Train Battery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

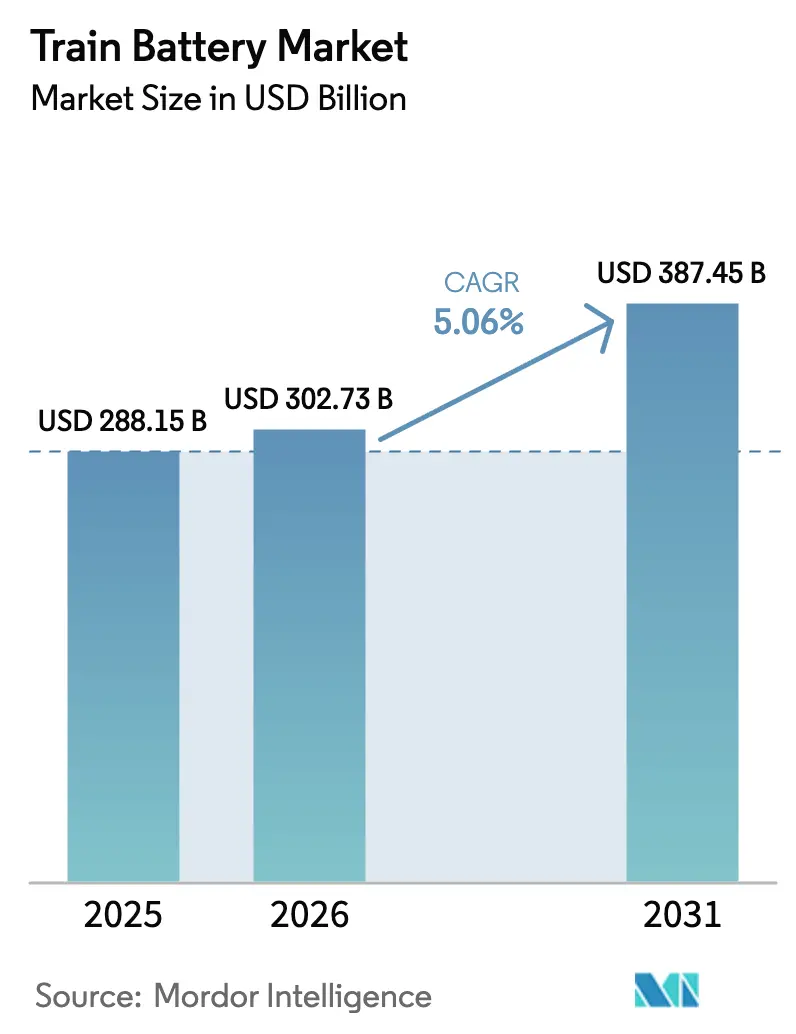

| Market Size (2026) | USD 302.73 Billion |

| Market Size (2031) | USD 387.45 Billion |

| Growth Rate (2026 - 2031) | 5.06% CAGR |

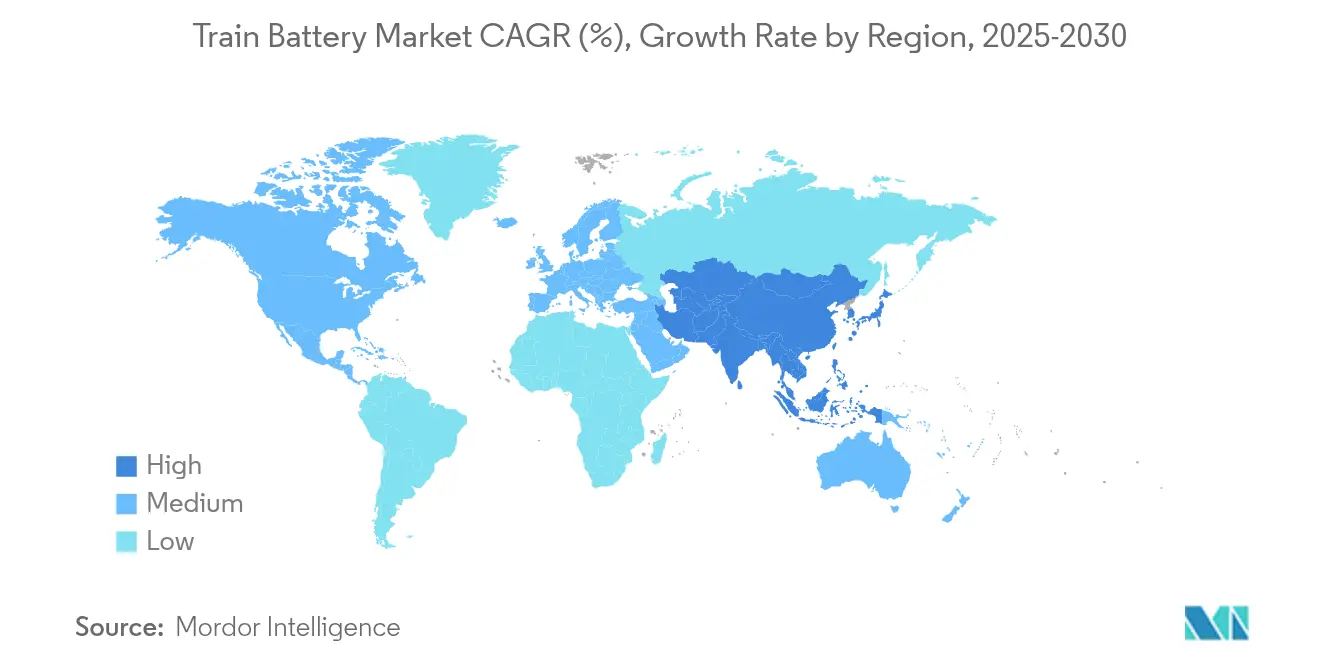

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

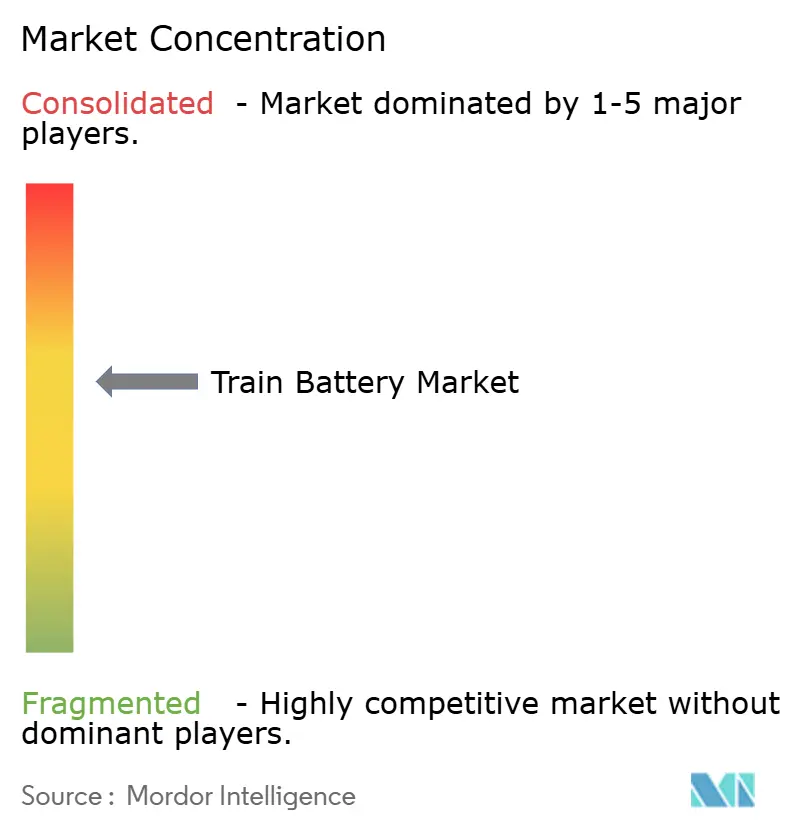

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Train Battery Market Analysis by Mordor Intelligence

The train battery market size is expected to grow from USD 288.15 billion in 2025 to USD 302.73 billion in 2026 and is forecast to reach USD 387.45 billion by 2031 at 5.06% CAGR over 2026-2031. Momentum comes from aggressive rail-electrification programs, falling lithium-ion costs, and stricter emissions rules that collectively shift procurement away from diesel traction toward battery-hybrid and battery-electric rolling stock. Operators increasingly consider total cost of ownership alongside upfront price, so chemistries offering longer life cycles and lower maintenance can displace legacy lead-acid solutions. Supply-chain localization programs in the United States and Europe are also spurring greenfield cell plants, while Asia-Pacific leverages existing scale advantages to deepen its dominance. Taken together, these forces keep the train battery market on a steady expansion path that balances cost, performance, and policy risk across regions.

Key Report Takeaways

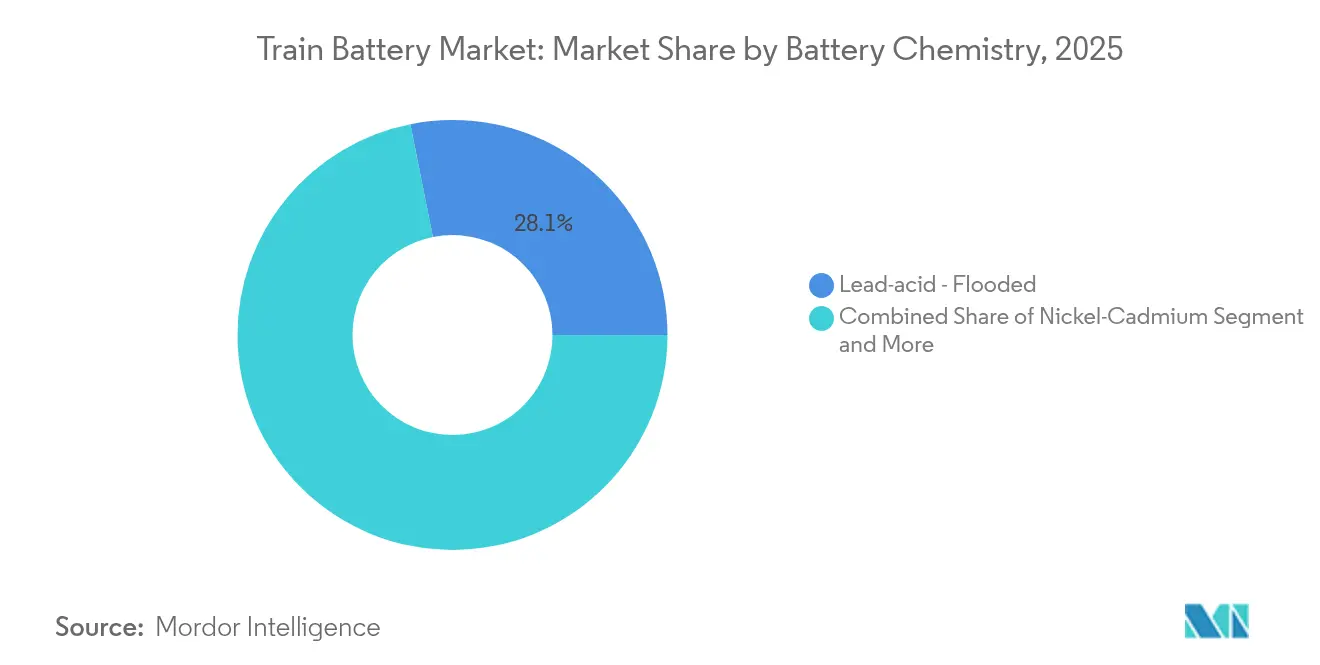

- By battery chemistry, lead-acid flooded units led with 28.14% revenue share in 2025; lithium-ion LFP chemistry is projected to grow fastest at a 7.12% CAGR through 2031.

- By capacity range, the 50-150 Ah band commanded 48.25% of the train battery market share in 2025, while >150 Ah packs are poised to advance at a 6.62% CAGR to 2031.

- By application, starter/cranking systems retained a 35.72% share of the train battery market size in 2025, whereas traction propulsion is set to post a 9.87% CAGR between 2026 and 2031.

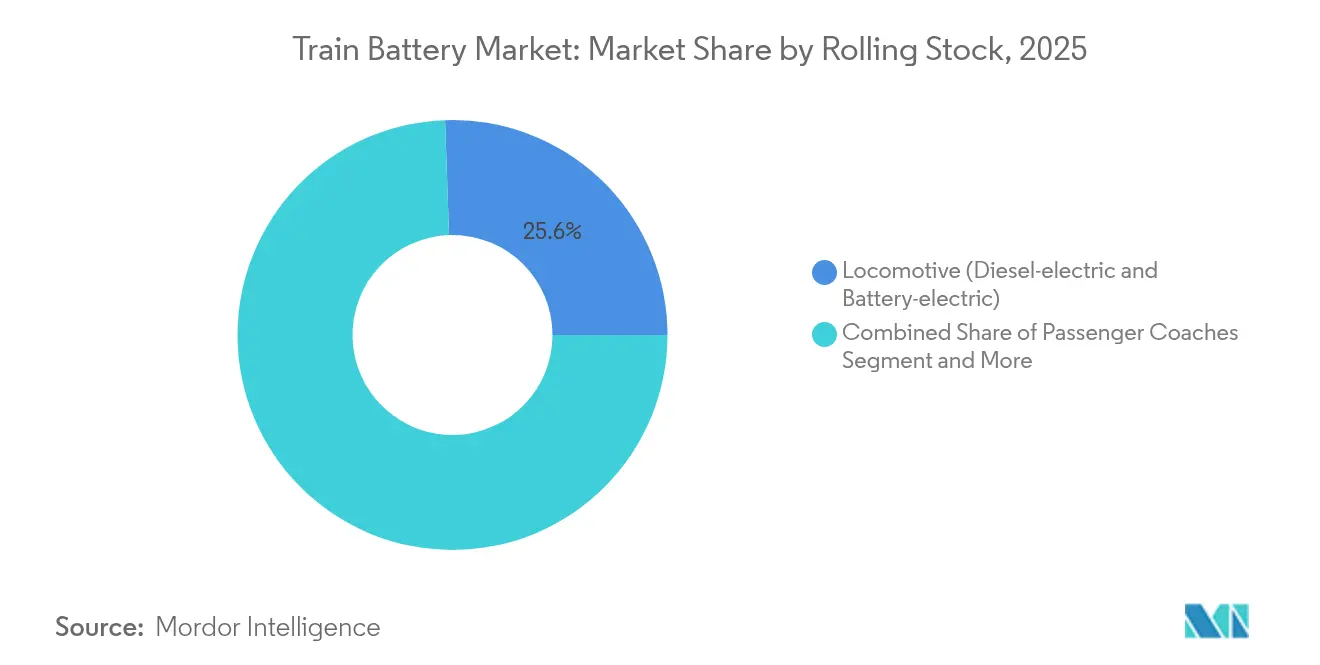

- By rolling stock, locomotive installations contributed 25.55% of 2025 revenue; EMU/BEMU formats are on track for the highest growth at 6.93% through 2031.

- By end-user, public rail operators held 49.10% of demand in 2025, but urban transit agencies are projected to lead growth at 8.86% CAGR to 2031.

- By geography, Asia-Pacific dominated with 47.30% of 2025 revenue and represents the fastest-growing geography at 7.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Train Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rail Electrification Across Urban & Regional Corridors | +1.2% | Global (APAC in front) | Medium term (2-4 years) |

| Diesel Phase-Out Mandates by 2030 | +0.9% | Global | Long term (≥4 years) |

| Cost & Weight Edge of Li-Ion / LFP Chemistries | +0.8% | Europe, North America spillover | Short term (≤2 years) |

| EU Funding for BEMU Adoption | +0.5% | Global | Long term (≥4 years) |

| Swap-Pack Maintenance Cuts Downtime | +0.4% | Europe, demonstration globally | Medium term (2-4 years) |

| AI-Driven BMS Extends Battery Life | +0.3% | APAC core, Europe spillover | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapid Electrification of Urban & Regional Rail Corridors

Policy mandates for carbon neutrality are pushing electrification into secondary and branch lines previously viewed as uneconomic for catenary. India lifted electrification to 96% of its network in 2024, more than tripling its annual track-wire rate over the last decade. Germany’s Schleswig-Holstein region will save 10 million L of diesel yearly once battery EMUs take over rural routes. Because overhead lines on low-density corridors can exceed USD 3 million per kilometer, batteries now represent a lower-risk path to decarbonization. Operators value the flexibility of trains that bridge electrified and non-electrified sections without service cuts, enabling step-wise capex profiles rather than all-or-nothing infrastructure outlays.

Cost / Weight Advantages of Next-Gen Li-Ion & LFP Chemistries

Lithium carbonate tumbled from USD 70,000 to under USD 15,000 per tonne between 2023 and 2025, pushing LFP system costs toward parity with lead-acid while slashing pack mass by 40% over five years. CATL now advertises 6C charging that fills a train pack in 10 minutes, meeting heavy-turnback urban timetables. Toshiba’s SCiB modules show 10,000 cycles with low fade, translating to longer intervals between overhauls [1]“SCiB Rail Battery Overview,” Toshiba Corp., toshiba.com. The resulting total-life economics drive broader uptake, particularly where labour costs and energy prices reinforce the benefits.

Mandates for Phasing-Out Diesel Locomotives in Europe by 2030

European Union rules that remove diesel locomotives by 2030 are locking in battery demand. Germany plans to lift its electrified share to 70% by 2030 while converting residual mileage to battery or hydrogen power. France’s SNCF has earmarked EUR 40 million for battery-powered TER regional units that can run 80 km off-wire [2]“TER Hybrid Battery Programme,” SNCF Press Office, sncf.com. Penalties tied to carbon pricing and track-access surcharges leave fleet owners little room for delay, so suppliers with proven rail-grade batteries enjoy a clear tender advantage.

AI-Enabled Predictive BMS Extends Duty Cycles

Machine-learning algorithms now parse temperature, cell impedance, and duty data to prescribe optimal charge windows. Bangkok MRT posted 9.65% traction-energy savings after rolling out AI-driven scheduling across wayside storage and rolling stock [3]“AI Optimised Energy Management on Bangkok MRT,” IEEJ Researchers, ieej.org. Toshiba’s latest SCiB packs integrate cell-level analytics that adjust charge rates to arrest thermal drift, adding an estimated 20-30% life extension.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Li-Ion Cost vs. Lead-Acid | -0.7% | Global, acute in price-sensitive markets | Short term (≤2 years) |

| Safety & Certification Barriers for Rail Packs | -0.5% | Global, stringent in developed markets | Medium term (2-4 years) |

| Nickel & Lithium Price Volatility | 0.4% | Global supply chains | Short term (≤2 years) |

| Grid Limits on Regenerative Storage | -0.3% | Urban networks with aging infrastructure | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Upfront Li-Ion Cost vs. Legacy Lead-Acid

Even after recent price drops, Li-ion packs still cost 3-5 times more than flooded lead-acid, so budget-constrained agencies often delay migration. Lead-acid’s 28.66% share in 2024 underscores its staying power in auxiliary duties where price trumps performance. Federal incentives such as EnerSys’s USD 199 million DOE grant soften the blow and create beachheads for higher-spec chemistries.

Thermal-Runaway & Certification Hurdles for Large Rail Packs

Stricter rules like China’s GB38031-2025 stretch validation timelines by up to 18 months and add USD 0.5-1 million per design. UL 1973 and European EN 50155 testing for vibration, EMC, and crashworthiness further raise barriers, favoring incumbents with deep lab capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Chemistry: LFP emerges as traction leader

Lead-acid flooded units retained 28.14% of 2025 revenue, a figure that pins down much of the starter and auxiliary space in the train battery market. Yet lithium-ion LFP packs are forecast to grow 7.12% annually, lifted by falling material costs and inherent thermal stability. The train battery market size for LFP traction systems is projected to widen especially quickly on regional lines that demand 100-km off-wire range.

Nickel-cadmium persists in critical safety roles, while lithium-ion NMC/NCA caters to space-constrained premium services despite higher commodity exposure. Emerging solid-state prototypes in Japan and China could enter service after 2028, promising another wave of density gains. Each step in chemistry evolution tilts life-cycle economics further toward advanced lithium platforms, tightening the grip on growth segments of the train battery market.

By Capacity Range: High-capacity systems drive growth

Packs rated 50-150 Ah held 48.25% of 2025 revenue, reflecting continued dominance in mixed auxiliary and hybrid propulsion duties within the train battery market. The >150 Ah bracket, however, records 6.62% CAGR as freight locomotives and regional EMUs specify multi-megawatt-hour arrays. A single FLXdrive can mount 8.5 MWh, equivalent to roughly 16,000 Ah at 525 V, underscoring the demand for ultra-high current architectures.

Project calls from Irish Rail and Caltrans each stipulate battery-only ranges above 80 km, a requirement met only with large-format modules and sophisticated thermal management. As traction-heavy-duty use cases accelerate, the train battery market share for high-capacity packs will expand, with swap-pack logistics further smoothing depot workflows.

By Application: Traction propulsion accelerates fastest

Starter/cranking roles still dominate at 35.72% of spending in 2025, an anchor point that cuts across both diesel and hybrid fleets. Yet traction propulsion is rising at 9.87% CAGR, the single strongest pace among use cases. SNCF’s hybrid TER trains that recuperate 90% of braking energy and Hitachi Rail’s intercity trials illustrate traction’s leap from pilot to mainstream.

Regenerative-only storage and hotel-load support round out application diversity, but propulsion remains the headline. As diesel bans tighten, propulsion will command a larger slice of the train battery market, converting auxiliary stalwarts into comprehensive energy-platform solutions.

By Rolling Stock: EMUs lead the electrification wave

Locomotives accounted for 25.55% of turnover in 2025, but EMU/BEMU sets are on track for a 6.93% CAGR to 2031. Distributed power lets EMUs hide batteries beneath each carriage, boosting redundancy and trimming axle loads. Siemens’ battery Vectron order for JeMyn AG shows how modular packs free shunters and regional freight from overhead-line dependency.

High-speed fleets deploy compact packs for emergency roll-out, as seen on Japan’s N700S, pointing toward secondary safety niches. Over the outlook, EMUs will continue to pull the train battery market with their multi-car architecture that soaks up mid-size packs in high volumes.

By End-User: Urban transit agencies accelerate adoption

Public rail operators booked 49.10% of 2025 demand, but urban transit agencies rose fastest at 8.86% CAGR as city authorities chase zero-tailpipe vows. Metra’s USD 169.3 million CMAQ grant underpins 16 battery trainsets, an emblem of policy-backed momentum.

OEM refurbish divisions also see upside, retrofitting mid-life fleets with battery-ready underframes. With city air-quality targets firming and congestion-charge schemes spreading, metropolitan agencies will keep reshaping the demand profile of the train battery market.

Geography Analysis

Asia-Pacific controlled 47.30% of 2025 revenue and is forecast to grow 7.18% annually by 2031, anchoring both size and momentum for the train battery market. India’s near-total rail electrification and China’s factory-to-network vertical integration secure supply and demand at scale. Japan continues to field-test solid-state packs, while South Korea’s battery firms eye export consortia with local rolling-stock OEMs.

Europe ranks second by value and remains the regulatory bellwether. EU diesel-phase-out rules, Germany’s 70% wiring target, and France’s TER battery fleet all combine to pull forward orders across Spain, Italy, and the Nordics. Funding through CEF and national climate banks lowers the weighted average cost of capital, giving smaller regional operators a path into battery programs. As these fleets enter daily service, they feed proven-platform confidence back into global tenders.

North America begins with low electrification (≈1%) yet shows accelerating take-up. California’s zero-emission rail blueprint and federal production credits under the Inflation Reduction Act spur domestic supply chains. EnerSys’s government-backed plant in Pennsylvania and Wabtec–GM’s Ultium pact both target “Made in USA” compliance, opening slots for battery locomotives on freight short lines and passenger corridors. Given the vast length of non-electrified track, batteries provide a practical bridge while wiring economics remain prohibitive.

Competitive Landscape

The train battery market shows moderate concentration. Top players—EnerSys, Saft, CATL, Toshiba, and Wabtec—hold scale advantages in cell manufacturing, systems integration, and certification know-how. Agile specialists focusing on AI-enabled BMS or swap-pack designs continue to secure niche contracts, keeping competitive pressure active.

Leaders differentiate through vertical integration and government-backed localisation. EnerSys leverages its USD 199 million DOE contract to anchor North American supply. CATL and BYD extend automotive volume economics to rail, bundling battery leasing and swapping infrastructure. Saft exploits legacy defence and aviation credentials to navigate stringent certification regimes. Meanwhile, Wabtec partners with GM’s Ultium platform to cross-pollinate automotive chemistries into freight locomotives.

Strategic partnerships shape procurement decisions. ABB and Stadler co-develop Pro-Series traction batteries assembled in Virginia for Metra and Caltrans, meeting Buy-America clauses. Toshiba’s long-running ties with JR East assure supply stability for SCiB modules. Patents around cell-level redundancy and predictive analytics harden entry barriers, while local content rules in the US and Europe increasingly influence tender scoring.

Train Battery Industry Leaders

EnerSys

Saft

GS Yuasa Corporation

Hitachi Rail

Exide Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ABB signed a deal with Stadler US to deliver traction converters and Pro Series batteries for Metra and Caltrans trainsets, with assembly in Virginia.

- February 2025: Siemens Mobility took its first order for Vectron locomotives featuring battery modules from JeMyn AG; deliveries start 2027.

- August 2024: CRRC Qishuyan sent a 1 MW hydrogen-battery locomotive to Chile’s Ferrocarril de Antofagasta.

- June 2024: Jupiter Electric Mobility and Log9 Materials agreed to supply 72.8 kWh LFP batteries for nine Vande Bharat trainsets after BHEL qualification.

Global Train Battery Market Report Scope

Train batteries are electrochemical batteries that leverage chemical reactions to produce an electric current. These batteries are used for engine start and power the different electrical components in the train, including HVAC units, lights, etc.

The train battery market is segmented by battery type (lead acid battery, nickel-cadmium battery, and lithium-ion battery), application type (starter battery and auxiliary battery), rolling stock type (locomotive, metro, monorail, tram, freight wagon, and passenger coaches), and Geography (North America, Europe, Asia-Pacific, and Rest of the World).

The report offers market size and forecasts for the train battery market in value (USD million) for all the above segments.

| Lead-acid - Flooded |

| Lead-acid - VRLA (AGM / Gel) |

| Nickel-Cadmium |

| Lithium-ion - LFP |

| Lithium-ion - NMC / NCA |

| Lithium-ion - LTO |

| Nickel - Metal Hydride |

| Below 50 Ah |

| 50 - 150 Ah |

| Above 150 Ah |

| Starter / Cranking |

| Auxiliary (Lighting, HVAC, Doors) |

| Traction Propulsion (Hybrid and Battery trains) |

| On-board Regenerative-Braking Storage |

| Locomotive - Diesel-electric and Battery-electric |

| Electric Multiple Unit (EMU) / Battery-EMU |

| Diesel Multiple Unit Hybrid |

| Metro and Light Rail |

| Monorail and People-Mover |

| High-speed Train |

| Freight Wagon (Cold-move, E-axle) |

| Passenger Coaches |

| Public Rail Operators |

| Private Freight Operators |

| Urban Transit Agencies |

| OEM Train Manufacturers |

| North America | United States | |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia & New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egpyt | ||

| Rest of Africa | ||

| By Battery Chemistry | Lead-acid - Flooded | ||

| Lead-acid - VRLA (AGM / Gel) | |||

| Nickel-Cadmium | |||

| Lithium-ion - LFP | |||

| Lithium-ion - NMC / NCA | |||

| Lithium-ion - LTO | |||

| Nickel - Metal Hydride | |||

| By Capacity Range | Below 50 Ah | ||

| 50 - 150 Ah | |||

| Above 150 Ah | |||

| By Application | Starter / Cranking | ||

| Auxiliary (Lighting, HVAC, Doors) | |||

| Traction Propulsion (Hybrid and Battery trains) | |||

| On-board Regenerative-Braking Storage | |||

| By Rolling Stock | Locomotive - Diesel-electric and Battery-electric | ||

| Electric Multiple Unit (EMU) / Battery-EMU | |||

| Diesel Multiple Unit Hybrid | |||

| Metro and Light Rail | |||

| Monorail and People-Mover | |||

| High-speed Train | |||

| Freight Wagon (Cold-move, E-axle) | |||

| Passenger Coaches | |||

| By End-User | Public Rail Operators | ||

| Private Freight Operators | |||

| Urban Transit Agencies | |||

| OEM Train Manufacturers | |||

| By Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia & New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egpyt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the train battery market?

The market is valued at USD 302.73 billion in 2026 and is projected to climb to USD 387.45 billion by 2031.

Which region leads the train battery market?

Asia-Pacific leads with 47.30% revenue share in 2025 and is also the fastest-growing region at a 7.18% CAGR.

Which battery chemistry is growing fastest?

Lithium-ion LFP packs record the quickest rise, forecast at 7.12% CAGR through 2031, thanks to lower cost and strong thermal stability.

How fast is traction propulsion demand expanding?

Battery systems for primary traction are expected to post a 9.87% CAGR from 2026 to 2031 as operators phase out diesel.

Page last updated on: