project over USD 2 trillion in annual transport capex through 2030, and hybrid train market players are positioned to capture a sizable slice of upgrades on non-electrified corridors.

Declining Lithium-Ion Battery Costs and Energy-Density Gains

Average pack prices fell sharply in 2024, crossing the USD 140 kWh threshold and lifting hybrid competitiveness [2]“Global EV Outlook 2024,” International Energy Agency, iea.org. CATL’s Freevoy Super Hybrid Battery charges at 4C and delivers ranges above 400 km, extending zero-emission operation windows. Energy-density gains yield up to 20% diesel reduction on mixed routes, documented by SNCF trials in France. Sodium-ion prototypes reach commercial readiness, hedging against lithium price volatility and geopolitical constraints. Broader chemistry options encourage operators to match battery type with duty cycles, tempering residual-value risk.

Diesel-Hybrid Retrofit Programs for Legacy Fleets

Retrofitting encourages adoption without requiring full fleet write-offs. Union Pacific’s collaboration with ZTR tests hybrid-battery units on heavy-haul freight, confirming 15% fuel savings. ABB’s modular traction kits provide three drive modes, adding zero-emission last-mile capability for commuter lines. Academic studies demonstrate 25% CO₂ reductions and 40% life-cycle savings over 15 years for retrofits compared to diesel rebuilds. Data collected from pilots informs future new-build specifications, reducing technology learning curves.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost vs. Diesel Refurbishment | -1.4% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Sparse Charging and Hydrogen Infrastructure | -1.1% | North America, Asia-Pacific, and emerging markets | Medium term (2-4 years) |

| Fast-Electrifying Corridors Cannibalizing Hybrids | -0.8% | European Union core corridors, expanding to Asia-Pacific | Medium term (2-4 years) |

| Rail-grade Battery Supply-chain Bottlenecks | -0.6% | Global, with concentration risks in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost vs. Diesel Refurbishment

Even with falling battery prices, a new hybrid locomotive can cost 50-70% more than a diesel rebuild. Hydrogen fuel remains a sizable operating expense, exceeding diesel cost parity on current supply chains. Smaller railroads managing Tier 0 engines lack balance-sheet capacity, slowing uptake. Leasing firms demand clear secondary market valuations before underwriting hybrid assets, extending negotiation cycles. Modular designs and escalating public incentives are gradually closing the gap.

Sparse Charging / Hydrogen Infrastructure Outside Europe

Europe operates more than 500 hydrogen plants, yet global rail-grade refueling nodes are still counted in hundreds. California alone forecasts a need for over 1 million chargers by 2030, highlighting the infrastructure scale challenge. Freight corridors that cross multiple states face service disruption risks without dependable hubs. Network operators respond by specifying larger on-board storage and co-locating refueling stations with intermodal depots, but progress remains uneven.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: Electro-Diesel Dominance Faces Hydrogen Challenge

In 2025, electro-diesel configurations captured 43.11% of the hybrid train market share, benefiting from proven reliability over mixed electrified routes. Operators favor their drop-in compatibility, which avoids locomotive changes and minimizes dwell time. Hydrogen sets the pace for growth, climbing 17.45% CAGR to 2031 as refueling networks scale beyond Germany. Battery-only sets carve out shuttles and branch-line duties, while gas models linger where natural-gas pipelines lie close to rail yards. Siemens’ Mireo Plus B, deployed in Baden-Württemberg, trims 1.8 million liters of diesel per year, showcasing mid-range savings [3]“Mireo Plus B Service Entry,” Siemens Mobility, press.siemens.com. The hybrid train market size for electro-diesel remains stable through the forecast, yet hydrogen’s cost trajectory suggests eventual overtaking in high-duty corridors.

The hybrid train market demand across propulsion types hinges on the speed of infrastructure build-outs and policy clarity. Projects such as the FCH2RAIL consortium are validating bi-mode fuel-cell architectures under European standards. Manufacturers embed AI algorithms that switch power sources dynamically, squeezing incremental efficiency gains. The resulting interoperability reduces stranded-asset risk, encouraging cautious buyers to transition.

By Operating Speed: Mid-Range Leadership with High-Speed Acceleration

Trains operating between 100–200 km/h generated 55.02% of the hybrid train market size in 2025, reflecting the segment’s fit with regional passenger timetables and regenerative-braking benefits. Segment growth continues as suburban networks opt for battery coasting through emission-sensitive downtowns. High-speed hybrids above 200 km/h expand at 12.34% CAGR, buoyed by track upgrades and the push for zero-emission entry into city cores. Hitachi and JR East jointly trial hydrogen trainsets designed for 300 km/h sprint segments, targeting commercial service in 2027.

Fleet planners weigh trade-offs between battery mass and acceleration curves. Software-defined power management offsets some weight penalties, equalizing journey times across speed classes. As component densities rise, the hybrid train market may see a narrowing performance gap, letting operators flex one fleet across wider duty cycles.

By Application: Passenger Focus Shifts Toward Freight Opportunity

Passenger services held 64.13% of the hybrid train market size in 2025, propelled by public subsidies tied to urban air-quality metrics. Predictable timetables match well with charging windows, and battery-only arrival modes cut station noise. Freight shows stronger momentum, sprinting at 9.56% CAGR on the promise of lower fuel bills and compliance with forthcoming EPA rules. Canadian National’s ongoing hybrid locomotive pilot underscores the sector’s curiosity.

Commercial freight adoption hinges on tractive-effort optimization and the alignment of refueling stops with hub-and-spoke logistics patterns. Longer-haul Class I carriers test range-extended hybrids, whereas short-line operators may favor modular retrofits that lighten capital load. The hybrid train market responds by offering configurable energy packs tailored to tonnage and grade profiles.

By Battery Chemistry: Lithium-Ion Leadership Meets Alternative Challenge

Lithium-ion maintained 67.35% hybrid train market share in 2025 thanks to deep manufacturing scale, yet supply-chain concentration triggers diversification moves. Sodium-ion volumes scale at 11.24% CAGR as miners’ de-risk from lithium, and rail operators appreciate resilience to thermal runaways. Research by Fraunhofer suggests sodium cells can satisfy rail duty cycles with 15% lower cost per kilowatt-hour. Lead-acid persists for hotel loads, while nickel-cadmium supports extreme-temperature freight lines in mining belts.

Chemistry choice correlates with route length and charging frequency. Hybrids on commuter services prize fast-charge lithium packs; long-distance freight may accept heavier sodium batteries to unlock cost advantages. A mixed-chemistry future is plausible as OEMs design universal battery bays, letting operators swap chemistries as price signals evolve.

Geography Analysis

Europe accounted for 40.12% of the hybrid train market in 2025, anchored by the EU Green Deal’s 90% transport-emission reduction target and well-funded hydrogen corridors such as Germany’s Coradia iLint deployments. France’s SNCF hybrid TER program trims energy use by 20%, showcasing operational wins on legacy routes. Despite leadership, peripheral lines still lack charging nodes, nudging policymakers to bundle infrastructure grants with rolling-stock orders. The hybrid train market share in Europe remains buoyed by mature supply chains and high public acceptance.

Asia-Pacific is the fastest-growing region at 10.03% CAGR through 2031, driven by China’s and India’s rail-capacity expansions and rising public scrutiny of diesel emissions. The Asian Development Bank forecasts 78,000 km of new conventional rail by 2030, a sizable field for hybrid insertion. Japan pioneers’ hydrogen multiple units, and Australia eyes solar-boosted hybrids for heavy-haul ore lines. Governments in the region often pair electrification with hybrid procurement for secondary branches, enabling staggered capital outlays.

North America represents a sizeable opportunity as freight operators navigate EPA rulemaking and state mandates. The USD 66 billion Infrastructure Investment and Jobs Act reserves funds for hybrid demonstrators, and Amtrak’s USD 3.4 billion order for 73 Venture battery-hybrid trainsets underlines passenger-sector momentum. Union Pacific and BNSF trial retrofits, targeting measurable fuel savings before fleet-wide rollouts. Sparse hydrogen stations outside California restrain long-haul adoption, but battery-dominant hybrids bridge the gap.

Competitive Landscape

Competitive intensity is moderate, with legacy manufacturers leveraging hybrid portfolios to differentiate bids and protect installed bases. Alstom booked EUR 10.9 billion (approximately USD 12.5 billion) in orders during H1 2024/25, spotlighting the Régiolis and Coradia platforms that promise 20% energy cuts. Siemens Mobility secured a USD 3.4 billion Amtrak deal, indicating a scale advantage in the hybrid battery segment. Hitachi clinched a significant contract for 45 tri-mode units with Arriva, proving competitiveness in the United Kingdom retrofit market.

Cross-industry alliances accelerate innovation. The FCH2RAIL consortium unites Toyota, CAF, and German Aerospace Center to commercialize overhead-plus-hydrogen power packs. CRRC’s entrée into Europe through Deutsche Bahn hybrid orders signals Asia-based price pressure. Niche disruptors such as OptiFuel Systems push RNG-electric hybrids, diversifying the technology mix.

Success factors now extend beyond hardware. OEMs embed AI-driven dispatch modules, predictive maintenance, and energy-market integration to offer bundled service contracts. After the European Commission blocked the Siemens–Alstom merger in 2019, market concentration levels encourage multi-vendor tenders, sustaining downward price pressure without stalling R&D.

Hybrid Train Industry Leaders

Alstom SA

Siemens Mobility GmbH

Hitachi Rail

CRRC Corporation Ltd

Stadler Rail AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The United Kingdom will join Denmark, Germany, France, Croatia, Italy, and Latvia in launching battery and hybrid trains to replace diesel-powered trains across Europe. This initiative aims to promote cleaner rail transportation and sustainable solutions for non-electrified rail lines.

- April 2025: Stadler secured hybrid train orders for southern France, reinforcing regional decarbonization programs.

- January 2025: Canadian National Railway initiated a hybrid locomotive pilot to gauge fuel-efficiency gains in freight service.

- April 2025: Hitachi secured a GBP 300 million (~USD 394.3 million) contract to supply 45 tri-mode battery hybrid trains to the Arriva Group, increasing capacity by 20% and reducing emissions by 30%.

Global Hybrid Train Market Report Scope

The scope includes segmentation by propulsion type (battery-operated, electro-diesel, hydrogen-powered, solar-powered, and gas-powered), operating speed (less than 100 km/h, 100-200 km/h, and above 200 km/h), application (passenger and freight), and battery chemistry (lithium-ion, lead-acid, nickel-cadmium, sodium-ion, and others). The analysis also covers regional-level segmentation, including North America, South America, Europe, Asia-Pacific, and the Middle East and Africa. Market size and growth forecasts are presented by value in USD.

| Battery-Operated |

| Electro-Diesel |

| Hydrogen-Powered |

| Solar-Powered |

| Gas-Powered |

| Less than 100 km/h |

| 100 - 200 km/h |

| Above 200 km/h |

| Passenger |

| Freight |

| Lithium-Ion |

| Lead-Acid |

| Nickel-Cadmium |

| Sodium-Ion & Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | Egypt |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East and Africa |

| By Propulsion Type | Battery-Operated | |

| Electro-Diesel | ||

| Hydrogen-Powered | ||

| Solar-Powered | ||

| Gas-Powered | ||

| By Operating Speed | Less than 100 km/h | |

| 100 - 200 km/h | ||

| Above 200 km/h | ||

| By Application | Passenger | |

| Freight | ||

| By Battery Chemistry | Lithium-Ion | |

| Lead-Acid | ||

| Nickel-Cadmium | ||

| Sodium-Ion & Others | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | Egypt | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the hybrid train market?

The hybrid train market is valued at USD 26.51 billion in 2026 and is set to reach USD 36.99 billion by 2031.

Which region leads hybrid train adoption?

Europe commands 40.12% of revenue in 2025 due to stringent emission policies and robust hydrogen infrastructure.

Which propulsion technology is growing fastest?

Hydrogen-powered hybrids post the highest CAGR at 17.45% through 2031 as refueling corridors expand.

What are the main barriers to wider hybrid train deployment?

High upfront capital relative to diesel refurbishment and limited charging or hydrogen infrastructure outside Europe remain the biggest constraints.

Page last updated on: