Forklift Battery Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 6.55 Billion |

| Market Size (2031) | USD 9.37 Billion |

| Growth Rate (2026 - 2031) | 7.41% CAGR |

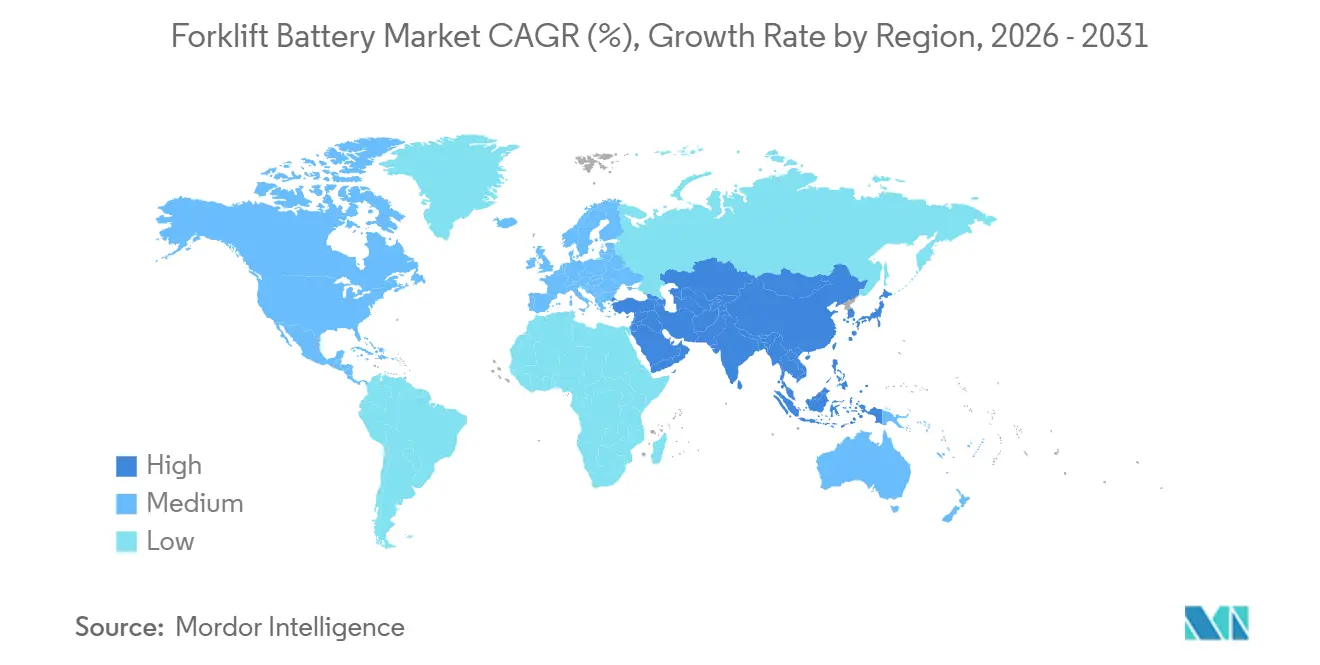

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

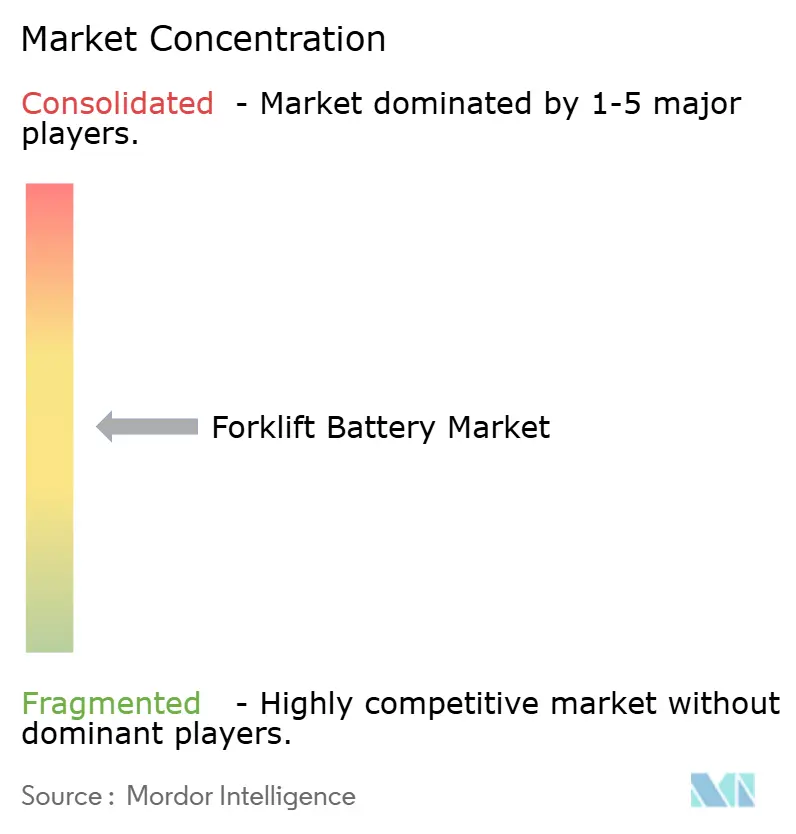

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Forklift Battery Market Analysis by Mordor Intelligence

The forklift battery market size is expected to increase from USD 6.10 billion in 2025 to USD 6.55 billion in 2026 and is forecast to reach USD 9.37 billion by 2031, growing at a CAGR of 7.41% during the forecast period (2026-2031). As e-commerce fulfillment density increases and zero-emission mandates become stricter, the shift toward electrification in material handling is gaining momentum. This trend is further supported by lithium-ion batteries achieving cost competitiveness with lead-acid alternatives on a total cost-of-ownership basis. Lithium-ion battery prices are expected to continue declining, removing the remaining barriers to widespread adoption. California’s Advanced Clean Fleets rule requires high-priority fleets to exclusively purchase zero-emission forklifts, a regulation anticipated to be adopted by other U.S. states. In the cold chain sector, operators are increasingly opting for lithium-iron-phosphate batteries, which retain a high percentage of capacity at low temperatures, thereby reducing the need for additional battery sets in refrigerated warehouses.

Key Report Takeaways

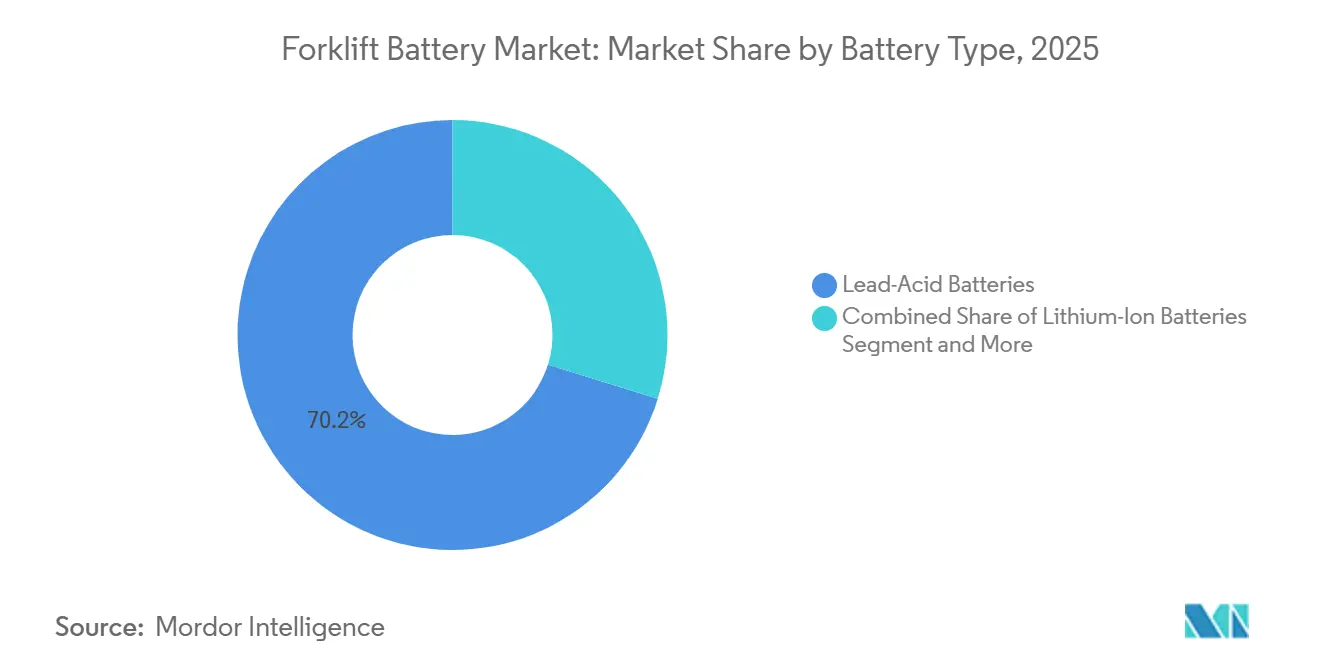

- By battery type, lead-acid led with 70.21% of the forklift battery market share in 2025, whereas lithium-ion is projected to have the highest growth at an 8.11% CAGR through 2031.

- By voltage capacity, the 24-36V class accounted for 38.22% of the forklift battery