EV Solid-state Battery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

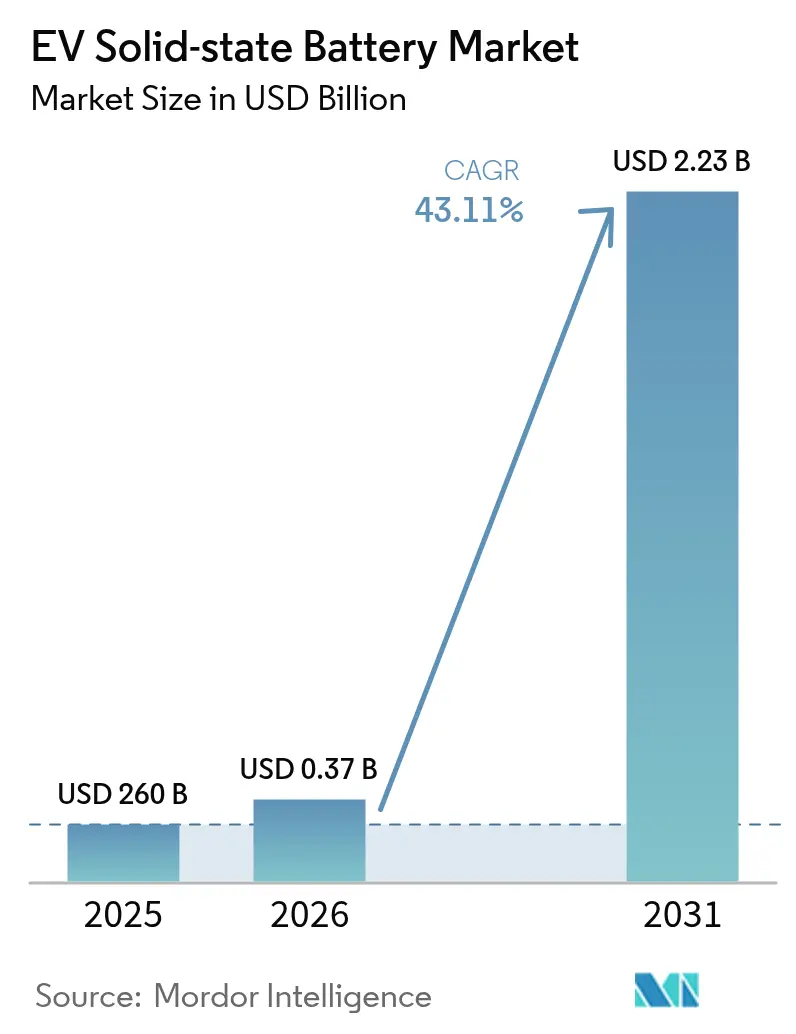

| Market Size (2026) | USD 0.37 Billion |

| Market Size (2031) | USD 2.23 Billion |

| Growth Rate (2026 - 2031) | 43.11% CAGR |

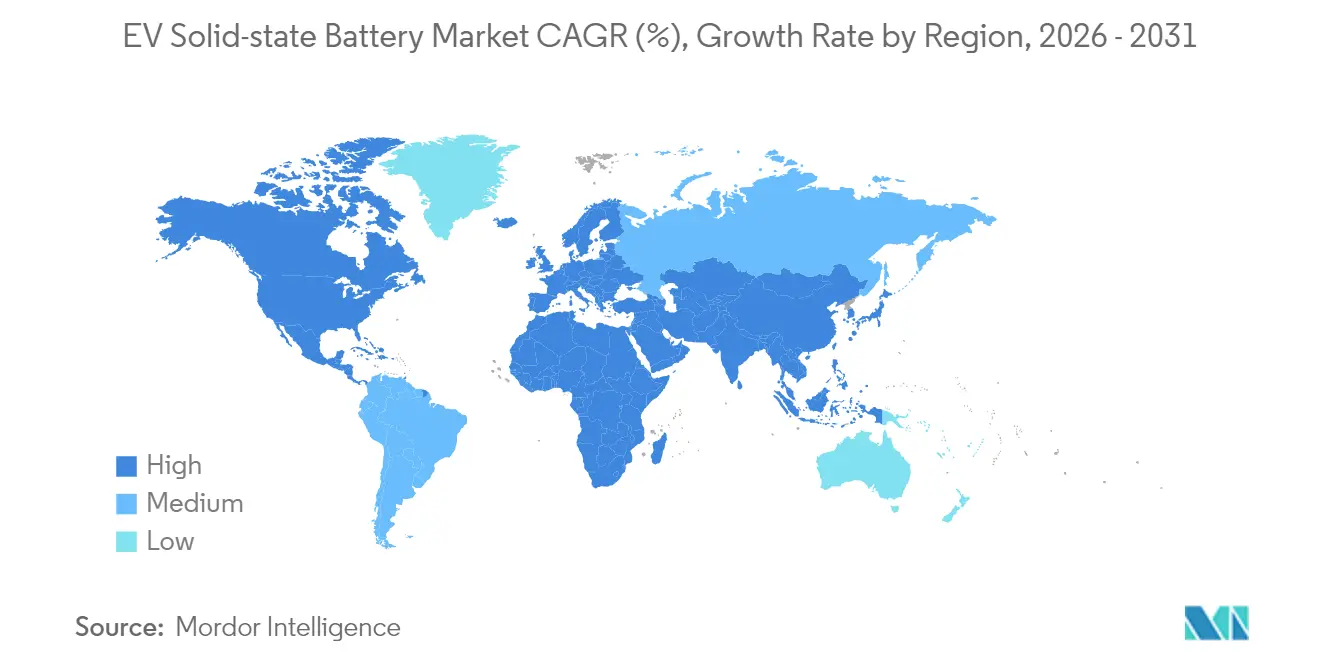

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

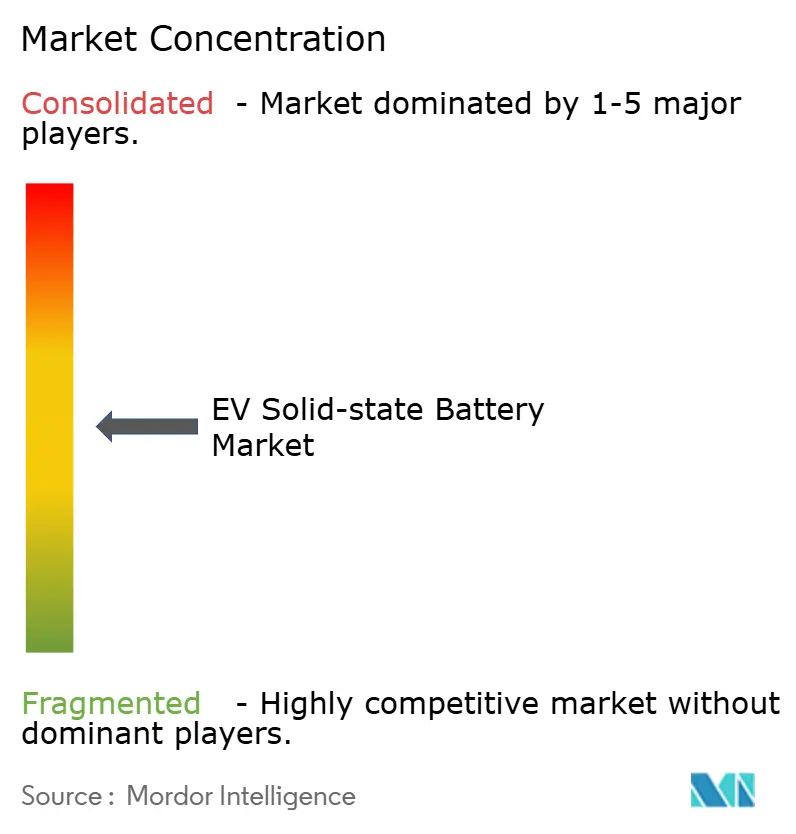

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

EV Solid-state Battery Market Analysis by Mordor Intelligence

EV solid-state battery market size in 2026 is estimated at USD 372.09 million, growing from 2025 value of USD 260 million with 2031 projections showing USD 2.23 billion, growing at 43.11% CAGR over 2026-2031. Intensifying zero-emission vehicle mandates, rapid advances in sulfide electrolyte processing, and automakers’ pilot-line investments are converging to accelerate adoption. Passenger cars remain the launchpad for commercial deployment, while commercial fleets register stronger incremental growth as operators recognise the technology’s lifetime cost advantages. Asia-Pacific leads global shipments, buoyed by integrated supply chains in Japan, South Korea, and China. Meanwhile, capacity additions in North America and Europe point to a broader geographic spread once manufacturing yields improve. Strategic risks concentrate around lithium-metal foil availability and roll-to-roll yield losses, but recent breakthroughs in anode-free cell formation and improved moisture-tolerant electrolytes are narrowing these gaps.

Key Report Takeaways

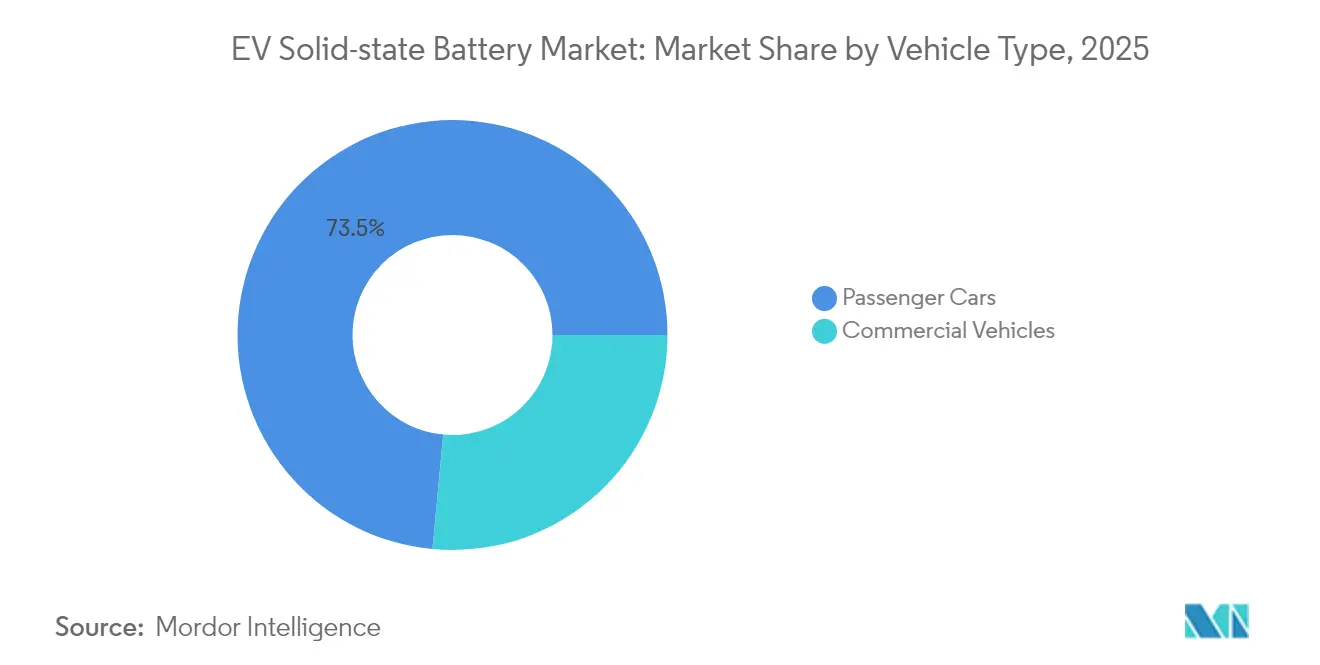

- By vehicle type, passenger cars led with 73.52% of the solid-state battery market share in 2025; commercial vehicles are projected to post the fastest 38.95% CAGR to 2031.

- By propulsion, battery electric vehicles (BEVs) accounted for 69.45% of the solid-state battery market size in 2025, and the segment is expected to rise at a 38.60% CAGR through 2031.

- By solid electrolyte type, sulfide chemistries commanded 46.92% market share in 2025, while oxide systems are forecast to expand at 30.25% CAGR to 2031.

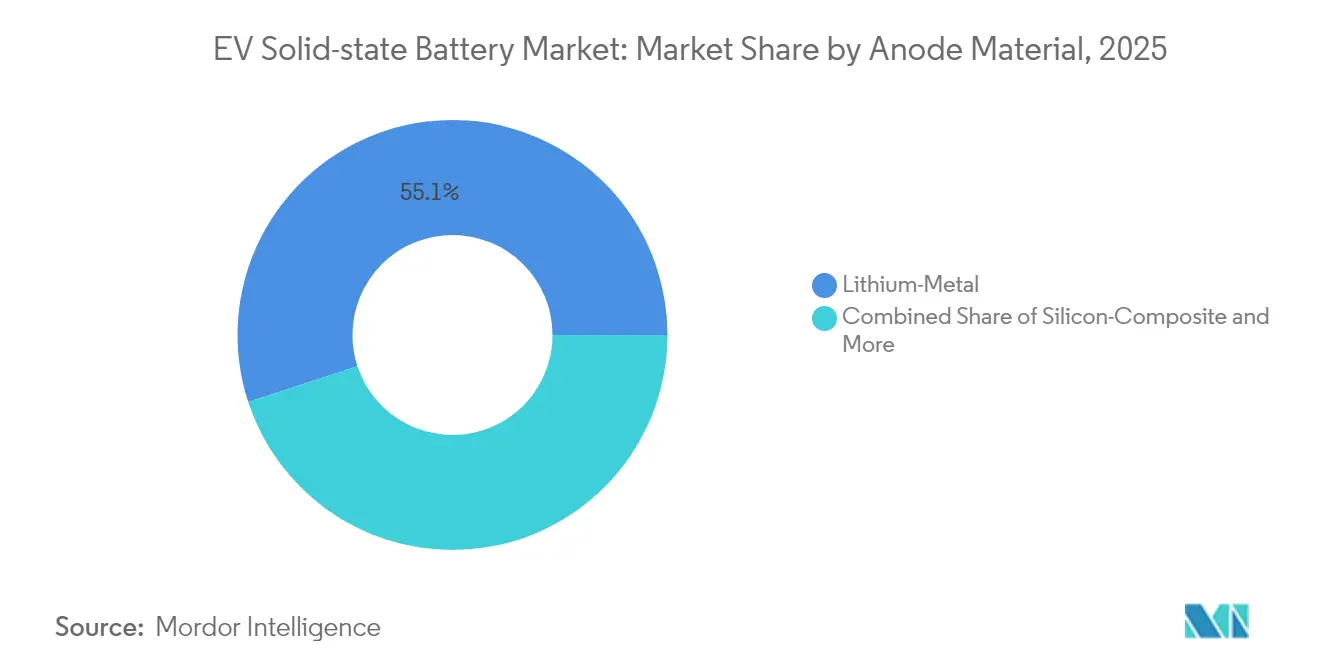

- By anode material, lithium-metal captured 55.05% share of the solid-state battery market size in 2025 and is advancing at a 44.10% CAGR between 2026 and 2031.

- By battery capacity, 20–100 Ah cells held 47.95% revenue share in 2025; cells above 100 Ah are projected to register the strongest 41.90% CAGR through 2031.

- By geography, Asia-Pacific dominated with 40.85% market share in 2025, whereas the Middle East and Africa are forecast to expand at a 35.40% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global EV Solid-state Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid EV Sales Expansion | +13.6% | Global, with concentration in China, Europe, North America | Medium term (2-4 years) |

| Energy Density and Safety Edge | +9.1% | Global, early adoption in premium segments | Long term (≥ 4 years) |

| ZEV Mandates and Incentives | +8.2% | North America, Europe, China | Short term (≤ 2 years) |

| Automaker Vertical Integration | +6.4% | Asia-Pacific, Europe, North America | Medium term (2-4 years) |

| Sulfide Roll-To-Roll Breakthroughs | +5.4% | Asia-Pacific core, spill-over to global manufacturing | Medium term (2-4 years) |

| Insurance Fire-Liability Pressure | +3.6% | North America & EU, regulatory-driven markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid growth in global EV sales volumes

Global electric-vehicle sales are expected to top 20 million units in 2025, roughly triple 2021 levels, intensifying automakers’ search for batteries that charge faster and go farther[1]International Energy Agency, “Global EV Outlook 2025,” iea.org. China’s production dominance gives Asian cell makers early-scale advantages, while commercial-fleet electrification widens demand beyond consumer segments. Larger pack orders allow suppliers to push pilot lines toward higher equipment utilisation, in turn lowering per-kilowatt-hour costs. These dynamics collectively lift the solid-state battery market by expanding both the addressable vehicle pool and the willingness of buyers to pay technology premiums. Regional variations persist, but the overall trajectory remains upward as safety and range anxieties decline.

Energy-density and safety edge over Li-ion packs

Solid-state prototypes routinely exceed 500 Wh/kg, far above the 250–300 Wh/kg range of conventional lithium-ion packs, driving innovation in the EV Solid-state Battery Market, and recent laboratory work reports ionic conductivities of 5.7 mS/cm for sulfide electrolytes while retaining structural integrity under mechanical stress. Removing flammable liquid electrolytes lowers thermal-runaway risk, an increasingly important criterion for regulators and insurers. Automakers can therefore shrink pack footprints, recapture cabin space, and trim vehicle mass. These benefits translate into longer driving ranges or smaller batteries for the same range, both of which unlock design flexibility and cost-of-ownership gains. The technology’s tolerance for pure lithium-metal anodes further widens the performance gap, creating a compelling pull for high-end and fleet platforms.

Government ZEV mandates and battery incentives

California’s Advanced Clean Cars II rule requires every new light-duty vehicle sold in the state to be zero-emission by 2035, with steep interim targets beginning in 2026[2]California Air Resources Board, “Advanced Clean Cars II Regulations,” arb.ca.gov. The policy aligns with federal tax credits that tie battery sourcing and assembly to domestic manufacturing, prompting automakers to localise next-generation cell lines. Europe’s Green Deal Industrial Plan adds parallel funding for battery gigafactories and raw-material processing. These synchronised policies shorten payback periods for solid-state capital investments and provide early demand certainty.

Automaker in-house pilot lines (Toyota, VW, BMW)

Toyota’s 3 GWh lithium-sulfide joint venture, Volkswagen’s 40 GWh partnership with QuantumScape, and BMW’s prototype programs highlight an emerging pattern in the EV Solid-state Battery Market: major automakers are vertically integrating cell development to secure differentiation. These projects improve knowledge spill-over across the supply chain, allowing rapid iteration on yield bottlenecks and quality control. Early production volumes will flow to premium models where margins are wider, but lessons learnt pave the way for higher-volume segments by 2028.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Production Cost and Yield Loss | -9.1% | Global, acute in early-stage manufacturing | Short term (≤ 2 years) |

| Limited Gigascale Capacity | -7.3% | Global, supply-demand imbalance | Medium term (2-4 years) |

| Lithium-Metal Foil Bottleneck | -5.4% | Global, concentrated in specialized suppliers | Medium term (2-4 years) |

| Recycling Pathway Uncertainty | -3.6% | Developed markets with strict recycling mandates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High production cost and low manufacturing yield

Present solid-state cells cost USD 400–500 per kWh, roughly four times the average cost of today’s lithium-ion packs, due to strict moisture controls and tight tolerances at solid–solid interfaces. Yield losses reach double-digit percentages on many pilot lines, amplifying unit costs during early runs. Process innovations, such as vapour-deposited lithium foils and anode-free stacking, show promise in halving defect rates, yet industrial validation is still underway. Until these improvements move from lab to line, price premiums will restrain widespread rollout.

Limited gigascale capacity before 2028

Most existing facilities are sized in the tens of megawatt-hours, insufficient for mainstream automotive demand, creating a key challenge for the EV Solid-state Battery Market. Despite multiple announcements, only a handful of confirmed projects will cross the gigawatt-hour threshold before 2028. The capital intensity of moisture-free roll-to-roll systems and the limited roster of specialised equipment makers slow build-outs. This mismatch between demand forecasts and physical output will limit near-term availability, thereby moderating adoption curves outside premium and fleet niches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger cars drive early adoption

The passenger-car segment generated 73.52% of 2025 revenue, reflecting early deployments in high-value models where performance and safety command price premiums. Commercial fleets trail in share yet post a 38.95% CAGR to 2031 as operators weigh total-cost-of-ownership savings from longer-lasting packs and reduced downtime. Toyota plans to launch solid-state packs first in luxury coupes, then cascade the chemistry to broader line-ups once costs fall. Fleet managers, by contrast, prioritise rapid charging and durability, making them receptive to higher upfront battery prices that cut maintenance.

The segment pattern indicates a two-wave adoption curve: personal-luxury vehicles establish brand credibility and engineering reliability, followed by light-duty vans and trucks that prize utilisation rates. As warranty data accumulate and unit costs slide, mainstream passenger segments will account for the bulk of unit volumes post-2028. This shift mirrors the historical rollout of high-nickel lithium-ion packs and creates a stepping-stone to mass-market penetration.

By Propulsion: BEVs lead solid-state integration

BEVs absorbed 69.45% of shipments in 2025 and are forecast to grow at 38.60% CAGR over the outlook period. Pure-electric platforms exploit the chemistry’s high energy density to extend range without enlarging packs, an advantage less critical to hybrids. PHEVs nonetheless gain from faster charge acceptance, which raises electric-only driving fractions and improves fleet emissions compliance.

Most automakers align their solid-state roadmaps with flagship electric architectures because premium margins can cover early cell premiums. As costs decline, PHEV and series-hybrid platforms will adopt thinner, lighter solid-state modules that free up packaging space or allow battery downsizing. In parallel, regulatory pressure for zero tailpipe emissions cements BEVs as the dominant propulsion fit for the technology.

By Solid Electrolyte Type: Sulfides dominate manufacturing

Sulfide electrolytes captured 46.92% share in 2025, and is projected to expand at a 35.80% CAGR thgrough 2031, owing to superior ionic conductivity and compatibility with existing roll-to-roll coating lines. Controlled-atmosphere requirements raise capex, yet early movers argue that the conductivity benefits outweigh handling complexity. Oxide systems provide enhanced moisture tolerance at the cost of thickness-induced resistance, while polymer variants serve specialist applications where flexibility matters more than absolute performance.

Recent research data show sulfide thin films achieving 900 Wh/L pack-level densities, supporting the case for high-volume electrified powertrains. Ongoing work on high-entropy argyrodite blends aims to raise conductivity above 6 mS/cm, equal to liquid electrolytes. Oxides will likely carve out niches in stationary storage and safety-critical mobility, whereas polymers remain focused on wearables and micro-mobility.

By Anode Material: Lithium-metal leads performance

Lithium-metal anodes claimed 55.05% market share in 2025, underlining the technology’s core benefit: maximum usable capacity. Solid-state separators suppress dendrites even under aggressive cycling, unlocking theoretical gravimetric capacities near 3,860 mAh/g. Silicon-composite and graphite-composite anodes offer intermediate steps for manufacturers wary of pure lithium scaling challenges.

Lithium-metal cells are projected to scale at 44.10% CAGR to 2031, partly driven by anode-free stack designs that plate lithium during first charge, reducing foil consumption. Silicon-dominant blends provide a hedge, exploiting existing supply chains and cell formats while preserving room for future upgrades. Consequently, the anode race will likely resolve in a hybrid landscape where different chemistries target distinct vehicle price bands.

By Battery Capacity: Mid-range dominates applications

Cells rated 20–100 Ah formed 47.95% of total shipments in 2025 as they map neatly to 50–100 kWh automotive packs. Above-100 Ah formats are growing fastest at 41.90% CAGR, reflecting efforts to cut module count and wiring complexity. Sub-20 Ah cells remain relevant for aerospace, medical, and niche consumer devices that value intrinsic safety more than lowest cost.

Ongoing scaling programmes aim to standardise large-format prismatic and 46-series cylindrical designs, each delivering six-fold energy increases over today’s 21700 cells. Rising capacities align with automakers’ push for simplified pack architecture, which in turn feeds back into lower assembly costs and easier recycling.

Geography Analysis

Asia-Pacific led the solid-state battery market with 40.85% share in 2025, anchored by Japan’s lithium-sulfide value chain and South Korea’s pilot-line expertise. Government funding underpins cell R&D and early vehicle integration projects, while established lithium-ion export corridors shorten scale-up learning curves.

North America, supported by Inflation Reduction Act credits and a target of more than 1,200 GWh annual cell capacity by 2030, emerges as the next major growth pole. Volkswagen’s planned St. Thomas gigafactory and multiple start-up pilot lines point to an ecosystem forming around domestic supply mandates. Companies leverage proximity to cobalt, lithium, and nickel deposits in Canada and the United States to secure raw-material resilience.

The Middle East and Africa register the highest CAGR at 35.40%, albeit from a small base, driven by green-hydrogen hubs and utility-scale storage pilots that leapfrog to solid-state chemistries for safety and durability reasons. Europe maintains steady progress with Germany’s FestBatt initiative and multi-partner consortia targeting commercial output by decade’s end. European automakers’ integration efforts ensure eventual demand pull, while public-private funding pools accelerate material science breakthroughs.

Value Chain Analysis

The EV solid-state battery value chain starts with upstream inputs including battery-grade lithium, nickel, cobalt, manganese, and specialty precursors for solid electrolytes (notably sulfide pathways), plus lithium-metal foil for lithium-metal and anode-free stacks. Midstream players convert these into cathode active materials, solid electrolyte powders/films, separators, and current collectors, followed by cell manufacturing that depends on moisture-controlled environments and high-precision lamination/stacking. Downstream, cells are assembled into modules and packs by cell makers, OEMs, or tier-1 integrators, then validated in OEM development vehicles before commercial shipment, with early demand concentrated in passenger cars and expanding through fleet programs.

The chain is currently organized around multi-party development ecosystems linking automakers with specialized cell developers and key materials partners. Examples include QuantumScape working with Honda on solid-state battery development and manufacturing processes (June 2026) and Stellantis integrating Factorial's FEST cells into a Dodge Charger Daytona development vehicle for road testing (June 2026), reflecting how qualification and industrialization activities now sit alongside materials scale-up. Bottlenecks continue to center on thin electrolyte production at automotive throughput, solid-solid interface stability, and manufacturing yield, which increases the strategic importance of process know-how such as dry electrode approaches highlighted by LG Energy Solution in 2026 as a route to reduce solvent-driven degradation and long drying steps.

Competitive Landscape

The solid-state battery market remains moderately fragmented. Competitive differentiation revolves around patent portfolios, electrolyte formulations, and roll-to-roll yields.

Toyota concentrates on sulfide chemistry and in-house pack integration. Samsung SDI pursues an anode-free design that improves volumetric density, while QuantumScape commercialises a ceramic separator licensed to multiple automakers. Start-ups such as ProLogium focus on flexible oxide stacks for premium consumer electronics and e-motorcycles, indicating wider horizontal applications beyond cars.

Strategic alliances between automakers and cell developers intensify as companies race to lock in capacity. Evidence of consolidation potential is visible in recent joint ventures and equity stakes, particularly where automakers exchange capital for guaranteed cell off-take. Nonetheless, the sector’s capital intensity and stringent quality thresholds limit viable entrants, suggesting a medium-term shift toward an oligopolistic structure once pilot lines mature.

EV Solid-state Battery Industry Leaders

Toyota Motor Corporation

Samsung SDI Co., Ltd

Solid Power Inc.

LG Energy Solution Ltd

QuantumScape Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace is concentrated in industrialization services and equipment/process capabilities that improve yield in controlled-atmosphere production, particularly for sulfide electrolytes and lithium-metal/anode-free architectures that dominate early performance targets. Vehicle-level validation programs are widening the funnel of near-commercial designs, as shown by Stellantis and Factorial moving FEST cells into an on-road development vehicle in June 2026, and by OEM and developer collaborations that focus on manufacturability, such as QuantumScape's agreement with Honda R&D on development and manufacturing processes (June 2026). These activities create demand for qualified solid electrolyte supply, moisture-control systems, and pilot-to-prep scale transfer services, while pushing more standardized specifications into procurement.

Policy and standards actions in Asia add concrete commercialization levers and clearer qualification thresholds. China implemented a national classification standard in July 2026 defining all-solid-state labeling using a liquid electrolyte mass threshold of less than 5% under 120 C testing, which tightens technical claims and supports differentiation for verified ASSB designs. China also announced a consumption tax policy effective September 1, 2026 that exempts solid-state batteries through end-2028, while other lithium-ion cells face a new tax, improving relative economics for compliant solid-state chemistries. In parallel, METI-backed funding in Japan (reported at USD 660 million in subsidies for all-solid-state supply chain projects in June 2026) and company actions such as Idemitsu's solid electrolyte pilot construction with Toyota and Gotion's completion of design work for a 2 GWh all-solid-state line point to investment focus areas: solid electrolyte production, qualification-grade pilot capacity, and manufacturing process stabilization.

Recent Industry Developments

- July 2026: Samsung SDI outlined a long-term investment plan totaling KRW 25 trillion across Ulsan and Cheonan through 2040, positioning Ulsan as a mass-production base for all-solid-state batteries and Cheonan as an R&D hub for validating next-generation technologies. The move signals sustained capex commitment to scale pathways and process readiness rather than short-cycle prototyping. It also raises the competitive bar for manufacturers without comparable pilot-to-production infrastructure.

- June 2026: QuantumScape announced a joint research agreement with Honda R&D Co., Ltd. focused on solid-state battery technology development and manufacturing processes. The partnership brings an additional global OEM into QuantumScape's industrialization ecosystem, reinforcing the role of co-development to de-risk scale-up steps such as separator processing and cell assembly. It also broadens potential downstream pull for qualified cells once pilot metrics meet automotive requirements.

- July 2024: Volkswagen's PowerCo and QuantumScape agreed to industrialize solid-state cells at an initial 40 GWh annual capacity, with an expansion pathway to 80 GWh. The agreement provided a defined commercialization route tied to a large-scale manufacturing entity, shifting solid-state efforts from lab validation toward factory deployment planning. It also intensified competitive pressure on other developer-OEM pairings to secure comparable capacity and offtake structures.

Research Methodology Framework and Report Scope

Market Definition and Coverage

In this methodology, the EV solid-state battery market is counted as revenue from solid-electrolyte traction battery packs supplied for use in electric vehicles, with the sale recorded at the point of first commercial shipment in USD.

Scope exclusions: We exclude prototype-stage cells that are not yet in commercial shipment, aftermarket replacements, and solid-state batteries meant for consumer electronics or stationary storage.

Segmentation Overview

- By Vehicle Type

- Passenger Cars

- Commercial Vehicles

- By Propulsion

- Battery Electric Vehicle (BEV)

- Plug-in Hybrid Electric Vehicle (PHEV)

- Hybrid Electric Vehicle (HEV)

- By Solid Electrolyte Type

- Sulfide-based

- Oxide-based

- Polymer-based

- By Anode Material

- Lithium-Metal

- Silicon-Composite

- Graphite-Composite

- By Battery Capacity

- Below 20 Ah

- 20 to 100 Ah

- Above 100 Ah

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Egypt

- Nigeria

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the guardrails for the model and to anchor the demand environment for solid-state EV batteries. We mainly referenced public adoption and production indicators that explain where EV programs and battery supply are moving, such as IEA EV outlook datasets, US DOE and national lab publications, USGS minerals statistics for key inputs, and patent databases to track solid-electrolyte and lithium-metal activity. We also reviewed standards and safety references for traction batteries and transport, such as UNECE battery-related regulations and similar regional rulebooks, since compliance timing can shift near-term shipments.

To translate demand signals into a realistic market pool, we used automaker and supplier public documents (annual reports, earnings decks, and product announcements) to capture stated pilot timelines, target pack formats, and intended vehicle launches. Where available, we supplemented this with paid subscriptions for company financials and news, patent lookups, and an import-export shipment-level database to sanity check materials availability and early trade flows. The sources listed here are illustrative and not exhaustive, and many other public sources were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were used to pressure-test desk assumptions and to close gaps on what is actually being shipped, qualified, or delayed in EV programs. We spoke with a mix of solid-state material suppliers, cell and pack developers, EV OEM-linked engineering teams, and downstream integrators to confirm commercialization readiness, expected ramp curves, and what pricing looks like at early volumes. Because this is a global market, we cross-checked inputs across APAC, EMEA, and the Americas so regional pilot-line realities and policy push were not generalized beyond what respondents described.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 21% | APAC: 44% |

| Mid tier: 40% | Functional/Unit leaders: 30% | EMEA: 29% |

| Smaller Players: 21% | Managers: 49% | Americas: 27% |

Market-Sizing & Forecasting

We built the market using a top-down and bottom-up approach, but the main build starts from EV production and program-level adoption signals that reconstruct the near-term shipment pool for solid-state packs. For each major EV-producing region, the model applies an adoption pathway for solid-state packs that is tied to identifiable program gates, which are then translated into pack shipments and revenue using a price curve that declines as volumes scale.

Key inputs that influence the size and year-by-year pattern include the timing of EV platform launches that mention solid-state integration, pilot-line and pre-series capacity announcements, assumed pack energy (kWh) by vehicle class, early-stage yield and scrap loss expectations, and pack-level pricing per kWh that changes as qualification risk drops. To avoid overstating the market during the early ramp, we treat delays, qualification resets, and constrained lithium-metal and solid-electrolyte supply as explicit friction variables rather than leaving them as generic narrative assumptions.

Forecasting was done using scenario analysis, because commercialization timing is still uneven across regions and vehicle programs. The base case is guided by interview consensus on likely SOP timing, ramp speeds, and pricing progression, and then it is checked against a selective bottom-up approximation using sampled pack ASP per kWh times expected shipment volumes and supplier capacity-to-output conversion assumptions. Where bottom-up visibility is weak, we apply conservative utilization bands and then re-check totals against independent EV output indicators so gaps do not silently inflate the forecast.

Data Validation & Update Cycle

Validation is done in layers so one assumption does not overly drive the final number. We compare outputs against independent signals such as EV production trajectories, disclosed pilot capacities, and implied pack energy demand, and then we review any large year-on-year jumps to confirm they are supported by a real program ramp or pricing change. If a data point looks inconsistent, it is reworked, and when needed the team reconnects with a relevant expert to clarify what changed.

Before final sign-off, the model goes through an internal analyst review that checks math, unit consistency (packs, kWh, and USD), and the logic behind regional splits. Reports are refreshed annually, with interim updates when a material event occurs such as a delayed SOP, a major pilot expansion, or a visible pricing reset. Right before delivery, a fresh pass is completed so clients receive the latest updated view rather than an older draft.

Mordor Intelligence's Ev Solid State Battery Market Size Measured Against Other Published Estimates

Published market sizes for EV solid-state batteries can vary widely because the category is still early and definitions are not always consistent. Differences usually come from what gets counted as a qualifying solid-state product, which revenue point is used (cell, pack, or vehicle-level value), and how aggressively ramp timing is assumed.

By tracking commercialization gates and pack shipment timing, Mordor Intelligence keeps the counted revenue tied to first commercial pack deliveries for EV use, which often excludes pilot and prototype activity that some estimates still price in. Another gap driver is pricing, since some sources assume a fast drop in USD per kWh without linking it to yield improvement and production scale, while others mix in non-EV applications or include aftermarket replacements that do not reflect OEM supply dynamics.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.37 B (2025) | |

| Trade Publisher A | USD 2.67 B (2025) | Often counts broader solid-state battery revenues, including non-EV uses and earlier-stage shipments, and may apply aggressive adoption and pricing assumptions without gating by vehicle program qualification. |

| Industry Report B | USD 0.27 B (2023) | Uses an earlier base year and a wider solid-state battery scope that can blend thin-film and small-format batteries, which changes the EV-only revenue pool and the effective average pricing. |

The table shows that the spread is mostly explained by scope and timing choices rather than simple math differences. When the counted revenue is limited to commercial EV pack shipments and pricing is linked to scale and yield, the market size becomes easier to trace back to clear variables and repeatable steps. This helps decision-makers compare scenarios without mixing unlike revenue pools.

Key Questions Answered in the Report

What is the current size of the solid-state battery market?

The solid-state battery market size stands at USD 372.09 million in 2026 and is forecast to reach USD 2.23 billion by 2031.

How fast is the solid-state battery market growing?

The market is projected to register a 43.11% compound annual growth rate between 2026 and 2031.

Which region leads the solid-state battery market?

Asia-Pacific holds the largest share at 40.85% in 2025 owing to integrated supply chains and aggressive pilot-line investment.

Why are solid-state batteries considered safer than lithium-ion?

They eliminate flammable liquid electrolytes, reducing thermal-runaway risk and enabling safer deployment in high-energy applications.

When will large-scale solid-state battery production begin?

Commercial output is expected to ramp from 2027 onward as pilot lines transition to multi-gigawatt-hour capacities.

Which vehicle segment will adopt solid-state batteries first?

Premium passenger cars are set to pioneer adoption, followed by commercial fleets that prioritise reduced charging downtime.

Page last updated on: