Tourniquet Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 646.48 Million |

| Market Size (2031) | USD 930.27 Million |

| Growth Rate (2026 - 2031) | 7.55% CAGR |

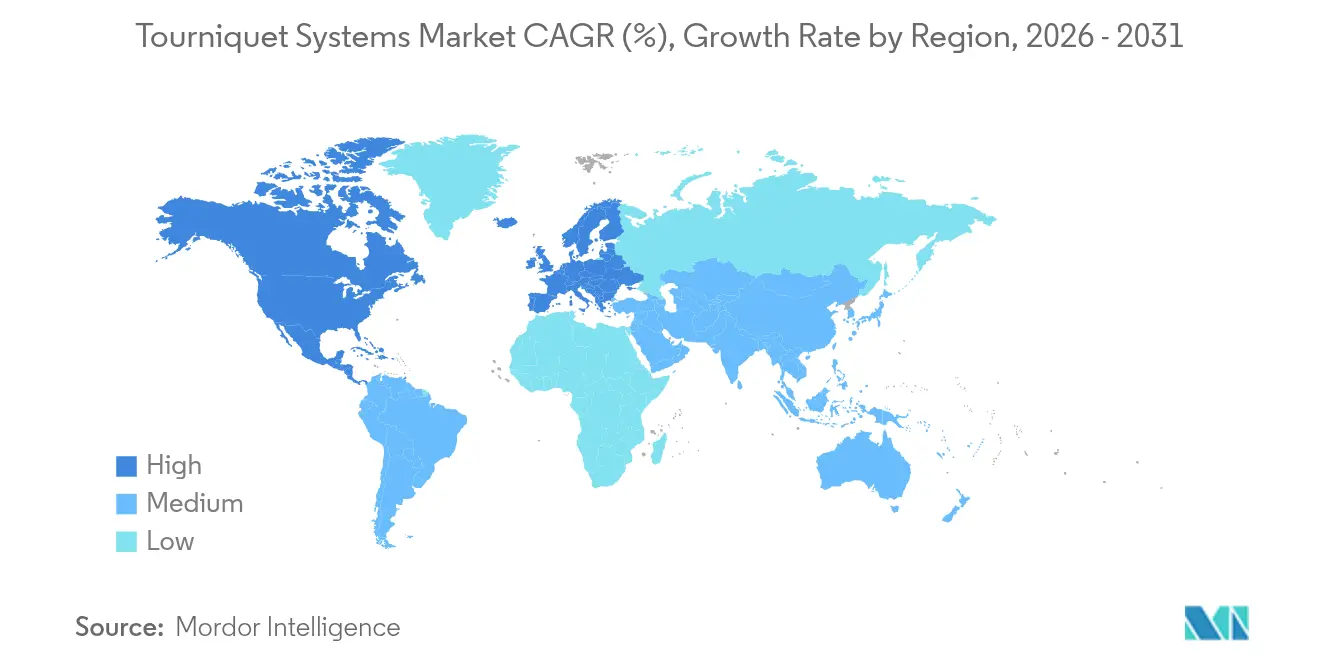

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

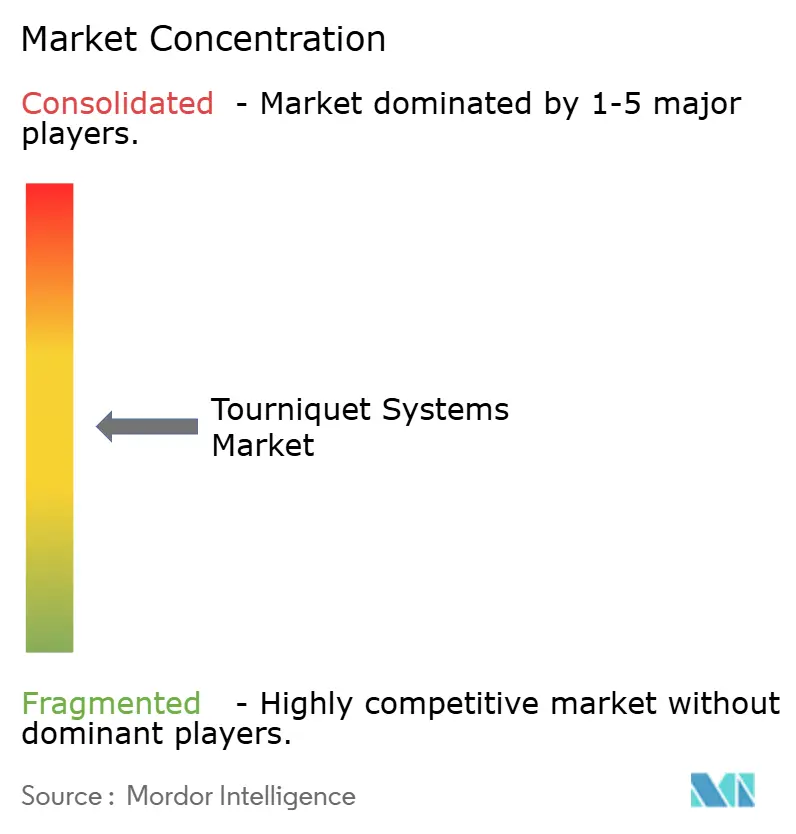

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tourniquet Systems Market Analysis by Mordor Intelligence

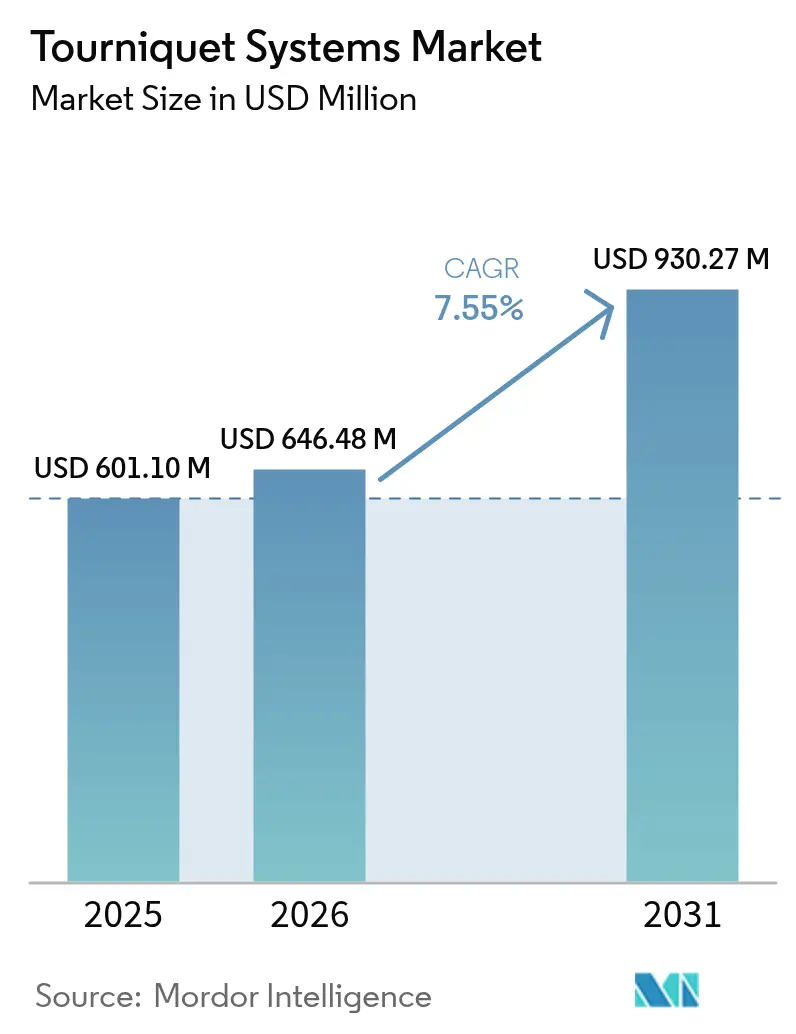

The tourniquet systems market size was valued at USD 601.10 million in 2025 and estimated to grow from USD 646.48 million in 2026 to reach USD 930.27 million by 2031, at a CAGR of 7.55% during the forecast period (2026-2031). Robust orthopedic procedure growth, sustained military demand and the transition to smart limb-occlusion-pressure (LOP) devices underpin this expansion. Hospitals continue to account for most unit placements, yet ambulatory surgical centers (ASCs) are accelerating purchases as same-day joint replacements and hand surgeries migrate into outpatient settings. On the technology front, automatic pressure calibration and cloud-connected data capture are reshaping procurement criteria, while material upgrades toward latex-free silicone and advanced thermoplastic elastomers support infection-control and patient-comfort targets. Competitive intensity remains moderate; leading suppliers leverage AI-driven compression algorithms, domestic manufacturing investments and selective acquisitions to defend share as regional specialist entrants target lower-price pneumatic niches.

Key Report Takeaways

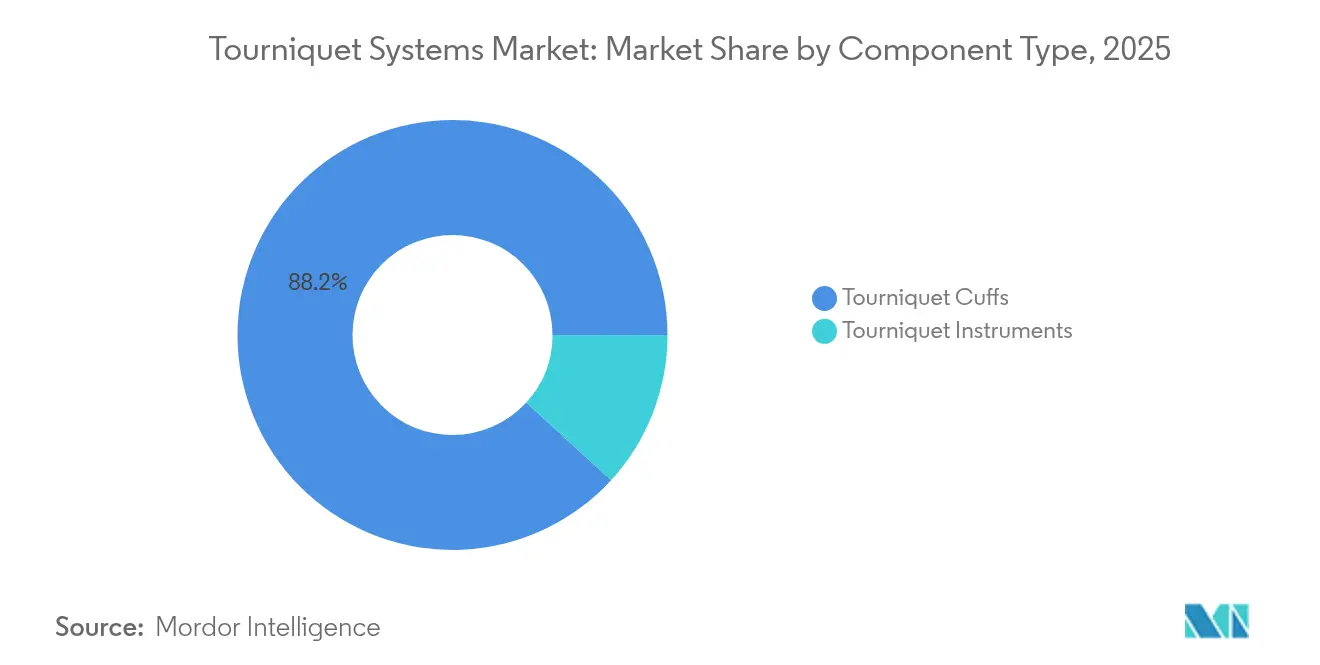

- By component type, tourniquet cuffs led with 88.20% of tourniquet systems market share in 2025, whereas instruments are forecast to expand at a 8.85% CAGR through 2031.

- By application, lower-limb surgery contributed 67.90% of tourniquet systems market size in 2025, while upper-limb surgery is projected to grow at 9.05% CAGR to 2031.

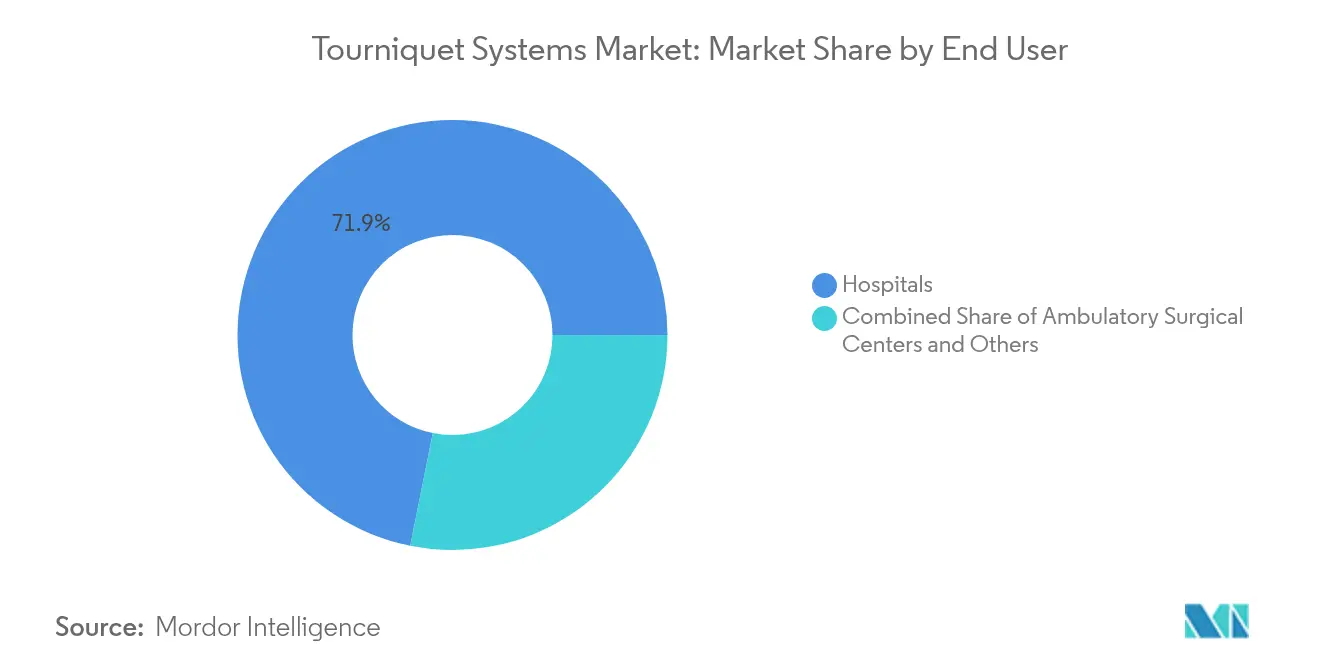

- By end-user, hospitals held 71.85% revenue share of the tourniquet systems market in 2025; ASCs record the highest anticipated CAGR at 9.65% through 2031.

- By material, nylon dominated with 41.95% of tourniquet systems market share in 2025, and silicone & rubber compounds are poised for a 9.12% CAGR to 2031.

- By geography, North America captured 44.98% of revenue in 2025, whereas Asia-Pacific is on track for a 9.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tourniquet Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Orthopedic & Trauma Surgeries Worldwide | +2.1% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Rapid Adoption Of Limb-Occlusion-Pressure (LOP) Smart Tourniquet Systems | +1.8% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Increasing Military Procurement Amid Prolonged Conflicts | +1.4% | Global, with focus on NATO countries & conflict zones | Short term (≤ 2 years) |

| Rising Prevalence Of Diabetes-Related Amputations | +1.2% | Global, with higher impact in developing regions | Long term (≥ 4 years) |

| Growth Of Outpatient & ASC Orthopedic Procedures | +1.0% | North America & Europe, spreading to APAC | Medium term (2-4 years) |

| Emergence Of Low-Cost Pneumatic Units For Emerging Markets | +0.9% | APAC, Latin America, and MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Orthopedic & Trauma Surgeries Worldwide

Elective and trauma-based orthopedic volumes continue to climb, buoyed by aging populations and sports-medicine demand. Same-day hip and knee arthroplasties moved from 1% in 2017 to 30.5% in 2021, compressing average stays to 0.94 days and lifting reliance on reliable limb exsanguination tools. The global hip-knee implant sector grew 7.2% year-on-year to USD 18.5 billion in 2023, with robotic guidance amplifying the need for clear operative fields. Geographic variability remains stark; emergency lower-extremity amputation rates ranged from 3.7% to 90% across U.S. zip codes, signaling under-served segments that require efficient tourniquet deployment. Collectively, these procedure trends bolster annual replacement cycles for cuffs and drive upgrades to micro-processor pumps, sustaining the tourniquet systems market.

Rapid Adoption of Limb-Occlusion-Pressure Smart Tourniquet Systems

Smart devices shift practice from empirical values toward patient-specific pressures. Stryker’s SmartPump 2.0 demonstrates lower occlusion thresholds while auto-documenting perioperative data streams [1]Stryker, “SmartPump 2.0 Performance Data,” stryker.com. Zimmer Biomet’s A.T.S. 5000 offers Personalized Pressure Technology that tailors inflation to limb morphology, reducing post-operative pain scores [2]Zimmer Biomet, “A.T.S. 5000 Personalized Pressure Technology,” zimmerbiomet.com. Comparative testing showed Delfi’s surgical-grade algorithms delivering 100% autoregulation accuracy versus variable performance among consumer devices. These capabilities resonate with hospital quality metrics and regulatory calls for safer pressure windows, positioning smart pumps as the fastest rising unit segment within the tourniquet systems market.

Increasing Military Procurement Amid Prolonged Conflicts

The U.S. and allied defense forces boosted medical kits following extended engagements in Ukraine and the Middle East. A USD 6.18 million DoD award in 2024 expanded domestic tourniquet manufacturing to fortify combat readiness. Battlefield studies confirm that correct tourniquet application can slash preventable hemorrhage deaths, driving orders for ruggedized devices featuring extended-use polymer windlasses and one-handed deployment locks. Innovations from defense programs, such as shape-memory polymer cuffs under Australia’s Future Soldier initiative, increasingly inform civilian product design. Military procurement therefore delivers a short-term volume stimulus and technology spill-over to the broader tourniquet systems market.

Rising Prevalence of Diabetes-Related Amputations

Diabetic foot complications remain a major amputation driver. An estimated 2.3 million people live with limb loss in the United States, and prevalence may soar 145% by 2060. Canada reports 7,720 diabetes-linked amputations each year, costing hospitals more than USD 750 million. Pandemic-era data show mortality after amputation climbing to 49% in 2020, stressing the importance of rapid, controlled blood-loss management during emergent surgeries. These trends sustain procedure counts and favor tourniquet systems that optimize occlusion with minimal ischemic risk.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Post-Operative Complication Risk (Nerve/Ischemia) | -1.5% | Global, with higher impact in regions with less training | Long term (≥ 4 years) |

| Shortage Of Skilled Staff For Pressure Calibration | -1.2% | Global, with acute impact in emerging markets | Medium term (2-4 years) |

| Sterilization Concerns With Reusable Cuffs | -0.9% | Global, with concentration in cost-sensitive markets | Medium term (2-4 years) |

| Regulatory Scrutiny Over Hazardous Pressure Thresholds | -0.8% | North America & Europe, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Post-Operative Complication Risk (Nerve/Ischemia)

Nerve palsy remains the primary adverse event linked to excessive tourniquet pressure or duration. A global scoping review identified ischemic pain, thromboembolic events and post-tourniquet syndrome as additional concerns, though incidence drops sharply when evidence-based protocols are followed. European trauma guidelines now highlight time limits and real-time monitoring to curb paralysis risk. AORN’s 2025 practice advisory mandates limb girth measurement, cuff fit checks and continuous pressure readouts, prompting facilities to reassess reusable cuff policies. Fear of litigation and higher insurance premiums can delay capital purchases among budget-sensitive hospitals, moderating the tourniquet systems market growth pace.

Shortage of Skilled Staff for Pressure Calibration

Advanced pumps require familiarity with limb-occlusion-pressure concepts, yet knowledge gaps persist. Surveys reveal that many orthopedic surgeons still default to fixed pressure values rather than personalized settings. The U.S. FDA’s 2024 guidance on pneumatic cuff conservation emphasized staff competency in cleaning and reuse, underscoring systemic training deficits. British Orthopaedic Association audits found inconsistent documentation of inflation times and pressures in trauma theaters, spotlighting procedural drift [3]British Orthopaedic Association, “Tourniquet Safety Audit Findings,” boa.ac.uk . Automated calibration eases the burden, but human oversight remains essential, particularly in smaller ASCs where multiskilling is common. Skill shortages therefore temper adoption, especially in emerging regions where clinical engineering support is scarce.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component Type: Cuffs Dominate Despite Instruments Surge

Tourniquet cuffs generated 88.20% of 2025 revenue, anchoring the tourniquet systems market as the consumable element most directly tied to procedure counts. Recurring replacement, single-use infection-control policies and varied limb-specific configurations lock cuffs into purchasing budgets. Smart pump adoption, while currently niche, is advancing at a 8.85% CAGR, and bundled contracts increasingly pair adaptive pumps with proprietary cuff lines to lock in post-sale consumable income.

Hospital value analyses repeatedly highlight the sterilization labor and quality-variation risks linked to reusable fabrics, steering procurement toward latex-free disposable nylon or silicone cuffs. During 2024 supply constraints, the FDA endorsed limited cuff reuse, which temporarily propped up older stock yet underscored the fragility of single-source chains. Smart systems integrate digital auto-pressure sensors that log each cycle to the EMR, supporting audit trails and preventive maintenance. As these data credentials influence payer audits, the component mix is expected to shift, but cuffs will remain the revenue cornerstone, sustaining the long-term outlook for the tourniquet systems market.

By Application: Lower-Limb Procedures Drive Volume Growth

Lower-extremity surgeries contributed 67.90% of 2025 procedures and USD 408.15 million of tourniquet systems market size, leveraging higher pressure thresholds and longer inflation times compared with arm applications. Arthroplasty growth, battlefield trauma and diabetic amputations converge to keep demand high, with each driver exhibiting durable multi-year trends.

Upper-limb procedures, although smaller in absolute numbers, are forecast to expand at 9.05% CAGR through 2031, outpacing market average as minimally invasive wrist and elbow work rises. Cost analyses show elastic straps saving USD 28.27 per hand surgery versus pneumatic alternatives without compromising field clarity. Such findings propel niche adoption of inexpensive mechanical loops, especially in ASCs. Elsewhere, EMS trauma kits and hybrid vascular cases fall into the “other” bucket that maintains a steady share as emergency clinicians integrate portable quick-release bands. Together, these segments keep the tourniquet systems market balanced between high-volume lower-limb and high-growth upper-limb niches.

By End-User: Hospitals Lead While ASCs Accelerate

Hospitals controlled 71.85% of unit demand in 2025, equal to USD 431.89 million of tourniquet systems market size, reflecting their broad procedural portfolio and capital budgets. Teaching institutions favor smart pumps for documentation compliance, while level-I trauma centers stock ruggedized pneumatic units for emergent amputations.

ASCs, projected to grow 9.65% CAGR, now account for more than 25% of total knee arthroplasty volumes in the United States, seeking compact pumps that integrate with handheld EMR scanners. Medicare reimbursements and surgeon ownership models reinforce this shift, prompting manufacturers to launch lightweight trolleys and single-button presets tailored to fast-turnover suites. Specialist clinics and emergency departments constitute a small yet strategically important cohort, particularly in emerging markets where centralized procurement may bundle tourniquet systems with general OR equipment upgrades. The cross-setting momentum sustains recurring demand and broadens the geographic spread of the tourniquet systems market.

By Material: Nylon Leads Innovation Drive

Nylon accounted for 41.95% of 2025 revenue thanks to its tensile strength, puncture resistance and favorable sterilization profile. The material’s supply chain maturity supports volume availability and keeps unit costs predictable for hospitals.

Silicone and next-gen thermoplastic elastomers are forecast to grow at 9.12% CAGR as facilities phase out latex. Teknor Apex’s Medalist TPE line replicates the elasticity of latex while meeting ISO 10993 biocompatibility, facilitating conversion in sensitive patient populations. Research on ultra-stretch elastomers with 5,000% elongation indicates future cuffs may combine micro-sensor arrays with skin-friendly surfaces. Meanwhile, Velcro-textile wraps remain staples in military kits for rapid field application. Material upgrades therefore intersect with infection-prevention and user-comfort goals, steering continued product refresh cycles across the tourniquet systems market.

Geography Analysis

North America booked 44.98% of 2025 revenue, reflecting dense orthopedic procedure volumes, broad insurance coverage and early adoption of LOP pumps. U.S. hospital consolidation and centralized purchasing contracts further anchor supplier footprints, while domestic manufacturing subsidies bolster capacity resiliency. Canada mirrors many of these drivers but exhibits faster uptake of single-use cuffs due to provincial infection-control guidelines.

Europe maintained steady growth on the back of rigorous CE branding and pan-regional orthopedic registries that promote evidence-based device selection. Germany and the Nordic countries exhibit higher penetrations of smart pumps, whereas Southern Europe favors cost-sensitive pneumatic bundles. The region is also seeing incremental demand from defense stockpiles as NATO members replenish tactical kits.

Asia-Pacific represents the fastest growing cluster, posting a 9.95% CAGR projection as procedure backlogs clear and private insurance penetration rises. China’s county-level trauma network expansion and India’s surge in road-traffic injuries catalyze cuff consumption. Japanese orthopedic societies are piloting AI-linked pressure algorithms, while Australia’s defense-driven R&D spills into civilian tenders. Middle East & Africa and South America trail in absolute size but offer double-digit growth pockets; Brazil’s move to universal digital health records and Saudi Arabia’s Vision 2030 hospital build-outs both embed smart tourniquet procurement clauses. Geo-specific product adaptations, such as battery-free pneumatic units for power-unstable regions, enable suppliers to extend the tourniquet systems market footprint.

Regulatory Landscape

In the United States, pneumatic tourniquets are regulated by the FDA as Class I medical devices under 21 CFR 878.5910, with related obligations spanning Medical Device Reporting (21 CFR 803), Corrections and Removals (21 CFR 806), Quality System requirements, and Unique Device Identification (21 CFR 830). A key update for manufacturers is the FDA Quality Management System Regulation (QMSR), which became effective on February 2, 2026, raising compliance expectations for design, manufacturing, and post-market processes that support tourniquet pump and cuff traceability. Across other major markets, conformity is increasingly anchored to recognized technical standards for medical electrical equipment used in pneumatic systems, including the IEC 60601-2-34 series, with a transition underway toward the 2024 edition as referenced in regulator-recognized consensus standards pathways.

In Europe, the EU MDR framework continues to shape clinical and post-market expectations, and Commission Delegated Regulation (EU) 2026/1451 (adopted March 20, 2026) modified clinical investigation obligations for specific device categories, reinforcing the need for companies to maintain strong clinical and technical documentation. In China, the release of a 2026-dated technical specification (T/GDNAS 074-2026) for pneumatic tourniquet first-aid processing signals continued formalization of requirements for emergency-use and pre-hospital handling workflows, affecting product instructions, reprocessing language, and distributor training materials.

Value Chain Analysis

The tourniquet systems value chain starts with raw materials and subcomponents (nylon, silicone/rubber compounds, thermoplastic elastomers, hook-and-loop textiles, adhesives, and medical-grade tubing), and extends into electromechanical parts for pneumatic systems (pumps, valves, pressure sensors, PCBs, batteries/power supplies, and connectors). Manufacturers then convert these inputs into two primary product streams: pneumatic systems (pressure-regulating unit plus tubing and inflatable cuffs) and nonpneumatic tourniquets (mechanical straps/tubing and windlass-style designs). Sterilization/packaging and labeling steps follow, supporting UDI and hospital scanning workflows.

Downstream, distribution runs through direct sales to hospitals and group purchasing contracts, plus channel partners for ambulatory surgical centers and emergency-care/military procurement. In 2026, supply-chain responses intensified with supplier diversification, nearshoring, and rapid prototyping/CNC machining for critical components, especially for ruggedized field-use products. Brands also rely on OEM/ODM partners to scale tactical and consumable cuff output without building dedicated capacity, while capital equipment suppliers bundle smart pumps with proprietary cuff lines to secure recurring consumable pull-through and service revenue.

Competitive Landscape

The tourniquet systems market is moderately fragmented. Stryker, Zimmer Biomet and Delfi collectively account for just under half of global shipments, each emphasizing precision pumps that interface with hospital informatics. Stryker expanded into peripheral vascular closure by acquiring Inari Medical for USD 760 million in 2025, leveraging SmartPump cross-selling into interventional suites. Zimmer Biomet strengthened its cuff portfolio through supplier co-development deals that guarantee exclusive materials access. Delfi maintains niche leadership in military and blood-flow-restriction training, supported by published accuracy trials.

Tier-two competitors such as Ulrich Medical, SourceMark Medical and Compression Works target disposable cuff bundles and junctional solutions, often winning regional tenders with price-plus-service propositions. Chinese entrants focus on low-cost pneumatic pumps, exporting to Southeast Asia under OEM labels. Meanwhile, digital health startups partner with university labs to embed optical perfusion sensors into cuffs, aiming for predictive ischemia alerts that may unlock subscription software revenue.

Regulatory dynamics influence rivalry. The FDA’s 2024 Unique Device Identification enforcement expanded data-logging demand, favoring suppliers with integrated barcode systems. European MDR certification hurdles raised costs, pushing smaller EU manufacturers toward contract OEM models. Collectively, these forces sustain technology investment and strategic alliances across the tourniquet systems market.

Tourniquet Systems Industry Leaders

Delfi Medical Innovations Inc

Zimmer Biomet Holdings Inc

Hammarplast Medical AB

Stryker Corporation

AneticAid Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A whitespace is emerging around automation and verification in tourniquet use, spanning both surgical LOP systems and emergency pneumatic designs that reduce dependence on operator technique and documentation discipline. Published 2026 efficacy data for an automated pneumatic approach reported complete occlusion success across 52 applications, along with rapid time-to-occlusion metrics, supporting a pathway for vendors to position automated control as a safety-and-workflow upgrade rather than a pure premium feature. This aligns with the market shift toward smart limb-occlusion-pressure devices and the heightened focus on safe pressure windows and traceable use records in hospital quality programs.

A second opportunity sits at the intersection of outpatient migration and integrated OR procurement, where ASCs increasingly value compact systems that simplify setup, minimize staff calibration burden, and fit bundled capital purchasing. Zimmer Biomet has been expanding its ASC-facing offering through partnerships that add operating room capital products into ASC solution bundles, creating a more integrated go-to-market route for tourniquet pumps, cuffs, and adjacent perioperative equipment. On the defense and emergency side, 2026 field testing activity by Nordic military units for a pneumatic tourniquet platform highlights demand for faster, more repeatable hemorrhage-control performance in austere settings, even as cost and training constraints keep room for tiered portfolios that span premium automated systems and cost-efficient pneumatic alternatives.

Recent Industry Developments

- June 2026: Zimmer Biomet entered a definitive agreement to acquire the Iovera cryoneurolysis device from Pacira BioSciences in a USD 140 million deal. The move expands Zimmer Biomet's orthopedic perioperative pain-management toolkit, strengthening its ability to bundle adjacent technologies with ASC and hospital solution offerings where tourniquet systems are commonly procured alongside OR equipment.

- July 2025: Zimmer Biomet formed a strategic partnership with Getinge to distribute Getinge operating room capital products to ambulatory surgery center customers through its ZBX ASC Solutions offering. The partnership reinforces a bundled OR procurement route that can influence tourniquet pump and cuff placement decisions within standardized ASC equipment packages.

- June 2024: A Canadian distribution agreement for the AAJT-S was signed between Technimount E.M.S. Holding and Compression Works, expanding EMS distribution channels in Canada and enabling faster access to junctional hemorrhage-control devices. This collaboration broadens the reach of EMS and incident response teams in Canada, supporting quicker deployment of junctional tourniquet solutions in field and pre-hospital scenarios.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers tourniquet systems used in clinical care to temporarily restrict blood flow, so a clearer, drier field is maintained during procedures. We treat the market as the value of tourniquet instruments and compatible cuffs sold into hospitals, ambulatory surgical centers, and similar care settings across major regions.

Scope exclusions: We exclude general wound dressings, sutures, and unrelated compression products that are not used as tourniquet systems for surgical or procedure-related blood flow control.

Segmentation Overview

- By Component Type

- Tourniquet Instruments

- Tourniquet Cuffs

- Pneumatic

- Non-pneumatic

- By Application

- Lower-limb Surgery

- Upper-limb Surgery

- Others

- By End-user

- Hospitals

- Ambulatory Surgical Centers

- Others

- By Material

- Nylon

- Silicone & Rubber

- Velcro & Textile

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the demand pool that uses tourniquet systems in procedure settings, then cross-checking that against device availability and purchasing pathways. Public sources were used to anchor procedure volumes and health system capacity, such as CDC and NIH publications, OECD health statistics, WHO datasets, and national health ministry portals where procedure and hospital activity metrics are reported.

To keep pricing and adoption assumptions grounded, we also reviewed manufacturer product literature, regulatory and recall notices where relevant, and hospital procurement disclosures when available, plus investor materials for medical device makers. A paid subscription for company financials and news intelligence was used for revenue context, and a patent database was reviewed to spot feature shifts like limb occlusion pressure tools and safety alarms. These desk research sources are illustrative and not exhaustive, and other public references were also used to validate specific data points and clarify open questions.

Primary Interviews and Surveys

Primary inputs were gathered through expert interviews and structured surveys with stakeholders across the value chain, including clinical users, procurement teams, distributors, and product managers. This step was used to confirm procedure-linked usage rates, typical replacement cycles for cuffs and instruments, and realistic price bands by region, then to stress-test assumptions that looked inconsistent across desk sources.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 12% | APAC: 49% |

| Mid tier: 56% | Functional/Unit leaders: 28% | EMEA: 30% |

| Smaller Players: 15% | Managers: 60% | Americas: 21% |

Market-Sizing & Forecasting

Sizing is built mainly from a top-down and bottom-up model mix, where surgical activity and care capacity signals are reconstructed into addressable demand, and then filtered through realistic adoption and replacement behavior for tourniquet instruments and cuffs. We then corroborate totals with selective bottom-up checks, such as sampled price by volume builds for key countries and channel conversations that help adjust the final curve.

Key model inputs include orthopedic and limb-related procedure volumes, hospital and ambulatory surgery center throughput, average cuffs used per procedure, replacement and reprocessing patterns, and average selling price ranges for instruments versus cuffs. Because pricing can drift with features and inflation, ASPs are updated by region using recent procurement cues and primary feedback, rather than carrying a single global price forward.

For forecasting, we use scenario analysis supported by expert consensus on procedure growth, outpatient shift, and adoption of safety features like limb occlusion pressure guidance. Where data is thin in smaller countries, proxy indicators are used (procedure mix and facility counts), and the impact is capped through conservative penetration assumptions before regional roll-ups are finalized.

Data Validation & Update Cycle

Outputs are validated by checking internal consistency across regions, applications, and component splits, then comparing results with independent signals like procedure growth rates and care setting shifts. When an outlier appears, we re-check driver assumptions, revisit currency conversions, and reconnect with selected respondents to confirm whether the change reflects a real market movement or a data artifact.

A multi-step review is followed before sign-off so calculation logic, units, and year alignment are consistent across tables. Reports are refreshed annually, and material events like large regulatory actions, supply disruptions, or sharp pricing moves trigger interim revisions. Before delivery, a final update pass is done so the numbers reflect the latest available public releases and interview learnings.

Mordor Intelligence's Tourniquet Systems Market Sizing Compared With Other Published Estimates

Published market sizes for tourniquet systems can look far apart even when they describe a similar product family, since update timing and pricing treatment are not the same across studies. Differences also show up when one source anchors the model to a specific base year, while another rolls forward from an earlier year without rechecking procedure and purchasing signals.

The spread usually comes from how ASPs are carried across years, how currency conversion is timed, and whether cuffs and instruments are counted with the same replacement logic. When refresh cadence is slower, older price points and utilization assumptions can stay in the model longer, which is why the year selected for the baseline matters for hospital procurement.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 646.48 M (2026) | |

| Industry Publisher A | USD 514.40 M (2023) | Uses an earlier base year, and the total can move depending on whether cuffs are modeled with higher replacement frequency versus instruments, and how 2023 pricing is rolled forward. |

| Research House B | USD 476.50 M (2024) | Anchors on 2024 with a different forecast window, and the total can shift if region-level currency timing and procedure-to-usage conversion factors are not revalidated close to the estimate year. |

The table shows that year anchoring and price refresh patterns are major drivers of the gap, especially when cuffs and instruments behave differently over the replacement cycle. By rechecking currency timing and refreshing regional ASP bands close to the sizing year through procedure-linked validation checks, the 2026 market size is kept aligned with current purchasing signals, which is where Mordor Intelligence tends to differ most from less frequently updated figures.

Key Questions Answered in the Report

What is the current Tourniquet Systems Market size?

The tourniquet systems market size sits at USD 646.48 million in 2026 and is forecast to reach USD 930.27 million by 2031.

Who are the key players in Tourniquet Systems Market?

Delfi Medical Innovations Inc, Zimmer Biomet Holdings Inc, Hammarplast Medical AB, Stryker Corporation and AneticAid Ltd are the major companies operating in the Tourniquet Systems Market.

Which component generates the most revenue?

Tourniquet cuffs dominate, holding 88.20% of 2025 revenue because they are consumables that require frequent replacement

Which region is growing fastest?

Asia-Pacific posts the highest regional CAGR at 9.95% as surgical volumes rise and hospitals adopt cost-effective pneumatic and smart devices.

Page last updated on: