Nickel-based Batteries For Electric Vehicles Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

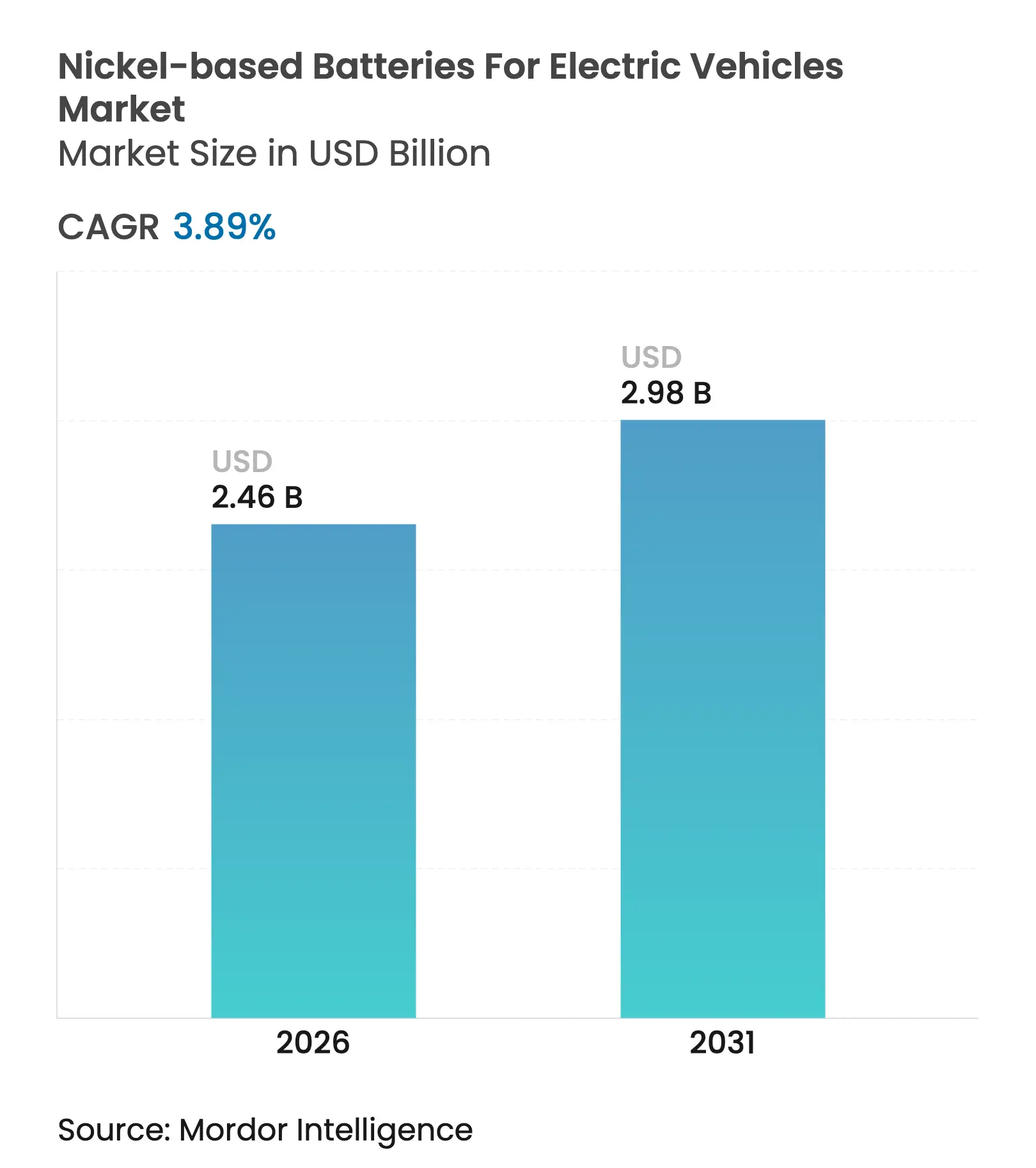

| Market Size (2026) | USD 2.46 Billion |

| Market Size (2031) | USD 2.98 Billion |

| Growth Rate (2026 - 2031) | 3.89 % CAGR |

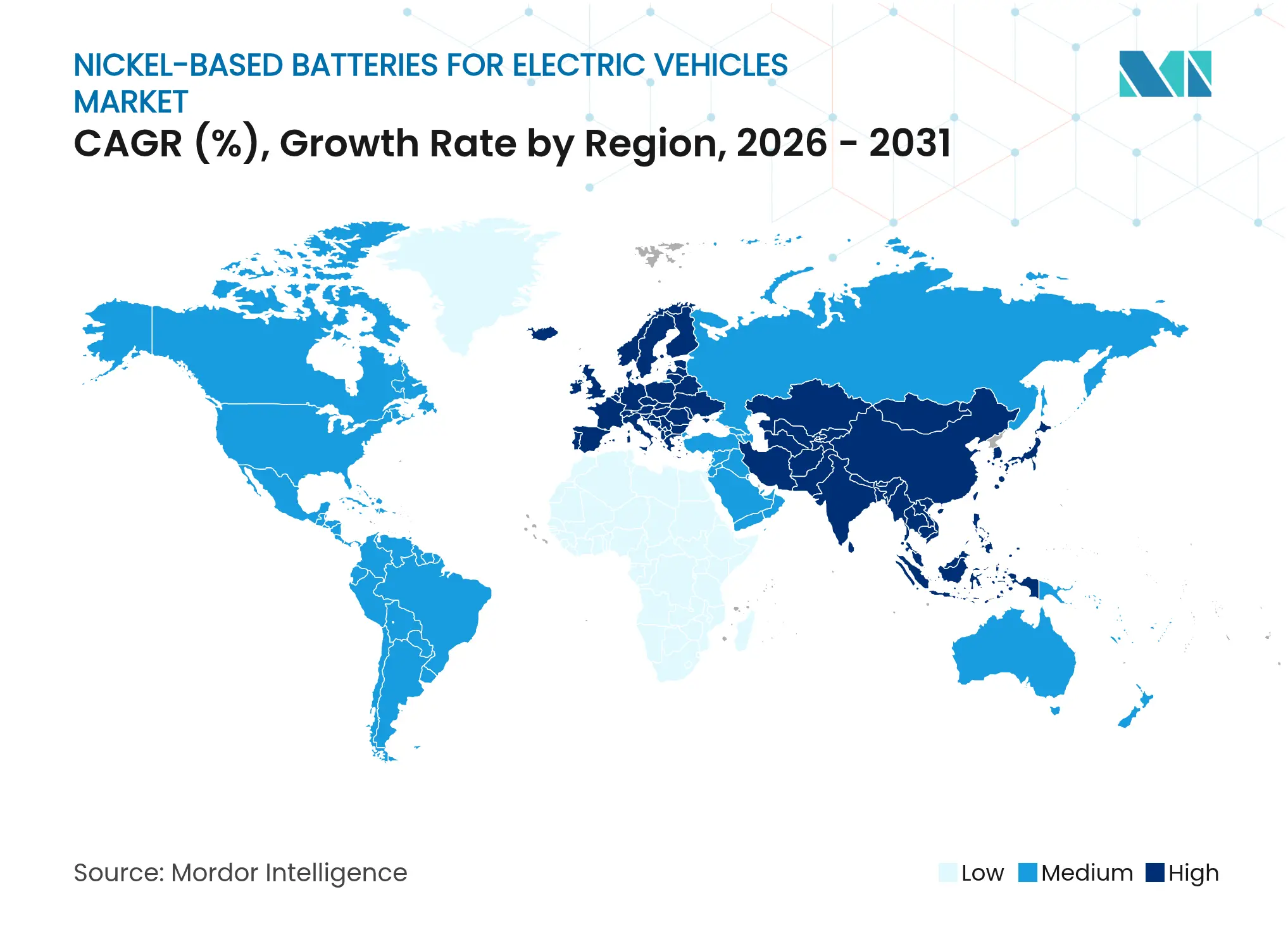

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

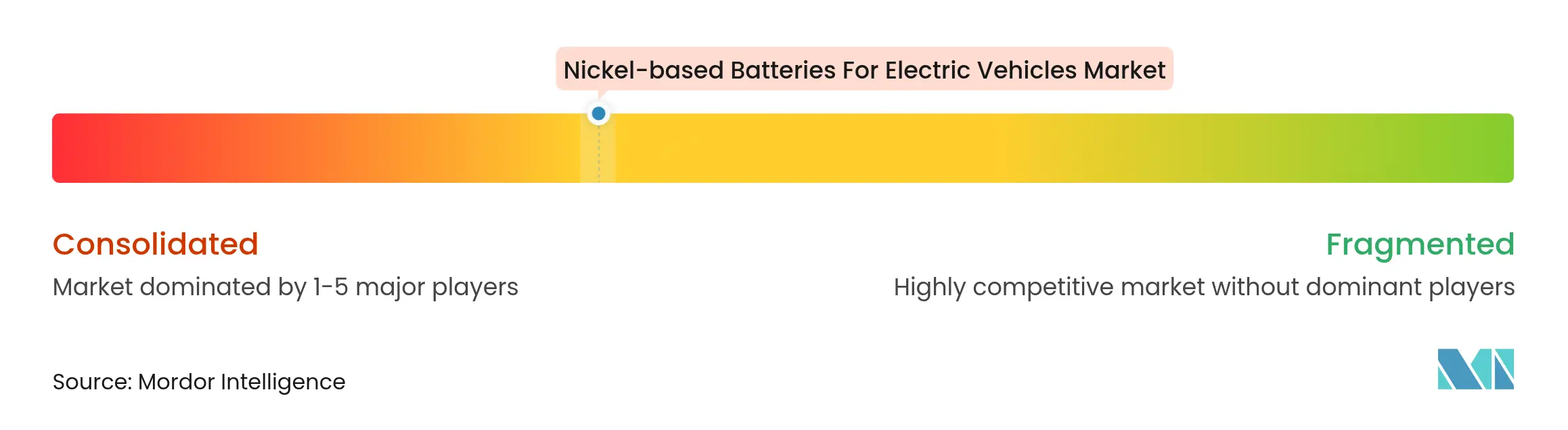

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Nickel-based Batteries For Electric Vehicles Market Analysis by Mordor Intelligence

The Nickel-based Batteries For Electric Vehicles Market size is expected to grow from USD 2.37 billion in 2025 to USD 2.46 billion in 2026 and is forecast to reach USD 2.98 billion by 2031 at 3.89% CAGR over 2026-2031. At present, the nickel based batteries for EV market size reflects a maturing phase in which demand plateaus in volume segments yet remains resilient in premium and commercial-fleet niches. Leading automakers keep high-nickel chemistries in flagship models to maintain 400-plus-mile ranges, while Western governments accelerate domestic mining and refining incentives to reduce import dependence. OEM migration to 800 V electrical platforms, rising adoption of battery-as-a-service contracts, and vertical integration into recycling continue to shape strategic priorities.

Key Report Takeaways

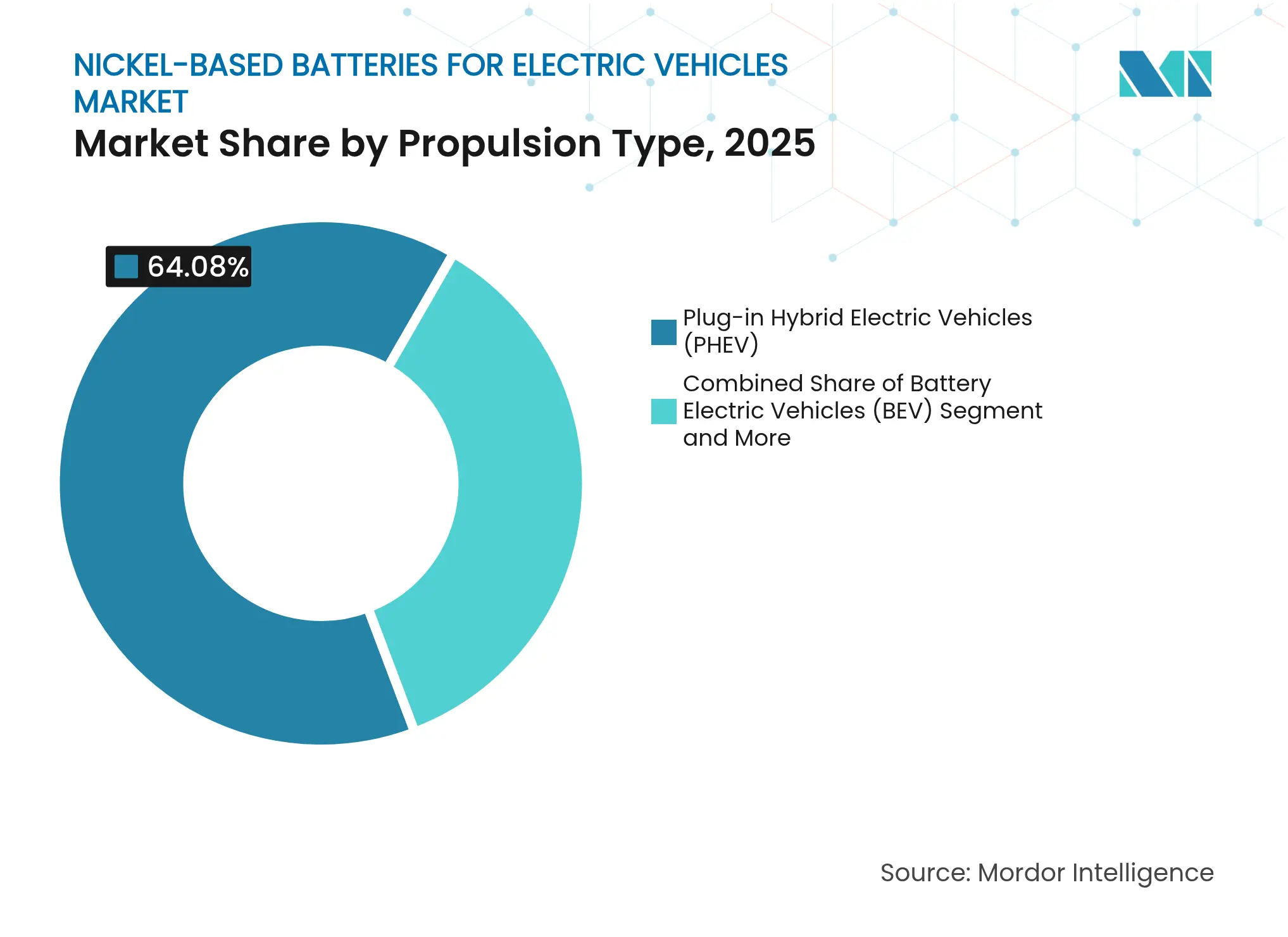

- By propulsion type, PHEVs led with 64.08% revenue share in 2025; BEVs are projected to post the highest 4.93% CAGR through 2031.

- By battery type, advanced NCA/NCM chemistries captured 50.92% of the nickel based batteries for EV market share in 2025, whereas NiMH is poised for a 4.52% CAGR to 2031.

- By vehicle type, commercial vehicles accounted for 62.88% of the 2025 nickel based batteries for EV market size; passenger cars are expected to outpace with a 4.03% CAGR.

- By form factor, pouch cells commanded 56.84% share in 2025, while cylindrical cells are forecast to register a 4.95% CAGR to 2031.

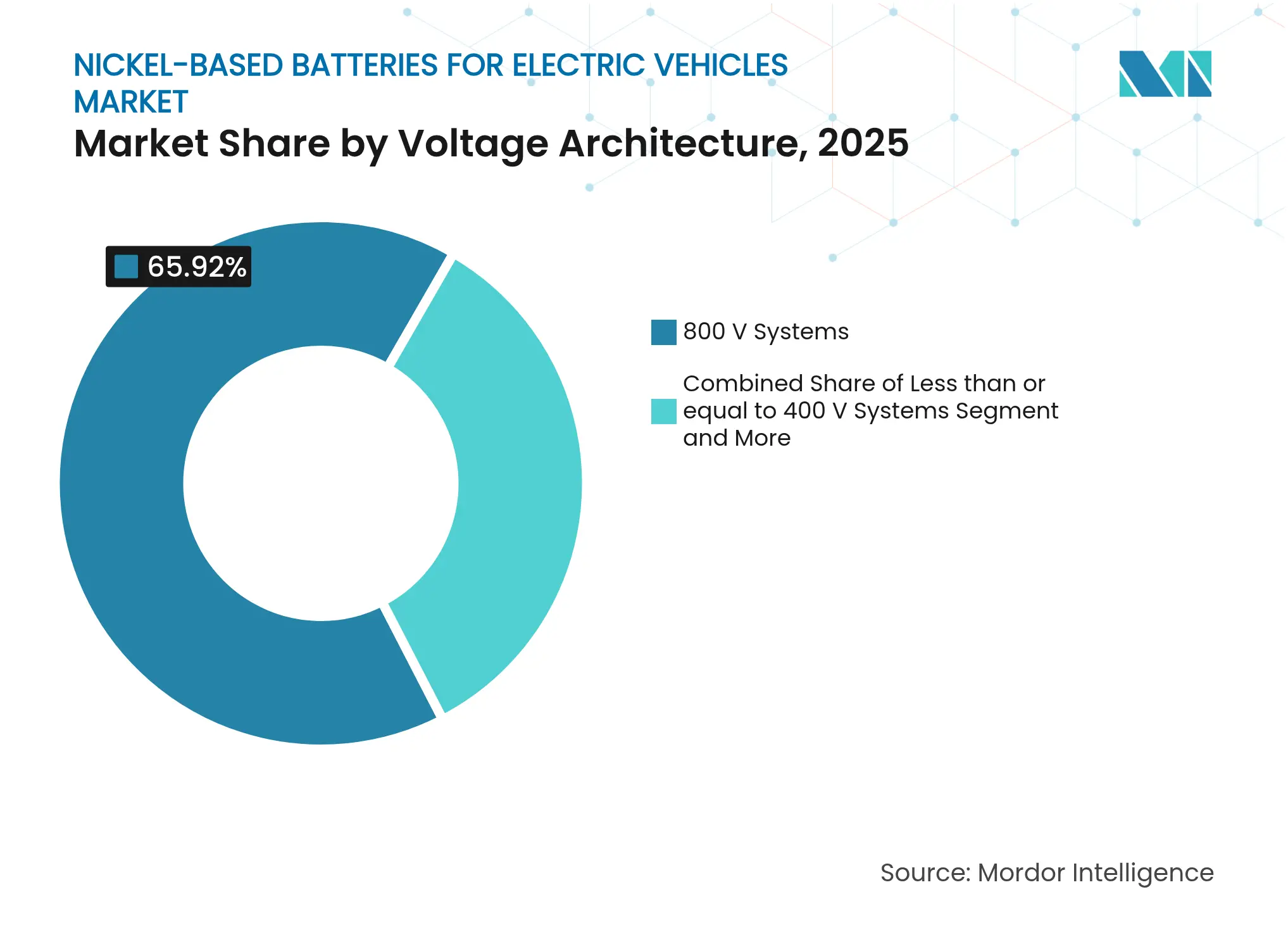

- By voltage architecture, 800 V systems held 65.92% share in 2025; Less than or equal to 400 V systems are set to grow at 4.26% CAGR.

- By end-user, fleet operators contributed 70.65% of demand in 2025, whereas OEM assembly lines are the fastest risers with a 4.11% CAGR.

- By geography, Europe led with 43.95% share in 2025, but Asia Pacific is the quickest climber, advancing at a 4.89% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nickel-based Batteries For Electric Vehicles Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rapid Scale-up of Global EV Production Rapid Scale-up of Global EV Production | +1.2% | Global, with APAC leading at 25.3 kg nickel per battery | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:Global, with APAC leading at 25.3 kg nickel per battery | Impact Timeline:Medium term (2-4 years) |

Aggressive Emissions-Reduction Mandates Aggressive Emissions-Reduction Mandates | +0.8% | Europe & North America, with IRA driving domestic sourcing | Short term (≤ 2 years) | |||

OEM Migration to 800V High-Nickel platforms OEM Migration to 800V High-Nickel platforms | +0.7% | Europe & North America premium segments | Medium term (2-4 years) | |||

Higher Energy Density of Nickel-Rich Chemistries Higher Energy Density of Nickel-Rich Chemistries | +0.6% | Global premium EV segment, concentrated in Europe & North America | Long term (≥ 4 years) | |||

Economies of Scale Lowering USD/kWh Economies of Scale Lowering USD/kWh | +0.4% | Asia-Pacific manufacturing hubs, spill-over to global markets | Medium term (2-4 years) | |||

Commercialization of Closed-Loop Nickel Recovery Commercialization of Closed-Loop Nickel Recovery | +0.3% | North America & Europe, with regulatory support | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rapid Scale-Up of Global EV Production Volumes

Acute growth in vehicle assembly volumes lifts absolute nickel demand even as cathode chemistries diversify. Global cell producers report an 8% year-on-year rise in nickel content per battery, averaging 25.3 kg in 2025, driven by premium SUVs requiring 400-mile range packs.[1]“EV Battery Nickel Use Surges in 2025,” Adamas Intelligence, adamasintelligence.com Panasonic’s USD 4 billion Kansas plant, operational since March 2025, shows industry commitment to domestic capacity, churning out more than 60 cells every second. Yet elevated exposure to premium demand leaves suppliers vulnerable to macro slowdowns that delay flagship-model launches.

Aggressive Emissions-Reduction Mandates & Fiscal Incentives

The United States Inflation Reduction Act earmarks over USD 70 billion in consumer credits and manufacturing grants, triggering unprecedented scrutiny over foreign-entity-of-concern sourcing rules.[2]“Inflation Reduction Act Guidebook,” White House, whitehouse.gov In Europe, fleet-average CO₂ targets tighten to 100 g/km in 2025, accelerating OEM preference for long-range nickel chemistries. Indonesia actively pursues bilateral agreements to keep its ore accessible, illustrating how geopolitical negotiations now steer strategic sourcing pathways.

OEM Migration to 800 V High-Nickel Platforms Enabling Ultra-Fast Charging

Automakers push 800 V topologies to cut charge times to sub-15 minutes for 300 km range replenishment. BMW’s sixth-generation eDrive introduces a cylindrical cell format with 20% higher energy density, while Volvo’s ES90 charges at 1 MW peak, adding 300 km in 10 minutes.[3]“Neue Klasse Battery Technology Details,” BMW Group, bmwgroup.com Silicon-carbide inverters, lighter copper harnesses, and stricter thermal margins reinforce the business case for high-nickel packs capable of sustaining large-current pulses without runaway risk.

Higher Energy Density of Nickel-Rich Chemistries versus LFP

Nickel-rich NCA cathodes regularly reach 260 Wh/kg at the cell level, whereas typical LFP formats remain closer to 160 Wh/kg. The gap is pivotal in long-haul trucks where payload penalties translate directly into lost freight revenue. Recent single-crystal cathode breakthroughs reduce residual lithium by 54%, shrinking early-cycle capacity fade and extending warranty life. Nonetheless, BYD’s blade-design LFP modules narrow volumetric disadvantages, forcing nickel suppliers to intensify R&D targeting more than 90% nickel content cathodes.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rapid Cost Decline of LFP Rapid Cost Decline of LFP | -1.1% | China leading, expanding to Europe & North America | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-1.1% | Geographic Relevance:China leading, expanding to Europe & North America | Impact Timeline:Medium term (2-4 years) |

Volatile Supply and Pricing Volatile Supply and Pricing | -0.9% | Global, with Indonesia controlling 60% of supply | Short term (≤ 2 years) | |||

Solid-State Lithium-Metal Road-Maps Solid-State Lithium-Metal Road-Maps | -0.8% | Global premium-segment planning | Long term (≥4 years) | |||

ESG Backlash ESG Backlash | -0.6% | Indonesia; Western import markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rapid Cost Decline of LFP Eroding Nickel Demand in Mass-Market BEVs

Scaled Chinese lines now deliver LFP packs at less than USD 80/kWh, a threshold that premiumizes nickel batteries outside budget segments. Automakers including Ford and GM pivot toward manganese-rich blends for mid-range cars, trimming cathode nickel intensity. Sodium-ion prototypes priced below USD 60/kWh threaten to remove nickel entirely from entry-level models, relegating nickel to applications where high gravimetric energy remains irreplaceable.

Volatile Supply & Pricing of Class-1 Battery-Grade Nickel

Nickel futures swung between USD 15,000 and USD 15,800 per tonne in early 2025 after landslides disrupted output at Morowali Industrial Park. High-pressure acid leaching waste streams raise environmental scrutiny, threatening access to Western markets. Western governments respond by fast-tracking domestic mine permitting, yet lead times of 7-10 years delay relief. Price uncertainty complicates long-term offtake contracts, discouraging downstream investment in new sulfate conversion facilities.

Segment Analysis

By Propulsion Type: PHEVs Bridge Electrification Gap

Plug-in hybrids contributed 64.08% of nickel-based batteries for electric vehicles market share in 2025, anchoring the nickel based batteries for EV market as automakers use the format to satisfy range expectations without overextending charging infrastructure. This share translates to the largest propulsion slice of the nickel based batteries for EV market size, underscoring its commercial weight. BEVs expand fastest, advancing at 4.93% CAGR, yet deployment hinges on rapid charger density. Hybrids retain relevance where grid capability lags, while fuel cell electric vehicles stay niche due to hydrogen scarcity.

Automakers blend nickel-rich packs into PHEVs to match 100 km electric-only targets set by regulators. Toyota’s historic NiMH reliance gradually gives way to lithium-ion partnerships, evidencing the technology shift. Fleet buyer preference for guaranteed ICE backup cements PHEV volumes, though tax policy shifts toward zero-tailpipe options could moderate growth. The propulsion matrix will therefore continue to allocate nickel primarily toward transitional formats through at least mid-decade.

Note: Segment shares of all individual segments available upon report purchase

By Battery Type: Advanced Ni-Rich Dominates Premium Applications

High-nickel NCA and NCM cathodes captured 50.92% share of nickel-based batteries for electric vehicles market, the single largest chemistry block inside the nickel based batteries for EV market. Continuous design cycles push nickel content beyond 90%, raising cell-level energy while compounding thermal management demands. NiMH cells, favored in hybrids, register the briskest 4.52% CAGR, supported by supply certainty and established recycling channels.

R&D efforts addressing surface microcracking and gas generation in high-nickel cathodes show measurable progress with single-crystal designs. OEM purchasing decisions remain energy-density-centric for luxury sedans and light trucks needing extended highway ranges. In contrast, nickel-cadmium, nickel-iron, and nickel-zinc chemistries persist in aviation ground equipment and stationary backup systems where temperature resilience outweighs gravimetric metrics.

By Vehicle Type: Commercial Fleets Drive Adoption

Commercial trucks, vans, and buses absorbed 62.88% of the 2025 nickel based batteries for EV market size. These operators optimize payload and duty cycle economics, relying on nickel’s high specific energy to balance battery mass against cargo capacity. Passenger cars rise at 4.03% CAGR, yet price sensitivity channels many buyers toward LFP alternatives.

Fleet procurement teams evaluate cents-per-mile over sticker price, leading to long-term service contracts that favor reliable cycle life. Total-cost models show that high-nickel packs, despite higher upfront cost, deliver superior lifetime value in routes exceeding 200 km daily. Two-wheelers and micro-EVs broaden geographic reach of the nickel based batteries for EV market in Southeast Asia, albeit with lower kWh per unit.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Form Factor: Pouch Cells Lead Design Flexibility

Pouch modules held 56.84% share, the highest form-factor stake within the nickel based batteries for EV market. Their thin, stackable geometry achieves superior pack-level volumetric energy, critical in performance-oriented architectures. Cylindrical cells advance at 4.95% CAGR, benefiting from automated winding lines that assure high yield.

European OEMs increasingly specify next-generation prismatic formats from Korean suppliers citing mechanical robustness and simpler thermal paths. Volkswagen’s intention to standardize prismatic units across 80% of future EVs confirms OEM confidence. Pouch swelling risk necessitates sophisticated compression frames and rigorous gas management protocols, raising system cost yet preserving energy advantages.

By Voltage Architecture: 800 V Systems Enable Ultra-Fast Charging

Systems operating at 800 V represented 65.92% nickel-based batteries for electric vehicles market share in 2025, cementing dominance inside the nickel based batteries for EV market. The configuration halves charge times relative to 400 V counterparts, lowering copper mass by up to 40 kg per vehicle. Less than or equal to 400 V platforms, growing at 4.26% CAGR, remain in cost-controlled segments that prioritize component commonality.

Charging-station interoperability challenges spark innovation in multi-voltage onboard converters capable of virtualizing battery segments. Silicon-carbide power modules reduce switching losses at higher voltages, though die cost premiums persist. Manufacturers anticipate More than 800 V prototypes beyond 2027 for heavy-duty trucking, indicating a path to megawatt-class roadside depots.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Fleet Operators Optimize Total Cost

Fleet entities accounted for 70.65% of 2025 demand, standing as the dominant consumption bloc in the nickel based batteries for EV market. Their analytical procurement strategies incorporate cycle life, residual value, and charging downtime into payback equations. OEM assembly lines expand 4.11% annually as automakers internalize cell assembly for strategic control.

Battery leasing models decouple vehicle price from battery depreciation. Honda–Mitsubishi venture ALTNA pits subscription fees against replacement cost, while CATL’s target of implementing massive number of swap stations shows infrastructure emphasis. Aftermarket retrofitters convert legacy trucks, creating a secondary channel for nickel batteries once primary usage ceases.

Geography Analysis

Europe controls 43.95% of global revenue, the highest regional slice of the nickel based batteries for EV market. Stringent fleet-average CO₂ ceilings and battery passport rules require traceability of nickel origin, encouraging vertically integrated supply chains. Regional refining could satisfy 70% of future demand if projects reach nameplate capacity, yet only 100 kt of waste batteries entered commercial recyclers in 2024.

Asia Pacific posts the quickest 4.89% CAGR, driven by manufacturing hub economies and plentiful raw materials. China consumed more than 340,000 t of nickel in the EV sector for 2025, dwarfing other regions. Indonesia’s ban on ore exports and expansion of HPAL lines raise domestic value addition in 2024. South Korean suppliers diversify into LFP and manganese-rich lines to meet US trade requirements, while Japan forges partnerships with Canada and Australia to lessen Chinese dependency.

North America benefits from the Inflation Reduction Act’s funding pool, translating into multiple gigafactory break-ground events. Panasonic’s Kansas site can equip over 1 million EVs annually when fully ramped. Redwood Materials’ Nevada hub claims 95% nickel recovery rates, closing material loops. The lack of a full-scale domestic nickel refinery remains a critical supply-chain gap, necessitating Canadian feedstock imports that elevate carbon footprints.

Competitive Landscape

Market Concentration

The nickel based batteries for EV market exhibits a moderate oligopoly as the top three cell makers—CATL, BYD, and LG Energy Solution. Their scale enables coordinated pricing and preferential access to class-1 nickel contracts. Vertical integration shapes strategy: CATL expands from cell production into swap stations, BYD cultivates blade-cell intellectual property, and LG intensifies high-nickel cathode research to surpass 90% nickel content.

Supply diversification drives partnership announcements between automakers and mining firms, locking in feedstock for a decade or more. Closed-loop recycling evolves from pilot to commercial scale; Redwood Materials’ facility expects to supply cathode material for 1.3 million EVs yearly by 2028. Solid-state aspirants led by QuantumScape and Toyota target commercialization windows between 2027 and 2029, giving incumbents time to enhance current chemistries.

White-space opportunity remains in off-highway equipment, mining trucks, and marine propulsion where rugged duty cycles value high-energy density. Battery integrators eye multi-chemistry pack architectures that stack nickel-rich modules with LFP cells to tune cost and range. Competitive intensity is likely to heighten as sodium-ion cells threaten entry-level segments, leading nickel providers to underscore performance differentiators.

Nickel-based Batteries For Electric Vehicles Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Nissan and SK On signed a USD 661 million multi-year EV battery supply contract solidifying long-term cell procurement strategies.

- February 2025: BMW Group launched sixth-generation eDrive with 800 V architecture and cylindrical nickel-based cells delivering 20% higher energy density.

- December 2024: CATL confirmed plans for 1,000 battery-swap stations by year-end, offering packs compatible with 80% of current EV models.

Table of Contents for Nickel-based Batteries For Electric Vehicles Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rapid scale-up of global EV production volumes

- 4.2.2Aggressive emissions-reduction mandates & fiscal incentives

- 4.2.3OEM migration to 800-V high-nickel platforms enabling ultra-fast charging

- 4.2.4Higher energy density of nickel-rich chemistries versus LFP

- 4.2.5Economies of scale lowering $/kWh for nickel batteries

- 4.2.6Commercialisation of closed-loop nickel recovery

- 4.3Market Restraints

- 4.3.1Rapid cost decline of LFP eroding nickel demand in mass-market BEVs

- 4.3.2Volatile supply & pricing of class-1 battery-grade nickel

- 4.3.3Solid-state lithium-metal road-maps threaten long-term relevance

- 4.3.4ESG backlash over Indonesian HPAL nickel projects

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers/Consumers

- 4.7.3Threat of New Entrants

- 4.7.4Intensity of Competitive Rivalry

- 4.7.5Threat of Substitute Products

5. Market Size & Growth Forecasts (Value (USD))

- 5.1By Propulsion Type

- 5.1.1Battery Electric Vehicles (BEV)

- 5.1.2Hybrid Electric Vehicles (HEV)

- 5.1.3Plug-in Hybrid Electric Vehicles (PHEV)

- 5.1.4Fuel Cell Electric Vehicles (FCEV)

- 5.2By Battery Type

- 5.2.1Nickel Metal Hydride (NiMH)

- 5.2.2Nickel Cadmium (NiCd)

- 5.2.3Nickel-Iron

- 5.2.4Nickel-Zinc

- 5.2.5Advanced Ni-rich Li-ion (NCA/NCM More than 70 % Ni)

- 5.3By Vehicle Type

- 5.3.1Passenger Cars

- 5.3.2Commercial Vehicles

- 5.3.3Two- & Three-Wheelers

- 5.3.4Off-Highway & Special-purpose EVs

- 5.4By Form Factor

- 5.4.1Cylindrical

- 5.4.2Prismatic

- 5.4.3Pouch

- 5.5By Voltage Architecture

- 5.5.1Less than or equal to 400 V Systems

- 5.5.2800 V Systems

- 5.5.3More than 800 V Systems

- 5.6By End-User

- 5.6.1OEM Assembly Lines

- 5.6.2Battery Leasing / BaaS Providers

- 5.6.3Fleet Operators

- 5.6.4Aftermarket / Retrofitters

- 5.7By Geography

- 5.7.1North America

- 5.7.1.1United States

- 5.7.1.2Canada

- 5.7.1.3Rest of North America

- 5.7.2South America

- 5.7.2.1Brazil

- 5.7.2.2Argentina

- 5.7.2.3Rest of South America

- 5.7.3Europe

- 5.7.3.1Germany

- 5.7.3.2France

- 5.7.3.3United Kingdom

- 5.7.3.4Italy

- 5.7.3.5Spain

- 5.7.3.6Netherlands

- 5.7.3.7Russia

- 5.7.3.8Rest of Europe

- 5.7.4Asia Pacific

- 5.7.4.1China

- 5.7.4.2Japan

- 5.7.4.3South Korea

- 5.7.4.4India

- 5.7.4.5ASEAN

- 5.7.4.6Australia

- 5.7.4.7Rest of Asia Pacific

- 5.7.5Middle East and Africa

- 5.7.5.1Saudi Arabia

- 5.7.5.2United Arab Emirates

- 5.7.5.3Egypt

- 5.7.5.4Turkey

- 5.7.5.5South Africa

- 5.7.5.6Rest of Middle East and Africa

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1Panasonic Energy Co., Ltd.

- 6.4.2Primearth EV Energy Co., Ltd.

- 6.4.3BYD Company Ltd.

- 6.4.4GS Yuasa International Ltd.

- 6.4.5LG Energy Solution Ltd.

- 6.4.6Samsung SDI Co., Ltd.

- 6.4.7Saft Groupe SAS

- 6.4.8VARTA AG

- 6.4.9EnerSys

- 6.4.10FDK Corporation

- 6.4.11AESC (Envision)

- 6.4.12Duracell Inc.

- 6.4.13GP Batteries International Ltd.

- 6.4.14HBL Power Systems Ltd.

- 6.4.15Alcad AB

- 6.4.16Leclanché SA

- 6.4.17OptimumNano Energy

- 6.4.18Farasis Energy

- 6.4.19SVOLT Energy Technology

- 6.4.20Contemporary Amperex Technology Co. Limited (CATL)

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Segmentation Overview

- By Propulsion Type

- Battery Electric Vehicles (BEV)

- Hybrid Electric Vehicles (HEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Fuel Cell Electric Vehicles (FCEV)

- Battery Electric Vehicles (BEV)

- By Battery Type

- Nickel Metal Hydride (NiMH)

- Nickel Cadmium (NiCd)

- Nickel-Iron

- Nickel-Zinc

- Advanced Ni-rich Li-ion (NCA/NCM More than 70 % Ni)

- Nickel Metal Hydride (NiMH)

- By Vehicle Type

- Passenger Cars

- Commercial Vehicles

- Two- & Three-Wheelers

- Off-Highway & Special-purpose EVs

- Passenger Cars

- By Form Factor

- Cylindrical

- Prismatic

- Pouch

- Cylindrical

- By Voltage Architecture

- Less than or equal to 400 V Systems

- 800 V Systems

- More than 800 V Systems

- Less than or equal to 400 V Systems

- By End-User

- OEM Assembly Lines

- Battery Leasing / BaaS Providers

- Fleet Operators

- Aftermarket / Retrofitters

- OEM Assembly Lines

- By Geography

- North America

- United States

- Canada

- Rest of North America

- United States

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Germany

- Asia Pacific

- China

- Japan

- South Korea

- India

- ASEAN

- Australia

- Rest of Asia Pacific

- China

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Egypt

- Turkey

- South Africa

- Rest of Middle East and Africa

- Saudi Arabia

- North America

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Mordor's Nickel-based Batteries For Electric Vehicles Baseline Holds True

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 2.37 Bn (2025) | Mordor Intelligence | Anonymized source:Mordor Intelligence | Primary gap driver: | |

USD 3.41 Bn (2024) | Global Consultancy A | Counts hybrid buses and motorcycles, projects continuous 27 % growth without price normalization | ||

USD 2.50 Bn (2024) | Trade Journal B | Limits scope to NiMH and NiCd and fixes pack ASP at 2023 levels | ||

USD 2.25 Bn (2025) | Regional Analyst C | Excludes nickel-rich NMC / NCA cells and omits regional mix adjustments |