market share in 2025, while 36-48V systems are forecast to expand at an 8.28% CAGR through 2031.

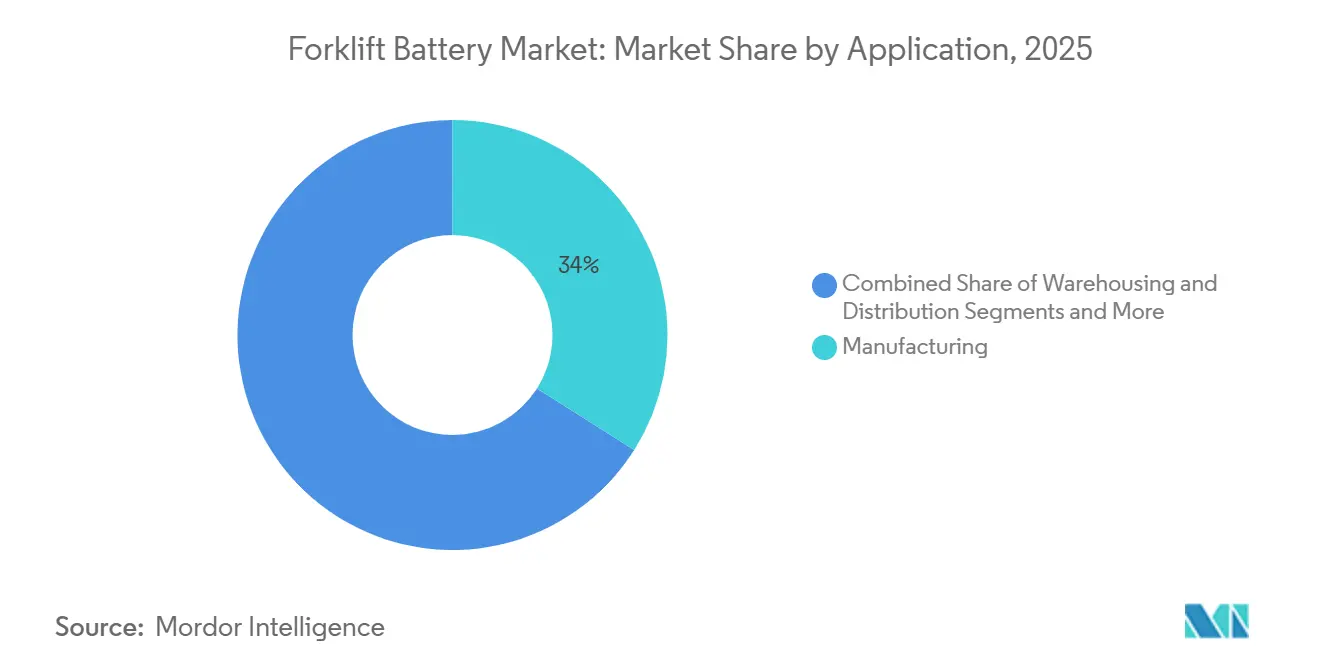

- By application, manufacturing accounted for 33.98% of the forklift battery market share in 2025, and warehousing and distribution are advancing fastest at a 7.93% CAGR through 2031.

- By sales channel, OEM deliveries accounted for 56.16% of the forklift battery market share in 2025, while the aftermarket is growing briskly at a 7.91% CAGR through 2031.

- By geography, Asia-Pacific commanded 46.34% of the forklift battery market share in 2025 and continues to lead growth at a 7.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Forklift Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Falling Li-Ion Costs and TCO Advantage | +1.5% | Global, strongest in North America and Europe due to higher labor/energy costs | Short term (≤ 2 years) |

| E-Commerce and Warehouse-Automation Boom | +1.2% | Global, concentrated in North America, Europe, Asia-Pacific logistics hubs | Medium term (2-4 years) |

| Stricter Zero-Emission Regulations | +1.0% | North America (California, New York), Europe (EU Battery Regulation), China (NEV mandates) | Long term (≥ 4 years) |

| Cold-Chain and 3PL Multi-Shift Demand | +0.9% | North America and Europe (food safety, pharmaceutical logistics), Asia-Pacific (cold-chain build-out) | Medium term (2-4 years) |

| Battery-as-a-Service Models Lowering Capex | +0.7% | Europe and North America (fleet operators, 3PLs), nascent in Asia-Pacific | Long term (≥ 4 years) |

| AI-Enabled BMS for Energy Optimization | +0.6% | Global, early adoption in North America and Europe automated warehouses | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Falling Li-ion Costs and TCO Advantage

Average prices for lithium-ion battery packs have significantly declined in recent years, with further reductions expected as advancements in cathode scaling and cell-to-pack integration continue. Lithium-iron-phosphate (LFP) packs, which are considerably cheaper than their nickel-manganese-cobalt counterparts, now dominate a substantial portion of global electric vehicle (EV) battery installations, offering forklift buyers notable economies of scale. By removing the need for watering labor, ventilation equipment, and dedicated battery rooms, operators can achieve significant reductions in total operating costs compared to traditional lead-acid systems. Additionally, regenerative braking in lithium systems recovers a higher percentage of energy than in lead-acid systems, resulting in lower electricity costs, particularly in high-throughput environments. The cost benefits extend beyond the battery packs themselves; for example, transitioning to electric equipment in enclosed operations has demonstrated substantial annual savings, primarily due to reduced ventilation requirements.

E-commerce and Warehouse-Automation Boom

As online retail surges, it's reshaping the distribution landscape. Every increase in e-commerce penetration drives significant demand for additional warehouse space. Modern warehouses, dominated by multi-shift forklift operations, are increasingly turning to lithium-ion batteries. These batteries allow for opportunity charging without the risk of voltage sag. Highlighting the trend, Geekplus’ cold-chain automation for JJCL significantly increased storage density and boosted picking efficiency. Such robotic advancements are proving instrumental in hastening the payback period for lithium battery retrofits. The transition from traditional retail stores to specialized fulfillment hubs has greatly increased the distribution space required per sales dollar. This shift has intensified the demand for sealed, maintenance-free battery chemistries. With many shippers now anticipating faster delivery times, the reliance on multi-shift duty cycles has surged. However, lead-acid batteries are struggling to keep pace with this increased demand.

Stricter Zero-Emission Regulations

California mandates the purchase of zero-emission forklifts for high-priority fleets, with a complete fleet conversion required over time. The European Union's Battery Regulation introduces carbon footprint disclosures and recycled-content thresholds, encouraging a shift away from lead-acid batteries toward recyclable lithium chemistries. China's New Energy Vehicle policy channels surplus cell capacity into industrial sectors, increasing lithium availability for lift-truck OEMs. Municipal contracts are increasingly prioritizing vendors with certified lithium solutions as compliance audits tied to environmental and safety standards become standard bidding requirements. Regions such as Los Angeles and the Rotterdam port districts demonstrate how local air-quality regulations can drive adoption ahead of broader national policies[1]“Advanced Clean Fleets,” California Air Resources Board, arb.ca.gov.

Cold-Chain and 3PL Multi-Shift Demand

LFP cells retain a higher capacity at cold temperatures than lead-acid batteries, eliminating the need for double battery sets in refrigerated warehouses. Geekplus demonstrated lithium's resilience in low temperatures by significantly increasing throughput at a frozen-food distribution center after upgrading forklifts to electric models. Many shippers now prioritize faster delivery times, pushing third-party logistics (3PL) operators to adopt continuous duty cycles, which lithium batteries support without the risk of sulfation. Food-and-beverage warehouses are adopting sealed lithium battery packs to comply with USDA hygiene standards, as vented lead-acid batteries cannot meet them. Lithium forklifts, operating at higher efficiency, enable faster lift speeds, reducing cycle times in high-frequency cold-storage aisles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Li-ion Recycling Infrastructure and Liability Risks | -0.7% | Europe and North America (strict regulatory mandates), nascent in Asia-Pacific and South America | Long term (≥ 4 years) |

| LFP-Cathode Precursor Supply Volatility | -0.6% | Global, supply concentrated in China; affects North America and Europe most | Long term (≥ 4 years) |

| Sparse Fast-Charging Infrastructure | -0.5% | North America and Europe outside major logistics corridors; Asia-Pacific tier-2/3 cities | Medium term (2-4 years) |

| OEM-Warranty Complexity on Retrofits | -0.3% | Global, concentrated in North America and Europe legacy fleets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Li-ion Recycling Infrastructure and Liability Risks

Europe's Battery Regulation mandates recycled-content thresholds for cobalt, lithium, and nickel, alongside ambitious collection targets. However, with China dominating global battery recycling, Europe and North America face challenges due to limited local facilities. The lack of closed-loop networks forces operators to export end-of-life packs or landfill them, exposing suppliers to extended producer responsibility liabilities and increased recycling costs. Rising thermal runaway incidents at recycling yards have also driven up insurance premiums, discouraging mid-size fleets from adopting lithium without costly fire-suppression upgrades. Mandatory digital battery passports will require material tracing, adding costs for smaller suppliers without advanced IT systems. Northvolt's Ett plant, which struggled with low utilization before insolvency, highlights the impact of declining lithium prices and high labor costs on Europe's domestic recycling efforts.

Sparse Fast-Charging Infrastructure

Operators are often left to self-fund DC fast-chargers, which can be highly expensive per site, as national freight-charging programs frequently overlook warehouse material-handling. While significant funding has been allocated for heavy-truck hubs in some regions, forklift chargers are scarce, especially outside major logistics zones. Current lead-acid chargers operate at low charging rates, which do not meet the charging profile required for lithium cells. This discrepancy necessitates costly electrical upgrades. Furthermore, connector standardization is lagging; for instance, while REMA's hot-pluggable couplings feature embedded temperature sensors, they haven't achieved universal adoption, resulting in interoperability challenges. Recent tariffs have increased the landed prices of imported DC chargers, extending the payback periods for related infrastructure projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Lithium-Ion Gains Despite Lead-Acid Dominance

Lead-acid batteries accounted for 70.21% of the forklift battery market share in 2025, mainly due to entrenched service ecosystems and compatibility with legacy chargers. Still, lithium-ion units are projected to grow at an 8.11% CAGR through 2031, as total ownership costs drop by about 40% below those of lead-acid, especially in multi-shift and cold-storage sites. While solid-state systems are still in the experimental phase, nickel-metal-hydride technology remains a niche player, with pack prices exceeding USD 400/kWh.

The rise of lithium technology is supported by the introduction of user-friendly retrofit kits. For example, BSLBATT launched a drop-in series featuring UL-certified modules compatible with trucks from brands such as Toyota, Hyster, Linde, and Jungheinrich. In contrast, AGM and enhanced-flooded lead-acid variants, like GS Yuasa’s YBX9625, offer extended cycle life but cannot match lithium’s superior energy density and rapid charging capabilities.

By Voltage Capacity: 48V Systems Capture Heavy-Duty Shift

The 24-36V class owned 38.22% of the forklift battery market share in 2025, suitable for single-shift pallet trucks and order pickers. Yet 36-48V solutions will expand at an 8.28% CAGR through 2031. Heavy-duty warehouses are now prioritizing equipment that offers significantly higher torque and faster lifts. Additionally, operating at a higher voltage reduces resistive losses, enabling notable energy recuperation.

Despite substantial conversion costs per truck, cold-chain and food-service fleets remain undeterred, emphasizing the need for reliable low-temperature performance and hygienically sealed housings. The market's gradual shift towards higher voltage is evident in OEM launches, such as EP North America's model featuring a lithium pack and onboard charging.

By Application: Warehousing Outpaces Manufacturing

Manufacturing accounted for 33.98% of the forklift battery market share in 2025 across automotive, aerospace, and electronics. Yet, warehousing and distribution will advance at a 7.93% CAGR as e-commerce drives incremental space and multi-shift forklift utilization. While the construction and mining sectors, albeit with a smaller share, are turning to lithium to achieve zero-emission goals and realize ventilation savings.

Logistics hubs are increasingly seeking opportunities to charge and use sealed chemistries, ensuring adherence to food-grade regulations and commitments to fast delivery timelines. In manufacturing, where replacement cycles are longer, the adoption of lithium lags behind the quicker refresh rate seen in fulfillment centers.

By Sales Channel: Aftermarket Retrofits Accelerate

Original Equipment Manufacturer (OEM) deliveries controlled 56.16% of the forklift battery market share in 2025 by bundling batteries with new trucks and offering unified warranties. Nonetheless, the aftermarket will climb at a 7.91% CAGR as drop-in lithium kits let fleets prolong chassis life while trimming maintenance costs.

BSLBATT's lithium battery models have obtained UL Solutions Revision 3 certificates, alleviating liability concerns that previously hindered retrofits. In response, OEMs are introducing integrated lithium-ion models, such as EP North America's CPD series, to secure customers within their factory ecosystems.

Geography Analysis

Asia-Pacific captured 46.34% of the forklift battery market share in 2025 and is on course for a 7.89% CAGR through 2031, as China dominates the global lithium-ion cell capacity with a significant share, while India has made substantial commitments to gigafactories [2]“India Lithium-Ion Gigafactory Investments,” Autocar Professional, autocarpro. in. CATL, a major player, supplies a large portion of the world's EV and grid-storage batteries. This dominance allows regional integrators to price forklift packs significantly lower than their Western counterparts. In line with Japan's ambitious goal of carbon neutrality, BSLBATT has strategically opened hubs in key locations [3]"BSLBATT Establishes Subsidiary to Strengthen Presence in Japan", BSL NEW ENERGY TECHNOLOGY CO., LTD, bslbatt.com.

Europe's market is under the purview of regulations mandating carbon-footprint disclosures and setting recycled-content benchmarks. Due to higher energy and labor costs, European cell manufacturers are considerably pricier than their Chinese counterparts. The recent bankruptcy of a major European manufacturer underscores the financial risks in the region. While Germany invests in charging infrastructure for heavy trucks, facilities for forklifts remain limited. This scarcity has led warehouse operators to take the initiative, self-financing their own chargers.

California's clean fleet policies are pivotal drivers in North America. Cold-storage facilities are increasingly adopting LFP packs, reaping benefits from their superior low-temperature capacity retention. This transition diminishes the need for redundant battery sets. Tariffs led to a notable surge in the landed cost of Chinese electrical gear. Consequently, many assemblers shifted their sourcing, now opting for cells from Korea or Japan. Despite high capital costs, South America shows promise: Brazil's e-commerce and Argentina's mining sectors are driving a burgeoning demand for lithium. In the Middle East, Saudi Arabia's retrofitting initiatives highlighted lithium's capabilities in extreme heat and challenging conditions.

Competitive Landscape

Market concentration remains moderate. Incumbents like EnerSys, East Penn, and Exide defend their established bases, while newcomers from China, such as BSLBATT and Narada Power, make inroads into North America and Europe. These Chinese firms offer UL-certified packs at significantly lower prices. Moreover, their vertical integration in cathode refining gives them a cost advantage that Western suppliers find hard to match without subsidies.

Three strategic patterns emerge. First, vertical integration: Amara Raja and Exide invest heavily in Indian cell plants to reduce imports. Second, modular product design: BSLBATT’s advanced cases are designed to accommodate various forklift brands, streamlining engineering processes. Third, financing innovation: The Battery-as-a-Service model holds promise for broader adoption among small fleets, contingent on the maturation of warranty terms and residual-value calculations.

Certification evolves into a competitive barrier. Listings from UL Solutions and EU battery passports introduce compliance costs that could be burdensome for smaller assemblers. In response, incumbents like EnerSys and GS Yuasa refresh their product lines—introducing offerings like the NexSys TPPL and YBX9625 AGM—to extend the relevance of lead-acid batteries, even as lithium prices decline.

Forklift Battery Industry Leaders

-

Crown Equipment Corporation

-

East Penn Manufacturing Company

-

Enersys

-

Amara Raja Batteries Ltd.

-

Exide Industries Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Kalmar has unveiled its next-gen lithium-ion (Li-ion) battery solution, designed for its suite of electric counterbalanced equipment, including reachstackers, empty container handlers, and forklifts. This upgraded battery system boasts greater energy capacity, superior thermal stability, and a consistent performance curve, ensuring reliability across diverse operating conditions.

- March 2025: Bobcat unveiled its new Li-ION battery range, boasting multiple capacity options, at LogiMAT 2025. Developed in-house, this dependable, high-quality battery technology will be integrated across all Bobcat series. Offering a lifespan 2–3 times that of traditional lead-acid batteries and featuring rapid, efficient charging, these lithium batteries promise enhanced flexibility in work operations.

Global Forklift Battery Market Report Scope

The forklift battery market report is segmented by battery type (lead-acid, lithium-ion, nickel-metal hydride, and others), voltage capacity (below 24V, 24V-36V, 36V-48V, and above 48V), application (warehousing and distribution, manufacturing, construction, mining, retail and wholesale, and others), sales channel (OEM and aftermarket), and geography. The Market forecasts are provided in terms of value (USD).

| Lead-Acid Batteries |

| Lithium-Ion Batteries |

| Nickel-Metal Hydride (NiMH) |

| Others (incl. Solid-State) |

| Below 24V |

| 24V - 36V |

| 36V - 48V |

| Above 48V |

| Warehousing and Distribution |

| Manufacturing |

| Construction |

| Mining |

| Retail and Wholesale |

| Others |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Turkey | |

| Rest of Middle East and Africa |

| By Battery Type | Lead-Acid Batteries | |

| Lithium-Ion Batteries | ||

| Nickel-Metal Hydride (NiMH) | ||

| Others (incl. Solid-State) | ||

| By Voltage Capacity | Below 24V | |

| 24V - 36V | ||

| 36V - 48V | ||

| Above 48V | ||

| By Application | Warehousing and Distribution | |

| Manufacturing | ||

| Construction | ||

| Mining | ||

| Retail and Wholesale | ||

| Others | ||

| By Sales Channel | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What CAGR is the forklift battery market projected to post between 2026 and 2031?

The forklift battery market is expected to grow at a 7.41% CAGR over 2026-2031, rising from USD 6.55 billion in 2026 to USD 9.37 billion by 2031.

Which chemistry is growing fastest in forklift batteries?

Lithium-ion, particularly lithium-iron-phosphate, is forecast to expand at an 8.11% CAGR, outpacing all other chemistries.

How do zero-emission regulations affect forklift battery choices?

Rules such as California’s Advanced Clean Fleets and EU Battery Regulation 2023/1542 push fleets toward zero-emission forklifts, accelerating lithium-ion adoption well before 2031.

Which region accounts for the largest share of forklift battery demand?

Asia-Pacific leads with 46.34% of global revenue thanks to China’s dominant cell production capacity and India’s growing gigafactory pipeline.

Page last updated on: